February 17, 2026 – Denver, Colorado: Elemental Royalty Corporation (“Elemental” or “the Company”) (TSX-V: ELE, NASDAQ: ELE) is pleased to announce that its Board of Directors has approved an inaugural dividend policy (the “Dividend Policy”). In accordance with the Policy, Elemental expects to declare an annual cash dividend to its shareholders of US$0.12 per Elemental common share, to be paid in quarterly instalments of US$0.03 per share, with the record date for the inaugural dividend to be paid at the end of the first calendar quarter of 2026, and at the end of each calendar quarter following for subsequent dividends.

The Company is also pleased to announce that it anticipates that qualifying registered shareholders will be able to elect to receive their dividend in the form of Tether Gold XAU₮ tokens, of par value to the dividend price, thereby providing Elemental shareholders with direct ownership of physical gold through their investment in gold royalties.

Highlights

Maiden Dividend Policy approved by the Board of Directors

Expected annual cash dividend of US$0.12 per Elemental share, paid quarterly

Anticipated that qualifying registered shareholders will be able to elect that their cash dividends be invested in Tether Gold’s XAU₮ token

The Dividend to shareholders is supported by Elemental’s strong projected revenue and cash flow growth profile in 2026 and beyond

Further information on how shareholders may elect to receive the dividend or dividend in kind, will be provided in due course

David M. Cole, Chief Executive Officer of Elemental Royalty, commented: “The approval of this dividend policy marks an important milestone in Elemental’s strategic trajectory and reflects our confidence in the strength and momentum of the business; we believe this is the right time to introduce a sustainable, long-term, dividend. The decision to offer investors a dividend in kind, in the form of Tether Gold, further differentiates Elemental as a forward-thinking, growth-oriented investment.”

Stefan Wenger, Chief Financial Officer of Elemental Royalty Corporation, commented: “Our inaugural dividend is underpinned by Elemental’s strong balance sheet and future revenue outlook in the near and longer-term: as of December 31, 2025, we had approximately US$53 million of cash and no debt, providing substantial financial flexibility as we continue to invest in growth. We will continue to maintain a disciplined approach to capital allocation, balancing returning capital to shareholders through a progressive dividend which we intend to maintain, or even increase, without compromising on our strategy of accretive growth through the acquisition and generation of precious metals streams and royalties.”

Juan Sartori, Executive Chairman of Elemental Royalty Corporation, commented: “We believe the initiation of this dividend policy is a world first for a royalty company: we anticipate enabling qualifying shareholders to elect to have their cash dividend invested in the purchase of the Tether XAU₮ token, thereby facilitating for shareholders greater exposure to physical gold through Tether Gold’s stablecoin and retaining real long-term value storage via a practical mechanism for gold-denominated investment returns.”

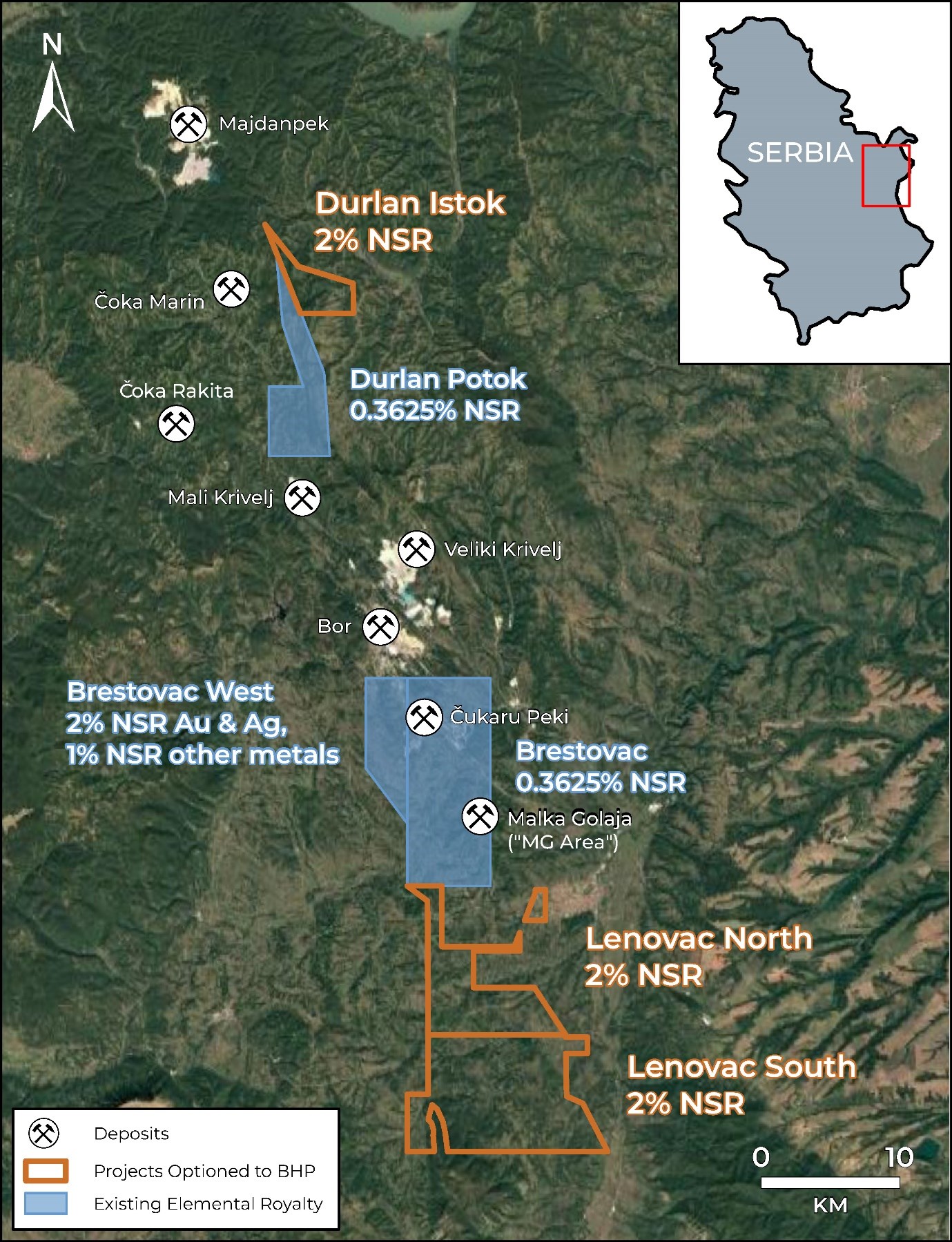

Vancouver, British Columbia–(Newsfile Corp. – January 16, 2026) – Elemental Royalty Corporation (TSXV: ELE) (NASDAQ: ELE) (“Elemental” or the “Company”) is pleased to announce the execution of a definitive option and earn-in agreement (the “Agreement”) covering three exploration licenses in the Bor Mining District of Serbia to a wholly owned subsidiary of BHP Group Limited (“BHP”). The three exploration-stage projects are currently held by Elemental’s wholly owned Serbian subsidiary Magma Resources doo (“Magma”) and BHP will have the option to acquire Magma in exchange for cash payments and by satisfying work commitments. Elemental will retain 2% NSR royalties on the projects as well as other considerations (see discussion of Commercial Terms below).

The Projects nicely complement Elemental’s other royalty interests in the Bor District, which include the Brestovac, Brestovac West, and Jasikovo East-Durlan Potok properties (see Figure 1). Brestovac is one of Elemental’s flagship royalties, covering Zijin Mining Group Co., Ltd’s producing Čukaru Peki copper-gold mine and recently discovered Malka Golaja copper-gold deposit. Zijin has been rapidly expanding its Čukaru Peki operations, increasing capacity at its current mill while continuing to add infrastructure for the development of the “Lower Zone” porphyry copper-gold deposit. Zijin’s published mineral resources and reserves for Čukaru Peki have also continued to grow rapidly, as shown in Zijin’s recent annual reports. The Lenovac projects, included in the BHP Agreement, cover the extension of the geologic trend that hosts the Čukaru Peki and Malka Golaja copper-gold deposits to the south.

Commercial Terms Overview. (all terms in USD) Pursuant to the Agreement, BHP can acquire and retain a 100% interest in Magma and the Projects by satisfying each of the following conditions: (a) making a payment of $200,000 to the Company on the six-month anniversary of the Agreement, (b) annual payments of $200,000 to the Company on every anniversary of the Agreement until the earn-in is complete, and (c) completing $5,000,000 in cumulative exploration expenditures on the Projects within five years.

Upon BHP’s option exercise and earn-in, Elemental will retain a 2% NSR royalty interest on each Project. BHP may buy back up to a total of half a percent (0.5%) of the royalty in quarter percent (0.25%) increments; 0.25% can be purchased for $5,000,000 before the eighth anniversary of the agreement and 0.25% can be purchased for $5,000,000 before the 11th anniversary of the agreement. BHP will also make annual advance royalty payments of $200,000 to the Company until the commencement of commercial production.

Overview of the Projects. The Bor Mining District in eastern Serbia has been one of Europe’s largest copper producers for over a century, where historic and current mining operations have been developed within a cluster of porphyry Cu-Au, high-sulfidation epithermal and skarn systems (including Bor, Veliki Krivelj, Majdanpek and Čukaru Peki; see Figure 1). The Elemental projects (the “Projects”) were originally acquired in 2023 and 2024 and are positioned along trend of Zijin Mining’s Bor and Čukaru Peki operations. Although there are still near-surface deposits being identified in the area, several recent discoveries have been made at relatively deep levels (such as Zijin’s Čukaru Peki and Dundee Precious Metals’ Čoka Rakita deposits) and require deep drilling. BHP’s deep-sensing geophysical capabilities and existing regional interest make them an ideal exploration partner for the Projects.

Elemental has acquired over 150 square kilometres of mineral rights along trend of the major copper and gold deposits within the Bor Mining District (see Figure 1). Previous exploration in the Bor District has typically targeted Upper Cretaceous andesite units, which host the majority of the epithermal and porphyry systems at the Bor Copper Complex and Čukaru Peki mine. However, new discoveries such as Dundee Precious Metals’ Čoka Rakita skarn deposit highlights that the different geologic settings and older Jurassic and Paleozoic host rocks are also prospective for additional discoveries. The Elemental Projects include both the traditionally prospective Upper Cretaceous andesite units of the Timok Magmatic Complex, as well as deeper host rock packages where several recent discoveries have been made.

The Lenovac North and South licenses lie directly south of the Zijin’s Brestovac license, which hosts the Čukaru Peki and the recently discovered Malka Golaja copper-gold deposits. Elemental’s Lenovac licenses cover the southern extension of this trend where a regional fault displaces the trend of mineralization and favorable host rocks to the southwest. The licenses are largely comprised of prospective Cretaceous volcanic and sedimentary units with some areas of Miocene cover.

The Durlan Istok license is located to the southeast of Zijin’s Majdanpek porphyry copper-gold mine and east of Čoka Marin, a high-grade polymetallic volcanogenic/epithermal deposit. The Durlan Istok license contains the stratigraphic sections that hosts Čoka Marin and the Čoka Rakita skarn further to the southwest.

Comments on adjacent or nearby Districts, Mines, and Deposits. The districts, mines, and deposits discussed in this news release provide context for Elemental’s projects, which occur in similar geologic settings, but this is not necessarily indicative that the Company’s projects host similar tonnages or grades of mineralization.

North American Investor Relations Elemental has retained the services of Renmark Financial Communications Inc. to handle its investor relations activities in North America. In consideration of the services to be provided, the monthly fees incurred by Elemental will be a cash consideration of up to C$9,000, starting January 1, 2026, for a period of seven months ending on July 31, 2026, and monthly thereafter. Renmark Financial Communications does not have any interest, directly or indirectly, in Elemental or its securities, or any right or intent to acquire such an interest.

About Elemental Royalty Corporation. Elemental Royalty is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 16 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental Royalty trades on the TSX Venture Exchange under the ticker symbol “ELE”, and on the NASDAQ Stock Market under the ticker symbol “ELE”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Qualified Person Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

Cautionary note regarding forward-looking statements This news release contains certain “forward looking statements” and certain “forward-looking information” as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar terminology.

Forward-looking statements and information include, but are not limited to, the Company’s ability to deliver a materially increased revenue profile with a lower cost of capital, the future growth, development and focus of the Company, and the acquisition of new royalties and streams. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental Royalty to control or predict, that may cause Elemental Royalty’ actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions, the absence of control over the mining operations from which Elemental Royalty will receive royalties, risks related to international operations, government relations and environmental regulation, the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits;; the possibility that future exploration, development or mining results will not be consistent with Elemental Royalty’ expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental Royalty for the year ended December 31, 2024. Elemental Royalty undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represents management’s best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Figure 1. Elemental Royalty interests and projects in the Bor Mining District of Serbia.

This Phase I drill program represents the first drilling at Cuddy Mountain in over 40 years.

Scout commenced drilling at Cuddy Mountain in late fall with permits allowing for continued drilling through fall 2026 – with the private placement closed updates can now be issued.

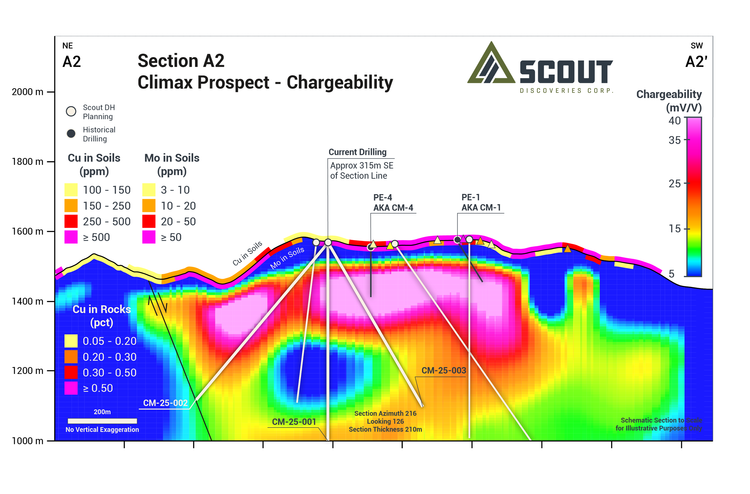

One internally operated core drill is focused on testing high-priority targets at the Climax zone through winter with two holes completed to target depth and the third ongoing.

Drilling will progress to the IXL and Railroad targets with additional rigs added as results warrant; assays to be released when enough holes comprise a complete test of the target.

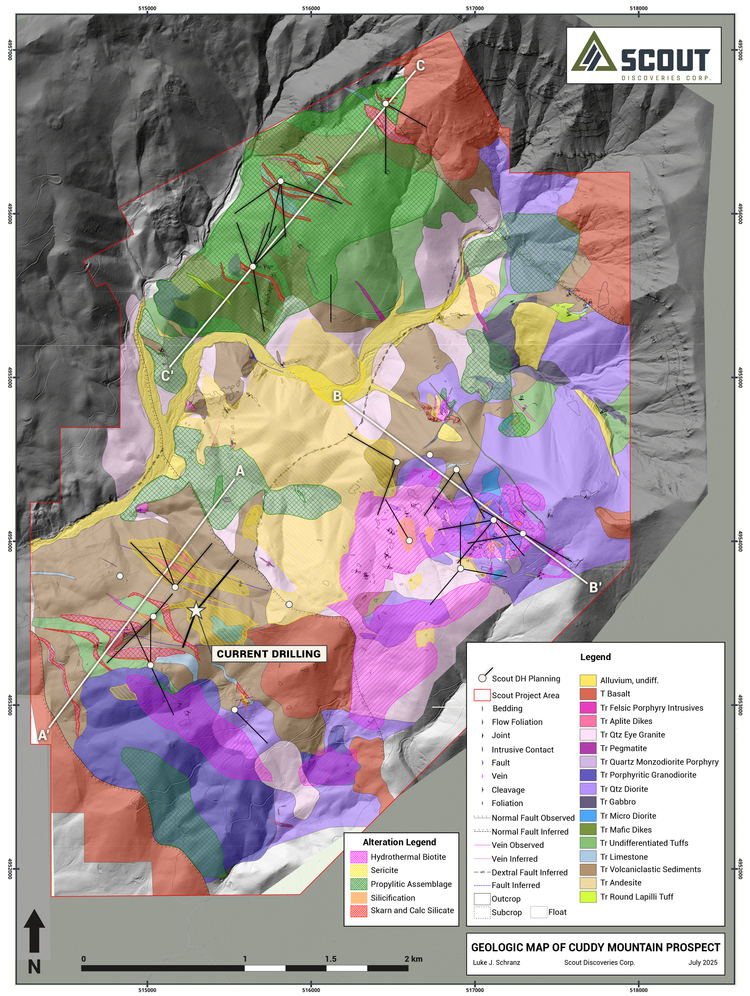

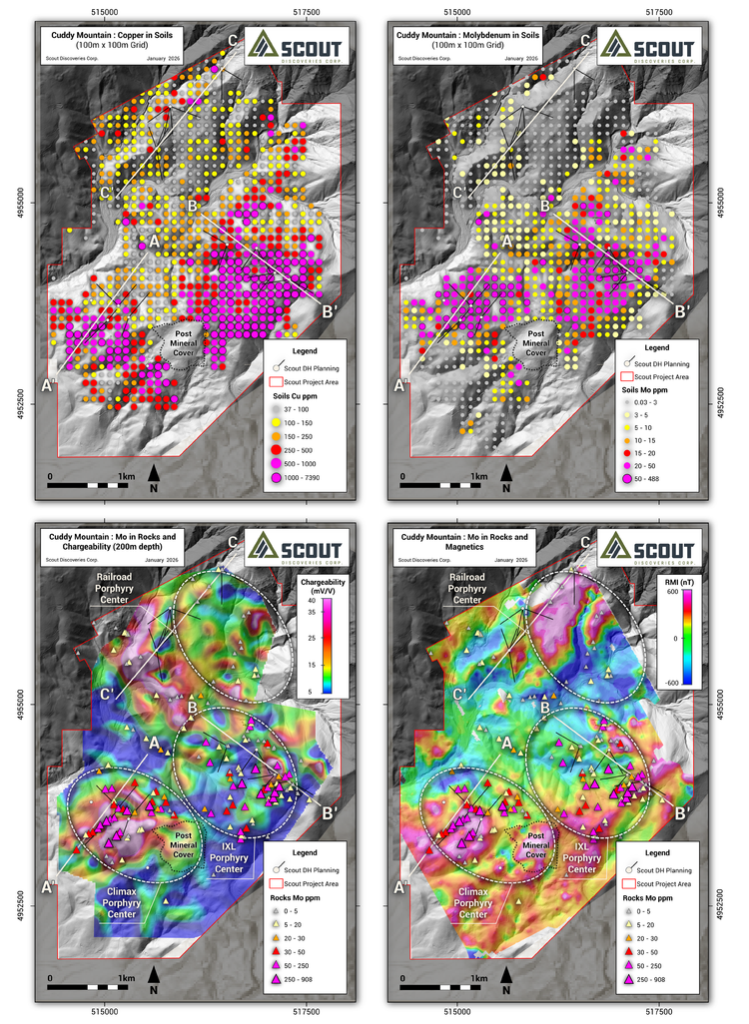

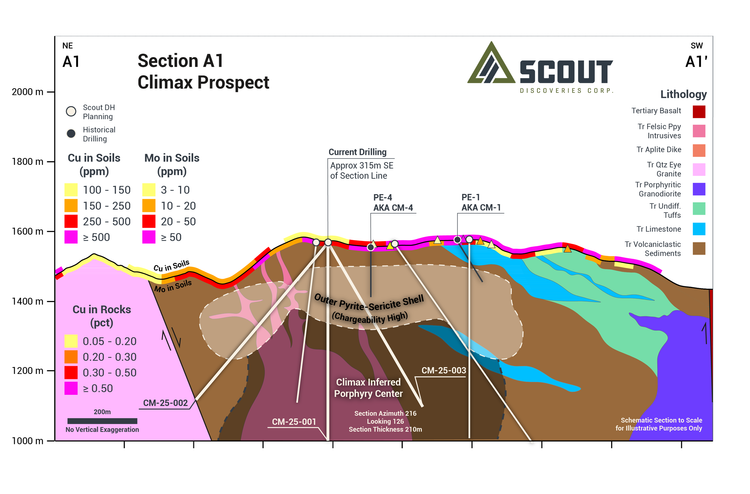

Coeur d’Alene, Idaho – January 15, 2026 – Scout Discoveries Corp. (“Scout” or the “Company”) is pleased to announce that drilling commenced at the Cuddy Mountain Project in late fall 2025 using one of the Company’s wholly owned drill rigs. This work is part of Scout’s planned Phase I core drilling program of up to 10,000 meters, detailed in the April 9th, 2025 news release. With the recent closing of Scout’s private placement (see January 5th, 2026 news release), the Company is now positioned to provide material updates on the drill program and other corporate developments.The ongoing Phase I drill program marks the first drilling at Cuddy Mountain in over 40 years. Drilling began at the Climax target (Figures 1 & 2) and will continue through the winter. Two completed holes and a third underway beneath the strong molybdenum soil anomaly at Climax shows it is a separate porphyry center from IXL. Assays are pending on both completed holes. Drill core observations reveal multiple porphyry intrusions, high-temperature alteration, and abundant sulfide-rich veins of varying generations ranging from early biotite halo, banded quartz molybdenite, magnetite, and sericite-chlorite-pyrite-(chalcopyrite) veins that are consistent with porphyry copper-molybdenum systems. Drilling will continue through the winter to vector toward inferred higher-temperature mineralization zones based on zoning observed to date.As snow melts in the spring, the Company plans to transition drilling to the IXL and Railroad targets while continuing work at Climax (Figures 1 & 2). Scout retains the flexibility to deploy additional rigs from its fleet of five surface core drills, should results warrant expanded drilling.

Curtis Johnson, Scout’s President and CEO commented, “The drill targets at Climax and IXL, including historic intercepts of 177 meters @ 0.34% Cu from surface with 40 meters @ 0.78% Cu, represent some of the most compelling near-surface porphyry targets in the broader Cuddy Mountain-Hercules mineral belt. This belt is emerging as the most significant new porphyry copper district discovered in the United States in well over 50 years. We look forward to utilizing our internally owned drills throughout 2026 to efficiently deploy shareholder capital and understand the full potential of the Cuddy Mountain project.”

Climax Target – Geologic Summary of Drilling to Date

The Climax area has emerged as one of the most compelling untested targets on the Cuddy Mountain project, having not been identified as a porphyry copper target prior to Scout’s 2024-2025 work programs. The Company utilized systematic geologic mapping, soil and rock geochemistry, and geophysics to guide drill targeting. Climax delivered impressive coincident IP, magnetic, and copper/molybdenum in soil anomalies in an area with newly discovered stockwork quartz-sulfide veining and multiple phases of porphyry dikes (Figures 1, 2, 3, and 4).

Drilling and Geology

Initial drilling of two variably oriented holes with a third ongoing, totaling 1,100 meters focused on testing the highest-magnitude portions of the molybdenum-in-soil anomaly (Figure 2) in multiple orientations. Drilling encountered poor ground conditions in highly faulted and fractured rock that necessitated short drill runs and persistent hole conditioning to maintain recovery and production.

The two completed drill holes (CM-25-001, 002) confirm the occurrence of multiple phases of intermediate to late-mineral quartz-feldspar porphyry dikes (Figure 5) exhibiting diverse degrees of sericite-chlorite alteration. These dikes intrude the adjacent andesitic volcanic, volcaniclastic, and carbonate wall rocks, which display a high abundance of sulfide-rich veins and mineralization with sericite-chlorite, potassic, and skarn alteration (Figure 5A-E). Multiple phases of porphyry intrusions and widespread sulfide-rich veining at Cuddy are consistent with many productive copper deposits. The observation that more high-temperature veins occur in wall rock than in drill-intersected intrusions suggests that early-mineral intrusions linked to copper-molybdenum mineralization are sourced at deeper levels or lateral to areas drilled.

Alteration patterns observed in drilling further reinforce the presence of a productive porphyry system at Climax. Magnetite-chlorite-sericite-pyrite alteration is pervasive throughout the volcanic wall rocks, while widespread epidote-garnet-magnetite-(pyrite-chalcopyrite) alteration affects both the volcanics, interbedded limestone, and segments of the porphyry intrusions, indicating strong and extensive hydrothermal fluid flow. Pyrite content ranges between 1-5% (up to 10%) with subordinate chalcopyrite present throughout the volcanics. Sulfide distribution correlates well with the intensity of the chargeability anomaly (Figure 4). Notably, banded quartz-molybdenite veins – hallmark features of porphyry systems – are present in all holes, reaching up to 1% by volume explaining the strong molybdenum soil anomaly (Figure 5A). This is complemented by biotite-selvage (“early halo type”) veins, garnet skarn, sericite selvages around pyrite-quartz veins, and trace to moderate chalcopyrite and native copper on fracture surfaces – all proximal indicators of porphyry systems.

Take-Aways and Future Drilling

Assays have not yet been received from the drilling completed to date, however, interpretation of geologic logging in the initial 1,100 meters of drilling confirms the presence of stockwork quartz veins, early halo veins, minor chalcopyrite with abundant pyrite, and banded quartz-molybdenite veins – classic indicators of proximal portions of a porphyry copper system (Figure 5B, G, H). The identification of molybdenum-rich veins, often found outboard of the high-copper shell in porphyry systems, suggests that current drilling may have intercepted a high-molybdenum shell adjacent to the center of the Climax porphyry system(s). Abundant sericite-chlorite alteration suggests drilling to date tested flanking or upper levels of the system. Increasing chalcopyrite-to-pyrite ratios in core toward areas with the highest-magnitude copper-in-soil (up to 0.2% copper) and molybdenum-in-soil values provide compelling evidence for potentially stronger mineralization in future holes.

IXL Porphyry Copper System – The Next Target to be DrilledThe IXL target contains a known outcropping of a Triassic porphyry copper-molybdenum system, where historic exploration work at Cuddy Mountain began in the 1950s. Mineralization is dominated by potassic alteration (secondary biotite, K-feldspar) associated with stockwork quartz-chalcopyrite-molybdenite veins and disseminated chalcopyrite, along with local mineralized breccias. A multi-kilometer copper and molybdenum-in-soil anomaly (Figure 2) coupled with strong chargeability highs outline a major porphyry system, which is what the Company believes lies concealed in the Climax target area. Recent detailed geologic mapping by Scout at IXL outlined a much broader area of “shreddy” secondary biotite (potassic) alteration containing copper than was previously recognized due to overprinting low-temperature chlorite alteration of biotite that prior operators interpreted as distal propylitic alteration unrelated to copper mineralization (Figure 1).Approximately 2,500 meters of shallow historical drilling was carried out by multiple operators at IXL in the 1950s to 1970s, with no known drilling completed since. As shown in the sections linked below, the majority of the newly identified soil and chargeability anomalies are poorly tested or untested by previous efforts. Most shallow holes in the IXL region intercepted broad zones of 0.1-0.3% Cu with associated molybdenite and no precious metals assays. The best historic interval is from hole AX-1, which intercepted from surface, 177 meters @ 0.34% Cu including 40 meters @ 0.78% Cu on the margin of a chargeability high. An underground adit was driven to explore this higher-grade sub-interval in the 1960s, which uncovered a mineralized breccia zone coring the potassic alteration with several underground holes identifying strong primary sulfide mineralization including 35 meters @ 1.23% Cu. Scout looks forward to testing these zones to depth and along strike in 2026.Refer to the following links for planned drill sections through the IXL target area showing geology, chargeability, and resistivity: IXL Target Geology, IXL Target Chargeability, IXL Target Resistivity.

Railroad Porphyry-Skarn TargetSimilar to the Climax target, the Railroad area has emerged as a compelling concealed target and potential third preserved porphyry center on the project following systematic exploration work by the Scout team. High-grade copper skarn mineralization was previously known in the area; however, detailed mapping has outlined a series of parallel, stacked skarn zones associated with mineralized porphyry dikes offering the potential for bulk tonnage copper mineralization at depth (Figure 1). Strong magnetic and chargeability anomalies at depth (Figure 2) further suggest potential for concealed porphyry style mineralization, which along with near surface skarn mineralization, will be the focus of exploration drilling in the target area in 2026-2027.Refer to the following links for sections through the Railroad target showing geology, chargeability, and resistivity: Railroad Target Geology, Railroad Target Chargeability, Railroad Target Resistivity.

About the Cuddy Mountain ProjectThe Cuddy Mountain Project is a porphyry copper-molybdenum (gold) project within the broader western Idaho copper belt. Scout identified the property as having potential in 2020 and acquired it through staking of open ground in 2021, prior to the discovery of the Leviathan porphyry on the adjacent Hercules property in 2023. Since that time, the Company has systematically advanced the large 12 square kilometer outcropping porphyry targets through detailed geologic mapping, surface geochemistry, geophysics and now the phase I drill program described herein.

About Scout Discoveries Corp.Scout Discoveries Corp., headquartered in Coeur d’Alene, Idaho, is a private U.S. mineral exploration company with rights to twelve separate precious and base metal projects in the western U.S.A., comprising one of the largest unpatented claim holdings in the region, totaling over 50,000 acres. Scout’s vision is to bring the full discovery process in-house from idea generation through resource drilling, lowering costs and increasing efficiency. With this model, the Company can rapidly advance its project portfolio through discovery by leveraging its five internal core drill rigs and experienced technical teams.For further information, visit: https://www.scoutdiscoveries.com/

Vancouver, British Columbia–(Newsfile Corp. – January 12, 2026) – Riverside Resources Inc. (TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY0) (“Riverside” or the “Company“), is pleased to outline its 2026 corporate outlook and work programs while highlighting key milestones achieved during 2025. Building on a year that saw the successful spin-out of Blue Jay Gold Corp., advancement of partner-funded work in Mexico, and a strategic investment of C$3.7 million which included Rick Rule and Sprott Wealth Management. Riverside now enters 2026 positioned to advance its key assets in the project generator and royalty portfolios.

Riverside maintains a solid balance sheet with strong cash, no debt and solid share structure with approximately 93 million shares outstanding following the December 2025 private placement. The recently completed non-brokered financing with strategic shareholders, including Rick Rule, Sprott Wealth Management, and Metallum, provides additional capital to advance key exploration, royalty, and transactional initiatives in 2026 while preserving the Company’s disciplined approach to share structure and capital allocation.

With a portfolio of projects in Canada and Mexico, a growing royalty platform anchored by Tajitos and Sugarloaf Peak (Arizona Metals Corp), and third-party funding from partners such as Questcorp Mining, Riverside will continue to focus on transactions and exploration programs that can create meaningful leverage for shareholders without overextending the treasury. This includes adding more assets this year, derisking key ones, and advancing partner-funded exploration programs as well as self-funded mineral exploration. Riverside also holds a portfolio of equity securities in partner and former partner companies which is separate from and in addition to the Company’s cash position.

“2025 was a pivotal year for Riverside as we delivered on several of the major objectives we laid out at the start of the year,” said John-Mark Staude, President and CEO of Riverside. “We completed the spin-out of Blue Jay Gold to our shareholders, marking the second time we have executed a successful spinout, the first being Capitan Silver, which also delivered a strong 2025 for its shareholders. Riverside secured an option agreement with Questcorp that funds exploration and first-phase drilling at the Union Project, and we strengthened our balance sheet through the completed strategic year-end financing. These actions place us in a strong position for 2026.”

“In 2026, we intend to keep doing what has worked for Riverside: emphasis on focused capital management, advance our best projects with our own capital and with third-party partner funding where prudent, and grow our royalty and equity portfolio exposure to potential discoveries and future value generation transactions. Our goal remains simple and opportunity-driven: to execute disciplined transactions, grow and advance our royalty interests, and pursue an exploration plan that fits Riverside’s model, while focusing on the best opportunities and working to deliver meaningful results over time.”

For an overview of Riverside’s 2025 progress and what we’re focused on heading into 2026, we encourage you to watch a short update video from President and CEO, John-Mark Staude. In the video, John-Mark highlights key milestones from the year, how our partner-funded model is advancing the portfolio, and the main priorities we’re working toward next.

Advance British Columbia Gold and REE Portfolio Continue systematic work at Red Jacket, Revel and Deer Park and related rare earth element and gold targets, with the objective of moving the British Columbia projects to more advanced exploration stages (including potential drill permitting, geophysics or partner exploration). The recent success of new mines in BC and higher commodity prices, combined with government and international strategic initiatives, makes for a good potential opportunity for Riverside.

In addition, China has implemented export controls and licensing requirements affecting certain rare earth materials, related products, and processing technologies, highlighting how concentrated and sensitive global REE supply chains remain. This reinforces why the Company intends to continue seeking REE opportunities that align with efforts to diversify supply and support strategic demand outside of China.

New Canadian Transactions Riverside plans to assess additional BC and other Canadian opportunities using Riverside’s database and technical team to secure attractive entry terms with the potential for future royalties and spinouts. In Q1, the Company intends to use a portion of the capital raised in December with strategic investors to add key tenures and continue to grow Riverside’s Canadian business.

2. Mexico Exploration and Partnerships

Union Project Complete assaying Union’s Phase 1 drilling program and plan the follow-up work to advance Union as the district-scale carbonate replacement region. The Company will continue exploring for gold and porphyry copper targets with Questcorp funding exploration under the option agreement.

Cecilia Project Advance the Cecilia Project following positive Q4 2024 drilling and 2025 follow-up targeting, interpretations program by integrating geophysics, structural modelling, and district-scale targeting to position the project for additional drilling and actively marketing it for an option or partnership. In light of recent positive statements and actions by the Mexican government, including the granting of new open-pit mining permits and titles, Riverside is stepping up its partner-seeking opportunities.

Advance and De-risk other Projects in Mexico Continue to progress and/or transact on the project portfolio through options, joint ventures, or asset sales, with the objective of providing shareholder return.

3. Royalty and Strategic Portfolio Growth

Leverage Existing Royalties Riverside’s royalty portfolio is anchored by its 2% NSR on the Tajitos Gold Project operated by Fresnillo and the Sugarloaf Peak gold project operated by Arizona Metals, where ongoing technical and permitting work by the operators could move these assets closer to future production decisions, with further leveraged upside from royalties on Capitan Silver’s Cruz de Plata Project and Blue Jay Gold’s Ontario properties.

Originate New Royalties through Transactions Structure new deals in Canada, Mexico and potentially in US jurisdictions where Riverside can retain NSRs and/or equity while transferring a portion of the capital burden to partners. Expanding the royalty portfolio including using the strong capital position of the Company.

4. Corporate Development & Capital Markets

Disciplined Deployment of New Capital Allocate the December 2025 financing proceeds into focused work programs and corporate development, prioritizing opportunities with clear value catalysts in an effort to deliver shareholders further potential returns.

Active Market Presence Continue regular outreach through conferences and targeted meetings, including key 2026 sector events, to broaden Riverside’s shareholder base and support liquidity. Attending key conferences including AME Roundup in Vancouver, January 26-29, 2026, and PDAC in Toronto, March 1-4, 2026.

2025 Recap and Highlights

Canada

Blue Jay Gold Spin-out and Ontario Portfolio Riverside completed the spin-out of Blue Jay Gold Corp. under a court-approved plan of arrangement, distributing one Blue Jay share and one new Riverside share for every five Riverside shares held on the May 22, 2025 effective date. This transaction gave Riverside shareholders direct exposure to a dedicated gold explorer while Riverside retained a royalty on Blue Jay’s Ontario property portfolio.

British Columbia – Gold and REE Projects Riverside advanced its BC portfolio with ongoing work at Red Jacket, Deer Park, Revel, and related projects, confirming strong analogues to the historic Yellowhead mining camp for Red Jacket and the Rossland mining camp at Deer Park as well as outlining a 12-kilometre-long carbonatite-style rare earth system at Revel that remains undrilled.

Mexico

Cecilia Gold Project Riverside reported positive results from the Q4 2024 drill program at Cecilia, which tested multiple targets. These holes provided geologic context and allow for the next phase of exploration work at the: San Jose vein system, East Target, Mayra Vein and South Mesa Fault among other targets. Most of the targets drilled in 2025 returned encouraging geological and gold indicators, confirming a large, low-sulphidation epithermal system.

The 2025 work focused on integrating structural, geochemical and geophysical data to better understand the scale and orientation of mineralization and expanded the targets setting the project up for the next exploration work.

Union Project – Questcorp Option & First-Year Work Riverside executed a definitive option agreement with Questcorp Mining (QQQ.CSE) on the 2,520-hectare Union Project in Sonora. The agreement provides for up to C$5.5 million in exploration expenditures and a staged path for Questcorp to earn in, while Riverside retains a royalty and became a shareholder of Questcorp. Under the terms of the agreement, Riverside will act as the exploration Operator for the project.

Questcorp issued 6,285,722 shares to Riverside (9.9% of Questcorp) and made cash payments. Following this, Riverside’s Mexico-based team began pre-drilling preparations, including contractor selection and geophysics to refine drill targets in the CRD-porphyry system. In late 2025, Riverside and Questcorp completed a partner-funded Phase 1 drill campaign of 12 holes totaling over 1,600 metres at Union, with assays pending for the first quarter of 2026.

Other Mexican Assets and Royalties The Company continued to advance its broader Mexican portfolio, including Cuarentas (drill permitted), Valle and the Ariel porphyry copper prospects, maintaining optionality for future joint ventures, sales or additional royalties.

Riverside’s royalty portfolio remained an important part of the value proposition, including the 2% NSR on the Tajitos Gold Project operated by Fresnillo and the 2% NSR on Arizona Metals’ Sugarloaf Peak gold project in Arizona, both of which continued to see operator-led technical and evaluation work through 2025.

Corporate & Financial

On December 1, 2025, Riverside closed a C$3.7 million non-brokered private placement with long-term strategic investors which included Rick Rule, Sprott Wealth Management and Metallum. The 18,460,000 units included half-warrants exercisable at C$0.30 for two years, adding potential future capital while keeping the structure straightforward. Following the financing, Riverside has 93 million shares outstanding and no debt, providing flexibility for 2026 programs and transactions.

Qualified Person & QA/QC The scientific and technical information contained in this news release has been reviewed and approved by Freeman Smith, P.Geo, a non-independent qualified person to Riverside Resources, who is responsible for ensuring that the geologic and technical information provided in this news release is accurate and who acts as a “qualified person” under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Riverside Resources Inc. Riverside is a well-funded exploration company driven by value generation and discovery. The Company has a solid balance sheet with no debt and tight share structure with a strong portfolio of gold-silver, copper and REE assets and royalties in North America. Further information about Riverside is available on the Company’s website at www.rivres.com.

ON BEHALF OF THE BOARD OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Investor Relations Riverside Resources Inc. Eric@rivres.com Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release contain forward-looking information. Forward-looking information involves risks, uncertainties and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking information. In addition, the forward-looking statements require management to make assumptions and are subject to inherent risks and uncertainties. There is significant risk that the forward-looking statements will not prove to be accurate, that the management’s assumptions may not be correct and that actual results may differ materially from such forward-looking statements. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Forward-looking statements contained in this press release may include, but are not limited to, use of proceeds, obtaining regulatory approval for the Offering and future business plans of the Company. Such information involves known and unknown risks, including the receipt of regulatory approval, the results of future financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.Except as required by applicable securities laws and regulation, Riverside disclaims any intention or obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Vancouver, British Columbia–(Newsfile Corp. – November 24, 2025) – Elemental Royalty Corporation (TSXV: ELE) (Nasdaq: ELE) (“Elemental” or the “Company“) is pleased to announce that its common shares will commence trading on the Nasdaq Capital Market (“Nasdaq“) at market open tomorrow under the ticker symbol “ELE”. Elemental’s common shares will continue to trade on the TSX Venture Exchange under the ticker symbol “ELE”.

David M. Cole, Chief Executive Officer of Elemental, commented: “We are delighted that Elemental shares have been approved for trading on Nasdaq, an important milestone for our newly merged company. This listing will allow our shareholders to trade more easily and provide exposure to a significantly broader base of institutional and retail investors. We expect this listing to enhance trading liquidity, increase coverage from U.S. investment banks, and create opportunities for potential index inclusion.”

Concurrent with the commencement of trading on Nasdaq, Elemental’s common shares will cease to be quoted on the OTCQX Best Market. Shareholders are not required to take any action; however, shareholders who purchased shares on OTCQX are encouraged to monitor their brokerage accounts to ensure holdings are correctly reflected in respect of the Nasdaq listing.

The listing does not involve any concurrent financing, and no new shares were issued.

TSXV: ELE | NASDAQ: ELE | ISIN: CA28619K1093 | CUSIP: 28619K109

About Elemental Royalty Corporation.

Elemental Royalty is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 16 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental Royalty trades on the TSX Venture Exchange and on Nasdaq under the ticker “ELE”.

Neither the TSXV nor its Regulation Service Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this press release.

This news release contains certain “forward-looking statements” and certain “forward-looking information” as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar terminology.

Forward-looking statements and information include, but are not limited to, statements with respect to the expected benefits of the Nasdaq listing, the Company’s ability to execute its growth strategy, future revenue and cash-flow profile, and the acquisition of additional royalties and streams. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable, and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental to control or predict, that may cause Elemental’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions, the absence of control over the mining operations from which Elemental will receive royalties, risks related to international operations, government relations and environmental regulation, the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results will not be consistent with Elemental’s expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental for the year ended December 31, 2024. Elemental undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represents management’s best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Edmonton, Alberta–(Newsfile Corp. – November 25, 2025) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) is pleased to announce a private placement offering of Units and FT Units for gross proceeds of up to $1 Million if fully subscribed (the “Offering”).

Private Placement Offering

The Offering consists of up to 8,333,333 Units and up to 25,000,000 of any combination of Units and FT Units, each priced at $0.03 per Unit or FT Unit. Each Unit shall consist of one common share of the Company (“Common Share”) and one Common Share purchase warrant entitling the warrant holder to purchase an additional Common Share for $0.05 and expiring on the earlier of a) 30 days following written notice by the Company to the warrant holder that the volume-weighted average trading price of the Common Shares on the TSX Venture Exchange is at or greater than CA$0.10 per Common Share for 10 consecutive trading days; and (b) 24 months from the date of issuance (“Warrant”). Each FT Unit shall consist of one Common Share and one half of one Warrant, each of which shall be issued as a “flow through share” for the purposes of the Income Tax Act (Canada). The Offering is being offered to qualified subscribers in the Provinces of Alberta, British Columbia and Ontario and in other jurisdictions as the Company may in its discretion determine, in reliance upon exemptions from the registration and prospectus requirements of applicable securities legislation.

The Company intends to use the proceeds of the Offering, if fully subscribed with the maximum of 25,000,000 in FT Units and 8,333,333 Units, as follows:

Mineral Property Exploration

$

750,000

Mineral Rights and Exploration Permits

35,000

Working capital

Outstanding management fees to Officers

$

32,000

Other accounts payable

47,000

79,000

Corporate Overhead

Management fees to Officers

$

24,000

(Approx. 4 months)

Other Corporate Overhead

112,000

136,000

Maximum proceeds

$

1,000,000

There is no minimum to the Offering. If the Company closes on less than the maximum proceeds, or if the proportion of Units and FT Units differs from the above, the use of proceeds will be adjusted.

In connection with the Offering, the Company may pay finders fees payable in any combination of cash, Units, and Warrants to registered broker dealers, limited market dealers or arm’s length persons in accordance with the policies of the TSX Venture Exchange (the “Exchange”) and applicable securities legislation and regulations. The Common Shares and any Common Shares issued on exercise of the Warrants are subject to restrictions on trading until four months and one day from the date of issuance in accordance with the policies of the Exchange.

The Offering is subject to acceptance of the TSX Venture Exchange.

ABOUT GRIZZLY DISCOVERIES INC.

Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and base metals properties in southeastern British Columbia. Grizzly is run by highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.

On behalf of the Board,

GRIZZLY DISCOVERIES INC. Brian Testo, CEO, President

Suite 363-9768 170 Street NW Edmonton, Alberta T5T 5L4

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Caution concerning forward-looking information

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward-looking information. Such forward-looking information and statements are frequently identified by words such as “may,” “will,” “should,” “anticipate,” “plan,” “expect,” “believe,” “estimate,” “intend” and similar terminology, and reflect assumptions, estimates, opinions and analysis made by management of Grizzly in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Grizzly’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon.

Risks and uncertainties that may cause actual results to vary include but are not limited to the availability of financing; fluctuations in commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedarplus.ca. Grizzly disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

NOT FOR DISSEMINATION IN THE UNITED STATES OF AMERICA

From defense-backed breakthroughs to scalable commercial launches, General Hypersonics is pioneering affordable, reusable hypersonics and next-generation space flight.

SPOKANE, WA AND AUSTIN, TX / ACCESS Newswire / September 22, 2025 / HyperSciences, Inc., dba General Hypersonics Corp. (General Hypersonics), today announced a world-first achievement under its U.S. Department of Defense (DoD) Phase II Small Business Innovation Research (SBIR) contract. This small business technology company is setting world records with a new rocketless launch platform. It successfully completed horizontal flight tests exceeding Mach 3 carrying electronic payloads and demonstrating groundbreaking payload separation capabilities from its horizontal ram accelerator, a novel tube-launch system, the Hypersonic Accelerator for Versatile Operational Kinetics (HAVOK). This breakthrough marks a critical step toward commercializing its reusable, low-cost hypersonic long-range and suborbital launch platform for defense and space missions.

The current DoD contract builds on a successful NASA Phase I effort that demonstrated the scalability of General Hypersonics launch platform for larger payloads. Purpose-built for aerospace applications, the HAVOK system’s unique capabilities were advanced through industrial drilling and tunneling research and development, where thousands of high impact launches validated its performance, precision, scalability, and affordability. Recent demonstrations confirm the company is on track to deliver rocketless, responsive, high-cadence suborbital access in 2026, with orbital launches targeted the following year.

World-First Ram Accelerator Achievements by General Hypersonics

Turnkey Hot-Fire of Ram Accelerator: First successful hot-fire of a ram accelerator tube, originally adapted for industrial drilling and then refined for space launch.

Ram Start with Heaviest Projectile Ever Accelerated: Achieved ignition and sustained flight with the highest mass for this scale projectile ever successfully ram-accelerated, demonstrating full-flight scalability with highest-density ram acceleration.

First Payload-Carrying Flight Through Ram Accelerator: Flew onboard electronics at hypersonic speeds above Mach 3.

Clean Separation of “Space Dart”: Demonstrated first ever smooth, mid-flight separation of a “Space Dart” payload within the launch tube-demonstrating feasibility to deploy hypersonic payloads, testing, targets, drones, and other payloads using a novel precision sabot system.

Technology Background and Significance

The ram accelerator is a rocketless propulsion platform that uses clean gases to accelerate payloads to hypersonic speeds. First conceived at the University of Washington, it was adapted by General Hypersonics for deep-earth industrial drilling and tunneling utilizing high speed impact. Validated through thousands of industrial field tests, the company has now refined the system for defense and space launches. Recent “hot-fire” field tests at the company’s hypersonic test-bed facility demonstrate its potential as a reusable, scalable, and cost-effective launch solution.

Advancing Toward Suborbital and Orbital Readiness

General Hypersonics’ Mach 5+ Space Dart demonstration, scheduled for Q4 2025, will advance its reusable system toward space readiness. In 2026, the company plans more world-first demonstrations: launching payloads from the HAVOK tube-launch system to the Kármán line (100 km) and repeating suborbital deliveries to validate affordability, reusability, and high-frequency launch capability – without a first-stage rocket.

“This disruptive propulsion technology can launch space and defense missions from land or sea,” said Mark Russell, CEO and Founder. “These results confirm our system’s scalability for both space and national security missions while opening doors to an entirely new class of hypersonic and space applications – at dramatically lower cost and faster launch rates. We intend to create a little ‘HAVOK’ as competitors try to keep up!“

General Hypersonics is creating a new way to reach space – affordable, frequent launches set to begin serving customers in 2026.

Aligned with the U.S. hypersonic and space strategies and backed by DoD programs, proven milestones, a strong IP base, and a veteran team of aerospace experts, General Hypersonics invites select partners and investors to help drive the future of next-generation, affordable, and high-frequency launch solutions. For details, contact: info@hypersciences.com

Media & Investor Contact

HyperSciences (dba General Hypersonics) 2311 E Main Ave, Ste 200, Spokane, WA 99202 (509) 443-5746 info@hypersciences.com