This update provides a clear look at the recent drilling activity for investors tracking the progress of the Northeast Tyro Zone. Derek McPherson, CEO of West Point Gold, walks through the specific drill intercepts and table data released by the company to confirm current exploration success. If you are following mining investment opportunities, this breakdown offers the necessary technical context on the gold grades identified in the latest reports.

The presentation focuses on the operational progress at the site, specifically detailing the high-grade intercepts that define the current phase of work. By analyzing the map and table data provided, viewers can understand the significance of these gold exploration findings and what they mean for the company’s timeline. This video is intended for those evaluating the technical milestones of West Point Gold and their recent impact on the project scope.

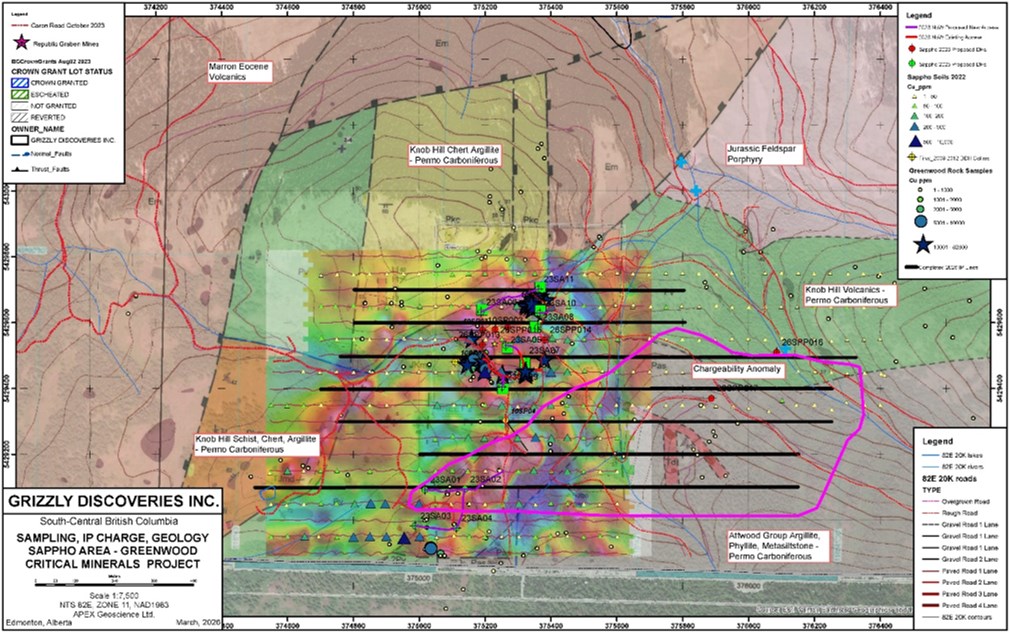

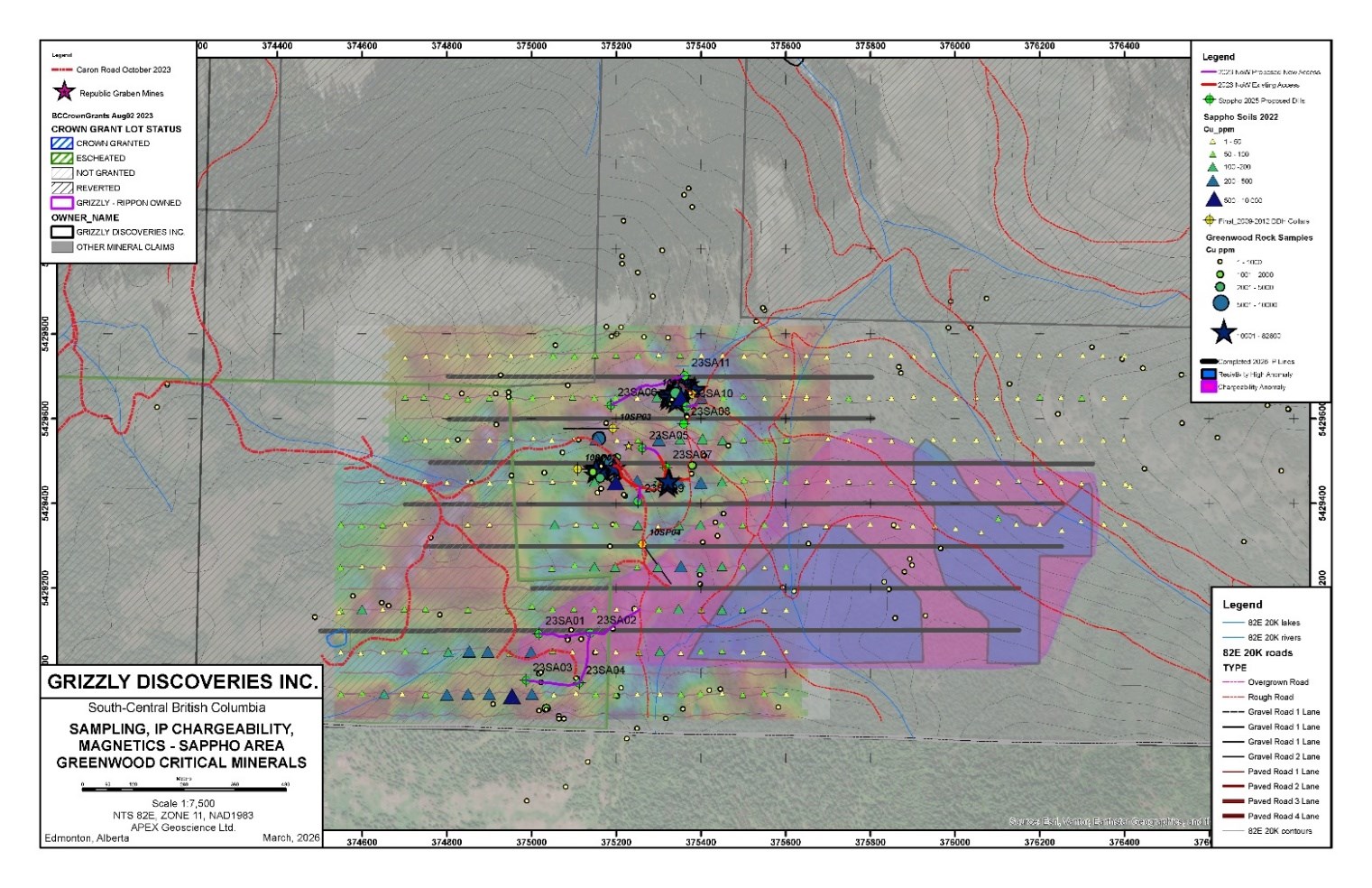

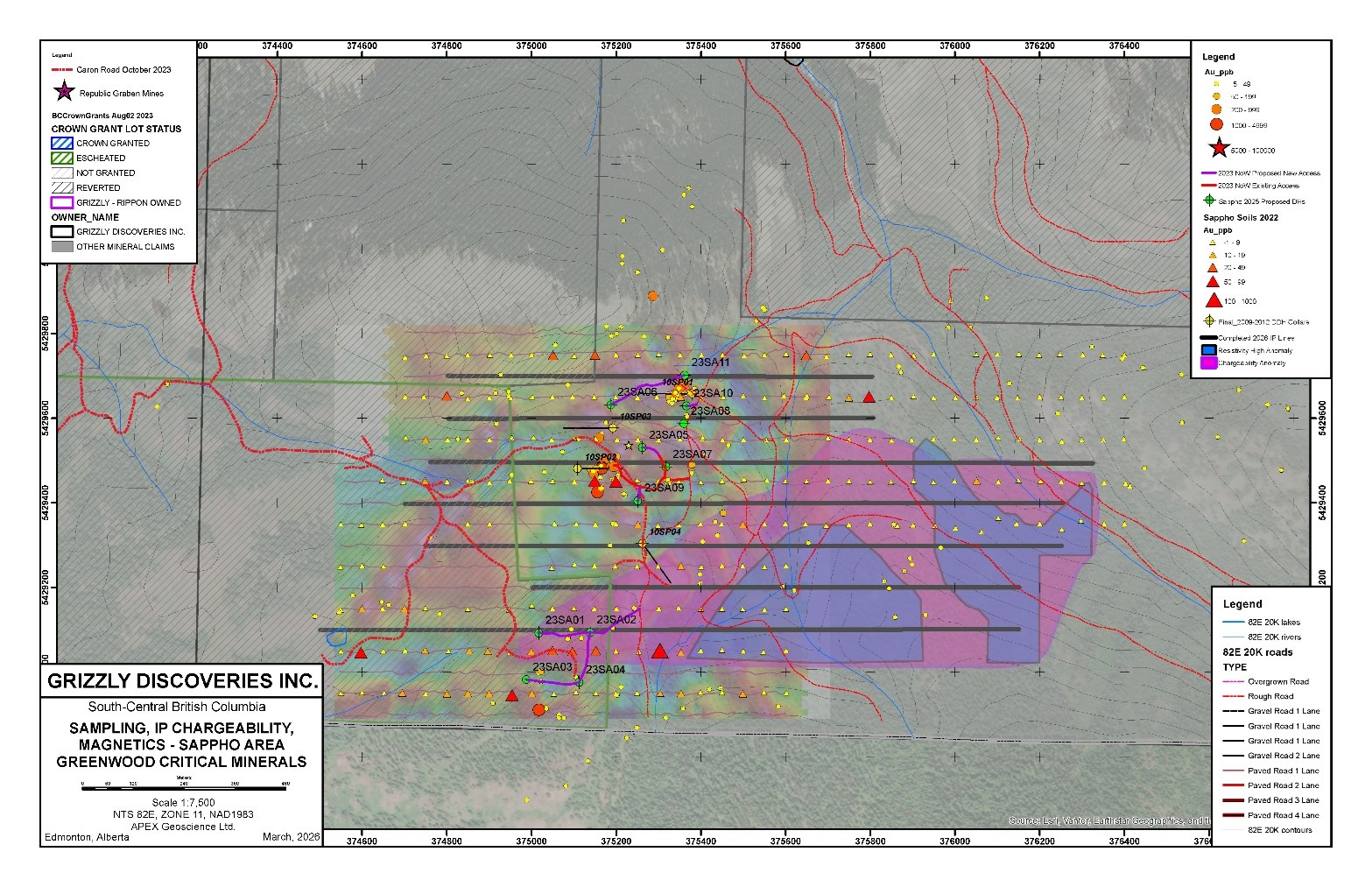

Edmonton, Alberta–(Newsfile Corp. – July 30, 2026) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) is pleased to announce that assay results have been received from ALS Global Limited (“ALS”) for the core drilling program conducted in late April to mid-May, 2026 to follow up excellent prior results from both surface sampling, historical drilling, magnetic surveys and the recent induced polarization (IP) results at the Sappho Critical Minerals Target (Figure 1).

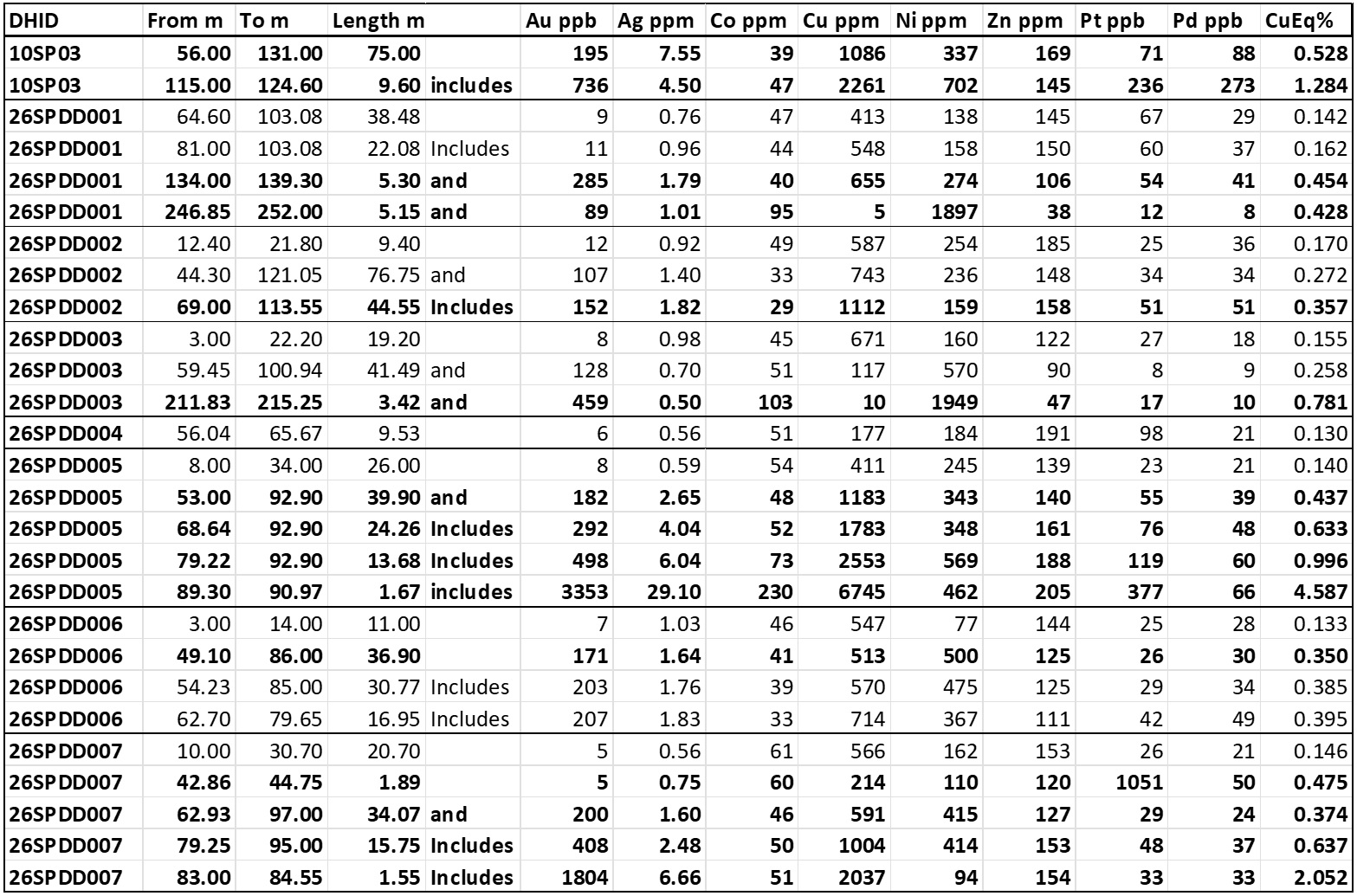

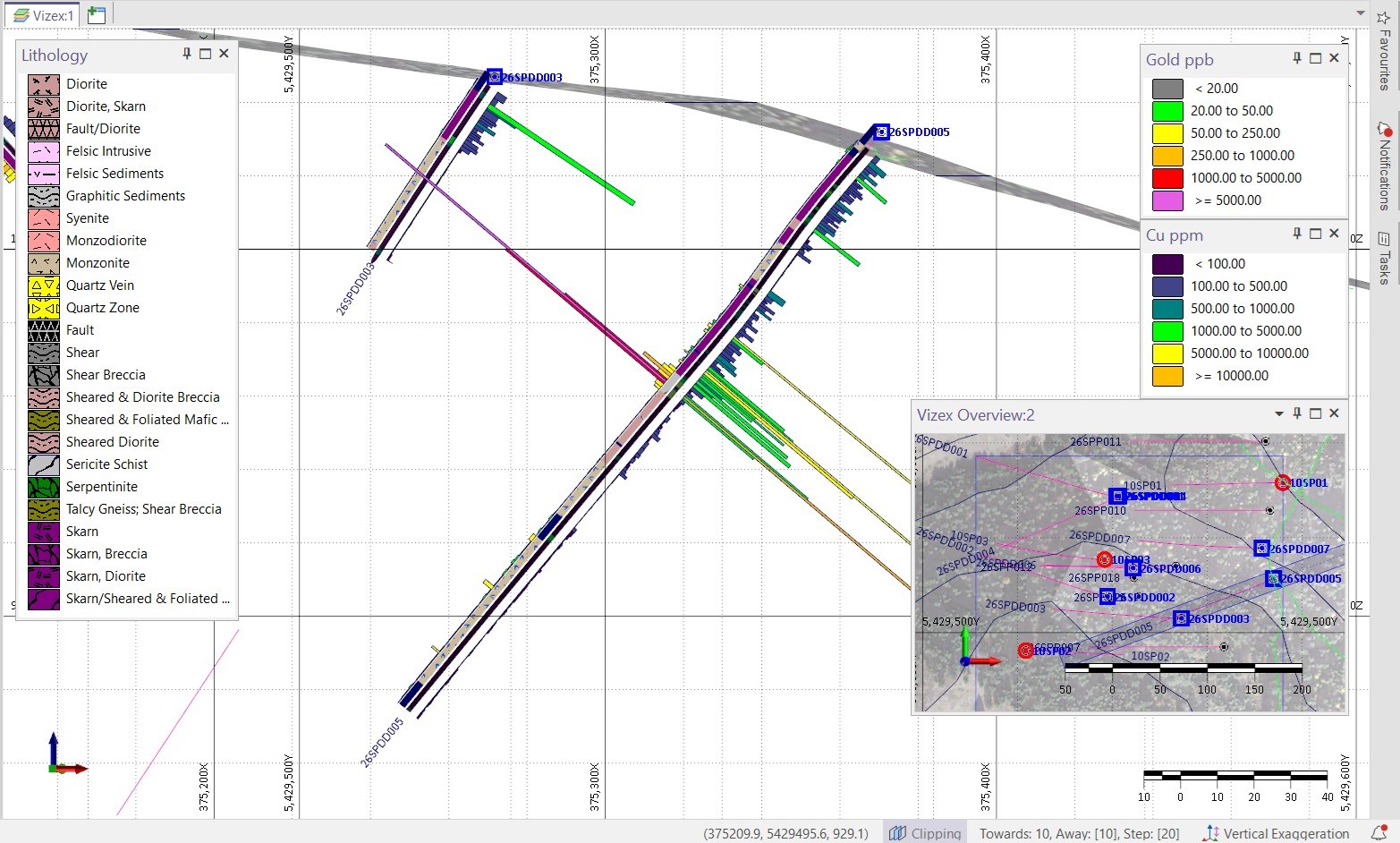

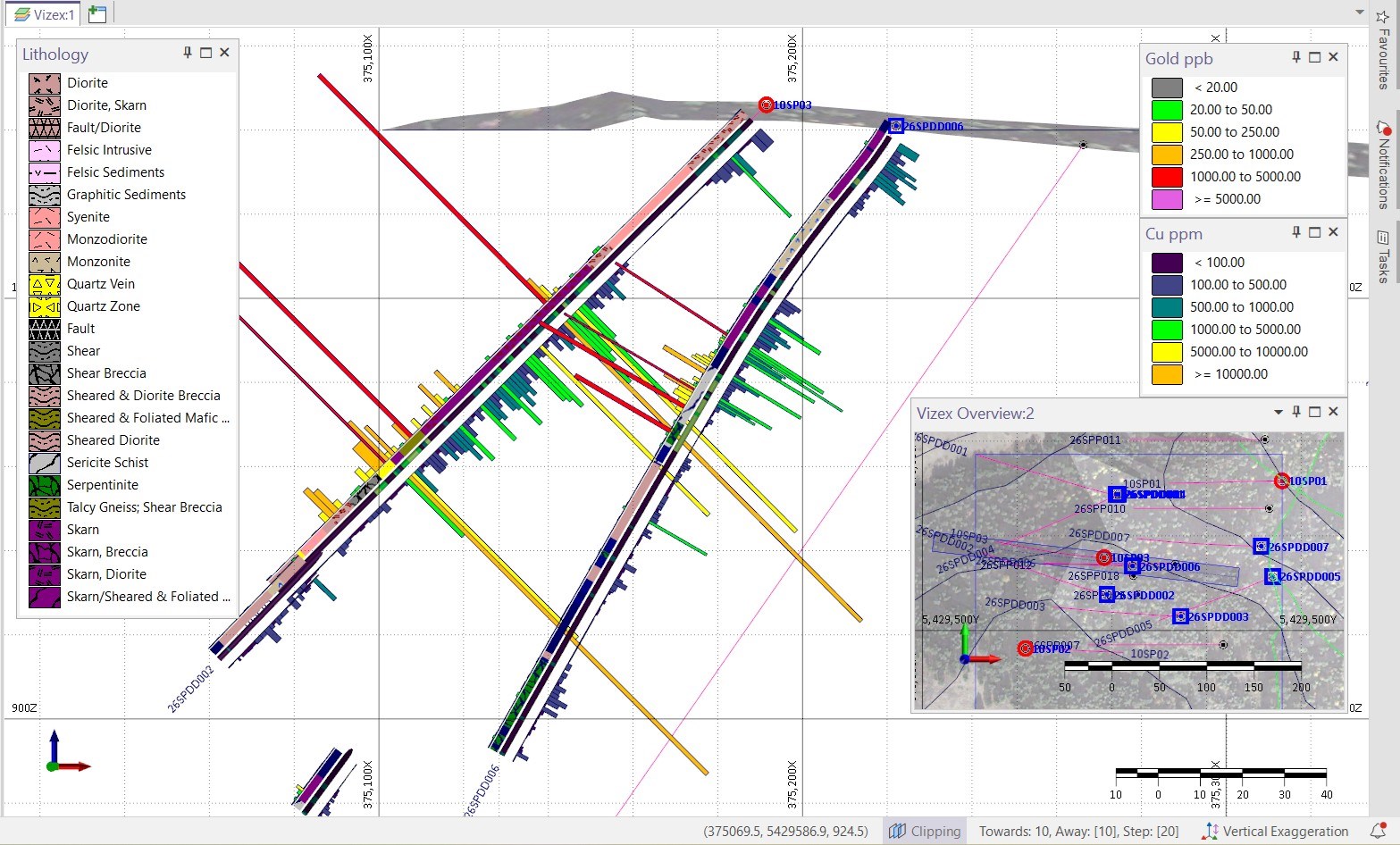

A total of seven (7) core holes for a total 1,485 metres (m) were completed targeting the near surface Main Sappho Skarn Target and an associated near surface IP conductivity. The skarn mineralization is also coincident with a number of magnetic anomalies and is characterized by the results of the 2010 core hole 10SP03 (Table 1) for copper-gold-silver-platinum group elements (Cu-Au-Ag-PGE). APEX Geoscience Ltd. (“APEX”) reports that all seven 2026 core holes intersected highly anomalous polymetallic mineralization with Cu-Au-Ag-cobalt (Co)-nickel (Ni)-zinc (Zn)-PGE’s (Table 1). The intervals with significant anomalous Cu-Au-Ag-Ni-Co-Zn-PGEs are most often characterized by garnet-pyroxene skarn with significant alteration including epidote-sericite-chlorite-pyrite-chalcopyrite. Some precious metal enriched zones are associated with serpentinite in fault zones in contact with skarn mineralization.

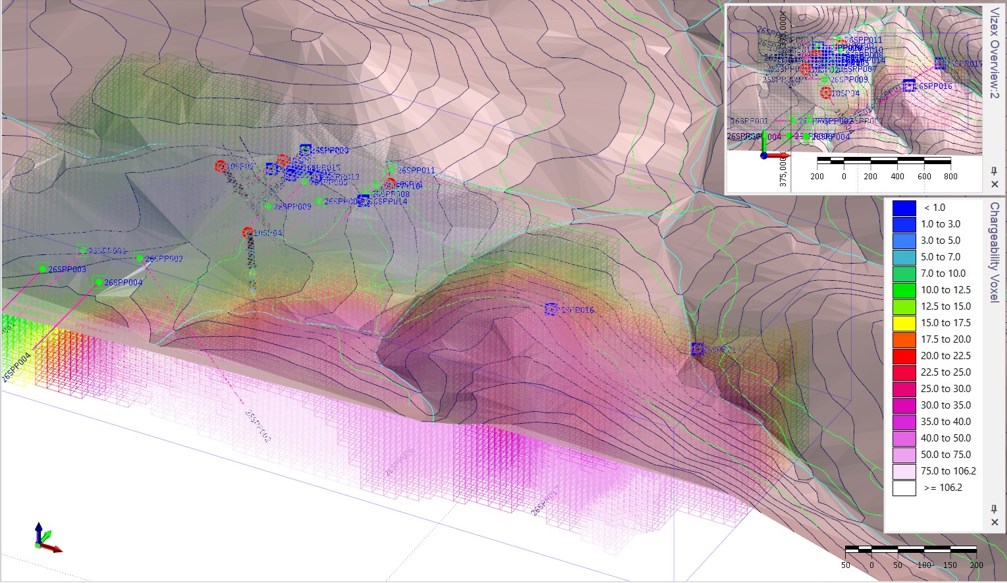

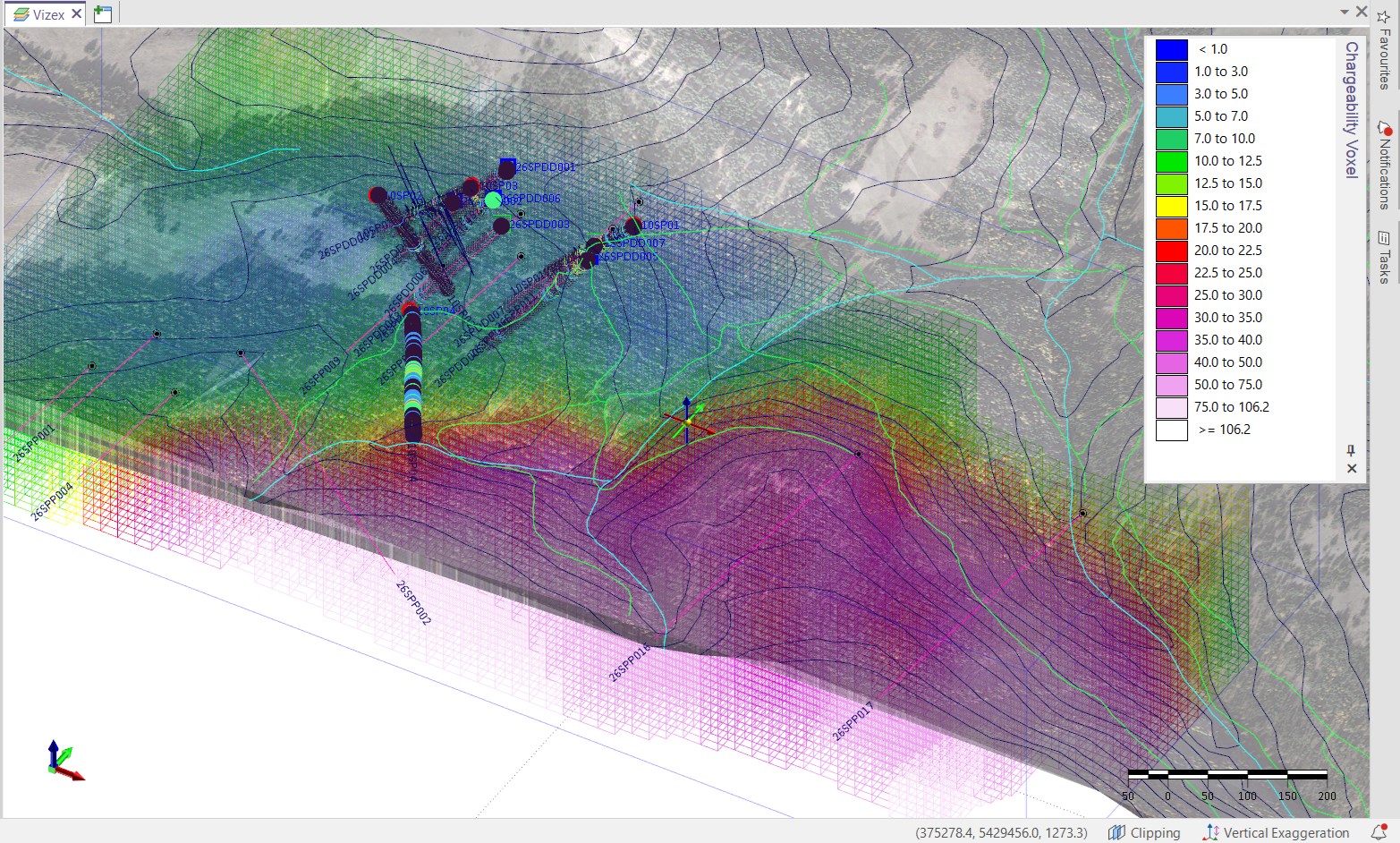

The Main Sappho Skarn Target is immediately adjacent to the recently identified Sappho IP chargeability anomaly. A total of 7 lines of IP for 10.1 line-kms were completed during the 2026 surveys at Sappho outlining a significant IP chargeability anomaly. It is interpreted that the strong chargeability anomaly likely represents disseminated sulphide related to a porphyry target. This anomaly was not targeted in the current drill program. The Company is currently in the process of permitting additional drillhole pads to complete drill testing of the Sappho IP chargeability target later in the year. Further IP work, geological mapping and surface sampling centered on the target are planned prior to the commencement of drilling.

Highlights

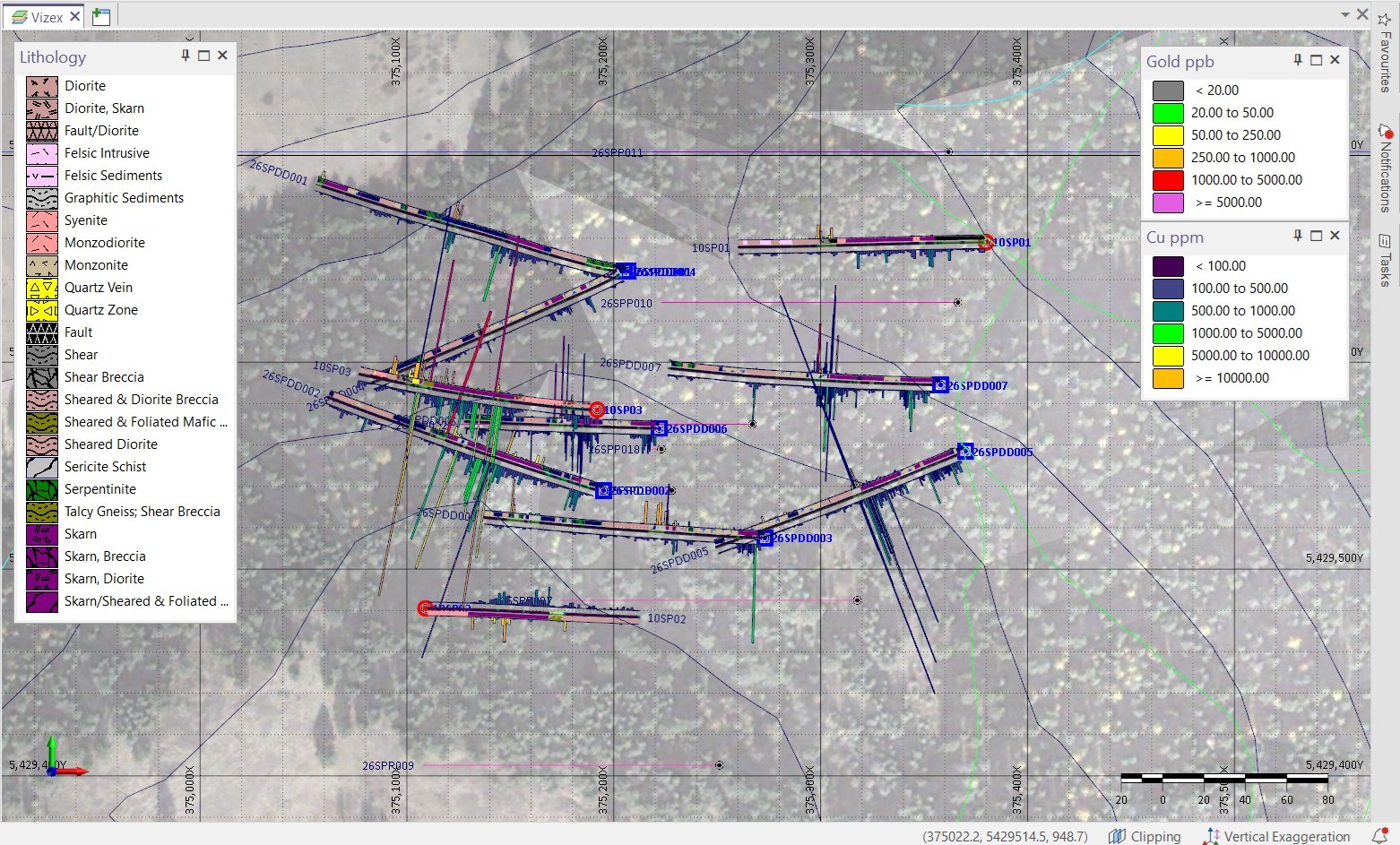

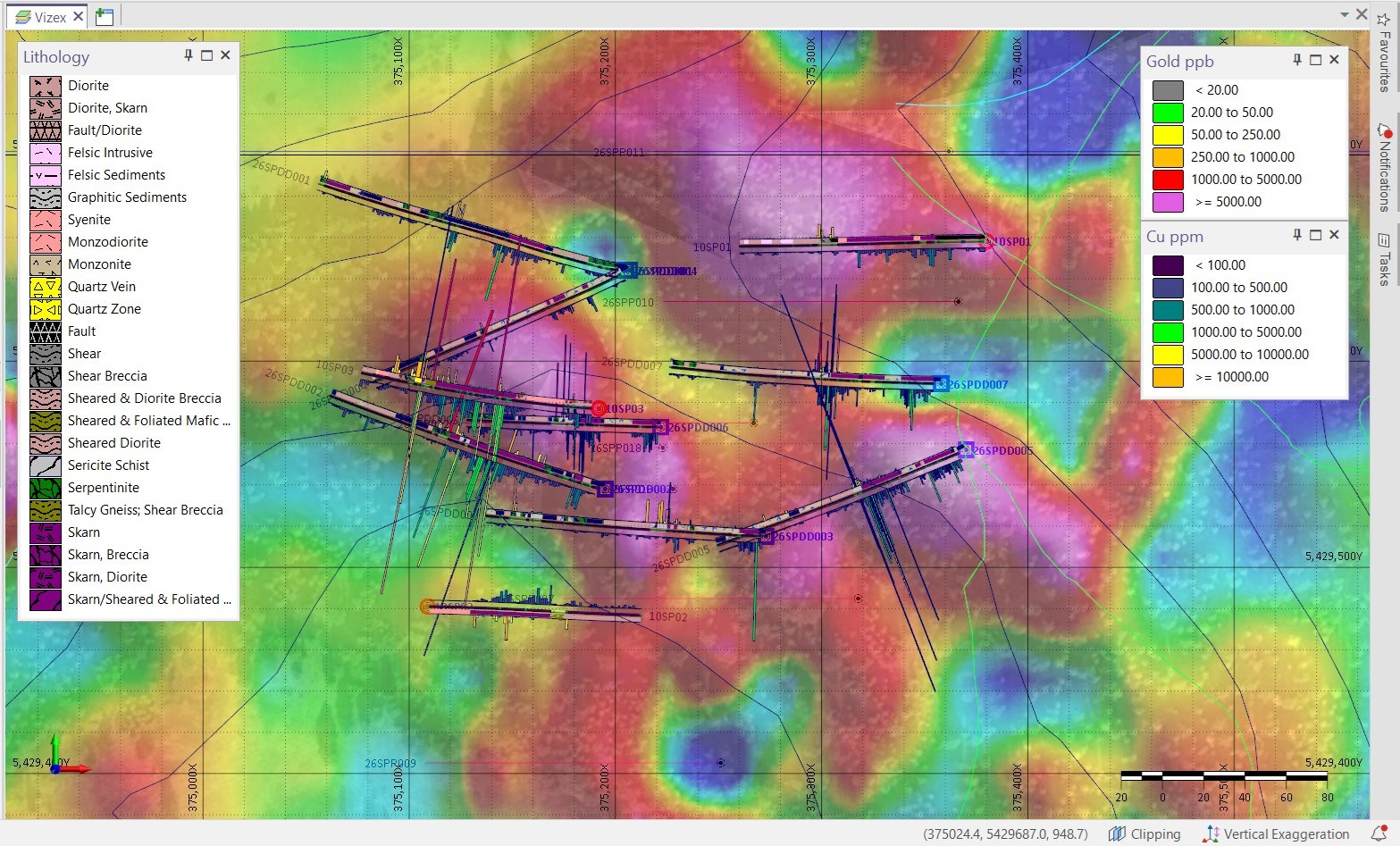

A total of 7 core holes and 1,485 m completed at the Sappho Skarn Target Area (Figures 2 to 5).

Anomalous Cu-Au-Ag-Ni-Co-Zn-PGEs intersected in all 7 core holes with multiple zones in most of the holes associated with garnet-pyroxene-magnetite skarn and the presence of pyrite and chalcopyrite (Figures 2 to 5).

Most of the core holes intersected a shallow Cu-rich skarn zone and a deeper Cu-Au-Ag-Ni-Zn-PGE-rich skarn often in contact with a serpentinite/breccia fault zone or an altered diorite intrusion at the base of the skarn enriched with precious metals.

Example weighted average grades: 0.17% CuEq* over 9.4 m starting at 12.4 m in hole 26SPDD002, followed by 0.357% CuEq* over 44.55 m starting at 69.0 m with an average grade of 0.111% Cu,152 parts per billion (ppb) Au, 51 ppb Pt and 51 ppb Pd over the interval (Table 1; Figures 2 to 5).

Hole 26SPDD005 yields 0.14% CuEq* over 26.00 m starting at 8 m downhole, with a lower zone of 1.0% CuEq* starting at 79.22 m with 0.255% Cu, 0.057% Ni, 498 ppb Au, 6 g/t Ag, 119 ppb Pt and 60 ppb Pd over 13.68 m (Table 1; Figures 2 to 5).

Accompanying widespread and often intense alteration consists of chlorite-epidote+/-sericite+/-k-feldspar along with a number of spatially associated diorite, quartz diorite to monzonite intrusions. The level of alteration outlines a significant and robust hydrothermal system and plumbing in the target area, along with complex multiple events of intrusive activity.

The Main Skarn Area of alteration and mineralization is on the order of 250 m x 350 m at surface (Figures 6 to 9) and is roughly about 250 to 300 m northwest of the large IP chargeability anomaly identified in the 2026 IP surveys to date (See Company news release dated July 6th, 2026).

A number of discreet magnetic anomalies were identified in the 2022 ground magnetic survey and were tested with drilling during the 2026 campaign. Most of the positive magnetic anomalies yielded skarn with magnetite or a mafic unit with magnetite (Figures 1 and 3).

Figure 1: Sappho Geology, Rock & Soil Sampling 2026 with IP Lines and Planned Drillhole Locations.

The northwest contact of the IP Chargeability Anomaly is coincident with soils anomalous in Cu and Au much like the Sappho Skarn area. This contact is likely a sympathetic fault to the northeast trend of the Toroda Graben faults (Figures 6 to 9).

The Geological Setting is the East Fault Contact of the Toroda Graben with numerous pyroxenite-monzonite-diorite (older – Jurassic) and younger quartz-feldspar porphyry (QFP)-diorite (Tertiary) intrusions into sediments and intermediate-mafic volcanics along with a complex magnetic feature at the Sappho Main Skarn Target area (Figures 1 and 3).

The East and West Faults of the Toroda Graben likely played a role in controlling the Au-Ag mineralization for the Buckhorn Skarn and Mine to the southwest and the Cu-Au-Ag mineralization for the Motherlode/Greyhound skarns to the north (Figure 10).

Widespread Skarn and porphyry style alteration and mineralization along with highly anomalous Cu-Ni-Co-Zn-PGE’s-Au-Ag are observed in outcrop and drill core along with a complex magnetic signature in the Main Sappho Skarn area (Figures 1 and 6 to 9).

Drilling seems to show a shallow sequence of sediments, volcanics, skarn, serpentinite with intrusions grading into a deep zone of mostly intrusions in the Main Sappho Skarn area. The base of the sediments and volcanics seems to be the area with the best mineralization in the skarn area and based upon the evident faulting and shearing may correspond to an underlying thrust fault.

Five (5) new sulphide showings were discovered during 2022 field work, with 4 of the 5 showings yielding rock grab samples with >1% copper (Cu) up to as high as 7.25% Cu (Figure 1 and see Company news release dated November 3rd, 2022).

Historical rock grab sampling has returned numerous samples with values >1% Cu up to 9.06% Cu, many also with anomalous Co, Ni, Zn, Au, Ag, Pt and Pd.

A total of 11 historical samples have yielded >500 ppb Pt and Pd up to 4.64 g/t Pt and 2.28 g/t Pd.

The Walcott 2026 IP Survey has detected a new significant deeper chargeability anomaly on the southeast part of the grid – likely up against one of the Main Sappho faults (Figures 1 and 6 to 9). The chargeability anomaly is not closed off and is on the order of 30 to greater than 100 millivolts per volt and is comparable in size and intensity with a number of porphyry targets that have yielded new porphyry discoveries in BC recently.

The Chargeability Anomaly and porphyry target appears to be gaining in strength and size approaching the USA Border. The Company has staked a total of 35 Bureau of Land Management (BLM) lode mineral claims in Washington State covering the potential southern extent of the anomaly in the USA.

Brian “Griz” Testo, President & CEO of Grizzly Discoveries, states: “The excellent new drilling results along with anomalous ground magnetics and now IP has outlined multiple and significant new targets across the Sappho Project. I am excited to see what the next phase of drilling might show us – Grizzly will continue to refine these targets to the drill ready stage for additional drilling in the next couple of months and I look forward identifying some new discoveries.”

Table 1: Summary Assay Results for 2026 Drill Holes at the Main Sappho Skarn Target Area.

*True widths are unknown at this stage of exploration, so all lengths are core length. For CuEq* calculation the price of metals utilized is as follows in US$ Cu $5/lb, Au $3,200/oz, Ag $50/oz, Co $25/lb, Ni $7/lb, Zn $1.5/lb, Pt $1,200/oz and Pd $1,200/oz with assumed recoveries of 90% as no metallurgical work has been completed to determine the metallurgical characteristics of the mineralization. No inference is being made with respect to recovery and economics of any of the metals listed, as the calculation of CuEq* is being used strictly to allow comparisons of varied polymetallic mineralization between drillholes across the property.

Figure 2: Sappho 2010 (Red) and 2026 (Blue) Core Hole Locations in Plan.

The Sappho area is being targeted for copper-gold skarn and porphyry type targets associated with a Jurassic alkalic intrusive complex and several younger diorite intrusions (Figure 1). A total of five new showings of copper oxide mineralization were found during the 2022 program (Figure 1). Previous surface sampling and drilling by Grizzly has yielded significant anomalous copper, gold, silver along with platinum and palladium. Numerous historical and new rock grab samples have yielded greater than 1% Cu, 1 g/t Au, 1 g/t Ag, 1 g/t Pt and 1 g/t Pd (Figure 1).

Historical 2010 drilling by the Company (4 core holes) yielded up to 0.31% Cu, 0.75 g/t Au, 0.34 g/t Pt, 0.39 g/t Pd and 6.57 g/t Ag over 6.5 m core length in skarn at Sappho (in hole 10SP03), including a 1 m core length intersections of 3.82 g/t Au and 199 g/t Ag, and in a separate sample 1.83 g/t Pt and 2.09 g/t Pd across 1 m – these results all are associated with >1% Cu in those samples. These higher-grade zones were contained within a 75 m core length zone logged as a pyroxene – sulphide skarn with a grade approaching 0.53% CuEq* derived from current metal prices for Cu, Au, Ag, Co, Ni, Zn, Pt and Pd. Drillhole 10SP03 targeted a magnetic anomaly and had no indications of surface mineralization at the time of drilling. One of the new 2022 showings has been found proximal to drillhole 10SP03 and the targeted magnetic anomaly.

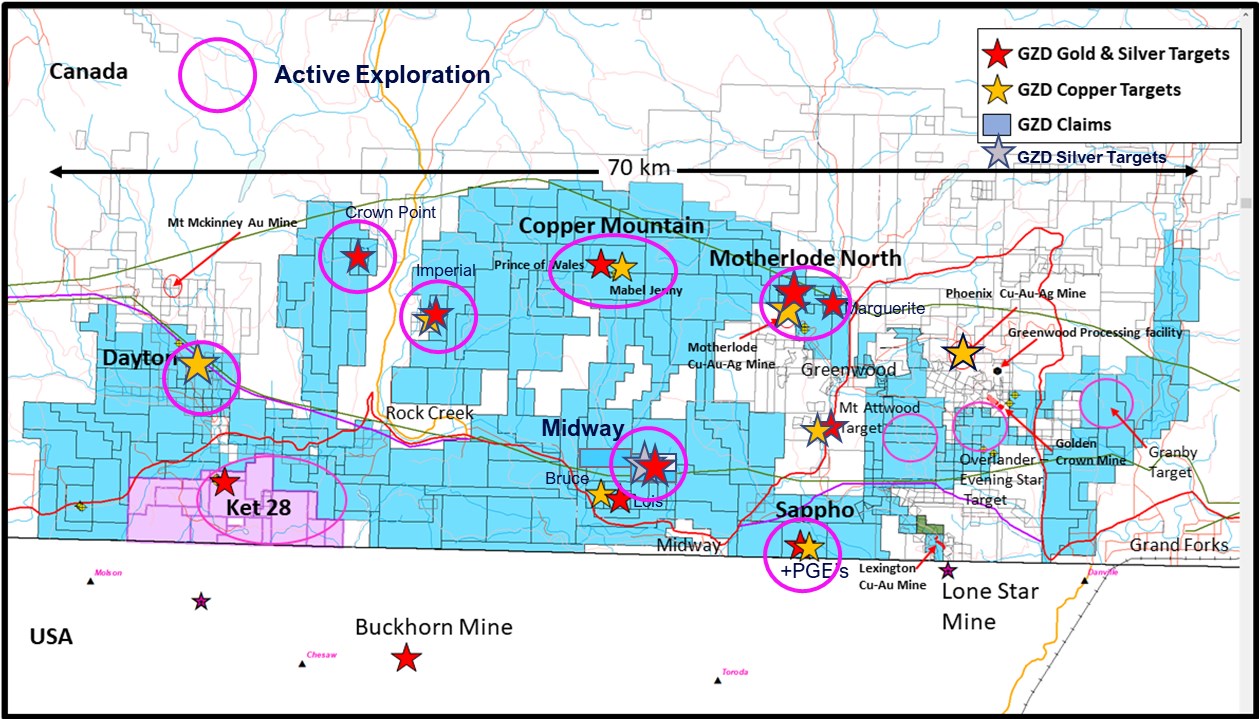

The Company is continuing with surface exploration in the Greenwood area. Crews from APEX completed trenching and rock sampling in June at the Midway Mine area, as well as some follow-up sampling at the Sappho Chargeability Target area. The 2026 exploration work is ongoing and includes prospecting and rock sampling at targets in the Motherlode area, the Rock Creek area, the Midway area, the Copper Mountain area, the Overlander-Attwood area and surrounding the Sappho (Figure 10). Additional groundwork including ground geophysical surveys are being planned and will comprise IP, magnetics and Loupe electromagnetics (EM) for the Sappho, the Midway and Motherlode areas (Figure 10). Drillhole and rock sampling results from the 2026 work are pending and will be released as they are received.

The analytical work on the Sappho Project drilling was performed by the ALS Global Limited in Kamloops and North Vancouver, an internationally recognized analytical service provider. All core samples were prepared using ALS procedure PREP-31A (dry, crush to 70% passing 2mm, riffle split off 250g, pulverize split to better than 85% passing 75 microns) and analyzed by method PGM-ICP27 (30g fire assay with ICP finish for Au, Pt and Pd) and ME-ICP61a (0.5g, four acid digestion and ICP-AES/MS analysis) for multielements. Any samples containing >10g/t Au are reanalyzed using method FAS-415 (30g Fire Assay with gravimetric finish). Samples containing >100 ppm Ag and/or >1% Cu, Pb, & Zn are reanalyzed using method ICF-6 (0.2g, 4-acid digest and ore grade ICP-AES analysis). Rock samples were analysed using Au-ICP21 (30g fire assay with ICP-AES finish) and multielements using ME-ICP41 (0.5g, aqua regia digestion and ICP-AES analysis).

The reported work has been completed using industry standard procedures, including a quality assurance/quality control (“QA/QC”) program consisting of the insertion of certified standards, blanks and duplicates into the sample stream by APEX personnel. The ALS geochemical laboratory data was provided directly to APEX and the QP and has been verified by the QP.

QUALIFIED PERSON (“QP”) STATEMENT

The technical content of this news release and the Company’s technical disclosure has been reviewed and approved by Michael B. Dufresne, M. Sc., P. Geol., P.Geo., who is a non-independent Qualified Person (“QP)” as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects.

ABOUT GRIZZLY DISCOVERIES INC.

Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and critical minerals properties in southeastern British Columbia. Grizzly is run by a highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.

On behalf of the Board,

GRIZZLY DISCOVERIES INC. Brian Testo, CEO, President

Suite 363-9768 170 Street NW Edmonton, Alberta T5T 5L4

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Caution concerning forward-looking information

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward-looking information. Such forward-looking information and statements are frequently identified by words such as “may,” “will,” “should,” “anticipate,” “plan,” “expect,” “believe,” “estimate,” “intend” and similar terminology, and reflect assumptions, estimates, opinions and analysis made by management of Grizzly in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Grizzly’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon.

Risks and uncertainties that may cause actual results to vary include but are not limited to the availability of financing; fluctuations in commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedarplus.ca. Grizzly disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

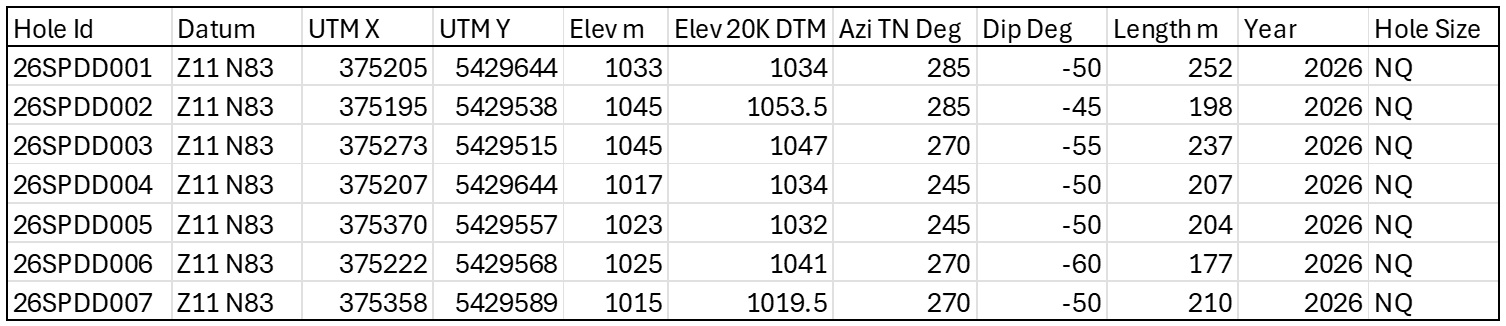

Table 2: Collars for the 2026 Drill Holes at the Main Sappho Skarn Target Area.

VANCOUVER, British Columbia, July 30, 2026 (GLOBE NEWSWIRE) — Riverside Resources Inc. (“Riverside” or the “Company“) (TSX-V: RRI) (OTCQB: RVSDF) (FSE: 5YY0), is pleased to announce that it has received mineral title for expanded property packages at its Revel and Red Jacket Projects in south-central BC. At Red Jacket, this nearly doubles the mineral tenure area controlled for the project. At Revel, it adds an additional 30% in area. In both cases, the expansion extends Riverside’s control over the prospective mineralized belt and covers targets along strike from known mineralization. Riverside’s generative program in BC continues to add prospective new projects, expanding the company’s footprint in western Canada.

The Revel Project is a carbonatite rare earth element (REE) district located approximately 20 kilometres with road access from the community of Seymour Arm, north of Revelstoke, in southeastern British Columbia. Carbonatites are a major source for REEs and targeting of this belt will continue this summer beginning with a planned airborne survey in the coming weeks.

The Red Jacket project is a volcanogenic massive sulfide system similar to the Yellowhead deposit in the Eagle Bay Formation. Red Jacket is easily accessed via paved highway and then by logging road, approximately 15 km east of Clearwater and 115 km north-northeast of Kamloops in central British Columbia. The project is north of Trekor Metals feasibility-stage Yellowhead Copper Project, which hosts a large Cu-Zn-AG-Au reserve and is considered a potential near-term future mine.

Location of Red Jacket and Revel Project in context with other Riverside properties and key cities in south central British Columbia

Figure 1: Location of Red Jacket and Revel Project in context with other Riverside properties and key cities in south central British Columbia

“Expanding our mineral tenure position at two of our growing British Columbia projects is a positive milestone for Riverside,” said John-Mark Staude, President and CEO of Riverside Resources. “Summer exploration programs are underway at both properties, and we expect results in the coming months. Securing larger land packages that capture more of the productive belt strengthens our position, adds cost-effective value, and sets us up for partner funding transactions and expanded exploration in stable, easily workable jurisdictions.”

About the Revel Project

The Revel Project is located approximately 20 kilometres from the community of Seymour Arm and north of Revelstoke, British Columbia, within a highly prospective carbonatite belt. The Project covers part of the Mount Grace Carbonatite, which is known to host rare earth element mineralization, and Riverside has outlined a 12-kilometre-long carbonatite-style rare earth system at Revel that remains undrilled. The newly added mineral claims cover the northern continuation of the carbonatite layer.

Additional Revel North claims added to the Revel Project highlighted in orange. Several main target horizons for the carbonatite REE targets are represented by the brown lines.

Figure 2: Additional Revel North claims added to the Revel Project highlighted in orange. Several main target horizons for the carbonatite REE targets are represented by the brown lines.

The Revel and Revel North claims (collectively Revel Project) occur along the northeast margin of the Frenchman Cap Gneiss Dome, comprising part of the Shuswap Metamorphic Terrain. The core gneisses are overlain by allochthonous cover rocks that host both extrusive and intrusive carbonatites and form part of the Monashee cover sequence. Recent exploration by Riverside at Revel has included detailed mapping and geochemical sampling designed to vector toward higher-grade REE zones in advance of drill testing.

The next planned work will include airborne geophysics and field exploration work during the coming months. Additional information on the Revel Project is available on Riverside’s website at www.rivres.com.

About the Red Jacket Project

The Red Jacket Project is well located, with access via paved highway and logging road, allowing for rapid, cost-effective exploration. Riverside assembled the project this year and has completed field soil and rock sampling along with reconnaissance mapping to refine volcanogenic massive sulfide (VMS) style targets. The project lies north of Trekor Metals feasibility-stage Yellowhead Copper Project, which hosts a large copper-zinc-silver-gold reserve and is considered a potential near-term mine.

Red Jacket is underlain by the Eagle Bay Assemblage, a Lower Cambrian to Mississippian package of deformed and metamorphosed volcanic and sedimentary rocks within the Kootenay Terrane. The same assemblage hosts Trekor’s copper reserves roughly 10 kilometres to the south and is a well-established host for volcanogenic massive sulphide deposits in the district, including Samatosum, Rea, Homestake and Chu Chua.

Historical soil geochemistry, mapping and geophysics completed by INCO in the 1970s and by Placer Dome through the 1980s, combined with Riverside’s own sampling in late 2025, outline a 4-kilometre-long northwest-southeast trend that takes in the Redtop, Snow and Sunrise showings. Riverside’s 2025 grab samples returned high-grade polymetallic values at surface in areas of past trenching. The horizon has seen very little drilling throughout its history. Placer Dome completed four short holes and recommended thirteen more that were never drilled so its full length remains a target. 2026 field work is underway with further results expected in the coming months. Additional information on the Red Jacket Project is available on Riverside’s website at www.rivres.com.

Additional claims added to the Red Jacket Project highlighted in orange. The approximate trend for two of the mineralized target horizons for the project are represented by the brown lines.

Figure 3: Additional claims added to the Red Jacket Project highlighted in orange. The approximate trend for two of the mineralized target horizons for the project are represented by the brown lines.

Qualified Person & QA/QC:

The scientific and technical data contained in this news release pertaining to the Project was reviewed and approved by Freeman Smith, P.Geo, a non-independent qualified person to Riverside Resources Inc., who is responsible for ensuring that the information provided in this news release is accurate and who acts as a “qualified person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects.

About Riverside Resources Inc.:

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has a strong balance sheet, no debt and tight share structure with a strong portfolio of gold-silver, copper, and REE assets and royalties in North America. Further information about Riverside is available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Investor Relations Riverside Resources Inc. Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Infographics accompanying this announcement are available at

Denver, Colorado–(Newsfile Corp. – July 29, 2026) – Elemental Royalty Corporation (NASDAQ: ELE) (TSX: ELE) (“Elemental” or the “Company“) notes the announcement by Capricorn Metals Ltd (ASX: CMM) (“Capricorn“) of a 32% increase in Mineral Reserves at the Karlawinda Gold Project (“Karlawinda“). Elemental holds an uncapped 2% net smelter return (“NSR“) royalty on Karlawinda.

Karlawinda is a cornerstone asset for Elemental, contributing US$8.9 million in zero-cost revenue in 2025 prior to completion of the Karlawinda Mine Expansion Project, which is in its final stages of commissioning.

Highlights

Significant increase in Mineral Reserves and Mineral Resources: recent drilling at Karlawinda contributed to a 32% increase in the Probable Mineral Reserve estimate to 76.4 million tonnes at 0.6 g/t gold, containing 1.57 million ounces of gold

Additionally, the Karlawinda Indicated Mineral Resource estimate increased by 30% to 124.9 million tonnes at 0.6 g/t gold, containing 2.38 million ounces of gold. Mineral Resources are inclusive of Mineral Reserves

Ongoing expansion: Capricorn’s expansion of the Karlawinda processing plant is nearing completion, with commissioning and transition to full operations expected during the third quarter of 2026

Extended mine life: Capricorn reports that the increased Mineral Reserve supports an approximately 10-year mine life, based on expanded processing capacity of approximately 6.5 million tonnes per annum and anticipated annual gold production of approximately 150,000 ounces

Conservative gold-price assumptions: Capricorn used variable gold prices of A$2,200 to A$2,600 per ounce for the Mineral Reserve estimate and a gold price of A$2,800 per ounce for the Mineral Resource estimate

Increased value for Elemental: the reported mine-life extension and additional Mineral Resources increase Elemental’s exposure to Karlawinda without additional capital contributions from the Company

Elemental Chief Executive Officer, David M. Cole, commented: “We are pleased to note the substantial increase in Mineral Reserves reported by Capricorn, which further strengthens the long-term value of our 2% NSR royalty over Karlawinda. With Capricorn’s plant expansion nearing completion and annual production expected to increase to approximately 150,000 ounces, Karlawinda is positioned to remain a cornerstone asset in our portfolio and an important contributor to Elemental’s royalty revenue.

Capricorn’s management team has an excellent track record, and we look forward to following its progress towards commissioning.”

About Karlawinda Karlawinda is a producing, open-pit gold mine located approximately 65 kilometres south-east of Newman in the Pilbara region of Western Australia and operated by Capricorn. Production commenced in June 2021, and Capricorn reports that the mine has produced approximately 564,000 ounces of gold since commissioning. Capricorn is currently completing an expansion designed to increase processing capacity to approximately 6.5 million tonnes per annum and annual gold production to approximately 150,000 ounces.

Recent drilling at Karlawinda, as reported by Capricorn in its announcement titled “Capricorn Gold Reserves Increase to 5.2 Million Ounces” dated July 27, 2026, contributed to an increase in the Probable Mineral Reserve estimate from 1.19 million ounces to 1.57 million ounces of gold, representing an increase of 32%. Capricorn reported that drilling targeted the conversion of Inferred Mineral Resources to Indicated Mineral Resources in areas down-dip of the 2024 reserve pit design, enabling conversion of a portion of the Mineral Resources to Probable Mineral Reserves. The updated Mineral Reserve estimate is based on 124.9 million tonnes at 0.6 g/t gold, containing 2.382 million ounces in the Indicated category, and 35.1 million tonnes at 0.5 g/t gold, containing 608,000 ounces in the Inferred category. Mineral Resources are inclusive of Mineral Reserves.

The updated Probable Mineral Reserve estimate incorporates depletion of approximately 103,000 ounces of gold from mining during the nine months ended March 31, 2026. After accounting for this depletion, the Probable Mineral Reserve increased from 1.19 million ounces to 1.57 million ounces of gold.

Technical Disclosure and Qualified Person

The Mineral Resource and Mineral Reserve estimates disclosed in this news release were prepared and reported by Capricorn in accordance with the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the “JORC Code”). Elemental has not independently verified the underlying data supporting those estimates and is relying on Capricorn’s public disclosure in its announcement titled “Capricorn Gold Reserves Increase to 5.2 Million Ounces” dated July 27, 2026, available on Capricorn’s website and through the ASX announcement platform. For purposes of disclosure under National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”), Elemental considers the JORC Code classifications of Indicated Mineral Resources, Inferred Mineral Resources and Probable Ore Reserves to be substantively equivalent to the corresponding categories under the CIM Definition Standards for Mineral Resources and Mineral Reserves adopted by the CIM Council, as amended. Mineral Resources are inclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

The scientific and technical information contained in this news release has been reviewed and approved by Michael Sheehan, an employee of the Company and a “Qualified Person” as defined in NI 43-101.

NASDAQ: ELE | TSX: ELE | ISIN: CA28620K1066 | CUSIP: 28620K106

About Elemental Royalty Corporation

Elemental is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 18 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental trades on Nasdaq and on the Toronto Stock Exchange under the ticker Symbol “ELE”.

This news release contains certain “forward looking statements” and certain “forward-looking information” as defined under applicable United States and Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar terminology (including negative and grammatical variations thereof).

Forward-looking statements and information include, but are not limited to, statements regarding future royalties and future consideration payments or issuances of shares, or other statements that are not statements of fact. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental to control or predict, that may cause Elemental’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions, the absence of control over the mining operations from which Elemental will receive royalties, risks related to international operations, government relations and environmental regulation, the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results will not be consistent with Elemental’s expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental for the year ended December 31, 2025. Elemental undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represent management’s best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Neither The Nasdaq Stock Market LLC nor the Toronto Stock Exchange, nor its Regulation Services Provider (as that term is defined in the policies of the Toronto Stock Exchange), accepts responsibility for the adequacy or accuracy of this news release.

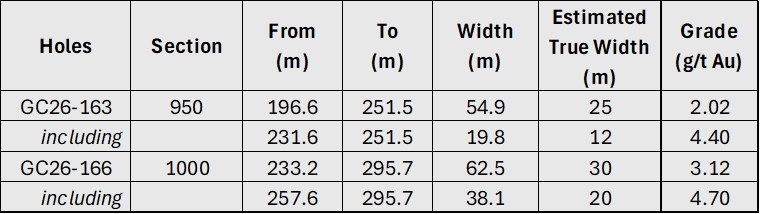

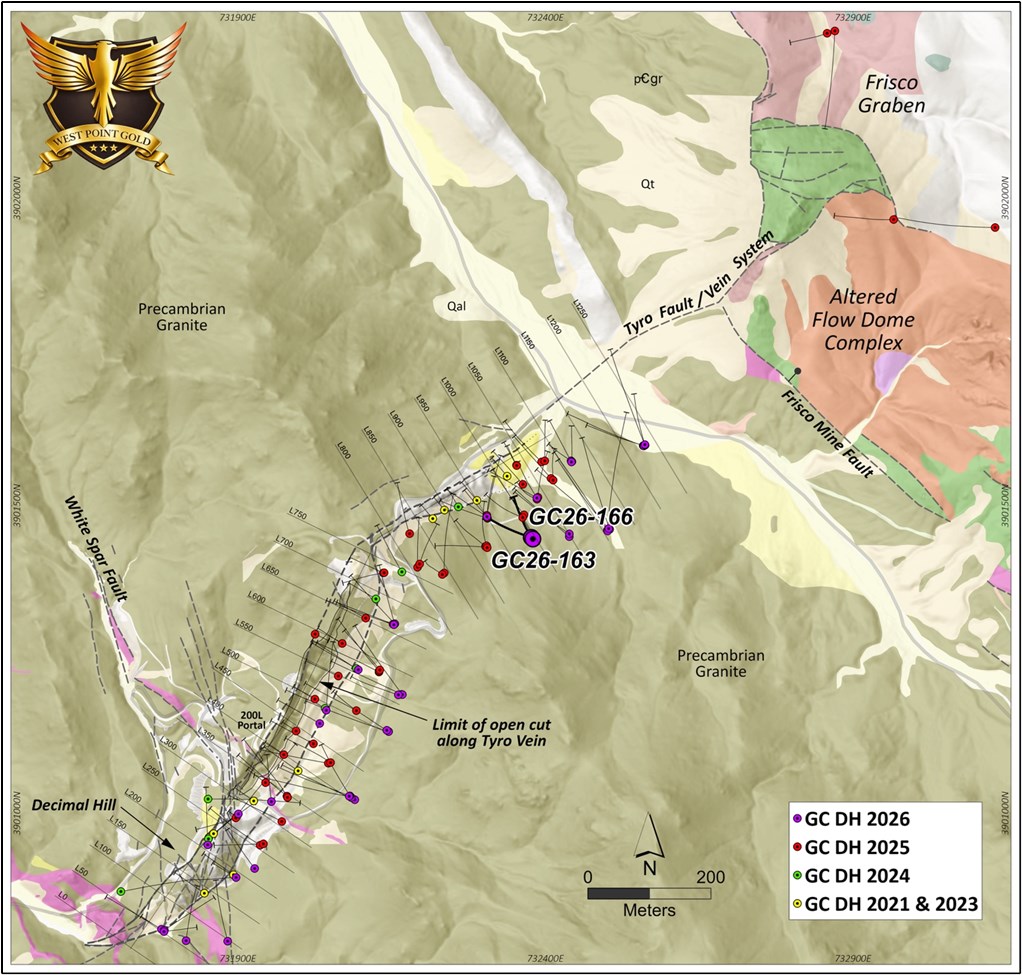

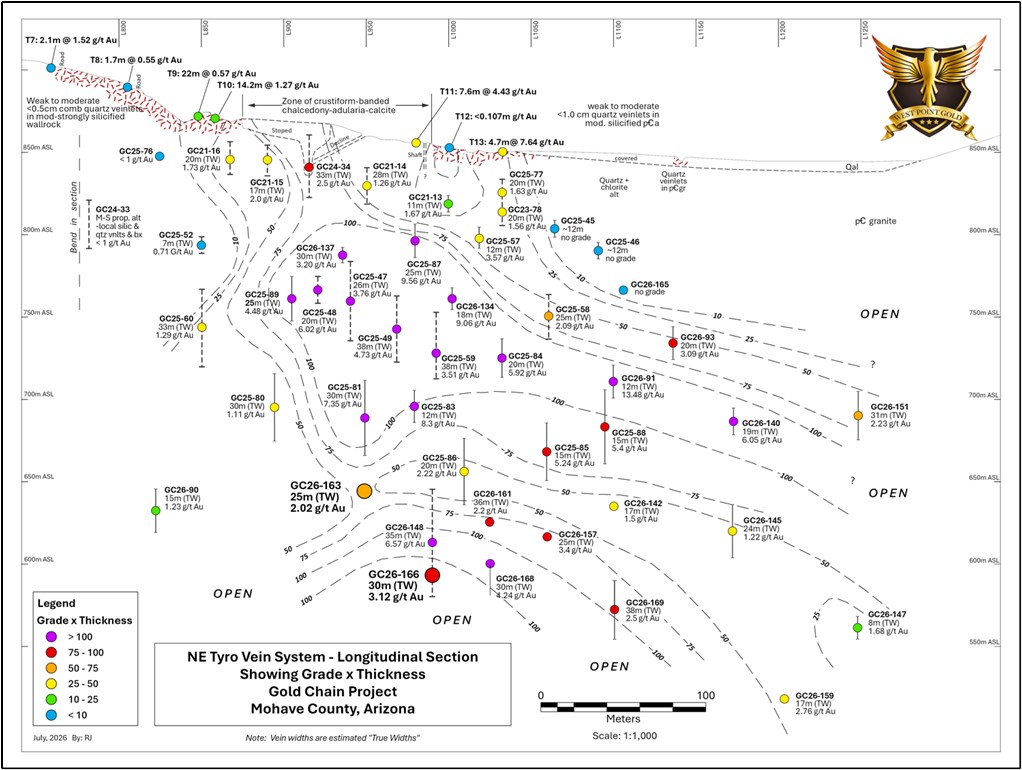

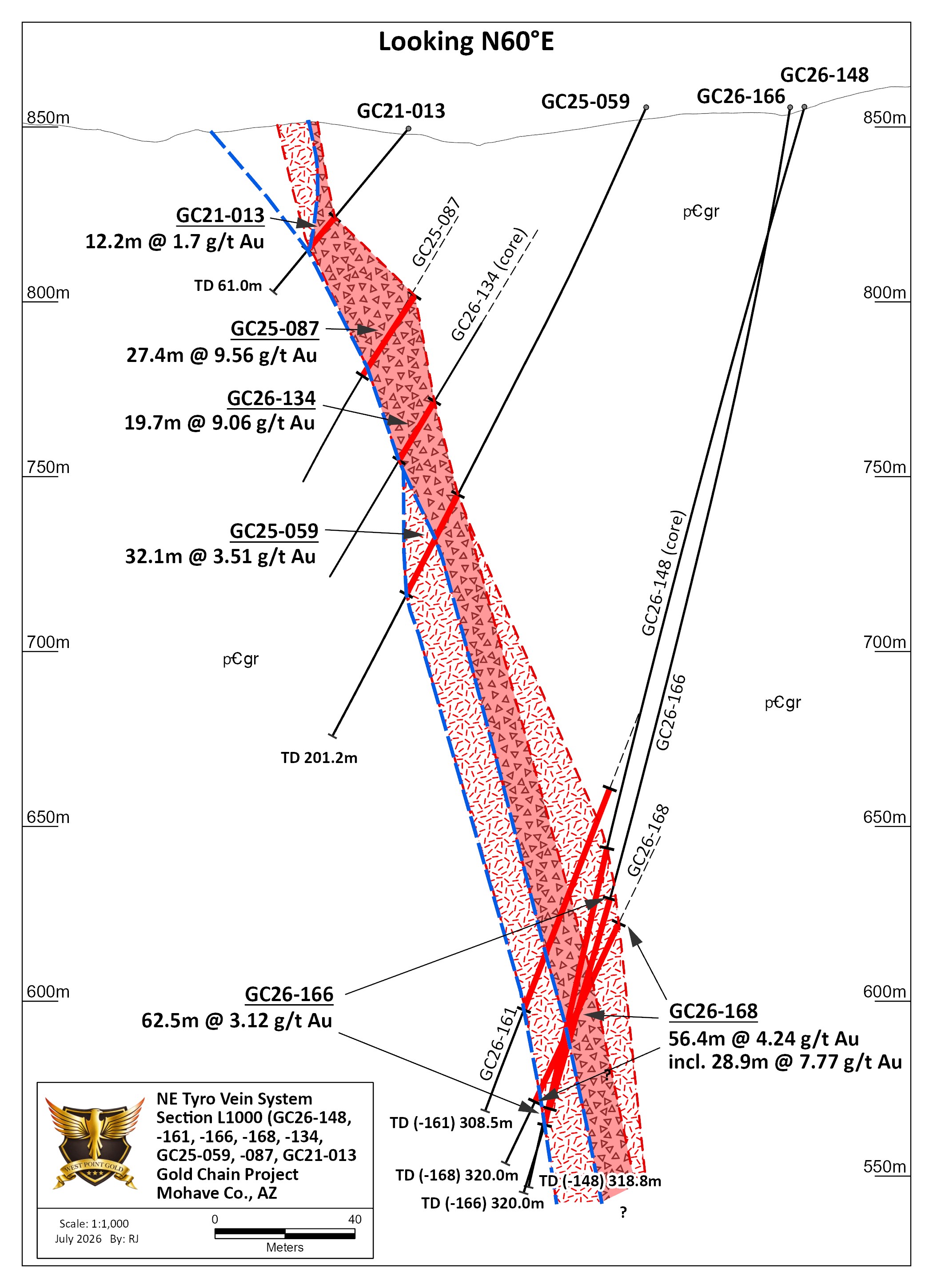

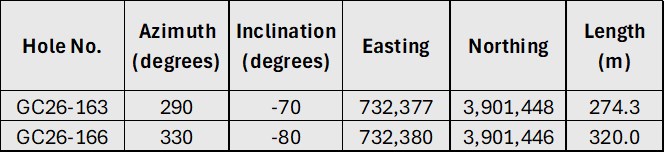

Vancouver, British Columbia–(Newsfile Corp. – July 29, 2026) – West Point Gold Corp. (TSXV: WPG) (OTCQX: WPGCF) (FSE: LRA0) (“West Point Gold” or the “Company”) is pleased to announce the results from two more drill holes from the high-grade Northeast (“NE”) Tyro zone at its flagship Gold Chain Project in Arizona. Results are highlighted by Hole GC26-166, which was a reverse circulation (“RC”) hole that intersected 62.5 metres (“m”) of 3.1 grams per tonne (“g/t”) gold (“Au”) from 233m, including 38.1m at 4.7 g/t Au. This intercept has an estimated true width (“TW”) of 30m. These holes continue to bolster the widths and continuity of the high-grade zone at NE Tyro, which remains open to depth and to the northeast towards the prospective Frisco Graben target.

The Company is reporting assay results for two drill holes (594.3m), GC26-163 and GC26-166, from the recently completed 21,079m drill program. Assays are pending for 4,907m from the Tyro Main Zone and Black Dyke targets. All drill data is currently being compiled, evaluated and analyzed as part of the Company’s upcoming maiden resource estimate expected to be released later in 2026.

Highlights:

Hole GC26-166 (Line 1000) intersected 62.5m at 3.12 g/t Au, about 20m in front of GC26-148 (66m at 6.57 g/t Au);

Hole GC26-163 (Line 950) intersected 54.9m at 2.02 g/t Au, including 19.8m at 4.40 g/t Au beginning approximately 197m below surface;

Results from both sections (L950 and L1000) indicate that the NE Tyro vein is well developed between 300 and 350m below the surface;

NE Tyro remains open to depth and to the northeast towards the Frisco Graben.

Derek Macpherson, President and CEO, stated, “Drilling this year at NE Tyro has materially expanded the zone to depth and to the northeast. More importantly, the results indicate that this high-grade zone remains open in multiple directions. We believe the consistency of the mineralization, the high grades, and the apparent widening of the zone at depth bode well for the pending maiden resource and the upcoming drill program. A key focus of West Point Gold’s next drill program is to continue expanding NE Tyro at depth and along strike.”

Figure 1. Plan view of the Tyro NE vein showing geology and drilling conducted in 2021, 2023, 2024, 2025, and 2026. Note the location of Hole Nos. GC26-163 (L950) and GC26-166 (L1000).

Figure 2. Longitudinal perspective of the Tyro NE zone contoured GT (g/t Au X estimated true thickness) highlighting the results from Holes GC26-163 and GC26-166.

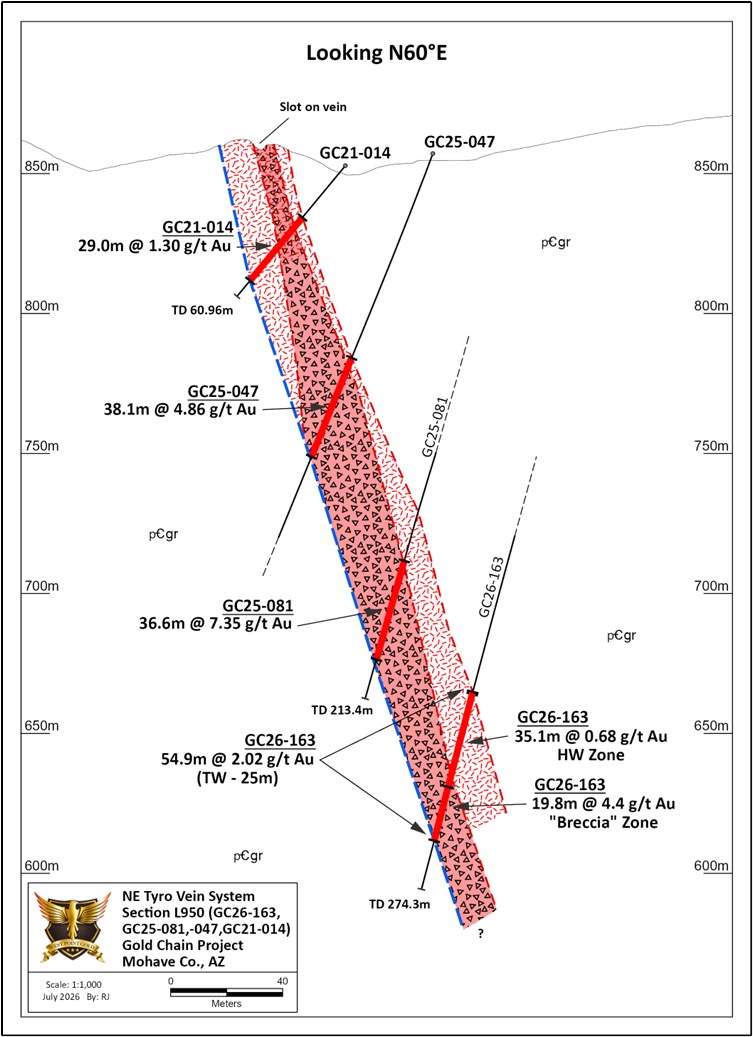

Section L950 (Figure 3) reveals that the NE Tyro vein system is continuously mineralized from the surface downward to an elevation of 635mASL, or at least 230m vertically. The mineralized zone, which is defined by a planar structure dipping at 70o, is dominated by vein breccia (hydrothermal) in the footwall and quartz-calcite-adularia veinlets dominating toward the hanging wall. The footwall vein breccia in Hole GC26-163 hosts about 12m of 4.4 g/t Au (TW; Figure 3). Figure 2 reveals that this strong vein remains open at depth and to the southwest.

Figure 3. Geologic section drawn along Line 950 showing vein and spatial relation between GC26-163, GC21-014, GC25-047 and GC25-081.

Section L1000, shown in Figure 4, contains Holes GC26-166, GC26-168, GC21-013, GC25-087, GC26-134 (core), GC25-059 and GC26-148 (core). This hole was designed to test the vein zone about 50m below GC26-148 but flattened slightly to cut the vein about 20m below. GC26-166 contained (Table 1) intersected 62.5m (TW = 30m) at 3.12 g/t Au including 38.1m of 4.7 g/t Au. Unlike GC26-163, quartz veining extends several meters into the footwall below the likely controlling structure. Alteration of the Precambrian granite across this zone consisted of moderate to strong illite-pyrite alteration replacing chlorite in the propylitic selvage

Figure 4. Geologic section drawn along Line 1000 showing vein and spatial relation between GC26-166, GC26-168, GC21-013, GC26-134, GC25-087, GC25-059 and GC26-148 (core).

The Company intends to issue 46,110 common shares of the Company, valued at CDN$1.466 per share, in connection with a US$48,000 (CDN$67,598) share payment due under the option agreement covering a portion of the Company’s landholdings for the Gold Chain Project in Arizona.

The common shares issued will have a statutory hold period of four months and one day from the date of issuance. This share for debt transaction remains subject to TSX Venture Exchange approval.

Qualified Person

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration, is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for overseeing all phases of the drilling program, including logging, cutting, labelling, bagging and transport from the project to American Assay Laboratories (AAL) of Sparks, Nevada. Reverse Circulation (RC) drill holes have a diameter of about 10cm (~4″), and samples have an approximate weight of 5 to 10kg. All samples are packaged for shipment at the facility and trucked to AAL in Reno. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, and over-limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), and over-limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. The results summarized above have been carefully reviewed with reference to the QA/QC results. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

About West Point Gold Corp.

West Point Gold is an exploration and development company focused on unlocking value across four strategically located projects along the prolific Walker Lane Trend in Nevada and Arizona, USA, providing shareholders with exposure to multiple discovery opportunities across one of North America’s most productive gold regions. The Company’s near-term priority is advancing its flagship Gold Chain Project in Arizona.

For further information regarding this press release, please contact: Aaron Paterson, Corporate Communications Manager Phone: +1 (778) 358-6173 Email: info@westpointgold.com

Certain statements contained in this press release constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, timing of the Company’s maiden resource estimate, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures. In particular, this press release contains forward-looking statements concerning the timing of a maiden resource estimate and the belief that Tyro NE will be open to depth following that estimate. The Company cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete any payments or expenditures required under the Company’s various option agreements for its projects; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainties related to resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data; the potential for delays in exploration or development activities; uncertainty related to the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results may vary from those expected; statements about expected results of operations, royalties, cash flows, financial position may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions. The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; fluctuating gold prices; possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR made by the Company with securities regulators. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate press release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Purpose-built AI application deployed at C.C. Carlton Industries, demonstrating AIAI’s Transformational AI strategy from framework to operational execution

DALLAS, TX / ACCESS Newswire / July 22, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announced the deployment of Bid Accelerator a custom built application developed under the Company’s Transformational AI (TAI) Integration Playbook, which was introduced in June to provide a disciplined framework for identifying, designing and implementing AI-enabled value creation opportunities across its portfolio companies. The application is being deployed within the wholly owned subsidiary C.C. Carlton Industries (“CCCI”), serving as a foundational demonstration of that strategy.

“Our June announcement introduced the framework for integrating Transformational AI across our portfolio,” said Todd Furniss, Chief Executive Officer and Co-Founder of AIAI Holdings.” The deployment of Bid Accelerator is a perfect example of the operational implementation of that strategy. More importantly, it demonstrates how our integration playbook moves from assessment to purpose-built AI solutions that address real operational challenges. We built Bid Accelerator by analyzing over $7 Billion from over 1500 bids developed by CCCI. The initial results have been profound. As Bid Accelerator continues learning from CCCI’s workflows and operational data, we believe it will deliver increasing value over time while establishing a repeatable model for future applications across our portfolio.”

Bid Accelerator is designed to augment CCCI’s experienced estimating professionals by streamlining bid preparation, preserving institutional knowledge and continuously learning from operational data. This makes every professional more productive and more focused on winning opportunities. Continuous learning enables organizations to further improve proposal quality, increase bid capacity, and enhance contract win rates over time. We expect the resulting productivity improvements and operational efficiencies will begin contributing to financial performance during the first half of 2027.

“The knowledge and judgment of our estimating professionals are among CCCI’s most valuable assets,” said Ben Lyon, Chief Executive Officer of C.C. Carlton Industries. “Bid Accelerator is designed to amplify that expertise by continuously learning from every bid and equipping our estimating professionals with increasingly intelligent decision support. We believe it will help us pursue more opportunities, improve proposal quality, increase contract win rates and strengthen our competitive position as we continue to grow.”

Bid Accelerator is a key demonstration of Ai2’s broader Transformational AI strategy and provides a repeatable model for future deployments across the Company’s portfolio. As additional applications are developed and implemented, each deployment is expected to expand Ai2’s operational intelligence, refine its integration playbook, accelerate future implementations and strengthen the Company’s growing library of proprietary AI capabilities designed to enhance productivity, improve decision-making and create long-term shareholder value.

About Bid Accelerator

Bid Accelerator is a purpose-built Transformational AI application developed utilizing M42’s AI technologies and deployed by AIAI Holdings within C.C. Carlton Industries. Designed specifically for construction estimating operations, the platform streamlines bid preparation, preserves institutional knowledge, continuously learns from operational data and historical project outcomes, and provides AI-assisted decision support intended to improve estimating efficiency, proposal quality, bid throughput and long-term contract win rates. By integrating mathematics and science AI with behavioral (psychometric) AI capabilities, Bid Accelerator is designed to become increasingly intelligent over time as it learns from organizational experience and operational workflows.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai2) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai2 is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries.

About C.C. Carlton Industries

C.C. Carlton Industries, Ltd. (CCCI), with over 30 years in Central Texas, delivers construction projects with 150+ years of executive team experience, ensuring timely and high-quality outcomes. Boasting over 50 safety certifications, a professional SWPPP team, and TxDOT prequalification, CCCI maintains an unrivaled safety program and compliance, bonding projects of any size.

C.C. Carlton Industries is a portfolio company of AIAI Holdings Corporation (NASDAQ:AIAI).

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

The forward-looking statements in this press release are based on information available to us as of the date hereof, and we disclaim any intention to, and, except as may be required by law, undertake no obligation to, update or revise forward-looking statements to reflect events or circumstances that subsequently occur or of which the Company hereafter become aware. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

Olympio Metals Limited (ASX: OLY) will acquire an 80% interest in Scout’s Jacknife silver project for US$120,000 in cash, 45,000,000 Olympio shares, and up to 25,000,000 performance shares, with a firm commitment of 17,000 meters of drilling over six years.

Scout retains a 20% interest, free-carried through to commercial production and will be the in-country operating partner, providing geological and drilling services with its internal teams and drill rigs at cost plus 25%.

The agreement extends Scout’s vertically integrated discovery-to-partnership model: the Company profitably advances its own projects with in-house drill rigs and geologic teams while retaining a carried interest.

Coeur d’Alene, Idaho – July 20, 2026 – Scout Discoveries Corp. (“Scout” or the “Company”) is pleased to announce the execution of a binding asset sale and joint venture agreement with Olympio Metals Limited (ASX: OLY) (“Olympio”). Under the agreement, Olympio will acquire an 80% interest in Scout’s Jacknife high-grade silver project (the “Project”), located in the Lakeview Mining District, Bonner County, Idaho, part of the broader Silver Valley region, and the parties will form an 80/20 joint venture to advance the Project, summarized below and in Table 1.

Transaction HighlightsUpfront Consideration:US$20,000 non-refundable deposit within 30 days of execution of the agreement, with a 30-day due diligence period; andUS$100,000 in cash and 45,000,000 fully paid ordinary Olympio shares on satisfactory completion of due diligence, with all shares subject to a 12-month voluntary escrow from the date of issue. Based on Olympio’s most recent closing share price of A$0.048, the 45,000,000 share position is worth approximately US$1.5 million.Performance Shares: Scout is eligible to receive up to 25 million additional Olympio shares upon achievement of the following milestones:5,000,000 shares on commencement of drilling at the Project;10,000,000 shares on granting of drilling approvals for the unpatented claims; and10,000,000 shares on announcement of a JORC or NI 43-101 compliant Mineral Resource Estimate of at least 3Moz AgEq.Joint Venture and FreeCarry: Olympio (80%) and Scout (20%) will form a joint venture for further exploration and development of the Project. Scout will be free-carried through to commercial production, with Olympio funding 100% of joint venture expenditure during the carry period, including work programs, claim maintenance, permitting, bonding, underlying payments, and insurance. Scout has no cash funding obligation and is not subject to dilution during the carry. Following commencement of commercial production, Olympio may recover mine development costs from Scout’s share of production, with prior exploration, drilling, overhead, and financing costs excluded.Required Work Obligations: Olympio must fund geologic mapping and geochemistry in Year 1, geophysics in Year 2, 5,000 meters of drilling by Year 3, and 17,000 meters of cumulative drilling by Year 6. Missed milestones trigger cure rights and reduction of Olympio’s interest, including full reversion of the Project to Scout for a Year 1 failure.Scout as Operating Partner: Scout will provide geological, drilling, and exploration services to the joint venture at cost plus 25% (land and claim payments passed through at cost), executed with the Company’s internal core drill rigs and geologic team.Assumed Obligations: Olympio will assume the pre-existing third-party royalty and advance royalty obligations on the Project and will hold the benefit of Scout’s right of first refusal over the nearby historical Lakeview Mill.Post-Carry Funding: After the carry period and recovery of carried costs, the parties fund pro rata or dilute. If Scout is diluted below 10%, it may elect to convert its interest to a 1% NSR royalty or retain its diluted interest.

Curtis Johnson, Scout’s President and CEO commented, “Jacknife is a clear example of Scout’s business model in action. We consolidated a district-scale silver project anchored by patented mining claims in one of the world’s premier silver regions, outlined the targets, and have now brought on a quality partner in Olympio to fund its advancement while Scout stays directly engaged as the operating partner. We maintain continuity with the targeting by drilling with our own rigs and geologic team, while generating meaningful revenue for Scout over the coming years. Most importantly, we retain a 20% interest free-carried through to commercial production, plus meaningful equity in Olympio to share in any future discovery success.”

About the Jacknife ProjectThe Jacknife Project covers 3,940 acres in the Lakeview Mining District, approximately 35 kilometers northeast of Coeur d’Alene, Idaho, and 45 kilometers north of the prolific Silver Valley Mining District, which has produced over 1.2 billion ounces of silver (Figure 1). The Project includes 335 acres of patented mining claims covering ~80% of a ~7-kilometer trend of mineralized shear zones hosted in the same Belt Supergroup formations as the Silver Valley deposits.Patented claims are private property requiring no federal permitting for exploration and limited permitting for underground mining. Six historical mines within the Project produced over 3.2Moz of silver at an average grade of 12.7 oz/t, including ~2Moz at grades up to 22 oz/t (684 g/t) Ag from the Conjecture Mine (1956–1964), which was developed to a depth of more than 600 meters. A 1975 historical estimate for the Conjecture Mine reported 632,081 tonnes @ 13 oz/t (405 g/t) Ag for 8.22Moz of silver, and mineralization remains open along strike and at depth. Historical drilling in 2012 returned intercepts including 1.4m @ 692 g/t Ag and 0.6m @ 1,106 g/t Ag.

Next Steps – Work ProgramOlympio will fund a maiden core drilling program at the Conjecture Shear Zone, targeting the continuity of grade between the historical mine levels, together with Project-wide geologic mapping and soil and rock sampling to generate and prioritize additional drill targets (Figure 2). Because the patented claims provide immediate access with no federal permitting for exploration, drilling can commence once a drill rig is available. Scout will execute the work programs as operating partner using its internal core drill rigs and geologic team.

Cautionary note: The Conjecture Mine estimate is a historical estimate prepared in 1975, prior to the establishment of modern reporting codes. It is not compliant with S-K 1300, NI 43-101, or the JORC Code (2012); a qualified or competent person has not done sufficient work to classify it as a current mineral resource; and it should not be relied upon. Further evaluation, including drilling, is required to verify the estimate. Historical production and drilling results are drawn from historical records that have not been independently verified.

About Olympio Metals LimitedOlympio Metals Limited (ASX: OLY) is an Australian listed mineral exploration company headquartered in West Perth, Western Australia. Olympio’s portfolio includes the Raven high-grade silver project and the Sawtooth antimony project in the western United States.

About Scout Discoveries Corp.Scout Discoveries Corp., headquartered in Coeur d’Alene, Idaho, is a private U.S. mineral exploration company with rights to twelve separate precious and base metal projects in the western U.S.A., comprising one of the largest unpatented claim holdings in the region, totaling over 50,000 acres. Scout’s vision is to bring the full discovery process in-house from idea generation through resource drilling, lowering costs and increasing efficiency. With this model, the Company can rapidly advance its project portfolio through discovery by leveraging its five internal core drill rigs and experienced technical teams.For further information, visit: https://www.scoutdiscoveries.com/

Forward-looking StatementsCertain statements in this news release are forward-looking and involve a number of risks and uncertainties. Such forward-looking statements are within the meaning of that term in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not comprised of historical facts. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. Forward-looking statements may be identified by such terms as “believes”, “anticipates”, “expects”, “estimates”, “may”, “could”, “would”, “will”, or “plan”. Since forward-looking statements are based on assumptions and address future events and conditions, by their very nature they involve inherent risks and uncertainties. Although these statements are based on information currently available to the Company, the Company provides no assurance that actual results will meet management’s expectations. Risks, uncertainties and other factors involved with forward-looking information could cause actual events, results, performance, prospects and opportunities to differ materially from those expressed or implied by such forward-looking information. Factors that could cause actual results to differ materially from such forward-looking information include, but are not limited to those risks set out in the Company’s public documents filed on EDGAR. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law. No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein.

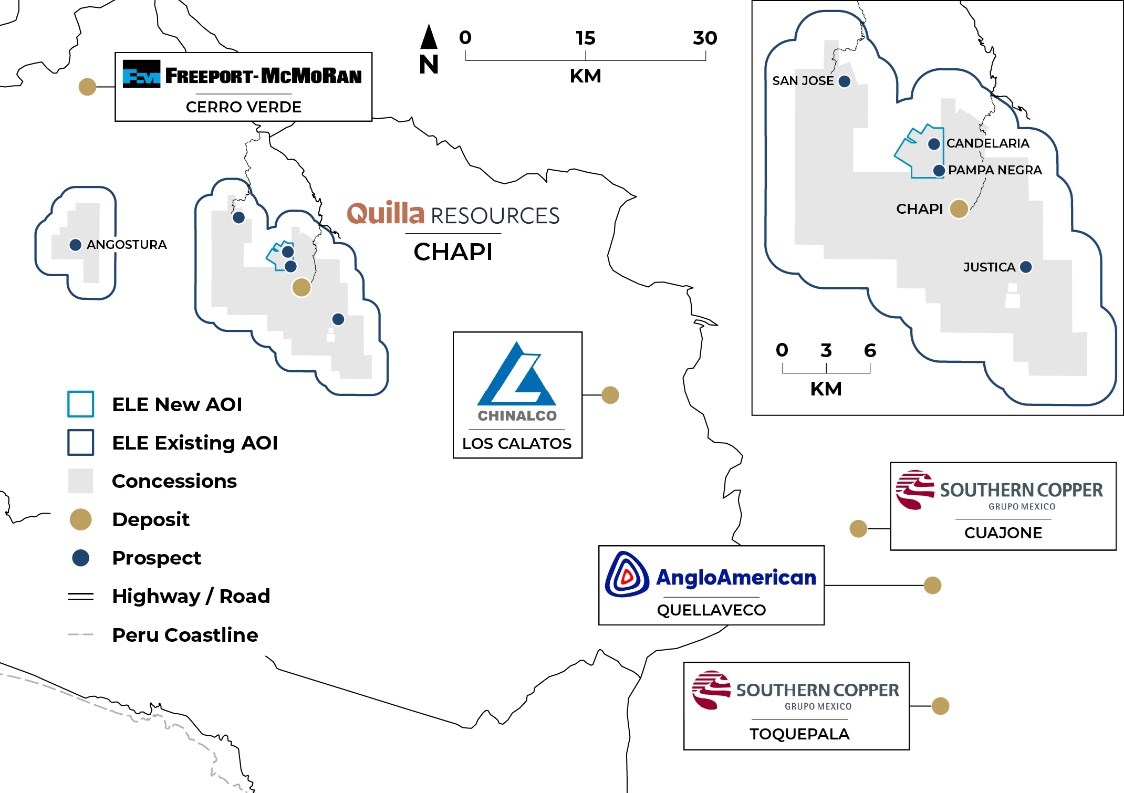

Denver, Colorado–(Newsfile Corp. – July 15, 2026) – Elemental Royalty Corporation (NASDAQ: ELE) (TSX: ELE) (“Elemental” or the “Company“) is pleased to announce that it has entered into a strategic US$25 million investment package (the “Transaction“) with Quilla Resources Inc. (“Quilla“) and its subsidiary Minera Pampa de Cobre S.A.C. (“MPC“) to expand Elemental’s royalty exposure to the producing Chapi Copper Project in Peru (“Chapi“) and support Quilla’s next phase of growth.

The Transaction includes the acquisition of both equity in Quilla, and an additional perpetual, uncapped 1.0% net smelter return (“NSR“) royalty over the Pampa Negra and Candelaria concessions, which are expected to be important contributors to Quilla’s planned expansion of Chapi.

Highlights

Existing Producing Royalty: Elemental has agreed a strategic US$25 million investment package with Quilla to expand its existing royalty exposure to the Chapi copper project and support Quilla’s next phase of growth

Increases Exposure to Project: Elemental acquired an additional perpetual, uncapped 1.0% NSR royalty over Quilla’s Pampa Negra and Candelaria concessions, increasing Elemental’s royalty interest to a total of 3.0% NSR

Expansion Plans underway: Pampa Negra and Candelaria will be important contributors to Quilla’s future expansion of Chapi from 10,000 tonnes per annum to 30,000 tonnes per annum of copper cathode production

Experienced team with track record of delivery: Quilla’s management team have an established history in Peru, including as senior executives at Rio Alto, Milpo, Buenaventura, and the Antamina mine.

Elemental Chief Executive Officer, David M. Cole, commented:“This transaction moves Chapi into a top ten royalty for Elemental by increasing our exposure to Quilla’s Phase 2 expansion at Pampa Negra and Candelaria following the recent successful commissioning of the Chapi mine. The management team’s proven track record of operating in Peru sets them up for continued growth, while Chapi is strategically located within the Southern Copper Belt alongside mines operated by Freeport-McMoRan, Buenaventura, Anglo American, and Southern Copper. We are very pleased to enhance our royalty on the project and simultaneously become a Quilla shareholder as they move toward listing on a public Exchange.”

Existing Chapi Royalty

In February 2025, EMX Royalty Corporation (“EMX“) acquired a 2.0% NSR royalty on minerals produced from the approximately 26,000 hectare property (“Property Royalty”) owned by Quilla, as well as a 2.0% NSR royalty from any minerals that are produced from outside the Property Royalty area, but that are processed at the Chapi Mine processing facilities. The agreement also includes a two-kilometre area of interest (“AOI“) (see Figure 1) around the Property Royalty area, and any property acquired by MPC within this AOI will also be subject to a 2.0% NSR royalty, stepping down to a 1.0% NSR royalty in July 2034.

Elemental acquired EMX in November 2025.

Figure 1: Existing and additional royalty Area of Interest over the Chapi Copper Project, Peru

Under the terms of the transaction, Elemental provided aggregate consideration of US$25 million to Quilla through a combined royalty and equity investment package. The package was structured to expand Elemental’s royalty exposure to the key growth areas at Chapi while also providing Quilla with capital in advance of Listing as it advances the Chapi exploration programme and expansion plans.

Elemental acquired an additional 1.0% NSR royalty over all minerals produced from the Pampa Negra and Candelaria concessions (see Figure 1). The royalty is perpetual, uncapped and not subject to any buyback, step-down or advance payment provisions. This adds to Elemental’s existing 2.0% NSR royalty footprint at Chapi and results in Elemental holding a 3.0% NSR royalty over Pampa Negra and a 3.0% NSR royalty over Candelaria, with the Candelaria royalty stepping down to 2.0% NSR in July 2034.

As part of the same transaction package, Elemental subscribed for shares in the company, representing approximately 9% of Quilla. The equity investment provides Elemental with additional alignment and upside as Quilla advances its planned expansion to 30,000 tonnes per annum of copper cathode and looks to go public.

Elemental funded the Transaction from cash on hand. Proceeds from the Transaction are to be used by Quilla to fast-track exploration as well as permitting and engineering work related to the planned expansion.

Background on Quilla

Quilla is a private Canadian company that, in December 2024, acquired MPC and the associated Chapi licence areas. Quilla was founded by a select group of shareholders, including Victor Gobitz, looking to rapidly build an intermediate-sized base metals company. Mr. Gobitz is a senior mining executive with extensive recent leadership experience at two of Peru’s most prominent mining companies. Prior to joining Quilla, he served as President and General Manager of the world-class Antamina mine, following his tenure as President and Chief Executive Officer of Compañía de Minas Buenaventura.

The Chapi Copper Project

Chapi is a former producing copper project that restarted production in Q1 2026 (see announcement dated March 2, 2026).

The Chapi Mine is located in the prolific Southern Peru porphyry copper belt across the Moquegua and Arequipa Departments, which host large scale operations including Southern Copper’s Toquepala, Anglo American’s Quellaveco Project, and Freeport-McMoRans’s majority owned Cerro Verde mine. The asset sits at an elevation of approximately 2,750 meters and has ready access approximately 50 kilometers south-southeast from the city of Arequipa. The mine, which was in operation from 2006-2012, reached maximum production levels of 8,500 tonnes per annum.

The historic Chapi Mine is comprised of two principal open pits, underground workings, a crushing and agglomeration circuit, heap leach pads, a solvent extraction plant, an electrowinning copper cathode plant, and related infrastructure including mine camp, office facilities, water supply, and power.

The restart and successful commissioning of the SX-EW plant in 2026 was achieved on time and budget, reflecting management’s strong track record as operators and work has begun on Phase 2 expansion as well as fast tracking investment in exploration and ongoing investment to optimise operations.

Technical Disclosure and Qualified Person

The scientific and technical information contained in this news release has been reviewed and approved by Michael Sheehan, a “Qualified Person” and employee of the Company as defined in National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101“).

Elemental is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 18 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental trades on Nasdaq and on the Toronto Stock Exchange under the ticker Symbol “ELE”.

This news release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable Canadian and United States securities laws. Forward-looking statements include, but are not limited to, statements regarding the completion of the Transaction, the timing and satisfaction of closing conditions, the expected use of proceeds by Quilla, the expected benefits of the Transaction to Elemental and its shareholders, Chapi’s expected ramp-up and expansion plans, future production levels, expected royalty revenue, potential exploration upside, Quilla’s potential IPO, copper market conditions and future opportunities for collaboration with Quilla and Hartree.

Forward-looking statements are based on assumptions that management believes to be reasonable as of the date of this news release, including assumptions regarding the receipt of required approvals, the accuracy of technical and operating information provided by the operator, future copper prices, mine plans, permitting timelines, capital availability, operating performance, exploration results and the ability of Quilla and MPC to advance Chapi.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause actual results to differ materially from those expressed or implied by such statements. These risks include, but are not limited to, the failure to complete the Transaction, changes in commodity prices, differences between projected and actual production, delays in ramp-up or expansion activities, permitting or regulatory delays, operational challenges, resource and reserve uncertainty, political and jurisdictional risks, title and royalty enforceability risks, foreign exchange fluctuations, capital markets conditions and the other risk factors described in Elemental’s public disclosure documents filed on SEDAR+ and EDGAR.

Readers should not place undue reliance on forward-looking statements. Elemental undertakes no obligation to update forward-looking statements except as required by applicable securities laws.

Ross McElroy Steps Down as President, CEO and Director Effective July 15, 2026

VANCOUVER, British Columbia, July 16, 2026 (GLOBE NEWSWIRE) — Apollo Silver Corp. (“Apollo Silver” or the “Company“) (TSX.V:APGO, OTCQB:APGOF, Frankfurt:6ZF) announces that Ross McElroy has stepped down as President and Chief Executive Officer of the Company and has resigned from the Company’s Board of Directors (the “Board”), effective July 15, 2026. The Company has entered into an agreement with Colin P. Sutherland, CPA, CA, under which Mr. Sutherland will assume the role of President and Chief Executive Officer, effective July 15, 2026. Mr. Sutherland is not joining the Board at this time.

“On behalf of the Board and the entire Apollo Silver team, I want to thank Ross for his leadership and the many contributions he has made in advancing the Company’s projects. Ross leaves the Company well positioned for its next phase of growth and we wish him well in his future endeavours,” said Tom Peregoodoff, Executive Chair of Apollo Silver. “At the same time, we are very pleased to welcome Colin Sutherland as our incoming President and CEO. Colin brings more than two decades of senior executive and financial leadership across gold and silver producers, having served as President, CEO, and CFO of companies operating internationally, in North America and more specifically, Mexico. His track record of capital markets execution, M&A leadership, and operational discipline makes him an excellent fit to lead Apollo Silver through its next stage of growth. Finally, to our shareholders, thank you for your continued trust and support as we build on the momentum Apollo Silver has established.”

“I am honoured to join Apollo Silver at such an important stage in the Company’s growth,” said Mr. Sutherland. “Apollo Silver holds one of the largest undeveloped primary silver assets in the United States, together with a high-quality option on the Cinco de Mayo project in Mexico. I believe my 20 plus years of corporate leadership and operating experience in Mexico, as well as other jurisdictions, is ideal for Apollo Silver’s current position and I look forward to working with the Board, management, and shareholders to advance these assets and build long-term value.”

About Colin Sutherland

Mr. Sutherland is a Chartered Professional Accountant with more than two decades of international experience in mining finance, capital markets, and operations, including senior executive and operating roles with Capital Gold Corporation, Nayarit Gold and McEwen Mining across projects in the broader Americas and globally.

At Capital Gold, owner of the producing El Chanate gold mine in Sonora, Mexico, he led the merger and acquisition process, including the combination with Nayarit Gold and the subsequent sale of the company, delivering positive returns to shareholders. He subsequently served as President of McEwen Mining, where he oversaw operations and capital markets activity across the company’s Mexican operations, delivering improving performance during his tenure. Mr. Sutherland’s background spans both M&A and operating sides of the mining business.

Mr. Sutherland is a permanent resident of Mexico.

Incentive Awards

Pursuant to the Company’s Omnibus Incentive Plan (the “Plan”) dated December 12, 2024, and the policies of the TSX Venture Exchange (the “TSXV”), the Company’s Board of Directors has approved the grant of incentive stock options (the “Options”) and deferred share units (the “DSUs”) to an officer and a director of the Company.

The Company has granted Options to purchase an aggregate of 250,000 common shares of the Company (each, a “Common Share”), at an exercise price of $2.52 per Common Share, being the closing price of the Common Shares on the TSXV on the date of grant. The Options vest over a 24-month period, with one-third vesting on the date of grant, one-third vesting 12 months from the date of grant, and the balance vesting 24 months from the date of grant. Once vested, each Option is exercisable into one Common Share for a period of five years from the date of grant.

The Company has also granted an aggregate of 100,000 DSUs. Each DSU entitles the holder, when settled, to receive one Common Share, and may only be settled once the holder ceases to serve as a director of the Company, in accordance with the terms of the Plan.

ABOUT APOLLO SILVER CORP.