Dr. Amy Wax recently appeared on Tucker Carson’s show, in which she called India a shithole. In the following talk with RBM, I disagree. India is a rotting, bubbling shithole that is rapidly falling apart under the rule of a thoroughly incompetent, crooked, and venal bunch of politicians and bureaucrats, who are backed by tribal, superstitious masses:

These days, on a daily basis people get arrested in India for posting anything negative about Modi, the PM of India. A friend, a freedom-fighter, and the National Vice President of Swatantra Bharat Party, the only libertarian party in India, Sanjay Garg, has been arrested without bail by the Indian government apparently for his social media posts. He has been deemed to be such a terrorist that the police report has not been made public.

On Investments

GCM Mining Warrant (GCM.WT.B; C$1.83) has fallen significantly over the last few weeks, perhaps because of the fear to do with the likelihood that the next president of Colombia might be a leftist. While this might happen, my view is that the market valuation of the company is sufficiently underpinned by its project in Guyana and the stock investments it has. Its investments with a marked-to-the-market value on 31st March 2022 of C$160 million have gone up by about 15%, something the market has perhaps forgotten to take note of. The Colombian project continues to make a good profit, which enables a 4.5% dividend yield.

Disclaimer: All information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, expressed or implied herein, are for informational, entertainment, or educational purposes only and should not be construed as personal investment advice. While the information provided is believed to be accurate, it may include errors or inaccuracies. The sole purpose of these musings is to show my thinking process when analyzing a stock, not to provide any recommendation. I will not and cannot be held liable for any actions you take as a result of anything you read here. Conduct your own due diligence, or consult a licensed financial advisor or broker before making any and all investment decisions. Any investments, trades, speculations, or decisions made on the basis of any information found on this site, expressed or implied herein, are committed at your own risk, financial or otherwise.

VANCOUVER, BC / ACCESSWIRE / June 9, 2022 / Sandy MacDougall, CEO of Noram Lithium Corp. (“Noram” or the “Company“) (TSXV:NRM | OTCQB:NRVTF | Frankfurt:N7R) is pleased to announce the successful completion of CVZ-77 (PH-04) and CVZ-78 (PH-11) and release of the final assay results. The Company completed core hole CVZ-77 at a depth of 458 feet (139.6 m). Sampling for assays began at 20 ft (6.1 m) and continued to the bottom of the hole, an interval thickness of 240 ft (73.2 m) was intersected from 48 ft (14.6 m) to 288 ft (87.8 m). The weighted average lithium values present are summarized below with a high of 2140 ppm. The Company completed core hole CVZ-78 at a depth of 451.5 feet (137.6 m). Sampling for assays began at 26.8 ft (8.2 m) and continued to the bottom of the hole, an interval thickness of 231.3 ft (70.5 m) was intersected from 26.8 ft (8.2 m) to 258 ft (78.6 m). The weighted average lithium values present are summarized below with a high of 2100 ppm present.

Noram Lithium Corp., Thursday, June 9, 2022, Press release picture

Noram Lithium Corp., Thursday, June 9, 2022, Press release picture

Figure 1 – Location of all past drill holes (Phase I to Phase V) previously completed in addition to the 12 proposed holes for Phase V1. Phase VI holes are indicated in purple.

Noram Lithium Corp., Thursday, June 9, 2022, Press release picture

Figure 2. Comparative stratigraphy and assay results for drill holes CVZ-77 and CVZ-78 as compared to CVZ-65 which was drilled as part of a prior program. The histogram on the sides of the holes are the composited lithium grades in ppm Li. The cross section has a 4X vertical exaggeration.

“As we continue to receive results that meet and/or surpass our expectations, our level of confidence in the resource model continues to increase. This program is providing us with vital information that will allow us to upgrade a significant portion of the resource from the Inferred Category to the Indicated Category. We could not be more proud of the team we have diligently advancing the Project. Noram management is focused on enhancing shareholder value as we continue to develop the resource” comments Brad Peek, VP of Exploration and geologist on all six phases of Noram’s Clayton Valley exploration drilling.

Hole ID

Sample No.

From (ft)

To (ft)

From (m)

To (m)

Li (ppm)

CVZ-77

1748459

20

28

6.1

8.5

610

CVZ-77

1748460

28

38

8.5

11.6

850

CVZ-77

1748461

38

48

11.6

14.6

870

CVZ-77

1748462

48

58

14.6

17.7

1010

CVZ-77

1748463

58

68

17.7

20.7

840

CVZ-77

1748464

68

78

20.7

23.8

910

CVZ-77

1748465

78

88

23.8

26.8

840

CVZ-77

1748466

88

98

26.8

29.9

940

CVZ-77

1748467

98

108

29.9

32.9

600

CVZ-77

1748468

108

118

32.9

36.0

1160

CVZ-77

1748469

118

128

36.0

39.0

980

CVZ-77

1748471

128

138

39.0

42.1

1540

CVZ-77

1748472

138

148

42.1

45.1

1340

CVZ-77

1748473

148

158

45.1

48.2

1400

CVZ-77

1748474

158

168

48.2

51.2

1510

CVZ-77

1748475

168

178

51.2

54.3

1860

CVZ-77

1748476

178

188

54.3

57.3

2140

CVZ-77

1748477

188

198

57.3

60.4

1300

CVZ-77

1748478

198

208

60.4

63.4

1290

CVZ-77

1748479

208

218

63.4

66.4

1450

CVZ-77

1748480

218

228

66.4

69.5

1630

CVZ-77

1748481

228

238

69.5

72.5

1250

CVZ-77

1748482

238

248

72.5

75.6

1060

CVZ-77

1748483

248

258

75.6

78.6

1080

CVZ-77

1748484

258

268

78.6

81.7

950

CVZ-77

1748485

268

278

81.7

84.7

1020

CVZ-77

1748486

278

288

84.7

87.8

990

CVZ-77

1748487

288

298

87.8

90.8

790

CVZ-77

1748488

298

308

90.8

93.9

620

CVZ-77

1748489

308

318

93.9

96.9

870

CVZ-77

1748490

318

328

96.9

100.0

760

CVZ-77

1748491

328

338

100.0

103.0

430

CVZ-77

1748492

338

348

103.0

106.1

610

CVZ-77

1748493

348

358

106.1

109.1

550

CVZ-77

1748494

358

368

109.1

112.2

550

CVZ-77

1748495

368

378

112.2

115.2

720

CVZ-77

1748496

378

388

115.2

118.3

540

CVZ-77

1748497

388

398

118.3

121.3

790

CVZ-77

1748498

398

408

121.3

124.4

780

CVZ-77

1748499

408

418

124.4

127.4

600

CVZ-77

1748500

418

428

127.4

130.5

550

CVZ-77

1748501

428

438

130.5

133.5

500

CVZ-77

1748502

438

448

133.5

136.6

379

Table 1 – Sample results from CVZ-77 from 20 ft (6.1 m) to depth of 448 ft (136.6 m).

Hole ID

Sample No.

From (ft)

To (ft)

From (m)

To (m)

Li (ppm)

CVZ-78

1748508

26.75

37.25

8.2

11.4

920

CVZ-78

1748509

37.25

48

11.4

14.6

1090

CVZ-78

1748510

48

58

14.6

17.7

910

CVZ-78

1748511

58

68

17.7

20.7

910

CVZ-78

1748512

68

78

20.7

23.8

980

CVZ-78

1748513

78

88

23.8

26.8

2100

CVZ-78

1748514

88

98

26.8

29.9

1160

CVZ-78

1748515

98

108

29.9

32.9

1190

CVZ-78

1748516

108

118

32.9

36.0

1640

CVZ-78

1748517

118

128

36.0

39.0

1830

CVZ-78

1748518

128

138

39.0

42.1

1240

CVZ-78

1748519

138

148

42.1

45.1

1180

CVZ-78

1748520

148

158

45.1

48.2

1380

CVZ-78

1748521

158

168

48.2

51.2

1350

CVZ-78

1748522

168

178

51.2

54.3

1280

CVZ-78

1748523

178

188

54.3

57.3

1000

CVZ-78

1748524

188

198

57.3

60.4

1060

CVZ-78

1748525

198

208

60.4

63.4

910

CVZ-78

1748527

208

218

63.4

66.4

960

CVZ-78

1748528

218

228

66.4

69.5

1020

CVZ-78

1748529

228

238

69.5

72.5

830

CVZ-78

1748530

238

248

72.5

75.6

580

CVZ-78

1748531

248

258

75.6

78.6

1110

CVZ-78

1748532

258

268

78.6

81.7

790

CVZ-78

1748533

268

278

81.7

84.7

650

CVZ-78

1748534

278

288

84.7

87.8

750

CVZ-78

1748535

288

298

87.8

90.8

890

CVZ-78

1748536

298

308

90.8

93.9

680

CVZ-78

1748537

308

318

93.9

96.9

730

CVZ-78

1748538

318

328

96.9

100.0

930

CVZ-78

1748539

328

338

100.0

103.0

740

CVZ-78

1748540

338

348

103.0

106.1

720

CVZ-78

1748541

348

358

106.1

109.1

560

CVZ-78

1748542

358

368

109.1

112.2

490

CVZ-78

1748543

368

378

112.2

115.2

560

CVZ-78

1748544

378

388

115.2

118.3

560

CVZ-78

1748545

388

398

118.3

121.3

670

CVZ-78

1748546

398

408

121.3

124.4

660

CVZ-78

1748547

408

418

124.4

127.4

460

CVZ-78

1748548

418

428

127.4

130.5

460

CVZ-78

1748549

428

438

130.5

133.5

530

CVZ-78

1748550

438

447

133.5

136.2

388

CVZ-78

1748551

447

451.5

136.2

137.6

399

Table 2 – Sample results from CVZ-78 from 26.8 ft (8.2 m) to depth of 451.5 ft (137.6 m).

All samples were analyzed by the ALS laboratory in Reno, Nevada. QA/QC samples were included in the sample batch and returned values that were within their expected ranges.

The technical information contained in this news release has been reviewed and approved by Brad Peek., M.Sc., CPG, who is a Qualified Person with respect to Noram’s Clayton Valley Lithium Project as defined under National Instrument 43-101.

About Noram Lithium Corp.

Noram Lithium Corp. (TSXV:NRM | OTCQB:NRVTF | Frankfurt:N7R) is a well-financed Canadian based advanced Lithium development stage company with less than 90 million shares issued and a fully funded treasury. Noram is aggressively advancing its Zeus Lithium Project in Nevada from the development-stage level through the completion of a Pre-Feasibility Study in 2022.

The Company’s flagship asset is the Zeus Lithium Project (“Zeus”), located in Clayton Valley, Nevada. The Zeus Project contains a current 43-101 measured and indicated resource estimate* of 363 million tonnes grading 923 ppm lithium, and an inferred resource of 827 million tonnes grading 884 ppm lithium utilizing a 400 ppm Li cut-off. In December 2021, a robust PEA** indicated an After-Tax NPV(8) of US$1.3 Billion and IRR of 31% using US$9,500/tonne Lithium Carbonate Equivalent (LCE). Using the LCE long term forecast of US$14,000/tonne, the PEA indicates an NPV (8%) of approximately US$2.6 Billion and an IRR of 52% at US$14,250/tonne LCE.

Sandy MacDougall Chief Executive Officer and Director C: 778.999.2159

For additional information please contact: Peter A. Ball President and Chief Operating Officer peter@noramlithiumcorp.com C: 778.344.4653

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release. This news release may contain forward-looking information which is not comprised of historical facts. Forward-looking information involves risks, uncertainties and other factors that could cause actual events, results, performance, prospects and opportunities to differ materially from those expressed or implied by such forward-looking information. Forward-looking information in this news release includes statements regarding, among other things, the completion transactions completed in the Agreement. Factors that could cause actual results to differ materially from such forward-looking information include, but are not limited to, regulatory approval processes. Although Noram believes that the assumptions used in preparing the forward-looking information in this news release are reasonable, including that all necessary regulatory approvals will be obtained in a timely manner, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. Noram disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by applicable securities laws. *Updated Lithium Mineral Resource Estimate, Zeus Project, Clayton Valley, Esmeralda County, Nevada, USA (August 2021) **Preliminary Economic Assessment Zeus Project, ABH Engineering (December 2021).

Vancouver, British Columbia–(Newsfile Corp. – June 9, 2022) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX“) is pleased to announce that it will receive a royalty payment of approximately US$2.7 million (pre-tax) from the Company’s effective 0.7335% net smelter return royalty (“NSR“) interest covering the Caserones Copper-Molybdenum Mine (“Caserones“) in Chile. This royalty payment distribution to EMX, anticipated later this month, is based upon first quarter (“Q1”) (i.e., January-March, 2022) copper and molybdenum production.

EMX initially acquired a 0.418% NSR royalty interest on Caserones in 2021 and acquired an additional 0.3155% NSR royalty interest in April of this year, bringing the Company’s total (effective) NSR royalty interest to 0.7335% (see EMX news release dated April 14, 2022). Although the recent royalty purchase was completed after the end of Q1, the agreement contained provisions for EMX to receive the Q1 distributions for the newly acquired interest. This new royalty interest (0.3155% NSR) accounted for US$1.2 million of the US$2.7 million (pre-tax) Q1 total. The higher-than-expected Q1 royalty distributions reflect strong copper prices and robust production throughput at higher grades.

In addition to Caserones, EMX receives production royalty payments from its Leeville royalty in Nevada, and expects addition cash flow in 2022 from the Cukaru Peki Mine in the Bor Mining District in Serbia, as well as the Gediktepe and Bayla royalty properties in Turkey. Together, these interests provide commodity diversity that includes base metals (i.e., copper, molybdenum, lead, and zinc) and precious metals (i.e., gold and silver) in key mining districts of Chile, the U.S., Serbia, and Turkey.

Since the acquisition of the initial royalty interest at Caserones, royalty distributions to EMX total US$6.3 million (pre-tax). This has provided meaningful positive cash flow in a very short time (four quarters). This performance reflects the quality of Caserones as a cornerstone Company asset that resulted from EMX’s royalty acquisition initiatives.

EMX has a unique approach to the royalty business which is based upon a combination of royalty purchases, sustainable organic royalty growth, and strategic investments. Royalties are financial instruments that grow in value via ongoing investments by operators, and at no expense to royalty holders. This upside optionality occurs throughout the life cycle of a royalty as further exploration leads to resource and reserve growth, while technological and engineering advancements lead to more efficient mining, all to the benefit of royalty holders. As inflation fears have roiled global financial markets in 2022, this is a time when royalties stand out the most, with no exposure to exploration, production, and development cost increases yet full exposure to commodity price inflation. As a result, royalties are a key hedge that will become increasingly important as the current inflationary cycle plays out.

Caserones Overview. The Caserones open pit mine is developed on a significant porphyry copper-molybdenum deposit in the Atacama Region of northern Chile’s Andean Cordillera, 162 kilometers southeast of the city of Copiapó. The mine has been in operation since 2014, and is owned and operated by SCM Minera Lumina Copper Chile SpA (“Minera Lumina”), which is 100% indirectly owned by JX Nippon Mining & Metals Corporation of Japan.

Caserones produces copper and molybdenum concentrates from a conventional crusher, mill and flotation plant, as well as copper cathodes from a dump leach, solvent extraction and electrowinning plant. The mine produced 94,846 tonnes of fine copper in concentrate, 2,287 tonnes of fine molybdenum in concentrate, and 14,829 tonnes of fine copper in cathodes in 20211.

In addition to currently defined zones of mineralization, considerable exploration upside exists on the Caserones property, and exploration for additional resources has been ongoing and continues at present.

Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and an employee of the Company, has reviewed, verified, and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”, and also trade on the Frankfurt Stock Exchange under the symbol “6E9”. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 973-8585 Dave@EMXroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@EMXroyalty.com

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding completion of the transaction, perceived merits of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential”, “upside” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors. It is possible EMX may not complete the transaction, as a result of failure to fulfill conditions of closing, unavailability of financing or for other reasons EMX cannot anticipate at this time.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended March 31, 2022 (the “MD&A”), and the most recently filed Annual Information Form (the “AIF”) for the year ended December 31, 2021, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and Financial Statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

VANCOUVER, BC / ACCESSWIRE / June 9, 2022 / Metallic Minerals (TSX.V:MMG)(OTCQB:MMNGF) (“Metallic Minerals“, or the “Company“) is pleased to report that it has closed its previously announced non-brokered private placement financing for aggregate proceeds of $4,032,000 through the issuance of 9,600,000 units at a price of $0.42 per flow-through unit (the “Private Placement”). Each Unit consists of one flow-through common share and one-half purchase warrant where each whole warrant is exercisable into a flow-through common share for 30 months at a price of $0.50 on the TSX Venture Exchange (“TSX-V”).

Greg Johnson, CEO and Chairman, noted, “We are pleased to complete this premium-to-market Private Placement and to strengthen our shareholder base with new institutional investors. These new funds will be primarily directed toward the ongoing exploration and development of our Keno Silver Project in the high-grade, Keno silver district of Canada’s Yukon Territory. Final planning is underway for the initiation of our 2022 exploration programs at Keno Silver, as well as at our La Plata silver-gold-copper project in Colorado, USA. We look forward to meeting with existing and potential shareholders during PDAC 2022 in Toronto June 13-15, as well as during the Yukon Property Tours and Conference June 20-24 in Dawson City.”

Proceeds from the Private Placement will be used toward eligible Canadian Exploration Expenses, within the meaning of the Income Tax Act (Canada). The Private Placement is subject to the final approval of the TSX-V. The flow-through shares will be subject to a hold period of four months and one day from their date of issuance under applicable Canadian securities law.

The flow-through shares have not been, and will not be, registered under the U.S. Securities Act or any U.S. state securities laws, and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons absent registration or any applicable exemption from the registration requirements of the U.S. Securities Act and applicable U.S. state securities laws.

An officer of the Company participated in the private placement for an aggregate of 4,400 FT Units. The participation by the insider in the private placement is considered to be a related-party transaction as defined under Multilateral Instrument 61-101. The transaction is exempt from the formal valuation and minority shareholder approval requirements of MI 61-101, as neither the fair market value of the securities being issued, nor the consideration being paid exceeds 25% of the Company’s market capitalization.

Upcoming Events

PDAC 2022 – Metallic will join fellow Metallic Group members, Stillwater Critical Minerals (formerly Group Ten Metals) and Granite Creek Copper, at PDAC in Toronto, June 13-15 (Booth IE2851).

Yukon Property Tours & Conference – Metallic will be in Dawson City June 20-24 for the 2022 Yukon Property Tours, with President, Scott Petsel, and CEO, Greg Johnson, both visiting the Keno Silver Project for exploration planning.

About Metallic Minerals

Metallic Minerals Corp. is an exploration and development stage company, focused on silver, gold and copper in the high-grade Keno Hill and La Plata mining districts of North America. Our objective is to create shareholder value through a systematic, entrepreneurial approach to making exploration discoveries, growing resources and advancing projects toward development. Metallic Minerals has consolidated the second-largest land position in the historic Keno Hill silver district of Canada’s Yukon Territory, directly adjacent to Alexco Resource Corp’s operations, with more than 300 million ounces of high-grade silver in past production and current M&I resources. In addition, the Company recently announced the inaugural resource estimate for the La Plata silver-gold-copper project in southwestern Colorado. All of the districts in which the Company works have seen significant mineral production and have existing infrastructure, including power and road access. Metallic Minerals is led by a team with a track record of discovery and exploration success on several major precious and base metal deposits, as well as having large-scale development, permitting and project financing expertise.

About the Metallic Group of Companies

The Metallic Group is a collaboration of leading precious and base metals exploration and development companies, with a portfolio of large, brownfields assets in established mining districts adjacent to some of the industry’s highest-grade producers of silver and gold, platinum and palladium, and copper. Member companies include Metallic Minerals in the Yukon’s high-grade Keno Hill silver district and La Plata silver-gold-copper district of Colorado, Granite Creek Copper in the Yukon’s Minto copper district, and Stillwater Critical Minerals (formerly Group Ten Metals) in the Stillwater PGM-nickel-copper district of Montana, USA and Kluane district in the Yukon. The founders and team members of the Metallic Group include highly successful explorationists formerly with some of the industry’s leading explorer/developers and major producers. With this expertise, the companies are undertaking a systematic approach to exploration and development using new models and technologies to facilitate discoveries in these proven, but under-explored, mining districts. Members of the Metallic Group have been recognized as recipients of awards for excellence in environmental stewardship demonstrating commitment to responsible resource development and appropriate ESG practices. The Metallic Group is headquartered in Vancouver, BC, Canada, and its member companies are listed on the Toronto Venture, US OTCQB and Frankfurt stock exchanges.

Forward Looking Statements: This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Metallic Minerals believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Metallic Minerals and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Integrous- Oil & Gas- Drilling & Exploration- The Answer to Supply-Side Inflation

Crude oil at the highest price since 2008- Inventories and product prices support higher highs

Natural gas is also at a fourteen-year high- Inventories, and European prices support the continuation of a very volatile bull market

The four reasons for higher fossil fuel prices- SPR releases are a temporary band-aid

Drilling and exploration are the answer to supply-side economic woes

XOP outperforming the stock market in 2022- The trend is your best friend

Throughout most of 2021, the US Federal Reserve called the rising inflationary pressures “transitory.” Late last year, increasing consumer and producer price data convinced the central bank that the economic condition was not a temporary event. The Fed told markets it was preparing to shift to a more hawkish approach to monetary policy to address the economy’s demand-side pressures. The artificially low interest rates, liquidity, and government stimulus in 2020 and 2021 planted the inflationary seeds which sprouted during the second half of 2020, throughout 2021, and into early 2022.

In early 2022, the geopolitical landscape threw a curveball at the central bank when Russia invaded Ukraine, launching the first major war in Europe since WW II. Sanctions on Russia and Russian retaliation began to cause even more upside pressure on commodity prices as Russia is a leading producer of energy and other raw materials. China and Russia’s “no-limits” support agreement complicated matters, setting the stage for the invasion.

Crude oil and natural gas prices had already been rising by the end of 2021. The leading benchmark crude oil futures are the Brent and WTI contracts. After falling to a record low below zero in April 2020, nearby WTI crude oil futures at $75.21 per barrel. Brent futures fell to $16 per barrel, the lowest price of this century in April 2020, and closed 2021 at the $77.78 level.

Meanwhile, nearby natural gas futures dropped to $1.44 per MMBtu in June 2020 and were at the $3.73 level on December 31, 2021. The oil and gas futures markets had been rising, making higher lows and higher highs throughout the second half of 2020 and in 2021. In 2022, they took off on the upside, reaching fourteen-year highs.

Increasing inflation and post-pandemic demand created a bull market in crude oil and natural gas that turned into a perfect bullish storm in 2022. The war and a dramatic geopolitical shift made dynamics shift from demand to supply-side concerns. The Fed has few if any tools to deal with supply-side economic events, and the only answer could be increasing supplies, which is a challenge in the current environment.

Just as the Fed mischaracterized inflation as “transitory,” US and European policies addressing climate change have played a role in the ascent of hydrocarbon prices. Since energy prices are inflation’s root cause, exploration and drilling could be the only answer to address the economic condition. Fossil fuels continue to power the world, and the price action is screaming that monetary policy has taken a backseat to the energy debacle.

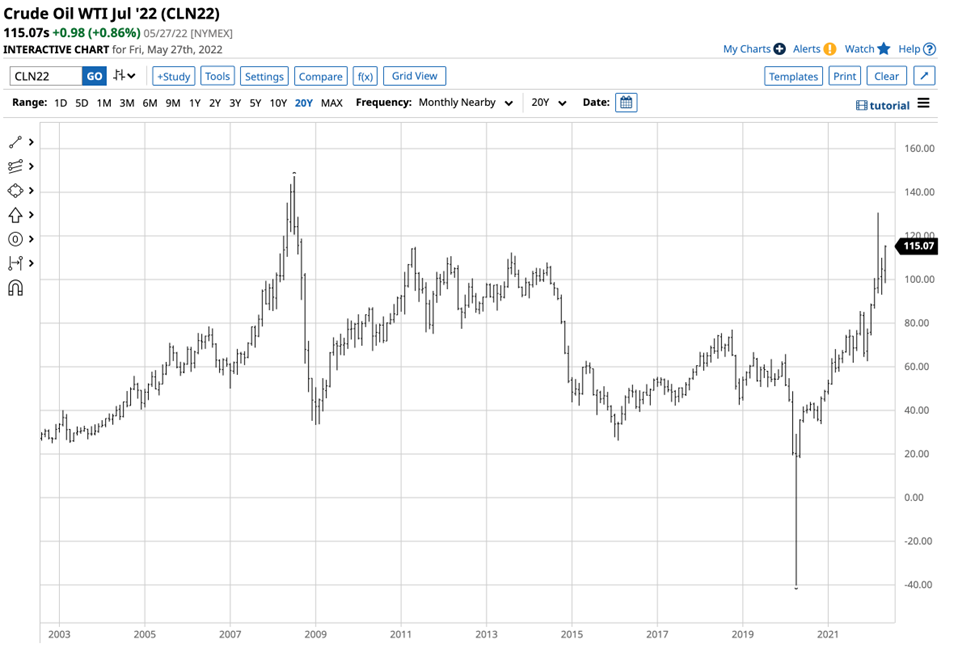

Crude oil at the highest price since 2008- Inventories and product prices support higher highs

Nearby NYMEX WTI futures rose to $130.50 per barrel on March 7 after Russia invaded Ukraine on February 24, and the war escalated.

Source: Barchart

The chart highlights that the WTI futures were sitting at just above the $115 level on May 27. Brent crude oil hit a high of $139.13 in early March.

Source: Barchart

The chart shows the price was at around the $119.43 per barrel level in late May 2022. The all-time 2008 peaks in WTI and Brent were at $147.27 and $147.50.

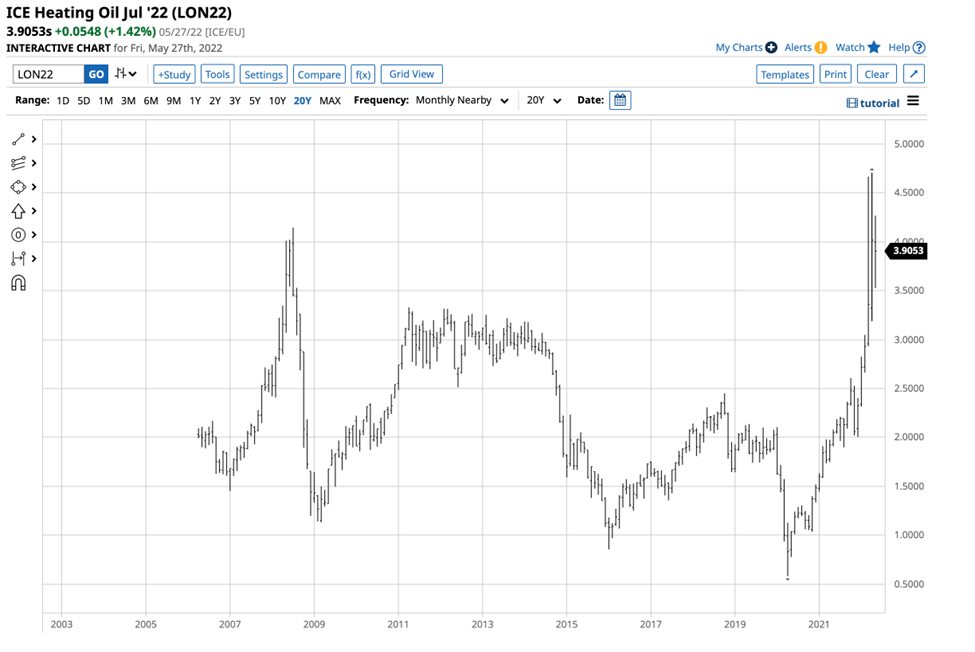

While crude oil missed an all-time high, gasoline and heating oil hit record prices in 2022.

Source: Barchart

The chart shows that gasoline futures prices reached $4.0640 per gallon wholesale in May, an all-time high. July gasoline was sitting at over the $3.90 level on May 27.

Source: CQG

Heating oil is also a proxy for distillates like diesel and jet fuels. The chart shows the spike to a record peak in distillate in April at $4.7072 per gallon wholesale. Heating oil was also over the $3.90 per gallon level on May 27.

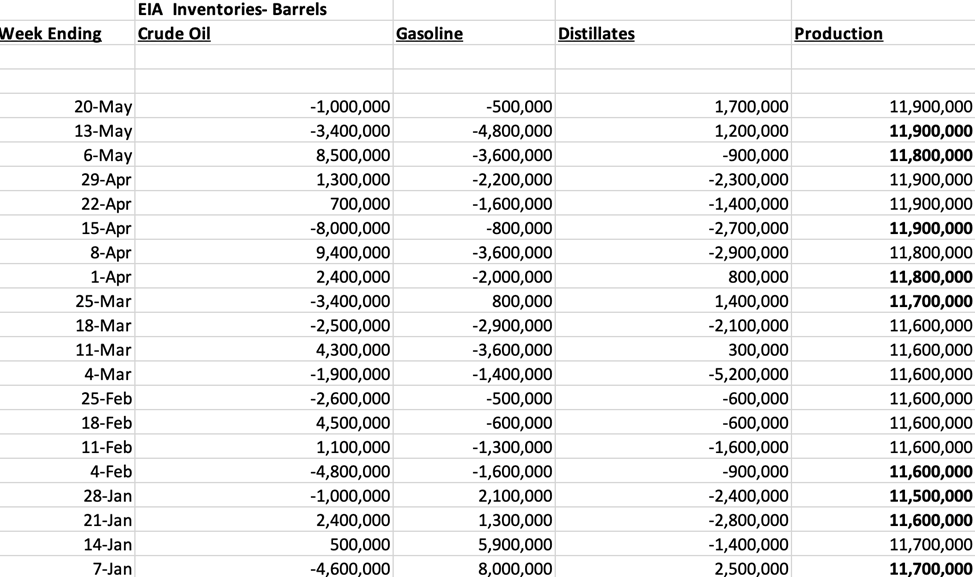

Inventories and US production have supported prices:

Source: US Energy Information Administration

So far, in 2022, US crude oil stockpiles rose by 1.9 million barrels, but the data includes strategic stockpile releases. Meanwhile, gasoline inventories declined by 12.9 million barrels, and distillate stocks fell by 19.9 million barrels from the beginning of 2022 through May 20. Consumers require oil products, and the data supports higher prices. While US daily output rose from 11.7 to 11.9 million barrels per day in 2022, they remain below the March 2020 13.2 mbpd record peak.

Natural gas is also at a fourteen-year high- Inventories, and European prices support the continuation of a very volatile bull market

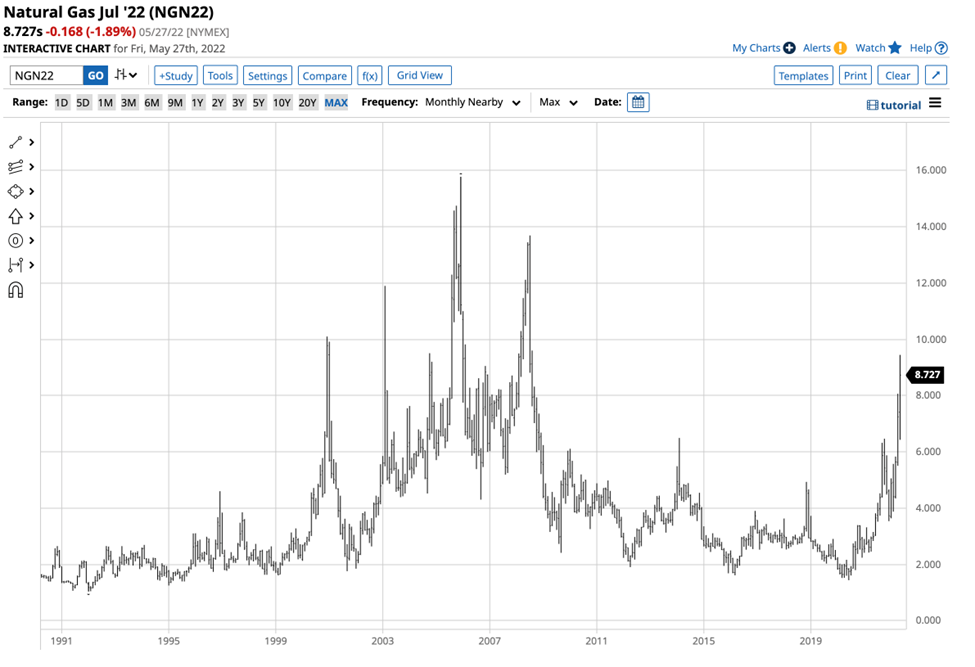

NYMEX natural gas futures fell to a twenty-five-year low in June 2020, reaching $1.432 per MMBtu.

Source: CQG

The long-term chart shows that natural gas futures moved over six times higher by May 2022, reaching a high of $9.447 per MMBtu and sitting at over the $8.70 level on May 27.

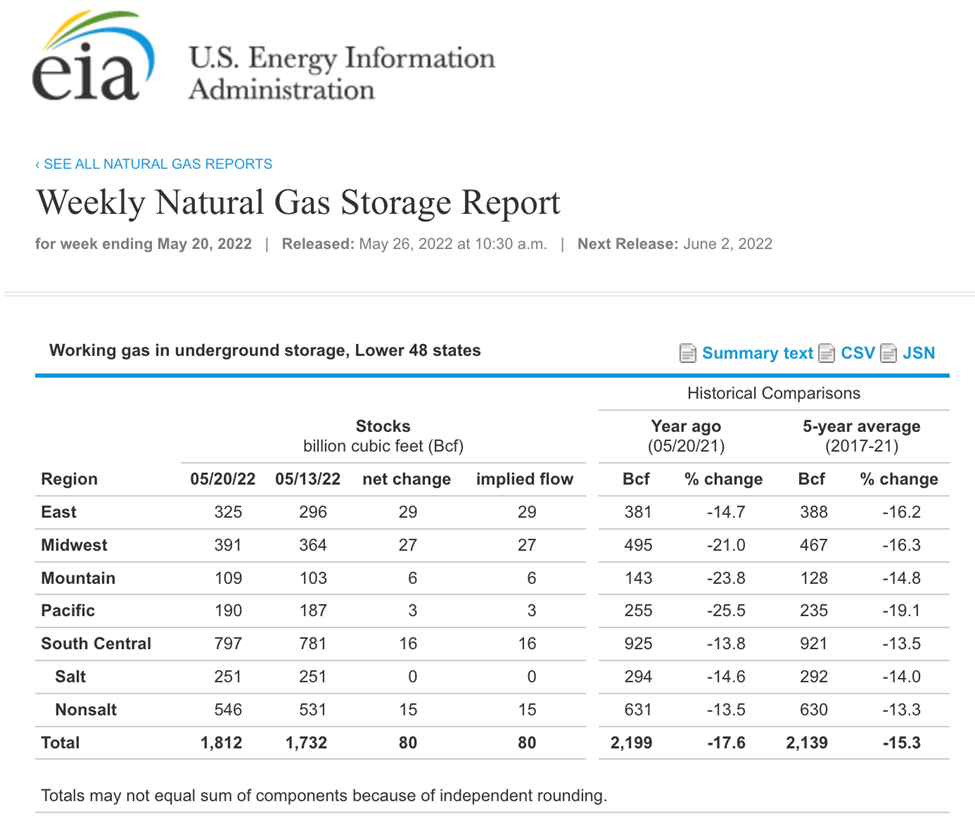

Natural gas inventories are at low levels, with the price at a fourteen-year high.

Source: EIA

At the 1.812 trillion cubic feet level on May 20, natural gas in storage across the US was 17.6% below last year’s level and 15.3% under the five-year average.

Over the past years, natural gas liquefication opened a burgeoning export market for the US energy commodity as it now travels worldwide via ocean vessels. Natural gas’s addressable market expanded far beyond the US pipeline network.

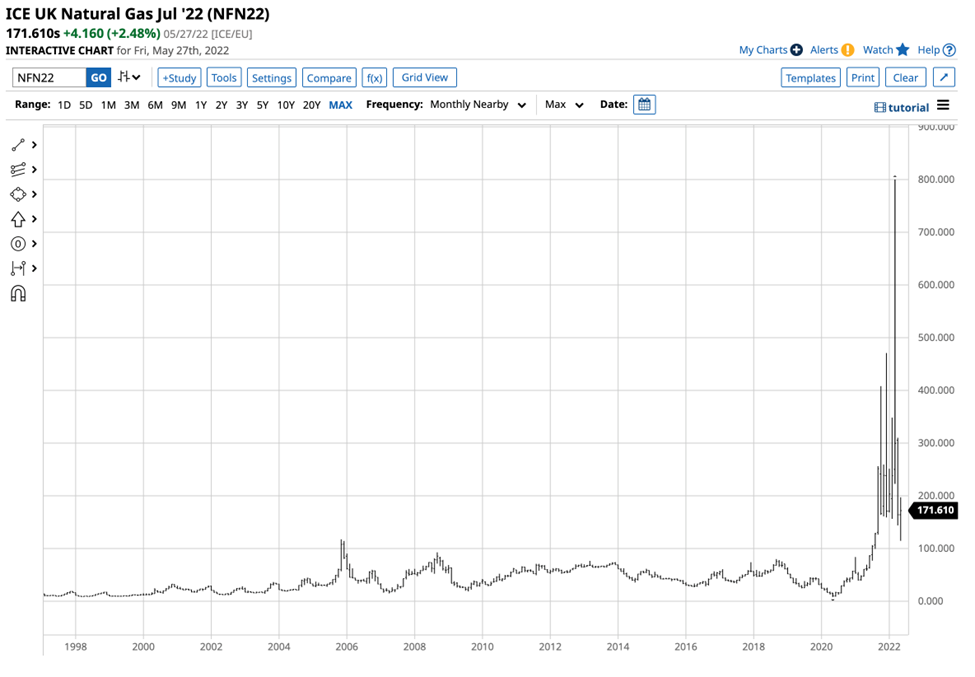

While US natural gas exports have sold LNG to Asian consumers under long-term contracts, the war in Europe and Russian retaliation for sanctions have sent European natural gas prices to record levels.

Source: Barchart

The chart shows that ICE UK natural gas futures rose to the 800 pounds per 1,000 thermals level in March 2022. Before 2021, the all-time high was at the 117 level, and at the 171.61 level on May 27, the price was well above the pre-2021 record peak. Russian natural gas travels by pipeline to European consumers. The Russians have demanded payment in rubles and have cut off “unfriendly” countries that support Ukraine. Moreover, Sweden and Finland’s plans to join NATO only increase Russian export bans, and European consumers are turning to the US for supplies. The bottom line is that

US natural gas has become an international energy market, and the supply shortage is lifting worldwide prices.

In the US, natural gas is heading into the volatile hurricane season. In 2005 and 2008, Hurricanes Katrina and Rita wreaked havoc along the Louisiana coast. The NYMEX futures delivery point is the Henry Hub in Erath, Louisiana, along the Gulf Coast hurricane corridor. Storms in 2008 and 2005 lifted the price to $13.694, and $15.65per MMBtu, respectively. Even if the natural gas market makes it through the annual hurricane season without category four or five storms, the 2022/2023 winter season in worn-torn Europe will likely push prices higher, with $10+ NYMEX futures prices on the horizon.

The four reasons for higher fossil fuel prices- SPR releases are a temporary band-aid

At least four factors favor higher oil and gas prices in late May 2022:

The Biden administration’s green energy initiative favors alternative and renewable fuels while inhibiting fossil fuel production. The US energy policy since early 2021 handed the pricing power to OPEC, the international oil cartel, and Russia. After years of suffering under low prices and lower US demand because of US shale oil and gas production, OPEC+ now controls supplies and owes the US and European consumers no favors. US requests for production increases fell on deaf ears in Riyadh, Moscow, and other production capitals.

The February 4 “no-limits” agreement between China and Russia creates a bifurcation of the world’s nuclear powers, with the US and Europe on the other side. Russia’s invasion of Ukraine could lead to Chinese reunification attempts with Taiwan. Hostilities and geopolitical tensions make hydrocarbons a political tool for the Russians and allied world oil and gas producers.

The crude oil and natural gas prices have been rising despite a COVID-19 lockdown in China. When the Chinese economy reopens, the global energy demand will likely rise, putting more upside pressure on oil and gas prices. Meanwhile, a historic heatwave in India is causing increased energy demand in the world’s second-most populous country. India has not cooperated with the US and Europe with sanctions on Russia.

Even if the US were to shift back to a drill-baby-drill and frack-baby-frack approach to traditional energy production, labor shortages and higher input and equipment prices put upside pressure on production costs. Moreover, the Biden administration has doubled down on its green initiatives, so the potential for production increases remains low.

Instead of increasing production over the past months, President Biden released a historical level of crude oil from the strategic petroleum reserve. Past SPR releases have not weighed on the price in challenging times. Moreover, the US will eventually need to replace its resources, leading to buying in the oil market. The administration released 30 million barrels in early 2022 and has been releasing one million barrels per day from the SPY. The price remains around the $115 per barrel level as the SPR sales have been a short-term, ineffective band-aid. Meanwhile, crack spreads, a real-time demand indicator rose to new all-time highs in May. The level of refining margins are a warning sign that higher crude oil prices are on the horizon.

Drilling and exploration are the answer to supply-side economic woes

The Fed is increasing interest rates and reducing its balance sheet to address the highest inflation in over four decades. The central bank’s toolbox contains monetary policy tools that deal with the economy’s demand-side. In 2020, slashing interest rates and government stimulus encouraged borrowing and spending and inhibited saving.

The Fed now faces supply-side economic factors caused by the war in Ukraine, sanctions, and geopolitical bifurcation. There are few, if any, tools that can deal with the supply-side issues that will continue to fuel inflation. While core inflation data excludes food and energy, food and energy are critical inflationary factors that impact individuals and businesses. Moreover, energy is a crucial cost of goods sold input in all sectors of the economy. Therefore, the only answer to dealing with supply-side inflationary pressures in the current environment is to increase supplies. Just as the Fed woke up from its “transitory” trance, the administration will likely realize that encouraging fossil fuel exploration and drilling is the only route out of the current inflationary spiral. The US is blessed with rich oil reserves in the shale regions, Alaska, and other oil-producing areas. The Marcellus and Utica shale contains quadrillions of cubic feet of natural gas. A hostile Russia and China could cause a reversal of the current path of US energy policy. Rising oil and gas prices will eventually choke all economic growth, and the administration may have no choice but to put climate change initiatives to the side while it deals with the inflationary spiral.

XOP outperforming the stock market in 2022- The trend is your best friend

The war, rising interest rates, a strong US dollar, increasing geopolitical turmoil, and other factors have weighed on the stock market in 2022.

Source: Barchart

The S&P 500 is the most diversified US stock market index. After closing at 4,766.18 on December 31, 2021, the index was 12.8% lower at 4,158.24 on May 27.

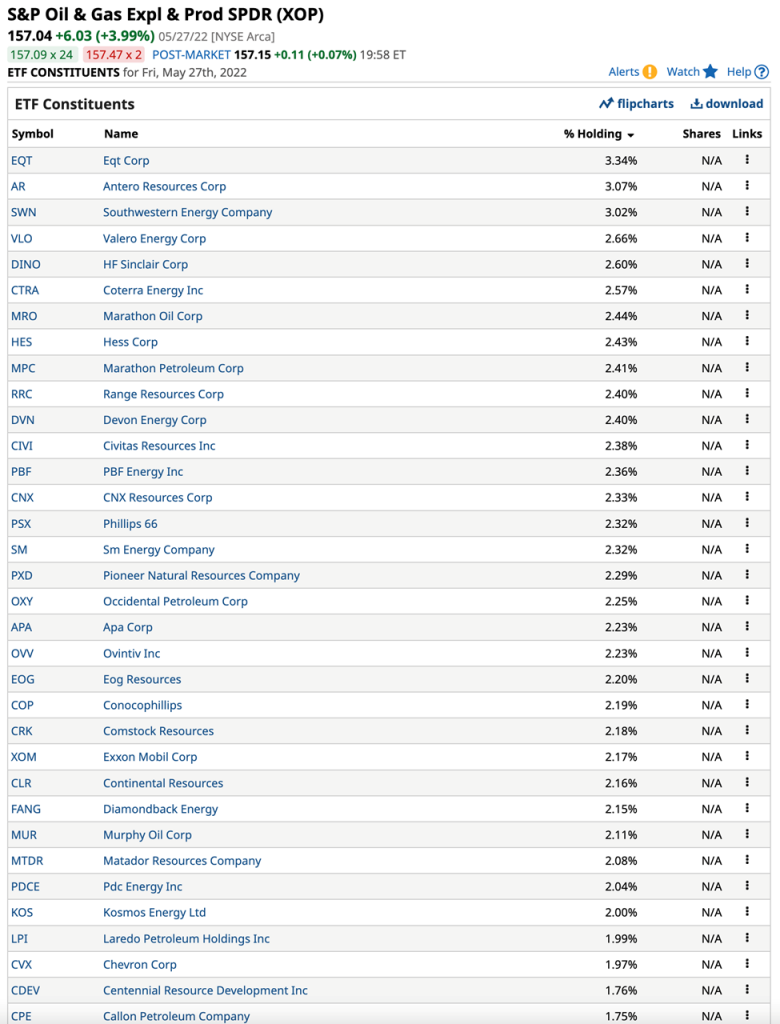

The S&P Oil & Gas Exploration and Production ETF product (XOP) holds many of the top US companies that explore, drill, and produce crude oil and natural gas, including:

While the S&P 500 is 12.8% lower in 2022, the XOP performance has been impressive:

Source: Barchart

The XOP closed at $95.87 at the end of 2021. At the $157.04 level on May 27, the ETF was over 63.8% higher this year.

Existing oil and gas exploration, drilling, and production companies have experienced a profit bonanza in 2022, but they are struggling to meet the growing worldwide hydrocarbon requirements. The bull market in oil and gas opens the door for newcomers in exploration and drilling. Dealing with inflation requires addressing the root cause, energy shortages, and high prices. An epiphany that shifts US energy policy is the path of fighting inflation. The supply-side problems are beyond the Fed’s reach, and SPR releases are only a band-aid on a worldwide gapping ax wound.

Written By: Andrew Hecht, on behalf of Maurice Jackson of Proven and Probable.

Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.

I have been waiting for a couple of years to write this story. For years Lion One has been my biggest holding because the story is so simple to understand. I’ve written half a dozen pieces on the company and the last one I wrote was seven months ago. I called it, Buying Lion One is like Stealing. And few listened. The shares were $.97 at the time. Between then and now the stock has barely edged higher in spite of excellent results such as their May 31 press release showing 584 grams of gold per tonne over 0.30 meters.

I love the chat boards. You get to see just how stupid some people can be in their failed attempts to look smart. Here is what someone said on the CEO.CA Lion One board in response on May 31st.

@NabtaPlayaEgypt Tuvatu continues to be restricted to returning very narrow (1/3 meter average) high grade shoots which unless such systems are spaced relatively close en-echelon, may not be economic to mine. At the rate that drilling returns are coming in, that it could take another 2-3 years minimum to create a significant resource update.

Someone wrote me privately and asked what I thought about the comment. Here is how he posted my response.

@WisGuy1 BM response: “Absolute rubbish. There is a similar mine a stone’s throw away that has produced millions of ounces of gold of similar grade and thickness.”

(Click on images to enlarge)

Investing in Lion One at a profit is about as difficult as learning how to fall off a bike. If you can handle that, you can make money on Lion One, because there is an identical age and grade alkaline deposit located about 40 km to the Northeast called the Vatukoula Gold mine. In production from 1932 the Vatukoula mine has produced over seven million ounces of gold and shows a resource of an additional four million ounces.

The deposits are identical in age, grade and type of deposit. So anyone saying you can’t mine a 584-gram intercept of gold over 0.30 meters is blowing smoke.

Lion One is fully permitted to go into production. They built their own assay lab and it is run to industry standards so assays that might take 2-3 months in Canada take 2-3 days in Fiji. Lion One plans on production to begin in Q3/Q4 of 2023.

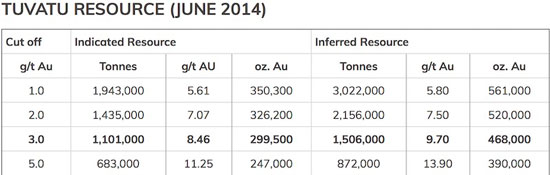

Lion One has a current 43-101 showing just over 910,000 ounces of gold at an average of 5.61 g/t to 5.8 g/t. I had a short conversation with Wally Berukoff about the production plans. He is shooting for annual numbers of around 100,000 ounces of gold. That is pretty much the magic number. The market will not take any company seriously below that number.

Because of silly Covid restrictions put in by the government of Australia and Fiji, Lion One has been pretty much delayed for two years. The stock hit a high of $2.67 in July of 2020 based on excellent results before drifting lower to a low a month ago of $.88. I’ll stand by every word I said in my piece from November of last year. Buying Lion One is like stealing. They have the goods.

Wally realized the project could not be run remotely from Perth so last year he put in a brilliant on site team in Fiji. If you watch this video, I think you will agree with me in saying that this is one of the most professional teams I have ever seen in twenty years.

Currently the company has about $34 million in cash in the treasury. They have six drills turning with two more on order. The incredible latest hole shows they have tapped into a feeder pipe. They will continue to drill to upgrade and increase the near surface gold resource for near term production but I expect them to pincushion the feeder to determine all its limits.

The worst thing that can happen to any stock is for shareholders to become bored. Once they do, they bail out at the first opportunity to break even. While the stock going up 17.5% on the news with over two million shares trading on the news, I suspect that was a lot of weak hands selling. Look for a couple of quiet days without a lot of price movement and then for the shares to go higher, perhaps much higher. The incredible results of the past two years tell me the high of $2.67 will be revisited soon. Lion One is still cheap.

Until the news of the incredible latest intercept hit the market my personal shares have been underwater for most of the last two years. My average price was $1.18 and it took this news to bring me into profit. But I have believed this story since I first heard it and continued to add to my position as the price dropped. I have never sold a single share and right now I am really glad.

Lion One is an advertiser. I love the company; I love the management and the team that Wally has put together. It will be a mine. It will be profitable and it will be a hell of a lot bigger than anyone imagines today. I expect majors will be sniffing around soon wanting to pick up a piece of it while it’s still cheap. That isn’t going to last long. As with the case of Newfound Gold, intercepts similar to this do not occur in a vacuum. There will be more record-breaking hits in the future.

I own shares and have participated in PPs in the past and will in the future. I am biased so do your own due diligence.

Lion One Metals LIO-V $1.34 (Jun 06, 2022) LOMLF OTCQX 156 million shares Lion One website

VANCOUVER, British Columbia, May 16, 2022 (GLOBE NEWSWIRE) — Rover Metals Corp. (TSXV: ROVR) (OTCQB: ROVMF) (FSE:4XO) (“Rover” or the “Company”) is pleased to provide a recording of the Company’s CEO, Judson Culter, presenting Rover’s high-grade gold exploration story in northern Canada, including an overview of current operations and upcoming milestones, while sharing the most recent Investor Presentation. We invite all investors and other interested parties to watch the recorded webinar at the link below. The discussion also includes Rover’s plans for gold exploration at its new project in the Battle Mountain gold district of Nevada.

About Rover Metals Rover is a precious metals exploration company specialized in North American (Canada and U.S.) precious metal resources, which is currently advancing the gold potential of its existing projects in the Northwest Territories of Canada (60th parallel), and north-central Nevada, USA. The Company owns five gold projects. Phase 3 Exploration at its Cabin Gold Project, 60th Parallel, NT, Canada, commenced in March 2022 and continues through to the date of this release. Phase 1 Exploration at its Tobin Gold Project commenced in May 2022 and continues through to the date of this release. Lastly, the Company, is also awaiting news from the Phase 2 Exploration Program at its Up Town Gold Project, in the Northwest Territories of Canada (60th parallel).

ON BEHALF OF THE BOARD OF DIRECTORS “Judson Culter” Chief Executive Officer and Director

For further information, please contact: Email: info@rovermetals.com Phone: +1 (778) 754-2617

Statement Regarding Forward-Looking Information This news release contains statements that constitute “forward-looking statements.” Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Rover’s actual results, performance or achievements, or developments in the industry to differ materially from the anticipated results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. There can be no assurance that such statements prove to be accurate. Actual results and future events could differ materially from those anticipated in such statements, and readers are cautioned not to place undue reliance on these forward-looking statements. Any factor could cause actual results to differ materially from Rover’s expectations. Rover undertakes no obligation to update these forward-looking statements in the event that management’s beliefs, estimates or opinions, or other factors, should change.

THE FORWARD-LOOKING INFORMATION CONTAINED IN THIS NEWS RELEASE REPRESENTS THE EXPECTATIONS OF THE COMPANY AS OF THE DATE OF THIS NEWS RELEASE AND, ACCORDINGLY, IS SUBJECT TO CHANGE AFTER SUCH DATE. READERS SHOULD NOT PLACE UNDUE IMPORTANCE ON FORWARD-LOOKING INFORMATION AND SHOULD NOT RELY UPON THIS INFORMATION AS OF ANY OTHER DATE. WHILE THE COMPANY MAY ELECT TO, IT DOES NOT UNDERTAKE TO UPDATE THIS INFORMATION AT ANY PARTICULAR TIME EXCEPT AS REQUIRED IN ACCORDANCE WITH APPLICABLE LAWS.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OF THIS RELEASE.

Provenance Gold Corp. is a precious metals exploration company with a focus on gold and silver resources within North America. The Company currently holds interests in three properties in Nevada, and one in eastern Oregon, USA. These properties include the 5,160 acre White Rock property situated in Elko County within the Delano Mining District, the 540 acre Mineral Hill property situated in Eureka County and the 2,024 acre Silver Bow property situated in Nye County in addition to the Eldorado property located in eastern Oregon.

WHITE ROCK The White Rock project spans 5,160 acres and covers an extensive gold system, the core of which hosts gold mineralization that extends across an area at least 3.2 Km by 1.6Km. Provenance believes the geology of the White Rock mineral system is similar to the geology of the nearby Black Pine mineral system in southern Idaho. At Black Pine, the gold system is hosted in a complex of thrust faults. Provenance believes a similar thrust complex underlies the White Rock mineralization, and the postulated thrust complex will be a future exploration target.

ELDORADO The Eldorado property will receive early focus in 2022 as historic data suggests it could hold up-to-a multimillion-ounce gold resource. The company is currently in an early stage of data acquisition, verification and compliance that will result in the completion of a National Instrument 43-101 resource technical report.

Corporate Office Provenance Gold Corp. 2200 – 885 W Georgia St. Vancouver, BC, V6C 3E8 +1-250-516-2455 email@provenancegold.com

Proven and Probable Where we deliver Mining Insights & Bullion Sales. I’m a licensed broker for Miles Franklin Precious Metals Investments (https://www.milesfranklin.com/contact/) Where we provide unlimited options to expand your precious metals portfolio, from physical delivery, offshore depositories, and precious metals IRA’s. Call me directly at (855) 505-1900 or you may email maurice@milesfranklin.com.

Proven and Probable provides insights on mining companies, junior miners, gold mining stocks, uranium, silver, platinum, zinc & copper mining stocks, silver and gold bullion in Canada, the US, Australia, and beyond.