Burlington, Ontario–(Newsfile Corp. – July 13, 2022) – Silver Bullet Mines Corp. (TSXV: SBMI) (OTCQB: SBMCF) (“SBMI” or “the Company”) is both pleased and proud to announce it has successfully produced silver and copper at its wholly owned 125 metric ton per day mill near Globe, Arizona.

“This production is the result of years of hard work, planning and dedication, and the incredible talents of the Arizona team,” said A. John Carter, SBMI’s CEO. “Over the past ten months, despite COVID-19 and global supply chain issues, we have spent less than three million dollars building this fully functional mill, a staggering feat. This is to my mind a one-of-a-kind experience.”

The mill produced its first silver concentrate from lower grade ore on July 12, 2022 and plans to soon pour its first dore bars. The Company intends to continue to use lower grade ore to optimize recovery efficiency and fine tune the various mill components. Higher grade ore will be introduced into the system once the mill is operating at higher rates of recovery. To date there have been no major setbacks and all components are operating within expected parameters.

Below is a photo of the first band of silver coming off the shaker table. The silver is visible on the left side of the photo. The secondary concentrate line is a silver/copper blend which will be bagged and sold. The initial concentrate and dore should be sold to various refineries, whose apparent demand should account for SBMI’s entire silver and copper production over the coming weeks.

A video of the shaker table operating can be found at the Company’s website, www.silverbulletmines.com.

The Buckeye Silver Mine is the source of the bulk sample ore for the mill. Both the mill and the Buckeye Mine are 100% controlled by SBMI. At the Buckeye, the field team is currently extracting ore from a vein at a location where it is approximately 12 feet wide. SBMI’s target is to have at least one month (5,000 tonnes) of raw ore available to the mill at all times, meaning management expects ore to be continually shipped from the Buckeye to the mill on a regular schedule.

Over the coming weeks management expects a steady stream of announcements as material milestones are met.

Please check the Company’s website www.silverbulletmines.com, or follow on Twitter @bulletmines or at YouTube “Silver Bullet Mines”.

For further information, please contact:

John Carter Silver Bullet Mines Corp., CEO cartera@sympatico.ca +1 (905) 302-3843

Peter M. Clausi Silver Bullet Mines Corp., VP Capital Markets pclausi@brantcapital.ca +1 (416) 890-1232

Cautionary and Forward-Looking Statements

Silver Bullet Mines Corp. trades on the TSX Venture Exchange under the symbol SBMI and on the OTCQB Venture Market under the symbol SBMCF. The OTCQB Venture Market is for early stage and developing U.S. and international companies. Companies listed there are current in their reporting and undergo an annual verification and management certification process. Investors can find current financial disclosure for the Company on www.otcmarkets.com and at https://money.tmx.com/en/quote/SBMI.

This news release contains certain statements that constitute forward-looking statements as they relate to SBMI and its subsidiaries. Forward-looking statements are not historical facts but represent management’s current expectation of future events, and can be identified by words such as “believe”, “expects”, “will”, “intends”, “plans”, “projects”, “anticipates”, “estimates”, “continues” and similar expressions. Although management believes that the expectations represented in such forward-looking statements are reasonable, there can be no assurance that they will prove to be correct.

By their nature, forward-looking statements include assumptions, and are subject to inherent risks and uncertainties that could cause actual future results, conditions, actions or events to differ materially from those in the forward-looking statements. If and when forward-looking statements are set out in this new release, SBMI will also set out the material risk factors or assumptions used to develop the forward-looking statements. Except as expressly required by applicable securities laws, SBMI assumes no obligation to update or revise any forward-looking statements. The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: the impact of SARS CoV-2 or any other global virus; reliance on key personnel; the availability of skilled and unskilled labour; the presence and recoverability of mineralization; ongoing availability of infrastructure such as electrical, diesel and road access; the thoroughness of its QA/QA procedures; the continuity of the global supply chain for materials for SBMI to use in the production and processing of ore; shareholder, permitting and regulatory approvals; activities and attitudes of communities local to the location of SBMI’s properties; price increases related to supply chain issues; risks of future legal proceedings; income tax matters; fires, floods and other natural phenomena; the rate of inflation; availability and terms of financing; distribution of securities; commodities pricing; currency movements, especially as between the USD and CDN; effect of market interest rates on price of securities; and, potential dilution. SARS CoV-2 and other potential global viruses create risks that at this time are immeasurable and impossible to define.

Vancouver, British Columbia–(Newsfile Corp. – July 13, 2022) – Dolly Varden Silver Corporation (TSXV: DV) (OTCQX: DOLLF) (the “Company” or “Dolly Varden“) is pleased to announce that Rob van Egmond, P.Geo has been appointed Vice President of Exploration and to give an update on ongoing drilling work at the Kitsault Valley Project, located near tidewater in northwestern British Columbia.

To-date, three drills have cored over 7,700 meters in 27 holes of the planned 30,000 meter program in 99 holes. Initial work has focussed on stepping out from wide, high grade silver intercepts, particularly at the Kitsol Vein and Wolf Mine. Based on visual indicators of mineralization and veining, drills have continued to step-out in these areas, with the deepest hole at Wolf extended to 720 meters long and 400 meters at Kitsol at the Torbrit Deposit. Assays are pending for this drilling, however lab turnaround times are expected to be much improved during the 2022 season.

“First, we are excited to promote Rob Van Egmond to Vice-President Exploration as an officer and leader of the Company, as we accelerate our new phase of growth for Dolly Varden Silver,” says Shawn Khunkhun, President and CEO. “Second, we are very encouraged with our initial drilling in multiple areas on the Property. Our focus is primarily resource expansion and discovery at our silver-rich targets at the south end of the Kitsault Valley trend and are now commencing resource upgrade drilling and regional exploration at our recently acquired gold and silver-rich Homestake Ridge targets in the north.”

Rob Van Egmond, VP Exploration

Over the past two years, Dolly Varden Silver has expanded its technical team to support exploration and potential future development its Kitsault Valley Project as well as ongoing Corporate Development work. As a leader in these efforts, Rob van Egmond has been appointed Vice President of Exploration. Rob brings extensive exploration experience from generative, grass-roots to advanced Project development, mine site exploration and production. He was part of the Team with Platinum Group Metals that discovered and defined the massive Waterburg Platinum-Palladium deposit within the previously unknown northern extension of the Bushveld complex in South Africa. As Candente Copper’s Country Manager for Peru, he led the exploration and resource definition work that defined the multi-billion tonne Canariaco copper porphyry deposit, from initial drilling to the Pre-Feasibility Studies. Additionally, he has extensive experience in Canada’s north, including diamond exploration and resource development for BHP at the Ekati Mine and for Kennecott/Aber JV at the Diavik Mine. While with BHP, Rob also worked as an open-pit mine geologist at the Island Copper Operation in B.C. and as an Exploration Geologist in the Hope Bay greenstone gold belt in Nunavut.

Rob started his exploration career in the Golden Triangle for Cominco and returned as Chief Geologist for the Dolly Varden Project in 2017.

Exploration Update

The 2022 exploration program is balanced between Mineral Resource expansion and upgrading at five of the deposits that comprise the Kitsault Valley Project and exploration work focusing on the discovery of new silver and gold deposits. The objective of infill drilling is to convert Inferred mineral resource to the Measured and Indicated category with infill, with an emphasis on Inferred Resources at the recently acquired Homestake Ridge Area. Step out drilling is being performed at most resource areas, with an early emphasis during the 2022 season at the Torbrit/Kitsol/North Star deposits and Mineral Resources at the historic Wolf Mine. Stepout drilling is also planned later in the Season at Homestake Ridge and Homestake Silver deposits. Late winter snowpacks have delayed the start of drilling at the latter, with initial drilling expected this week. Drill productivity and core recovery have been excellent during the first five weeks of exploration on the Property.

Over half of this season’s exploration work is allocated to discover of new deposits, primarily silver-rich systems but also gold and copper targets. The Kitsault Valley Project currently contains 34.7 million ounces of silver and 166 thousand ounces of gold in the Indicated category and 29.3 million ounces of silver and 817 thousand ounces of gold in the Inferred category within a 163 square km consolidated land package. There are numerous new exploration targets located in the 5.4 kilometer long corridor between the Homestake Ridge and Dolly Varden deposits that are currently being explored, with one drill currently targeting these areas. Ongoing surface geology by the Company’s strong technical team and geophysical exploration will be used to generate and vector into drill targets. Currently, 20 exploration targets have been identified, eight of which are considered highest priority. Ground Induced-Polarity (“IP”) geophysical surveys will be commencing shortly on the Kitsault Valley Project.

In addition to drilling and surface exploration, Camp expansion and infrastructure upgrades have been completed in Alice Arm, BC as well as upgrades and repairs to the road bed and right of way that extends north to from tidewater to the Torbrit Mine.

About Dolly Varden Silver Corporation

Dolly Varden Silver Corporation is a mineral exploration company focused on advancing its 100% held Kitsault Valley Project (which combines the Dolly Varden Project and the Homestake Ridge Project) located in the Golden Triangle of British Columbia, Canada, 25kms by road to the Pacific ocean. The 163 sq. km. project hosts the high-grade silver and gold resources of Dolly Varden and Homestake Ridge along with the past producing Dolly Varden and Torbrit silver mines. It is considered to be prospective for hosting further precious metal deposits, being on the same structural and stratigraphic belts that host numerous other, on-trend, high-grade deposits, such as Eskay Creek and Brucejack. The Kitsault Valley Project also contains the Big Bulk property which is prospective for porphyry and skarn style copper and gold mineralization, similar to other such deposits in the region (Red Mountain, KSM, Red Chris).

QP Statement

Rob Van Egmond, P.Geo., Vice President Exploration for the Company and a Qualified Person, as defined by NI 43-101, has reviewed and approved the scientific and technical content of this release.

Forward-Looking Statements

This release may contain forward-looking statements or forward-looking information under applicable Canadian securities legislation that may not be based on historical fact, including, without limitation, statements containing the words “believe”, “may”, “plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”, “expect”, “potential”, and similar expressions. Forward-looking statements involve known and unknown risks, uncertainties, and other factors which may cause the actual results, performance, or achievements of Dolly Varden to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. Forward-looking statements or information in this release relates to, among other things, completion of the Offering, TSX Venture Exchange approval of the Offering, the use of proceeds with respect to the Offerings, the results of previous field work and programs and the continued operations of the current exploration program, interpretation of the nature of the mineralization at the project and that that the mineralization on the project is similar to Eskay and Brucejack, results of the mineral resource estimate on the project, the potential to grow the project, the potential to expand the mineralization and our beliefs about the unexplored portion of the property.

These forward-looking statements are based on management’s current expectations and beliefs and assume, among other things, the ability of the Company to successfully pursue its current development plans, that future sources of funding will be available to the company, that relevant commodity prices will remain at levels that are economically viable for the Company and that the Company will receive relevant permits in a timely manner in order to enable its operations, but given the uncertainties, assumptions and risks, readers are cautioned not to place undue reliance on such forward-looking statements or information. The Company disclaims any obligation to update, or to publicly announce, any such statements, events or developments except as required by law.

For additional information on risks and uncertainties, see the Company’s most recently filed annual management discussion & analysis (“MD&A“) and management information circular dated January 21, 2022 (the “Circular“), both of which are available on SEDAR at www.sedar.com. The risk factors identified in the MD&A and the Circular are not intended to represent a complete list of factors that could affect the Company.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this news release.

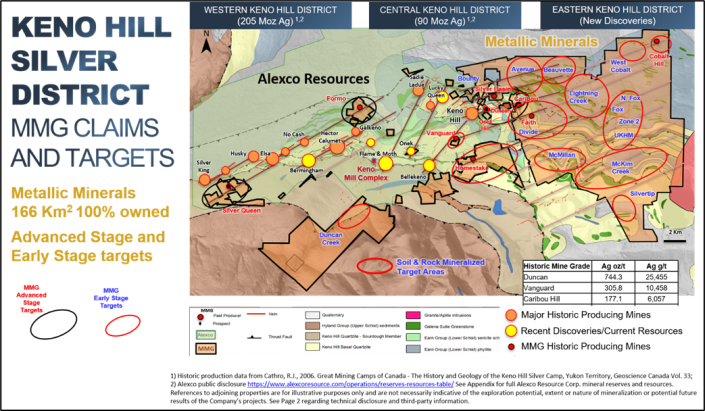

VANCOUVER, BC / ACCESSWIRE / July 13, 2022 / Metallic Minerals (TSXV:MMG | US OTCQB:MMNGF) (“Metallic Minerals“, or the “Company“) announces the commencement of field activities at the Company’s 100% owned, 166 square kilometer Keno Silver project, located in the historic Keno Hill silver district of Canada’s Yukon Territory. In July 2022, Hecla Mining Company (“Hecla”), the largest silver producer in the United States and third largest in the world1, announced the acquisition of neighboring Alexco Resource Corp.(“Alexco”), which holds the western portion of the district and mining and milling operations. Metallic Minerals owns the second largest land position in the prolific district covering the east, and parts of central and western Keno Hill, including eight high-grade, shallow past-producing deposits.

The 2022 exploration program is expected to consist of at least 3,000 meters of diamond core drilling, focused on resource definition drilling at multiple advanced-stage targets including Formo and Caribou deposits in the West Keno and Central Keno areas and the recently discovered Fox target area in East Keno, as well as step out drilling at several new discoveries. Detailed geophysical and soil surveys will also be conducted to aid in refinement and prioritization of reconnaissance drill targets in several untested target areas. Additionally, for the first time, the district will be flown for a LIDAR survey, which will provide greater precision in survey and topographic control while aiding in lineament detection in the search for new Keno-style high-grade silver discoveries.

Metallic Minerals President, Scott Petsel, commented: “We are excited to be initiating our 2022 field campaign at the Keno Silver project, particularly in the wake of the recently announced acquisition of our neighbors at Alexco by Hecla. This is a re-energizing catalyst for the Keno Hill silver district and highlights the quality of the existing reserves and resources and the exploration potential in one of the world’s highest grade silver producing regions that has produced over 200 million ounces of ultra-high-grade silver. We have enjoyed a close and productive working relationship with the team at Alexco and are excited to see the mining operation reach its full potential.”

Metallic Minerals Corp., Tuesday, July 12, 2022, Press release picture

“Metallic Minerals is on the cusp of transforming our own story in the Keno silver district as this year’s drill program is focused on advancing existing mineral inventories to formal NI 43-101 resources at our most advanced targets. In addition, we expect to announce commencement of field activity at our La Plata silver-gold-copper project in Colorado shortly, as well as updates with regard to planned activities on our Klondike alluvial gold royalty portfolio.”

Private Placement

Metallic has completed and closed its second non-brokered private placement financing for total proceeds raised of $4,649,820. Proceeds from the two private placements will be used toward eligible Canadian exploration expenses, within the meaning of the Income Tax Act (Canada) and for general working capital.

The second private placement consisted of the issuance of 1,471,000 units at a price of $0.42 per unit for aggregate proceeds of $617,820. Each unit consisted of one common share and one-half purchase warrant where each whole warrant is exercisable into a common share for 30 months at a price of $0.50. A total of 846,000 units were sold on a flow-through basis with the common share comprising the units being issued as a flow-through common share.

The common shares comprising the units are subject to a hold period of four months and one day from their date of issuance under applicable Canadian securities law. The flow-through shares have not been, and will not be, registered under the U.S. Securities Act or any U.S. state securities laws, and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons absent registration or any applicable exemption from the registration requirements of the U.S. Securities Act and applicable U.S. state securities laws.

An officer of the company participated in the private placement for a total of 25,000 units. The participation by the insider in the private placement is considered to be a related party transaction as defined under Multilateral Instrument 61-101. The transaction is exempt from the formal valuation and minority shareholder approval requirements of MI 61-101, as neither the fair market value of the securities being issued, nor the consideration being paid exceeds 25% of the Company’s market capitalization.

About the Keno Silver Project

Keno Hill is one of the world’s highest-grade silver districts, with nearly 300 million ounces (“Moz”) of silver in past production and current M&I resources1,2 and featuring excellent existing infrastructure, including grid power, road access and nearby community services. In July 2022, Hecla announced the acquisition of Alexco Resource Corp, which holds the western portion of the district and mining and milling operations. Metallic Minerals’ Keno Silver project is adjacent and contiguous, covering the east, and parts of the central and western Keno silver district and includes eight high-grade, shallow past-producing mines. Prior to the Company’s consolidation of the land package, very little modern exploration had been completed in these parts of the district due to fragmented, private land ownership. Metallic Minerals has advanced three targets in the district from discovery to expansion drilling with several additional targets at drill-ready status along the known historically productive trends. In addition, recent exploration has defined and expanded 12 new priority multi-kilometer-scale early-stage targets for reconnaissance drilling in the under-explored parts of the district where highly elevated silver, lead and zinc in soils and high-grade rock samples have been identified.

Metallic Minerals Corp., Tuesday, July 12, 2022, Press release picture

2022 Drilling at Fox Target at East Keno

About Metallic Minerals

Metallic Minerals Corp. is an exploration and development stage company, focused on silver, gold and copper in the high-grade Keno Hill and La Plata mining districts of North America. Our objective is to create shareholder value through a systematic, entrepreneurial approach to making exploration discoveries, growing resources and advancing projects toward development. Metallic Minerals has consolidated the second-largest land position in the historic Keno Hill silver district of Canada’s Yukon Territory, directly adjacent to Alexco Resource Corp’s operations, with more than 300 million ounces of high-grade silver in past production and current M&I resources. Hecla Mining Company, the largest primary silver producer in the USA and fourth largest in the world, announced the acquisition of Alexco in July 2022. Metallic recently announced the inaugural NI 43-101 mineral resource estimate for its La Plata silver-gold-copper project in southwestern Colorado. The Company also continues to add new production royalty leases on its holdings in the Klondike gold district in the Yukon. All three districts have seen significant mineral production and have existing infrastructure, including power and road access. Metallic Minerals is led by a team with a track record of discovery and exploration success on several major precious and base metal deposits, as well as having large-scale development, permitting and project financing expertise.

About the Metallic Group of Companies

The Metallic Group is a collaboration of leading precious and base metals exploration and development companies, with a portfolio of large, brownfields assets in established mining districts adjacent to some of the industry’s highest-grade producers of silver and gold, platinum and palladium, and copper. Member companies include Metallic Minerals in the Yukon’s high-grade Keno Hill silver district and La Plata silver-gold-copper district of Colorado, Granite Creek Copper in the Yukon’s Minto copper district, and Stillwater Critical Minerals in the Stillwater PGE-nickel-copper district of Montana and Kluane district in the Yukon. The founders and team members of the Metallic Group include highly successful explorationists formerly with some of the industry’s leading explorer/developers and major producers. With this expertise, the companies are undertaking a systematic approach to exploration and development using new models and technologies to facilitate discoveries in these proven, but under-explored, mining districts. Members of the Metallic Group have been recognized as recipients of awards for excellence in environmental stewardship demonstrating commitment to responsible resource development and appropriate ESG practices. The Metallic Group is headquartered in Vancouver, BC, Canada, and its member companies are listed on the Toronto Venture, US OTCQB and Frankfurt stock exchanges.

Forward Looking Statements: This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Metallic Minerals believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Group Ten and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Burlington, Ontario–(Newsfile Corp. – July 12, 2022) – Silver Bullet Mines Corp. (TSXV: SBMI) (OTCQB: SBMCF) (“SBMI” or “the Company”) announces it has settled a payable to a significant shareholder of the Company in the amount of $70,800 by the issuance of 236,000 common shares at $0.30 cents per share. This shareholder elected to settle the payable by taking equity rather than cash, a strong sign of confidence in SBMI’s business plan.

John Carter Silver Bullet Mines Corp., CEO cartera@sympatico.ca +1 (905) 302-3843

Peter M. Clausi Silver Bullet Mines Corp., VP Capital Markets pclausi@brantcapital.ca +1 (416) 890-1232

Cautionary and Forward-Looking Statements

Silver Bullet Mines Corp. trades on the TSX Venture Exchange under the symbol SBMI and on the OTCQB Venture Market under the symbol SBMCF. The OTCQB Venture Market is for early stage and developing U.S. and international companies. Companies listed there are current in their reporting and undergo an annual verification and management certification process. Investors can find current financial disclosure for the Company on www.otcmarkets.com and at https://money.tmx.com/en/quote/SBMI.

This news release contains certain statements that constitute forward-looking statements as they relate to SBMI and its subsidiaries. Forward-looking statements are not historical facts but represent management’s current expectation of future events, and can be identified by words such as “believe”, “expects”, “will”, “intends”, “plans”, “projects”, “anticipates”, “estimates”, “continues” and similar expressions. Although management believes that the expectations represented in such forward-looking statements are reasonable, there can be no assurance that they will prove to be correct.

By their nature, forward-looking statements include assumptions, and are subject to inherent risks and uncertainties that could cause actual future results, conditions, actions or events to differ materially from those in the forward-looking statements. If and when forward-looking statements are set out in this new release, SBMI will also set out the material risk factors or assumptions used to develop the forward-looking statements. Except as expressly required by applicable securities laws, SBMI assumes no obligation to update or revise any forward-looking statements. The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: the impact of SARS CoV-2 or any other global virus; reliance on key personnel; the availability of skilled and unskilled labour; the presence and recoverability of mineralization; ongoing availability of infrastructure such as electrical, diesel and road access; the thoroughness of its QA/QA procedures; the continuity of the global supply chain for materials for SBMI to use in the production and processing of ore; shareholder, permitting and regulatory approvals; activities and attitudes of communities local to the location of SBMI’s properties; price increases related to supply chain issues; risks of future legal proceedings; income tax matters; fires, floods and other natural phenomena; the rate of inflation; availability and terms of financing; distribution of securities; commodities pricing; currency movements, especially as between the USD and CDN; effect of market interest rates on price of securities; and, potential dilution. SARS CoV-2 and other potential global viruses create risks that at this time are immeasurable and impossible to define.

To view the source version of this press release, please visit

Joining us for a conversation is Dr. Roger Moss the CEO as Labrador Gold has just announced its highest-grade mineralization coming from the Big Vein along with updates on the Golden Glove and Midway Targets on the 100% owned Kingsway Project.

Labrador Gold is a Canadian-based mineral exploration (junior mining) company focused on the acquisition and exploration of prospective gold projects in Eastern Canada. The Company is advancing the Kingsway Gold Project, located in the Gander Gold District of Newfoundland. The project is strategically located contiguous to New Found Gold’s Queensway Project and lies along strike to the northeast of their recent discovery of 92.86g/t Au over 19.0 meters.

Key Shareholders: Eric Sprott, Quinton Hennigh, Crescat Capital, Palisaides Goldcorp, & New Found Gold.

In the recent Wall Street Journal article “Inflation Surge Earns Monetarism Another Look,” Greg Ip writes that a recent surge in inflation is not likely to bring authorities to reembrace monetarism. According to Ip, money supply had a poor record of predicting US inflation because of conceptual and definitional problems that haven’t gone away.

The head of the monetarist school, the late Milton Friedman, held that inflation is always and everywhere a monetary phenomenon. Friedman and other monetarists believed that the key driving factor for general increases in prices is increases in money supply.

This viewpoint has come under scrutiny since the early 1980s because the correlation between inflation and money supply disappeared. According to Ip in 2020, Alan Detmeister, an economist at UBS Group AG and formerly of the Fed, found inflation’s correlation to M2 since the early 1980s was weak and its correlation to both the monetary base and M1 was negative. Most economists have stopped using money supply as an indicator for inflation since the early 1980s.

Many mainstream economists have attributed the breakdown in the correlation between the money supply and inflation on the unstable velocity of money. What is it? According to the famous equation of exchange, MV = PT, where:

M stands for money,

V stands for the velocity of money,

P stands for the price level, and

T for the volume of transactions.

This equation states that money multiplied by velocity equals the value of transactions. Many economists employ GDP (gross domestic product) instead of PT, thereby concluding that

MV = GDP = P (real GDP).

The equation of exchange appears to offer a wealth of information regarding the state of an economy. For instance, if one were to assume stable velocity, then for a given stock of money one can establish the value of GDP. Furthermore, a given real output and a given stock of money enables us to establish the price level.

For most economists the equation of exchange is regarded as a very useful analytical tool. The debates that economists have are predominantly with respect to the stability of velocity. If velocity is stable, then money is seen as a very powerful tool in tracking the economy. The importance of money as an economic indicator however diminishes once velocity becomes less stable and hence less predictable.

However, an unstable velocity could occur because of an unstable demand for money. Most experts believe that since the early 1980s, innovations in financial markets made money velocity unstable. This in turn made money an unreliable indicator of inflation.

We believe the alleged failure of money as an indicator of inflation emanates from an erroneous definition of inflation and money supply. This failure has nothing to do with an unstable demand for money, and just because people change their demand for money does not imply instability. Because an individual’s goals may change, he might decide that it benefits him to hold less money. Sometime in the future, he might increase his demand for money. What could possibly be wrong with this? The same goes for any other goods and services—demand for them changes all the time.

Defining Inflation

According to Murray Rothbard and Ludwig von Mises, inflation is defined as the increase of the money supply out of “thin air.” Following this definition, one can ascertain that increases in money supply set economic impoverishment in motion by creating an exchange of nothing for something, the so-called counterfeit effect.

General increases in prices are likely to be symptoms of inflation—but not always, however. Note that prices are determined by both real and monetary factors. Consequently, it can occur that if the real factors are “pulling things” in an opposite direction to monetary factors, no visible change in prices is going to take place. If the growth rate of money is 5 percent and the growth rate of goods supply is 1 percent then prices are likely to increase by 4 percent. If, however, the growth rate in goods supply is also 5 percent then no general increase in prices is likely to take place.

If one were to hold that inflation is about increases in prices, then one would conclude that, despite the increase in money supply by 5 percent, inflation is 0 percent. However, if we were to follow the definition that inflation is about increases in the money supply, then we would conclude that inflation is 5 percent, regardless of any movement in prices.

Defining Money Supply

Prior to 1980, it was popular to employ various money supply definitions in the assessment of the changes in the prices of goods and services. The criterion for the selection of a particular definition was its correlation with national income. However, since the early 1980s, correlations between various definitions of money and national income have broken down. Some analysts believe that this breakdown is because of changes in financial markets, making past definitions of money irrelevant.

A definition presents the essence of a particular entity, something no statistical correlation could ever provide. To establish the definition of money we have to explain the origins of the money economy. Money has emerged because barter cannot support the market economy. Money is the general medium of exchange and has evolved from the most marketable commodity. Mises wrote:

There would be an inevitable tendency for the less marketable of the series of goods used as media of exchange to be one by one rejected until at last only a single commodity remained, which was universally employed as a medium of exchange; in a word, money.

Since the general medium of exchange was selected out of a wide range of commodities, the emerged money must be a commodity. Rothbard wrote:

In contrast to directly used consumers’ or producers’ goods, money must have pre-existing prices on which to ground a demand. But the only way this can happen is by beginning with a useful commodity under barter, and then adding demand for a medium to the previous demand for direct use (e.g., for ornaments, in the case of gold).

Through an ongoing selection process, individuals settled on gold as standard money. In today’s monetary system, the core of the money supply is no longer gold, but rather coins and notes issued by the government and central bank that are employed in transactions as goods and services are exchanged for cash. Hence, one trades all other goods and services for money.

Part of the stock of cash is stored through bank deposits. Once someone places money in a bank’s warehouse, he is engaging in a claim transaction, never relinquishing his ownership of the money. Consequently, these deposits, which are labelled demand deposits, are part of money.

This is contrasted with a credit transaction, where the lender relinquishes his claim over the money for the duration of the loan. In a credit transaction, money is transferred from a lender to a borrower, but the overall amount of money in the economy does not change because of the credit transaction.

The introduction of electronic money seems to cast doubt on the definition of money. It would appear that deregulated financial markets generate various forms of new money. Notwithstanding, various forms of electronic money or e-money, like digital currency, do not have a “life of their own.”

Various financial innovations do not generate new forms of money but rather new ways of employing existing money in transactions. Irrespective of these financial innovations, the nature of money does not change. Money is the thing that all other goods and services are traded for. Once the essence of money is established by excluding various credit transactions, one can identify the status of inflation. Changes in prices are not going to be relevant here.

Conclusion

Contrary to popular thinking, inflation is not about increases in the prices of goods and services but about increases in money supply. Following this definition, we can establish that the key damage caused by inflation is economic impoverishment through the exchange of nothing for something. What matters as far as inflation is concerned is not the correlation between money supply and the prices of goods and service but increases in money supply.

Contrary to popular thinking, the essence of money did not change because of various financial innovations. Money is a thing that is employed as a medium of exchange. Furthermore, according to Mises’s regression theorem, the historical link between paper currency and gold is what holds the present monetary system together.

Frank Shostak‘s consulting firm, Applied Austrian School Economics, provides in-depth assessments of financial markets and global economies. Contact: email.

Vancouver, British Columbia–(Newsfile Corp. – July 5, 2022) – Strikepoint Gold Inc. (TSXV: SKP) (OTCQB: STKXF) (“StrikePoint” or the “Company”) is pleased to announce that exploration work has commenced at its 100%-owned Properties located near Stewart, BC in British Columbia’s prolific Golden Triangle. 3,000 metres of drilling is planned at the Willoughby gold-silver and Porter Silver Properties, in addition to surface sampling and mapping programs with an emphasis on exploration at the Porter Silver Property.

Shawn Khunkhun, President and CEO of Strikepoint states, “With a healthy treasury over $5 million, we are excited to commence our drilling programs at the Porter and Willoughby Properties. At Porter, our work will continue to test the limits and source of the historic silver mines; at Willoughby, we will also seek new high-grade gold-silver discoveries in previously unexplored areas.”

Porter Silver Property

The Porter Property hosts the three highest-grade pure silver historic producers in the Stewart area: the Prosperity, Porter Idaho and Silverado mines. Objectives for the 2022 season include:

Drill extensions to high-grade silver mineralization outlined in historic resource estimates

Explore for the roots of the silver veins and gold-silver-rich intrusive-related mineralization

Assess the underground access and workings for future rehabilitation

1,600 metres of drilling is planned at Porter, initially targeting the past-producing Prosperity, Blind and D veins in 8-10 holes. Additionally, mapping and sampling will be completed prioritizing exploring the northwest and eastern areas of the Property. Work at the western side will investigate strong alteration and gossan with historic gold-rich prospects along northwest trending structures. On the eastern side of the Property, significant glacial retreat of the Marmot glacier and alpine icefields have revealed new exposures that have never seen modern exploration.

The Porter Project contains two shears-hosted silver-rich vein systems: the Silverado and Prosperity-Porter Idaho. The showings are 2.35 km apart, located on opposite sides of Mt. Rainey, overlooking the town of Stewart. The Project is located strategically at the head of the Portland Canal, a deep-water port with year-round, ice-free access. Significant underground workings on multiple levels were used by the historic operators. During the 2022 season, StrikePoint will investigate the feasibility of completing rehabilitation of the workings, most recently used in the 1980s for exploration work, to complete a future underground drilling program.

The initial discovery of silver mineralization on Mt. Rainey occurred in the early 1900s. Prosperity-Porter Idaho veins were the focus of the initial work where mineralization is hosted in six parallel dipping shear zones which have been traced in underground workings for up to 425 metres along strike and 360 metres downdip with widths between 2 and 13 metres. The zones remain open at depth. The deposit was mined between 1929 and 1931 and produced 27,123 tonnes with recovered grades of 2,542 g/t silver (73.8 oz/ton) and 1 g/t gold (yielding approximately 2.2 million ounces of silver). Direct shipping ore was transported to the port at Stewart via aerial tramway.

Willoughby Gold-Silver Property

Strikepoint’s 2022 drilling season will commence at the Willoughby gold-silver Property with 1,400 metres in 6-8 holes. Objectives for the Willoughby exploration program include:

Drill northern and southern extensions to the 600 metre long trend of mineralized zones along the Willoughby nunatak

Exploratory drilling to discover new mineralization to the west of the Willoughby nunatak trend

Willoughby occurs along the eastern margin of the Cambria Icefield, approximately seven kilometres east of the advanced-stage Red Mountain Deposit owned by Ascot Resources. Upper Triassic Stuhini rocks and Lower Jurassic Hazelton volcano-sedimentary rocks underlay the property, subsequently intruded by an early Jurassic-aged hornblende-feldspar porphyry, potentially comagmatic with the Goldslide Intrusive suite at the nearby Red Mountain deposit. Intrusive-related mineralized zones consist of primary pyrite with lesser pyrrhotite, sphalerite, galena, chalcopyrite and native gold. Eight gold and silver mineralized zones have been identified to date over a one-kilometre strike-length mineralized trend.

Qualified Person

The Qualified Person for this news release for National Instrument 43-101 is Andrew Hamilton, P. Geo, technical advisor to StrikePoint. He has read and approved the scientific and technical information that forms the basis for the disclosure contained in this news release.

About StrikePoint

StrikePoint Gold is a gold exploration company focused on building high-grade precious metals resources in Canada. The company controls two advanced-stage exploration assets in BC’s Golden Triangle. The past-producing high-grade silver Porter Project and the high-grade gold property Willoughby, adjacent to Ascot Gold’s Red Mountain development project. The company also owns a portfolio of gold properties in the Yukon.

ON BEHALF OF THE BOARD OF DIRECTORS OF STRIKEPOINT GOLD INC.

“Shawn Khunkhun”

Shawn Khunkhun Chief Executive Officer and Director

Statements in this release that are forward-looking statements are subject to various risks and uncertainties concerning the specific factors disclosed under the heading “Risk Factors” and elsewhere in the company’s filings with Canadian securities regulators. Such information contained herein represents management’s best judgment as of the date hereof based on information currently available. The company does not assume any obligation to update any forward-looking statements, save and except as may be required by applicable securities laws.

Neither the TSX Venture Exchange nor it’s Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Vancouver, British Columbia–(Newsfile Corp. – June 30, 2022) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX”) is pleased to report that all proposed resolutions were approved at the Company’s Annual General Meeting of shareholders held on June 30, 2022, in Vancouver, British Columbia (the “Meeting“). The number of directors was set at 6 and all director nominees, as listed in the Management Information Circular dated May 19, 2022 (the “Information Circular”), were elected as directors of the Company at the Meeting to serve for a one-year term and hold office until the next annual meeting of shareholders. According to the proxy votes received from shareholders, the results were as follows:

Director

Votes FOR

Votes WITHHELD

Brian E. Bayley

96.68%

3.32%

David M. Cole

99.25%

0.75%

Sunny Lowe

98.98%

1.02%

Henrik Lundin

99.31%

0.69%

Larry M. Okada

96.45%

3.55%

Michael D. Winn

99.26%

0.74%

Shareholders voted 99.11% in favour of setting the number of directors at six, 99.29% in favour of appointing Davidson & Company LLP, Chartered Accountants as auditors, and 92.09% in favour of approving and ratifying the Company’s Stock Option Plan.

Voting results for all resolutions noted above are reported in the Report on Voting Results as filed under the Company’s SEDAR profile on June 30, 2022.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”, and also trade on the Frankfurt exchange under the symbol “6E9”. Please see www.EMXroyalty.com for more information.https://embed.fireplace.yahoo.com/embed?ctrl=Monalixa&m_id=monalixa&m_mode=document&site=sports&os=android&pageContext=%257B%2522ctopid%2522%253A%25221542500%253B1577000%2522%252C%2522hashtag%2522%253A%25221542500%253B1577000%2522%252C%2522wiki_topics%2522%253A%2522Annual_general_meeting%253BCompany%253BVancouver%253BNYSE_American%253BTSX_Venture_Exchange%253BChartered_accountant%2522%252C%2522lmsid%2522%253A%2522a0V0W00000HOPDcUAP%2522%252C%2522revsp%2522%253A%2522newsfile_64%2522%252C%2522lpstaid%2522%253A%2522f7514462-52d7-3a71-aedf-024feb72969f%2522%252C%2522pageContentType%2522%253A%2522story%2522%257D

Whoa! Joining us for an action packed interview is the legendary Bob Moriarty the founder of http://www.321gold.com/, as we will cover a lot of ground in this interview! Topics ranging from Market Conditions, Bitcoin, the Colorado River, Junior Mining Companies, and Precious Metals. This is an absolute must watch!