This video features a deep-dive interview with Derek MacPherson, President and CEO of West Point Gold ($WPG), regarding the significant new gold discovery at the Black Dyke target within the Gold Chain Project in Arizona. Below is a detailed breakdown of the discussion with associated timestamps:

“Check out the timestamp links below to jump directly to the detailed technical analysis of the new Black Dyke discovery zone!”

0:00 – Introduction & Company Overview 1:30 – The Oatman District & Walker Lane Trend 3:15 – Black Dyke Target: 36.6m of Surface Gold Breakdown 5:45 – Validating a Potential Deeper System: Deeper Drill Hits 8:00 – 15,000m Program: Where are the Next 24 Drill Hole Assays Pending? 10:30 – Key Milestones defining a ‘Successful’ 2026 12:45 – Capital Structure & Financial Discipline 15:00 – CEO’s Closing Message & How to Invest

February 17, 2026 – Denver, Colorado: Elemental Royalty Corporation (“Elemental” or “the Company”) (TSX-V: ELE, NASDAQ: ELE) is pleased to announce that its Board of Directors has approved an inaugural dividend policy (the “Dividend Policy”). In accordance with the Policy, Elemental expects to declare an annual cash dividend to its shareholders of US$0.12 per Elemental common share, to be paid in quarterly instalments of US$0.03 per share, with the record date for the inaugural dividend to be paid at the end of the first calendar quarter of 2026, and at the end of each calendar quarter following for subsequent dividends.

The Company is also pleased to announce that it anticipates that qualifying registered shareholders will be able to elect to receive their dividend in the form of Tether Gold XAU₮ tokens, of par value to the dividend price, thereby providing Elemental shareholders with direct ownership of physical gold through their investment in gold royalties.

Highlights

Maiden Dividend Policy approved by the Board of Directors

Expected annual cash dividend of US$0.12 per Elemental share, paid quarterly

Anticipated that qualifying registered shareholders will be able to elect that their cash dividends be invested in Tether Gold’s XAU₮ token

The Dividend to shareholders is supported by Elemental’s strong projected revenue and cash flow growth profile in 2026 and beyond

Further information on how shareholders may elect to receive the dividend or dividend in kind, will be provided in due course

David M. Cole, Chief Executive Officer of Elemental Royalty, commented: “The approval of this dividend policy marks an important milestone in Elemental’s strategic trajectory and reflects our confidence in the strength and momentum of the business; we believe this is the right time to introduce a sustainable, long-term, dividend. The decision to offer investors a dividend in kind, in the form of Tether Gold, further differentiates Elemental as a forward-thinking, growth-oriented investment.”

Stefan Wenger, Chief Financial Officer of Elemental Royalty Corporation, commented: “Our inaugural dividend is underpinned by Elemental’s strong balance sheet and future revenue outlook in the near and longer-term: as of December 31, 2025, we had approximately US$53 million of cash and no debt, providing substantial financial flexibility as we continue to invest in growth. We will continue to maintain a disciplined approach to capital allocation, balancing returning capital to shareholders through a progressive dividend which we intend to maintain, or even increase, without compromising on our strategy of accretive growth through the acquisition and generation of precious metals streams and royalties.”

Juan Sartori, Executive Chairman of Elemental Royalty Corporation, commented: “We believe the initiation of this dividend policy is a world first for a royalty company: we anticipate enabling qualifying shareholders to elect to have their cash dividend invested in the purchase of the Tether XAU₮ token, thereby facilitating for shareholders greater exposure to physical gold through Tether Gold’s stablecoin and retaining real long-term value storage via a practical mechanism for gold-denominated investment returns.”

Apollo Silver: Capitalized, Strategically Backed, and Positioned for the Next Silver Cycle

In a recent episode of Proven and Probable, host Maurice Jackson spoke with Ross McElroy President and CEO of Apollo Silver, to discuss the company’s latest financing, strategic shareholder support, and its growth strategy amid a strengthening silver market.

Apollo Silver recently completed a $27.5 million financing, increasing its treasury to nearly $60 million. The raise was led primarily by strategic investors and insiders, most notably Eric Sprott and Jupiter Asset Management, Apollo Silver’s two largest shareholders. Their continued participation and increased ownership underscore strong institutional confidence in the company’s assets, leadership, and execution capability.

The majority of the capital will be deployed at Apollo Silver’s Calico Project in San Bernardino County, California, one of the largest primary silver deposits in the United States. Calico hosts an updated mineral resource totaling approximately 125 million ounces of silver in the Measured and Indicated category, with an additional 58 million ounces inferred. Planned work includes advanced metallurgical testing, geotechnical studies, recovery optimization, mine planning, and exploration across an expanded land package.

Mr. McElroy addressed investor concerns regarding California as a mining jurisdiction, emphasizing that San Bernardino County is mining-friendly, with a long history of active mining operations and strong local support for responsible resource development.

In addition to Calico, Apollo Silver controls the Cinco de Mayo Project in Chihuahua, Mexico, a high-grade carbonate replacement deposit originally discovered by MAG Silver. The project hosts a substantial historic resource and significant expansion potential. Should Apollo Silver secure a long-term access agreement with the local community, Cinco de Mayo has the potential to become a company-making flagship asset, given its scale, grade, and jurisdiction.

The conversation also explored silver’s evolving role as both a precious and industrial metal, particularly following its designation as a U.S. critical mineral. With rising demand from solar energy, electronics, defense applications, and persistent global supply deficits, Apollo Silver is positioning itself to benefit from favorable long-term market fundamentals.

With a strong balance sheet, top-tier shareholders, two world-class silver assets in stable jurisdictions, and an experienced management team, Apollo Silver enters the coming year with multiple catalysts and a clear path forward.

New full-scale sample prep facility to be co-branded “Scout Analytical, Powered by Paragon” with funding and operations handled by Paragon.

Local prep, faster assays at scale: this facility bolsters Scout’s current sample preparation capabilities in Coeur d’Alene, further removing shipping and long queue bottlenecks.

Preferred rates + priority lanes: The facility is open to all third parties, Paragon will provide preferred rates and Tier‑1 priority processing for Scout and its partners.

Scout Analytical paired with Paragon’s PhotonAssay™ capabilities will enable assay turnaround in days instead of weeks, a paradigm shift in exploration speed.

Coeur d’Alene, Idaho – January 20, 2026 – Scout Discoveries Corp. (“Scout” or “the Company”) has executed a strategic partnership with Paragon Advanced Labs Inc. (through Paragon Geochemical Laboratories Inc.) to establish a sample preparation facility at Scout’s northern operations hub in Coeur d’Alene, Idaho, co-branded “Scout Analytical, Powered by Paragon.” The facility integrates local sample preparation with Paragon’s ISO-certified analytical capabilities including a Chrysos PhotonAssay™ network to compress assay turnaround time and materially improve efficiency across Scout’s exploration programs.

A New Standard for Exploration SpeedThe partnership integrates Scout’s exploration team, robust drilling fleet, and Idaho-based infrastructure with Paragon’s industry-leading geochemical expertise, fire assay and network of Chrysos PhotonAssay™ technology. By establishing localized sample preparation at Scout’s northern operations hub, this partnership removes the logistical bottlenecks that have traditionally hindered exploration progress in the emerging Idaho Copper Belt and adjacent Silver Valley, enabling faster and more efficient project advancement. With Paragon’s ISO-certified analytics now built into Scout, the entire exploration process – including targeting, drilling, logging, core imaging, processing, and assaying – is available to Scout and its partners in a single package.

Key Highlights of the PartnershipFully Vertically Integrated: Adding another crucial element to Scout’s vertically integrated model, enabling Scout and its partners to benefit from a seamless workflow, from drilling through to high-precision, independently validated assay results.Priority Processing: Samples from Scout’s exploration projects, along with its partner’s projects, will receive Tier-1 priority at the Coeur d’Alene facility, along with access to Scout’s core processing ensuring rapid data-driven drilling adjustments.Technology-First Approach: The facility will feature advanced Orbis crushing and pulverizing systems, with specialized workflows optimized for PhotonAssay™ — the fastest, most sustainable gold analysis method in the industry.Assay Credits: Scout will receive assay credits equal to the sale amount of its currently operated Orbis OM50WM crusher and pulverizer being transferred to Paragon for use in the new prep facility.Expansion into Nevada: The agreement includes provisions for Scout to assist Paragon in establishing a reciprocal core-processing facility in Sparks, NV, further expanding the partnership’s geographic footprint and expanding the Paragon facility in Sparks to include core-cutting services.

“This partnership is exactly the kind of strategic move that defines Scout’s approach to vertical integration of the discovery process,” said Dr. Curtis Johnson, President & CEO of Scout. “By bringing Paragon’s world-class lab capabilities and standards directly into our operations, we are not just improving efficiency, we are fundamentally changing the pace of exploration for our own projects and for our partners, by cutting weeks off the assay turnaround time. In a competitive market, speed is our greatest asset.”

Peter Shippen, CEO of Paragon added: “Paragon is committed to being where the discovery action is. Coeur d’Alene is a premier mining jurisdiction, and partnering with Scout—a leader in US exploration—allows us to deploy our ‘Powered by Paragon’ model in a way that benefits the entire regional mining community.”

The Coeur d’Alene facility is expected to be fully operational by Q1 2026 for Scout and its partners, Paragon, customers, and all third parties – coinciding with the launch of the spring drilling season.

About ParagonParagon Advanced Labs Inc. provides innovative analytical technologies to the global mining industry. By embracing new technology, the Company is addressing critical capacity bottlenecks in mineral assaying through the deployment of PhotonAssay™ technology and complementary analytical solutions. The Company delivers faster, more accurate, and cost-effective mineral analysis for mining operators worldwide.

About Scout Discoveries Corp.Scout Discoveries Corp., headquartered in Coeur d’Alene, Idaho, is a private U.S. mineral exploration company with rights to twelve separate precious and base metal projects in the western U.S.A., comprising one of the largest unpatented claim holdings in the region, totaling over 50,000 acres. Scout’s vision is to bring the full discovery process in-house from idea generation through resource drilling, lowering costs and increasing efficiency. With this model, the Company can rapidly advance its project portfolio through discovery by leveraging its five internal core drill rigs and experienced technical teams.For further information, visit: https://www.scoutdiscoveries.com/

Vancouver, British Columbia–(Newsfile Corp. – January 6, 2026) – West Point Gold Corp. (TSXV: WPG) (OTCQB: WPGCF) (FSE: LRA0) (“West Point Gold” or the “Company”) is pleased to announce the results for four holes from the high-grade zone at Northeast (NE) Tyro, part of the ongoing 15,000 metre (m) drill program at its flagship Gold Chain Project in Arizona. The Company is reporting assay results for four drill holes (936 m), GC25-85 through GC25-88.

Highlights:

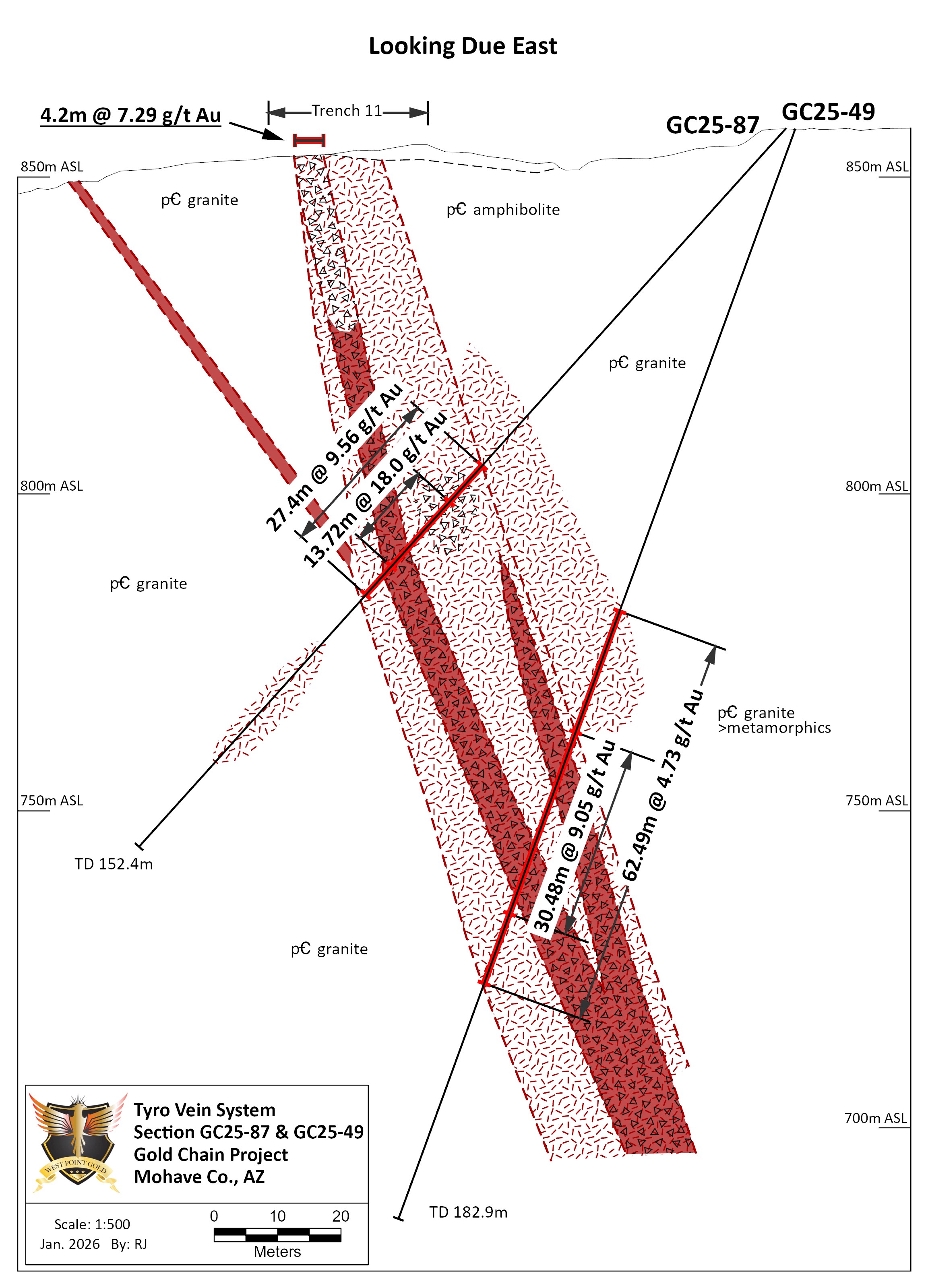

Hole GC25-87 returned 27.4m of 9.56 g/t Au at 71.6m to 99.1m, including 13.7m of 18.00 g/t Au at 79.3m to 93.0m, about 50m up-dip from GC25-49 (62.5m at 4.73 g/t Au) – expanding the highest-grade part of the zone up-dip.

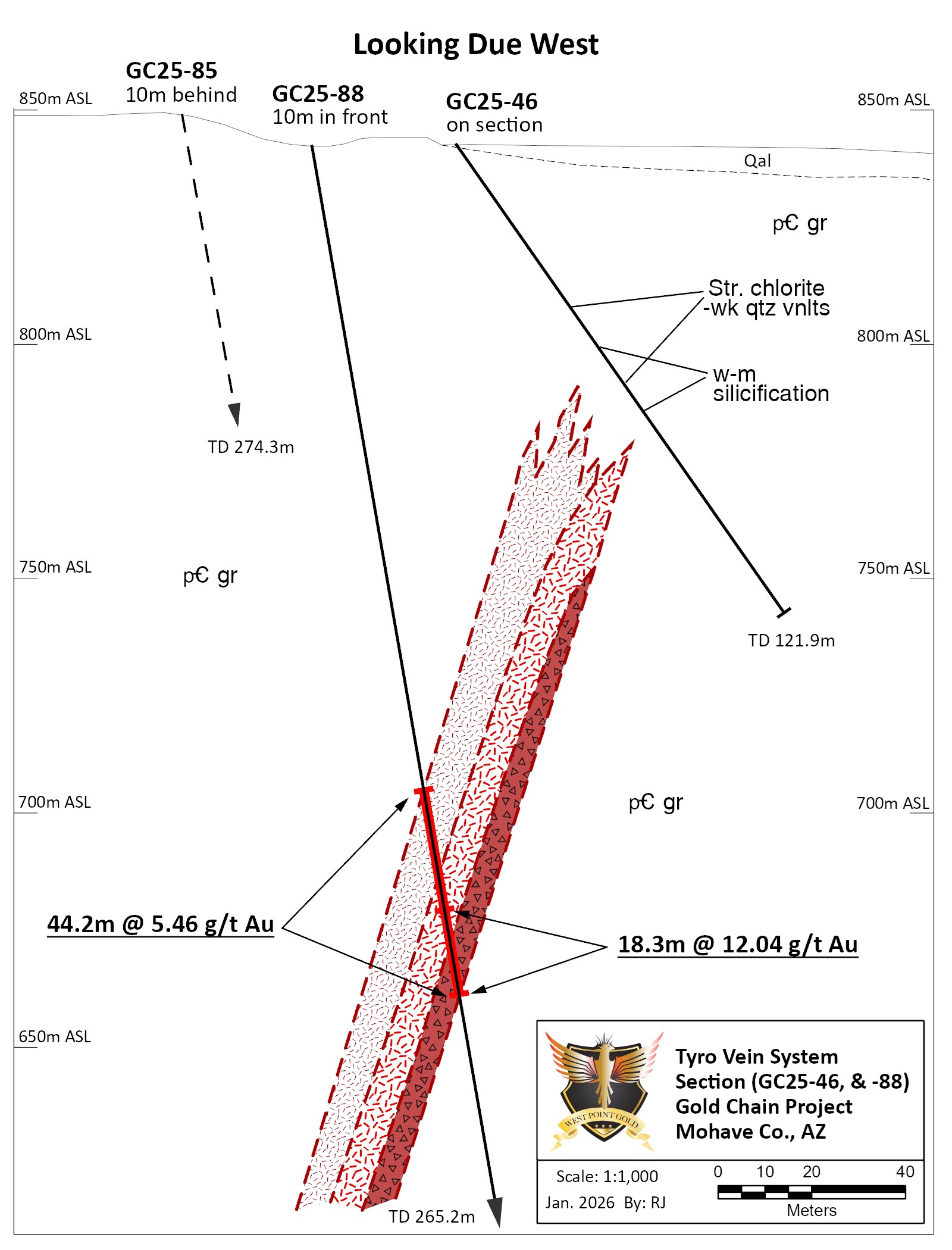

Hole GC25-88 returned 44.2m of 5.46 g/t Au at 140.2m to 184.4m, including 18.3m of 12.04 g/t Au at 166.1m to 184.4m – expanding the high-grade zone along strike, as this is the furthest northeast hole at Tyro.

Hole GC25-85 returned 29.0m of 5.24 g/t Au at 164.6m to 193.6m, including 12.2m of 10.48 g/t Au at 176.8m to 189.0m, about 80m down-dip from hole GC25-58 which returned 32.0m of 2.01 g/t Au.

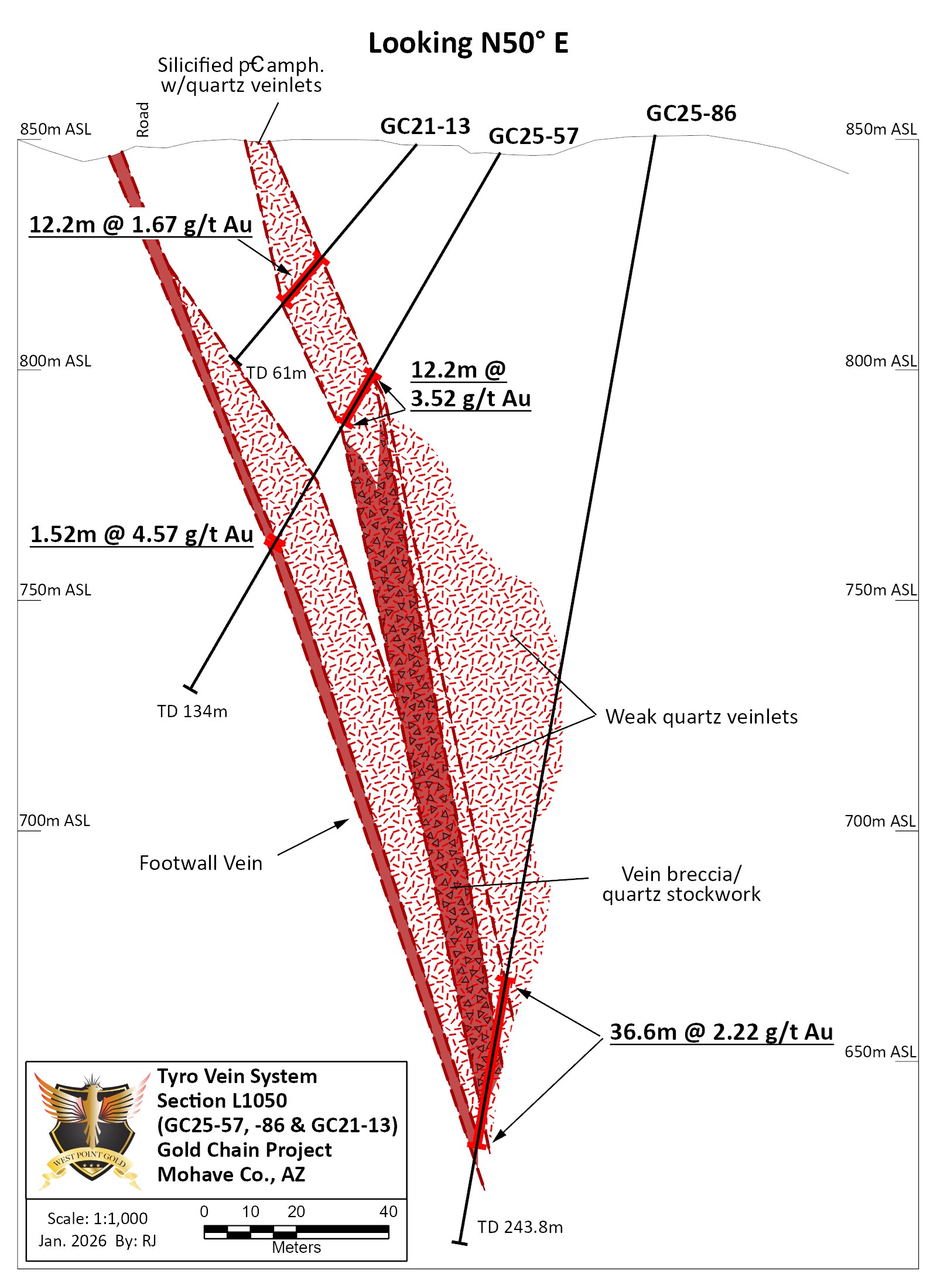

Hole GC25-86 returned 36.6m of 2.22 g/t Au at 179.8 to 216.4m about 140m down-dip from GC25-57 which returned 12.2m at 3.52 g/t Au.

Drilling continues to explore the deeper portions of the high-grade zone between the Tyro NE and Main zones, with two holes (540 m) completed with assays pending. A total of 3,769 m of the planned 15,000m program was completed in 2025.

“Drilling at NE Tyro continues to return better than expected grades with good continuity at relatively shallow depths. The high-grade zone at NE Tyro appears to continue at depth and to the northeast, suggesting the zone remains open to further expansion as we continue drilling. We expect these results to positively impact the grade profile and the overall scale of our upcoming maiden resource. Drilling continues at Gold Chain, with one rig at NE Tyro, and one at Tyro South,” stated Derek Macpherson, President and CEO.

Table 1: Drill Results

Holes

From (m)

To (m)

Width (m)

Grade (g/t Au)

GC25-85

164.6

193.6

29.0

5.24

including

176.8

189.0

12.2

10.48

GC25-86

179.8

216.4

36.6

2.22

GC25-87

71.6

99.1

27.4

9.56

including

79.3

93.0

13.7

18.00

GC25-88

140.2

184.4

44.2

5.46

including

166.1

184.4

18.3

12.04

Note: All widths shown are downhole; true widths are approximately 50-90% of downhole widths; see Figure 3 for estimated true widths.

Figure 1: Plan view of the Main Tyro vein showing geology and drilling conducted in 2021, 2023, 2024 and 2025. Note the location of Hole Nos. GC25-85 through GC25-88.

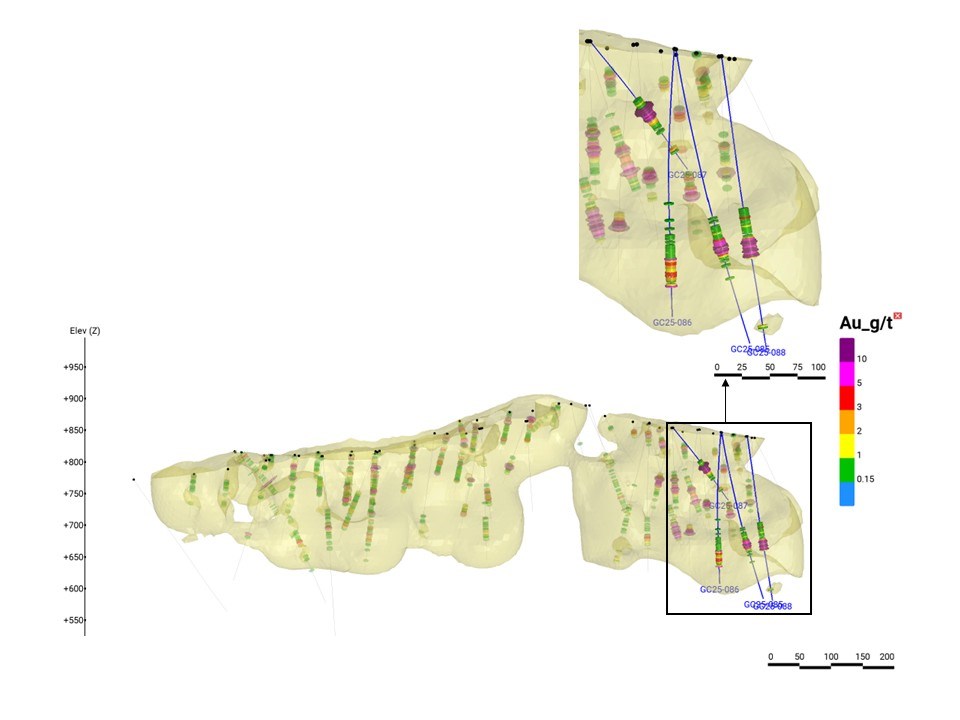

Figure 2. Longitudinal perspective of the Tyro Main and NE Zones, Showing Core and RC Drilling to Date. Holes GC25-85 through GC25-88 are highlighted and described below.

Summary The drilling of holes GC25-85 through GC25-88 continues to expand and provide improved definition for high-grade gold mineralization in the NE Tyro zone at the Company’s Gold Chain project in Arizona. The four holes comprising this release, GC25-85 through GC25-88, represent 936 m of the 3,769 m drilled to date in the current 15,000m program.

Each hole is briefly described below and graphically presented in both sectional and longitudinal views. Additionally, Figure 3 is a generalized longitudinal view of the NE Tyro zone showing the intercept’s mid-point, composite gold grade and estimated true width based upon geologic sections. The core of this zone remains mostly open to the northeast and to depth. West Point Gold anticipates the receipt of its Plan of Operations in early 2026, which will permit the drilling of both core and RC holes outside of the controlled patented claims, allowing for deeper tests and further exploration to the northeast and toward the Frisco Graben target area.

Along with the increased gold grades at depth, close inspection of the drill cuttings reveals an increase in varicolored chalcedony, crustiform banding, adularia and illite(?)-pyrite alteration in the wallrock.

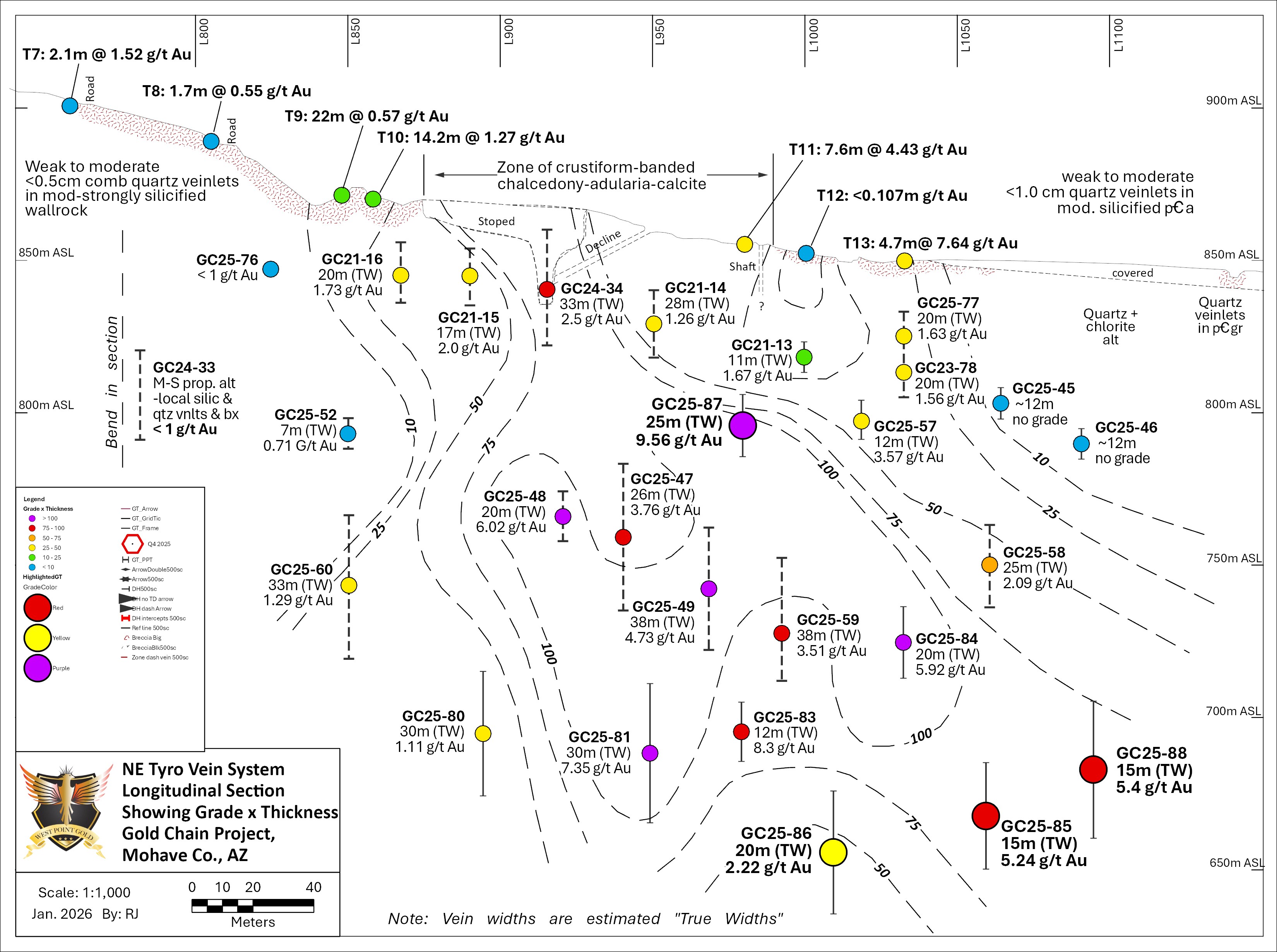

Figure 3. Longitudinal Section Along the NE Tyro Zone Showing Drill Hole Pierce Points, Estimated True Width and Intercept Grade. Grades are Colour Coded to Better Illuminate the Shape and Orientation of the High-Grade Zone.

Hole GC25-85 Hole GC25-85 traversed the Tyro NE vein/zone about 30m southwest of GC25-88 (44.2m at 5.46 g/t Au) and encountered from 164.6m to 193.6m (29.0m) 5.24 g/t Au enveloping a higher-grade zone of 12.2m at 10.48 g/t Au (Figure 2). The intercept’s midpoint is about 200m below the surface and without a surface expression, i.e. blind. The position of GC25-85 is provided in Figures 1 through 3.

Hole GC25-86 Hole GC25-86 was drilled about 140m beneath hole GC25-57 and about 200m beneath a weak surface exposure of the vein. The hole traversed a broad zone of quartz veinlets which appeared to coalesce with depth. A mineralized zone was encountered at 179.8m to 216.4m (36.6m) at 2.22 g/t Au. A geologic summary of this hole is provided in Figures 3 and 4. The quartz-chalcedony-adularia-calcite vein resembles the surrounding intercepts, and the vein package remains broad. The results indicate that the mineralized zone has coalesced into a more discrete mineralized package or vein in the relatively short distance below Hole GC25-57.

Figure 4: Cross-Sectional View of Hole GC25-86 down-dip from Holes GC25-57 and GC21-13.

Hole GC25-87 Hole GC25-87 was designed to test the NE Tyro zone between the surface and Hole GC25-49 (62.5m at 4.73 g/t Au). The hole traversed the NE Tyro structure about 65 metres below the surface and 50 m above GC25-49 (Figure 5) from 71.6m to 99.1m (27.4 m) containing 9.56 g/t Au. An internal zone of higher gold grades corresponds to quartz-chalcedony-adularia-calcite vein and breccia, along with likely stockwork veining; the zone consisted of 13.7m of 18 g/t Au. Both intercepts shown in Figure 5 suggest good continuity in this area of the vein. Sections across the vein system in this area suggest a true width of 20 to 25 metres.

Figure 5: Cross-Sectional View of Hole GC25-87 up-dip from Hole GC25-49.

Hole GC25-88 Hole GC25-88, located in Figure 1, was designed to incrementally expand the limits of gold mineralization to the northeast and beneath earlier holes (GC25-45 and GC25-46) which encountered altered and weakly veined host rocks with negligible gold. A strong vein, shown in Figure 6, was encountered about 110 metres beneath GC25-46 from 140.2m to 184.4m and contained 5.46 g/t Au over 44.2m. An internal higher-grade interval, composed of mostly quartz-chalcedony-adularia-calcite, was identified at 166.1m to 184.4m containing 12.04 g/t Au over 18.3 metres. The overall intercept is dominated by quartz veinlets which coalesce into a vein breccia approaching the footwall contact. The estimated true width of this zone is about 15 metres and remains open to the northeast and at depth.

Figure 6: Cross Sectional View of Hole GC25-88 down-dip from Hole GC25-46.

Qualified Person Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration, is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for overseeing all phases of the drilling program, including logging, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Drillholes have a diameter of about 10cm, and samples have an approximate weight of 5 to 10kg. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, and over-limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), and over-limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. The results summarized above have been carefully reviewed with reference to the QA/QC results. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

About West Point Gold Corp. West Point Gold is an exploration and development company focused on unlocking value across four strategically located projects along the prolific Walker Lane Trend in Nevada and Arizona, USA, providing shareholders with exposure to multiple discovery opportunities across one of North America’s most productive gold regions. The Company’s near-term priority is advancing its flagship Gold Chain Project in Arizona.

For further information regarding this press release, please contact: Aaron Paterson, Corporate Communications Manager Phone: +1 (778) 358-6173 Email: info@westpointgold.com

FORWARD-LOOKING STATEMENTS: Certain statements contained in this press release constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, timing of the Company’s maiden resource estimate, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures. The Company cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete any payments or expenditures required under the Company’s various option agreements for its projects; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainties related to resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data; the potential for delays in exploration or development activities; uncertainty related to the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results may vary from those expected; statements about expected results of operations, royalties, cash flows, financial position may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions. The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; fluctuating gold prices; possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR+ made by the Company with securities regulators. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate press release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

VANCOUVER, British Columbia, Dec. 29, 2025 (GLOBE NEWSWIRE) — Apollo Silver Corp. (“Apollo Silver” or the “Company”) (TSX.V:APGO, OTCQB:APGOF, Frankfurt:6ZF) is pleased to announce that it has upsized its previously announced non-brokered private placement by an additional $2,500,000, to be subscribed for primarily by insiders of the Company, for total aggregate gross proceeds of up to $27,500,000, through the issuance of up to 5,500,000 units (the “Units”) at a price of $5.00 per Unit (the “Upsized Offering”).

As previously announced, Mr. Eric Sprott and a fund managed by Jupiter Asset Management (the “Jupiter Fund”), Apollo Silver’s two largest shareholders, are participating in the Upsized Offering, and will each subscribe for 2,500,000 Units of the Company, for combined gross proceeds of $25,000,000. Following completion of the Upsized Offering, the Jupiter Fund will own approximately 12% of Apollo Silver’s issued and outstanding common shares, while Eric Sprott will own approximately 9.5%, on an undiluted basis. On a partially diluted basis, each investor’s ownership interest will increase accordingly.

Each Unit issued pursuant to the Upsized Offering will consist of one common share (a “Share”) in the capital of the Company and one common Share purchase warrant (a “Warrant”). Each Warrant entitles the holder thereof to purchase one Share at an exercise price of $7.00 for 24 months from the closing date of the Upsized Offering.

All securities issued in connection with the Upsized Offering will be subject to a four-month hold period from the date of closing. Finder’s fees may be payable on some or all of the funds raised, in accordance with the policies of the TSX Venture Exchange (the “TSXV”). The Company intends to use the net proceeds from the Upsized Offering to fund exploration and development activities across the Company’s projects, as well as for general working capital and corporate purposes.

Closing of the Upsized Offering is subject to regulatory approval, including that of the TSXV.

The Upsized Offering is expected to include participation by certain insiders of the Company for an aggregate amount of up to $2,500,000. Such participation constitutes a “related party transaction” under Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101”). The issuance of securities to insiders will be exempt from the valuation requirement pursuant to section 5.5(b) of MI 61-101, as the Company’s shares are not listed on a specified market, and from the minority shareholder approval requirement pursuant to section 5.7(a) of MI 61-101, as the fair market value of the securities issued to related parties will not exceed twenty-five percent of the Company’s market capitalization.

The Shares have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any U.S. state securities laws, and may not be offered or sold in the United States without registration under the U.S. Securities Act and all applicable state securities laws or compliance with the requirements of an applicable exemption therefrom. This news release shall not constitute an offer to sell or the solicitation of an offer to buy securities in the United States, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

About Apollo Silver Corp.

Apollo Silver is advancing one of the largest undeveloped primary silver projects in the US. The Calico project hosts a large, bulk minable silver deposit with significant barite credits – a critical mineral essential to the US energy and medical sectors. The Company also holds an option on the Cinco de Mayo Project in Chihuahua, Mexico, which is host to a major carbonate replacement (CRD) deposit that is both high-grade and large tonnage. Led by an experienced and award-winning management team, Apollo Silver is well positioned to advance the assets and deliver value through exploration and development.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release includes “forward-looking statements” and “forward-looking information” within the meaning of Canadian securities legislation. All statements included in this news release, other than statements of historical fact, are forward-looking statements including, without limitation, statements with respect tothe expected timing for completion of the Upsized Offering, and the intended use of proceeds from the Upsized Offering. Forward-looking statements include predictions, projections and forecasts and are often, but notalways,identifiedbytheuseofwordssuchas“anticipate”,“believe”,“plan”,“estimate”,“expect”,“potential”,“target”, “budget” and “intend” and statements that an event or result “may”, “will”, “should”, “could” or “might” occur or be achieved and other similar expressions and includes the negatives thereof.

Forward-looking statements are based onthe reasonable assumptions,estimates, analysis, and opinions of the management of the Company made in light of its experience and its perception of trends, current conditions and expected developments, as well as other factors that management of the Company believes to be relevant and reasonable in the circumstances at the date that such statements are made.Forward-looking information is based on reasonable assumptions that have been made by the Company as at the date of such information and is subject to known and unknown risks, uncertainties and other factors that may have caused actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information, includingbutnot limited to: risks associated with mineral exploration and development; metal and mineral prices; availability of capital; accuracy of the Company’s projections and estimates; realization of mineral resource estimates, interest and exchange rates; competition; stock price fluctuations; availability of drilling equipment and access; actual results of current exploration activities; government regulation; political or economic developments; environmental risks; insurance risks; capital expenditures; operating or technical difficulties in connection with development activities; personnel relations; and changes in Project parametersasplanscontinuetoberefined. Forward-looking statements are based on assumptions management believes to be reasonable, includingbutnotlimitedtothepriceofsilver,goldandbarite;thedemandforsilver,goldandbarite;theability tocarry on exploration and development activities; the timely receipt of any required approvals; the ability to obtain qualified personnel, equipment and services in a timely and cost-efficient manner; the ability to operate in a safe, efficient and effective matter; and the regulatory framework regarding environmental matters, and such other assumptions and factors as set out herein. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause resultsnottobeasanticipated,estimatedorintended.Therecanbenoassurancethatforward-lookingstatementswill prove to be accurate and actual results, and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward looking information contained herein, exceptinaccordancewithapplicablesecuritieslaws.Theforward-lookinginformationcontainedhereinispresentedfor thepurposeofassistinginvestorsinunderstandingtheCompany’sexpectedfinancialandoperationalperformanceand theCompany’splansandobjectivesandmaynotbeappropriateforotherpurposes.TheCompanydoesnotundertake to update any forward-looking information, except in accordance with applicable securities laws.