A Third-Generation Miner’s Journey

For almost three decades, Justin Tolman has crafted a career defined by a pioneering spirit and a talent for problem solving. His work has been shaped by a willingness to push into the unknown and be comfortable doing uncomfortable things in pursuit of potential opportunity. The search for buried metals has long driven humanity to explore, settle and ultimately tame some of Earth’s inhospitable places. Tolman’s professional journey reflects that same instinct: a belief that rewards are often found beyond the well-worn path.

Tolman is a third-generation miner who grew up in mining towns. He knew he would be a geologist by his teen years when he realized you could combine a love of the outdoors with the challenge of making discoveries in emerging frontiers. But the path to turning rocks into money is not a straight one.

“Economic geology is a lifelong pursuit focused on the art of turning rocks into value.” —Tolman

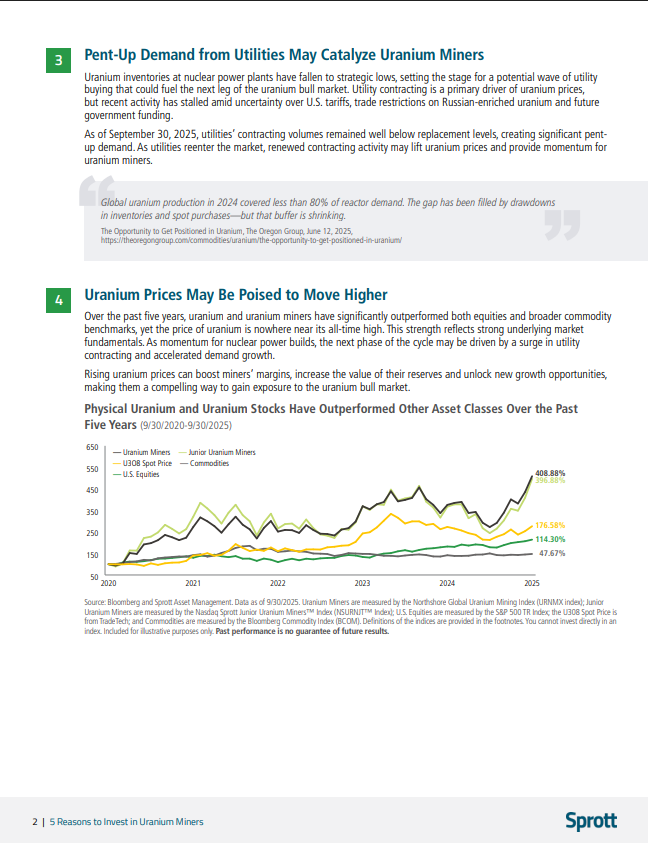

Tolman started working in the mining industry after high school, working elbow-deep in grease at a coal mine in Australia before and between pursuing studies at James Cook University. Since then, he has taken on roles at multiple mines and projects, gaining exposure to underground and open-cut operations, greenfield and brownfield exploration,1 learning and applying geochemistry, geophysics and geostatistics. A recurring theme was always trying to look at an enterprise from as many angles as possible. From engineers to metalworkers, Tolman sought collaboration with every team member, building a foundation of practical knowledge and a deep understanding of the mining sector.

Tolman examining artisanal workings underground at the site of a high-grade silver and gold development project in Jalisco, Mexico.

This early foundation laid the groundwork for Tolman’s later career, which increasingly involved corporate development and the valuation of mining properties, blending traditional financial analysis and leveraging his MBA from La Trobe in Australia. Over the years, the push for new challenges led Tolman to relocate himself and his family multiple times across three continents. He has held leadership positions at both multinational mining companies and small entrepreneurial explorers, giving him a broad perspective on the mining industry.

Throughout his education and career, Tolman learned that economic geology is far more than an academic pursuit. It is the art and science of turning (often incomplete) geological data into measurable economic outcomes. At its core, economic geology is about evaluating an ore deposit and determining whether it can generate tangible value. For Tolman, the insight that ultimately drives investment decisions is an analytical framework, derived from rigorous geologic study and bolstered by high-quality fieldwork. That distinction—between understanding geology and applying it to capital allocation—is what separates theory from actionable advantage.

Economic geologists live in two worlds simultaneously as they apply a business or finance lens to a sector that often operates on the edges of civilization. A spirit of exploration is what built the mining industry, and it continues to drive it today. Economic geologists are responsible for identifying resources, conducting economic evaluations and assessing risks. With global demand for materials set to double by 2040,2 the role of economic geologists is likely to grow in importance. This journey from discovery to production begins with assessing not only what lies in the ground but also whether it can be developed responsibly and profitably.

Tolman exploring early-stage, emerging copper discoveries in the Democratic Republic of the Congo.

First on the Scene: Identifying Mining Resources

Most exploration and new mineral discoveries are pioneering activities conducted in remote places worldwide. If a discovery is of sufficient importance, a mine will be developed, with infrastructure around it, providing jobs and resources for a growing community. This is where balance comes into play. Responsible mining companies strive to both unlock natural resources and support areas that are experiencing new growth and development.

“Mineral discoveries contribute more than raw resources. The investment in infrastructure like roads, power, ports and services follows; later, ancillary services can spring up, and over time, new communities take shape, pushing civilization forwards.” — Tolman

Emerging regions present both opportunities and challenges, but when development is approached responsibly, Tolman believes the benefits far outweigh the risks. There are examples of success, particularly this century, of meaningful engagement with First Nations and local stakeholders in resource-rich countries like Canada, Australia and Chile, with well-developed mining industries, setting a high standard. These collaborative models are now being adopted globally, demonstrating how inclusive practices can drive sustainable progress.

Tolman reviewing a zinc-silver-tin discovery being delineated in the Andes in Central Peru with local geologists.

Geologists often serve as the mining industry’s front line, first venturing into new regions to identify and conceptualize potential targets. Their role extends beyond technical expertise and they often serve as ambassadors for what follows: engaging with local communities, tribal leaders and stakeholders to build trust and clarify intentions. Success depends on cultural sensitivity and effective communication; without it, projects can falter before they begin.

“If you minimize your environmental impact, treat stakeholders with respect and operate with quality governance, that’s simply a formula for good business. It is not something we needed a new acronym for.” —Tolman

While mining can bring transformative benefits, such as living wages and career opportunities in areas where employment is scarce, it is important to acknowledge that resources are finite. The goal is to ensure that, by the time extraction ends, sustainable businesses and transferable skills have been established, creating lasting opportunities beyond the mine’s life. Increasingly, the mining industry is focused on fostering these outcomes through local enterprise development and skill-building initiatives.

Turning Raw Geology into Real-World Value

The work at the mine site and in the community is just the beginning. Once a mining resource has been identified, the project’s viability must be continually assessed through modeling and planning. Mine development and production are not quick processes. On average, it takes 15 to 20 years from discovery to production.3

Once data from drilling, mapping and sampling are collected, 3-D models of the mine are created, and resources are classified. This leads to the planning of the mine and the infrastructure surrounding it. Capital expenditures (CAPEX) and operating expenditures (OPEX) are determined, followed by revenue projection, financial modeling and analysis.

Tolman and crew examining core samples from the Platreef platinum-palladium-nickel mine in South Africa just ahead of first production after years of delineation and development.

Pressure Testing Scenarios

Mining projects rarely unfold as planned. Geology varies, geopolitical conditions shift, permitting timelines slip, costs escalate and commodity prices swing. Because of this, economic geologists pressure-test multiple scenarios before committing capital. Their evaluations funnel into “stage-gates” that determine whether a mining project is viable and investable. Even with this research, fewer than 1% of exploration projects reach production.4

- Is there a deposit?

- At the ground level, an economic geologist needs to confirm whether mineralization exists in meaningful quantity, quality and continuity. This includes extensive analysis, assessments and evaluation of any uncertainties.

- Can it be mined?

- If the deposit exists, the ability for it to be mined needs to be appraised. Economic geologists and a variety of other professionals work collaboratively to determine which type of mine could be developed (open pit, underground or hybrid), mitigate geotechnical and metallurgical risks, and identify infrastructure requirements.

- Can it make money?

- For this step, economic geologists work with engineers and analysts to determine the project’s feasibility, including its sensitivity to commodity prices, estimated position on the cost curve, expected margins and potential complexities.

- Can it be permitted and sustained?

- Even if the project is deemed viable and profitable, it can still face many hurdles. Permitting timelines, environmental constraints, community engagement risks and jurisdictional stability can all affect a mine’s long-term sustainability.

Where Geology Meets Capital and Meaningful Differentiation

While identifying promising deposits is critical, fieldwork alone is not enough when investing in mining equities. Geological insights must be translated into actionable investment intelligence. Tolman is convinced that blending economic geology with mining equity investing provides clear and meaningful differentiation. By grounding investment decisions in first principles geological analysis,5 independent views can be formed regarding a project’s potential rather than relying on company narratives or sell-side interpretations.

This discipline may allow promising discoveries to be identified earlier than peers, often well before they are appreciated by the broader market, creating potential opportunities for more attractive entry points. Equally important, geological expertise helps surface fatal flaws and material risks that may be overlooked by the average market participant, likely enabling downside exposure to be managed. Additionally, economic geologists’ bird’s-eye view of the industry allows them to interpret growing trends that can drive long-term market positioning.

Boots-on-the-Ground Experience Meets Investment Strategy

While most financial professionals feel at home in the boardroom, Justin Tolman is equally comfortable with his boots on the ground. His work in the field spans continents, commodities and a variety of economic conditions. Tolman has been deeply involved in every layer of resource exploration, from identifying mineralization to assessing resources and determining whether they can be economically extracted. So, when it comes to investing, he and the investment team at Sprott bridge macro and micro: connecting top-down commodity fundamentals to bottom-up asset-level realities through a perspective shaped by years of hands-on geological and commercial experience.

At Sprott, Tolman applies his expertise as an economic geologist to translate field data into investment insight. He integrates analysis of macroeconomic forces shaping commodity markets with evaluation of individual mining companies to inform portfolio construction and capital allocation. His work focuses on identifying and supporting new mine development opportunities, with the aim of generating value for clients while contributing to the growth of local economies and communities.

“I have spent my career moving across the world, working in mines, doing exploration, valuing projects and helping make discoveries in multiple continents. I’ve stopped counting, but I have lived, worked and undertaken project reviews in more than 40 countries. This ‘renaissance geologist’ experience has given me deep insight into what it takes to succeed in this industry. This is a valuable tool when evaluating potential mining and metals investments, helping to efficiently and effectively evaluate new companies, teams and projects.” —Tolman

Tolman in the Cote d’Ivoire holding a freshly poured gold bar from a new gold mine.

About Justin Tolman, BSc (Hons), MBA

Managing Partner, Sprott Inc. & Senior Portfolio Manager and Economic Geologist, Sprott Asset Management USA, Inc.

Justin Tolman joined Sprott in 2018 as an economic geologist. He specializes in project and company evaluations. Tolman is a Portfolio Manager for Sprott Gold Equity Fund, Senior Portfolio Manager, Economic Geologist, of Sprott Concentrated M&A Strategy, and Portfolio Manager of Sprott Active Gold & Silver Miners ETF (GBUG) and Sprott Active Metals & Miners ETF (METL). For the two decades prior to joining Sprott, Tolman held a series of increasingly senior roles with global mining and exploration companies, including Newmont, New Gold, Exeter Resources and MIM Holdings, managing programs and leading discovery teams across the globe. Mr. Tolman holds a BSc with 1st Class Honors in Economic Geology from James Cook University (Queensland) and an MBA from La Trobe University (Victoria). He is a fellow of the Society of Economic Geologists and the Australian Institute of Geoscientists, and a registered Professional Geologist with the Association of Professional Geoscientists of Ontario (APGO).

Source: https://sprott.com/insights/the-metamorphosis-of-a-career-turning-rocks-into-value-investing/