Vancouver, British Columbia–(Newsfile Corp. – July 13, 2022) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX”) is pleased to announce the achievement of commercial production for oxide gold mineralization at its flagship Gediktepe royalty property in western Turkey. EMX holds a 10% net smelter return (“NSR”) royalty on oxide gold production at Gediktepe, and operator Polimetal Madencilik Sanayi ve Ticaret A.S. (“Polimetal”), a private Turkish company, has informed EMX that it has produced over 10,000 ounces of gold equivalent[1] ounces, the trigger for commencement of production royalty payments to EMX. In addition to the oxide gold royalty, EMX also owns a 2% NSR royalty on production from an underlying polymetallic copper, zinc, lead and gold deposit that is slated for future development.

The Gediktepe royalty was acquired by EMX as part of its purchase of a portfolio of royalties from SSR Mining Inc. (“SSR”) in 2021 (see EMX News Release dated July 29, 2021). On a go forward basis, Polimetal has informed EMX that it expects to produce between 35,000 and 45,000 ounces of gold per year from Gediktepe (with additional contributions from silver production) while mining the oxide gold cap over the next 3-4 years. The Gediktepe royalty is the subject of a NI 43-101 technical report authored by Dama Engineering with an effective date of February 1, 2022. This technical report has been filed on SEDAR under the Company’s profile and contains historical mining reserve and mineral resource estimates.

In addition to the royalty production payments, EMX is slated to receive cash payments of US$4,000,000 upon the first anniversary of commercial production for oxide gold mineralization, US$3,000,000 on the date that commercial production commences from the underlying sulfide deposit, and US$3,000,00 upon the first anniversary of the commencement of commercial production from the sulfide deposit.

Gediktepe VMS Deposit: The Gediktepe volcanogenic massive sulfide (“VMS”) deposit is a polymetallic system with precious metal, copper, and zinc rich domains. The upper portion of the deposit is oxidized, forming a precious metal-enriched gossanous cap that will be mined first, followed by production from the underlying polymetallic sulfide deposit.

Gediktepe was discovered in 2012 by a joint venture between Alacer Gold Corporation (which merged with SSR in 2020) and Lidya Madencilik Sanayi ve Ticaret A.S. (“Lidya”), a private Turkish company. Alacer Gold Corp later converted its 50% joint venture interest at Gediktepe into the royalty interests now owned by EMX. Polimetal is a wholly owned subsidiary of Lidya and serves as the operator for the Gediktepe project.

More information on the Gediktepe royalty asset can be found at www.EMXroyalty.com.

Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and the TSX Venture Exchange under the symbol EMX, and also trade on the Frankfurt exchange under the symbol “6E9”. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 973-8585 Dave@emxroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@emxroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserve and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential”, “go forward” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended March 31, 2022 (the “MD&A”) and the most recently filed Annual Information Form (the “AIF”) for the year ended December 31, 2021, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

[1] Gold equivalent ounces as referred to in the definition of “Oxide Commercial Production” in the 2019 Gediktepe share purchase agreement between Alacer Gold Madencilik A.S. and Lidya Madencilik.

In the recent Wall Street Journal article “Inflation Surge Earns Monetarism Another Look,” Greg Ip writes that a recent surge in inflation is not likely to bring authorities to reembrace monetarism. According to Ip, money supply had a poor record of predicting US inflation because of conceptual and definitional problems that haven’t gone away.

The head of the monetarist school, the late Milton Friedman, held that inflation is always and everywhere a monetary phenomenon. Friedman and other monetarists believed that the key driving factor for general increases in prices is increases in money supply.

This viewpoint has come under scrutiny since the early 1980s because the correlation between inflation and money supply disappeared. According to Ip in 2020, Alan Detmeister, an economist at UBS Group AG and formerly of the Fed, found inflation’s correlation to M2 since the early 1980s was weak and its correlation to both the monetary base and M1 was negative. Most economists have stopped using money supply as an indicator for inflation since the early 1980s.

Many mainstream economists have attributed the breakdown in the correlation between the money supply and inflation on the unstable velocity of money. What is it? According to the famous equation of exchange, MV = PT, where:

M stands for money,

V stands for the velocity of money,

P stands for the price level, and

T for the volume of transactions.

This equation states that money multiplied by velocity equals the value of transactions. Many economists employ GDP (gross domestic product) instead of PT, thereby concluding that

MV = GDP = P (real GDP).

The equation of exchange appears to offer a wealth of information regarding the state of an economy. For instance, if one were to assume stable velocity, then for a given stock of money one can establish the value of GDP. Furthermore, a given real output and a given stock of money enables us to establish the price level.

For most economists the equation of exchange is regarded as a very useful analytical tool. The debates that economists have are predominantly with respect to the stability of velocity. If velocity is stable, then money is seen as a very powerful tool in tracking the economy. The importance of money as an economic indicator however diminishes once velocity becomes less stable and hence less predictable.

However, an unstable velocity could occur because of an unstable demand for money. Most experts believe that since the early 1980s, innovations in financial markets made money velocity unstable. This in turn made money an unreliable indicator of inflation.

We believe the alleged failure of money as an indicator of inflation emanates from an erroneous definition of inflation and money supply. This failure has nothing to do with an unstable demand for money, and just because people change their demand for money does not imply instability. Because an individual’s goals may change, he might decide that it benefits him to hold less money. Sometime in the future, he might increase his demand for money. What could possibly be wrong with this? The same goes for any other goods and services—demand for them changes all the time.

Defining Inflation

According to Murray Rothbard and Ludwig von Mises, inflation is defined as the increase of the money supply out of “thin air.” Following this definition, one can ascertain that increases in money supply set economic impoverishment in motion by creating an exchange of nothing for something, the so-called counterfeit effect.

General increases in prices are likely to be symptoms of inflation—but not always, however. Note that prices are determined by both real and monetary factors. Consequently, it can occur that if the real factors are “pulling things” in an opposite direction to monetary factors, no visible change in prices is going to take place. If the growth rate of money is 5 percent and the growth rate of goods supply is 1 percent then prices are likely to increase by 4 percent. If, however, the growth rate in goods supply is also 5 percent then no general increase in prices is likely to take place.

If one were to hold that inflation is about increases in prices, then one would conclude that, despite the increase in money supply by 5 percent, inflation is 0 percent. However, if we were to follow the definition that inflation is about increases in the money supply, then we would conclude that inflation is 5 percent, regardless of any movement in prices.

Defining Money Supply

Prior to 1980, it was popular to employ various money supply definitions in the assessment of the changes in the prices of goods and services. The criterion for the selection of a particular definition was its correlation with national income. However, since the early 1980s, correlations between various definitions of money and national income have broken down. Some analysts believe that this breakdown is because of changes in financial markets, making past definitions of money irrelevant.

A definition presents the essence of a particular entity, something no statistical correlation could ever provide. To establish the definition of money we have to explain the origins of the money economy. Money has emerged because barter cannot support the market economy. Money is the general medium of exchange and has evolved from the most marketable commodity. Mises wrote:

There would be an inevitable tendency for the less marketable of the series of goods used as media of exchange to be one by one rejected until at last only a single commodity remained, which was universally employed as a medium of exchange; in a word, money.

Since the general medium of exchange was selected out of a wide range of commodities, the emerged money must be a commodity. Rothbard wrote:

In contrast to directly used consumers’ or producers’ goods, money must have pre-existing prices on which to ground a demand. But the only way this can happen is by beginning with a useful commodity under barter, and then adding demand for a medium to the previous demand for direct use (e.g., for ornaments, in the case of gold).

Through an ongoing selection process, individuals settled on gold as standard money. In today’s monetary system, the core of the money supply is no longer gold, but rather coins and notes issued by the government and central bank that are employed in transactions as goods and services are exchanged for cash. Hence, one trades all other goods and services for money.

Part of the stock of cash is stored through bank deposits. Once someone places money in a bank’s warehouse, he is engaging in a claim transaction, never relinquishing his ownership of the money. Consequently, these deposits, which are labelled demand deposits, are part of money.

This is contrasted with a credit transaction, where the lender relinquishes his claim over the money for the duration of the loan. In a credit transaction, money is transferred from a lender to a borrower, but the overall amount of money in the economy does not change because of the credit transaction.

The introduction of electronic money seems to cast doubt on the definition of money. It would appear that deregulated financial markets generate various forms of new money. Notwithstanding, various forms of electronic money or e-money, like digital currency, do not have a “life of their own.”

Various financial innovations do not generate new forms of money but rather new ways of employing existing money in transactions. Irrespective of these financial innovations, the nature of money does not change. Money is the thing that all other goods and services are traded for. Once the essence of money is established by excluding various credit transactions, one can identify the status of inflation. Changes in prices are not going to be relevant here.

Conclusion

Contrary to popular thinking, inflation is not about increases in the prices of goods and services but about increases in money supply. Following this definition, we can establish that the key damage caused by inflation is economic impoverishment through the exchange of nothing for something. What matters as far as inflation is concerned is not the correlation between money supply and the prices of goods and service but increases in money supply.

Contrary to popular thinking, the essence of money did not change because of various financial innovations. Money is a thing that is employed as a medium of exchange. Furthermore, according to Mises’s regression theorem, the historical link between paper currency and gold is what holds the present monetary system together.

Frank Shostak‘s consulting firm, Applied Austrian School Economics, provides in-depth assessments of financial markets and global economies. Contact: email.

Integrous- Oil & Gas- Drilling & Exploration- The Answer to Supply-Side Inflation

Crude oil at the highest price since 2008- Inventories and product prices support higher highs

Natural gas is also at a fourteen-year high- Inventories, and European prices support the continuation of a very volatile bull market

The four reasons for higher fossil fuel prices- SPR releases are a temporary band-aid

Drilling and exploration are the answer to supply-side economic woes

XOP outperforming the stock market in 2022- The trend is your best friend

Throughout most of 2021, the US Federal Reserve called the rising inflationary pressures “transitory.” Late last year, increasing consumer and producer price data convinced the central bank that the economic condition was not a temporary event. The Fed told markets it was preparing to shift to a more hawkish approach to monetary policy to address the economy’s demand-side pressures. The artificially low interest rates, liquidity, and government stimulus in 2020 and 2021 planted the inflationary seeds which sprouted during the second half of 2020, throughout 2021, and into early 2022.

In early 2022, the geopolitical landscape threw a curveball at the central bank when Russia invaded Ukraine, launching the first major war in Europe since WW II. Sanctions on Russia and Russian retaliation began to cause even more upside pressure on commodity prices as Russia is a leading producer of energy and other raw materials. China and Russia’s “no-limits” support agreement complicated matters, setting the stage for the invasion.

Crude oil and natural gas prices had already been rising by the end of 2021. The leading benchmark crude oil futures are the Brent and WTI contracts. After falling to a record low below zero in April 2020, nearby WTI crude oil futures at $75.21 per barrel. Brent futures fell to $16 per barrel, the lowest price of this century in April 2020, and closed 2021 at the $77.78 level.

Meanwhile, nearby natural gas futures dropped to $1.44 per MMBtu in June 2020 and were at the $3.73 level on December 31, 2021. The oil and gas futures markets had been rising, making higher lows and higher highs throughout the second half of 2020 and in 2021. In 2022, they took off on the upside, reaching fourteen-year highs.

Increasing inflation and post-pandemic demand created a bull market in crude oil and natural gas that turned into a perfect bullish storm in 2022. The war and a dramatic geopolitical shift made dynamics shift from demand to supply-side concerns. The Fed has few if any tools to deal with supply-side economic events, and the only answer could be increasing supplies, which is a challenge in the current environment.

Just as the Fed mischaracterized inflation as “transitory,” US and European policies addressing climate change have played a role in the ascent of hydrocarbon prices. Since energy prices are inflation’s root cause, exploration and drilling could be the only answer to address the economic condition. Fossil fuels continue to power the world, and the price action is screaming that monetary policy has taken a backseat to the energy debacle.

Crude oil at the highest price since 2008- Inventories and product prices support higher highs

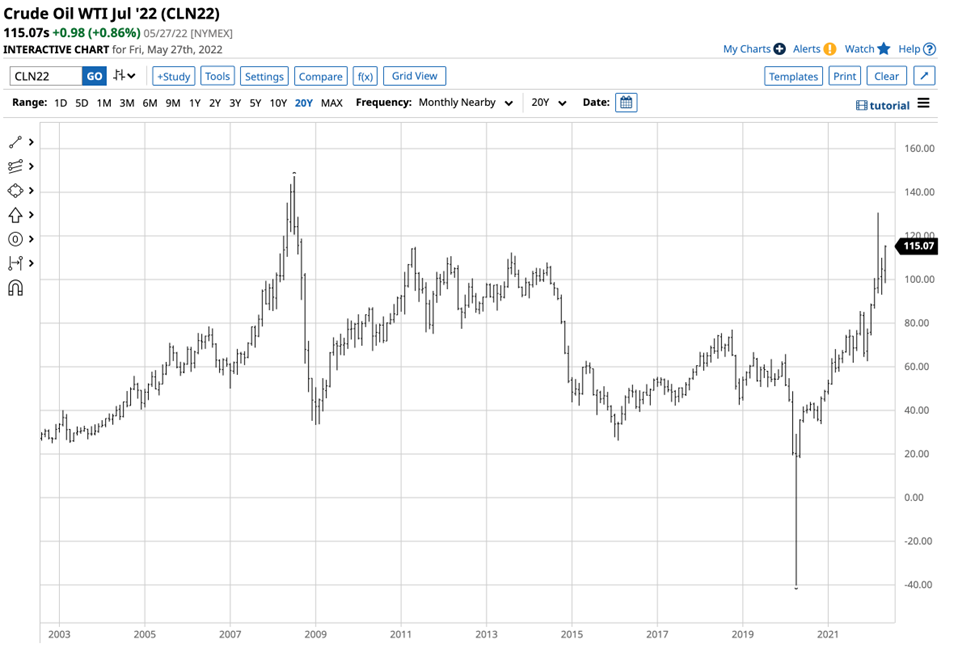

Nearby NYMEX WTI futures rose to $130.50 per barrel on March 7 after Russia invaded Ukraine on February 24, and the war escalated.

Source: Barchart

The chart highlights that the WTI futures were sitting at just above the $115 level on May 27. Brent crude oil hit a high of $139.13 in early March.

Source: Barchart

The chart shows the price was at around the $119.43 per barrel level in late May 2022. The all-time 2008 peaks in WTI and Brent were at $147.27 and $147.50.

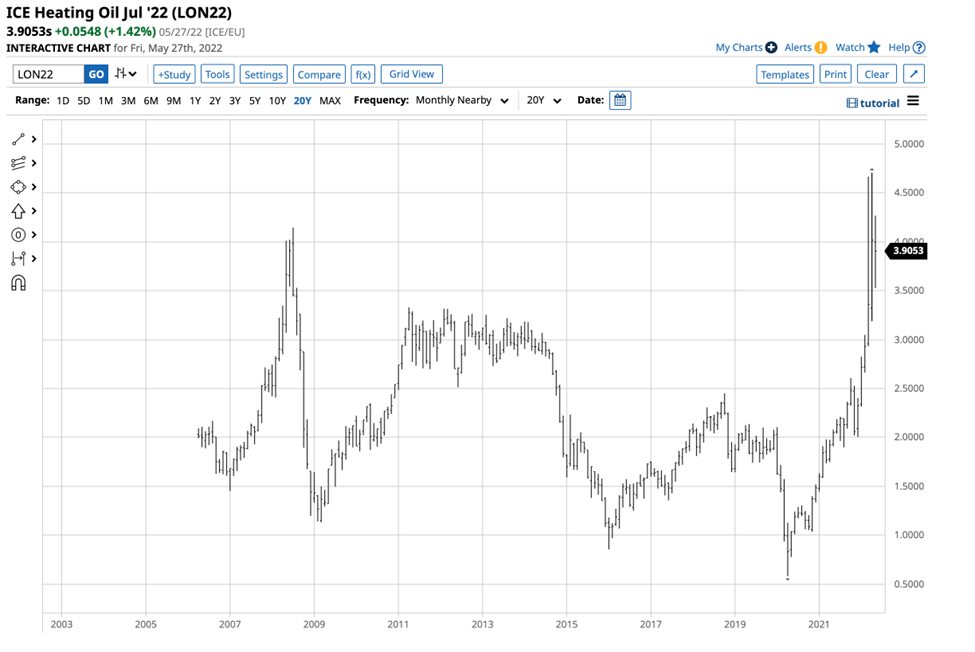

While crude oil missed an all-time high, gasoline and heating oil hit record prices in 2022.

Source: Barchart

The chart shows that gasoline futures prices reached $4.0640 per gallon wholesale in May, an all-time high. July gasoline was sitting at over the $3.90 level on May 27.

Source: CQG

Heating oil is also a proxy for distillates like diesel and jet fuels. The chart shows the spike to a record peak in distillate in April at $4.7072 per gallon wholesale. Heating oil was also over the $3.90 per gallon level on May 27.

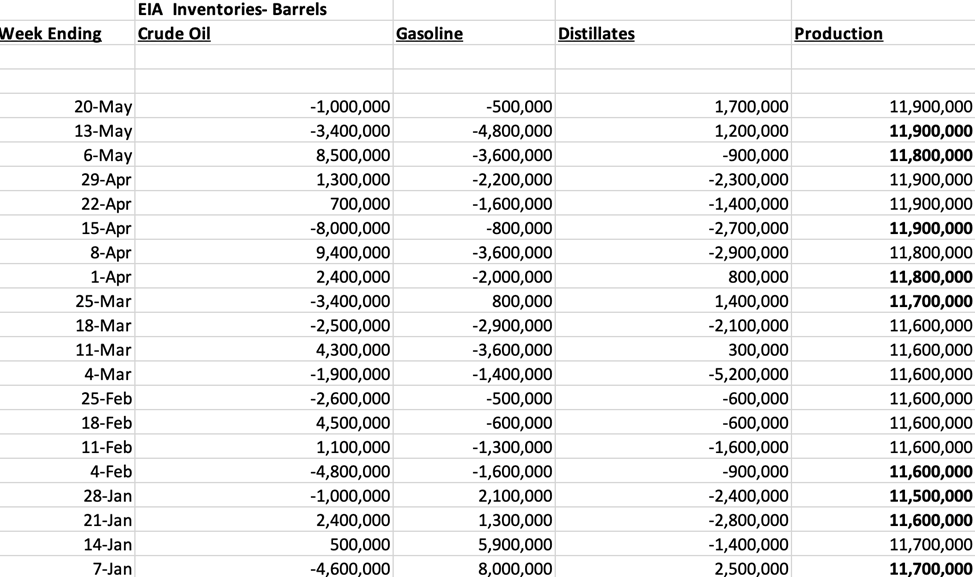

Inventories and US production have supported prices:

Source: US Energy Information Administration

So far, in 2022, US crude oil stockpiles rose by 1.9 million barrels, but the data includes strategic stockpile releases. Meanwhile, gasoline inventories declined by 12.9 million barrels, and distillate stocks fell by 19.9 million barrels from the beginning of 2022 through May 20. Consumers require oil products, and the data supports higher prices. While US daily output rose from 11.7 to 11.9 million barrels per day in 2022, they remain below the March 2020 13.2 mbpd record peak.

Natural gas is also at a fourteen-year high- Inventories, and European prices support the continuation of a very volatile bull market

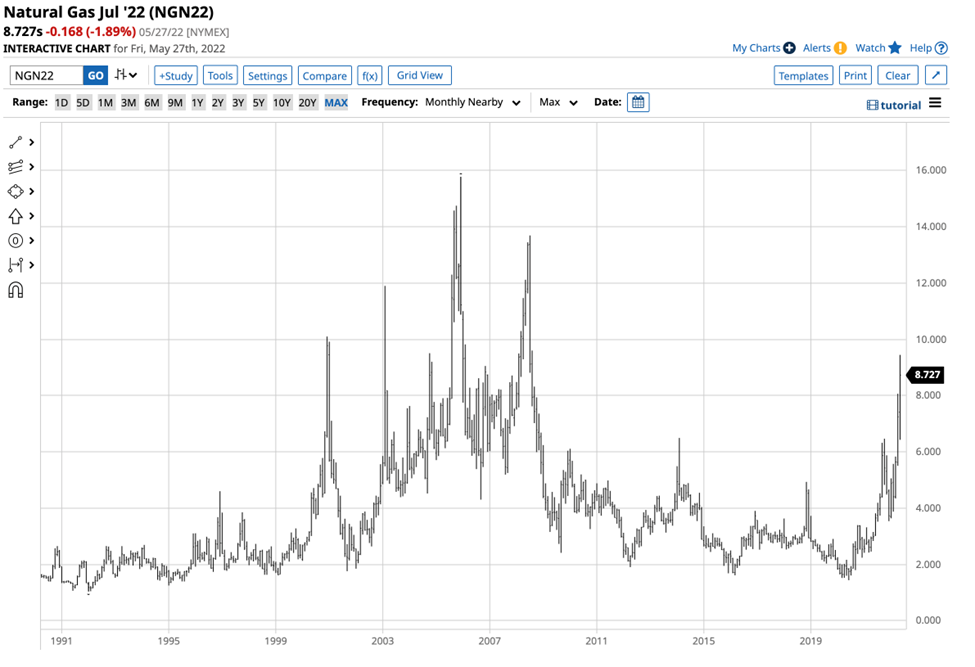

NYMEX natural gas futures fell to a twenty-five-year low in June 2020, reaching $1.432 per MMBtu.

Source: CQG

The long-term chart shows that natural gas futures moved over six times higher by May 2022, reaching a high of $9.447 per MMBtu and sitting at over the $8.70 level on May 27.

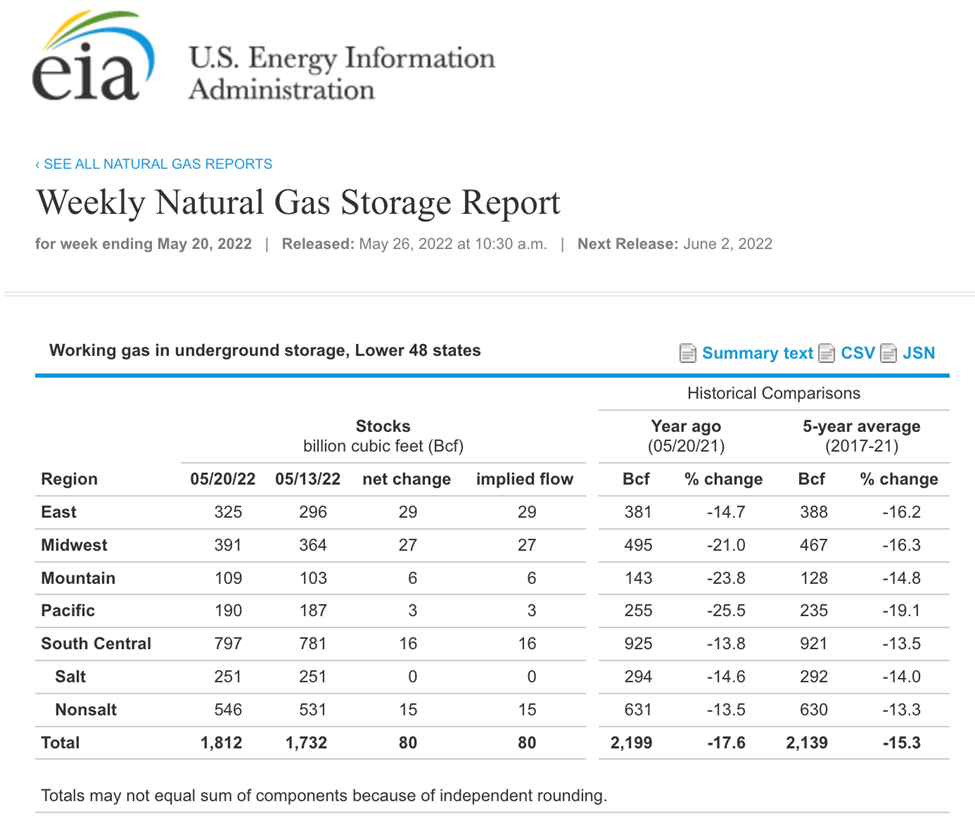

Natural gas inventories are at low levels, with the price at a fourteen-year high.

Source: EIA

At the 1.812 trillion cubic feet level on May 20, natural gas in storage across the US was 17.6% below last year’s level and 15.3% under the five-year average.

Over the past years, natural gas liquefication opened a burgeoning export market for the US energy commodity as it now travels worldwide via ocean vessels. Natural gas’s addressable market expanded far beyond the US pipeline network.

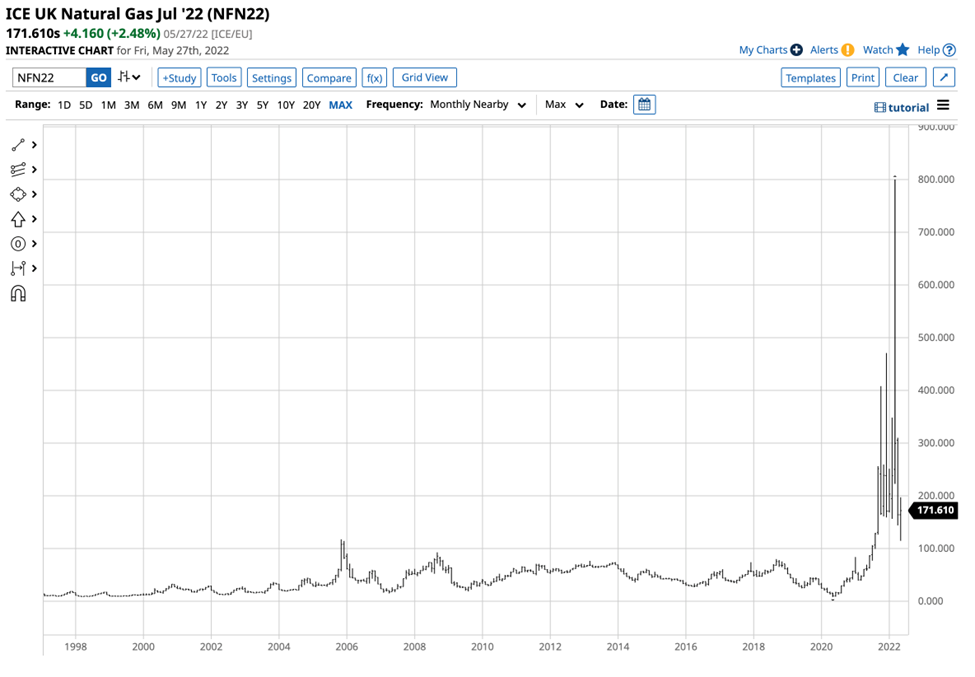

While US natural gas exports have sold LNG to Asian consumers under long-term contracts, the war in Europe and Russian retaliation for sanctions have sent European natural gas prices to record levels.

Source: Barchart

The chart shows that ICE UK natural gas futures rose to the 800 pounds per 1,000 thermals level in March 2022. Before 2021, the all-time high was at the 117 level, and at the 171.61 level on May 27, the price was well above the pre-2021 record peak. Russian natural gas travels by pipeline to European consumers. The Russians have demanded payment in rubles and have cut off “unfriendly” countries that support Ukraine. Moreover, Sweden and Finland’s plans to join NATO only increase Russian export bans, and European consumers are turning to the US for supplies. The bottom line is that

US natural gas has become an international energy market, and the supply shortage is lifting worldwide prices.

In the US, natural gas is heading into the volatile hurricane season. In 2005 and 2008, Hurricanes Katrina and Rita wreaked havoc along the Louisiana coast. The NYMEX futures delivery point is the Henry Hub in Erath, Louisiana, along the Gulf Coast hurricane corridor. Storms in 2008 and 2005 lifted the price to $13.694, and $15.65per MMBtu, respectively. Even if the natural gas market makes it through the annual hurricane season without category four or five storms, the 2022/2023 winter season in worn-torn Europe will likely push prices higher, with $10+ NYMEX futures prices on the horizon.

The four reasons for higher fossil fuel prices- SPR releases are a temporary band-aid

At least four factors favor higher oil and gas prices in late May 2022:

The Biden administration’s green energy initiative favors alternative and renewable fuels while inhibiting fossil fuel production. The US energy policy since early 2021 handed the pricing power to OPEC, the international oil cartel, and Russia. After years of suffering under low prices and lower US demand because of US shale oil and gas production, OPEC+ now controls supplies and owes the US and European consumers no favors. US requests for production increases fell on deaf ears in Riyadh, Moscow, and other production capitals.

The February 4 “no-limits” agreement between China and Russia creates a bifurcation of the world’s nuclear powers, with the US and Europe on the other side. Russia’s invasion of Ukraine could lead to Chinese reunification attempts with Taiwan. Hostilities and geopolitical tensions make hydrocarbons a political tool for the Russians and allied world oil and gas producers.

The crude oil and natural gas prices have been rising despite a COVID-19 lockdown in China. When the Chinese economy reopens, the global energy demand will likely rise, putting more upside pressure on oil and gas prices. Meanwhile, a historic heatwave in India is causing increased energy demand in the world’s second-most populous country. India has not cooperated with the US and Europe with sanctions on Russia.

Even if the US were to shift back to a drill-baby-drill and frack-baby-frack approach to traditional energy production, labor shortages and higher input and equipment prices put upside pressure on production costs. Moreover, the Biden administration has doubled down on its green initiatives, so the potential for production increases remains low.

Instead of increasing production over the past months, President Biden released a historical level of crude oil from the strategic petroleum reserve. Past SPR releases have not weighed on the price in challenging times. Moreover, the US will eventually need to replace its resources, leading to buying in the oil market. The administration released 30 million barrels in early 2022 and has been releasing one million barrels per day from the SPY. The price remains around the $115 per barrel level as the SPR sales have been a short-term, ineffective band-aid. Meanwhile, crack spreads, a real-time demand indicator rose to new all-time highs in May. The level of refining margins are a warning sign that higher crude oil prices are on the horizon.

Drilling and exploration are the answer to supply-side economic woes

The Fed is increasing interest rates and reducing its balance sheet to address the highest inflation in over four decades. The central bank’s toolbox contains monetary policy tools that deal with the economy’s demand-side. In 2020, slashing interest rates and government stimulus encouraged borrowing and spending and inhibited saving.

The Fed now faces supply-side economic factors caused by the war in Ukraine, sanctions, and geopolitical bifurcation. There are few, if any, tools that can deal with the supply-side issues that will continue to fuel inflation. While core inflation data excludes food and energy, food and energy are critical inflationary factors that impact individuals and businesses. Moreover, energy is a crucial cost of goods sold input in all sectors of the economy. Therefore, the only answer to dealing with supply-side inflationary pressures in the current environment is to increase supplies. Just as the Fed woke up from its “transitory” trance, the administration will likely realize that encouraging fossil fuel exploration and drilling is the only route out of the current inflationary spiral. The US is blessed with rich oil reserves in the shale regions, Alaska, and other oil-producing areas. The Marcellus and Utica shale contains quadrillions of cubic feet of natural gas. A hostile Russia and China could cause a reversal of the current path of US energy policy. Rising oil and gas prices will eventually choke all economic growth, and the administration may have no choice but to put climate change initiatives to the side while it deals with the inflationary spiral.

XOP outperforming the stock market in 2022- The trend is your best friend

The war, rising interest rates, a strong US dollar, increasing geopolitical turmoil, and other factors have weighed on the stock market in 2022.

Source: Barchart

The S&P 500 is the most diversified US stock market index. After closing at 4,766.18 on December 31, 2021, the index was 12.8% lower at 4,158.24 on May 27.

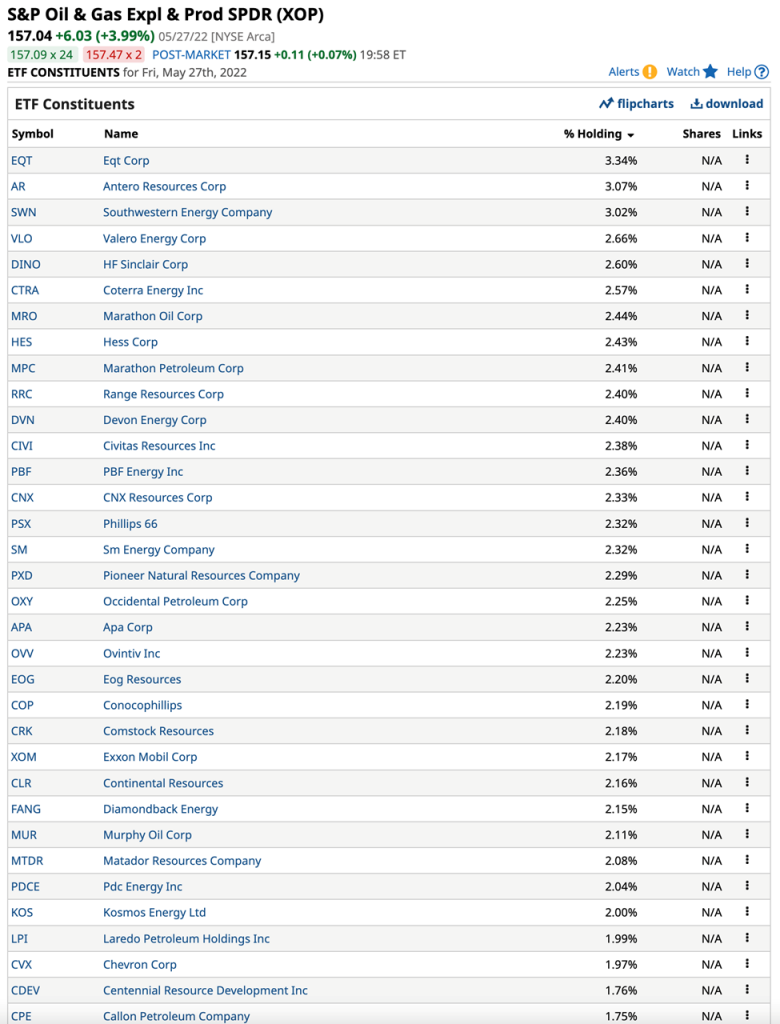

The S&P Oil & Gas Exploration and Production ETF product (XOP) holds many of the top US companies that explore, drill, and produce crude oil and natural gas, including:

While the S&P 500 is 12.8% lower in 2022, the XOP performance has been impressive:

Source: Barchart

The XOP closed at $95.87 at the end of 2021. At the $157.04 level on May 27, the ETF was over 63.8% higher this year.

Existing oil and gas exploration, drilling, and production companies have experienced a profit bonanza in 2022, but they are struggling to meet the growing worldwide hydrocarbon requirements. The bull market in oil and gas opens the door for newcomers in exploration and drilling. Dealing with inflation requires addressing the root cause, energy shortages, and high prices. An epiphany that shifts US energy policy is the path of fighting inflation. The supply-side problems are beyond the Fed’s reach, and SPR releases are only a band-aid on a worldwide gapping ax wound.

Written By: Andrew Hecht, on behalf of Maurice Jackson of Proven and Probable.

Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.

Skyharbour holds an extensive portfolio of uranium exploration projects in Canada’s Athabasca Basin and is well positioned to benefit from improving uranium market fundamentals with six drill-ready projects covering over 240,000 hectares of land. Skyharbour has acquired from Denison Mines, a large strategic shareholder of the Company, a 100% interest in the Moore Uranium Project which is located 15 kilometres east of Denison’s Wheeler River project and 39 kilometres south of Cameco’s McArthur River uranium mine. Moore is an advanced stage uranium exploration property with high grade uranium mineralization at the Maverick Zone that returned drill results of up to 6.0% U3O8 over 5.9 metres including 20.8% U3O8 over 1.5 metres at a vertical depth of 265 metres. The Company has plans for upcoming drill programs at the project.

Skyharbour has a joint-venture with industry-leader Orano Canada Inc. at the Preston Project whereby Orano has earned a 51% interest in the project through exploration expenditures and cash payments. Skyharbour now owns a 24.5% interest in the Project. Skyharbour also has a joint-venture with Azincourt Energy at the East Preston Project whereby Azincourt has earned a 70% interest in the project through exploration expenditures, cash payments and share issuance. Skyharbour now owns a 15% interest in the Project. Preston and East Preston are large, geologically prospective properties proximal to Fission Uranium’s Triple R deposit as well as NexGen Energy’s Arrow deposit.

The Company also owns a 100% interest in the South Falcon Uranium Project on the eastern perimeter of the Basin, which contains a NI 43-101 inferred resource totaling 7.0 million pounds of U3O8 at 0.03% and 5.3 million pounds of ThO2 at 0.023%. Skyharbour has signed a Definitive Agreement with ASX-listed Valor Resources on the Hooke Lake (previously North Falcon Point) Uranium Project whereby Valor can earn-in 80% of the project through $3,500,000 in total exploration expenditures, $475,000 in total cash payments over three years and an initial share issuance.

Skyharbour’s goal is to maximize shareholder value through new mineral discoveries, committed long-term partnerships, and the advancement of exploration projects in geopolitically favourable jurisdictions.

To find out more about Skyharbour Resources Ltd. (TSX-V: SYH) visit the Company’s website at www.skyharbourltd.com.

For further information contact: Spencer Coulter Corporate Development and Communications Skyharbour Resources Ltd. Telephone: 604-687-3376 Toll Free: 800-567-8181 Email: info@skyharbourltd.com

Join us as we sit down with Eric Jensen the general manager of exploration for EMX Royalty as we discuss the latest exciting press release detailing 5 option agreements on battery metal projects located in Scandinavia. The projects (Flåt Project, Bamble Project, Brattåssen Project, Mjövattnet Project, and the Njuggträskliden Project) are located in Norway and Sweden and host Nickel, Cobalt, Copper, and Platinum Group Elements. Plus, shareholders will find out the latest developments on the existing royalty projects, such as the Cukaru Peki Copper Project in Serbia, when EMX plans to pay a dividend?!? Find out why Rick Rule is a shareholder of EMX Royalty right here!

🕘TIMESTAMP🕒 EMX share price review – :36 Company Introduction – 1:26 Production & Consumption on Nickel & Cobalt – 3:16 Scandanavian Mining Jurisdiction – 5:31 Copper supply and demand fundamentals – 7:40 Platinum Group Elements (PGE’s) Outlook – 10:48 How is EMX positioning shareholders to take advantage of battery metals – 12:07 EMX Royalty Executes Option Agreement on 5 Battery Metal Projects – 14:00 Overview of Swedish Projects – 16:39 Overview of Norwegian Projects – 17:50 Exploration Plans for 2021 – 19:07 Assay Results – 20:00 Capital Structure – 20:56 When will EMX begin paying dividends – 22:05 What are the latest updates from Serbia on the Cukaru-Peki Project – 23:27 What is the next unanswered question for EMX – 25:34 What keeps you up at night – 27:03 What did I forget to ask – 27:51

About EMX Royalty: EMX Royalty Corporation has a long-standing track record of success in exploration discovery, royalty generation, royalty acquisition, and strategic investments. Our diversified, three-pronged business approach provides exposure to multiple upside opportunities while minimizing the impact on EMX’s treasury.

EMX’s business model is designed to efficiently manage the risks inherent to the minerals exploration and mining industry. Key elements and resulting advantages of our unique approach are: We organically generate royalties through low-cost property acquisition and early-stage exploration to build value, and then develop partnerships with quality companies to advance the projects, with EMX retaining a royalty interest and receiving pre-production payments. Our organic royalty growth is supplemented by purchases of royalties from other parties, as well as strategic investments. Cash flow from royalties, advance royalties, and other property payments are supplemented by returns from strategic investments, and provide “self-funding” operating capital for our ongoing business initiatives. Using this model, we sustainably grow the royalty portfolio, with minimal dilution to our shareholders. EMX’s royalty and property portfolio spans five continents and consists of a balanced mix of precious metal, base metal, and other assets.