Vancouver, British Columbia–(Newsfile Corp. – July 13, 2022) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX”) is pleased to announce the achievement of commercial production for oxide gold mineralization at its flagship Gediktepe royalty property in western Turkey. EMX holds a 10% net smelter return (“NSR”) royalty on oxide gold production at Gediktepe, and operator Polimetal Madencilik Sanayi ve Ticaret A.S. (“Polimetal”), a private Turkish company, has informed EMX that it has produced over 10,000 ounces of gold equivalent[1] ounces, the trigger for commencement of production royalty payments to EMX. In addition to the oxide gold royalty, EMX also owns a 2% NSR royalty on production from an underlying polymetallic copper, zinc, lead and gold deposit that is slated for future development.

The Gediktepe royalty was acquired by EMX as part of its purchase of a portfolio of royalties from SSR Mining Inc. (“SSR”) in 2021 (see EMX News Release dated July 29, 2021). On a go forward basis, Polimetal has informed EMX that it expects to produce between 35,000 and 45,000 ounces of gold per year from Gediktepe (with additional contributions from silver production) while mining the oxide gold cap over the next 3-4 years. The Gediktepe royalty is the subject of a NI 43-101 technical report authored by Dama Engineering with an effective date of February 1, 2022. This technical report has been filed on SEDAR under the Company’s profile and contains historical mining reserve and mineral resource estimates.

In addition to the royalty production payments, EMX is slated to receive cash payments of US$4,000,000 upon the first anniversary of commercial production for oxide gold mineralization, US$3,000,000 on the date that commercial production commences from the underlying sulfide deposit, and US$3,000,00 upon the first anniversary of the commencement of commercial production from the sulfide deposit.

Gediktepe VMS Deposit: The Gediktepe volcanogenic massive sulfide (“VMS”) deposit is a polymetallic system with precious metal, copper, and zinc rich domains. The upper portion of the deposit is oxidized, forming a precious metal-enriched gossanous cap that will be mined first, followed by production from the underlying polymetallic sulfide deposit.

Gediktepe was discovered in 2012 by a joint venture between Alacer Gold Corporation (which merged with SSR in 2020) and Lidya Madencilik Sanayi ve Ticaret A.S. (“Lidya”), a private Turkish company. Alacer Gold Corp later converted its 50% joint venture interest at Gediktepe into the royalty interests now owned by EMX. Polimetal is a wholly owned subsidiary of Lidya and serves as the operator for the Gediktepe project.

More information on the Gediktepe royalty asset can be found at www.EMXroyalty.com.

Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and the TSX Venture Exchange under the symbol EMX, and also trade on the Frankfurt exchange under the symbol “6E9”. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 973-8585 Dave@emxroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@emxroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserve and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential”, “go forward” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended March 31, 2022 (the “MD&A”) and the most recently filed Annual Information Form (the “AIF”) for the year ended December 31, 2021, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

[1] Gold equivalent ounces as referred to in the definition of “Oxide Commercial Production” in the 2019 Gediktepe share purchase agreement between Alacer Gold Madencilik A.S. and Lidya Madencilik.

In the recent Wall Street Journal article “Inflation Surge Earns Monetarism Another Look,” Greg Ip writes that a recent surge in inflation is not likely to bring authorities to reembrace monetarism. According to Ip, money supply had a poor record of predicting US inflation because of conceptual and definitional problems that haven’t gone away.

The head of the monetarist school, the late Milton Friedman, held that inflation is always and everywhere a monetary phenomenon. Friedman and other monetarists believed that the key driving factor for general increases in prices is increases in money supply.

This viewpoint has come under scrutiny since the early 1980s because the correlation between inflation and money supply disappeared. According to Ip in 2020, Alan Detmeister, an economist at UBS Group AG and formerly of the Fed, found inflation’s correlation to M2 since the early 1980s was weak and its correlation to both the monetary base and M1 was negative. Most economists have stopped using money supply as an indicator for inflation since the early 1980s.

Many mainstream economists have attributed the breakdown in the correlation between the money supply and inflation on the unstable velocity of money. What is it? According to the famous equation of exchange, MV = PT, where:

M stands for money,

V stands for the velocity of money,

P stands for the price level, and

T for the volume of transactions.

This equation states that money multiplied by velocity equals the value of transactions. Many economists employ GDP (gross domestic product) instead of PT, thereby concluding that

MV = GDP = P (real GDP).

The equation of exchange appears to offer a wealth of information regarding the state of an economy. For instance, if one were to assume stable velocity, then for a given stock of money one can establish the value of GDP. Furthermore, a given real output and a given stock of money enables us to establish the price level.

For most economists the equation of exchange is regarded as a very useful analytical tool. The debates that economists have are predominantly with respect to the stability of velocity. If velocity is stable, then money is seen as a very powerful tool in tracking the economy. The importance of money as an economic indicator however diminishes once velocity becomes less stable and hence less predictable.

However, an unstable velocity could occur because of an unstable demand for money. Most experts believe that since the early 1980s, innovations in financial markets made money velocity unstable. This in turn made money an unreliable indicator of inflation.

We believe the alleged failure of money as an indicator of inflation emanates from an erroneous definition of inflation and money supply. This failure has nothing to do with an unstable demand for money, and just because people change their demand for money does not imply instability. Because an individual’s goals may change, he might decide that it benefits him to hold less money. Sometime in the future, he might increase his demand for money. What could possibly be wrong with this? The same goes for any other goods and services—demand for them changes all the time.

Defining Inflation

According to Murray Rothbard and Ludwig von Mises, inflation is defined as the increase of the money supply out of “thin air.” Following this definition, one can ascertain that increases in money supply set economic impoverishment in motion by creating an exchange of nothing for something, the so-called counterfeit effect.

General increases in prices are likely to be symptoms of inflation—but not always, however. Note that prices are determined by both real and monetary factors. Consequently, it can occur that if the real factors are “pulling things” in an opposite direction to monetary factors, no visible change in prices is going to take place. If the growth rate of money is 5 percent and the growth rate of goods supply is 1 percent then prices are likely to increase by 4 percent. If, however, the growth rate in goods supply is also 5 percent then no general increase in prices is likely to take place.

If one were to hold that inflation is about increases in prices, then one would conclude that, despite the increase in money supply by 5 percent, inflation is 0 percent. However, if we were to follow the definition that inflation is about increases in the money supply, then we would conclude that inflation is 5 percent, regardless of any movement in prices.

Defining Money Supply

Prior to 1980, it was popular to employ various money supply definitions in the assessment of the changes in the prices of goods and services. The criterion for the selection of a particular definition was its correlation with national income. However, since the early 1980s, correlations between various definitions of money and national income have broken down. Some analysts believe that this breakdown is because of changes in financial markets, making past definitions of money irrelevant.

A definition presents the essence of a particular entity, something no statistical correlation could ever provide. To establish the definition of money we have to explain the origins of the money economy. Money has emerged because barter cannot support the market economy. Money is the general medium of exchange and has evolved from the most marketable commodity. Mises wrote:

There would be an inevitable tendency for the less marketable of the series of goods used as media of exchange to be one by one rejected until at last only a single commodity remained, which was universally employed as a medium of exchange; in a word, money.

Since the general medium of exchange was selected out of a wide range of commodities, the emerged money must be a commodity. Rothbard wrote:

In contrast to directly used consumers’ or producers’ goods, money must have pre-existing prices on which to ground a demand. But the only way this can happen is by beginning with a useful commodity under barter, and then adding demand for a medium to the previous demand for direct use (e.g., for ornaments, in the case of gold).

Through an ongoing selection process, individuals settled on gold as standard money. In today’s monetary system, the core of the money supply is no longer gold, but rather coins and notes issued by the government and central bank that are employed in transactions as goods and services are exchanged for cash. Hence, one trades all other goods and services for money.

Part of the stock of cash is stored through bank deposits. Once someone places money in a bank’s warehouse, he is engaging in a claim transaction, never relinquishing his ownership of the money. Consequently, these deposits, which are labelled demand deposits, are part of money.

This is contrasted with a credit transaction, where the lender relinquishes his claim over the money for the duration of the loan. In a credit transaction, money is transferred from a lender to a borrower, but the overall amount of money in the economy does not change because of the credit transaction.

The introduction of electronic money seems to cast doubt on the definition of money. It would appear that deregulated financial markets generate various forms of new money. Notwithstanding, various forms of electronic money or e-money, like digital currency, do not have a “life of their own.”

Various financial innovations do not generate new forms of money but rather new ways of employing existing money in transactions. Irrespective of these financial innovations, the nature of money does not change. Money is the thing that all other goods and services are traded for. Once the essence of money is established by excluding various credit transactions, one can identify the status of inflation. Changes in prices are not going to be relevant here.

Conclusion

Contrary to popular thinking, inflation is not about increases in the prices of goods and services but about increases in money supply. Following this definition, we can establish that the key damage caused by inflation is economic impoverishment through the exchange of nothing for something. What matters as far as inflation is concerned is not the correlation between money supply and the prices of goods and service but increases in money supply.

Contrary to popular thinking, the essence of money did not change because of various financial innovations. Money is a thing that is employed as a medium of exchange. Furthermore, according to Mises’s regression theorem, the historical link between paper currency and gold is what holds the present monetary system together.

Frank Shostak‘s consulting firm, Applied Austrian School Economics, provides in-depth assessments of financial markets and global economies. Contact: email.

Maurice: Before we deep dive into company specifics, Mr. Sussman, please introduce us to Collective Mining and the exciting opportunity the company presents to shareholders.

Ari Sussman: Collective Mining was born as a result of the COVID lockdowns, so just some background, my previous company was named Continental Gold, which was responsible for discovering and constructing the largest and most modern gold mine in Colombia, which was sold one week before the global lockdowns to a large Chinese mining company named Zijin Mining in March 2020, for a total sum of approximately $2 billion.

Within a month, my core team and I were bored at home like we all were, and said, “Let’s get back to the drawing board.”

And that is how Collective Mining was born.

Just some background on Collective, the name Collective Mining represents our business model. It’s a collective mining model, meaning, yes, we’re going to build, we hope to make a big discovery, and we’re hopefully going to build a mine and, or, sell the company and then reward our shareholders for being involved. But it’s also going to reward the local stakeholders involved in this project. We want to ensure that people living in the area of influence of the project, benefit, learn and grow with us. As we advance, they advance.

Maurice: Well, quite the pedigree of success here. Let’s find out more. Mr. Sussman, take us to the mining-friendly department of Caldas and Colombia, and please acquaint us with the region, potential mineral endowment, and the mining jurisdiction.

Ari Sussman: Let’s start with Colombia and then work our way inwards.

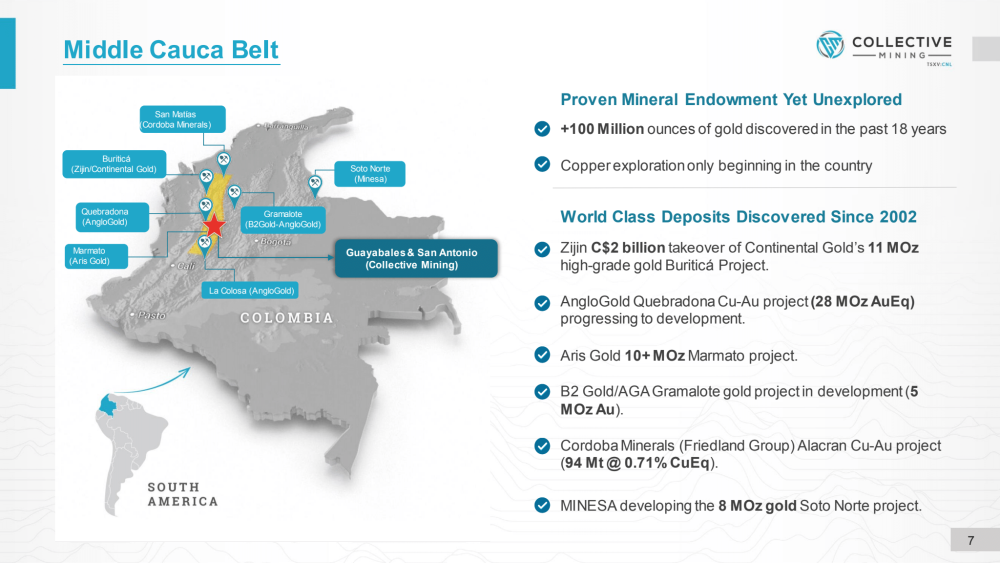

Colombia is a mining jurisdiction, for a country in South America that has the infrastructure in place, and there is no more prospective mining environment to be in. This is the Andes Mountain chain continuation, which starts in Chile and works its way northward, and goes right through Colombia. In theory, all of the large-scale types of discoveries will be made in Colombia that countries like Peru and Chile currently enjoy.

With that said, I don’t want readers to think that Colombia is an early stage country for mining because, it is in terms of discoveries in commodities that we care about (copper, gold, silver, et cetera), but it’s quite mature in the mining of coal.

Colombia is one of the world’s top largest coal producers and most of those mines have been in production for 50 years or more. So as a result, it’s a mature destination for companies to go and make discoveries in.

What I mean by mature destination, is there’s a very strong mining code in place. Royalty rates have been stable for decades on end. There is a mining association, well established in place that represents the mining industry and will lobby the government on behalf of the industry. These are things that we expect to see in countries like the United States where I am, or Canada, but this is also in Colombia. From that perspective, it’s stable and it’s great.

Zooming in a little bit, we are in the department, which you mentioned, named Caldas. I don’t think most people have heard of Caldas. Colombia refers to states as departments, by comparison. But if any of your listeners are coffee experts or coffee aficionados, they will have heard of Caldas because it’s reputed to have the best coffee beans in the world. I, for one, am not the foremost coffee expert. I enjoy the coffee, Maurice, I do, but I don’t have a real comparison, but this is what it’s known for.

What makes Caldas so special, are two things. One is the coffee, and it’s got a large, big industrialized business in Caldas. This entire department is made up of more mom-and-pop-style coffee farms, very specialized and high end and each coffee farm competes with its neighbor to produce a better bean and that leads to excellent quality.

But secondly, there is a mine which is currently operating in Caldas, which happens to be next door to our main property, named Marmato. Why I’m mentioning this now is, that Marmato has helped to create a very mining-friendly environment in Caldas. The reason for that is that Marmato has been producing gold and silver continuously for more than 500 years, believe it or not, and is still producing today. Virtually every person that lives in the department of Caldas has or had, mining in their blood in one way, shape, or form. As a result, there’s a very strong comfort level with mining in this state and it’s an excellent place to be.

Maurice: Collective Mining currently has two projects with district-scale potential. It has identified 11 highly prospective targets in the Cauca belt. Let’s get acquainted with your flagship Guayabales project. Briefly walk us through the genetic and expiration model and share with us what has your team excited.

Ari Sussman: We are operating in the Cauca Belt. This is a well-known metal belt of Colombia, which runs along the Andes mountain chain. Just to understand how prospective it is. First off, let me back up. Colombia was not a mining destination due to security concerns in the 1980s and 90s, as everyone knows. Those were the horrible times for Colombia that have now resulted in many shows, like Narcos, et cetera, being made as a result of what happened in those times. But, the country turned around with the election of the former president Álvero Uribe in 2002. Now we’ve had 20 years of Colombia being open and prospective.

The Middle Cauca belt prospectivity. There has been somewhere in the neighborhood of three million meters of diamond drilling done since 2002, in this belt. That has resulted in the discovery of more than 100 million ounces of gold. Let me caveat that by saying that a lot of that gold is never going to come out of the ground. It’s not all economic gold, but if you look at the prospectivity, for example, in my former company, Continental Gold, we discovered and drilled off 11 million ounces of high-grade gold at around 8 grams per ton and that deposit was open to grow further.

It would be when we got taken out by Zijin, just starting to pour gold from finishing construction. AngloGold alone has drilled off more than 40 million ounces of gold over a series of projects, for an approximately 20-year period. Then there are many others. So prospectivity is remarkable and being in the Cauca belt is fantastic.

Zooming in, I mentioned this project named Marmato, which we do not own, that is in another company. Marmato is an approximate 8 million ounce resource with less than 8 million ounces of reserves, that is pushing toward production, as we speak. What we recognized that one of the best places to find a mine, is next to a mine?

Marmato is a porphyry-related vein system. I want readers to think of Chile because Chile is the world’s largest copper producer and the bulk of that copper production comes from porphyry deposits.

Porphyries are intrusions in the earth where individual fingers of porphyry rock come up, the pulse pushes them up and then you get these complexes, they are typically about, let’s say, up to four miles by four miles in circumference within which, you will have fingers of porphyries which can be very large, in the billions of tonnes. Then you have breccia’s related to the porphyry and you have vein systems related to the porphyries. A key feature of the porphyries, breccia related to porphyries, and vein systems related to porphyries, is the dimensions of these deposits can get very large.

I mentioned billions of tonnes for porphyries, vein systems, my former project Buriticá at Continental Gold contained 11 million ounces. It has been drilled off over about 2 kilometers, or call it almost 1.5 miles vertically. That is enormous, and whatever you end up having in vertical, you end up having in lateral dimensions about mile-long vein systems along with huge vertical dimensions.

Breccia’s, porphyry-related breccias are also huge. I’m sure readers are familiar with Filo Mining in Argentina, which has been a huge success. They have a porphyry deposit, but what is driving their value is a porphyry-related breccia which sits in the middle of their porphyry and that’s where those unbelievable grades we’ve seen of copper-gold and silver are coming out of this breccia.

Why is that relevant to Collective Mining? We recognize that Marmato is on the fringe of one of those four by four-mile circumference areas that have porphyry intrusion centers and they are our neighbor. We have come in with complete grassroots exploration, and I want to highlight that there are very few companies today doing grassroots exploration. Most companies are retreading old projects with new interpretations that have had lots of drilling and lots of work done. This is true grassroots exploration.

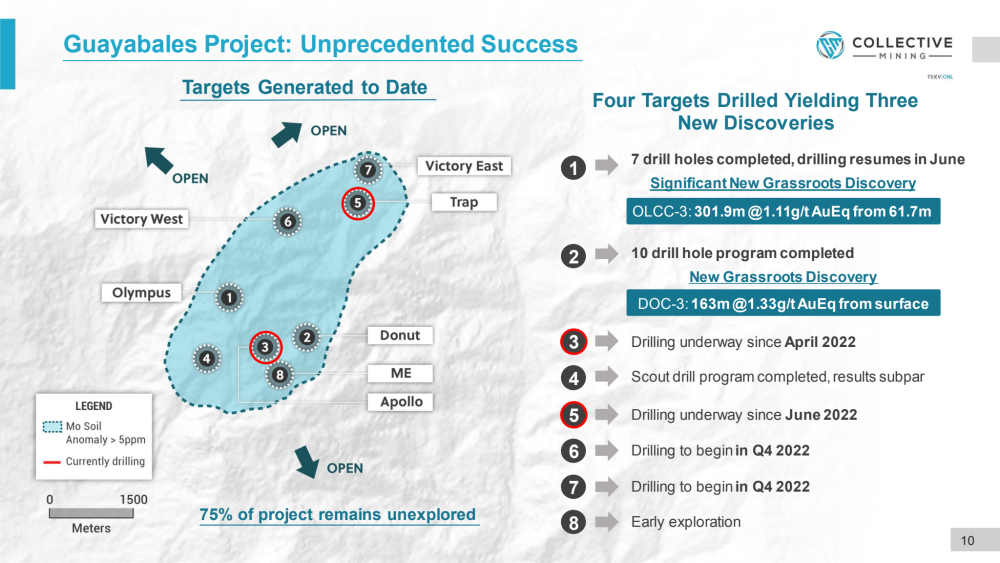

Collective Mining has generated 11 targets on two projects. Our flagship is called Guayabales. That is the one that is contiguous to the historic and current large resource the aforementioned Marmoto. And then we have another one calledSan Antonio. Although it’s a second project, it’s only about a mile away as the crow flies from the edge Guayabales to the concession edge of San Antonio. So, it’s part of the same geological complex. And what we have identified in those 11 targets are either porphyry targets for drilling, porphyry-related breccia targets, or porphyry-related vein systems for drilling. I mentioned grassroots, so we’ve brought all of those targets except for two of them up to the drill, ready status as we speak.

Our flagship Guayabales Project has generated eight targets. I’m going to say something that I don’t say lightly, but this is the best exploration project that I have ever seen or been involved with (period).

And I said that when my technical team identified it, and I iterate it much stronger today because I’m able to back that up with initial drilling success. Today at Guayabales, we have drilled or are currently drilling five of those eight targets.

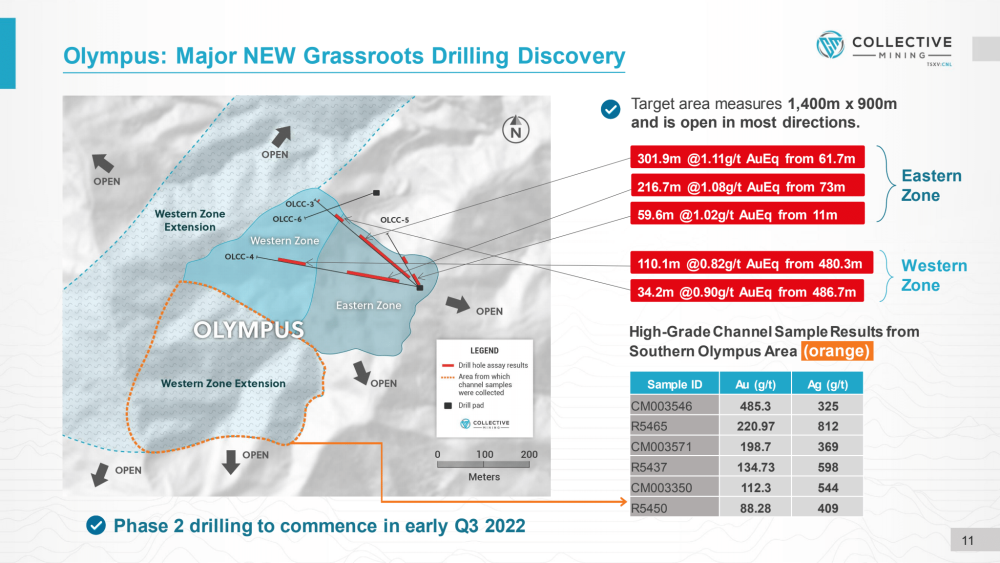

Our Olympus Target may be on the cusp of a significant discovery, which is a vein system over-printing breccia, porphyry-related. And as a result, we’ve drilled big bulk intercepts, including the discovery hole of 302 meters at 1.1 grams per ton, gold equivalent, starting just below surface. We will find out it’s open-pitable as we do more work in the future and prove that up.

We think that Olympus has the earmarks of a multimillion-ounce gold and silver system. Looks similar to Marmato next door and similar to my previous project, Buriticá, which I previously mentioned, we drilled off 11 million total ounces.

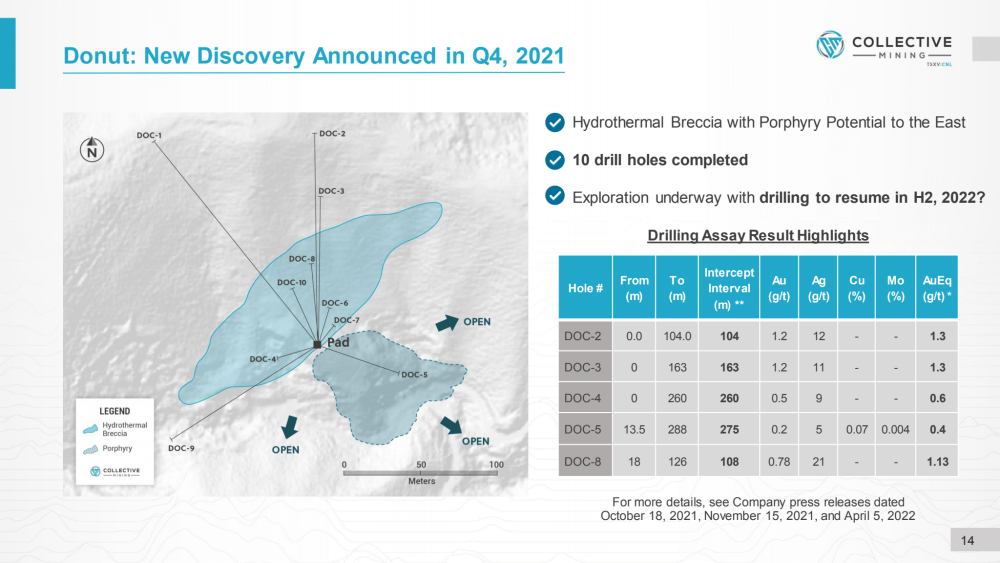

The second target with assays is called Donut. Donut is a porphyry-related breccia. I don’t think this one is going to be huge. It doesn’t have the potential of Olympus, but it’s still significant. It starts right at surface and we have amazing intercepts in it, including up to 163 meters at 1.3 grams per ton, gold equivalent, beginning right at surface.

Why do I say modest? I don’t think this one has multimillion-ounce potential. But if it does turn into a mine, with further work, I think it’ll be a satellite operation that can feed a much larger complex for processing and it’ll be nice to have because it will add incremental ounces onto the total deposit.

The third target that we drilled was called the Box. I say ‘was’ because that one didn’t work for us. We drilled it, we published results, it doesn’t have large-scale potential like we’re looking for and therefore, we’ve concluded that Box is out.

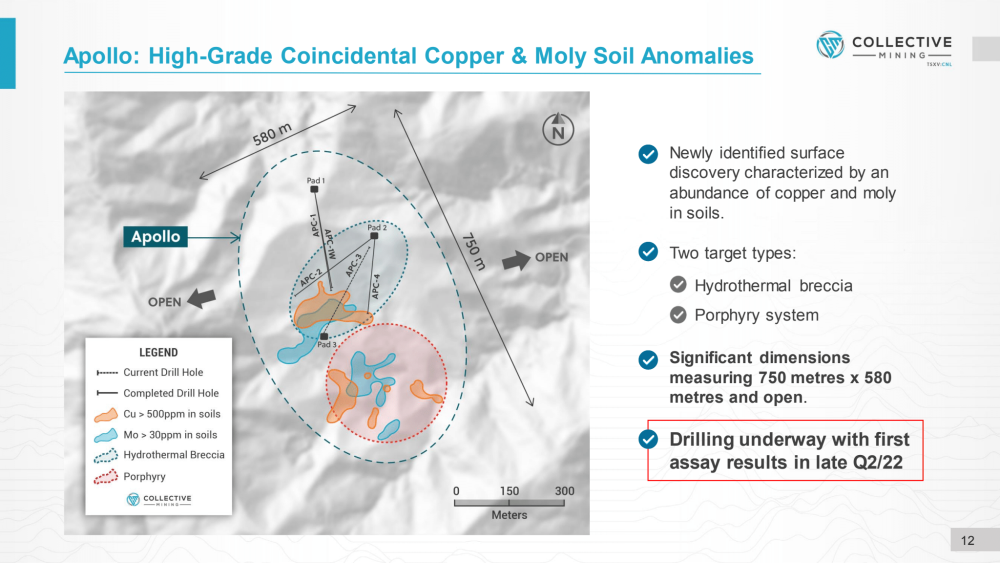

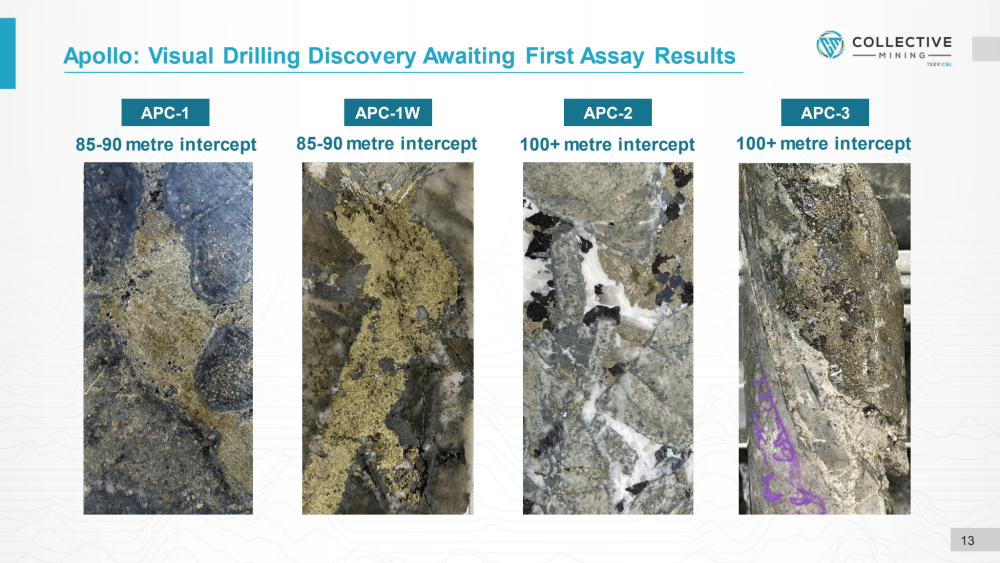

Our fourth target, the Apollo, we are currently drilling and to say we’re over the moon on it is an understatement.

Now, I’m going to put a big caveat out there for readers. We do not have assay results for it yet. We are expecting the initial first assay results for the first drill into it in the next two to four weeks. That is a caveat. I want everyone to know that at the end of the day, the only truth in mining is the assay results. We can like what we see visually, but we need to prove it with the assay results.

With that said, we’re pretty good at identifying rocks and what we see at Apollo, visually, is a porphyry-related breccia. It has an abundance of chalcopyrite and pyrite in the breccia matrix. For those that don’t know what chalcopyrite is, that is a mineral that contains copper in it, so there’s going to be a copper component to this one.

And then we expect there to be gold related to both the chalcopyrite and the pyrite, as well as silver. But, what makes us excited about it is, that the breccia that is mineralized and then over-printing the breccia is a porphyry-related vein system.

How do we know this? We see the pathfinder minerals of porphyry-related veins.

It’s important to note, that porphyry-related veins are known for being gold and silver-rich, which they typically are, but they also have byproducts of lead-zinc and to some extent, copper. So, what we see in the minerals that bring lead-zinc into the matrix are sphalerite for zinc and galena for lead.

These are very easy to identify, sphalerite is typically a brownish color and galena is a grayish color, and you get blobs of them. Why we know it’s over-printed is, instead of being veins that are typically narrow anywhere in the world, when they get into the breccia, the metal blows out from the veins and fills up the matrix of the breccia.

Think of it like this, when you’ve tried to complete a puzzle, there’s a lot of porosity or space between the individual pieces of the puzzle when they’re put together. Metal fluids will come into a breccia structure that looks similar to that, and it will fill up those spaces. Because it’s porous, the metal will spread out into those spaces. What’s happened with the veins is they’ve come into the breccia and there’s been room for the metal to spread. These have spread out into the breccia matrix, which suggests that we may have two overlapping systems.

Why I think this is significant, with the caveat that we don’t have assays, is, in my experience, that big deposits in the world are very rarely found when there’s only one style of mineralization dumping metal into the system. You typically need to see two or more styles. And here we have two very distinct styles.

So, stay tuned on Apollo, quite excited for the results. Then the first hole will be out soon. And, I should add that we are drilling thick visual intercepts at Apollo. This is not one or two meters we’re drilling intercepts of the three holes that are completed so far, visually, between 85 meters and over 200 meters. We’re hoping for long, big intercepts, and with some luck, with the assay, if mother nature is generous to us, we’ll have some decent grade in that breccia.

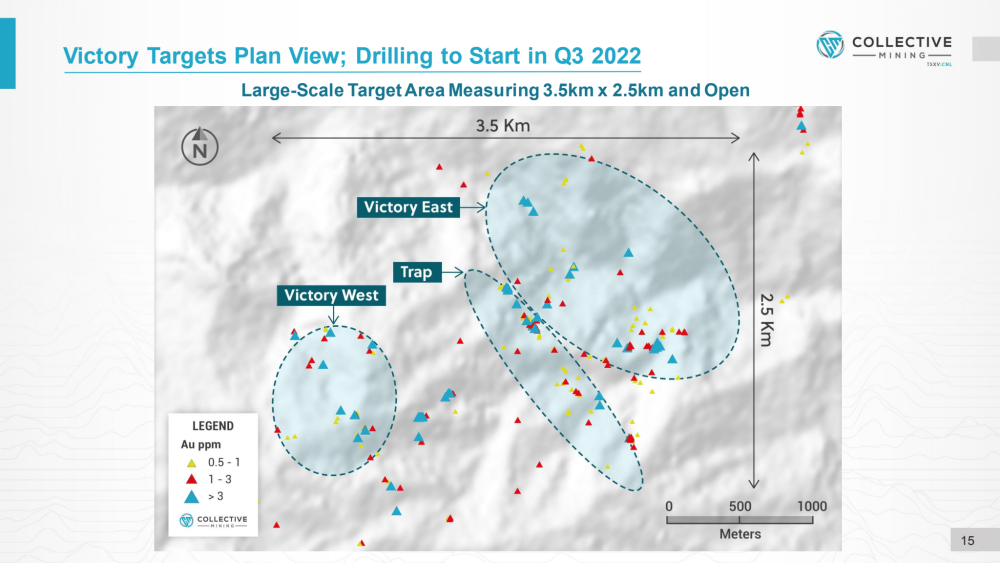

Maurice: Well, speaking of visually, that was a good analogy there. Can you conclude by taking us north for a victory lap and talk to us about the Victory Targets? What are you exploring there?

Ari Sussman: The Victory is the Northern complex of targets located in copper-gold country. We have identified a series of intrusions that are outcropping at surface, particularly at the Victory East Target. That is the one that excites us the most in the victory complex.

Victory has a Victory East, a Victory West, and something called Trap, which is in the middle. Trap is called Trap because it’s trapped porphyry-related veins within a structurally controlled corridor. Victory West, I won’t spend any time on it. It’s a blind target that has interesting geophysics, there may be a porphyry below.

Regarding Victory East, we have identified multiple porphyry intrusion centers that are outcropping and continue to collect and see a significant amount of rocks that are very enriched with magnetite, which in this kind of porphyry setting will contain gold or should contain gold and some silver, as well as chalcopyrite, which is that copper mineral that I mentioned before.

Noteworthy of mention, chalcopyrite is typically about 34% copper. Therefore, when logging a core in a drill hole, indicating there’s 2% chalcopyrite, assuming your logging’s correct, you can multiply by 0.34 and that should give you an approximation of what your copper content is.

We see a mineral that will contain copper and an element that will contain gold and a little bit of silver, over a very large area. We’re working diligently to have Victory East drill-ready for Q4 of this year. I think we have another four hard months of work ahead of us. It’s very big and the dimensions of the area, we’re in the plus mile range in every direction. Our team is trying to figure out where the end of the system is, to be frank, before we zero in and decide where we’re going to drill. That’s what we’re doing right now.

Maurice: To summarize this, early days. But Collective Mining may be on the cusp of at least two potential tier-one deposits before us.

Ari Sussman: Look, mining is a very difficult business. The professionals that are smarter than me, estimate you have about a one in 1,000 chance of making a discovery that ever becomes a mine. Making a discovery is very rare in a grassroots exploration program, and a huge compliment to the geological acumen of our technical team.

We are optimistic that we have two major discoveries under our belt already at Olympus and Apollo, subject to a lot more work. And they’re going to require a lot of proving up. But we’re seeing all the right indications of two big systems and Victory is indicating an enormous, grassroots discovered outcropping porphyry complex that we’re looking forward to seeing if that offers the kind of potential that Apollo and Olympus have already shown us from initial drilling,

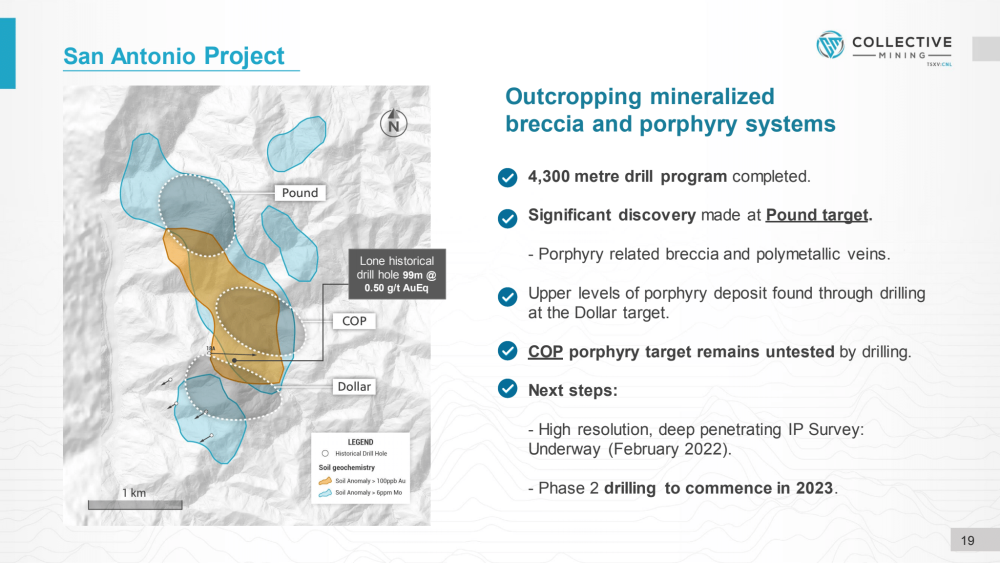

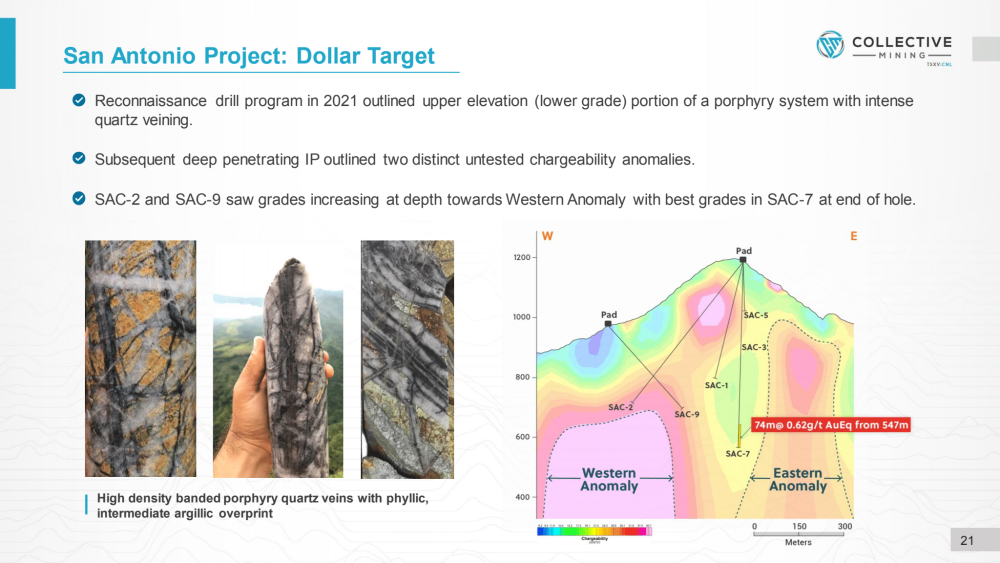

Maurice: Leaving the Guayabales, let’s visit Collective Mining’s secondary project, the San Antonio, which has over 4,300 meters of drilling completed along with a significant discovery. Sir, please introduce us to the San Antonio, along with the genetic and exploration model.

Ari Sussman: OurSan AntonioProject is about a mile as the crow flies from the edge of its concession to Guayabales. It’s a peripheral part of this same complex of porphyry intrusions. We got into San Antonio in mid-2020. We did a lot of surface work. We did some additional geophysics and were able to generate three targets.

The northern target is called Pound, the middle target is called COP, and the southern target is called Dollar. We got busy drilling it, it was an easy one to drill. It came with water permits in place, it was ready to go. So, we put a bunch of holes into the Dollar Target and two holes into Pound. We have not drilled COP as we speak.

This was in late 2020 into early 2021, and those that follow the mining space know that there’s been a significant problem with assay delays plaguing the industry, resulting from COVID.

I think that was probably the peak of the problem at that point. To date, we have built 4,300 meters of core and had no assays and we were frustrated and shut down the program and said, “Well, we can’t drill more until we wait and get assays.” It took months and lo and behold, we got assays. I would say the results, we got a mixed bag. The mixed bag is as follows: Dollar, we drilled the most beautiful looking porphyry core you could imagine.

I urge any geologists to look at the photos of Dollar core. It is remarkable. However, we’re in the very upper portions of a porphyry system where the metal content is leached, indicating that it needs to be drilled deeper, and that is something we plan to do in 2023 to see if we find the portion that contains the metal.

The surprise for us is known as the Pound Target. At the time that we drilled Pound, I can honestly say that the two holes that we put in were more of a Hail Mary attempt. We had done very little work on Pound.

We had found a porphyry-related breccia with a very small footprint, at the time it surfaced, and said, “Let’s put two holes into it and see what happens.”

And the discovery you alluded to is as follows. We drilled two long holes, both slightly more than 700 meters in length, and both hit. They hit about a .5 gram gold equivalent in each. That’s not a grade that I think you’re going to build a mine on in the future, it’s too low. But anytime you drill a system that has two intervals with more than 700 meters of mineralization, and I should add, that both of those holes ended in mineralization, then there’s a big system somewhere there.

Subsequently went in and conducted some surface work. We have outlined a zone that’s over a mile to the north-south by about a half a mile east-west, and open in each direction. And that is worth going back and drilling one or two or three more holes.

The San Antonio is our secondary project, and it doesn’t offer the near-surface, exciting grades visually and with assays, that we’re seeing at Guayabales, but it offers big scale. So our plan is, let’s poke a few more holes into both of these targets. If we get lucky, we’re going to be talking again about it in great deal. If we don’t, I think the business plan would be to bring in a joint venture partner, which would be a major who’s excited about drilling deeper porphyry-style targets. Who’s willing to fund long drill holes and let someone spend that money and to earn a majority interest in the project and Collective Mining shareholders will get carried along for the ride and the potential upside.

Maurice: Before we leave the project sites, a multi-layered question. What is the next unanswered question for Collective Mining? When can we expect a response? What determines success? And what can we expect as far as news flow?

Ari Sussman: Anyone that invests in us wants the excitement of a drill hole. That is why you would invest in us. You are going to see a steady flow of drilling assay results beginning later this month, which would be the first hole from Apollo.

Then we will have a series roughly every month between now and year-end coming out of Apollo. Additionally, our phase two drill program at Olympus. We are going to be drilling from underground to test the high-grade center of the Olympus area. Olympus is characterized by having approximately a hundred artisanal miners that are mining very high-grade veins.

We’ve reported assay results close to 500-gram gold, and well over 1 kilo silver from these veins in channel samples. We want to drill that area because we know there’s a large vein system there. We don’t know how large, but we’re going to prove it out with drilling.

We also think that it could be a bulk tonnage target. The first results from that will start to flow in August or September. So, if you invest in us today, you’re going to see heavy news flow and particularly heavy beginning in August, and it will continue through the balance of the year.

Maurice: Leaving the project site, let’s discuss some important topics germane to your projects. Do you own your projects 100%?

Ari Sussman: So we have an option to earn 100% undivided interest in both projects by making a series of option payments over a number of years. The payments will culminate in 2031. No private royalties are underlying the property. There are no streams, et cetera. We will be clean and clear for 100% pathway to production. Colombia as a jurisdiction, as far as if you were to build a mine, is favorable from a tax perspective. If you’re in the gold business, the royalty rate is 3.2%. That’s below the Latin American average, which is in the +5 something percent range, as we speak. And taxes are in the low 30% which is kind of common for any country. We are in a good jurisdiction, favorable potential economics based on success and constructing a mine and we are excited to be there, 100% ownership is the only way to go on these things.

Maurice: Are you fully permitted?

Ari Sussman: Currently, Collective Mining is permitted for exploration. We are not permitted to build a mine. That is something that you will do once you complete a feasibility study and then follow the procedures in Colombia. Keep in mind, that I have permitted in Colombia, it’s an excellent jurisdiction to permit. We permitted a gold mine, as I mentioned, and it’s not an overbearing process in terms of timeline. It’s very detailed in terms of the workload. It is first class in terms of the government’s ability to assess permits and evaluate them, but they give you a reasonable timeline. You can permit a project in under one year to construct a mine in Colombia. You compare that to the United States where I think the average now is about 10 years. So much more favorable, but it’s a lot of work. But, as far as exploration goes, yes, we are permitted to explore for several years.

Maurice: Is the ultimate goal to build a mine or arbitrage?

Ari Sussman: Having been through this, you need to plan to build a mine. Because, what we can’t control, any of us, is the cycle itself. We all know commodities are cyclical. And so there are periods in the cycle where M&A is very active. Then there are periods where it’s slow. You must build your company as if you’re going to build a mine. But you keep the option open to be taken out. And if someone wants to acquire the cycle’s right, you do that.

That is how we’re going to proceed. If I have a choice in the matter, and I can determine my future, I don’t know if I’d want to build a mine again. I enjoyed the experience, but at its peak, we had about 5,000 people working at our former project Buriticá, between employees and contractors at the peak of construction. It’s a lot to manage, so we are willing to do it again? Yes. Would we want to do it again? I think ideally we would like to sell before we commence construction,

Maurice: We’ve discussed the good, let’s address the bad. What can go wrong and what are your action plans to mitigate that wrong?

Ari Sussman: Colombia. For good or bad, Colombia is very similar to investing in Peru. We all know Peru is one of the world’s largest producers of silver, gold, and copper. But not all projects work in Peru and the reason for that is Peru has a lot of population, similar to Colombia. virtually anywhere that you’re going to find a project that you want to explore and hopefully construct a mine on, you’re going to be dealing with populations, whether it’s villages, towns, or even larger. And what I mean by that, is why it’s like Peru is, that we see projects in Peru that succeed and then we see others that fail. The typical failure is based on having opposition from the locals that are in your area of influence on your projects. So, if you do that part well, you should succeed. If you don’t, you’re going to have problems. And that is critical.

Environment, Social, and Governance (ESG), is a big buzzword that all industries are talking about today. Having been in Colombia for more than a decade, this was critical for us more than 10 years ago when it wasn’t as popular a topic because we would not have succeeded if we didn’t have a good program.

What does a good program mean in ESG? Everyone throws it around like, “How do we do it?” But what does it mean?

It means many things. One, it’s education. People need to understand that mining can be beneficial for their communities and not a detriment.

Two, in Colombia you’re dealing in an agriculture-based economy, so it’s educating people that Colombia and mining are not competitors. They coexist well and are good for the economy because they’re cyclical but at different points in the cycle. So, it’s always nice to have one industry that’s strong while the other one has a low point in the cycle and struggling, to offset each other. That’s very good.

And three, make sure that you strengthen local businesses. I’ve seen this all over the world, a company comes and says, “Hey, we’re going to hire thousands of people locally and that’s great. And indirectly, we’re going to impact thousands more.” And of course, that’s great. But if the businesses that aren’t going to be solely focused on selling to the mine, don’t understand what mining is and how to strengthen their businesses to succeed in that environment, they’re going to fail.

Companies must be willing to spend money, help, and time. Helping small businesses evolve and mature so that they can continue to service the area for whatever goods and products they service, plus accommodate the mining company coming in there, because there’s a big change coming where there are areas of mining, in terms of the number of people. Populations grow due to the needs of a mine. Those are just some of the elements. ESG is the critical thing to focus on. If we don’t do this well, if our sustainability program isn’t strong, it doesn’t matter how many great drill holes or scales of deposit we find, we will get stopped.

Maurice: One of the virtues of Collective Mining is the pedigree of commercial success of building those relationships your team has a proven track record of, it may not make headwinds by saying that you’re permitted and you have the buy-in of the community, but it makes the difference of whether you can proceed or not. That’s one of the virtues, again, that Collective Mining brings to the table.

Switching gears, let’s discuss the people responsible for increasing shareholder value. Please introduce us to your board of directors, management team, and, technical teams, which bring along a vast amount of intellectual capital and have a track record of creating value.

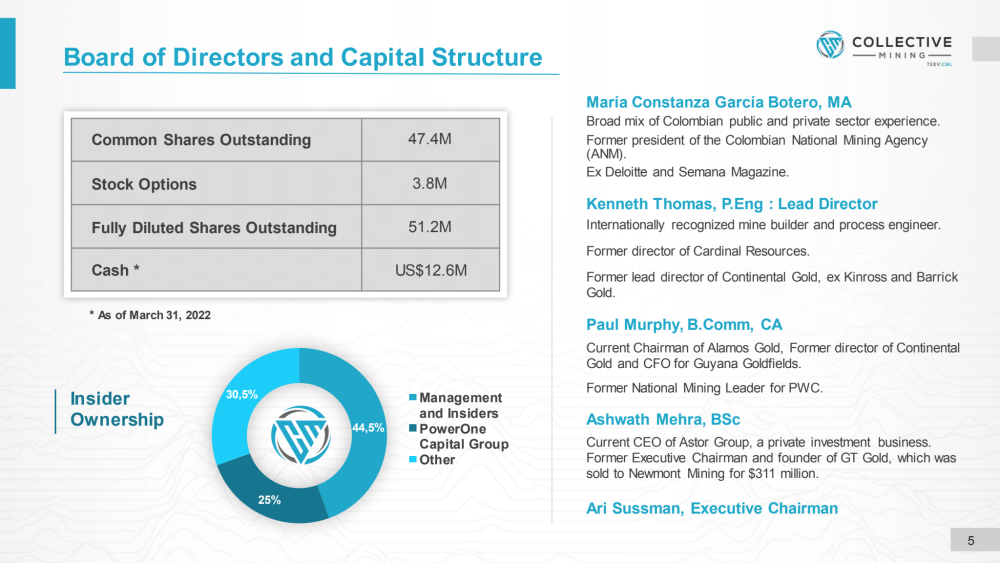

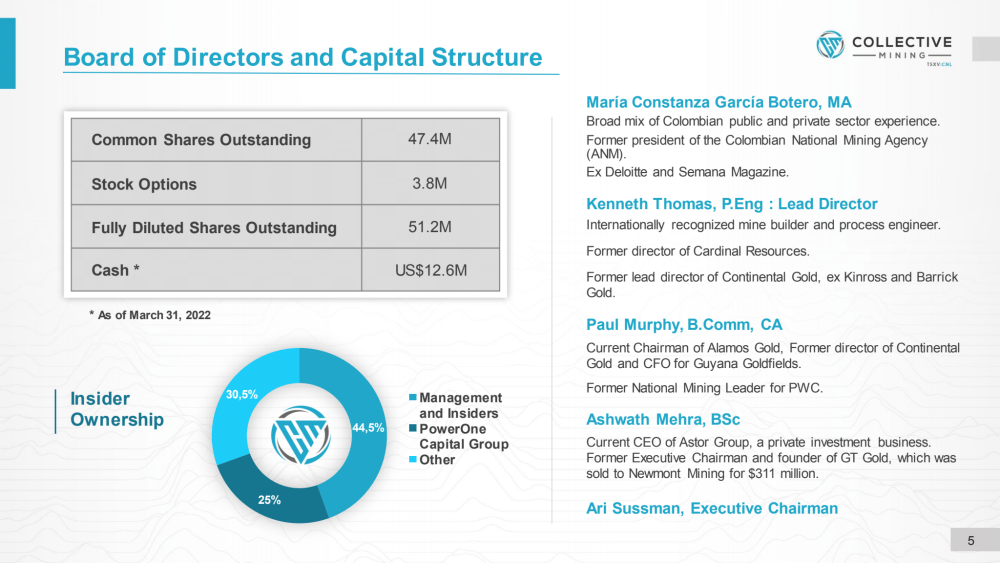

Ari Sussman: Let’s start with the Board of Directors. We have one Colombian representative on our Board, an amazing woman named Maria Constanza. She brings something very strong to the table for us. Although she doesn’t work in the mining business today, she’s been very involved in mining over her career, including being the original president of the A&M, which is the Colombian mining agency that is the division of the government in charge of titling for the country from an exploration standpoint, as well as from an operating standpoint, not environmental permits, but a mining license.

So, we have a deep knowledge of both the private sector and the public sector with her and she’s been involved in numerous companies and has lots of experience.

We come out of Colombia, and on our board of directors is an individual named Ken Thomas. Ken, in the mine building business, is extremely well known, has been around a long time, won many awards over his long and illustrious career, including being one of the original engineers of Barrick Gold when it used to be known as American Barrick. He was around when Goldstrike, which is the largest mine in the Americas, in Nevada, was founded and evolved and grew. So, excellent experience.

We have another individual on our board named Paul Murphy. He’s also the chairman of Alamos Gold Inc. (AGI:TSX; AGI:NYSE), which I’m sure some of your readers are familiar with. But, importantly, he was the national mining leader of PricewaterhouseCooper for a quarter of a century. Paul’s experience in leading the audit committee team in financing projects, he’s an amazing person for that.

And lastly, we have a Swiss national named Ashwath Mehra who is a fantastic guy, and readers probably remember GT Gold, which Newmont purchased for $311 million about two years ago. Ashwath founded that company, brought it forward, and led the sale to Newmont. So, success breeds success, and we’re happy to have him involved on our management team.

We have a big management team. Allow me to begin with myself, I’m the executive chairman of the board of directors, meaning I’m involved in management. Omar Ossma is the president and CEO of the company. Omar is a Colombian, accomplished, and very smart lawyer trained and based in Colombia.

One of the things we wanted to do this time around is to make sure that the President and CEO must have boots on the ground on a full-time basis because the challenges that a company will face will be in the host country in which you operate.

We have an executive vice president named Ana Milena Vásquez, who is recognized as one of the top 100 most influential women in mining, by a prominent UK organization in 2020. And more importantly, she is a sustainability expert as well as government relations. So, ESG is synonymous with Ana and she’s a very powerful force representing our company.

Paul Begin is our chief financial officer. He was the chief financial officer for almost the entire evolution of Continental Gold, so been there, done that, and helped finance and build our former mine Buriticá.

Lastly, I’ll mention two names, two special advisors to the company from a technical perspective. David Reading, David is an internationally recognized economic geologist. Importantly, he was the founding partner of Mark Bristow for Randgold, which is now part of Barrick, to create the largest gold company. And David was instrumental in making multiple multimillion ounce discoveries in West Africa as the team leader of the exploration team of Randgold.

Then lastly, we have another special advisor named Richard Tosdal, better known as Dick. In our view, this is one of the world’s top porphyry experts. I mentioned to you that we have a porphyry complex. We always make sure we bring the best technical talent to the geology end of it to ensure we have the best chance of success and having Dick’s leadership is paramount. That oversees our Colombian team. We have a strong group of vice presidents.

Carlos Rios is our vice president of exploration. This is a geologist who thinks like a business person and has a resource modeling background, not just a pure explorationist. Rodolfo Higuera is our vice president of sustainability, he is responsible for ensuring that on the ground, where we operate, our relationship with all the area of influence communities is sound and solid, and they’re transparently educated on what we’re doing and able to speak. We want to remain in good standing with the communities, and this is key to the platform. Transparency is paramount for our success.

Maurice: Well, let’s get into some numbers. Mr. Sussman, please provide the capital structure for Collective Mining.

Ari Sussman: Collective Mining has approximately 47 million shares outstanding and slightly more than 50 million fully diluted. No warrants are outstanding from any financings. The difference between the outstanding and fully diluted is simply stock options to employees, which everyone will hold long-term.

We are well-financed, meaning we’re fully financed for the calendar year, 2022. And that’s financed for a 20,000 to 25,000-meter diamond drill program. We are going to spend $13.5 million this year, and then we will need money to advance the plans for 2023. That’s something we will look to do toward the end of the year, is to raise additional capital. And that will be done on the back of what we hope is going to be a significant success from drilling at Olympus and Apollo.

Maurice: And how much debt do you have?

Ari Sussman: We have no debt. So we’re very clean. There’s no intent to take on any debt for a very long time. The only time I would ever consider debt is if it’s part of a financing package to construct an actual mine.

Maurice: What percentage of ownership does management have and who are the major shareholders?

Ari Sussman: Management controls approximately 40% of the 47 million shares that are outstanding. We put our money where our mouth is. Management intends to do well as we have confidence that our share price will appreciate, not by drawing exorbitant salaries out of the company to maintain a lifestyle. In addition to that, we have very strong support from a group named PowerOne Capital, who was intimately involved with me at my predecessor company, as well as today.

They are long-term shareholders and they own about 25%. We don’t expect their stock to ever come out into the market and be sold. I can confidently say that the founding partner of PowerOne Capital group invested in Continental Gold previously, held his stock through our sale, to Zijin Mining, and participated in all financing rounds along the way. If you invest with us, you not only have our money where our mouth is, so to speak, because we’re very large shareholders of the company, but you will see management and strong supporters participate in subsequent financings that come as we evolve the business and advance.

Maurice: Well, that 40% ownership is very positive. That’s not common.

Ari Sussman: I would agree with you that 40% ownership is not common.

Maurice: I’m used to hearing about 10%.

Ari Sussman: Collective Mining is a tightly held stock. This is an ideal and more advantageous position for retail investors at this point, more than the institutions. Junior Mining companies, have to do a series of financings over the next number of years to get from today to a production decision. And so, the stock float will loosen up in time and that’s by design because we want to make sure we have a structure that works in the market today and can withstand downturns in the cyclical business we’re in, but will also benefit us in the future as we evolve and leave.

The whole point is to get the share price up as high as possible, and hopefully sold, based on the success of the company. And we don’t want to ever be in the position where we’re in a financing spiral where the market cap grows, but the share price doesn’t. Many mining companies seem to fit that bill, unfortunately, we don’t plan to subscribe to that business model.

Maurice: In closing, what keeps you up at night that we don’t know about?

Ari Sussman: Well, it keeps me up at night. It’s 100% making sure that we maintain the strong sustainability-based program and meaningful relationships with the local communities that we currently enjoy. It’s making sure that we apply our collective model properly so that it is collective for everyone. Everybody needs to jointly benefit together in our success, as well as take the risk with the project. If you want the upside, you have to be involved in the risk too.

Maurice: Last question. What did I forget to ask?

Ari Sussman: I just want to remind readers that Collective Mining expects strong news flow with lots of drilling activity. We are a discovery-based company with already significant results under our belt, and I hope everyone either tries to participate by buying shares, or at least watches us continue to put out news, and hopefully, we’ll end up convincing the naysayers in a short time with what we have in the ground.

Maurice: And for the record, I am a proud shareholder. Mr. Sussman, for someone who wants to learn more about Collective Mining, please share the website address.

Maurice: Mr. Sussman, it’s been a pleasure speaking with you today, wishing you and Collective Mining, the absolute best, sir.

And as a reminder, I am a licensed representative to buy and sell precious metals through Miles Franklin Precious Metals Investments, where we have several options to expand your precious metals portfolio, from physical delivery of gold, silver, platinum, palladium, and rhodium, to offshore depositories, and precious metals IRA’s. Give me a call at 855.505.1900 or you may email: Maurice@MilesFranklin.com. Finally, please subscribe to www.provenandprobable.com, where we provide: Mining Insights and Bullion Sales, subscription is free.

VANCOUVER, BC / ACCESSWIRE / March 7, 2022 / Group Ten Metals Inc. (TSX.V:PGE; OTCQB:PGEZF; FSE:5D32) (the “Company” or “Group Ten”) today reports partial results from four drill holes in a second tranche of drill results from the 14-hole resource expansion campaign completed at the Company’s flagship Stillwater West PGE-Ni-Cu-Co + Au project in Montana, USA.

Results continue to support the Company’s priority objective of expanding the October 2021 inaugural mineral resource estimates, with multiple wide and highly mineralized intervals returned in step-out drilling at three deposit areas that span seven kilometers of the 12-kilometer core project area (see Figure 1). Mineralization remains open to expansion along trend and at depth in all deposit areas.

2021 Drill Highlights:

IM2021-04 returned 115 meters of 0.37% Nickel Equivalent (“NiEq”), or 0.98 g/t Palladium Equivalent (“PdEq”) in a step-out hole to the south of the HGR deposit area at Iron Mountain. Mineralization starts at surface and runs the entire length that has been assayed to date, returning 369 meters at 0.22% NiEq (0.60 g/t PdEq). Assays are pending from the bottom 53 meters of the 422-meter hole. As shown in Table 1, successive contained higher-grade intervals include:

9.8 meters of 1.43 g/t 3E (Pd+Pt+Au) plus Ni, Cu, and Co values for total mineralization of 0.74% NiEq, or 1.98 g/t PdEq, and;

4.8 meters of 1.35% NiEq (equal to 3.60 g/t PdEq) as 0.74% Ni, 0.65% Cu, 0.07% Co, and 0.24 g/t 3E.

CM2021-03 returned 0.24% NiEq (0.63 g/t PdEq) across its entire 428-meter length in step-out drilling in the DR and Hybrid deposit area, including contained intervals at higher grades:

30.3 meters of 0.99 g/t 3E plus Ni, Cu, and Co values for a total of 0.51% NiEq, or 1.36 g/t PdEq;

0.50% NiEq, or 1.34 g/t PdEq, over 9.2 meters, and;

0.50% NiEq, or 1.34 g/t PdEq over 7.2 meters in a separate, lower interval.

CM2021-02 returned top-to-bottom mineralization with 333 meters at 0.23% NiEq, or 0.61 g/t PdEq, and successive higher-grade intervals including 17.0 meters of 0.51% NiEq (1.35 g/t PdEq).

These results, in addition to results released December 20, 2021, demonstrate significant potential to expand the October 2021 mineral resource estimates with multiple long intervals at grades well above the 0.20% NiEq cut-off grade used in that study. Moreover, as shown in Figures 2 and 3, these results provide important intercepts in step-out drill holes located up to several hundred meters from three of the five deposits modeled in the 2021 resource estimate:

CM2021-02 and -03 are two of six holes drilled in 2021 in the DR and Hybrid deposit area to step out from high-grade nickel sulphide-PGE mineralization identified in hole CM2020-04. In addition, these holes also returned potentially significant extensions of hybrid-type mineralization. Hole CM2021-01, reported December 20, 2021, was drilled south from the same pad as CM2021-02 and returned 728 meters of continuous sulphide mineralization at 0.27% NiEq, or 0.73 g/t PdEq, with multiple contained intervals at successively higher grades;

CZ2021-02 is one of two holes drilled in 2021 to step-out to the south of the CZ deposit in the area of wide, high-grade mineralization returned in hole CZ2019-01. Hole CZ2021-01, reported December 20, 2021, returned the widest high-grade intercept to date on the project being 63.7 meters of 0.92% NiEq (2.46 g/t PdEq) in this area;

IM2021-04 is one of six holes drilled in the HGR deposit area with the objective of expanding on wide intervals of high-grade mineralization returned in hole IM2019-03 which returned 272 meters at 0.43% NiEq (1.16 g/t PdEq) including 26.8 meters at 1.24 g/t 4E, 0.34% Ni, 0.15% Cu, and 0.019% Co, for 0.96% NiEq (2.55 g/t PdEq).

Assay results remain pending from eight holes, in addition to rhodium assay results on the majority of mineralized intervals reported to date.

Michael Rowley, President and CEO, commented, “The Stillwater Igneous Complex has been a large-scale American source of critical minerals for many decades, from chromium mined in the 1940s and 1950s to palladium and platinum that became essential in the 1980s. Our “Platreef-in-Montana” model is well-timed for what we believe will be the next phase of the Stillwater district’s contribution to critical mineral supply and commodity independence in the USA; world-class nickel and copper sulphide deposits, enriched in palladium, platinum, rhodium, gold, and cobalt and hosted in the lower Stillwater complex at Stillwater West.”

“This second tranche of drill results from our resource expansion campaign builds nicely upon the first results and continues to advance us towards expanded resource estimates in three of the five deposit areas on a priority basis. We continue to see demonstrations of a large mineralized system with an impressive endowment of eight of the commodities listed as critical by the US government in numerous holes across the 12-kilometer core project area. In addition, we continue to see good optionality on possible mining methods with successively higher-grade intervals contained within wider intervals of hundreds of meters of lower grade mineralization. We look forward to reporting additional drill results, exploration plans for 2022, and other news in the near term.”

Table 1 – Highlight Results from 2021 Expansion Drill Campaigns at the DR, Hybrid, CZ, and HGR Deposit Areas

Assays pending for rhodium and certain intervals denoted by *. Highlighted significant intercepts with grade-thickness values over 20 gram-meter PdEq are presented above, except as noted. Grade thickness values cover significant mineralized intervals with total palladium and nickel equivalent grade-thickness determined by multiplying the thickness of continuous mineralization (in meters) by the palladium equivalent grade (in grams/tonne) to provide gram-meter values (g-m) or by multiplying the nickel equivalent grade (in percent) to provide percent-meter values as shown. Total nickel and palladium equivalent calculations reflect total gross metal content using metals prices as follows (all USD): $7.00/lb nickel (Ni), $3.50/lb copper (Cu), $20.00/lb cobalt (Co), $1,000/oz platinum (Pt), $1,800/oz palladium (Pd), and $1,600/oz gold (Au). Equivalent values have not been adjusted to reflect metallurgical recoveries. Total metal equivalent values include both base and precious metals. In terms of dollar value, 0.20% nickel equates to a copper value of 0.40%, or a palladium value of 0.53 g/t, using the above metal values. Intervals are reported as drilled widths and are believed to be representative of the actual width of mineralization.

Upcoming News and Events

Jeffrey Christian, Managing Director of CPM Group, will join Group Ten CEO Michael Rowley for a live webinar on March 8, 2022, at 10:00 am PT (1:00 pm ET) for a concise overview and update on the Company and the Stillwater West PGE-Ni-Cu-Co+Au project with in-depth discussion on the global macro-economic picture, trends and implications for the broader commodities sector and critical minerals, in particular.

This will be an interactive event with participants encouraged to submit questions and comments throughout.

Group Ten is rapidly advancing the Stillwater West PGE-Ni-Cu-Co + Au project towards becoming a world-class source of low-carbon, sulphide-hosted nickel, copper, and cobalt, critical to the electrification movement, as well as key catalytic metals including platinum, palladium and rhodium used in catalytic converters, fuel cells, and the production of green hydrogen. Stillwater West positions Group Ten as the second-largest landholder in the Stillwater Complex, with a 100%-owned position adjoining and adjacent to Sibanye-Stillwater’s PGE mines in south-central Montana, USA1. The Stillwater Complex is recognized as one of the top regions in the world for PGE-Ni-Cu-Co mineralization, alongside the Bushveld Complex and Great Dyke in southern Africa, which are similar layered intrusions. The J-M Reef, and other PGE-enriched sulphide horizons in the Stillwater Complex, share many similarities with the highly prolific Merensky and UG2 Reefs in the Bushveld Complex. Group Ten’s work in the lower Stillwater Complex has demonstrated the presence of large-scale disseminated and high-sulphide battery metals and PGE mineralization, similar to the Platreef in the Bushveld Complex2. Drill campaigns by the Company, complemented by a substantial historic drill database, have delineated five deposits of Platreef-style mineralization across a core 12-kilometer span of the project, all of which are open for expansion into adjacent targets. Multiple earlier-stage Platreef-style and reef-type targets are also being advanced across the remainder of the 32-kilometer length of the project based on strong correlations seen in soil and rock geochemistry, geophysical surveys, geologic mapping, and drilling.

About Group Ten Metals Inc.

Group Ten Metals Inc. is a TSX-V-listed Canadian mineral exploration company focused on the development of high-quality platinum, palladium, nickel, copper, cobalt, and gold exploration assets in top North American mining jurisdictions. The Company’s core asset is the Stillwater West PGE-Ni-Cu-Co + Au project adjacent to Sibanye-Stillwater’s high-grade PGE mines in Montana, USA. Group Ten also holds the high-grade Black Lake-Drayton Gold project adjacent to Treasury Metals’ development-stage Goliath Gold Complex in northwest Ontario, and the Kluane PGE-Ni-Cu-Co project on trend with Nickel Creek Platinum‘s Wellgreen deposit in Canada‘s Yukon Territory.

About the Metallic Group of Companies

The Metallic Group is a collaboration of leading precious and base metals exploration companies, with a portfolio of large, brownfield assets in established mining districts adjacent to some of the industry’s highest-grade producers of silver and gold, platinum and palladium, and copper. Member companies include Metallic Minerals in the Yukon’s high-grade Keno Hill silver district and La Plata silver-gold-copper district of Colorado, Group Ten Metals in the Stillwater PGM-nickel-copper district of Montana, and Granite Creek Copper in the Yukon’s Minto copper district. The founders and team members of the Metallic Group include highly successful explorationists formerly with some of the industry’s leading explorers/developers and major producers. With this expertise, the companies are undertaking a systematic approach to exploration using new models and technologies to facilitate discoveries in these proven, but under-explored, mining districts. The Metallic Group is headquartered in Vancouver, BC, Canada, and its member companies are listed on the Toronto Venture, US OTC, and Frankfurt stock exchanges.

Note 1: References to adjoining properties are for illustrative purposes only and are not necessarily indicative of the exploration potential, extent or nature of mineralization or potential future results of the Company’s projects.

Note 2: Magmatic Ore Deposits in Layered Intrusions-Descriptive Model for Reef-Type PGE and Contact-Type Cu-Ni-PGE Deposits, Michael Zientek, USGS Open-File Report 2012-1010.

2021 drill core samples were analyzed by ACT Labs in Vancouver, B.C. Sample preparation: crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 µm included cleaner sand. Gold, platinum, and palladium were analyzed by fire assay (1C-OES) with ICP finish. Selected major and trace elements were analyzed by peroxide fusion with 8-Peroxide ICP-OES finish to insure complete dissolution of resistate minerals. Following industry QA/QC standards, blanks, duplicate samples, and certified standards were also assayed.

Mr. Mike Ostenson, P.Geo., is the qualified person for the purposes of National Instrument 43-101, and he has reviewed and approved the technical disclosure contained in this news release.

Forward-Looking Statements

Forward Looking Statements: This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Group Ten believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Group Ten and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

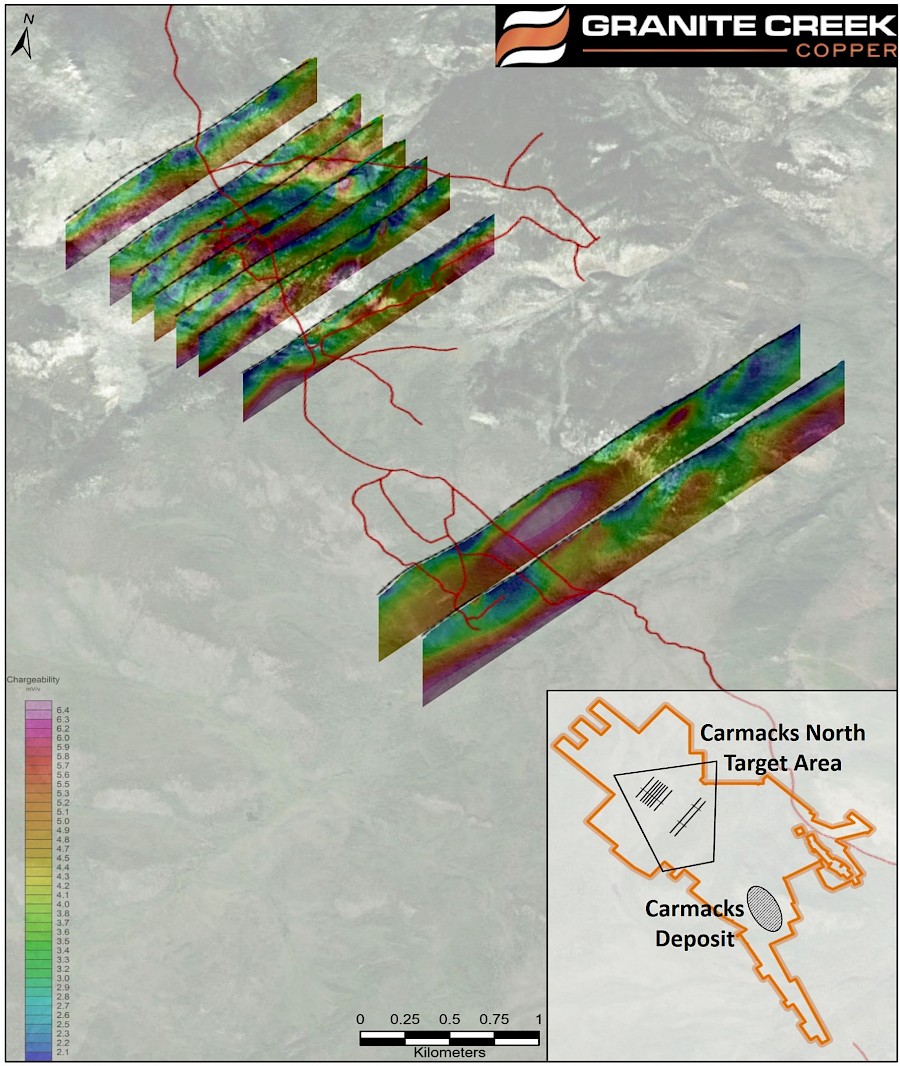

Vancouver, B.C., Granite Creek Copper Ltd. (TSX.V: GCX | OTCQB: GCXXF) (“Granite Creek” or the “Company”) is pleased to announce that Simcoe Geophysics has completed a 20.8 line kilometer (“km”) induced polarization (IP) survey on the Company’s Carmacks North target area. Preliminary results from the survey have identified several near surface chargeability anomalies that have been prioritized as trenching and reverse circulation (“RC”) drill targets for Phase 2 of the 2021 season.

Granite Creek further announces the completion of Phase 1 of its 2021 drilling program, which consisted of 19 holes totalling 6355 meters of diamond drilling on Zones 1, 2000S and 13 of the Carmacks deposit. The first tranche of assays from Phase 1 are expected very soon and will be released in batches as received and reviewed by the Company. With this initial stage of drilling completed, Vision Quest Exploration, based in Whitehorse, Yukon, has mobilized a reverse circulation (“RC”) drill rig to the property and commenced Phase 2 drilling which is expected to consist of approximately 3000 meters.

Given the early start to the 2021 field season and encouraging early indications of success, Granite Creek has made the decision to expand the previously defined 10,000-meter program by adding a third phase which is expected to add an additional 2700 meters of diamond drilling to the overall program. Launch date for Phase 3 is tentatively targeted for early September, with potential to bring that forward to late August. The Company will provide further guidance in this regard in the ensuing weeks.

Granite Creek President & CEO, Tim Johnson, commented, “We are extraordinarily pleased with the progress we have made to date in advancing the Carmacks project. It is a testament to the strength and dedication of our team that we have been able to maintain a very aggressive pace as we move towards an updated 43-101 resource estimate and subsequent economic assessment. This drill campaign has been a showcase of professionalism from our site teams and contractors, and we are very much looking forward to carrying that momentum ahead through Phase 2 and the newly announced Phase 3. In total, we are now expecting to complete over 13,000 meters of drilling, data from which will be incorporated into the new resource update being targeted for Q4.”

Carmacks North Target Area

The Carmacks North Target area is comprised of Zones A-D, as well as additional targets currently being developed. Prior to the Granite Creek’s inaugural drill program completed last fall (see news release dated Feb 11, 2021), little work had been completed on the area since 1980. Historical high-grade copper intercepts of up to 2.52% Cu, 1.64 g/t Au, 12.84 g/t Ag over 19.81 meters were successfully followed up with intercepts of 4.31% Cu, 3.41 g/t Au, 23.78 Ag over 4.36 meters and 0.97% Cu, 0.32 g/t Au, 2.84 g/t Ag over 25 meters. Recognizing the discovery potential in the target area the Company is pleased to deploy modern, advanced exploration tools such as the Alpha Induced Polarization survey employed by Simcoe Geophysics. Capable of measuring the chargeability and resistivity of the rock up to 1000m below the surface these types of surveys greatly improves the chance of success with drilling. The use of a rapidly deployable drill rig such as the RC rig being supplied by Vision Quest along with excavator trenching allows for testing of multiple high priority targets during a single field season.

OTCQB Metals and Mining Virtual Conference

Granite Creek Copper will be presenting at the upcoming Green Energy and Precious Metals Investor Conference hosted by OTC Markets on July 29 at 1:30pm ET. President & CEO, Tim Johnson, will provide a comprehensive overview of the Company, including an update on 2021 exploration activities to date and upcoming newsflow. To register, click here.

COVID-19 Protocols

Granite Creek has worked closely with the Yukon government to develop a COVID-19 safety plan that enables the Company to implement an effective work plan while maintaining the highest degree of safety of our workers and surrounding communities. The Company strictly adheres to mandates put in place by health authorities at the Federal and Territorial government level and holds the health and safety of our workers, and the citizens of the communities in which we work, in the highest regard.

Figure 1: Oblique view of the UBC 2D DCIP inversion sections of the chargeability from 20.8 km of IP collected by Simcoe Geophysics over Carmacks North

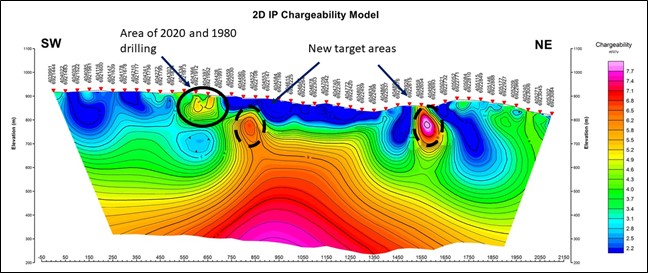

Figure 2: 2D IP chargeability model of Line 3

About Granite Creek Copper

Granite Creek, a member of the Metallic Group of Companies, is a Canadian exploration company focused on the 176 square kilometer Carmacks project in the Minto copper district of Canada’s Yukon Territory. The project is on trend with the high-grade Minto copper-gold mine, operated by Minto Explorations Ltd, to the north and features excellent access to infrastructure with the nearby paved Yukon Highway 2, along with grid power within 12 km. More information about Granite Creek Copper can be viewed on the Company’s website at www.gcxcopper.com.

Ms. Debbie James, P.Geo., a qualified person for the purposes of National Instrument 43-101, has reviewed and approved the technical disclosure contained in this news release.

Forward-Looking Statements This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Granite Creek Copper believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource esti-mates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more infor-mation on Granite Creek Copper and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

“We’re pleased to get the 2021 drill program underway,” said president and CEO of Azincourt, Alex Klenman. “East Preston has had only 12 holes drilled to date, and these early results confirm we have the right basement unconformity uranium setting with the right rocks, structure and alteration. We’re still very early in the exploration phase, and with the recent geophysics program adding significantly to the drill target inventory we’re confident we’re on the path to discovery. We’re looking forward to continuing the development of East Preston,” commented Mr. Klenman.

For further information contact : Spencer Coulter

Corporate Development and Communications

Skyharbour Resources Ltd.

Telephone: 604-687-3376

Email: info@skyharbourltd.com

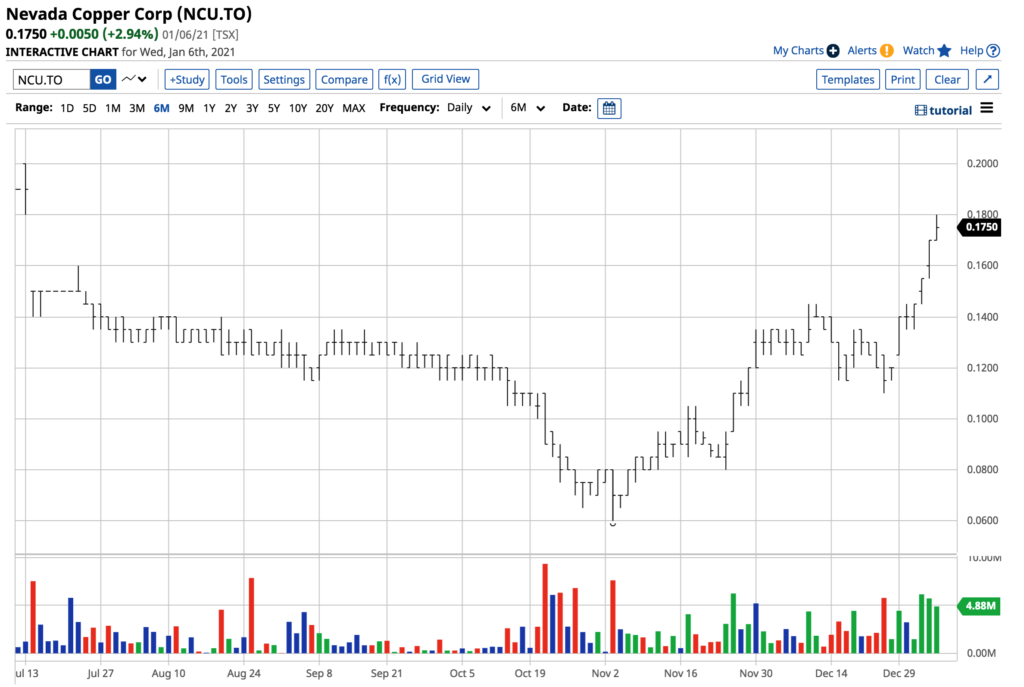

Copper is on a bullish tear- More upside in 2021 in all metals

China is a massive buyer- A reason the US is next

Nevada Copper- A strong management team with solid financing

Proven and probable reserves in the US with the potential for more

An emerging producer- Risk-reward and the value proposition favors lots of upside

Finding value in the stock market is a challenge these days. At the end of 2019, Tesla shares were trading at a split-adjust level of below $90 per share. On December 18, they were at $695. Returns like that are hard to come by; they require taking a fair amount of risk. Elon Musk had more than his share of detractors in late 2019. In 2020, they became very quiet.