Maurice Jackson:

Joining us for conversation is Kyle Floyd, the CEO and Chairman of Vox Royalty (TSX.V: VOX | OTCQX: VOXCF). Sir, it’s a pleasure to speak with you today, as we deep dive into the value proposition of Vox Royalty, which offers a smart way to invest in commodities. Before we begin, Mr. Floyd, please introduce us to Vox Royalty and the opportunity the company presents to shareholders.

Kyle Floyd:

Vox Royalty Corp has been around since 2014. Our business model focuses on buying third-party royalties, which we believe is the most value-enhancing way to play the commodity sector. And so, we have built what is the fastest-growing royalty company on the planet. We also believe one of the royalty companies trading at the most attractive valuations, and we have a management team and business entirely engaged and finding deep value by buying these third-party royalties all around the world. And we’ve been very, very successful in building Vox Royalty for our investors over the last eight years.

Maurice Jackson:

Before we take a step forward, let’s take a step back. What are some of the merits of royalty companies for shareholders?

Kyle Floyd:

Well, royalty companies offer a better risk-adjusted way to play commodity exposure. And there are a couple of key reasons for that. Royalties typically are revenue interests essentially that run with the mining assets. And so you take a top-line percentage interest in these projects. You’re not exposed to a lot of the costs and the risks that these mining companies face, which can be quite significant. If there’s a cost overrun, the royalty company gets to continue to generate its revenue from the project without having to fund any of the projects or being diluted. If that underlying entity needs to raise capital.

The other costs that the mining that the roads and conveys are not associated with the mining companies face are the general input costs, the variable cost structure, whether it’s for fuel people, you name it, all the inputs that go into mining companies, all those costs are increasing and royalty companies are exposed to that.

The other benefit, then, on the upside is there’s a lot of diversification you get from royalty companies. Vox Royalty has 5 production stage assets going to 10 production stage assets and beyond means that we’re diversified across a suite of assets. And so we don’t have single asset risks that you have in a lot of mining companies. So a lot less risk, but a lot of the same upside, if not better upside that you realize in mining companies in the form of metal prices going up helps increase the value of royalty companies, increase in production, increases in reserves, increasing resources. All of that goes to fuel royalty company growth. And we’re not on the hook for any of those costs in terms of building out those assets further. So that’s a quick synopsis on why we’re so bullish on royalties and we believe that’s backed up in the market as well to companies that outperform for the better part of the last two decades.

Maurice Jackson:

One of the virtues of royalty companies, several embedded optionality. And speaking of royalties, to truly appreciate the value proposition of Vox Royalty, Mr. Floyd, what is a royalty juxtaposed to a stream? We hear those terms often, but they get co-mingled, but they’re not the same.

Kyle Floyd:

That’s a great question. Royalties are these third-party interests. So, interest not held by the operating party of the mining company, they’re the prospector or the junior mining company or the family that owned a ranch that sold the asset eventually to the mining company and typically retained a royalty, which was that right in the upside of revenue generated for these mines typically for the life of those mines. A stream is a structure where you’re typically financing a mining company, and the counterparty is the mining company. You’re giving them capital and in return, you are taking a percentage of a certain metal that’s generated from that opportunity.

And you’re continuing to remit payments to get that metal over the life or over the term of that commercial arrangement. The big difference is typically on streams. You’re giving money to a mining company, so you need them to meet capital versus our royalty model. We’re not giving money to the mining company. We’re purchasing a right held by a third party. And typically those are non-core assets for these groups. Therefore, we’re not restricted by mining companies needing capital to find really interesting deals for our investors.

Maurice Jackson:

Now that we have a better understanding of the merits of royalty companies, Mr. Floyd, what differentiates Vox Royalty?

Kyle Floyd:

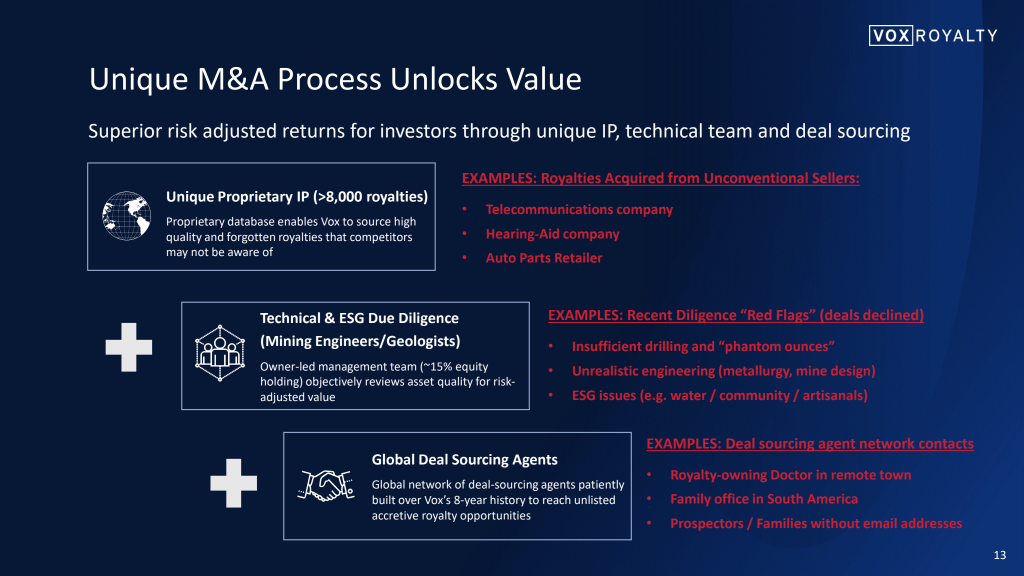

There are a few things that differentiate Vox Royalty and we built a business model to be differentiated, to offer better risk-adjusted exposure for investors. And one of the key differentiators is we focus exclusively on buying third-party royalties. We don’t compete at the big end of town trying to finance multi-billion dollar projects with streams. Our niche is finding third-party royalties all over the globe. We have a database that has 8,000 proprietary royalties that provide us a roadmap for finding great royalties in jurisdictions that range from West Africa to Australia, to North America, to South America. And we use a technical team made up of mining engineers and geologists that help screen for good projects that have these amazing royalties over them. And then we connect with these owners of these projects, with our deal sourcing agents all around the world to be able to transact on these opportunities.

Vox Royalty built this ecosystem, this business model around finding third-party royalties, where we think the best value is generated. And if you look at the historical returns of the Franco’s and the Royals, that’s where they’ve generated the best returns, buying these third party royalties, much less the streams and the financing of mining companies that have been completed over the last decade. That being said, they performed very, very well overall. And so that is our business model. Third-party royalties finding amazing assets with great royalties over them, all around the world. And those three kind of key pillars of that stool, the deal sourcing agent network that I think goes farther than probably anybody in our range, the technical team, and intellectual property in the form of a database. And all those combined to make us what has been the fastest-growing royalty company. And I believe also at the best value over the last three years.

Maurice Jackson:

Speaking of the database, Vox Royalty owns one of the world’s largest proprietary royalty databases, consisting of over 8,000, most of which are located in Australia, Canada, and the USA. Mr. Floyd, please introduce us to Vox Royalties property bank.

Kyle Floyd:

It’s a very exciting asset for us, and it’s a huge competitive advantage. Our database has been built over the better part of the last 10 years. Vox was building our database and building our intellectual property. But one of the things that we were acutely aware of is there was the potential that someone was farther ahead of us in terms of this effort to build out proprietary advantages in finding third-party royalties. And sure enough, there was a company that was farther ahead, and that was a company called Mineral Royalties Online.

So they had, at that time, it was a database of 7,000 third-party royalties in their database, all around the world. They had built this database bottoms-up through first principles and first-party data. They went into different mining ministries and exploration offices all around the world and made deals to essentially get this hard copy data and then translate that into data that was online. And so we purchased that database in 2019, that has underpinned a lot of our success and our growth rate. And so that database gives us an edge all around the globe in terms of finding these third-party royalties and being able to transact and closes and bring those into the portfolio.

Maurice Jackson:

I see that Vox has undertaken a keen interest in Australia. Why Australia?

Kyle Floyd:

Well, there’s not just one reason for Australia. There’s a lot of reasons for us in Australia. Australia is, and we’re slightly biased, but it’s also backed up by a lot of the third-party rating agencies, is one of the best, if not the best, mining jurisdictions on the planet. According to the Fraser Institute, Western Australia, which is home to most of our royalties, is the best mining jurisdiction. Investors understand the value of Nevada royalties because Australia is a better mining jurisdiction, in our opinion. We believe Australia is the place that you want to have significant exposure to, complimented by our IP, which has a very strong basis in Australian royalties, and technical team, three of our four key Business Development Executives are also Australian citizens. We understand what we believe is the best major mining market, as well as anybody, if not better than anybody else.

We’ve accumulated what is now the second-largest holding of hard rock mining royalties in Australia. And that’s significant because Australia, beyond just being a fundamentally great jurisdiction with great golden endowments, it has had a very buoyant gold price in Aussie dollar terms. It’s been trading at almost all-time high prices in Aussie dollars for the last almost four years. And so what’s happened is a lot of the exploration development projects that we forecasted would do well have exceeded expectations because the buoyant equity markets have allowed these companies to raise as much capital as needed to advance these projects. And so it’s been a huge boon to our business in terms of the growth of assets already in the portfolio, and having them grow ahead of expectations and realizing tremendous value for our investors. And so, us picking Australia as a place to focus on has paid off for our shareholders.

Maurice Jackson:

Sounds quite intriguing. Now within the property bank, Vox Royalty has producing assets and a pipeline of growth assets. Sir, please acquaint us with your top three key producing assets beginning in Australia.

Kyle Floyd:

This year we acquired the Janet Ivy, and we were engaged on it before it goes back into production. It’s now in production, but it has a huge expansion plan ahead of it, which we expect to take place late next year and that’ll make it a very, very significant cash flow for us. We also have the Koolyanobbing Royalty, which we bought from a telecom business, If you can believe that. It was held in one of their subsidiaries for a very long time, and we’re engaged on a pre at going into production.

That’s had a huge run and huge growth, obviously with the iron ore up in prices. And then we also have a host of other royalties that are in production, Coure Resources, Higginsville operations. We have three open-pits that feed that mill. And so that’s been running at a record pace for us. And then one that we’re excited about is the Segiolola Project that we bought pre-production. It is the highest-grade open-pit gold project in West Africa, and they just announced the first gold pour. So we expect to see revenue from that asset in Q4. So really a tremendous amount of growth in our portfolio from producing and production stage assets.

Maurice Jackson:

We’ve covered the key producing assets. Sir, please introduce us to the growth assets of your property bank.

Kyle Floyd:

I could go on for days about our growth assets. I’ve got to work hard to kind of narrow it down for the readers. I’ll name a couple that I’m excited about. The Ashburton is one. When we bought that royalty, which was in the portfolio of Northern Star. It was a little bit sleepy, but we saw a huge potential in the asset. And what we believed would eventually happen was that other Northern Star would start upping the development curve on this and the timeline on it, or it would transact to a more nimble junior. And sure enough, that happened just a few months after the acquisition of this royalty. The Ashburton is a 1.65 million-ounce gold resource in Western Australia. It’s owned by Calamos Resources now. They’ve got 12,000 meters of drilling going on and their target is three plus million ounces for this asset. So that’s a really exciting NSR royalty for us.

The other one that I’m excited about is The Bowdens Project, which is the largest developing primary silver project in all of Australia. It’s got great fundamentals. The Bowdens Project is an open-pit that’s now exploring the very strong potential to go underground either after the open-pit is exhausted or contemporaneous with open-pit mining. And that is a royalty that has a very multi-decade mine life potential. So those are a couple of the key development stage assets that we’re excited about.

We also have a host of royalties that are going to be coming into production in the very near term. The Pitombeiras is a Vanadium Project in Brazil that they are expecting to come into production in the first half of next year. The Bulong Gold Project is a development stage, production stage asset that’s expected to go into production in mid, next year, over Western Australia Gold Project. And then there’s many more that we can get into without belaboring the point that we have a tremendous amount of growth assets. We have 20 plus development-stage assets, many of which are aggressively moving forward. So it’s a fantastic portfolio of assets with real growth in front of it that’s being delivered to the market every quarter. And that’s increasing value for shareholders.

Maurice Jackson:

Realizing this is a forward-looking statement. We’re going to get into some members later in this discussion, but how much revenue potential is before us under the current market conditions, if we combine the producing and the growth assets?

Kyle Floyd:

And it’s very much a forward-looking statement. I would caution on that. We’ve done a fantastic job of finding royalties 3 to 24 months out before production, where we find the really good value we’re able to bring in those assets that are good fits within our portfolio. We take away the risk from the disparate holders of these third-party royalties all around the world on their non-core assets. So there’s risk asymmetry. They fit better in our portfolio. They don’t fit as one-off assets. And so we’re able to find really good value all around the world, finding these near-production assets. We came out and I think we’ve validated that business over the last 12, 18 months. We recently doubled revenue guidance. We’ll probably talk about that more, but that’s really on the basis that we’re finding these royalties pre-production and then allowing them the time. And usually, it’s not a very long time to go to get into production.

And so when we step out and look at our portfolio, I believe that there’s $15 to $20 million of long-life revenue potential in the portfolios. There’s reason for tremendous upside on that number as well. And that there are 15, 20 exploration stage assets. Some that are generating bonanza grade drill hits are increasing the possibility that those are going to become mines. So very active exploration projects that would kind of fuel growth on top of that. But I believe it’s one of the most undervalued royalty portfolios out there as very strong potential to generate that type of cash flow over the medium and long term. But again, I caution that it was a forward-looking statement. Those are numbers based on operator guidance. They’re based on the technical engineering studies that, that coincide with these assets. But we feel very good about the revenue-generating capability of this portfolio.

Maurice Jackson:

Now germane to revenue, how do mergers and acquisitions impact your portfolio?

Kyle Floyd:

Vox Royalty has a very disciplined approach to acquisitions. We have not the best of our knowledge have not won a single royalty in a sales process. Most royalty companies, in fact, almost all royalty companies, have been growing their business by winning sales processes. So that’s royalties that are being shopped by investment banks and they’re paying top dollar pretty much in every scenario to bring those royalties in the portfolio. What we do is we’ve built a business around finding, these third-party royalties, and disparate shareholders all around the world where these are non-core assets. And so we’ve been able to transact it a really good value. We’re very disciplined on what good value looks like. It has to be accretive across kind of three different key metrics: absolute return on investment basis, relative net asset value, and relative cash flow multiples. Most royalty companies cannot stack up to what Vox is accomplishing in terms of acquisition that’s bringing in across those three metrics. Usually, one, if not two, if not all, three of those metrics break down when other royalty companies are purchasing third-party royalties like we are.

Maurice Jackson:

Now, before we leave the property bank. The multilayered question, what is the next unanswered question for Vox Royalty? When can we expect a response and what will determine success?

Kyle Floyd:

Well, the next step for Vox is we continue to invest in our loyalty database. We will continue to build on that competitive advantage. It’s fueled a lot of our growth and given us a huge leg up on the competition. So we continue to invest in that asset for us, we continue to expand our relationships around the globe. We are finding interesting royalties from Australia to South America, to West Africa and everywhere, pretty much in between. And so, from Vox and what you’ll continue to see on us is expanding on that competitive advantage, expanding on the capability to find really good value for our investors on really exciting projects, where our mining engineers and our geologists understand the quality of those assets so that your readers and the generalist audience out there does not have to do that work. And I think that’s a big advantage that we present for investors is this competitive advantage, that’s good to find a good value.

Maurice Jackson:

Leaving the property bank. Let’s discuss the people responsible for increasing shareholder value. Mr. Floyd, please introduce us to your management team.

Kyle Floyd:

I’m excited about our management team, we’ve handpicked and recruited the management team that we have to fill the roles that we believe needed to be filled over the years to create shareholder value. I founded the concept back in 2013, 2014, and with the belief that we needed to have competitive advantages and skillsets that increase shareholder value and the capability to do so. And so, a few of our key management team members, Spencer Cole is our Chief Investment Officer with a background as a mining engineer, previously worked at South 32 and BHP, and BHP is where the Mineral Royalties Online business, the inspiration was found. Riaan Esterhuizen, who is one of our Executive Vice-Presidents out of Australia. Riaan’s a geologist, Riaan’s led some of the most interesting grassroots exploration campaigns for the who’s who of majors. They went about building Mineral Royalties Online. They built that business. They came into Vox and we acquired that business. And that’s been a huge part of our success. Simon Cooper has been with us for a very long time. Simon’s a mining engineer, a geologist, entrepreneurial, and brings a significant amount of technical capability. He’s worked with some of the most interesting projects all around the world, but also has a very good skill set in terms of finding acquisitions to bring in those acquisitions into our portfolio. And then we have a great CFO in Pascal Attard, and a great General Counsel in Adrian Cochrane. So we believe that we’ve built one of the most exciting and capable management teams in the small-cap royalty space. And it’s a huge asset for our business and our investors.

Maurice Jackson:

And here’s an opportunity to brag on yourself, who is Kyle Floyd, and what makes him qualified for the task at hand?

Kyle Floyd:

It’s always hard to talk about yourself. I’m supposed to be talking about others. But just a little bit about my background. I ran the Mining Investment Banking Division for a firm called Roth Capital. And the inspiration to build Vox was around helping mining companies raise capital, but then seeing that capital not get deployed in the right means and the right ways. And at the end of the day, not generating great risk-adjusted results for investors. And so I’d advise multiple companies on selling streams and royalties and acquiring streams and royalties.

And I believe that was the best business model for the generalist investor to get exposure to commodities. And I went about building a business model for investors, by investors? We started with a seven and a half million dollar investment and began building this company around generating better risk-adjusted returns in the commodity sector. And we’ve been very successful at doing so. And so that’s a little bit of my background. I graduated in Finance from the University of Washington, then a stint at Colorado School of Mines in the Mineral and Energy Economics Department, but a business built around achieving great risk-adjusted returns for our investors.

Maurice Jackson:

Switching gears, let’s look at some numbers, Mr. Floyd, please provide the capital structure for Vox Royalty.

Kyle Floyd:

Vox Royalty has a tight share structure of 39 million shares issued. We, when we went public in May of last year, we had to forward split the stock, which I would tell you, is almost an anomaly in the resource sector. We have 5 million warrants outstanding, at this stage they have a strike at $4.50, which is out of the money as we speak today, and no debt and a very, very strong working capital position. Vox is very well-financed. We have a tight capital structure. We have no intentions of going back to the equity markets anytime soon, and we will continue to be able to build our asset portfolio combination of debt and strategic acquisitions and minimize dilution in doing so. So I’m excited about where our capital structure is today for investors. I think it’s a very unique opportunity from that perspective,

Maurice Jackson:

Who are some of the major shareholders?

Kyle Floyd:

We’ve done a pretty good job of cultivating a nice institutional shareholder base. Management owns 15%. The founding investors own another 15% to 30%. And then we’ve got a nice institutional shareholder roster made up of Konwave, US Global, Adrian day, EuroPacific Gold Fund, and many others that have taken positions in us over the last year and a half.

Maurice Jackson:

In closing. Mr. Floyd, for current and prospective shareholders, why Vox and why now?

Kyle Floyd:

Vox, I believe is a tremendous opportunity emboldened by the fact that we are trading at the very low end, the relative valuation spectrum versus our peers. If you look at some of our closest comps, I’ll refrain from naming them, but they’re trading at multiples of our relative valuation. Yet we’re growing faster, we’re growing at a better value. We’re growing with better fundamentals. And we have competitive advantages that a lot of the industry wishes that they had. And so I believe we’re a tremendous growth opportunity. There is a lot lower risk given our lower relative multiple. So the risk of return upside, I think is there. We’re very optimistic about what we’re going to be achieving for investors over the immediate future and the long term. You have a management team that’s committed to the success of this business owning 15% combined. We look at this as solely an opportunity to create long-term shareholder wealth. And I think our business model is achieving that for our shareholders every day.

Maurice Jackson:

Last question. What did I forget to ask?

Kyle Floyd:

I think we’ve covered just about everything, and it’s really about finding the best risk-adjusted way to play commodities. That’s why we’re here. I believe we’re offering that for investors. We’ve continued to demonstrate that with our recent quarterly results and investors expect more of that as we continue to progress and build this business. And what I believe is realized a re-rating for our shareholders. And even if we don’t, we’re going to continue realizing and create value for our shareholders, and it should also be reflected in the share price and our share value at the end of the day.

Maurice Jackson:

Mr. Floyd, for someone that wants to learn more about Vox Royalty, please share the contact details.

Kyle Floyd:

Absolutely. Voxroyalty.com. We’re on all the social media channels as well. We are happy to engage. There’s also, IR@voxroyalty.com. Please, feel free to be in touch. We love engaging with our investors, and we’ll be happy to share more information.

Maurice Jackson:

Mr. Floyd, it’s been a pleasure to speak with you. Wishing you and Fox Royalty the absolute best sir.

And as a reminder, I am a licensed representative to buy and sell precious metals through Miles Franklin Precious Metals Investments, where we have several options to expand your precious metals portfolio, from physical delivery of gold, silver, platinum, palladium, and rhodium, to offshore depositories, and precious metals IRA’s. Give me a call at 855.505.1900 or you may email: Maurice@MilesFranklin.com. Finally, please subscribe to www.provenandprobable.com, where we provide: Mining Insights and Bullion Sales, subscription is free.