Vancouver, British Columbia–(Newsfile Corp. – January 6, 2026) – West Point Gold Corp. (TSXV: WPG) (OTCQB: WPGCF) (FSE: LRA0) (“West Point Gold” or the “Company”) is pleased to announce the results for four holes from the high-grade zone at Northeast (NE) Tyro, part of the ongoing 15,000 metre (m) drill program at its flagship Gold Chain Project in Arizona. The Company is reporting assay results for four drill holes (936 m), GC25-85 through GC25-88.

Highlights:

- Hole GC25-87 returned 27.4m of 9.56 g/t Au at 71.6m to 99.1m, including 13.7m of 18.00 g/t Au at 79.3m to 93.0m, about 50m up-dip from GC25-49 (62.5m at 4.73 g/t Au) – expanding the highest-grade part of the zone up-dip.

- Hole GC25-88 returned 44.2m of 5.46 g/t Au at 140.2m to 184.4m, including 18.3m of 12.04 g/t Au at 166.1m to 184.4m – expanding the high-grade zone along strike, as this is the furthest northeast hole at Tyro.

- Hole GC25-85 returned 29.0m of 5.24 g/t Au at 164.6m to 193.6m, including 12.2m of 10.48 g/t Au at 176.8m to 189.0m, about 80m down-dip from hole GC25-58 which returned 32.0m of 2.01 g/t Au.

- Hole GC25-86 returned 36.6m of 2.22 g/t Au at 179.8 to 216.4m about 140m down-dip from GC25-57 which returned 12.2m at 3.52 g/t Au.

- Drilling continues to explore the deeper portions of the high-grade zone between the Tyro NE and Main zones, with two holes (540 m) completed with assays pending. A total of 3,769 m of the planned 15,000m program was completed in 2025.

“Drilling at NE Tyro continues to return better than expected grades with good continuity at relatively shallow depths. The high-grade zone at NE Tyro appears to continue at depth and to the northeast, suggesting the zone remains open to further expansion as we continue drilling. We expect these results to positively impact the grade profile and the overall scale of our upcoming maiden resource. Drilling continues at Gold Chain, with one rig at NE Tyro, and one at Tyro South,” stated Derek Macpherson, President and CEO.

Table 1: Drill Results

| Holes | From (m) | To (m) | Width (m) | Grade (g/t Au) |

| GC25-85 | 164.6 | 193.6 | 29.0 | 5.24 |

| including | 176.8 | 189.0 | 12.2 | 10.48 |

| GC25-86 | 179.8 | 216.4 | 36.6 | 2.22 |

| GC25-87 | 71.6 | 99.1 | 27.4 | 9.56 |

| including | 79.3 | 93.0 | 13.7 | 18.00 |

| GC25-88 | 140.2 | 184.4 | 44.2 | 5.46 |

| including | 166.1 | 184.4 | 18.3 | 12.04 |

Note: All widths shown are downhole; true widths are approximately 50-90% of downhole widths; see Figure 3 for estimated true widths.

Figure 1: Plan view of the Main Tyro vein showing geology and drilling conducted in 2021, 2023, 2024 and 2025. Note the location of Hole Nos. GC25-85 through GC25-88.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/279547_08e927cc54e4ea19_002full.jpg

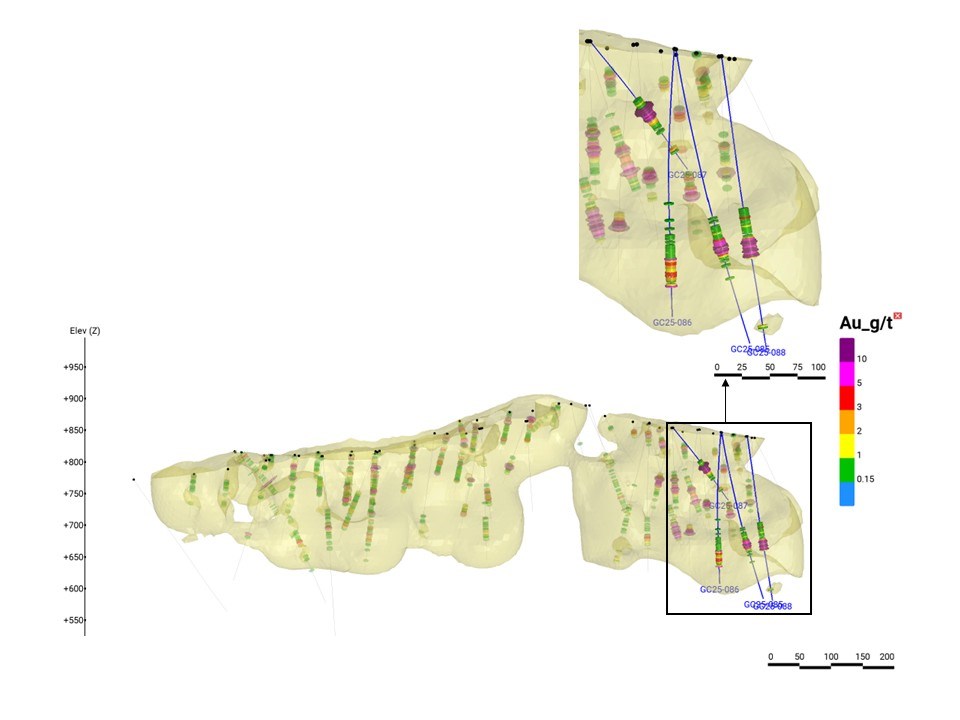

Figure 2. Longitudinal perspective of the Tyro Main and NE Zones, Showing Core and RC Drilling to Date. Holes GC25-85 through GC25-88 are highlighted and described below.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/279547_08e927cc54e4ea19_003full.jpg

Summary

The drilling of holes GC25-85 through GC25-88 continues to expand and provide improved definition for high-grade gold mineralization in the NE Tyro zone at the Company’s Gold Chain project in Arizona. The four holes comprising this release, GC25-85 through GC25-88, represent 936 m of the 3,769 m drilled to date in the current 15,000m program.

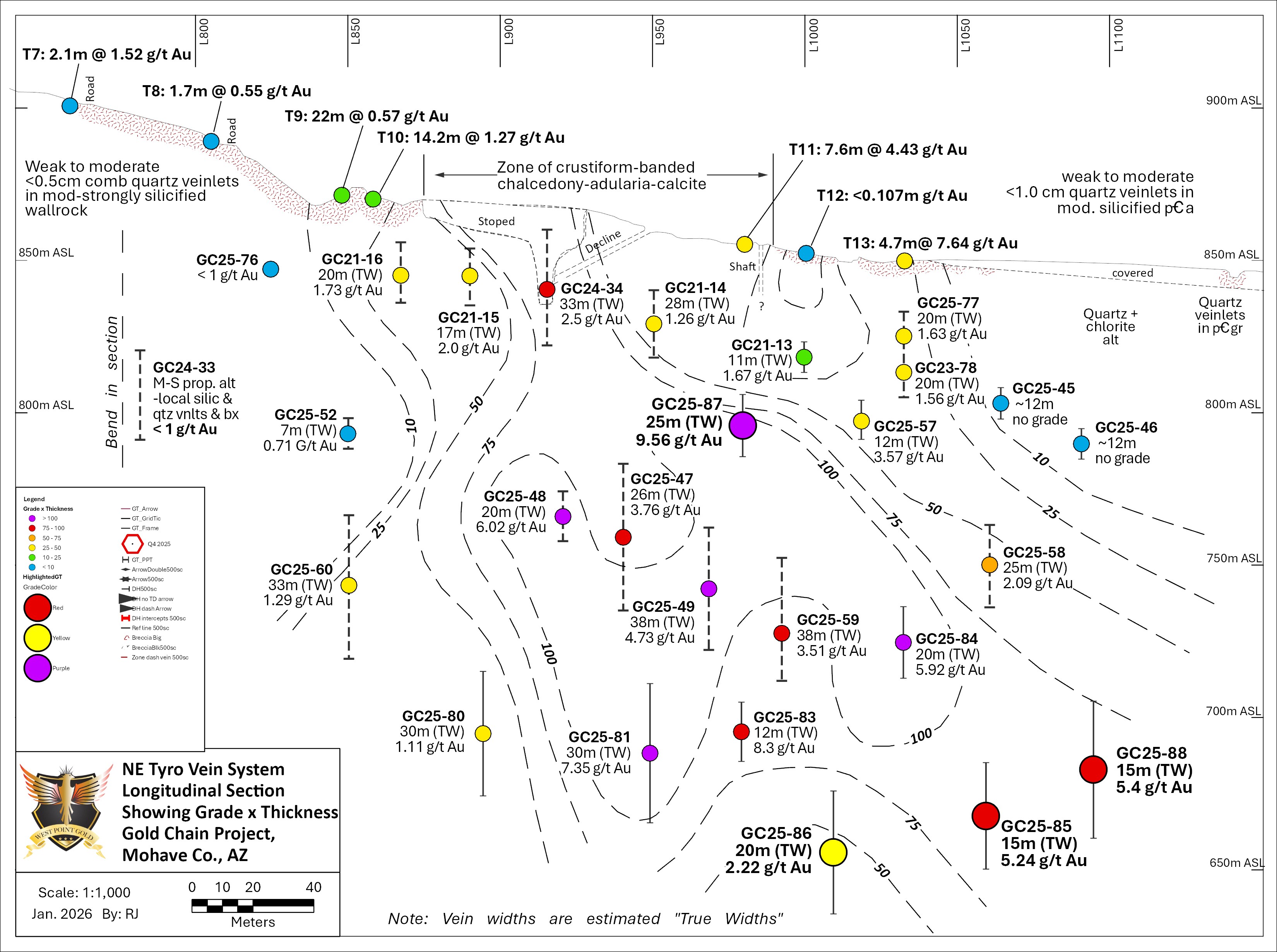

Each hole is briefly described below and graphically presented in both sectional and longitudinal views. Additionally, Figure 3 is a generalized longitudinal view of the NE Tyro zone showing the intercept’s mid-point, composite gold grade and estimated true width based upon geologic sections. The core of this zone remains mostly open to the northeast and to depth. West Point Gold anticipates the receipt of its Plan of Operations in early 2026, which will permit the drilling of both core and RC holes outside of the controlled patented claims, allowing for deeper tests and further exploration to the northeast and toward the Frisco Graben target area.

Along with the increased gold grades at depth, close inspection of the drill cuttings reveals an increase in varicolored chalcedony, crustiform banding, adularia and illite(?)-pyrite alteration in the wallrock.

Figure 3. Longitudinal Section Along the NE Tyro Zone Showing Drill Hole Pierce Points, Estimated True Width and Intercept Grade. Grades are Colour Coded to Better Illuminate the Shape and Orientation of the High-Grade Zone.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/279547_08e927cc54e4ea19_004full.jpg

Hole GC25-85

Hole GC25-85 traversed the Tyro NE vein/zone about 30m southwest of GC25-88 (44.2m at 5.46 g/t Au) and encountered from 164.6m to 193.6m (29.0m) 5.24 g/t Au enveloping a higher-grade zone of 12.2m at 10.48 g/t Au (Figure 2). The intercept’s midpoint is about 200m below the surface and without a surface expression, i.e. blind. The position of GC25-85 is provided in Figures 1 through 3.

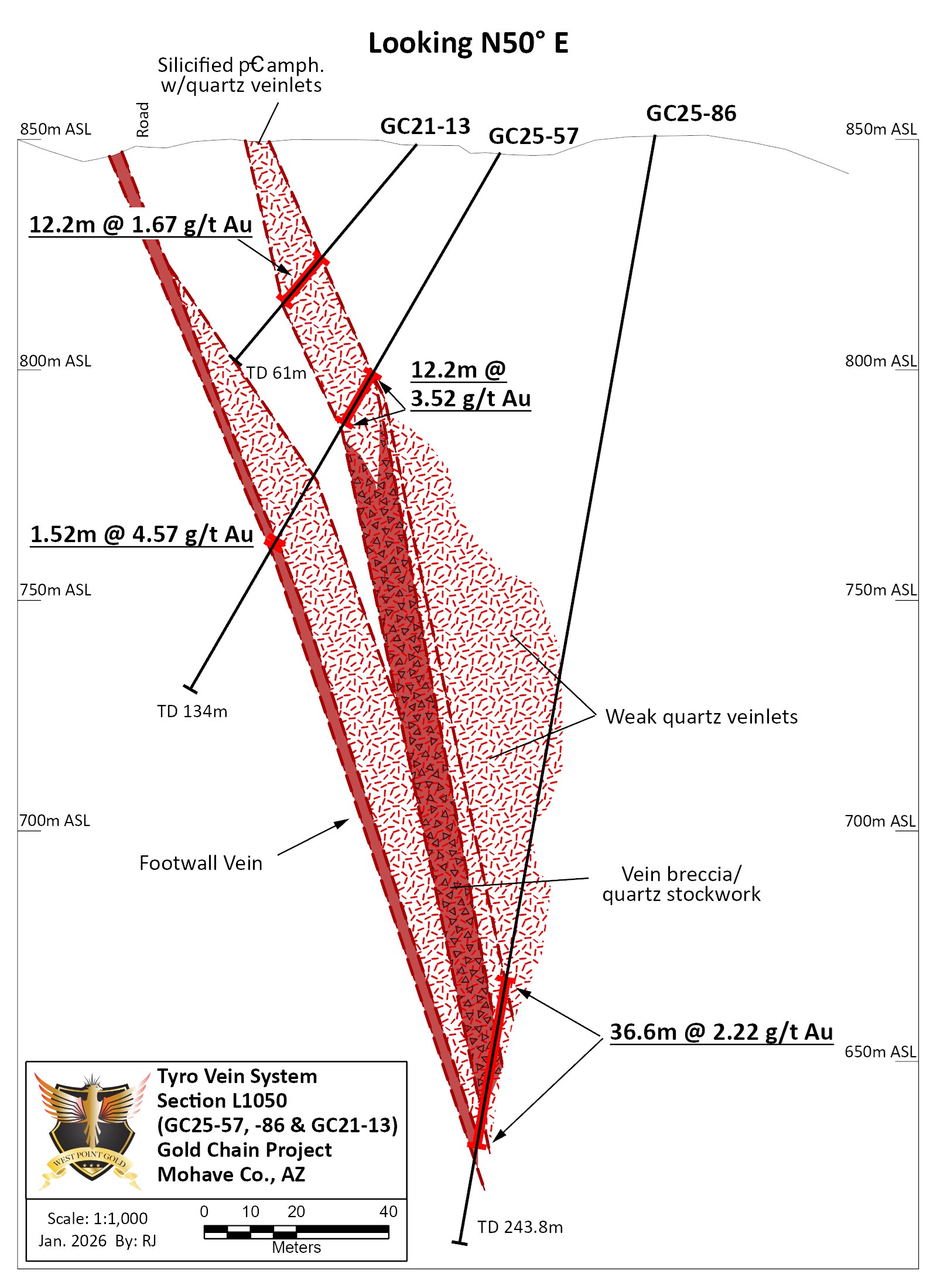

Hole GC25-86

Hole GC25-86 was drilled about 140m beneath hole GC25-57 and about 200m beneath a weak surface exposure of the vein. The hole traversed a broad zone of quartz veinlets which appeared to coalesce with depth. A mineralized zone was encountered at 179.8m to 216.4m (36.6m) at 2.22 g/t Au. A geologic summary of this hole is provided in Figures 3 and 4. The quartz-chalcedony-adularia-calcite vein resembles the surrounding intercepts, and the vein package remains broad. The results indicate that the mineralized zone has coalesced into a more discrete mineralized package or vein in the relatively short distance below Hole GC25-57.

Figure 4: Cross-Sectional View of Hole GC25-86 down-dip from Holes GC25-57 and GC21-13.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/279547_08e927cc54e4ea19_005full.jpg

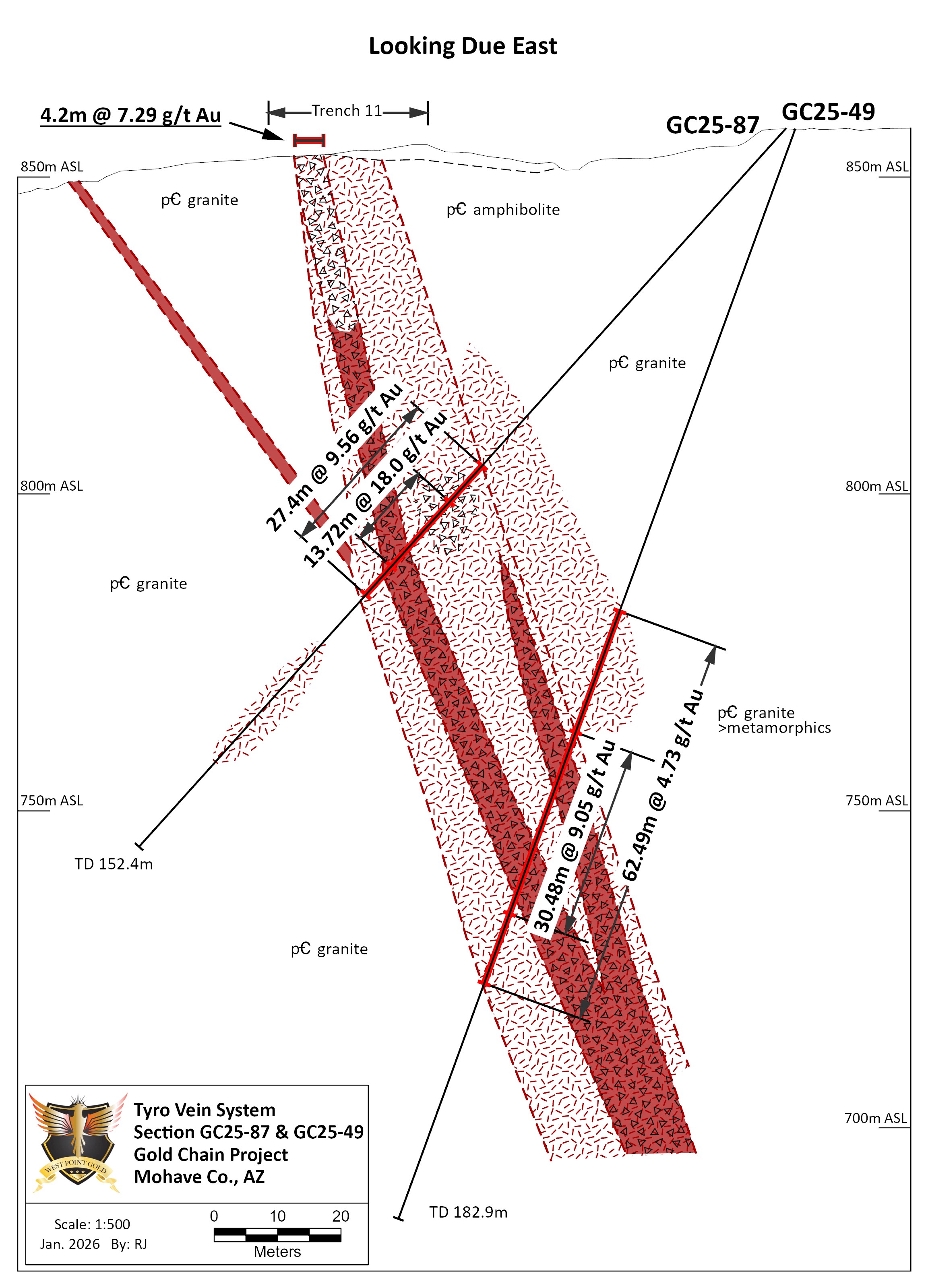

Hole GC25-87

Hole GC25-87 was designed to test the NE Tyro zone between the surface and Hole GC25-49 (62.5m at 4.73 g/t Au). The hole traversed the NE Tyro structure about 65 metres below the surface and 50 m above GC25-49 (Figure 5) from 71.6m to 99.1m (27.4 m) containing 9.56 g/t Au. An internal zone of higher gold grades corresponds to quartz-chalcedony-adularia-calcite vein and breccia, along with likely stockwork veining; the zone consisted of 13.7m of 18 g/t Au. Both intercepts shown in Figure 5 suggest good continuity in this area of the vein. Sections across the vein system in this area suggest a true width of 20 to 25 metres.

Figure 5: Cross-Sectional View of Hole GC25-87 up-dip from Hole GC25-49.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/279547_08e927cc54e4ea19_006full.jpg

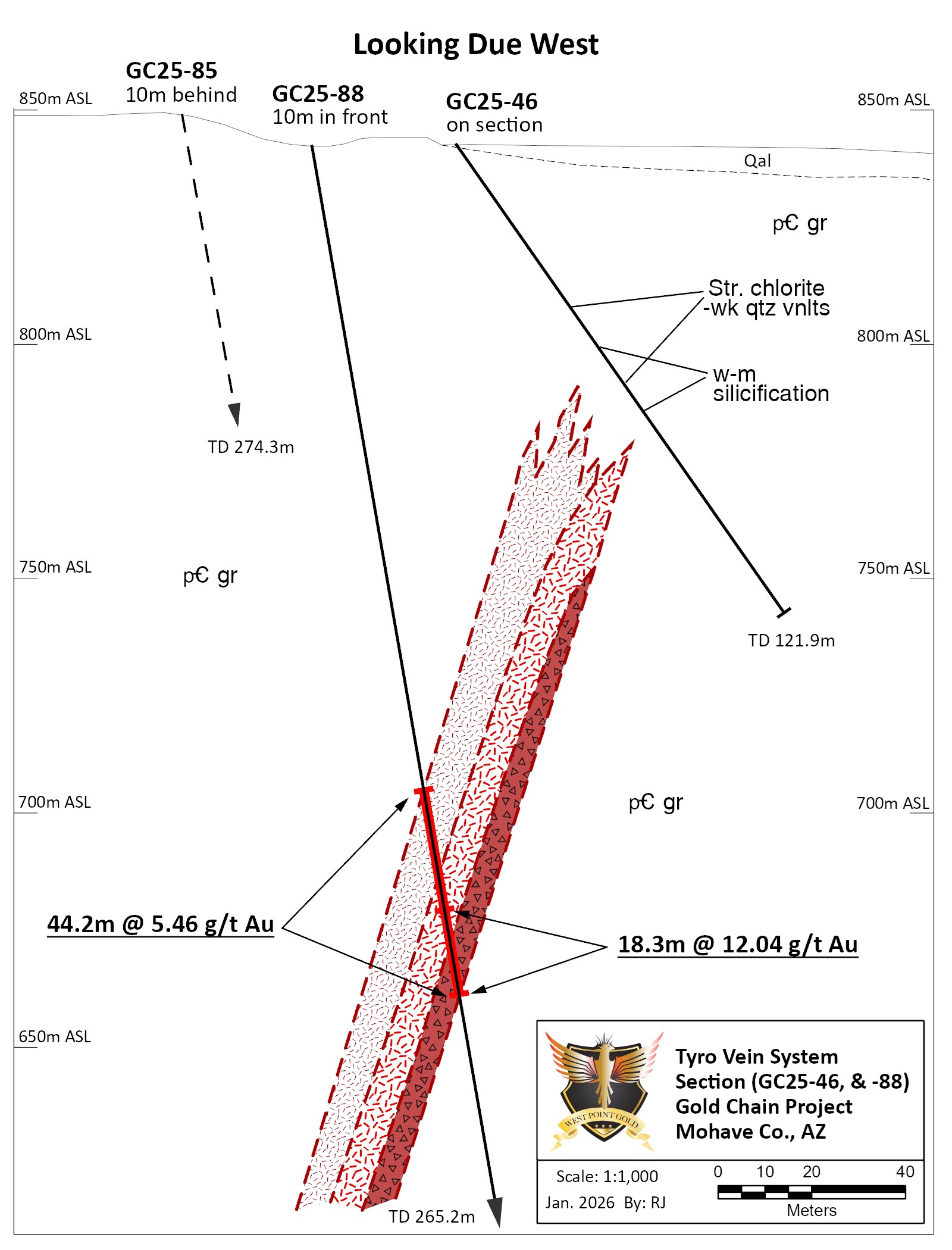

Hole GC25-88

Hole GC25-88, located in Figure 1, was designed to incrementally expand the limits of gold mineralization to the northeast and beneath earlier holes (GC25-45 and GC25-46) which encountered altered and weakly veined host rocks with negligible gold. A strong vein, shown in Figure 6, was encountered about 110 metres beneath GC25-46 from 140.2m to 184.4m and contained 5.46 g/t Au over 44.2m. An internal higher-grade interval, composed of mostly quartz-chalcedony-adularia-calcite, was identified at 166.1m to 184.4m containing 12.04 g/t Au over 18.3 metres. The overall intercept is dominated by quartz veinlets which coalesce into a vein breccia approaching the footwall contact. The estimated true width of this zone is about 15 metres and remains open to the northeast and at depth.

Figure 6: Cross Sectional View of Hole GC25-88 down-dip from Hole GC25-46.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/5717/279547_08e927cc54e4ea19_007full.jpg

Table 2: Drill hole locations and descriptions

| Hole No. | Azimuth | Inclination | Easting | Northing | Length (m) |

| (degrees) | (degrees) | ||||

| GC25-085 | 0 | -80 | 732388 | 3901514 | 274.3 |

| GC25-086 | 290 | -80 | 732386 | 3901511 | 243.8 |

| GC25-087 | 10 | -48 | 732305 | 3901484 | 152.4 |

| GC25-088 | 0 | -80 | 732413 | 3901542 | 265.2 |

Qualified Person

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration, is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for overseeing all phases of the drilling program, including logging, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Drillholes have a diameter of about 10cm, and samples have an approximate weight of 5 to 10kg. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, and over-limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), and over-limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. The results summarized above have been carefully reviewed with reference to the QA/QC results. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

About West Point Gold Corp.

West Point Gold is an exploration and development company focused on unlocking value across four strategically located projects along the prolific Walker Lane Trend in Nevada and Arizona, USA, providing shareholders with exposure to multiple discovery opportunities across one of North America’s most productive gold regions. The Company’s near-term priority is advancing its flagship Gold Chain Project in Arizona.

For further information regarding this press release, please contact:

Aaron Paterson, Corporate Communications Manager

Phone: +1 (778) 358-6173

Email: info@westpointgold.com

Stay Connected with Us:

LinkedIn: linkedin.com/company/west-point-gold

X (Twitter): @westpointgoldUS

Facebook: facebook.com/Westpointgold/

Website: westpointgold.com/

FORWARD-LOOKING STATEMENTS:

Certain statements contained in this press release constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, timing of the Company’s maiden resource estimate, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures. The Company cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete any payments or expenditures required under the Company’s various option agreements for its projects; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainties related to resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data; the potential for delays in exploration or development activities; uncertainty related to the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results may vary from those expected; statements about expected results of operations, royalties, cash flows, financial position may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions. The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; fluctuating gold prices; possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR+ made by the Company with securities regulators. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate press release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/279547