Toronto, Ontario–(Newsfile Corp. – June 23, 2026) – Coyote Copper Mines Inc. (TSXV: CCMM) (“CCMM” or the “Corporation”) announces that further to its news releases dated May 13, 2026, May 25, 2026, June 2, 2026 and June 15, 2026 it has closed the final tranche (the “Final Tranche“) of its previously announced non-brokered private placement financing of up to 34,353,483 Units issued at a price of CAD$0.25 per Unit with each Unit consisting of one (1) fully-paid Common Share (a “CommonShare“) and one half (½) Common Share purchase warrant (a “HalfWarrant“) in the capital of the Corporation, for aggregate gross proceeds of $8,588,370.75 to be used for exploration and general corporate purposes (the “Offering“).

Two Half Warrants will entitle the holder thereof to purchase one common share of the Corporation. Each Warrant will expire thirty six (36) months from the date of issue and will entitle the holder thereof to purchase one Common Share at a price of CAD$0.50 per Warrant Share within 36 months from the date of issue.

An aggregate of 20,956,830 Units was sold under the First Tranche for total gross proceeds of C$5,239,207.50

An aggregate of 13,396,313 Units was sold under the Final Tranche for total gross proceeds of C$3,349,163.25

In connection with closing of the financing, the Company paid aggregate finder’s fees consisting of (i) C$528,085.00 (the “Cash Consideration”) and (ii) 1,836,260 compensation warrants (the “Compensation Warrants”) to eligible finders. Each Compensation warrant entitles the holder to acquire one Common Share at a price of C$0.50 per Common Share for a period of 36 months from the date of issuance of the Compensation Warrant.

The closing of the Financing is subject to the receipt of all necessary regulatory approvals, including the final approval of the TSX Venture Exchange. All securities issued and issuable pursuant to the First Tranche of the Offering are subject to a four-month plus one day hold period commencing on the date of issuance.

Neither the Exchange nor its Regulation Services Provider (as that term is defined in the policies of the Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in the United States. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“) or any state securities laws and may not be offered or sold within the United States or to U.S. persons unless registered under the U.S. Securities Act and applicable state securities laws or an exemption from such registration is available.

information is based on currently available competitive, financial and economic data and operating plans, strategies or beliefs as of the date of this news release, but involve known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, performance or achievements of the Corporation to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors may be based on information currently available to the Corporation including information obtained from third-party industry analysts and other third-party sources, and are based on management’s current expectations or beliefs. Any and all forward-looking information contained in this news release is expressly qualified by this cautionary statement.

as of the date of this news release and, other than as required by law, the Corporation disclaims any obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information.

Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking information prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected. Although the Corporation has attempted to identify important risks, uncertainties and factors which could cause actual results to differ materially, there may be others that cause results not to be as anticipated, estimated or intended. The Corporation does not intend, and does not assume any obligation, to update this forward-looking information except as otherwise required by applicable law.

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

Yahoo Finance

M

ADVERTISEMENT

This is a paid press release. Contact the press release distributor directly with any inquiries.

AIAI Holdings Unveils AI Integration Playbook for Portfolio Companies

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

“Transformational AI is intelligence grounded in a business’s actual operations, acting as a core driver of value rather than an add-on,” said Todd Furniss, Chief Executive Officer and Co-founder of AIAI Holdings Corporation. “At Ai2 we don’t sell this technology, we buy companies then bake it into their DNA, converting complex services into durable cash flows. This requires meeting each portfolio company where it is today, understanding its workflows and data environment, and then building the appropriate foundation for AI-enabled value creation. Disorganized or incomplete data is not a weakness; it is the norm. Identifying, organizing, and analyzing that information is a critical part of the transformation process. Once that foundation is in place, we can implement targeted AI and operational strategies designed to drive both revenue growth and EBITDA expansion wherever the greatest opportunities exist.”

The framework provides Ai² with a disciplined, repeatable process for assessing newly acquired and existing portfolio companies, identifying practical AI-enabled value creation opportunities, evaluating operational and data readiness, and developing phased implementation plans that can be executed responsibly over time.

The Company is also pleased to announce that C.C. Carlton Industries (“CCCI”), a wholly owned subsidiary of Ai² and a Central Texas construction company with more than 30 years of operating history, is among the first Ai2 portfolio companies to move through the Company’s structured Transformational AI assessment and onboarding process.

“C.C. Carlton Industries is excited to be an initial benefactor of Ai²’s Transformational AI integration framework,” said Ben Lyon, CEO of C.C. Carlton Industries. “As an operating business with established workflows, project complexity, customer requirements, safety considerations, and opportunities for process improvement, we believe TAI assessment process can help identify practical opportunities to improve efficiency, quality, safety, speed to completion, and decision-making over time.”

The Company expects that early implementation work will help establish repeatable processes and reusable AI tools that can support future acquisitions and additional portfolio company integrations. Over time, Ai² intends to build a portfolio-wide Transformational AI playbook that can support faster assessment, improved execution and scalability across diverse industries.

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

“Transformational AI is intelligence grounded in a business’s actual operations, acting as a core driver of value rather than an add-on,” said Todd Furniss, Chief Executive Officer and Co-founder of AIAI Holdings Corporation. “At Ai2 we don’t sell this technology, we buy companies then bake it into their DNA, converting complex services into durable cash flows. This requires meeting each portfolio company where it is today, understanding its workflows and data environment, and then building the appropriate foundation for AI-enabled value creation. Disorganized or incomplete data is not a weakness; it is the norm. Identifying, organizing, and analyzing that information is a critical part of the transformation process. Once that foundation is in place, we can implement targeted AI and operational strategies designed to drive both revenue growth and EBITDA expansion wherever the greatest opportunities exist.”

The framework provides Ai² with a disciplined, repeatable process for assessing newly acquired and existing portfolio companies, identifying practical AI-enabled value creation opportunities, evaluating operational and data readiness, and developing phased implementation plans that can be executed responsibly over time.

The Company is also pleased to announce that C.C. Carlton Industries (“CCCI”), a wholly owned subsidiary of Ai² and a Central Texas construction company with more than 30 years of operating history, is among the first Ai2 portfolio companies to move through the Company’s structured Transformational AI assessment and onboarding process.

“C.C. Carlton Industries is excited to be an initial benefactor of Ai²’s Transformational AI integration framework,” said Ben Lyon, CEO of C.C. Carlton Industries. “As an operating business with established workflows, project complexity, customer requirements, safety considerations, and opportunities for process improvement, we believe TAI assessment process can help identify practical opportunities to improve efficiency, quality, safety, speed to completion, and decision-making over time.”

The Company expects that early implementation work will help establish repeatable processes and reusable AI tools that can support future acquisitions and additional portfolio company integrations. Over time, Ai² intends to build a portfolio-wide Transformational AI playbook that can support faster assessment, improved execution and scalability across diverse industries.

The Company emphasized that the framework is not intended to represent a complete enterprise-wide transformation of each acquired business. Rather, the objective is to ensure that meaningful Transformational AI integration begins early in the ownership cycle, with selected use cases identified, prioritized, tested, and moved into active implementation during the initial post-acquisition period.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai2) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai2 is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries.

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

Yahoo Finance

M

ADVERTISEMENT

This is a paid press release. Contact the press release distributor directly with any inquiries.

AIAI Holdings Unveils AI Integration Playbook for Portfolio Companies

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

“Transformational AI is intelligence grounded in a business’s actual operations, acting as a core driver of value rather than an add-on,” said Todd Furniss, Chief Executive Officer and Co-founder of AIAI Holdings Corporation. “At Ai2 we don’t sell this technology, we buy companies then bake it into their DNA, converting complex services into durable cash flows. This requires meeting each portfolio company where it is today, understanding its workflows and data environment, and then building the appropriate foundation for AI-enabled value creation. Disorganized or incomplete data is not a weakness; it is the norm. Identifying, organizing, and analyzing that information is a critical part of the transformation process. Once that foundation is in place, we can implement targeted AI and operational strategies designed to drive both revenue growth and EBITDA expansion wherever the greatest opportunities exist.”

The framework provides Ai² with a disciplined, repeatable process for assessing newly acquired and existing portfolio companies, identifying practical AI-enabled value creation opportunities, evaluating operational and data readiness, and developing phased implementation plans that can be executed responsibly over time.

The Company is also pleased to announce that C.C. Carlton Industries (“CCCI”), a wholly owned subsidiary of Ai² and a Central Texas construction company with more than 30 years of operating history, is among the first Ai2 portfolio companies to move through the Company’s structured Transformational AI assessment and onboarding process.

“C.C. Carlton Industries is excited to be an initial benefactor of Ai²’s Transformational AI integration framework,” said Ben Lyon, CEO of C.C. Carlton Industries. “As an operating business with established workflows, project complexity, customer requirements, safety considerations, and opportunities for process improvement, we believe TAI assessment process can help identify practical opportunities to improve efficiency, quality, safety, speed to completion, and decision-making over time.”

The Company expects that early implementation work will help establish repeatable processes and reusable AI tools that can support future acquisitions and additional portfolio company integrations. Over time, Ai² intends to build a portfolio-wide Transformational AI playbook that can support faster assessment, improved execution and scalability across diverse industries.

The Company emphasized that the framework is not intended to represent a complete enterprise-wide transformation of each acquired business. Rather, the objective is to ensure that meaningful Transformational AI integration begins early in the ownership cycle, with selected use cases identified, prioritized, tested, and moved into active implementation during the initial post-acquisition period.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai2) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai2 is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries.

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

The forward-looking statements in this press release are based on information available to us as of the date hereof, and we disclaim any intention to, and, except as may be required by law, undertake no obligation to, update or revise forward-looking statements to reflect events or circumstances that subsequently occur or of which the Company hereafter become aware. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

West Point Gold CEO Derek Macpherson breaks down the latest high-grade drill results and what they mean for the company future. See why this 66.2 meter intercept at 6.57 GPT Au is a critical indicator for the project’s potential. Netting a 435 Gram/Meter is exceptional!

This update is designed for investors tracking West Point Gold who want a clear view of the company capital structure, ownership, and current analyst coverage. We review the specific technical data from the recent drilling program to provide a grounded perspective on the robust vein system currently being tested.

By evaluating these high-grade drill results, viewers will better understand how the company is positioning its assets within the broader gold mining stocks market. We focus strictly on the data provided by the CEO to help you assess the operational progress and the strategic outlook for the site.

Subscribe for weekly mining investment analysis updates, and comment below on which exploration project you want us to cover next.

Few prognosticators and only a rare investor sees the enormous impact Israel’s failed war on Iran will bring. By closing the Strait of Hormuz Iran turned the tide of battle. Their actions have redrawn the borders of the Middle East.

Persia (Now Iran since 1935) was the reigning power in the Middle East for 2500 years when Saudia Arabia and the rest of the GCC were herding goats and sheep. Anyone both sane and fairly sober now recognize the incredible mistake Trump and the US made getting dragged into another war of aggression on Israel’s part. The primary effect of the war has been to reestablish Iran as the dominant power in the region as Israel’s planned “Greater Israel” landed on the garbage heap of history.

There are dozens of surprise knock-on effects from the war that are only beginning to be visible. While closing the Strait of Hormuz effectively won the war for Iran, it also demonstrated the danger of a single country having within its power the ability to destroy the economy of the world. Other oil export dependent countries in the area now recognize the importance of having a Plan-B for moving their products.

While admittedly the ability of the west to tap the Strategic Petroleum Reserves in various countries in conjunction with China dropping its import requirements of crude oil managed to keep the retail price of fuel under control so far, it’s obvious the world needs a number of Plan Bs for all sorts of commodities that prior to the war few recognized.

Uranium is going to be viewed as a more attractive source of energy not subject to the whims of countries in the Middle East. I see the demand for uranium to be used in new reactors increasing a lot. Anything related to agriculture will be viewed as an attractive alternative to supplies dependent on the Middle East.

A company contacted me recently with a compelling fertilizer story. The company is named Sage Potash (SAGE-V) and has a large potash project in eastern Utah. But you need to know a little about growing plants. They need three different chemicals for ideal growth, nitrogen, phosphorus and potassium. Potash supplies the potassium. For the US Canada supplies about 81% of the needed material with Russia providing an additional 15%. The US only produces 5-10% of the potash demanded, the rest is imported. Potash costs about $300 a tonne. The USGS reports that Utah contains about 2 billion tonnes of potash. Sage shows a grade of 36-46% KCL, one of the highest grades reported in the world. Sage plans on using a solution mining technique where they pump brine into a deep well to the location of the 5.5-7.3 meter thick intercept of potash.

Sage reports two beds of high-grade potash, the Upper Cycle 18 measuring 7.26 meter of 46% KCL for 179 million tonnes and Lower Cycle 18 giving 5.46 meters of 35.77% KCL for 128 million tonnes. Sage has begun a drill program designed to expand the resource in the 43-101. The current 43-101 shows an inferred resource of 298 million tonnes at 36-46% KCL. The current PEA demonstrated a NPV of $502 million with an after-tax profit of 39%. The company believes they can release an update 43-101 and results from the current drill program by September. With a current market cap of about $22 million, about 0.4% of the NPV the shares seem absurdly cheap to me.

Sage is an advertiser and I have bought shares in the open market. Naturally I am biased so do your own due diligence. Their only problem is a lack of visibility.

Sage Potash CorpSAGE-V $.13 Jun 19, 2026 SGPTF-OTCQB 171 million shares Sage Potash website

Toronto, Ontario–(Newsfile Corp. – June 17, 2026) – Coyote Copper Mines Inc. (TSXV: CCMM) (“CCMM” or the “Corporation”) announces that further to its news releases dated May 13, 2026, May 25, 2026, June 2, 2026 and June 15, 2026 it has closed the final tranche (the “Final Tranche“) of its previously announced non-brokered private placement financing of up to 34,000,000 Units issued at a price of CAD$0.25 per Unit with each Unit consisting of one (1) fully-paid Common Share (a “CommonShare“) and one half (½) Common Share purchase warrant (a “HalfWarrant“) in the capital of the Corporation, for aggregate gross proceeds of $8,500,000 to be used for exploration and general corporate purposes (the “Offering“).

Two Half Warrants will entitle the holder thereof to purchase one common share of the Corporation. Each Warrant will expire thirty six (36) months from the date of issue and will entitle the holder thereof to purchase one Common Share at a price of CAD$0.50 per Warrant Share within 36 months from the date of issue.

An aggregate of 20,956,830 Units was sold under the First Tranche for total gross proceeds of C$5,239,207.50

An aggregate of 13,043,170 Units was sold under the Final Tranche for total gross proceeds of C$3,260,792.50

In connection with closing of the financing, the Company paid aggregate finder’s fees consisting of (i) C$528,085.00 (the “Cash Consideration”) and (ii) 1,836,260 compensation warrants (the “Compensation Warrants”) to eligible finders. Each Compensation warrant entitles the holder to acquire one Common Share at a price of C$0.50 per Common Share for a period of 36 months from the date of issuance of the Compensation Warrant.

The closing of the Financing is subject to the receipt of all necessary regulatory approvals, including the final approval of the TSX Venture Exchange. All securities issued and issuable pursuant to the First Tranche of the Offering are subject to a four-month plus one day hold period commencing on the date of issuance.

Neither the Exchange nor its Regulation Services Provider (as that term is defined in the policies of the Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in the United States. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“) or any state securities laws and may not be offered or sold within the United States or to U.S. persons unless registered under the U.S. Securities Act and applicable state securities laws or an exemption from such registration is available.

Cautionary Statement Regarding Forward-Looking Information

This news release contains statements which constitute “forward-looking information” within the meaning of applicable securities laws, including statements regarding the plans, intentions, beliefs and current expectations of the Corporation.

Often, but not always, forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes” or variations (including negative variations) of such words and phrases, or statements formed in the future tense or indicating that certain actions, events or results “may”, “could”, “would”, “might” or “will” (or other variations of the forgoing) be taken, occur, be achieved, or come to pass. Forward-looking information includes information regarding the Offering, the business plans and expectations of the Corporation and expectations for other economic, business, and/or competitive factors. Forward-looking information is based on currently available competitive, financial and economic data and operating plans, strategies or beliefs as of the date of this news release, but involve known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, performance or achievements of the Corporation to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors may be based on information currently available to the Corporation including information obtained from third-party industry analysts and other third-party sources, and are based on management’s current expectations or beliefs. Any and all forward-looking information contained in this news release is expressly qualified by this cautionary statement.

Investors are cautioned that forward-looking information is not based on historical facts but instead reflect management’s expectations, estimates or projections concerning future results or events based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made. Forward-looking information reflects management’s current beliefs and is based on information currently available to them and on assumptions they believe to be not unreasonable in light of all of the circumstances. In some instances, material factors or assumptions are discussed in this news release in connection with statements containing forward-looking information. Such material factors and assumptions include, but are not limited to those set forth in the Filing Statement under the caption “Risk Factors”. Although the Corporation has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended. Forward-looking information contained herein is made as of the date of this news release and, other than as required by law, the Corporation disclaims any obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information.

Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking information prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected. Although the Corporation has attempted to identify important risks, uncertainties and factors which could cause actual results to differ materially, there may be others that cause results not to be as anticipated, estimated or intended. The Corporation does not intend, and does not assume any obligation, to update this forward-looking information except as otherwise required by applicable law.

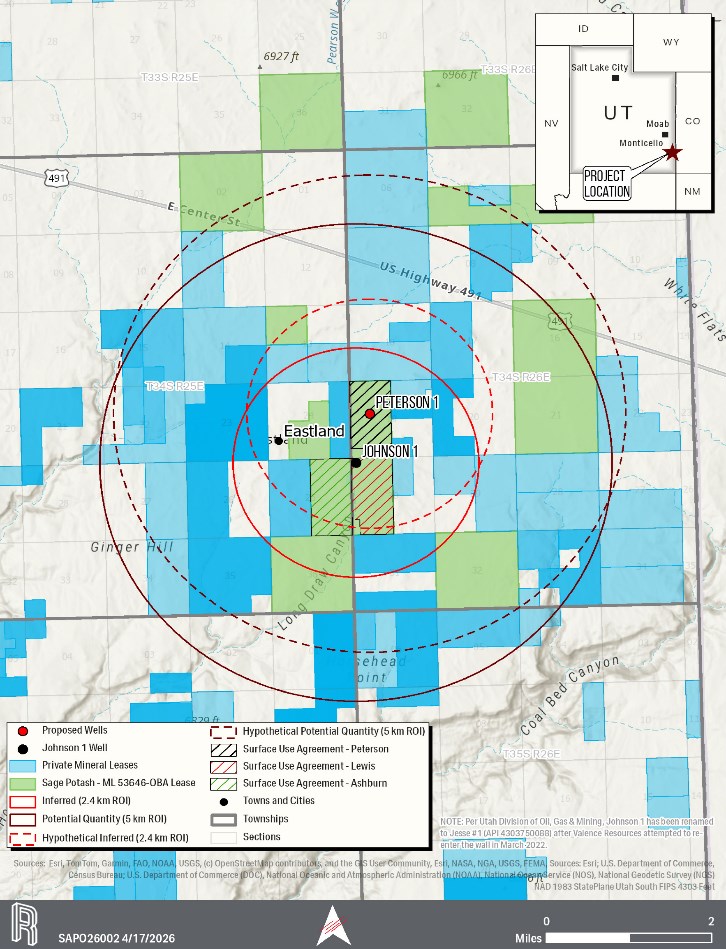

South Jordan, Utah and Vancouver, British Columbia–(Newsfile Corp. – June 18, 2026) – Sage Potash Corp. (TSXV: SAGE) (OTCQB: SGPTF) (“Sage Potash” or the “Company”) is pleased to announce the Company has now received all required approvals and permits from both the local County and the State of Utah to proceed with drilling operations at its Sage Plain project in San Juan County in Utah. Final approvals were granted following a customary site inspection conducted on May 28, 2026, by representatives of the Utah Division of Oil, Gas and Mining (“DOGM”), accompanied by personnel from Sage Potash and its contractors, along with posting of drilling related bonds.

As previously announced, the Company has engaged Westrock Energy Services (USA) Inc. to oversee and coordinate all aspects of the drilling program, alongside Drake Well Service Inc. as drilling contractor. The Company will be drilling a 1.275 km (3/4 mile) step out hole to the NNE from the maiden hole from which the Company’s current resource is calculated.

Figure 1 – Peterson 1 drill hole location relative to Johnson 1 and hypothetical resource expansion radius at the Sage Plain Potash Project, Utah

Historical drillhole data has identified significant potash mineralization within the Cycle 18 Upper and Lower beds at depths of approximately 2,100 metres (6,890 feet), demonstrating strong economic potential across the Project area. As outlined in the Company’s April 7, 2026 news release, the current drilling program is specifically designed to target these potash-bearing horizons and expand and upgrade the resource confidence levels for what management believes to be one of the most prospective and high-grade solution mining potash targets in the United States.

In addition to confirming potash mineralization, the drilling program will include a comprehensive hydrogeological assessment. The Company plans to conduct targeted Drill Stem Tests (“DSTs”) in formations exhibiting sufficient water flow in order to evaluate yield rates and water quality (primarily targeting saline non-potable aquifers) for future solution mining operations. Fluid sampling and detailed water analysis will also be undertaken to support future processing design and cavern development.

Following completion of coring operations, the open borehole will undergo an extensive suite of geophysical wireline logs. Recovered potash horizon core samples will then be transported to an independent analytical laboratory for detailed geological logging, geochemical sampling, and assaying under strict QA/QC protocols to confirm the grade, continuity, and thickness of the sylvinite mineralization.

“Receiving final approvals marks a major milestone in the advancement of the Sage Plain Potash Project,” stated J. Patricio Varas, Chief Executive Officer of Sage Potash Corp. “Our technical team has designed a focused multi-purpose drill program aimed at generating the critical geological and hydrogeological data required to potentially upgrade the resource and advance the Project toward feasibility studies and detailed engineering. We are confident this program will further demonstrate the quality and scale of the Project while being executed safely and efficiently.“

The Company expects to release an updated resource estimate in Q3 2026, incorporating results from the current drilling campaign and historical drilling data. The updated estimate is expected to support the next stage of project advancement, including feasibility studies, detailed engineering, and broader development planning.

The Company and its contractors intend to mobilize for this drill program in short order.

About Sage Potash Corp.

Sage Potash Corp. (TSXV: SAGE) (OTCQB: SGPTF) is dedicated to the development of its flagship Sage Plain Potash Project, located in the Paradox Basin, Utah. With a large and high-grade resource base, the Company is advancing toward its goal of establishing a secure and sustainable domestic potash production platform in the United States. Sage Potash is committed to food security, environmental stewardship, and creating value for shareholders and stakeholders alike.

On Behalf of the Board of Directors, J. Patricio Varas, CEO and Director 1 (236) 521-1521 Website: www.sagepotash.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities legislation. The forward-looking statements herein are made as of the date of this news release only, and the Company does not assume any obligation to update or revise them to reflect new information, estimates or opinions, future events or results or otherwise, except as required by applicable law. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects”, “is expected”, “budgets”, “scheduled”, “estimates”, “forecasts”, “predicts”, “projects”, “intends”, “targets”, “aims”, “anticipates” or “believes” or variations (including negative variations) of such words and phrases or may be identified by statements to the effect that certain actions “may”, “could”, “should”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking information in this news release includes, but is not limited to, statements with respect to future events or future performance of Sage Potash, including the satisfactory design and supervision of the Company’s upcoming drill program, the achievement of positive results of the drill program, the achievement of targeting Cycle 18 horizons and continuous core recovery, the achievement of satisfactory potash evaluation and hydrogeological testing in the drill program, the timing of the mobilization and the commencement of the drill program and potentially upgrading the resource and advancing the Project toward feasibility studies, detailed engineering and broader development planning. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including, but not limited to, the risk factors set out under the heading “Risk Factors and Uncertainties” in the Company’s Management’s Discussion & Analysis available for review under the Company’s profile at www.sedarplus.ca. Such forward-looking information represents management’s best judgement based on information currently available. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

DALLAS, TX / ACCESS Newswire / June 18, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai²” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI to enhance portfolio performance, today announced that John P. Rochon, Chairman of Ai² and entities controlled by the family of Mr. Rochon, collectively, have acquired approximately $100 million of Ai² shares at $20.00 per share through a privately negotiated transaction with an existing large shareholder.

This transaction represents a significant incremental investment by the Rochon family, further increasing their already substantial ownership position in Ai². The purchase underscores a deep and continuing conviction in the Company’s long-term strategy, its differentiated position in Transformational AI, and the proven ability of its Board and management team to execute at scale. The Rochon family has been a longstanding supporter of Ai², and this latest investment further aligns their interests with the Company’s long-term value creation objectives. This transaction reinforces a stable and strategically aligned shareholder base.

“This is not simply a financial investment; it is a statement of belief in where Ai² is going and how we intend to get there,” added John P. Rochon, Sr. “We are building something enduring, with a focus on disciplined execution, durable growth and long-term value creation.”

Ai² continues to execute against a robust pipeline of AI-driven initiatives across multiple sectors, focusing on enterprise-grade psychometric intelligence, scalable deployment architectures, and high-value commercial applications. The Rochon family believes it is well-positioned to capitalize on accelerating demand for applied AI solutions that deliver measurable business outcomes.

The Company was not involved in negotiating this transaction and will not receive any proceeds. Additionally, the Company expects to file its Quarterly Report on Form 10-Q for the quarter ended March 31, 2026 with the Securities and Exchange Commission next week. The Company notes that the period covered by the 10-Q predates both its direct listing and the acquisition of its Portfolio Companies and therefore will not reflect the consolidated financial results of those subsidiaries. The financial results to be presented in the forthcoming Form 10-Q will reflect only the historical operations of the Company’s predecessor entity and will include transaction-related expenses incurred in connection with the business combination, as well as the effects of operational disruptions arising from, among other factors, closing the transaction, adverse weather conditions and military hostilities in the Middle East, each of which impacted performance during the first quarter. As a result, the Company believes the financial results that will be reported in the forthcoming Form 10-Q will not be representative of the Company’s normalized operating performance.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai²) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai² is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries. More information can be found at www.aiaiholdings.com.

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

The forward-looking statements in this press release are based on information available to us as of the date hereof, and we disclaim any intention to, and, except as may be required by law, undertake no obligation to, update or revise forward-looking statements to reflect events or circumstances that subsequently occur or of which the Company hereafter become aware. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

Vancouver, British Columbia–(Newsfile Corp. – June 17, 2026) – Riverside Resources Inc. (TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY0) (“Riverside” or the “Company”) is pleased to announce the appointment of Marco Strub as an Independent Director of the Company, effective immediately.

Marco is a long-time shareholder of Riverside and has worked with major European investment firms with vast connections in mining networks. He is principal of Sircon AG, a consulting and investment research company based in Zurich, Switzerland, and was formerly a partner of Exulta AG, a portfolio management company from 1997 to 2003. He is an Independent Director of Triumph Gold Corp., and Canada Zinc Metals Corp. (Formerly: Mantle Resources Inc.). He has also been a Director of Open Gold Corp (aka, Range Capital Corp) since 2009 and Mexigold Corp. (formerly, BCY Resources Inc.) since 2011. He served as a Director at Margaret Lake Diamonds, Inc. (JDV Capital Corp.) from 2011 to 2014, and as a Director of MVE Capital Corp. since 2007. He received a Master of Arts degree from the University of St. Gallen, Switzerland in 1982.

“We are pleased to welcome Marco to the Board,” commented John-Mark Staude, CEO of Riverside Resources. “His deep background in investment research, portfolio management, and capital markets, combined with his extensive experience serving on the boards of public mining companies, brings valuable perspective as Riverside continues to advance its project portfolio and partnership model. We look forward to his contributions and counsel.”

“Riverside has built a disciplined approach to project generation and value creation in the resource sector,” said Mr. Strub. “I am pleased to join the Board and to support the Company and its shareholders as it advances its exploration and partnership initiatives.”

Riverside would like to thank James Ladner for his service as a director. After choosing not to stand for re-election, James leaves behind a legacy of meaningful contribution where his deep expertise in accounting, mining finance, and the broader mineral business has been invaluable to the Company. While Mr. Ladner will no longer serve as a formal director, he will continue to share his insights and provide input to Riverside going forward.

Results of Annual General Meeting of Shareholders

The Company is pleased to provide the results of its Annual General Meeting of Shareholders which was held on June 4, 2026.

At the Annual General Meeting of shareholders, 6,365,550 shares were voted, representing 6.81% of the total 93,443,464 issued and outstanding shares, and the Company received majority shareholder approval for the following:

1. To set the number of directors at five (5):

2. Elected one new and re-elected four incumbent directors, total of five directors for the ensuing year as follows:

Director

Votes For

%

John-Mark Staude

6,358,050

99.88%

James Clare

6,358,050

99.88%

Walter Henry

6,358,050

99.88%

Bryan Wilson

6,358,050

99.88%

Marco Strub

6,358,050

99.88%

3. Appointment of Auditor: To appoint Davidson & Company LLP, Chartered Professional Accountants, as auditors of the Company for the ensuing year and to authorize the directors to fix their remuneration.

4. To consider, and if deemed advisable, pass an ordinary resolution, substantially in the form set out in the accompanying management information circular (the “Information Circular”), re-approving the continued use of Riverside’s stock option plan.

Details of the matters approved at the meeting are set out in the Company’s Information Circular dated April 20, 2026 and available under the Company’s profile on SEDAR+ at www.sedarplus.ca.

About Riverside Resources Inc.

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has a solid balance sheet with no debt and 93M shares outstanding with a strong portfolio of gold-silver and copper assets and royalties in North America. Riverside has extensive experience and knowledge operating in Mexico and Canada and leverages its large database to generate a portfolio of prospective mineral properties. Riverside has properties available for option, with information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information, contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Corporate Communications Riverside Resources Inc. Eric@rivres.com Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the risk that the Transaction will not be completed as contemplates, or at all, availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Denver, Colorado–(Newsfile Corp. – June 11, 2026) – Elemental Royalty Corporation (TSX: ELE) (NASDAQ: ELE) (“Elemental” or the “Company“) is pleased to announce that it has filed Notice of Intention to Make a Normal Course Issuer Bid (“NCIB“) with the Toronto Stock Exchange (the “TSX“) and intends to transact the NCIB through the facilities of the TSX, the Nasdaq Capital Market (“Nasdaq“), other designated exchanges and/or alternative trading systems in Canada and the United States or by such other means as may be permitted under applicable securities laws during the term of the NCIB.

Pursuant to the NCIB, Elemental may, during a 12-month period commencing June 15, 2026, and ending June 14, 2027, purchase up to 3,222,537 common shares in the capital of the Company (the “Shares“), being up to 5% of Elemental’s issued and outstanding Shares as at June 4, 2026.

The Board of Directors of Elemental believes that, from time to time, the market price of the Shares may not fully reflect the underlying value of Elemental’s royalty portfolio, cash flow profile and growth prospects. Accordingly, Elemental believes that the NCIB provides an additional capital allocation tool and that purchasing its Shares may represent an appropriate and desirable use of corporate funds and an opportunity to enhance shareholder value.

The average daily trading volume (“ADTV“) of the Company’s Shares on the TSX for the period from April 7, 2026, to June 4, 2026, as calculated in accordance with TSX rules, was 43,645 Shares. Accordingly, purchases made through the facilities of the TSX will be subject to a daily purchase limit of 10,911 Shares, representing 25% of the ADTV, subject to certain permitted exceptions under TSX rules for larger block purchases. In addition to purchases made through the facilities of the TSX, the Company intends to purchase Shares through the facilities of the Nasdaq and other designated exchanges and/or alternative trading systems in Canada and the United States as part of its NCIB, subject to applicable securities laws and exchange requirements. Given that the substantial majority of the Company’s trading volume is conducted on Nasdaq, the Company expects that the majority of repurchases under the NCIB will be made through the facilities of Nasdaq.

The price that Elemental will pay for any such Shares will be the prevailing market price at the time of acquisition. The number of Shares which may be purchased pursuant to the NCIB, and the timing of any such purchases, will be determined by the Company’s management. Purchases under the NCIB will be made from time to time by Raymond James Ltd. (the “Broker“) on behalf of Elemental. All Shares purchased pursuant to the NCIB will be returned to treasury for cancellation. Elemental has not purchased any of its Shares in the previous 12-month period.

In connection with the NCIB, Elemental intends to enter into an automatic share purchase plan (the “Plan“) with the Broker to allow for purchases of the Shares during “blackout” or “closed” periods under Elemental’s stock trading policy. Such purchases would be at the discretion of the Broker on parameters established by Elemental prior to any blackout or closed period. The Plan may be terminated by Elemental or the Broker in accordance with its terms and will otherwise terminate on the expiry of the NCIB.

A copy of the notice filed with the TSX may be obtained by any shareholder of the Company without charge by contacting the Company.

TSX: ELE | NASDAQ: ELE | ISIN: CA28620K1066 | CUSIP: 28620K106

About Elemental Royalty Corporation. Elemental is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 18 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental trades on Nasdaq and on the Toronto Stock Exchange under the ticker symbol “ELE”.

Cautionary note regarding forward-looking statements This news release contains certain “forward looking statements” and certain “forward-looking information” as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar terminology (including negative and grammatical variations thereof).

Forward-looking statements and information include, but are not limited to, statements with respect to the purchase of Shares under the NCIB and the enhancement of shareholder value as a result thereof, the implementation of the Plan, the future growth, development and focus of the Company, and the acquisition of new royalties and streams. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental to control or predict, that may cause Elemental actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions; the absence of control over the mining operations from which Elemental will receive royalties; risks related to international operations, government relations and environmental regulation; the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits; the impact of any pandemic or epidemic; economic uncertainties created by the war in Ukraine and hostilities in the middle-east including the military conflict in Iran; the possibility that future exploration, development or mining results will not be consistent with Elemental expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses; commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; cybersecurity threats, security breaches and hacks; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental for the year ended December 31, 2025. Elemental undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represents management’s best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Neither the Nasdaq, nor the TSX or its Regulation Service Provider (as that term is defined in the policies of the TSX) accepts responsibility for the adequacy or accuracy of this press release.

🔥 Mark your calendars! Going live TOMORROW at 9:00 AM Eastern, Todd Furniss, CEO of AIAI Holdings ($AIAI / “AI Squared”), sits down with Maurice Jackson on Proven and Probable for a masterclass on scaling enterprise intelligence! 🌐🚀

Forget the hype cycle. Discover how AI Squared is building a powerful, diversified moat by acquiring traditional brick-and-mortar operating companies and embedding proprietary, transformational AI directly into their core infrastructure to unlock massive hidden value. 📈💼

Key Discussion Highlights: 🔹 Moving Beyond the Hype: Why the real AI winners won’t just sell software, but fundamentally transform how businesses operate. 🔹 The Scalability Architecture: Tuning verticalized data models to dominate complex sectors like healthcare, defense, and logistics. 🔹 Driving Shareholder Return: A look at the company’s laser focus on capital allocation, revenue growth, and long-term dividend strategies following their Nasdaq listing.