Scout Discoveries will be in Beaver Creek next week during the Precious Metals Summit. If you’ll be in the area and would like to connect, we’d love to hear from you!

Key Take-AwaysCenterra can earn up to 70% of the Lehman Butte project by investing US $30.0 million over eight (8) years in two stages, with committed US $2.0 million in expenditures within the first two (2) years.Scout will be operator with its internal teams at cost plus 20%; the Lehman Butte project is drill-ready with permits in hand.This agreement is the crystallization of Scout’s vertically integrated approach, which allows the Company to be paid to advance its own projects using in-house drill rigs and geologic team.Coeur d’Alene, Idaho – August 27, 2025 – Scout Discoveries Corp. (“Scout” or the “Company”) is pleased to announce the execution of a definitive agreement with Centerra Gold Inc. (“Centerra”). Under this agreement, Centerra has the right to earn up to a 70% interest in Scout’s Lehman Butte epithermal Au-Ag project (the “Project”), located in Custer County, Idaho, through a two-stage Earn-In structure, summarized below and in Table 1. All amounts referenced are in U.S. dollars.Earn-In Agreement HighlightsExecution Payment:Centerra will pay Scout $75,800 (2025 BLM Claim fees and underlying royalty) within thirty (30) business days following execution of the Agreement (August 8, 2025).Initial Stage 1 Earn-In Option: Centerra may earn an initial 51% interest in the Project by incurring a minimum of $15.0 million in qualifying work expenditures over the initial five (5) year period (the “First Option”), which includes:Funding of $500,000 and $1.5 million (a total of $2.0 million) in exploration expenditures on or before each of the first and second anniversaries of the agreement, respectively, as a firm commitment.An additional $13.0 million in qualifying exploration expenditures must be funded by the fifth anniversary of the agreement, bringing the total to $15.0 million.During the First Option, Scout will continue as the exploration and drilling operator for the Project, operating at cost plus 20% for the first $10.0 million and cost plus 15% thereafter.Centerra and Scout will each elect two representatives to a technical steering committee, which will meet quarterly to review budgets and monitor exploration progress.If Centerra does not complete the expenditure requirements of the First Option within five (5) years, 100% ownership of the project will revert back to Scout.Stage 2 Earn-In Option: Subject to Centerra having exercised the First Option, Centerra shall retain the sole right and option to earn an additional 19% ownership interest in the Project, for a total aggregate of 70% ownership interest (the “Second Option”), by:Sole-funding an additional $15.0 million in qualifying work expenditures over a three (3) year period following the First Option.Centerra has the option to assume operatorship of the Project and pay Scout a 10% fee on all expenditures or continue with Scout as operator at cost plus 20% for the first $10.0 million spent under the Section Option and cost plus 15% thereafter.Continued Advancement, Dilution of Ownership:To ensure the project continues to advance if either party elects to do so,following the completion of either the First Option or in the Second Option, if no exploration or development program is undertaken by Centerra within twelve (12) months, Scout maintains the right to propose such a program.If Centerra declines to fund the program, Scout may elect to fund it independently, and Centerra’s ownership will be diluted on a pro rata basis.If either party’s interest drops below 10%, its interest will be converted to a 2% NSR royalty, with 1% buyable upon commencement of commercial production at the net present value (5% discount rate) as defined by the feasibility study.Either party may convert its interest to a 2% NSR royalty at any time during the agreement or joint venture.

Curtis Johnson, Scout’s President and CEO commented, “This agreement with Centerra is the core of our business model. We generate the project, advance it through drill targeting, then partner with a strong group to aggressively drill the targets while staying directly engaged as operator through our vertically integrated platform. By drilling with our internal rigs and leveraging our geologic team, we move faster, drill more meters per dollar for ourselves and partners, and keep momentum and positive cash flow working for shareholders. This is a sustainable exploration model that will allow Scout to test more targets to overcome the low odds of making a tier one discovery.”

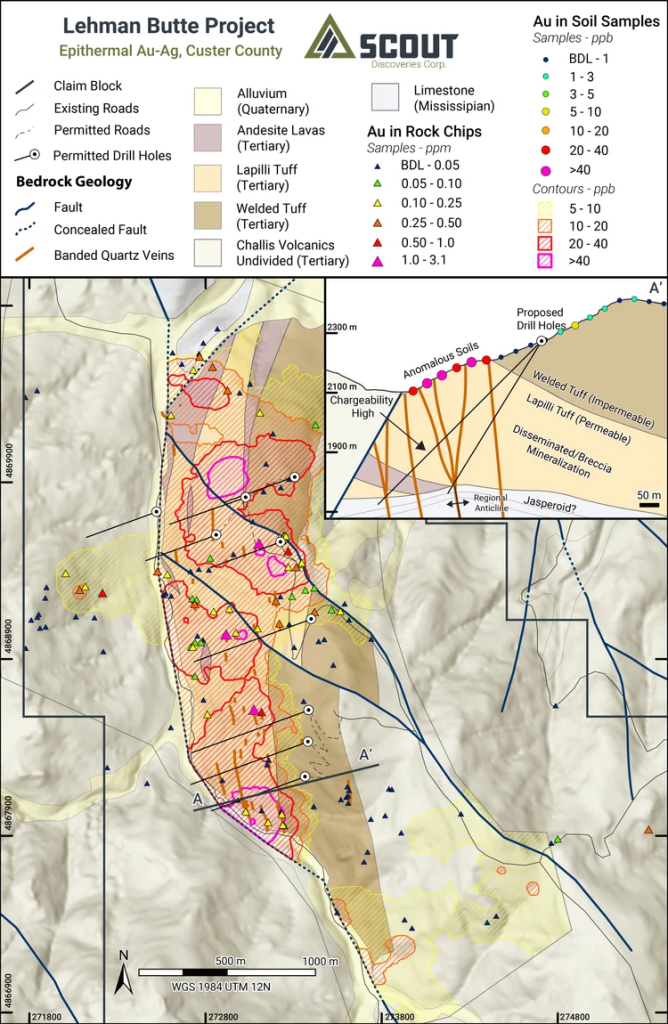

About the Lehman Butte ProjectThe Lehman Butte project, located in central Idaho (Figure 1), features extensive low-sulfidation epithermal veining and quartz-clay-adularia alteration within intermediate volcanic rocks, as well as jasperoid replacement in underlying Mississippian limestone. Exploration by the Scout team, during their tenure at EMX Royalty Corp. and with prior partners, has outlined a cohesive 1.5 x 3 km gold-in-soil anomaly. Rock chip samples have returned values up to 3.1 g/t Au and 19.8 g/t Ag (n=214, avg. 0.145 g/t Au and 4.8 g/t Ag). These results indicate bulk-tonnage style mineralization, centered around a zone of banded quartz-adularia feeder veins up to 2.5 m wide, mapped across 3 km of strike. Coincident magnetic, chargeability, and resistivity anomalies support the targets identified through surface sampling and mapping. The project is permitted for drilling, with primary targets including a bulk-tonnage Au-Ag deposit hosted in volcanics, as well as high-grade bonanza-style epithermal veins at depth.

Next Steps – Work ProgramIn fall 2025, the Scout team will collaborate with Centerra to design and execute an advanced-stage exploration program, funded by Centerra. This will include additional geologic mapping, surface rock sampling, soil sampling, and drone magnetics across the southern portion of the land position that has not yet been covered by these methods. These efforts will lead to a planned Phase I core drilling program in spring-summer 2026, targeting up to 5,000 meters within the primary target zone as outlined in Figure 2.

Execution of Additional Drilling ContractIn addition to the above, Scout has executed an all-in-drilling contract with Mammoth Minerals Limited to carry out an initial 1,500-meter core drilling program in Nevada, including core drilling, rig management, core logging and cutting, as well as TerraCore hyperspectral imaging. The Company has used funds from the advance payment for this program to acquire its fifth surface core drilling rig; an excellent condition, used Boart Longyear track-mounted LF-70.

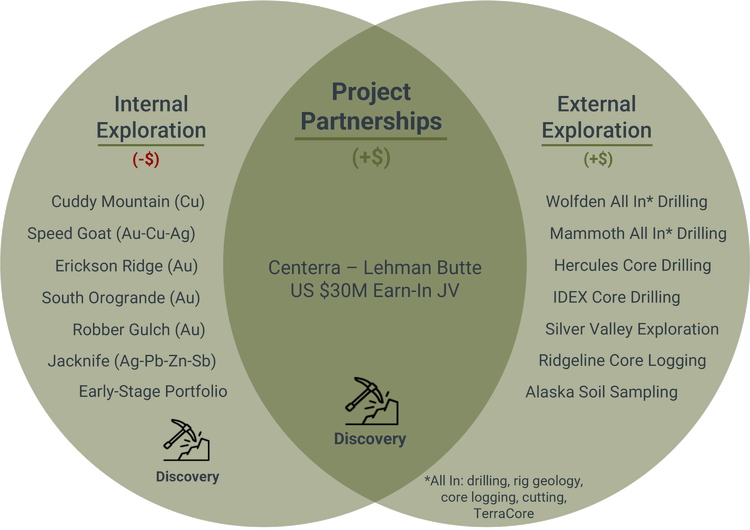

Our Discovery‑to‑Partnership ModelDiscovery generator + vertical integration: Scout’s strategy combines the breadth of a prospect generator with the execution discipline of a major mining company. We advance projects internally, from mapping and geophysics through internal core drilling, with these costs offset by external contracts, then partner when scale and capital intensity increase on the project, preserving upside and accelerating timelines (Figure 3).Lower cost, more meters, aligned structure: Because we manage the full exploration stack in‑house (including drilling), we can reduce exploration costs by ~50–75% versus third‑party contractors. That efficiency lets us drill more meters per dollar and iterate targets faster, supporting rapid decision‑making across the portfolio. This structure is fully aligned with partners earning in on our projects, as Scout’s primary goal is to maximize exploration work done per dollar.Maintaining momentum through partnerships: When a project reaches the right inflection point, we partner with strong groups, such as Centerra at Lehman Butte, to scale work programs while staying directly engaged as operator. Under the Option Agreement, Scout is the initial Project Planner and Operator, enabling continuity of planning, permitting, and drilling cadence as capital ramps, and helping keep momentum squarely on advancing the asset.

About Centerra Gold Inc.Centerra Gold Inc. is a Canadian-based gold mining company focused on operating, developing, exploring and acquiring gold and copper properties in North America, Türkiye, and other markets worldwide. Centerra operates two mines: the Mount Milligan Mine in British Columbia, Canada, and the Öksüt Mine in Türkiye. The Company also owns the Kemess Project in British Columbia, Canada, the Goldfield Project in Nevada, United States, and owns and operates the Molybdenum Business Unit in the United States and Canada. Centerra’s shares trade on the Toronto Stock Exchange under the symbol CG and on the New York Stock Exchange under the symbol CGAU. The Company is based in Toronto, Ontario, Canada.

About Scout Discoveries Corp.Scout Discoveries Corp., headquartered in Coeur d’Alene, Idaho, is a private U.S. mineral exploration company with rights to twelve separate precious and base metal projects in the western U.S.A., comprising one of the largest unpatented claim holdings in the region, totaling over 50,000 acres. Scout’s vision is to bring the full discovery process in-house from idea generation through resource drilling, lowering costs and increasing efficiency. With this model, the Company can rapidly advance its project portfolio through discovery by leveraging its five internal core drill rigs and experienced technical teams. For further information visit: https://www.scoutdiscoveries.com/

Forward-looking StatementsCertain statements in this news release are forward-looking and involve a number of risks and uncertainties. Such forward-looking statements are within the meaning of that term in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not comprised of historical facts. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. Forward-looking statements may be identified by such terms as “believes”, “anticipates”, “expects”, “estimates”, “may”, “could”, “would”, “will”, or “plan”. Since forward-looking statements are based on assumptions and address future events and conditions, by their very nature they involve inherent risks and uncertainties. Although these statements are based on information currently available to the Company, the Company provides no assurance that actual results will meet management’s expectations. Risks, uncertainties and other factors involved with forward-looking information could cause actual events, results, performance, prospects and opportunities to differ materially from those expressed or implied by such forward-looking information. Factors that could cause actual results to differ materially from such forward-looking information include, but are not limited to those risks set out in the Company’s public documents filed on EDGAR. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law. No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein.

Speed Goat is a large-scale porphyry Au-Cu-Ag drill discovery made by the Scout team in northern Nevada’s Battle Mountain mining region following only minor shallow historic drilling.

Multiple holes drilled with +100-meter intervals of 0.5 g/t AuEQ (0.56% CuEQ), large strike length and continuity from surface to 400m depth confirmed and remains open.

Robust thicknesses of porphyry Au-Cu-Ag mineralization at grades and mineralogy consistent with the nearby Phoenix Complex operated by Nevada Gold Mines.

The topography is favorable for surface mining, with road access and proximity to infrastructure, including high-voltage power lines on the property.

Scout continues to aggressively advance its portfolio, expanding operations from two to four surface core drills, which are generating significant revenues for the Company.

Coeur d’Alene, Idaho – August 20, 2025 – Scout Discoveries Corp. (“Scout” or the “Company”) is pleased to provide drill results from its Phase II core drilling program at the Speed Goat Project in Nevada, as well as updates on internal and external core drilling programs and exploration activities. The Company continues to build long-term value through its vertically integrated team by balancing internal drilling and exploration on its portfolio, moving toward a Tier-One discovery and executing cash-flow-generating contracts.

Including 164.8m (from 23.23-188.1m) @ 0.51 g/t Au, 0.15% Cu, 1.98 g/t Ag (0.67 g/t AuEQ; 0.75% CuEQ)

Including 38.9m (from 149.2-188.1m) @ 1.02 g/t Au, 0.27% Cu, 2.25 g/t Ag (1.29 g/t AuEQ; 1.44% CuEQ)

SG25-05: 317.9m (from 0-317.9m) @ 0.25 g/t Au, 0.11%Cu, 1.66 g/t Ag (0.37 g/t Au EQ; 0.41% CuEQ)

Including 136.1m (from 30.4-166.5m) @ 0.42 g/t Au, 0.16% Cu, 2.47 g/t Ag (0.59 g/t AuEQ; 0.66% CuEQ)

Including 43.4m (from 36.3-79.7m) @ 0.73 g/t Au, 0.25% Cu, 4.03 g/t Ag (1.00 g/t AuEQ; 1.11% CuEQ)

Scout Operational Update Highlights:

Exploration Updates: Scout has made substantial progress in exploring its project portfolio during the 2025 season, including:

Geological mapping at Cuddy Mountain, along with a large-scale joint Magnetotelluric–Natural Source Induced Polarization (MT–NSIP) survey with Hercules Metals.

Surface mapping and soil sampling at Independence and soil sampling at Moose Ridge. Further mapping and sampling are planned at Lehman Butte and Muldoon.

Aggressive generative exploration for copper in the western U.S., with one newly staked project now advancing through evaluation phases including mapping and sampling.

Cuddy Mountain Permitting: Scout is finalizing permits for 18 drill sites at Cuddy Mountain and anticipates drilling to commence at the Climax target in September or October, utilizing its internal drilling division.

Operations: The Company has expanded its drilling operations from two to four surface core drills after securing three major contracts expected to deliver strong cash flow through 2026:

Hercules Metals, adjacent to Cuddy Mountain: two rigs for 2025.

IDEX Metals, north of Cuddy Mountain: one core rig plus TerraCore imaging.

Wolfden Resources: one rig, rig management, core logging/cutting, and TerraCore imaging – a full turnkey program.

Speed Goat Phase II Drill Results

Scout has successfully completed a 2,000-meter, 6-hole core drilling program at its Speed Goat porphyry Au-Cu (Ag) project in Nevada. This Phase II program follows up on initial successful drilling conducted in 2022 by the team during their tenure at EMX Royalty Corp. (“EMX”), prior to spinning out as Scout. That work intercepted robust porphyry Au-Cu-Ag mineralization beginning at surface – significant results are outlined above in the summary section, and in Table 1.

The Speed Goat project is located within the prolific Battle Mountain mining region of north-central Nevada (Figure 1). This district hosts multiple producing gold (Marigold, SSR Mining) and gold-copper mines (Phoenix Complex, Nevada Gold Mines). The project was initially identified and acquired through staking by the Scout team, formerly as EMX employees, in 2021.

Historical exploration is uncertain; however, previous drilling and exploration work is reported to have taken place in the mid-1990s between Pittston Nevada Gold Co. and Newmont Mining Corp. To date, Scout has relied solely on its own drill results to guide its exploration efforts. The outcropping mineralization at Speed Goat, combined with strong reconnaissance geochemistry, proved compelling even without historic drill data available in 2022, prompting the completion of an initial 862-meter Phase I core program. Notable intercepts from Phase I, beginning at surface, included 284.0m @ 0.34 g/t Au, 1.87 g/t Ag, and 0.10% Cu (0.46 g/t AuEQ or 0.43% CuEQ; with a higher-grade interval of 16.9 meters at 0.76 g/t Au, 1.24 g/t Ag, and 0.20% Cu (0.96 g/t AuEQ or 0.82% CuEQ.

The Phase II program outlined here was designed to test previously drilled holes, both at depth and along strike, to better understand the scale potential. Strong porphyry Au-Cu-Ag mineralization was intercepted in all step-outs, indicating significant tonnage potential starting at surface.

Figure 1: Speed Goat Property Map

Geologic Mapping: During 2025, the Scout technical team remapped the Speed Goat project area using digital “Anaconda-style” outcrop mapping to document lithology, structure, alteration, and mineralization in detail (Figure 2). The primary goal was to assess the time-space relationships between the host Jurassic igneous units, the later Eocene (?) mineralized porphyry dikes, and the outcropping mineralization, in order to better understand the tonnage potential. Figure 3 displays results of this work, which shows widespread early potassic and later sericitic alteration, with zones of >10 quartz-pyrrhotite-chalcopyrite veins per meter documented across an ~1 square kilometer area associated with a series of porphyry dikes. Several high-priority new targets were identified, particularly when considered in context with insights gained during this latest drill program (Figure 4 and Figure 5). Figure 6 through Figure 9 are drill sections of Holes SG25-04 to 06 displaying Au and Cu grades. Refer to the following links for drill sections of Ag for Holes SG25-04, SG25-05 and SG25-06.

Figure 2: New Geology and Alteration Map

Figure 3: Quartz Veins Per Meter in Latest Drilling and Outcrop

Figure 4: Long Section Showing AuEQ Grades in 2022 and 2025 Drill Programs

Figure 5: Long Section Showing CuEQ Grades in 2022 and 2025 Drill Programs

Table 1: Speed Goat Phase II Drilling Intercepts (click on hole IDs to view Intellicore photos, mineralogy, and assays)

Table 1: Speed Goat Phase II Drilling Intercepts (click on hole IDs to view Intellicore photos, mineralogy, and assays) SG25-06: The Phase II drill program successfully extended mineralization both along strike and at depth, while also identifying a higher-grade Au-Cu-Ag zone that warrants follow-up. Hole SG25-06 was the last and most significant of this program, which drilled beneath the best channel samples. The entire 357.5m hole assayed 0.35 g/t Au, 0.11% Cu, 1.66 g/t Ag (0.46 g/t AuEQ; 0.52% CuEQ). This included a higher-grade interval of 38.9m (from 149.2-188.1m) @ 1.02 g/t Au, 0.27% Cu, 2.25 g/t Ag (1.29 g/t AuEQ; 1.44% CuEQ) within 164.8m (from 23.23-188.1m) @ 0.51 g/t Au, 0.15% Cu, 1.98 g/t Ag (0.67 g/t AuEQ; 0.75% CuEQ). The hole ended in strong mineralization and was terminated at the Nevada Gold Mines property boundary to the northeast.

Figure 6: Drill Section for SG25-05 and 06 Showing Au Grades in Core

Figure 7: Drill Section for SG25-05 and 06 Showing Cu Grades in Core

Figure 8: Drill Section for SG25-04 Showing Au Grades in Core

Figure 9: Drill Section for SG25-04 Showing Cu Grades in Core

SG25-04 and 05: Both holes demonstrated that Au-Cu-Ag grades are largely continuous across ~400m of outcropping mineralization. SG25-04 was drilled at -60 degrees beneath the previous hole SG-22-02 (-45 degrees). This hole successfully showed vertical continuity of mineralization over the 483m hole length (~420m true depth), without exiting potassic alteration or mineralized Au-Cu-Ag veins. The hole was terminated because vein dips had shallowed and the inclination had steepened moderately to where the hole was nearly parallel to the quartz vein sets, making it no longer representative. There remains potential to expand mineralization beyond 420m with different hole orientations beneath SG25-04 and steeper drilling beneath SG25-06.

SG25-01 to 03: The Company drilled three holes from one drill pad to test for southeast extensions of the porphyry Au-Cu-Ag system under post-mineral gravel cover in the hanging wall of a post-mineral fault. Bedrock was encountered ~25 meters below gravel, with all holes intercepting strong zones of porphyry-style sericitic alteration and local zones of >0.5 g/t Au up to 1.23 g/t Au over 0.94m and 0.05% Cu over 0.81m. These results suggest upper portions of a porphyry system are preserved, and the pediment area holds potential for additional porphyry Au-Cu-Ag mineralization. Further drilling will be necessary to vector into higher-temperature and potentially higher-grade zones of the porphyry system(s) in the pediment. Refer to the following link for drill sections of SG25-01 to 03 showing Au, Cu and Ag grades in core.

Figure 10: Core photos from SG25-04, 05, and 06 highlighting key porphyry mineralization styles and associated grades with sheeted to stockwork quartz-pyrrhotite-chalcopyrite veins cutting Jurassic quartz monzonite.

Economic Potential and Next Steps: Vein mineralization at Speed Goat is primarily pyrrhotite-chalcopyrite with minor molybdenite in potassic alteration, and later pyrite-dominant mineralization associated with sericitic alteration. This is directly analogous to intrusion-hosted Eocene porphyry mineralization at similar Au-Cu-Ag grades, processed at the Phoenix Mining Complex, ~25km southeast, using standard gravity, flotation, and carbon-in-leach methods. Although metallurgical work at Speed Goat has not yet been completed, the simple sulfide composition and uniform geology suggest a straightforward processing approach.

The Speed Goat project lies within Nevada’s “checkerboard” land, where alternating one-mile by one-mile sections are either BLM or private land, largely owned by Nevada Gold Mines. Thanks to its fortuitous surface and mineral rights history, Speed Goat connects with BLM land over two sections (Figure 1), forming a contiguous land position containing >95% of the known outcropping Au-Cu-Ag mineralization. The site offers easy road access, favorable topography for open-pit mining, and high-voltage power lines across the project in a major mining region. These advantages position Speed Goat for aggressive advancement to demonstrate significant scale and grade potential for porphyry Au-Cu-Ag mineralization.

Exploration and Permitting Updates

Scout is advancing earlier-stage projects and generating near-term cash flow through drilling while awaiting final U.S. Forest Service permits for a 10,000-meter drill program at the Cuddy Mountain project, expected still for 2025. Upon receipt of the permits, the Company plans to mobilize drill rigs to Cuddy Mountain for the 12-month permit period, including drilling at the Railroad targets located on private land.

As part of a collaborative initiative, Scout and Hercules Metals completed a 120 km² district-scale MT–NSIP geophysical survey across the Cuddy Mountain and Hercules properties. The survey was conducted by Moombarriga Geoscience, a global leader in deep-sensing geophysical methods. Scout helped Moombarriga expand to the U.S.A. in 2024 when the firm completed a 3D-IP survey at Cuddy Mountain. This MT-NSIP survey enables structural interpretation to depths of up to six kilometers — an order of magnitude deeper than previous techniques — and is expected to significantly enhance targeting and porphyry discovery potential across the region.

Scout’s in-house exploration team is now focused on advancing gold and copper targets across its Idaho portfolio — including the Muldoon, Independence, Moose Ridge, and Century projects — toward drill-ready status for 2026 and beyond.

External Revenue Generating Contracts

Scout expanded from two to four surface core drills through three new contracts via its wholly owned drilling division, Scout Drilling LLC. Current operations include two rigs at Hercules Metals, one at IDEX Metals, and a fourth in western Nevada with Wolfden Resources. The agreements with IDEX and Wolfden include TerraCore hyperspectral imaging (see May 9, 2024 news release). Scout is also overseeing program management, core logging and cutting for Wolfden. These contracts strengthen Scout’s financial profile position as a major cash-flow-generative operator. They also highlight increasing demand for its integrated drilling and technical services, supporting continued advancement of its internal exploration portfolio without significant shareholder dilution.

Building Long-Term Value with a Vertically Integrated Model

Scout’s unique positioning as a vertically integrated exploration and drilling company with the ability to offer technical services, enables long-term value creation (Figure 11):

Cash Flow Generation – Three active drilling contracts with four drills provide steady cash flow into 2026.

Exploration Leverage – Ongoing cash flow allows Scout to advance its own projects independently of equity markets, reducing shareholder dilution.

Technical Depth – Stable finances support a robust internal technical team for advancing drilling and exploration programs for Scout and partners.

Strategic Visibility – Partnerships with Hercules Metals, IDEX Metals, and Wolfden Resources enhances Scout’s profile and provide insight on emerging mineral belts.

Figure 11: Scout Discoveries Vertically Integrated Model Venn Diagram

With a sustained balance of external contracts providing significant cash flow generation and a project pipeline moving towards discovery with compelling porphyry Au-Cu-Ag drill results at Speed Goat, Scout is well-positioned to deliver meaningful catalysts with a strong balance sheet in the second half of 2025 and beyond.

Curtis Johnson, President & CEO commented: “We are highly encouraged by the results to date at Speed Goat and will continue to advance the project as a key goal of the Company, in conjunction with Cuddy Mountain and other high priority targets in our portfolio. First and foremost, Scout is a discovery-focused company and will always be so – as genuine economic discovery is what drives value creation in this industry. In pursuit of this, Scout’s vision is to transform exploration by bringing the discovery process in-house — reducing costs, increasing efficiency, and building a sustainable, profitable business. Our goal is to combine external contracts as described here with discovery upside on our portfolio through earn-in joint venture agreements – whereby Scout is both the underlying project owner and technical services provider. This is a fully aligned partnership structure where Scout provides drilling and technical services at lower cost to earn-in partners, while profitably advancing our large portfolio through discovery. The more efficient we are in advancing our projects for partners, the more work is done per dollar and the better odds we have of discovery. We are motivated to demonstrate this model and continue to advance partnership discussions with multiple parties across our portfolio.”

About Scout

Scout Discoveries Corp., headquartered in Coeur d’Alene, Idaho, is a private U.S. mineral exploration company with rights to fourteen separate precious and base metal projects in the western U.S.A., comprising one of the largest unpatented claim holdings in the region, totaling over 50,000 acres. Scout’s vision is to bring the full discovery process in-house from idea generation through resource drilling, lowering costs and increasing efficiency. With this model, the Company can rapidly advance its project portfolio through discovery by leveraging its four internal core drill rigs and experienced technical teams. For further information: https://www.scoutdiscoveries.com/

Download PDF

Forward-looking Statements

Certain statements in this news release are forward-looking and involve a number of risks and uncertainties. Such forward-looking statements are within the meaning of that term in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are not comprised of historical facts. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. Forward-looking statements may be identified by such terms as “believes”, “anticipates”, “expects”, “estimates”, “may”, “could”, “would”, “will”, or “plan”. Since forward-looking statements are based on assumptions and address future events and conditions, by their very nature they involve inherent risks and uncertainties. Although these statements are based on information currently available to the Company, the Company provides no assurance that actual results will meet management’s expectations. Risks, uncertainties and other factors involved with forward-looking information could cause actual events, results, performance, prospects and opportunities to differ materially from those expressed or implied by such forward-looking information. Factors that could cause actual results to differ materially from such forward-looking information include, but are not limited to those risks set out in the Company’s public documents filed on EDGAR. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law. No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein.

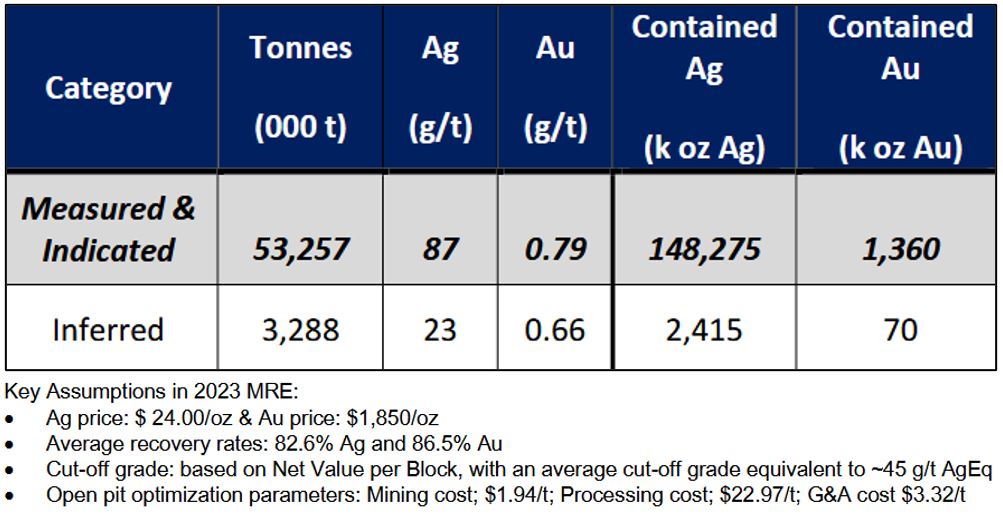

Vancouver, British Columbia–(Newsfile Corp. – August 20, 2025) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (the “Company” or “EMX”) congratulates AbraSilver Resource Corp. (“AbraSilver”) on its recent updated Diablillos mineral resource estimate (“MRE”) that increased total open pit constrained, oxide mineral resources to 199 million ounces of contained silver (+34%) and 1.72 million ounces of contained gold (+27%) in the measured and indicated (“MI”) categories.1,2 AbraSilver is also further enhancing project economics with ongoing drilling, advancing other priority initiatives (e.g., engineering optimization, investment incentives, among others), and is expected to receive EIA approval in the latter half of 2025 and on schedule to deliver a definitive feasibility study (“DFS”) for the Project in Q1 2026. EMX retains a 1% NSR royalty on the Diablillos Project, and all known mineralization occurs within EMX’s royalty ground.

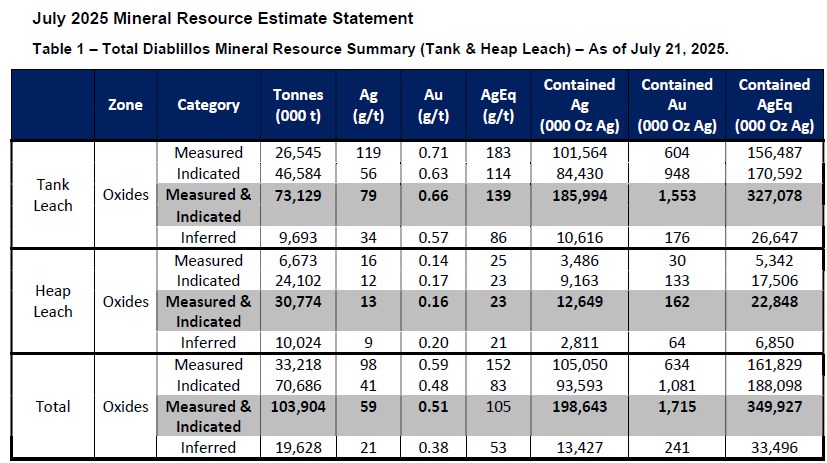

The updated Diablillos MRE reports tank leach resources, which previously was the sole metallurgical processing assumption for the Project, as well as contributions from a maiden heap leach MRE. The additional heap leach resources represent a milestone advancement in converting near surface and peripheral lower grade “waste” material within the constraining open pit configuration to mineralization potentially recoverable via a low-cost processing route. AbraSilver reported total (i.e., tank and heap leach) oxide MI resources as 104 Mtonnes averaging 59 g/t silver and 0.51 g/t gold. The tank leach MI resources account for approximately 70% of the tonnes and over 90% of the contained silver and gold, with the heap leach resources contributing the balance which provides the potential to reduce the strip ratio and enhance project economics.

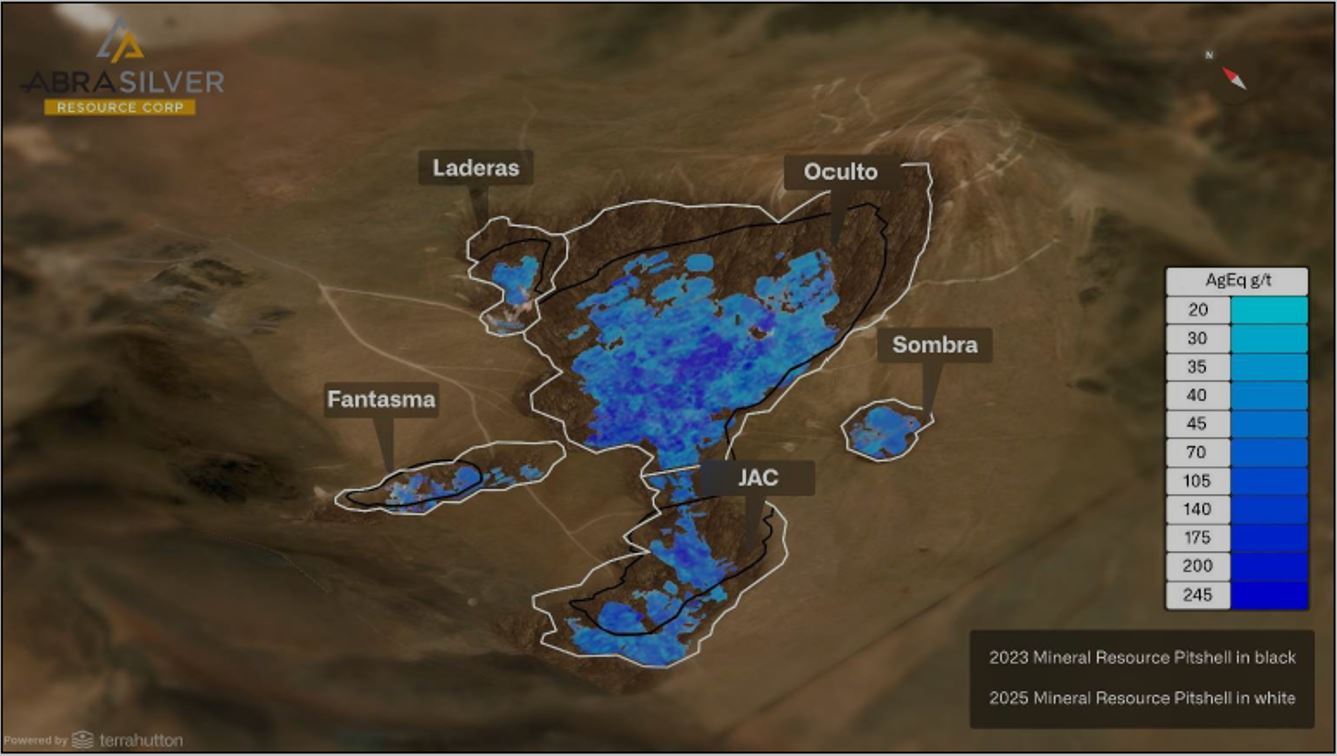

There were significant MI increases across all five resource deposits (i.e., Oculto, JAC, Fantasma, Laderas and Sombra) (see Figure 1 reference map), with the largest tonnage and contained metal increases driven by the JAC deposit, which is characterized by high-grade, near-surface silver-gold mineralization, as well as the Oculto deposit. The Sombra deposit, a recent discovery immediately south of Oculto and JAC, represents a first-time addition to the Project MRE totals.

There is significant district scale exploration upside at Diablillos with an ongoing Phase V 20,000 meter drill program scheduled for completion by early 2026. This program includes step-out drilling at Oculto East, JAC, and Sombra, as well as exploration drilling at the Cerro Viejo and Cerro Blanco porphyry targets.

EMX congratulates AbraSilver for its success in rapidly building value at the Diablillos royalty property. In addition to the significant increases in silver-gold mineral resources via drilling and metallurgical advancements, AbraSilver is currently evaluating other initiatives to further enhance project economics as inputs to the H1 2026 DFS (e.g., connecting to national grid for power, upgrading the fleet size, outsourcing waste movement, and optimizing TSF design to co-locate waste with tailings).3 Moreover, Diablillos is eligible for Argentina’s Incentive Regime for Large Investments (i.e., RIGI), which includes lower tax rates, elimination of export duties, and accelerated depreciation; an investment decision by Q2 2027 is required to fully qualify. Clearly, AbraSilver is on a fast track in advancing Diablillos to a production decision, and thereby unlocking the value of EMX’s royalty interest.

Comments on the Updated MRE. The updated Diablillos MRE reports total (i.e., tank and heap leach) measured resources of 33,218 Ktonnes @ 98 g/t Ag (105,050 Koz contained) and 0.59 g/t Au (634 Koz contained) and indicated resources of 70,686 Ktonnes @ 41 g/t Ag (93,593 Koz contained) and 0.48 g/t Au (1,081 Koz contained). In addition, the updated MRE includes total inferred resources of 19,628 Ktonnes @ 21 g/t Ag (13,427 Koz contained) and 0.38 g/t Au (241 Koz contained).

Comments on the December 2024 PFS. AbraSilver’s PFS study updated in December 2024 outlined an average 14 year life of mine with annual production of 7.6 Moz of silver and 72 Koz of gold yielding an NPV(5) of US$747 million, 28% IRR, and a two year payback using base case prices of $25.50/oz silver and $2,050/oz gold. Importantly, the PFS production profile over the first five years of full mine production averages 11.7 Moz silver and 59 Koz gold which underlines the Project’s early-stage potential for strong cash-flow generation and corresponding royalty payments to EMX. AbraSilver’s ongoing initiatives and sustained silver and gold bull market prices suggest significant additional Project upside.

About the Diablillos Silver-Gold Royalty Property. Diablillos is a high sulfidation silver-gold project located in the Puna region of Salta Province, Argentina. There are multiple mineralized zones in a district scale area covered by EMX’s uncapped 1% NSR royalty ground. Of note, in April of this year the Company received an early final property payment from AbraSilver totaling US$6.85 million.

Michael P. Sheehan, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release

Forward-Looking Statements This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter June 30, 2025 (the “MD&A”), and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2024, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedarplus.ca and on the SEC’s EDGAR website at www.sec.gov.

Figure 1. Diablillos Project Plan View of Mineral Resource Estimate (taken from Figure 2, AbraSilver news release dated July 29, 2025).

1 See AbraSilver news release dated July 29, 2025 and Appendix 1 of this news release 2 Increases referenced to the November 2023 MRE 3 See AbraSilver “August 2025” Corporate Presentation 4 See AbraSilver news release dated December 3, 2024

Vancouver, British Columbia–(Newsfile Corp. – August 19, 2025) – Questcorp Mining Inc. (CSE: QQQ) (OTCQB: QQCMF) (FSE: D910) (the “Company” or “Questcorp“) is pleased to announce they have completed 25% of the planned drilling program on its La Union Project in northwest Sonora, Mexico. This work is being carried out by property vendor and operator Riverside Resources Inc. (TSXV: RRI).

Highlights

The Company has completed 300 metres of the planned drill program of 1200 to 1500m.

Drilling to test the carbonate-hosted replacement deposit (CRD) style of mineralization, with gold associated with mantos, chimneys, and along structural zones.

Angled drill holes are aimed at cutting perpendicular to stratigraphic targets and some structural targets which is typical in CRD systems

Structural features may have served as mineralizing conduits and are key targets in the current drill program.

Questcorp is capitalizing on the recent exploration work over the past three months by Riverside that improved the understanding of the structural geology and stratigraphy that is guiding current exploration efforts at La Union. The exploration target focus is for a large potential gold discovery that expands from previous smaller scale mine operations on the property. The drill program will begin to test the new concepts and expand past previous mining.

Saf Dhillon, President & CEO states, “Questcorp is pleased with the progress being made at this first ever drill program at La Union. The Riverside team has been able to work throughout these hot summers months to enable the successful completion of this Maiden drill.

Earlier this year, Questcorp entered into a definitive option agreement with Riverside’s wholly owned subsidiary, RRM Exploracion, S.A.P.I. DE C.V. to acquire a 100% interest in the La Union Project. As part of the agreement, Questcorp issued shares to Riverside, making Riverside a shareholder and aligning both parties’ interests in the Project’s success. With funding provided by Questcorp, an initial C$1,000,000 exploration program is now underway. This marks the first phase of a larger, C$5,500,000 work commitment, contingent on exploration results and Questcorp’s continued participation.

The Drill Program Targets include more than four different areas, beginning with this early-stage stratigraphic and orientation phase of drilling exploration aimed at evaluating the scale of alteration and indications of a mineralized system. This will be the first drilling ever conducted on most of the targets, despite past mining having occurred in the majority of these areas. The initial program will consist of one to three holes per area, primarily for orientation purposes. Follow-up drilling is planned and can be expanded based on initial results, which will help verify the stratigraphy, lithologies, and structural features allowing for improved modeling and next-stage discovery targeting. The four areas are listed below:

Union Main MineArea – The program will use angled drill holes to test limestone and other carbonate stratigraphic hosts within the Clemente Formation, with the potential to reach the underlying Caborca Formation. These units are considered the primary hosts for replacement-style mineralization.

North Union Mine Area – The initial focus of the program will be on testing structural interpretations. Additional drilling is anticipated following this first phase, as results will help guide future drill testing of areas with past mining activity and various structural orientations.

Cobre MineArea – The Clemente Formation is the primary host unit, and structural features combined with areas of past mining provide multiple target zones. Drilling will begin with an initial stratigraphic test hole to help orient around the thickness of the host unit and extend into the lower Caborca Formation, which is also a favorable host for CRD-style mineralization.

Central UnionArea – Structural targets, as possible mineralization feeder zones, are a key focus in this past mining manto area. There are extensive additional target zones in the area, and this initial orientation drilling will provide vectoring for the next stage of drilling and further study of the Clemente Formation, and possibly into the Caborca Formation as currently interpreted.

General Overview of La Union Project

The Project is summarized in a recently published NI 43-101 Technical Report available under Questcorp’s SEDAR+ profile (www.sedarplus.ca). Riverside initially acquired the Project and subsequently consolidated additional inlier mineral claims, building a strong land position. Riverside then advanced the Project through surface access agreements and drill permitting, making it a turn-key exploration opportunity for Questcorp.

The Project was originally identified through Riverside’s exploration work in the western Sonora Gold Belt, conducted in collaboration with AngloGold Ashanti Limited, Centerra Gold Inc., and Hochschild Mining Plc. Earlier research by Riverside Founder John-Mark Staude also contributed to recognizing the district’s potential. Initial work by members of the Riverside team, drawing on more than two decades of geological compilation and analysis, further confirmed the region as highly prospective.

At the Project, historical mining by the Penoles Mining Company targeted chimney and manto-style replacement bodies within the upper oxide zones. As a result, the underlying sulfide zones represent immediate and compelling drill targets for further exploration.

At the La Union Project, immediate drill targets offer the potential for significant-scale discoveries. La Union is well positioned for near-term exploration success, with targets that include both oxide and deeper sulfide mineralization.

The La Union Project

The La Union Project is a carbonate replacement deposit (“CRD”) project hosted by Neoproterozoic sedimentary rocks (limestones, dolomites, and siliciclastic sediments) overlying crystalline Paleoproterozoic rocks of the Caborca Terrane. The structural setting features high-angle normal faults and low-to-medium-angle thrust faults that sometimes served as mineralization conduits. Mineralization occurs as polymetallic veins, replacement zones (mantos, chimneys), and shear zones with high-grade metal content, as shown in highlight grades of 59.4 grams per metric tonne (g/t) gold, 833 g/t silver, 11% zinc, 5.5% lead, 2.2% copper, along with significant hematite and manganese oxides, consistent with a CRD model (see the technical report entitled “NI 43-101 Technical Report on the Union Project, State of Sonora, Mexico” dated effective May 6, 2025 available under Questcorp’s SEDAR+ profile). These targets also demonstrate intriguing potential for large gold discoveries potentially above an even larger porphyry Cu district potential as the Company’s target concept at this time.

Questcorp cautions investors that grab samples are selective by nature and not necessarily indicative of similar mineralization on the property.

The technical and scientific information in this news release has been reviewed and approved by R. Tim Henneberry, P. Geo (BC), a director of the Company and a “qualified person” under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Questcorp Mining Inc.

Questcorp Mining Inc. is engaged in the business of the acquisition and exploration of mineral properties in North America, with the objective of locating and developing economic precious and base metals properties of merit. The Company holds an option to acquire an undivided 100% interest in and to mineral claims totaling 1,168.09 hectares comprising the North Island Copper Property, on Vancouver Island, British Columbia, subject to a royalty obligation. The Company also holds an option to acquire an undivided 100% interest in and to mineral claims totaling 2,520.2 hectares comprising the La Union Project located in Sonora, Mexico, subject to a royalty obligation.

This news release includes certain “forward-looking statements” under applicable Canadian securities legislation. Forward-looking statements include, but are not limited to, statements with respect to Riverside’s arrangements with geophysical contractors to undertake orientation surveys and follow up detailed survey to confirm and enhance the drill targets. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable, are subject to known and unknown risks, uncertainties, and other factors which may cause the actual results and future events to differ materially from those expressed or implied by such forward-looking statements. Such factors include but are not limited to: the ability of Riverside to secure geophysical contractors to undertake orientation surveys and follow up detailed survey to confirm and enhance the drill targets as contemplated or at all, general business, economic, competitive, political and social uncertainties, uncertain capital markets; and delay or failure to receive board or regulatory approvals. There can be no assurance that the geophysical surveys will be completed as contemplated or at all and that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Explore the Union Project with Riverside Resources! ⛏️ The team is on-site in Sonora, Mexico, showcasing their gold exploration efforts and the potential of the old Union Mine. 🗺️ Check out the drilling process, core samples, and drone footage of the site. 👷♂️ 🔗 https://youtu.be/_O6AKIkW_1c

Vancouver, British Columbia–(Newsfile Corp. – August 11, 2025) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (the “Company” or “EMX”) is pleased to report results for the six months ended June 30, 2025 (in U.S. dollars unless otherwise noted). EMX delivered revenue and other income of $14.7 million, adjusted royalty revenue[1] of $19.0 million and adjusted EBITDA1 of $12.1 million.

Dave Cole, EMX CEO, commented, “For the first half of 2025 we achieved growth in adjusted royalty revenue and adjusted EBITDA, and strengthened our financial position through disciplined capital management and opportunistic share buybacks. With rising commodity prices and growing revenue, we have increased our 2025 revenue guidance as we continue our momentum into the second half of 2025.”

Q2 2025 Financial Highlights

Adjusted royalty revenue1 of $8.2 million, similar to comparative quarter;

Adjusted cash flows from operating activities1 of $9.0 million, up 570% from the comparative quarter primarily due to the collection of $6.9 million and $1.5 million in deferred payments from AbraSilver Resources and Aftermath Silver, respectively;

Adjusted EBITDA1 of $4.9 million, similar to comparative quarter, demonstrating strong cash flow conversion; and

Cash and cash equivalents as of June 30, 2025 of $17.2 million and working capital1 of $30.2 million, demonstrating financial flexibility for growth.

Summary of Financial Highlights for the Period Ended June 30, 2025 and 2024:

Three months ended June 30,

Six months ended June 30,

(In thousands)

2025

2024

2025

2024

Statement of Income (Loss)

Revenue and other income

$

6,239

$

6,005

$

14,661

$

12,245

General and administrative costs

(1,616

)

(1,694

)

(3,786

)

(3,842

)

Royalty generation and project evaluation costs, net

(2,176

)

(2,907

)

(4,678

)

(5,841

)

Net income (loss)

$

642

$

(4,022

)

$

1,902

$

(6,249

)

Statement of Cash Flows

Cash flows from operating activities

$

6,892

$

(514

)

$

8,181

$

513

Non-IFRS Financial Measures1

Adjusted revenue and other income

$

8,686

$

8,758

$

20,114

$

17,051

Adjusted royalty revenue

$

8,214

$

7,836

$

18,965

$

15,493

Adjusted cash flows from operating activities

$

8,978

$

1,341

$

11,884

$

4,002

EBITDA

$

3,065

$

(981

)

$

7,957

$

268

Adjusted EBITDA

$

4,949

$

4,639

$

12,050

$

7,862

GEOs sold

2,505

3,352

6,261

7,047

Key Strategic Developments

During the three months ended June 30, 2025, and the period subsequent to quarter end EMX completed several key transactions that demonstrate our strategy of incremental revenue growth and disciplined capital management. These key developments include:

In April 2025, the Company made a $10.0 million early repayment towards the Franco-Nevada credit facility, decreasing the principal outstanding from $35.0 million to $25.0 million;

In April 2025, the Company received an early Diablillos property payment from AbraSilver Resource Corp. totaling $6.9 million;

In June 2025 the Company received an early Berenguela property payment from Aftermath Silver Ltd. totaling $1.5 million;

The Company announced the sale of its Nordic operational platform to First Nordic Metals Corporation, a current partner of EMX and operator on multiple EMX royalty properties in Sweden and Finland. This strategic divestment included EMX’s infrastructure, exploration equipment and employees in the Nordic countries;

The Company executed an exploration alliance agreement in the country of Morocco with Avesoro Morocco Limited (“Avesoro”), a wholly owned subsidiary of Avesoro Holdings LTD, a privately owned, West Africa-focused mid-tier gold producer. In Morocco, EMX and Avesoro will work together to advance a portfolio of exploration projects that EMX has assembled and will cooperatively explore for new opportunities. Avesoro will fully fund the alliance activities, which will include the advancement of certain projects in the EMX Moroccan portfolio, as well as new projects identified by the alliance for acquisition; and

The Company commenced a new NCIB program during the quarter which allows for the repurchase and cancellation of 5,440,027 common shares over a 12-month period. We repurchased and cancelled 1,202,168 shares during the quarter for a total cost of $2.6 million. Subsequent to the end of the period, the Company repurchased 400,929 common shares under the new NCIB for a total cost of $1.2 million.

Outlook

Updated 2025 Guidance

Please see our “Forward-Looking Statements” below for more details on our guidance.

Updated 2025 Guidance[2]

Original 2025 Guidance[3]

GEO sales[4]

10,500 to 12,000

10,000 to 12,000

Adjusted royalty revenue3

$30,000,000 to $35,000,000

$26,000,000 to $32,000,000

Option and other property income

$1,000,000 to $2,000,000

$1,000,000 to $2,000,000

Based on the Company’s existing royalties and information available from its counterparties, we now expect GEO sales3 to range from 10,500 to 12,000 GEOs and adjusted royalty revenue3 to range from $30,000,000 to $35,000,000 in 2025. The noted increase in expected adjusted royalty revenue compared to the original guidance is due to the significant increases in metal prices to date in 2025.

Guidance is based on public forecasts, other disclosure by the owners and operators of our assets, historical performance and management’s understanding of the underlying producing assets. Additionally, the Company may receive information from the owners and operators of the properties, which the Company is not permitted to disclose to the public pursuant to the underlying agreement or the information has not been prepared in accordance with Canadian disclosure standards, including National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”).

Capital Management

For 2025, EMX continues to believe that capital management is critical to the success of the business and therefore maintain the following capital allocation goals for 2025:

Approximately 20% decrease in operating expenditures when compared to 2024, primarily resulting from a decrease in generative expenditures, weighted toward the second half of 2025;

Continued return of capital through our renewed Normal-Course Issuer Bid program in 2025;

Implementation of a measured and consistent debt repayment strategy; and

Evaluation of a potential revolving credit facility available to EMX to fund royalty acquisitions.

Portfolio Growth

The drivers for near and long term growth in cash flow will come from the material producing assets at Caserones in Chile and Timok in Serbia. At Caserones, Lundin Mining Corporation (“Lundin”) has initiated an exploration program which is intended to expand mineral resources and mineral reserves while at the same time looking to increase throughput at the plant. At Timok, Zijin Mining Group Co. (“Zijin”) continues to develop the Lower Zone copper porphyry block cave project while continuing to produce from the high-grade Upper Zone. Zijin also announced the recently discovered high-grade Malka Golaja Copper-Gold Deposit south of the Cukaru Peki mine and within EMX’s royalty footprint. Analysis of recent satellite imagery over the Brestovac license, which contains the Cukaru Peki Mine and is covered by EMX’s royalty, shows substantial development of new drill pads with numerous drill rigs visible in the images in the southeast corner of the license where Malka Golaja is located.

We anticipate the recently announced $10,000,000 acquisition of a royalty on the Chapi Copper Mine property in Peru will begin contributing to royalty revenue in 2026. We are excited by the addition of a high-quality copper royalty to the portfolio that has excellent upside development and exploration potential located in the prolific Paleocene-Eocene copper-molybdenum porphyry belt of Southern Peru.

AbraSilver Resource Corp. continues to advance Diablillos in Argentina, announced that it expects to complete its definitive feasibility study by Q1 2026 and make a construction decision in the second half of 2026 and released an updated MRE in Q2 2025.

At the Vittangi Graphite development project, an appeals review process was recently concluded for the issuance of an Exploitation Concession, a key step in the mine permitting process in Sweden. Talga Group now has all major permits in force for their Nunasvaara South Mine, which is part of Europe’s largest and highest grade JORC classified natural graphite resource. At the Viscaria copper-iron-silver development project in Sweden, the Supreme Court of Sweden announced in April 2025 it will not grant leave to appeal Viscaria’s environmental permit. This decision means that Viscaria’s environmental permit can no longer be appealed and thus gains legal force. Viscaria now has all permits in place to start the construction of the industrial area including the enrichment plant, and to start operations in the mine. These developments are all examples of the upside optionality that exists throughout EMX’s global royalty portfolio.

EMX is well positioned to identify and pursue new royalty and investment opportunities, while continuing to grow a pipeline of royalty generation properties for partnership. As the Company continues to generate revenues from its producing royalty assets as well as from other option, advance royalty and pre-production payments across its global asset portfolio, various opportunities for capital redeployment will be evaluated. Such opportunities may include the direct acquisition of royalties, continued organic generation of royalties through partner funded projects and select strategic investments.

Results for the Three Months Ended June 30, 2025

In Q2 2025, the Company recognized $8.7 million and $8.2 million in adjusted revenue and other income1 and adjusted royalty revenue[5], respectively, which represented a 1% decrease and a 5% increase, respectively, compared to Q2 2024. The noted decrease in GEOs compared to 2024 is due to EMX’s heavy exposure to copper-based assets, specifically, Caserones and Timok. With copper prices being relatively stable, a significant increase in gold prices will have a negative impact on the GEOs of a copper-based asset.

The following table is a summary of GEOs1 sold and adjusted royalty revenue1 for the three months ended June 30, 2025 and 2024:

2025

2024

(In thousands)

GEOs Sold

Revenue (in thousands)

GEOs Sold

Revenue (in thousands)

Gediktepe

588

1,928

772

1,806

Caserones

746

$

2,447

1,178

$

2,753

Timok

496

1,625

678

1,586

Leeville

431

1,412

508

1,187

Other Producing Assets

221

725

204

478

Advanced royalty payments

23

77

11

26

Adjusted royalty revenue

2,505

$

8,214

3,352

$

7,836

Results for the Six Months Ended June 30, 2025

In 2025, the Company recognized $20.1 million and $19.0 million in adjusted revenue and other income1 and adjusted royalty revenue1, respectively, which represented a 18% and 22% increase, respectively, compared to 2024. The increase is largely due to a $1.4 million increase in royalty revenue from Gediktepe and a $0.6 million increase in the Company’s share of royalty revenue from Caserones when compared to 2024.

The following table is a summary of GEOs1 sold and adjusted royalty revenue1 for the six months ended June 30, 2025 and 2024:

2025

2024

(In thousands)

GEOs Sold

Revenue (in thousands)

GEOs Sold

Revenue (in thousands)

Gediktepe

2,092

6,233

2,216

4,796

Caserones

1,796

$

5,453

2,168

$

4,806

Timok

1,049

3,208

1,290

2,853

Leeville

748

2,322

925

2,051

Other Producing Assets

511

1,555

336

750

Advanced royalty payments

64

194

113

237

Adjusted royalty revenue

6,261

$

18,965

7,047

$

15,493

Shareholder Information – The Company’s filings for the year are available on SEDAR+ at www.sedarplus.ca, on the U.S. Securities and Exchange Commission’s EDGAR website at www.sec.gov, and on EMX’s website at www.EMXroyalty.com. Financial results were prepared in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board.

About EMX – EMX is a precious, and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release

Forward-Looking Statements

This news release may contain “forward looking information” or “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding the future price of copper, gold and other metals, the estimation of mineral reserves and mineral resources, realization of mineral reserve estimates, the timing and amount of estimated future production, the Company’s growth strategy and expectations regarding the guidance for 2025 and future outlook, including revenue and GEO estimates, anticipated reductions in operating expenditures, repayment of outstanding debt and the timing thereof, the acquisition of additional royalty and royalty generation interests and other investment opportunities, the purchase of securities pursuant to the Company’s NCIB, exploration and development plans at the Company’s royalty properties and the expected timing thereof or other statements that are not statements of fact. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects,” “anticipates,” “believes,” “plans,” “projects,” “estimates,” “assumes,” “intends,” “strategy,” “goals,” “objectives,” “potential,” “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are based on a number of material assumptions, including those listed below, which could prove to be significantly incorrect, including disruption to production at any of the mineral properties in which the Company has a royalty, or other interest; estimated capital costs, operating costs, production and economic returns; estimated metal pricing (including the estimates from theCIBC Global Mining Group’s Consensus Commodity Price Forecasts published on March 3, 2025 and July 1, 2025), metallurgy, mineability, marketability and operating and capital costs, together with other assumptions underlying the Company’s resource and reserve estimates; the expected ability of any of the properties in which the Company holds a royalty, or other interest to develop adequate infrastructure at a reasonable cost; assumptions that all necessary permits and governmental approvals will remain in effect or be obtained as required to operate, develop or explore the various properties in which the Company holds an interest; and the activities on any on the properties in which the Company holds a royalty, or other interest will not be adversely disrupted or impeded by development, operating or regulatory risks or any other government actions.

Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward-looking statements include, amongst others, failure to maintain or receive necessary approvals, changes in business plans and strategies, market conditions, share price, best use of available cash, copper, gold and other commodity price volatility, discrepancies between actual and estimated production, mineral reserves and resources and metallurgical recoveries, mining operational and development risks relating to the parties which produce the gold or other commodity the Company will purchase, regulatory restrictions, activities by governmental authorities (including changes in taxation), currency fluctuations, the global economic climate, dilution, share price volatility and competition.

Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: the impact of general business and economic conditions, the absence of control over mining operations from which the Company will receive royalties from, and risks related to those mining operations, including risks related to international operations, government and environmental regulation, actual results of current exploration activities, conclusions of economic evaluations and changes in project parameters as plans continue to be refined, risks in the marketability of minerals, fluctuations in the price of gold and other commodities, fluctuation in foreign exchange rates and interest rates, stock market volatility, as well as those factors discussed in the Company’s MD&A for the quarter ended June 30, 2025, and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2024, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR+ at www.sedarplus.ca and on the SEC’s EDGAR website at www.sec.gov. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The Company does not undertake to update any forward-looking statements that are contained or incorporated by reference, except in accordance with applicable securities laws.

Future-Oriented Financial Information

This news release may contain future-oriented financial information (“FOFI”) within the meaning of Canadian securities legislation, about prospective results of operations, financial position, GEOs and anticipated royalty payments based on assumptions about future economic conditions and courses of action, which FOFI is not presented in the format of a historical balance sheet, income statement or cash flow statement. The FOFI has been prepared by management to provide an outlook of the Company’s activities and results and has been prepared based on a number of assumptions including the assumptions discussed under the headings above entitled “Outlook” and “Forward-Looking Statements” and assumptions with respect to the future metal prices, the estimation of mineral reserves and resources, realization of mineral reserve estimates and the timing and amount of estimated future production. Management does not have, or may not have had at the relevant date, or other financial assumptions which may have been used to prepare the FOFI or assurance that such operating results will be achieved and, accordingly, the complete financial effects are not, or may not have been at the relevant date of the FOFI, objectively determinable.

Importantly, the FOFI contained in this news release are, or may be, based upon certain additional assumptions that management believes to be reasonable based on the information currently available to management, including, but not limited to, assumptions about: (i) the future pricing of metals, (ii) the future market demand and trends within the jurisdictions in which the Company or the mining operators operate, and (iii) the operating cost and effect on the production of the Company’s royalty partners. The FOFI or financial outlook contained in this news release do not purport to present the Company’s financial condition in accordance with IFRS, and there can be no assurance that the assumptions made in preparing the FOFI will prove accurate. The actual results of operations of the Company and the resulting financial results will likely vary from the amounts set forth in the analysis presented in any such document, and such variation may be material (including due to the occurrence of unforeseen events occurring subsequent to the preparation of the FOFI). The Company and management believe that the FOFI has been prepared on a reasonable basis, reflecting management’s best estimates and judgments as at the applicable date. However, because this information is highly subjective and subject to numerous risks including the risks discussed under the heading above entitled “Forward-Looking Statements” and under the heading “Risk Factors” in the Company’s public disclosures, FOFI or financial outlook within this news release should not be relied on as necessarily indicative of future results.

Non-IFRS Financial Measures

The Company has included certain non-IFRS financial measures in this press release, as discussed below. EMX believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provide investors an improved ability to evaluate the underlying performance of the Company. These non-IFRS financial measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These financial measures do not have any standardized meaning prescribed under IFRS, and therefore may not be comparable to other issuers.

Non-IFRS financial measures are defined in National Instrument 52-112 – Non-GAAP and Other Financial Measures Disclosure (“NI 52-112”) as a financial measure disclosed that (a) depicts the historical or expected future financial performance, financial position or cash flow of an entity, (b) with respect to its composition, excludes an amount that is included in, or includes an amount that is excluded from, the composition of the most directly comparable financial measure disclosed in the primary financial statements of the entity, (c) is not disclosed in the financial statements of the entity, and (d) is not a ratio, fraction, percentage or similar representation. A non-IFRS ratio is defined by NI 52-112 as a financial measure disclosed that (a) is in the form of a ratio, fraction, percentage or similar representation, (b) has a non-IFRS financial measure as one or more of its components, and (c) is not disclosed in the financial statements.

The following table outlines the non-IFRS financial measures, their definitions, the most directly comparable IFRS measures and why the Company use these measures.

Non-IFRS financial measure

Definition

Most directly comparable IFRS measure

Why we use the measure and why it is useful to investors

Adjusted revenue and other income

Defined as revenue and other income including the Company’s share of royalty revenue related to the Company’s effective royalty on Caserones.

Revenue and other income

The Company believes these measures more accurately depict the Company’s revenue related to operations as the adjustment is to account for revenue from a material asset

Adjusted royalty revenue

Defined as royalty revenue including the Company’s share of royalty revenue related to the Company’s effective royalty on Caserones.

Royalty revenue

Adjusted cash flows from operating activities

Defined as cash flows from operating activities plus the cash distributions related to the Company’s effective royalty on Caserones.

Cash flows from operating activities

The Company believes this measure more accurately depicts the Company’s cash flows from operations as the adjustment is to account for cash flows from a material asset.

Gold equivalent ounces (GEOs)

GEOs is a non-IFRS measure that is based on royalty interests and calculated on a quarterly basis by dividing adjusted royalty revenue by the average gold price during such quarter. The gold price is determined based on the LBMA PM fix. For periods longer than one quarter, GEOs are summed for each quarter in the period.

Royalty revenue

The Company uses this measure internally to evaluate our underlying operating performance across the royalty portfolio for the reporting periods presented and to assist with the planning and forecasting of future operating results.

Earnings before interest, taxes, depreciation and amortization (EBITDA) and adjusted EBITDA

EBITDA represents net earnings or loss for the period before income tax expense or recovery, depreciation and amortization, finance costs. Adjusted EBITDA adds all revenue from the Caserones Royalty less any equity income from the equity investment in SLM California (Caserones Royalty holder). Additionally, it removes the effects of items that do not reflect our underlying operating performance and are not necessarily indicative of future operating results. These may include: share based payments expense; unrealized and realized gains and losses on investments; write-downs of assets; impairments or reversals of impairments; foreign exchange gains or losses; and other non-cash or non-recurring expenses or recoveries.

Earnings or loss before income tax

The Company believes EBITDA and adjusted EBITDA are widely used by investors and analysts as useful indicators of our operating performance, our ability to invest in capital expenditures, our ability to incur and service debt and also as a valuation metric.

Working capital

Defined as current assets less current liabilities. Working capital does not include assets held for sale and liabilities associated with assets held for sale

Current assets, current liabilities

The Company believes that working capital is a useful indicator of the Company’s liquidity.

Reconciliation of Adjusted Revenue and Other Income and Adjusted Royalty Revenue:

During the three and six months ended June 30, 2025 and 2024, the Company had the following sources of revenue and other income:

(In thousands of dollars)

Three months ended June 30,

Six months ended June 30,

2025

2024

2025

2024

Royalty revenue

$

5,767

$

5,083

$

13,512

$

10,687

Option and other property income

284

492

587

680

Interest income

188

430

562

878

Total revenue and other income

$

6,239

$

6,005

$

14,661

$

12,245

The following is the reconciliation of adjusted revenue and other income and adjusted royalty revenue:

Three months ended June 30,

Six months ended June 30,

(In thousands of dollars)

2025

2024

2025

2024

Revenue and other income

$

6,239

$

6,005

$

14,661

$

12,245

SLM California royalty revenue

$

5,727

$

6,442

$

12,762

$

11,247

The Company’s ownership %

42.7

42.7

42.7

42.7

The Company’s share of royalty revenue

$

2,447

$

2,753

$

5,453

$

4,806

Adjusted revenue and other income

$

8,686

$

8,758

$

20,114

$

17,051

Royalty revenue

$

5,767

$

5,083

$

13,512

$

10,687

The Company’s share of royalty revenue

2,447

2,753

5,453

4,806

Adjusted royalty revenue

$

8,214

$

7,836

$

18,965

$

15,493

Reconciliation of Adjusted Cash Flows from Operating Activities:

Three months ended June 30,

Six months ended June 30,

(In thousands of dollars)

2025

2024

2025

2024

Cash provided by (used in) operating activities

$

6,892

$

(514

)

$

8,181

$

513

Caserones royalty distributions

2,086

1,855

3,703

3,489

Adjusted cash flows from operating activities

$

8,978

$

1,341

$

11,884

$

4,002

Reconciliation of EBITDA and Adjusted EBITDA:

Three months ended June 30,

Six months ended June 30,

(In thousands of dollars)

2025

2024

2025

2024