Now, I’ve seen a thing or two in my time, from the muddy banks of the Mississippi to the wild, woolly, and mostly-full-of-lies silver rushes out West. The talk of riches—it’s like a siren’s song, ain’t it? It’ll make a man forget his grammar, his good sense, and sometimes his very trousers. The world is full of fellows who’d sell you a gold brick made of brass, and another sort who’ll show you a hole in the ground and swear it’s a direct-to-Heaven express line for your pocketbook.

And so it is, that a body must approach a matter of finance with a mind as clear as a bottle of good whiskey before the cork’s been pulled. And I’ve been looking at this Apollo Silver business, and it’s a curious thing, a right proper puzzle for a man who’s seen a few. It ain’t about the grand promises of a bonanza that’ll make you the next Rockefeller, a-building libraries and a-dressing in finery. No sir. That kind of talk is for the greenhorns and the giddy.

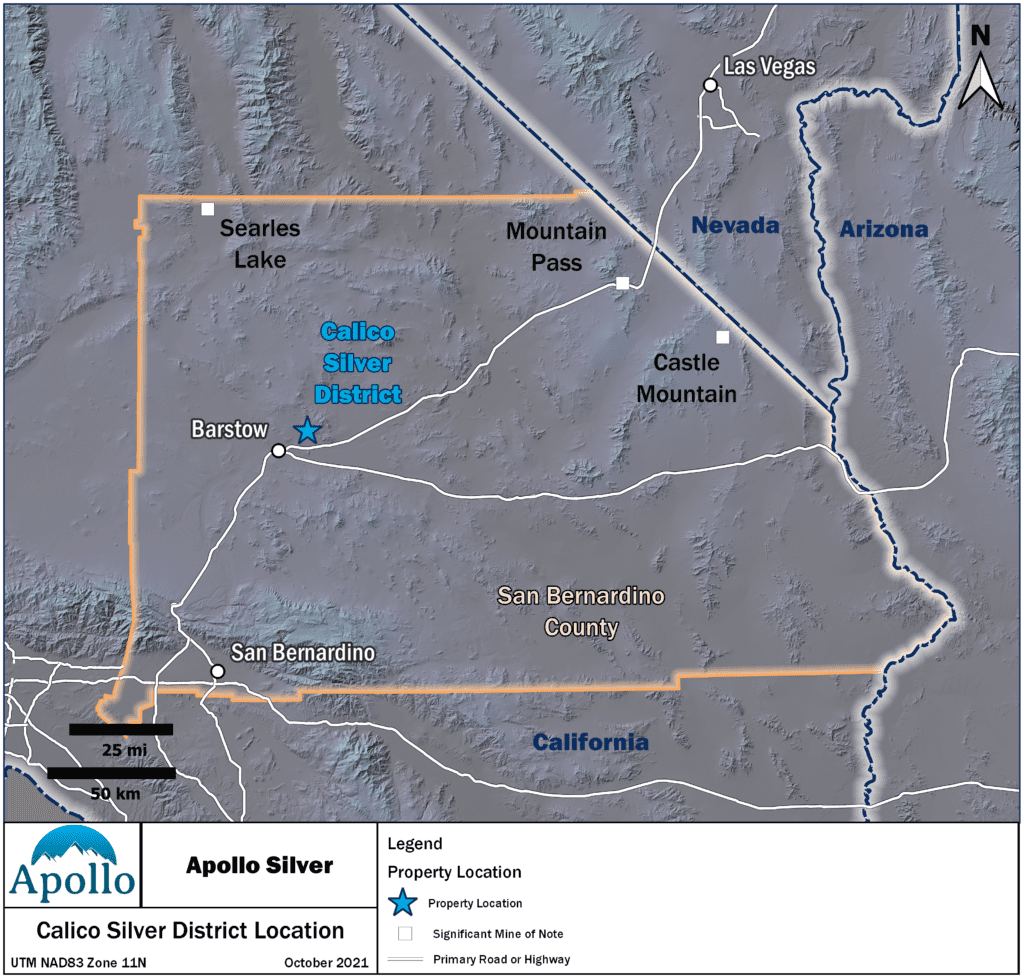

What’s to be said for Apollo is a different tune entirely. It’s a calm, measured sort of melody, like a riverboat gliding on a Sunday afternoon. You see, they’ve got this Calico project out in California, and another one, Cinco de Mayo, down in Mexico. And when they speak of it, they ain’t waving their arms about or using words too big for their boots. They’re talking about a mineral resource. And not just a vague promise, but numbers that have been “measured,” “indicated,” and “inferred.” That’s the part that sticks to a man’s ribs like a good meal.

And there’s history to back it up, too. The Calico district ain’t some new-fangled idea; it’s a place where they’ve been pulling silver from the earth for a long spell. Back in 1881, after a big discovery, Calico became a real humdinger of a town. It was a place that produced millions of dollars in silver over a dozen years, a wild and colorful place that drew in folks from all over the globe, a town with a name that came right from the “calico-colored” mountains themselves. A fella by the name of Walter Knott, who had a berry farm and a fondness for history, even went and restored the old place after it became a ghost town. So, the ground there, it’s got a reputation.

And in that reputable ground, they’ve got a proper accounting. The Calico project is said to hold a mighty 110 million ounces of silver in the “Measured and Indicated” category, which is a powerful lot of the shiny stuff. And on top of that, there’s another 51 million ounces of silver in the “Inferred” category. That’s a sum a body can get his head around.

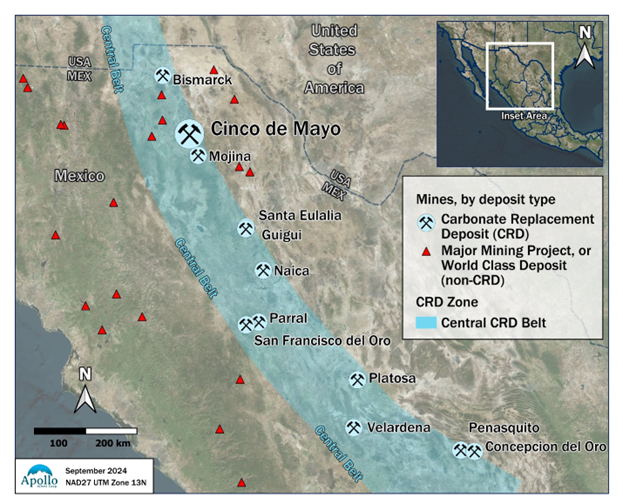

Now, as for the Cinco de Mayo project down in Chihuahua, Mexico, well, that region is a whole other book of stories. Mexico’s got a history with silver that goes back centuries, and a fella who knows a thing or two about rocks will tell you that the very geology of the area is famous for these “carbonate replacement deposits,” the kind that have been responsible for a good 40% of all the silver ever pulled out of the ground in that country. And while their report on this project is of a historical nature, it still speaks to a substantial resource, with a historical estimate of 52.7 million ounces of silver in the “Inferred” category. It’s a testament to the region’s long-standing character.

Now, I’ve seen men go bust on a whim, throwing their money at some fly-by-night scheme with a map that had more flourishes than truth. But this here, this is a matter of geography and common sense. It’s in places where they’ve been digging silver for a hundred years, and where the land itself seems to say, “Why yes, there’s more where that came from.” And the folks in charge—they’ve got a long-standing acquaintance with the business of pulling wealth from the earth, not just from the pockets of others.

So, a man must ask himself, what’s the virtue in this? The virtue is in the lack of fancy. It’s a bet on what’s already there, not what might be. It’s the difference between a high-stakes poker game where you might lose your shirt, and a man walking into a store to buy a new one. It ain’t a get-rich-quick scheme. It’s a slow, deliberate trundle down the road of reason. And in a world where every huckster with a shovel has a story to tell, a story about a resource measured and counted is a mighty comfortable thing to rest your hat on.

(Please note: Apollo Silver is a sponsor of Proven And Probable, and we are biased.)

In this episode of ‘Proven and Probable,’ we engage with Bob Moriarty, a distinguished commentator on geopolitical and economic affairs. Bob’s extensive experience includes serving as a Marine F-4B pilot during the Vietnam War, where he flew over 820 combat missions and became one of the most highly decorated pilots of the conflict.

We delve into the recent tragic collision between an American Airlines plane and a military helicopter near Washington, D.C., exploring Bob’s insights on the incident, the National Transportation Safety Board’s investigative approach, and media coverage.

The discussion also covers U.S. tariff policies, international responses, and the current state of gold and precious metals, providing a comprehensive analysis of these pressing issues.

Join us for an in-depth conversation that offers clarity and depth on these complex topics.

In this interview we sit down with Shawn Khunkhun the CEO of Dolly Varden Silver (TSX.V: DV | OTCQX: DOLLF) to discuss the disconnect with Silver and Silver Equities, the latest news regarding more high-grade Silver results from the Homestake Silver Deposit, and the recent consolidation with addition of the Big Bulk Copper-Gold Porphyry Project.

Longtime readers of 321Gold know I am a giant fan of the Daily Sentiment Indicator put out by Jake Bernstein. The DSI is sending out important signals such as bonds, the dollar, gold, silver, the Euro, the Swiss Franc, British Pound, Yen and the Aussie Dollar. Basically when readings go below 10 you are near a major bottom. When they go above 90 you are near a major top.

As of September 27th close of trading the DSI for treasuries is 10, 93 for the dollar, 8 for gold, 8 for silver, 5 for the Swiss Franc, 7 for the Euro, 10 for the Yen, 9 for the Aussie dollar and 12 for the British pound. To show that it really doesn’t matter what commodity the DSI tracks, the turns it projects says that even boring Orange Juice at 93 is about to tumble.

So in short, the dollar is getting close to a top, gold, silver, bonds and most currencies are near a bottom and about to turn higher. When these moves take place, it will happen all at the same time. Including OJ taking a swan dive.

These numbers are not as extreme as they have been in the past and don’t suggest a turn will happen tomorrow but it will happen soon. That could be as much as a month from now.

There are two kinds of investment information, signal and noise. For some reason many gold bugs are fixated on manipulation and price suppression as being important. I cannot agree. All financial markets are manipulated by everyone involved all of the time. So a sincere belief in manipulation of gold and silver provides no information that would lead to a profitable trade. In other words, if everything is manipulated, and that is true, who cares? You can’t profit. It generates neither a buy signal nor a sell signal. It’s noise, not signal. The DSI on the other hand is the most valuable and consistent signal I know of. In simple terms, you can take it to the bank.

The markets I have identified above are going to reverse direction in the next month. You can write that down on a piece of paper and take it to your local bank and cash it.

For those who are not subscribers to the DSI it seems expensive. Because it is. It is aimed at serious commodity traders who can make all of the cost up in one trade. But if you contact Jake and whine that you can’t afford it, he might give you a break. That’s what I did.

I’ve written about Lion One (LIO-V) probably a dozen times over the last couple of years. They are the only junior in the world with 100% ownership of a major alkaline gold system. Their Tuvatu gold project is located in Fiji on the Pacific Ring of Fire with multiple 20 million ounces high-grade gold mines on the same structure.

With a market cap of only about $171 million CAD the market seems to value the company for only their 2018 43-101 resource estimate of just over 720,000 ounces. But the company is about to be revalued in three different ways.

First of all, the resource does not reflect an accurate count of how much gold they have. The Tuvatu Gold project is similar in size to the Vatukoula Gold Mine in production since 1938 having shipped over seven million ounces of gold. Vatukoula is about 35 km from Tuvatu on the same structure. Vatukoula still reports about 3.8 million ounces in a resource.

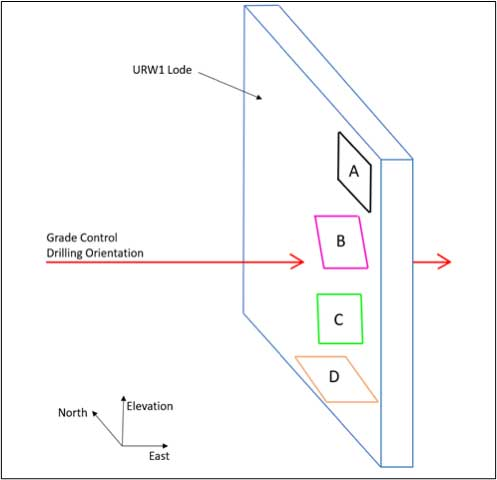

These alkaline gold systems have an unusual form of gold. There will be hundreds of tiny fractures in the rock where flash gold has appeared. The veins may only be a couple of centimeters but are ultra-high grade. Since they vary widely in orientation it is not possible to get a representative assay of the real grade because there is no angle that you can drill that catches all of the tiny veins. Actually in one of the latest press releases the company changed how they sample assays of greater than 10 g/t gold to more accurately reflect the real grade.

What I’m trying to say is that in spite of having spent tens of millions of dollars in drilling, the company still does not know what an accurate grade is for the gold. But the good side of that issue is that no matter how you drill and sample it, you are always showing a lower grade than actually exists. Which means regardless of what they say they have for grade, production will in almost all cases show higher values for gold. It’s a good problem to have.

Lion One reported actually starting to mine in a May press release. The company has been predicting actual milling and gold production in the 4th quarter. Chief Operating Officer Patrick Hickey has been struggling to make the 4th quarter goal. He is so far ahead of schedule that there may be some “TRIAL” gold processing in the 3rd quarter, i.e. in a month.

In that May 18th press release there was a vital visual drawing of why grade control is always inaccurate. No matter how you drill, you miss veins. Here is an image from the press release.

The official first gold pour is scheduled for Fiji Day on October 10th in conjunction with a bunch of officials from the government who are thrilled to see a 2nd gold mine getting into production in Fiji. I know of no other jurisdiction where a junior company was able to go from exploration to production with greater support from the host country.

Lion One is on the sweet spot of valuation on the Lassonde Curve as the project begins production. That will give the stock a revaluation based on the risk has been removed from the stock.

The third part of the revaluation will be when gold and gold stocks start their next bull run. I see a general market crash between now and October. It could well take the metals and resource stocks with it. But when the dust settles, gold and gold stocks are going to be the only safe haven in town. The brilliant Bob Hoye is calling for October-November to be a good time to buy shares.

At startup the company is planning on production of 300 tonnes per day. The crushing circuit can do 1,000 TPD but for now the grinding circuit is limited to about 300 TPD. The company has already stockpiled over a two-month supply of material to mill. Plans are in progress to expand production to 500 TPD by September of 2024.

Guess estimates for grade are 6-7 g/t gold for the startup phase but COO Patrick Hickey has his fingers crossed and is hoping for 10 g/t gold. I think I have an understanding of the vein swarms and how they are always undercounted in assays. I’ll climb out on a limb and suggest that they will be doing 13-15 g/t gold a lot sooner than current investors understand.

I’ll make an important comment for investors to know here. I’ve been a small part of this story since Wally brought Quinton Hennigh on board in early 2019. Wally was making progress but it wasn’t visible. Quinton offered a lot of suggestions as to how and where to drill and what changes they needed to make in terms of personnel.

Quinton realized the company needed a professional team on site. He contacted two of the leading guys in mining, Patrick Hickey and Sergio Cattalani and convinced them to come on board. Prior to their entry management was being run out of Perth in Western Australia and frankly that just didn’t work. Investors should read the press release. I am triple impressed with both of them. I shared an hour-long update with Patrick last week. He has things totally under control. He’s the most impressive mine builder I have ever talked to.

Lion One is cashed up to production as a result of the last couple of private placements. Between standard warrants and broker warrants issued with prior placements, there are about 41 million outstanding warrants at prices between $0.77 and $1.49 dated for just over two years. As the warrants are exercised, it will bring in about $53 million. I don’t see cash being a problem for the company. There are about 15 million tradable warrants at $1.25 and I suspect they will add to the liquidity of the company since it allows investors to speculate on the price of the company with a degree of leverage. They expire in November of 2025.

I was in on a call with management of Lion One a week ago after I enquired as to the status of going into production. I was very impressed with the quality of the team and the direction the company is moving. I think the price will soon reflect the quality of management and high-grade of the ore. This should be one of the lowest cost producers in the industry. The government of Fiji is solidly supportive of the company and I see no problems on the horizon at any level.

Lion One has been my largest position for a couple of years now. The company is an advertiser and I couldn’t be more biased. Do your own due diligence.

Lion One Metals LIO-V $.84 (Aug 22, 2023) LOMLF OTCQX 206 million shares Lion One website

The Best Video on Why and When to Buy and Sell Physical Precious Metals:

I’m a licensed broker for Miles Franklin Precious Metals Investments, The Only Online Dealer that is Licensed and Bonded Period! Where we provide unlimited options to expand your precious metals portfolio, from:

As my regular readers fully understand, I am a big fan of measuring sentiment to gauge just where we are in the metals cycle. On September 1st I said we were at a tradable low. That was accurate to the day for silver and gold plodded along for another four weeks before touching the low. I picked that timeframe based mostly on DSI but also use every other way to measure sentiment that I can find including talking to others I have respect for in the industry.

If you are looking for a holiday treat for yourself, the DSI is on sale from now and ending on December 15th at a 60% discount. If you are a serious investor, it is the best tool you will ever find. I know there are half a dozen GURUs out there who claim to be experts who have never made a single accurate call.

I called the top in silver to the day in 2011 and this latest silver bottom to the day. I know of no other writer who can say that. And I am neither a guru nor an expert. I just used the same tools available to all of us.

I have reached out to the people whose judgment I appreciate the most to make sense of what I have seen in the last few months. The sentiment is worse across the board than what I saw back in 2000-2001 when both gold and silver made historic lows. You can see it in the trading volume and absurdly low prices.

It tells me this is your time to make your fortune. I don’t know how many times I have repeated that you have to buy when no one wants to buy and sell when everyone wants to buy. I see dozens of stocks including some real piece of shit stocks with rotten management that have 1000% potential in the near future. Forget reading tealeaves and plucking through chicken entrails and pondering what the Fed might screw up next. Sentiment moves markets but you have to see it. Anyone looking at the DSI and $BPGDM could make the same to the day predictions I have made dozens of times without being a guru.

I’ll say it again. Dolly Varden is silver.

The company has a 163 km land package in the midst of the Golden Triangle in Northern BC, Canada. It consists of two primary parts, the Homestake Ridge with about 20 million ounces of silver with just short of a million ounces of gold. Homestake was bought from Fury for $5 million in cash and 76.5 million DV shares. Fury recently sold 17 million of those shares reducing their overall ownership of Dolly Varden to 26%. The second part would be of course the Dolly Varden property and mine with an additional 44.5 million ounces of silver.

Dolly likes to use both silver and gold equivalent ounces. If using silver Eq, they have a total of 137 million Ag Eq ounces. If using gold it would be 1.83 million Au Eq ounces. With a $133 million CAD market cap and $10 million in cash, Dolly is getting less than $1 CAD an ounce or $.70 USD. Well before the marvelous run up to near $50 an ounce in 2011 silver companies were getting $3 to $5 an ounce USD and it will happen again. Dolly certainly could have a 400-700% move higher when silver investors wake up.

They have not woken up yet. Silver touched a low of $17.56 on September 1st. Last week it hit a high of $22.24 on Wednesday. That is a 26% gain in less than three months. And investors in the resource space have not woken up yet. These subsurface rallies can go higher and faster than you can imagine. It happened in early 2016 and again in 2020 when silver blasted higher from under $12 an ounce to almost $30 in ten months.

Dolly’s 2022 drill program called for 30,000 meters of drilling in 99 holes with four rigs turning. The company is releasing results on a regular basis. Their last press release from November 7, 2022 showed 12.51 meters of 442 g/t Ag. That’s almost $300 rock in USD and highly economic.

One thing that I would like to point out that even I didn’t know, until I poured through their company presentation, is that the ownership is almost totally in the hands of professional investors. Sprott owns 11%, Hecla another 10%, I mentioned Fury with 26% and another 45% in institutional investors. There is a mere 8% in the clutches of retail investors yet they are the people who move the stock. When silver is hot again and it will be, Dolly Varden is going to be the go-to silver stock once again.

Dolly Varden is an advertiser and I participated in their last private placement so I am biased. Please do your own due diligence.