Vancouver, British Columbia–(Newsfile Corp. – June 4, 2026) – West Point Gold Corp. (TSXV: WPG) (OTCQX: WPGCF) (FSE: LRA0) (“West Point Gold” or the “Company”) is pleased to announce results from its property-wide target testing program. The initial drilling campaign into the Union Pass Fault Corridor at the Bull 8 target returned significant gold values highlighted by a 21.4 metre (“m”) broad interval of gold (“Au”) mineralization at 1.01 grams per tonne (“g/t”). The Bull 8 target is approximately 6 kilometres (“km”) northwest (“NW’) of the Tyro zone, outside of where the company is working on its upcoming maiden mineral resource estimate (“MRE”).

The Union Pass Fault is a major regional structural feature, with several associated faults mapped and sampled along its 12km strike length on the property. Initial drilling into the Union Pass Fault Corridor was targeted at Bull 8, which has several historical prospect pits and trenches. West Point Gold completed surface mapping and sampling in the area, which revealed a broad northwest-trending zone of highly prospective mineralization; rock types hosted within gold-bearing structures that have returned gold values greater than 2 g/t Au. Bull 8 is on the northwest portion of the Union Pass Fault Corridor, shown to be a controlling structure of the Frisco Graben.

To date, 20,116m of the ongoing drill program at the Gold Chain project has been completed. Results are pending from the Black Dyke, Tyro Main, and NE Tyro zones representing 35 holes (7,697m).

Highlights:

- Hole GC26-136 returned 21.4m (18m true width) at 1.01g/t Au from 71.6m to 93.0m within a broadly mineralized envelope.

- Hole GC26-130 returned 12.2m of 0.41g/t Au from 6.1m to 18.3m (Figure 2), identifying an extensive near surface lower grade zone.

- The structural corridor that hosts the Bull 8 prospect also is one of the controlling features of the Frisco Graben. Extensive quartz veining, hydrothermal alteration and anomalous gold values can be observed over the entire 12kms.

- All holes drilled across the Bull 8 prospect intersected gold mineralization.

“The significance of the results in GC26-136 has less to do with the significant gold values intersected and more to do with the structural setting. The Union Pass Fault Corridor, and the associated Frisco Mine fault are major regional structural features with approximately 12km of demonstrated strike length on Gold Chain. Exploration success at Bull 8 supports the Company’s view that these major features, which also control the Frisco Graben, appear to have played an important role in the mineralizing events at Gold Chain. We believe these results de-risk other targets along the Union Pass Fault Corridor, including the Frisco Graben,” stated Derek Macpherson, President and CEO.

Table 1: Drill Results

| Holes | From (m) | To (m) | Width (m) | Grade (g/t Au) |

| GC26-126 | 118.9 | 182.9 | 64.0 | 0.12 |

| GC26-128 | No Significant Values | |||

| GC26-130 | 6.1 | 18.3 | 12.2 | 0.41 |

| GC26-132 | 57.9 | 65.5 | 7.6 | 0.35 |

| including | 89.9 | 99.0 | 9.1 | 0.22 |

| GC26-136 | 71.6 | 93.0 | 21.4 | 1.01 |

| GC26-141 | 36.6 | 39.6 | 3.1 | 0.25 |

Note: All widths shown are downhole. True widths are estimated to be 80 to 90% of apparent widths except in GC26-126 which is about 25%.

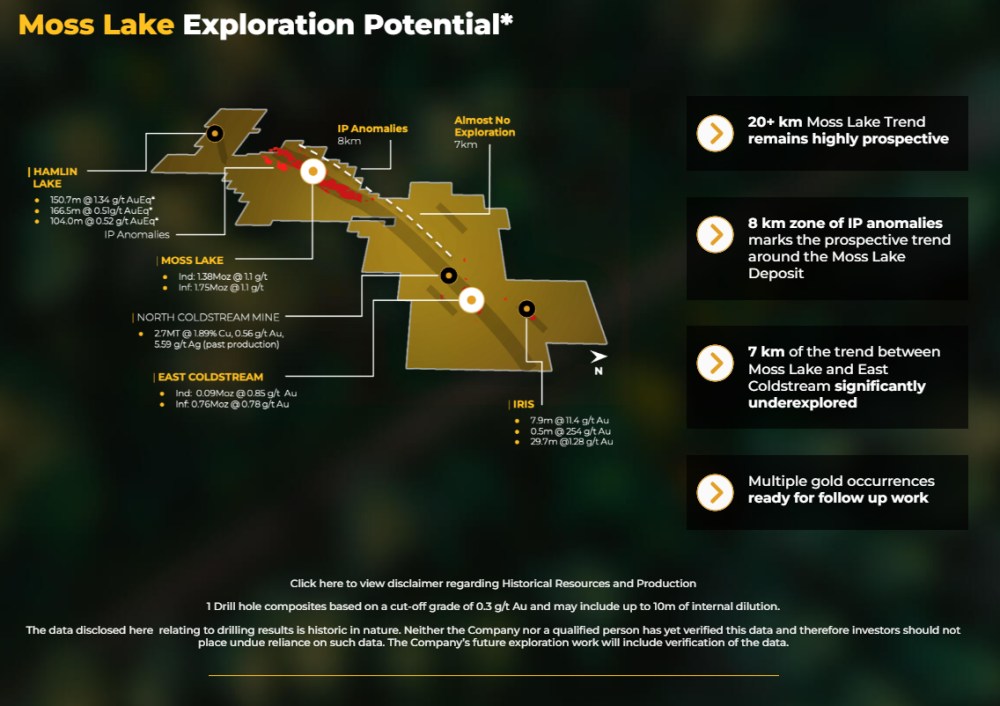

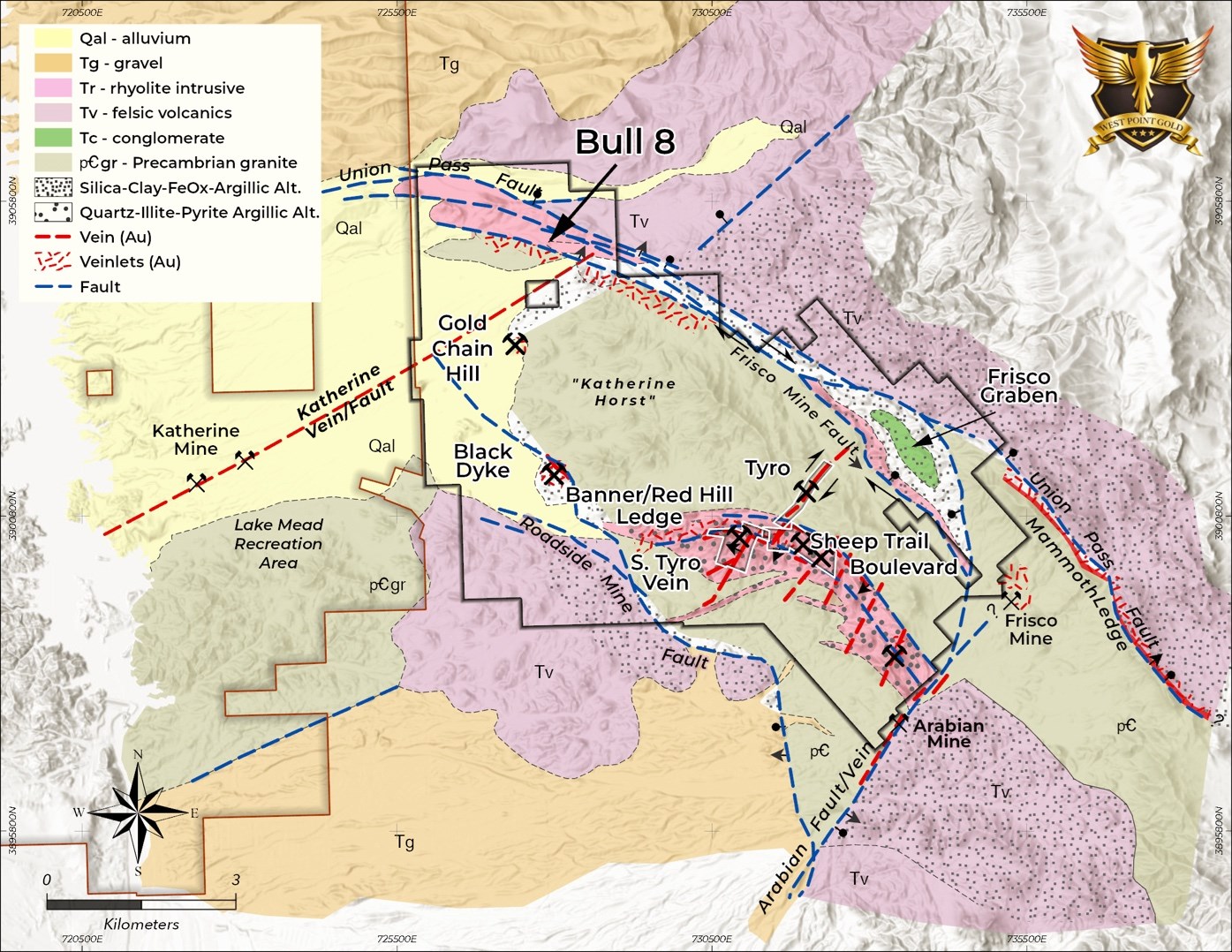

Figure 1: Plan view of the Gold Chain project showing geology, historical mines and/or current prospects. Note the location of the Bull 8 prospect.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/300085_e9717b29241cbb12_002full.jpg

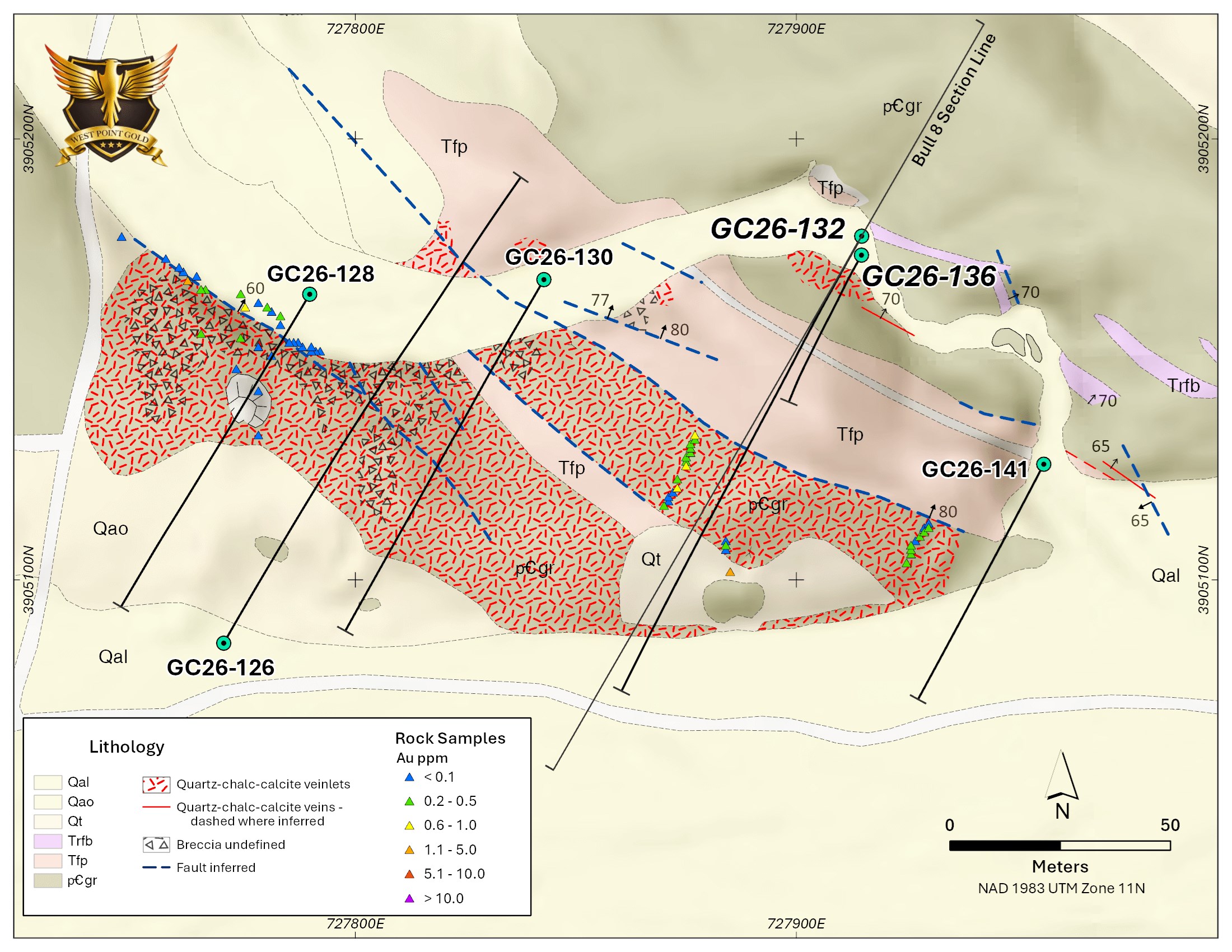

Figure 2. Geologic map of the Bull 8 prospect showing the NW-trending mineralized zone following the intensely broken and sheared Union Pass Fault Corridor. Also shown are the reported drill holes, Au-in-rock values and historical pits and trenches.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/300085_e9717b29241cbb12_003full.jpg

Summary

West Point Gold has recently completed an initial drilling campaign composed of 6 holes totalling 855.7m (Table 2) at Bull 8. The identification of broadly veined intervals at a dike/Precambrian contact within a regional shear zone hosting low-level gold values (100 to 500 ppb Au) suggests follow-up drilling is warranted. This structural corridor, which hosts widespread, high-level veining with anomalous gold values over several kilometres, hosts numerous additional targets. Hole GC26-136, the deepest hole drilled in this campaign, identified 21.4m at 1.01 g/t Au, supporting the Company’s belief that surface features are a manifestation of concealed gold mineralization.

The exploration conducted to date at the Bull 8 prospect, along with more regional geologic, geochemical, and geophysical studies, reveals that a regional northwest structural corridor is the dominant geologic feature. The Bull 8 prospect is a small hill surrounded (Figure 2) on 3 sides by Quaternary alluvium. This hill is traversed by several fault-bounded dikes emplaced into widely sheared, brecciated and altered Precambrian granite, which has been tested by several historical pits, adits and trenches; surface gold values are up to 2.09 g/t Au. The dikes and confining structures dip steeply to the north-northeast and are consistent with attitudes seen along the Union Pass Fault

Corridor (including the Frisco Mine Fault) across the Gold Chain project (about 12km). Throughout the entire strike length documented by West Point Gold, the hanging wall (HW) is strongly altered to silica + clay + hematite (steam-heated environment), whereas the footwall (FW) (generally Precambrian granite) is propylitized. Quartz veinlets and cemented breccias are also widespread and commonly anomalous in gold.

Exposures of the mineralized zone at Bull 8 reveal strongly sheared and brecciated Precambrian granite hosting both quartz vein fragments and quartz-chalcedony veinlets and silicification. The sheared and brecciated rocks contained abundant iron oxides, which were observed in all of the drill holes. The highly variable appearance of the mineralized zone, including quartz styles, textures and colours, suggests prolonged tectonism and mineralization, including widespread evidence of post-mineral movements. Distinct, continuous veins are not apparent.

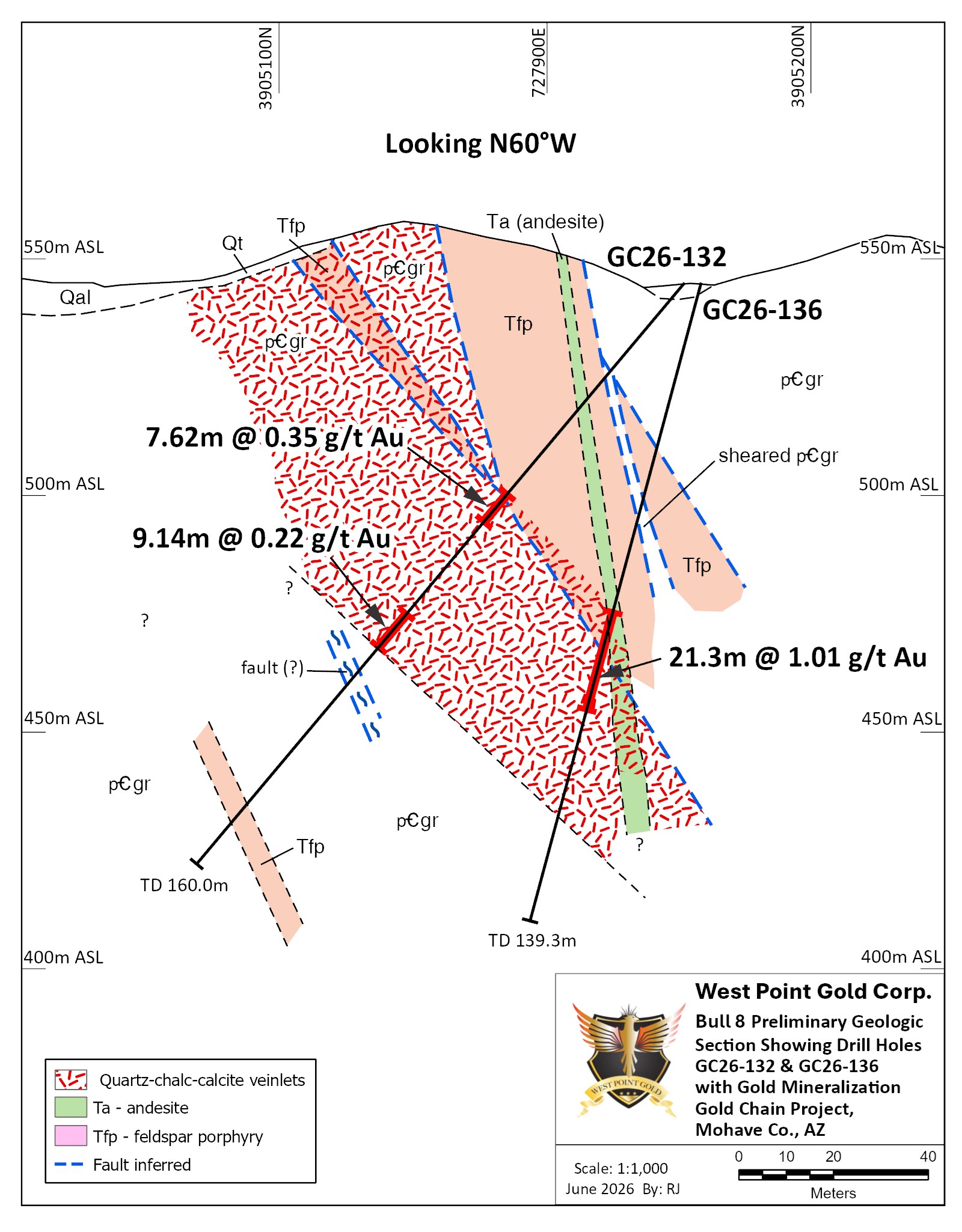

Figure 3. Geologic section drawn along Holes GC26-132 and GC26-136 showing felspar porphyry and andesite dikes emplaced into a shear zone. Gold mineralization is concentrated along the footwall contact of the dike complex.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/300085_e9717b29241cbb12_004full.jpg

Figure 3 provides a geologic sketch of the two deeper holes, GC26-132 and -136. The section reveals a close correlation between quartz veining, along with gold, and the footwall contact of a feldspar porphyry dike complex and the Precambrian granite. This contact, along with other dike contacts, are faults. Surface exposures of the dike do not reveal shearing, brecciation, or fracturing as seen in the surrounding Precambrian granite, suggesting that the dikes were emplaced into the structural corridor after much of the tectonism. Similar features have been observed several kilometres to the southeast, i.e. Frisco Graben and Tyro Vein, suggesting a prolonged structural history.

Importantly, Hole GC26-136 encountered gold grades up to 5.96 g/t Au and 21.4m at 1.01 g/t Au from 70.6 to 93.0m. Approximately 50m above (Figure 3), Hole GC26-132 encountered a broad zone of moderate to strong quartz veinlets with 7.62m at 0.35 g/t Au at the HW contact and 9.14m at 0.22 g/t Au along the FW; strongly anomalous gold values exist between the two intervals. Most importantly, veining appears to coalesce with depth, along with an increase in gold values. This scenario is similar to the uppermost NE Tyro vein where strongly altered, weakly mineralized rock sits immediately above broad widths and high gold grades.

Table 2: Drill hole locations and descriptions

| Hole No. | Azimuth (degrees) | Inclination (degrees) | Easting | Northing | Length (m) |

| GC26-126 | 30 | -50 | 727,770 | 3,905,087 | 181.4 |

| GC26-128 | 210 | -50 | 727,790 | 3,905,165 | 125.0 |

| GC26-130 | 210 | -50 | 727,843 | 3,905,168 | 138.7 |

| GC26-132 | 210 | -50 | 727,915 | 3,905,178 | 160.0 |

| GC26-136 | 210 | -75 | 727,915 | 3,905,174 | 139.3 |

| GC26-141 | 210 | -60 | 727,956 | 3,905,126 | 111.3 |

New Era Publishing Inc. marketing engagement

West Point Gold has engaged New Era Publishing Inc. (“New Era”), also doing business as Katusa Research, an arm’s-length service provider, to provide the Company certain investor relations and marketing services, in accordance with the policies of the TSX Venture Exchange and applicable securities laws. Based in Vancouver, BC, New Era specializes in media and investor relations services, within the natural resource sector. Under a consulting agreement dated May 27, 2026, New Era will provide media relations, investor communication and market awareness services to the Company for a three-month term for a one-time fee of $250,000 (U.S.), payable at the commencement of services. The Company will not issue any securities to New Era as compensation for its services. As of the date hereof, to the Company’s knowledge, New Era (including its directors and officers) does not own any securities of the Company. The marketing agreement with New Era is subject to TSX Venture Exchange approval.

Qualified Person

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration, is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for overseeing all phases of the drilling program, including logging, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Drillholes have a diameter of about 10cm, and samples have an approximate weight of 5 to 10kg. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, and over-limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), and over-limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. The results summarized above have been carefully reviewed with reference to the QA/QC results. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

About West Point Gold Corp.

West Point Gold is an exploration and development company focused on unlocking value across four strategically located projects along the prolific Walker Lane Trend in Nevada and Arizona, USA, providing shareholders with exposure to multiple discovery opportunities across one of North America’s most productive gold regions. The Company’s near-term priority is advancing its flagship Gold Chain Project in Arizona.

For further information regarding this press release, please contact:

Aaron Paterson, Corporate Communications Manager

Phone: +1 (778) 358-6173

Email: info@westpointgold.com

Stay Connected with Us:

LinkedIn: linkedin.com/company/west-point-gold

X (Twitter): @westpointgoldUS

Facebook: facebook.com/Westpointgold/

Website: westpointgold.com/

FORWARD-LOOKING STATEMENTS:

Certain statements contained in this press release constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, timing of the Company’s maiden resource estimate, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures. The Company cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete any payments or expenditures required under the Company’s various option agreements for its projects; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainties related to resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data; the potential for delays in exploration or development activities; uncertainty related to the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results may vary from those expected; statements about expected results of operations, royalties, cash flows, financial position may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions. The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; fluctuating gold prices; possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR+ made by the Company with securities regulators. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate press release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/300085