(Bloomberg) — Platinum surged to its highest level since 2014 as supply concerns and a wave of speculative buying jolted the market.

The precious metal surged as much as 4.6%, while palladium was up more than 5% at one point. Gold edged higher as investors waited for clearer signs that Israel-Iran tensions won’t spill over again, and for more certainty on the Federal Reserve’s interest rate path.

“The recent surge in Chinese investment and jewelry replacement is shining a spotlight on platinum’s supply deficit,” said Justin Lin, an analyst at Global X ETFs. “Palladium and platinum are intrinsically linked as they can be substituted for one another for use in autocatalysts depending on relative prices, so we can expect some positive momentum in palladium off of platinum’s rally.”

The dominant platinum spot market in London and Zurich has shown signs of tightness for months, after approximately half a million ounces surged into US warehouses, spurred by a lucrative arbitrage and fear of tariffs.

Forward prices for platinum are now trading well below spot, a situation known as backwardation, which indicates tight market conditions. The implied cost of borrowing the metal is also still high, at an annualized rate of roughly 13% for a one-month lease, well above the usual rate of close to zero.

Platinum surged 3.4% to $1,400.75 an ounce as of 11:25 a.m. in London and palladium jumped 2.4% to $1,093.46. Gold rose 0.2% to $3,339.20 and silver added 1%. The Bloomberg Dollar Spot Index declined 0.5%.

Vancouver, British Columbia–(Newsfile Corp. – May 7, 2025) – Riverside Resources Inc.(TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY) (“Riverside” or the “Company“), is pleased to announce that, it’s subsidiary, Blue Jay Gold Corp. (“Blue Jay“) issued 2,305,000 common shares (the “Blue Jay Shares“) at an issue price of $0.40 per share for total gross proceeds of $922,000 as part of a previously announced non-brokered private placement of the Blue Jay Shares. Riverside now holds 74.80% of the issued and outstanding Blue Jay Shares.

“We’re very pleased with the strong investor interest that led to the upsizing and successful close of the Blue Jay Gold seed round,” stated John-Mark Staude, CEO of Riverside Resources. “This outcome reinforces the value we’ve built in the Ontario portfolio and reflects confidence in Blue Jay’s leadership and exploration potential. As Riverside shareholders, we continue to benefit through our retained equity and royalty exposure, while Blue Jay moves forward as a focused, well-capitalized company.”

“The successful closing of our seed round provides Blue Jay Gold with a solid foundation to advance exploration across our Ontario portfolio,” said Geordie Mark, CEO of Blue Jay Gold. “We’re grateful for the strong support from our shareholders and look forward to executing a disciplined, data-driven exploration program to unlock the potential of our assets.”

Certain directors and officers of Riverside and Blue Jay participated in the private placement, subscribing for 268,750 Blue Jay Shares in the aggregate; each such director or officer is a “related party” and each such subscription is a “related party transaction” within the meaning of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101“). The Company is relying on exemptions from the formal valuation and minority shareholder approval requirements under section 5.5(a) and 5.7(1)(a) of MI 61-101, respectively, in respect of such insider participation, in each case, as the fair market value of the private placement, insofar as it involves related parties does not exceed 25% of the Company’s market capitalization.

The balance of the Blue Jay Shares held by Riverside will be distributed to Riverside’s shareholders in connection with Riverside’s previously announced plan of arrangement under section 288 of the Business Corporation Act (British Columbia) (the “Arrangement“), which will be effected pursuant to the arrangement agreement dated January 27, 2025 between Blue Jay and Riverside (the “Arrangement Agreement“). The Arrangement received Riverside shareholder approval on March 31, 2025 and the final approval of the Supreme Court of British Columbia on April 3, 2025.

The Arrangement Agreement and additional details about the Arrangement are included in the Company’s management information circular dated February 18, 2025 which are each available on Riverside’s SEDAR+ profile at www.sedarplus.ca and on the Company’s website at www.rivres.com.

About Blue Jay Gold

Blue Jay Gold Corp. is a Canadian gold exploration company focused on high-grade discovery in Ontario’s prolific Beardmore-Geraldton and Wawa Greenstone Belts, regions known for hosting numerous past-producing and active gold mines. The Company’s flagship asset, the Pichette Project, features extensive banded iron formation (BIF) trends and high-grade historical gold intercepts, offering near-surface discovery potential. With three strategically located projects and a leadership team experienced in geology and capital markets, Blue Jay Gold is advancing a disciplined, modern exploration strategy in one of Canada’s most prospective and mining-friendly jurisdictions.

About Riverside Resources Inc.

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has over $4M in cash, no debt and less than 75M shares outstanding with a strong portfolio of gold-silver and copper assets and royalties in North America. Riverside has extensive experience and knowledge operating in Mexico and Canada and leverages its large database to generate a portfolio of prospective mineral properties. In addition to Riverside’s own exploration spending, the Company also strives to diversify risk by securing joint-venture and spin-out partnerships to advance multiple assets simultaneously and create more chances for discovery. Riverside has properties available for option, with information available on the Company’s website at www.rivres.com.

About Blue Jay Gold Corp.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Investor Relations Riverside Resources Inc. Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, that the Arrangement may not occur within the timelines contemplated or at all, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

In this episode of ‘Proven and Probable,’ we engage with Bob Moriarty, a distinguished commentator on geopolitical and economic affairs. Bob’s extensive experience includes serving as a Marine F-4B pilot during the Vietnam War, where he flew over 820 combat missions and became one of the most highly decorated pilots of the conflict.

We delve into the recent tragic collision between an American Airlines plane and a military helicopter near Washington, D.C., exploring Bob’s insights on the incident, the National Transportation Safety Board’s investigative approach, and media coverage.

The discussion also covers U.S. tariff policies, international responses, and the current state of gold and precious metals, providing a comprehensive analysis of these pressing issues.

Join us for an in-depth conversation that offers clarity and depth on these complex topics.

In 2024, Americans faced several financial challenges that impacted their ability to save and manage their finances effectively. Inflation remained a top concern, leading to increases in the cost of essentials such as housing, groceries, and utilities, and straining household budgets.

Credit card debt also reached record highs. Rising interest rates on credit cards and loans made it harder for consumers to pay down their balances. Additionally, many households depleted the excess savings they accumulated during the pandemic, leaving them with less of a financial cushion.

With all of this in mind, Yahoo Finance partnered with Marist Poll to survey more than 3,000 banked adults in the U.S. (those with at least one checking or savings account) to shed light on the financial struggles and concerns facing households. Here’s what Americans say have been their biggest barriers to saving and how they feel about their finances heading into 2025. (See our full methodology here.)

This embedded content is not available in your region.

Key findings

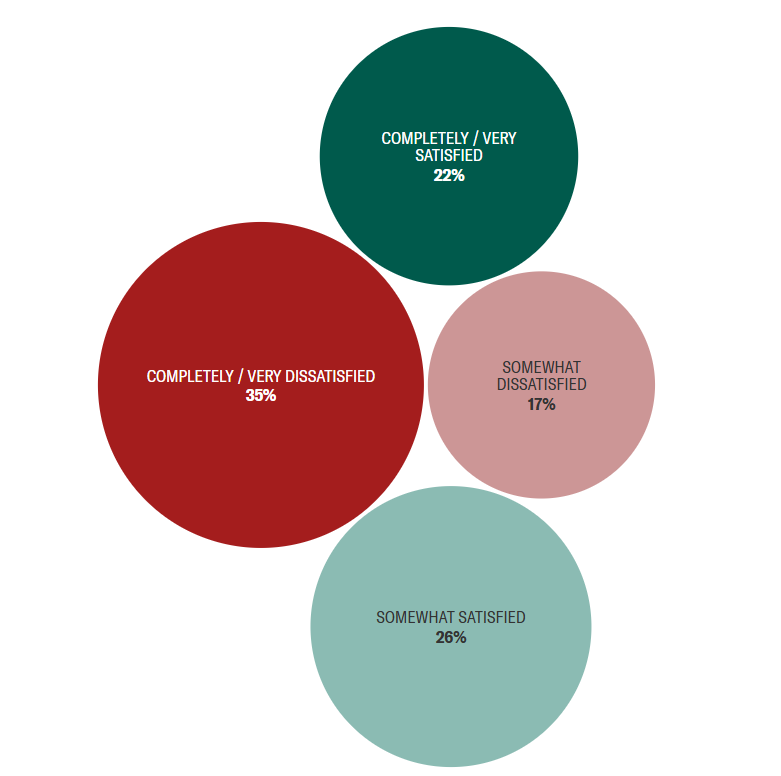

Only 22% of respondents report being very or completely satisfied with their savings, while 35% are very or completely dissatisfied. Forty percent of women are very or completely dissatisfied with their savings, compared to 28% of men.

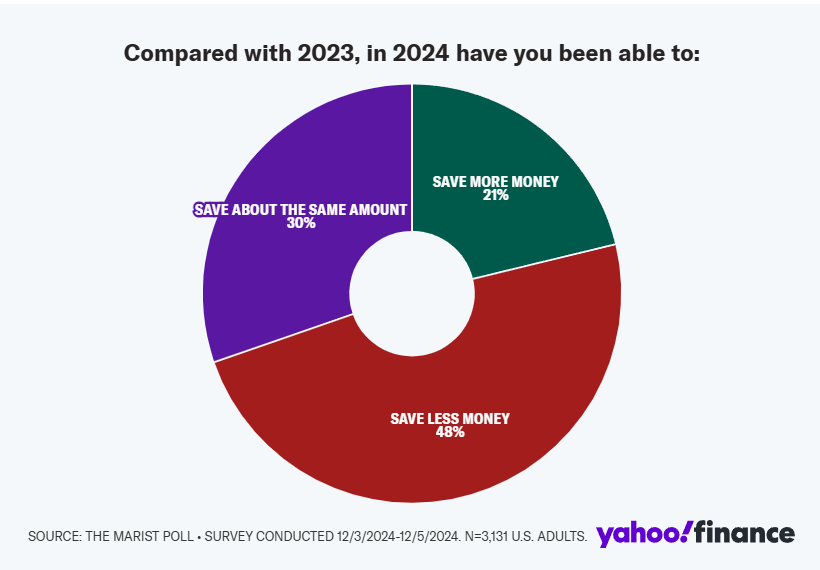

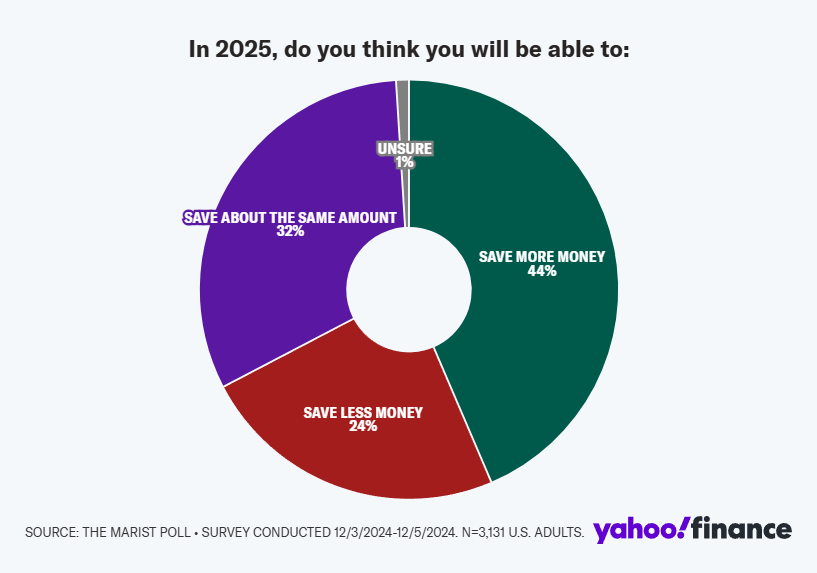

Nearly half (48%) of respondents saved less in 2024 compared to the previous year, with only 21% saving more.

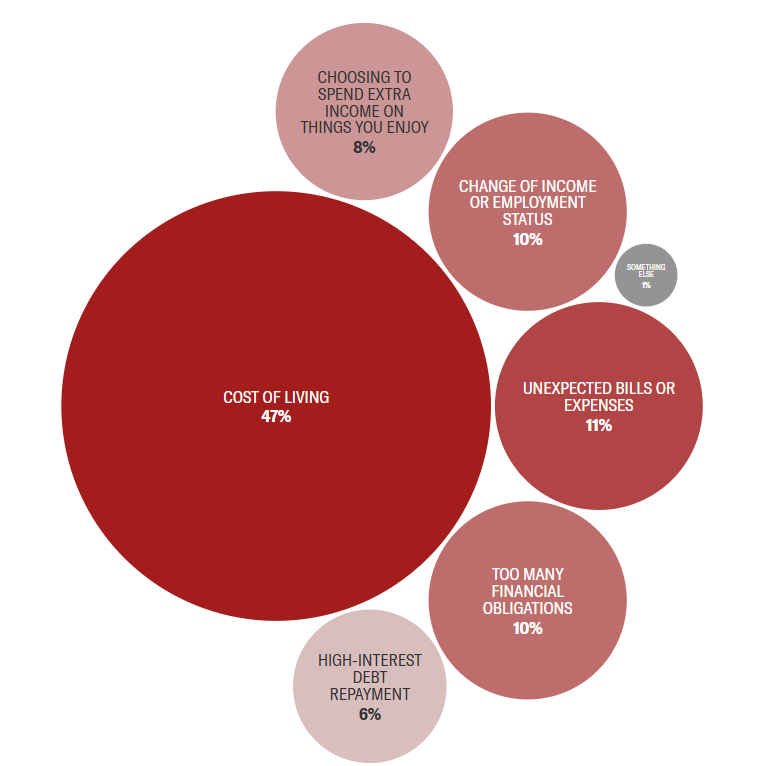

Nearly half (47%) of respondents cite the cost of living as their biggest obstacle to saving.

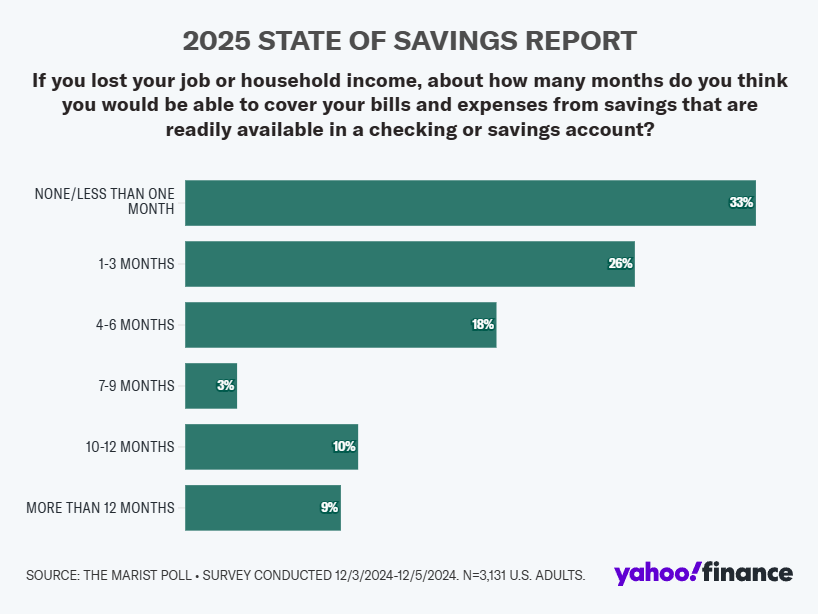

One-third (33%) of respondents couldn’t cover bills for even one month if they lost their income.

44% of respondents believe they will save more in 2025, with optimism highest among Gen Z (63%) and millennials (53%).

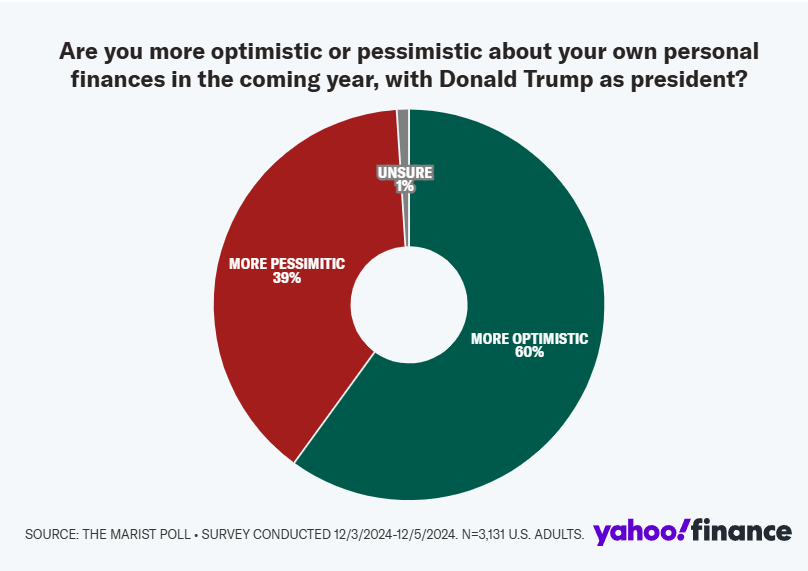

60% of respondents say they are more optimistic about their finances for the coming year with Donald Trump as president. This optimism crosses generational lines, with Gen Z (70%) as the most optimistic.

The Yahoo Finance/Marist Poll 2025 national survey on the state of savings

We set out to learn more about how higher costs and competing financial obligations have impacted Americans’ savings. Here’s what we found:

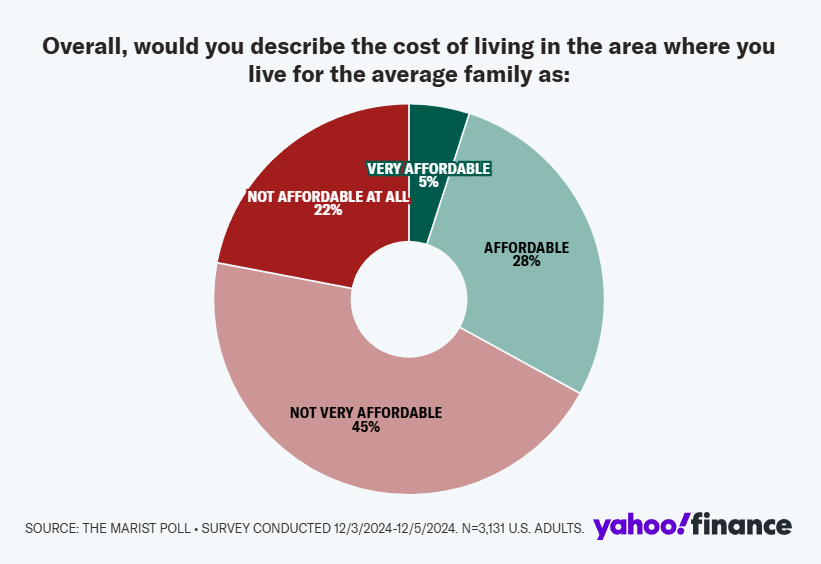

Two-thirds of respondents say the cost of living for the average family in their area is not affordable

In a post-COVID-19 world, the rising cost of living dominated financial news headlines. Many households felt the pinch as inflation reached a 40-year high of 9.1% in June 2022. Though the inflation rate has since tempered (the Consumer Price Index was up 2.7% year over year in November 2024), the sky-high costs of housing, groceries, and other essentials are here to stay for the foreseeable future.

Overall, our survey found that most respondents describe the cost of living in their area as “not very affordable” (45%), while another 22% say it’s not affordable at all.

On the other hand, Gen Z respondents were more likely to describe the cost of living as “very affordable” (9%) compared to other generations: millennials (8%), Gen X (3%), and baby boomers/silent/greatest generations (2%).

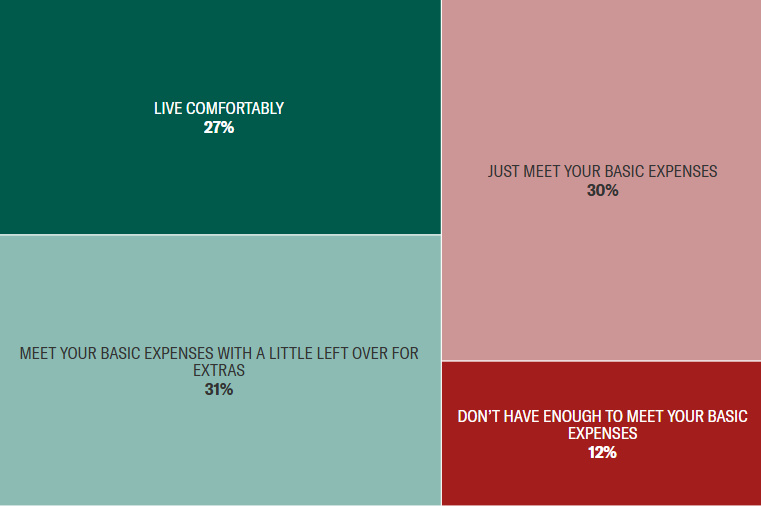

Only one-quarter of Americans say they live comfortably

Not only are survey respondents unhappy with the cost of living in their area, but most are struggling to pay for necessities while putting money away for the future.

Just over a quarter of survey respondents say they live comfortably. Older Americans (baby boomer/silent/greatest generations) were more likely to say they live comfortably (40%).

Meanwhile, 31% of respondents are able to meet their basic expenses with a little money left over for extras, while another 30% are just able to meet their basic expenses. And 12% say they don’t have enough money to cover their basic living expenses.

More women are dissatisfied with how much they’ve saved than men

Everyone’s savings goals are different, based on lifestyle, family size, debt obligations, and more. When it comes to whether Americans are satisfied with how much they’ve saved so far, the results are mixed.

Thirty-five percent of respondents in our survey are dissatisfied with the amount of money they’ve saved. Women (40%) are more likely than men (28%) to say that they are very or completely dissatisfied with their savings — perhaps not surprising given the financial challenges that many women face, including the gender pay gap and a higher burden of caregiving responsibilities.

About half of Americans say they saved less in 2024 compared to 2023

This past year proved to be a difficult one for Americans’ savings. Despite historically high deposit account interest rates, consumers were also faced with inflation, skyrocketing interest rates on debt, record-level education costs, and more.

Nearly half of respondents in our survey report they saved less money in 2024 compared to 2023; only 21% reported saving more money. Nearly a third of respondents said they saved about the same amount.

Overall, women were more likely to say they’ve saved less money in 2024 than they did in 2023 (53% versus 42% of men), especially millennial and Gen X women (57% and 59%, respectively).

Younger generations are more optimistic about their savings potential in the new year

With a new year — and a new administration — we sought to find out how Americans believe their savings habits will change in 2025.

It’s not all doom and gloom, especially for younger savers. Younger Americans are more likely to say they will save more: 63% of Gen Z and 53% of millennials versus 44% of Gen X and 25% of baby boomers/silent/greatest generations.

Most likely to save about the same amount in 2025 are those in the baby boomer/silent/greatest generations (44%). Women, however, are more likely than men to say they will save less this year (27% vs. 20%, respectively).

Cost of living has been the most significant barrier to saving

We wanted to learn more about the various challenges savers are facing that are preventing them from reaching their savings goals.

Nearly half of respondents (47%) pointed to cost of living as their biggest obstacle when it comes to saving money. Other common reasons included unexpected bills or expenses (11%), too many financial obligations (10%), and change of income or employment status (10%).

Older Americans were most likely to report they face no challenges to saving money (19%).

Gen Zers and millennials are most likely to ask family and friends for help in a financial emergency

In times of financial distress, there are several avenues you might take to cover your bills — some of which are better for your bottom line than others.

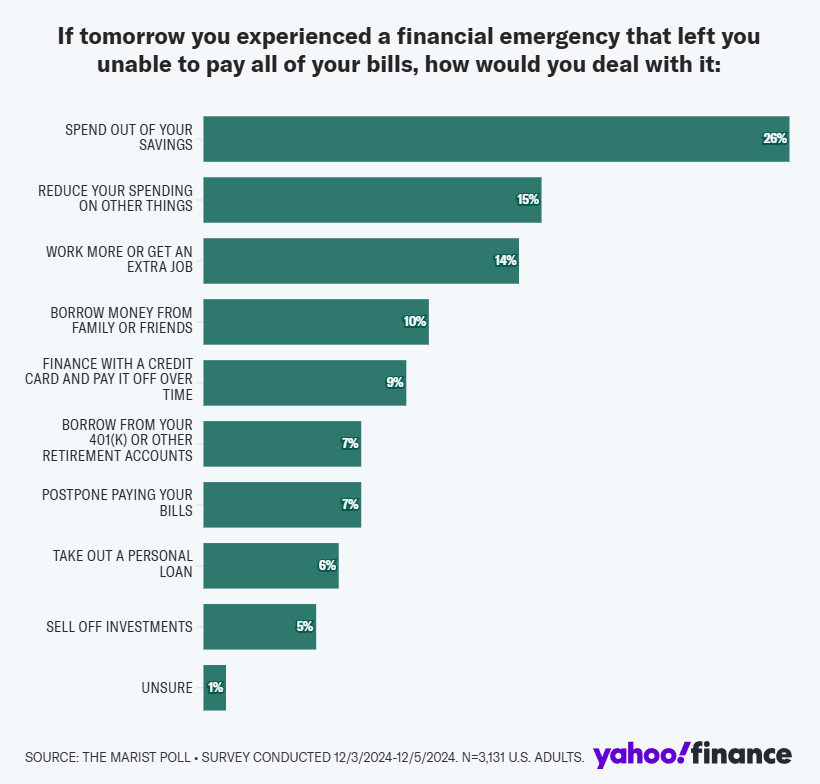

The largest percentage of respondents (26%) say that their solution would be to tap into their savings. Fifteen percent say they’d cut down on their spending, while 14% would pick up an extra job or more hours at work.

Another 10% of respondents say they would ask a family member or friend for help in a financial emergency, with Gen Zers and millennials the most likely to do so (15% for both).

Gen Xers and baby boomers/silent/greatest generations are more likely to put their expenses on a credit card (10%).

A third of households couldn’t cover one month’s worth of bills if they lost their job or source of income

Most experts recommend saving at least three to six months’ worth of expenses in an emergency fund. However, given the many barriers to saving that Americans face, not everyone is able to meet this guideline.

The average length of time respondents could cover their expenses using money that is readily available in their checking or savings account is seven months.

However, about 1 in 3 respondents say they would not be able to cover their bills and expenses for even one month. Gen Z (38%) and millennials (41%) are more likely than other generations to say they could not pay their bills for one month.

In contrast, Gen X and baby boomers/silent/greatest generations (19% for both) are more likely than younger generations to have enough savings to manage for one year or more.

60% of Americans are more optimistic about their finances in the coming year with Donald Trump as president

For better or worse, with a new administration often comes a new economic agenda. And most Americans are expecting positive changes.

A majority of respondents (60%) are more optimistic about their personal finances with Trump as the next president. This was the consensus across generations, with Gen Z being the most optimistic (70%). Baby boomers/silent/greatest generations were the most pessimistic (46%).

This survey of 3,131 adults was conducted Dec. 3 through Dec. 5, 2024, by the Marist Poll sponsored in partnership with Yahoo Finance. Adults 18 years of age and older residing in the United States were contacted through a multi-mode design: By phone using live interviewers, by text, or online. All potential respondents were screened for age.

Probability-based sampling frames include RDD landline plus listed landline, RDD cell phone sample plus cell phone sample based on billing address to account for inward and outward mobility within a state. These samples were provided by Dynata and used to administer the surveys collected via phone and text to web. A sampling frame based on aggregated non-probability online research panels was randomly selected from Cint’s digital insights platform to administer the surveys collected via web.

Survey questions were available in English or Spanish. All samples were selected to ensure that each region was represented in proportion to its adult population. The samples were then combined and balanced to reflect the 2022 American Community Survey five-year estimates for age, gender, income, race, and region.

Results for all adults (n=3,131) are statistically significant within ±2.1 percentage points. Results for banked households (n=2,828) are statistically significant within ±2.2 percentage points. The design effect for this survey is 1.4 which has been incorporated in the calculation of all reported margins of error. The partisan breakdown for this survey among registered voters is 38% Democrat, 36% Republican, and 25% Independent.

As of December 18th, 2024 the DSI for gold is 48, for silver 21. The highest value for gold based on the DSI showed 89 back in May of this year. On the same day silver reached a peak DSI of 90. Those numbers are not good enough to make a major top in either gold or silver. For example, it took a DSI of 96 to mark the top for silver in April of 2011 and a DSI of 95 on January 21, 1980 to mark the all-time high for silver. In my view gold and silver are going to go a lot higher not far off. I expect silver to break its all time high of $50.75 in the next six months or so. Once silver makes a new all-time high I think it will be off to the races.

Tax Loss Silly Season is that six week or so period starting in November and running into just before Christmas when investors clean out the stocks they own that have gone down the most to be able to write off the losses for the current year. It’s the worst time of the year to sell and the best time of the year to buy. Since so many junior lottery tickets have been hammered this year there has been a lot of carnage in the space due to the lack of liquidity and the sheer number of punters willing to take anything on offer for their shares.

But all things change.

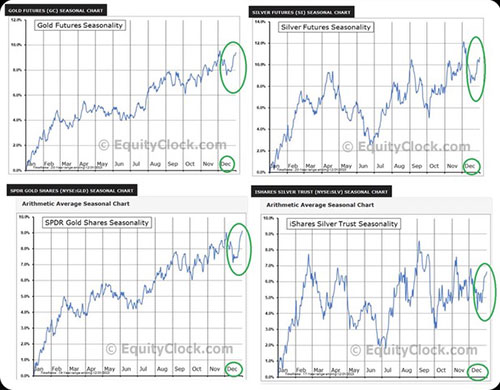

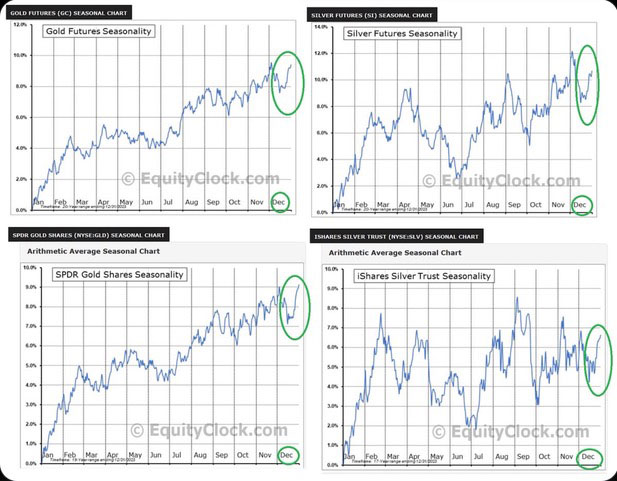

The ten-week period from the middle of December each year into the end of February is seasonally the best time of the year for gold and silver. In the past five days, gold has gone down about $130 or over 5%. Now looks to be a good buying opportunity if Trump isn’t whacked between now and a month from now. If he gets whacked, it would be an extraordinary opportunity as the US moves into a civil war.

I’m Maurice Jackson, the founder of Proven and Probable. We specialize in identifying under valued stocks that have a massive potential upside. Today we are highlighting what we believe to be the best silver proposition for your portfolio nestled in the bottom of the Golden Triangle located in British Columbia, which has seen over $5B in M&A since 2018!

We have been buyers of this stock 4 years and counting. Dolly Varden Silver has begin the first in a series of press release announcing the results from their 2024 Drill Program of 25,000 Meters. Find out why Eric Sprott, Rick Rule, Hecla Mining, Fury Gold Mines, Fidelity Investments, Sprott, Sprott USA, Delbrook, and High-Net-Worth investors, with a 7% float! Watch now!

Dolly Varden Silver Corporation is a mineral exploration company focused on advancing its 100% held Kitsault Valley Project located in the Golden Triangle of British Columbia, Canada, 25kms by road to deep tide water.

The 163 sq. km. project hosts the high-grade silver and gold resources of Dolly Varden and Homestake Ridge along with the past producing Dolly Varden and Torbrit silver mines. It is considered to be prospective for hosting further precious metal deposits, being on the same structural and stratigraphic belts that host numerous other, on-trend, high-grade deposits, such as Eskay Creek and Brucejack. The project also contains the Big Bulk property which is prospective for porphyry and skarn style copper and gold mineralization, similar to other such deposits in the region (Red Mountain, KSM, Red Chris).

The Company’s common shares are listed and traded on the TSX.V under the symbol DV and on the OTCQX system under the symbol DOLLF.

WEBSITE: https://provenandprobable.com/ 🥇🥈Get Your Online Gold/ Silver Here 🥇🥈 Call Me Directly at 855.505.1900 or Email: Maurice@MilesFranklin.com