I’m Maurice Jackson, the founder of Proven and Probable. We specialize in identifying under valued stocks that have a massive potential upside. Today we are highlighting what we believe to be the best silver proposition for your portfolio nestled in the bottom of the Golden Triangle located in British Columbia, which has seen over $5B in M&A since 2018!

We have been buyers of this stock 4 years and counting. Dolly Varden Silver has begin the first in a series of press release announcing the results from their 2024 Drill Program of 25,000 Meters. Find out why Eric Sprott, Rick Rule, Hecla Mining, Fury Gold Mines, Fidelity Investments, Sprott, Sprott USA, Delbrook, and High-Net-Worth investors, with a 7% float! Watch now!

Dolly Varden Silver Corporation is a mineral exploration company focused on advancing its 100% held Kitsault Valley Project located in the Golden Triangle of British Columbia, Canada, 25kms by road to deep tide water.

The 163 sq. km. project hosts the high-grade silver and gold resources of Dolly Varden and Homestake Ridge along with the past producing Dolly Varden and Torbrit silver mines. It is considered to be prospective for hosting further precious metal deposits, being on the same structural and stratigraphic belts that host numerous other, on-trend, high-grade deposits, such as Eskay Creek and Brucejack. The project also contains the Big Bulk property which is prospective for porphyry and skarn style copper and gold mineralization, similar to other such deposits in the region (Red Mountain, KSM, Red Chris).

The Company’s common shares are listed and traded on the TSX.V under the symbol DV and on the OTCQX system under the symbol DOLLF.

WEBSITE: https://provenandprobable.com/ 🥇🥈Get Your Online Gold/ Silver Here 🥇🥈 Call Me Directly at 855.505.1900 or Email: Maurice@MilesFranklin.com

Ottawa, Ontario–(Newsfile Corp. – August 15, 2023) – Gold79 Mines Ltd. (TSXV: AUU) (OTCQB: AUSVF) (“Gold79” or the “Company”) announces that it has issued 2,062,548 common shares of the Company in connection with a US$48,000 ($63,283) share payment due under the option agreement covering a portion of the Company’s landholdings for the Gold Chain project in Arizona. The common shares issued have a statutory hold period until December 15, 2023.

About Gold79 Mines Ltd.

Gold79 Mines Ltd. is a TSX Venture listed company focused on building ounces in the Southwest USA. Gold79 holds 100% earn-in option to purchase agreements on three gold projects: the Jefferson Canyon Gold Project and the Tip Top Gold Project both located in Nevada, USA, and, the Gold Chain Project located in Arizona, USA. In addition, Gold79 holds a 32.3% interest in the Greyhound Project, Nunavut, Canada under JV by Agnico Eagle Mines Limited.

For further information regarding this press release contact:

This press release may contain forward looking statements that are made as of the date hereof and are based on current expectations, forecasts and assumptions which involve risks and uncertainties associated with our business including the uncertainty as to whether further exploration will result in the target(s) being delineated as a mineral resource, capital expenditures, operating costs, mineral resources, recovery rates, grades and prices, estimated goals, expansion and growth of the business and operations, plans and references to the Company’s future successes with its business and the economic environment in which the business operates. All such statements are made pursuant to the ‘safe harbour’ provisions of, and are intended to be forward-looking statements under, applicable Canadian securities legislation. Any statements contained herein that are statements of historical facts may be deemed to be forward-looking statements. By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties. We caution readers of this news release not to place undue reliance on our forward-looking statements as a number of factors could cause actual results or conditions to differ materially from current expectations. Please refer to the risks set forth in the Company’s most recent annual MD&A and the Company’s continuous disclosure documents that can be found on SEDAR at www.sedar.com. Gold79 does not intend, and disclaims any obligation, except as required by law, to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Grizzly Discoveries: TSX-V : GZD | OTCQB : GZDIF | FWB : G6H Grizzly is targeting a number of new and existing high-priority battery metals targets at Robocop (copper, cobalt and silver) along with precious metals – battery metals targets at Greenwood (gold-silver-copper and other based metals). Recent geophysical results have outlined large areas with anomalous geological potential for new discoveries at both projects.

The Best Video on Why and When to Buy and Sell Physical Precious Metals:

I’m a licensed broker for Miles Franklin Precious Metals Investments, The Only Online Dealer that is Licensed and Bonded Period! Where we provide unlimited options to expand your precious metals portfolio, from:

Register Here for the Metallic Minerals Live Webinar: https://bit.ly/3KPXJpn Press Release: https://bit.ly/3ZwEN31 Website: https://mmgsilver.com/ Investor Relations: Chris Ackerman Email: chris.ackerman@metallic-minerals.com Phone: 604-629-7800 ext. 1 Toll Free: 1-888-570-4420

TimeStamp: :47 Introduction to Metallic Minerals 1:18 On-Site to the La Plata Project/Mineral Resource Overview 3:31 Highlight from Press Release 6:00 Next Steps on the La Plata 7:13 Updated Resource 2023? 7:48 Latest Updates on the Keno Silver Project 12:13 MMG Partners with Discovery Channel – Parker Schnabel – Gold Rush 15:00 Will MMG be on the Show? 15:12 Alluvial Project Updates 17:00 Live Webinar (https://bit.ly/3KPXJpn) 18:24 MMG Capital Structure 19:09 Message to Shareholders

Metallic Minerals Corp. (TSX-V: MMG / US OTC: MMNGF) is a growth stage exploration company focused on the acquisition and development of high-grade silver and gold projects within underexplored districts proven to produce top-tier assets. Our objective is to create value through a disciplined, systematic approach to exploration, reducing investment risk and maximizing probability of long-term success. Our core Keno Silver Project is located in the historic Keno Hill Silver District of Canada’s Yukon Territory, a region which has produced over 200 million ounces of silver and currently hosts one of the world’s highest-grade silver resources. The Company’s La Plata silver-gold-copper project is located in the high-grade La Plata district of the prolific Colorado Mineral Belt and our McKay Hill project northeast of Keno Hill is a high-grade historic silver-gold producer. Metallic Minerals is also building a portfolio of gold royalties in the historic Klondike Gold District. Metallic Minerals is led by a team with a track record of discovery and exploration success, including large scale development, permitting and project financing.

Group Ten Metals: (TSX-V: PGE | OTCQB: PGEZF) Website: https://grouptenmetals.com/ Corporate Presentation: https://grouptenmetals.com/investors/presentations/

Granite Creek Copper: (TSX.V: GCX) Website: https://www.gcxcopper.com/ Corporate Presentation: https://www.gcxcopper.com/investors/presentations/

The Best Video on Why and When to Buy and Sell Physical Precious Metals:

I’m a licensed broker for Miles Franklin Precious Metals Investments, The Only Online Dealer that is Licensed and Bonded Period! Where we provide unlimited options to expand your precious metals portfolio, from:

Burlington, Ontario–(Newsfile Corp. – February 15, 2023) – Silver Bullet Mines Corp. (TSXV: SBMI) (OTCQB: SBMCF) (‘SBMI’ or ‘the Company’) announces strong initial assay results from the interception of the upper main vein at the Buckeye Mine near Globe, Arizona.

The vein was intercepted approximately 380 feet from the entrance to the adit. Immediately on contact with the vein, the first significant assays from the vein were 43, 178.6, and 270.6 ounces silver per ton. The samples yielding these results did not include material from the footwall. The samples were selected at random from the mineralized material removed from the vein and then were sent to SBMI’s assay lab for processing.

The Company is now mining along the exposed vein with assay results pending from the face. SBMI has extended the workings to 420 feet from the entrance to the adit, the vein is ten feet wide and eleven feet high, and the footwall is estimated by the field team to be four feet wide.

SBMI has stockpiled in excess of 450 tons of vein material at surface at the Buckeye Mine site, for shipment to the mill. The Company is mining 150 to 200 tons of mineralized material per day, although this rate will vary. The Company believes it has achieved the targetted grade necessary to support processing this material at the Company’s mill and to then pour dore bars or create concentrate. Both the dore bars and the concentrate will saleable product, and the Company does not expect to encounter any significant difficulties in finding buyers for those products.

SBMI is also pleased to announce it has begun to resolve the issues with pouring dore bars from this material. The picture below shows a malformed dore bar from September, 2022.

The Company thanks Dr. Andrew Macdonald, a mineralogist with Harquail School of Earth Sciences at Laurentian University, for his assistance. Initial results from his work indicate the presence of a highly magnetic iron alloy in the mineralized material. The iron alloy smelts at temperatures of over 3000 degrees F, which is above the silver smelting temperature of roughly 1800 degrees F, and therefore it interferes with the silver smelting process. SBMI has confirmed this thesis by using a high intensity magnet to pull the iron alloy from the concentrate prior to smelting. The dore bar below, poured in February, 2023, resulted from concentrate after the iron alloy was removed.

Dore bar poured after the iron alloy was removed; Feb 2023

As a result, the Company intends to permanently install a high intensity magnetic separator in the milling operation to improve the likelihood the Company can smelt silver dore bars. The Company intends to store the magnetic concentrates for future research. Continued research will be needed.

The Company is still awaiting the check assay results from American Assay Labs and Actlabs.

SBMI’s near term goal is to process the higher grade material at the Company’s mill to produce saleable product.

QAQC

All the samples above were collected by SBMI’s field team. Samples were collected and placed in sample bags with their appropriate tag and processed at the Company’s own assay lab. Like any responsible producer, the Company owns its own assay lab and regularly takes samples as part of its production process.

The samples analyzed by SBMI at its facility near Globe, Arizona were processed through the Lab Jaw Crusher, Lab Hammer Mill and Splitter Box into an aliquot. Most of the pulverized aliquot was mixed with a flux and flour combination and melted in a crucible at 1,850 degree Fahrenheit, with the remainder being logged and archived. Upon cooling, the poured melt was in the form of a metal button and slag, following which a bone ash cupel was utilized to eliminate the lead in the button to form a bead. The bead was then weighed, following which a solution of 6 to 1 distilled water to nitric acid was utilized to dissolve the silver in the bead at approximately 175 degrees Fahrenheit. A much more detailed description of the process and a picture of the assay lab can be found at https://www.silverbulletmines.com/qaqcassaylab.

Readers should be aware that the SBMI facilities have been designed for quick production grade control and are not ISO compliant; however, duplicate sampling with other ISO labs has been done on past samples with good correlation.

Mr. Robert G. Komarechka, P.Geo., an independent consultant, has reviewed and verified SBMI’s work referred to herein, and is the Qualified Person for this release.

For further information, please contact:

John Carter Silver Bullet Mines Corp., CEO cartera@sympatico.ca +1 (905) 302-3843

Peter M. Clausi Silver Bullet Mines Corp., VP Capital Markets pclausi@brantcapital.ca +1 (416) 890-1232

Cautionary and Forward-Looking Statements

This news release contains certain statements that constitute forward-looking statements as they relate to SBMI and its subsidiaries. Forward-looking statements are not historical facts but represent management’s current expectation of future events, and can be identified by words such as “believe”, “expects”, “will”, “intends”, “plans”, “projects”, “anticipates”, “estimates”, “continues” and similar expressions. Although management believes that the expectations represented in such forward-looking statements are reasonable, there can be no assurance that they will prove to be correct.

By their nature, forward-looking statements include assumptions, and are subject to inherent risks and uncertainties that could cause actual future results, conditions, actions or events to differ materially from those in the forward-looking statements. If and when forward-looking statements are set out in this new release, SBMI will also set out the material risk factors or assumptions used to develop the forward-looking statements. Except as expressly required by applicable securities laws, SBMI assumes no obligation to update or revise any forward-looking statements. The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: the impact of SARS CoV-2 or any other global virus; reliance on key personnel; the thoroughness of its QA/QA procedures; the continuity of the global supply chain for materials for SBMI to use in the production and processing of mineralized material; the presence of mineable economic mineralized material; shareholder and regulatory approvals; activities and attitudes of communities local to the location of the SBMI’s properties; risks of future legal proceedings; income tax matters; fires, floods and other natural phenomena; the rate of inflation; availability and terms of financing; distribution of securities; commodities pricing; currency movements, especially as between the USD and CDN; effect of market interest rates on price of securities; and, potential dilution. SARS CoV-2 and other potential global pathogens create risks that at this time are immeasurable and impossible to define.

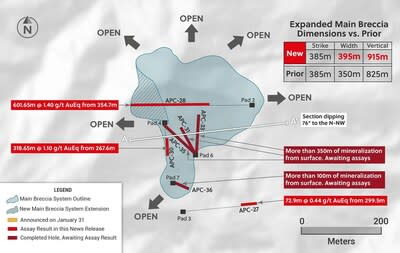

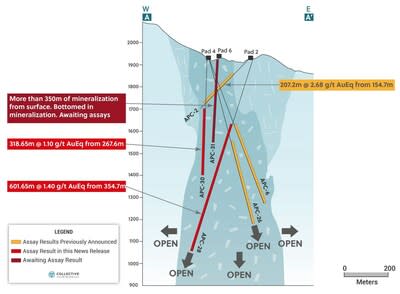

Step-out drill hole APC-28, which was drilled to the west from the eastern side of the Main Breccia system at Apollo cut the longest intercept to date as follows:

As a result of APC-28, the maximum width and vertical dimensions of the Main Breccia system have increased to 395 metres (previously 350 metres) and 915 metres (previously 825 metres), respectively.

Drill hole APC-28 bottomed while still in mineralization indicating that the Main Breccia system remains open for expansion to the west and at depth (as well as to the east and north based on previously announced assay results).

Hole APC-30 was drilled southwards on the western side of the deposit and intercepted the Main Breccia system over a broad interval as follows:

Four holes have now been completed into the Main Breccia system as part of the 2023 Phase II drill program at the Guayabales project. All four holes appear to have intercepted the Main Breccia system with mineralization beginning from surface. Assay results for these holes are expected in the near term.

Ari Sussman, Executive Chairman commented: “The Main Breccia system at Apollo continues to yield positive surprises. The Company drilled three long holes in 2022, APC-17, APC-22 and APC-28, with each hole expanding the size of the deposit and bottoming while still in mineralization. In addition, 2023 drilling is off to an excellent start with the initial four holes testing the Main Breccia system all intersecting mineralization beginning at surface. Our aim for 2023 is to define the newly discovered high-grade and near surface mineralization while continuing to be aggressive with expansion drilling. Without question, we have discovered a large copper-silver-gold deposit in a mining friendly jurisdiction of Colombia which will play a vital role in the country’s aggressive decarbonization goals.”

TORONTO, Feb. 15, 2023 /CNW/ – Collective Mining Ltd. (TSXV: CNL) (OTCQX: CNLMF) (“Collective” or the “Company”) is pleased to announce assay results from a further three holes drilled into the Main Breccia system at the Apollo target (“Apollo”), which is part of the Guayabales project located in Caldas, Colombia. The Main Breccia is a high-grade, bulk tonnage copper-silver-gold porphyry-related system, which owes its excellent metal endowment to multiple phases of mineralization which includes older copper-silver-gold porphyry mineralization and younger, overprinting, low and intermediate sulphidation, precious metal rich sheeted carbonate base metal vein systems.

Details (See Table 1 and Figures 1–5)

Assay results for all thirty-one diamond drill holes from the Phase I drilling program for 2022 have now been announced at Apollo. The Phase II drilling program for 2023 is advancing on schedule with assay results for the first holes expected in the near term. This press release summarizes assay results of the final three diamond drill holes from the Phase I program with results summarized below.

APC-28 was a step-out hole drilled steeply to the west from Pad 2 to a maximum depth of 956.35 metres (915 metres vertical) and was designed to test western and depth extensions to the Main Breccia system. The hole intersected the longest interval drilled to date within the system, commencing at 354.70 metres down hole (335 vertical) and averaging:

601.65 metres @ 1.4 g/t gold equivalent and including internal intervals of:

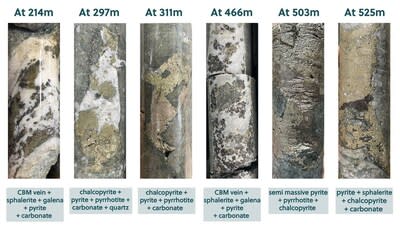

The mineralized angular breccia of this intercept represents the largest accumulation of metal returned to date within the Main Breccia system and contains a sulphide matrix which includes 0.5% up to 2.5% chalcopyrite and between 1% and 3% pyrite plus some pyrrhotite. The breccia has been overprinted by zones of carbonate and base metal (sphalerite and galena) veins, which yield the higher gold equivalent intervals. APC-28 stopped in mineralized breccia due to rig constraints. This hole has extended the main breccia westwards by 115 metres and is the deepest intercept drilled to date outlining continuity of mineralized breccia to a vertical depth of approximately 915 metres below surface. APC-28 also represents the westernmost hole drilled into the Main Breccia system and demonstrates that the mineralization is thickening with depth and has an inverted funnel morphology as outlined in Figure 2 below. This western area of the deposit remains open for expansion as the hole stopped in strong mineralization.

As a result of drill hole APC-28, the overall volume of rock in which the Main Breccia system is located has grown in width to 395 metres (from 350 metres) and a vertical dimension of 915 metres (from 825 metres). The strike of the system remains the same at 385 metres.

APC-30 was drilled southwards from Pad 4 to a total length of 589 metres downhole and intersected mineralized breccia from 267.60 metres downhole (240 metres vertical), averaging:

318.85 metres @ 1.10 g/t gold equivalent and including internal intervals of:

Gold, silver and copper mineralization relates to sulphides hosted within the angular breccia matrix with average concentrations of pyrite (2%) and chalcopyrite (0.5%). An upper zone of 60.8 metres bearing 2% to 3% chalcopyrite was intercepted at the beginning of the mineralized interval and a sheeted and overprinting sphalerite rich CBM vein zone of 81.4 metres was encountered from 472.3 metres downhole.

Reconnaissance hole APC-27 was drilled due east away from the Main Breccia system to test outcropping mineralization at surface. From 300.40 metres downhole (210 metres vertical depth) the Company intersected a new zone of continuous low-grade mineralization with assay results as follows:

Core logging of the breccia system at Apollo by the Company’s geologists has identified that the crackle breccia as seen in this newly discovered zone, is typically found both above and on the periphery of the more intensely mineralized angular breccia phase. As a result of this assessment, the Company may have drilled over top of an angular breccia zone with stronger mineralization than was intercepted in APC-27. Further exploratory drilling will be undertaken in this area.

The Company’s Phase II 2023 program is well underway with three rigs focused on drilling near surface, high grade mineralization below mineralized outcrops in the southern and central areas of the Main Breccia system from newly constructed pads 6 and 7. To date, four shallow holes have been completed and confirm continuous mineralized angular breccia from surface. Three of these holes were drilled from Pad 6 and were terminated while still in strong mineralization. The fourth hole from Pad 7 appears to have drilled out the east side of the system indicating a more vertical orientation to the system that was previously modelled. Assay results are expected in the near term.

The Apollo target area, as defined to date by surface mapping, rock sampling and copper and molybdenum soil geochemistry, covers a 1,000 metres X 1,200 metres area. The Apollo target area hosts the Company’s Main Breccia system and multiple additional untested breccia, porphyry and vein targets. The overall Apollo target area also remains open for further expansion.

Table 1: Apollo Target Assays Results for Holes APC-27, APC-28, and APC-30

Hole ID

From (m)

To (m)

Intercept (m)

Au (g/t)

Ag (g/t)

Cu %

Mo %

AuEq (g/t) *

APC-27

299.50

372.40

72.90

0.30

6

0.02

0.002

0.44

APC-28

286.60

305.55

18.95

1.11

12

0.04

0.001

1.30

And

354.70

956.35

601.65

0.89

24

0.10

0.001

1.40

Incl

354.70

614.65

259.95

1.21

43

0.20

0.001

2.15

713.10

772.80

59.70

2.04

15

0.14

0.04

2.23

863.15

868.80

5.65

2.00

13

0.04

0.001

2.17

APC-30

267.60

586.25

318.65

0.61

19

0.12

0.002

1.10

Incl

267.60

328.40

60.80

0.17

48

0.40

0.002

1.64

472.30

553.70

81.40

1.95

18

0.04

0.002

2.22

*AuEq (g/t) is calculated as follows: (Au (g/t) x 0.95) + (Ag g/t x 0.016 x 0.95) + (Cu (%) x 1.83 x 0.95)+ (Mo (%)*9.14 x 0.95) and CuEq (%) is calculated as follows: (Cu (%) x 0.95) + (Au (g/t) x 0.51 x 0.95) + (Ag (g/t) x 0.01 x 0.95)+ (Mo(%)x 3.75 x 0.95) utilizing metal prices of Cu – US$4.00/lb, Ag – $24/oz Mo US$20.00/lb and Au – US$1,500/oz and recovery rates of 95% for Au, Ag, Mo and Cu. Recovery rate assumptions are speculative as no metallurgical work has been completed to date.

** A 0.2 g/t AuEq cut-off grade was employed with no more than 15% internal dilution. True widths are unknown, and grades are uncut.

Figure 1: Plan View of the Main Breccia System at Apollo Highlighting Drill Holes APC-27, APC-28, APC-30 and Visual Results for APC-31, APC-33, APC-35 and APC-36 (CNW Group/Collective Mining Ltd.)

Figure 2: East-West Cross Section Highlighting APC-28, ACP-30, and Visual Results for APC-31 (CNW Group/Collective Mining Ltd.)

Figure 3: Plan View of the Guayabales Project Highlighting the Apollo Target (CNW Group/Collective Mining Ltd.)

To see our latest corporate presentation and related information, please visit www.collectivemining.com

Founded by the team that developed and sold Continental Gold Inc. to Zijin Mining for approximately $2 billion in enterprise value, Collective Mining is a copper, silver and gold exploration company based in Canada, with projects in Caldas, Colombia. The Company has options to acquire 100% interests in two projects located directly within an established mining camp with ten fully permitted and operating mines.

The Company’s flagship project, Guayabales, is anchored by the Apollo target, which hosts the large-scale, bulk-tonnage and high-grade copper, silver, and gold Main Breccia system. The Company’s near-term objective is to continue with expansion drilling of the Main Breccia system while increasing confidence in the highest-grade portions of the system.

Management, insiders and close family and friends own nearly 52% of the outstanding shares of the Company and as a result, are fully aligned with shareholders. The Company is listed on the TSXV under the trading symbol “CNL” and on the OTCQX under the trading symbol “CNLMF”.

Qualified Person (QP) and NI43-101 Disclosure

David J Reading is the designated Qualified Person for this news release within the meaning of National Instrument 43-101 (“NI 43-101”) and has reviewed and verified that the technical information contained herein is accurate and approves of the written disclosure of same. Mr. Reading has an MSc in Economic Geology and is a Fellow of the Institute of Materials, Minerals and Mining and of the Society of Economic Geology (SEG).

Technical Information

Rock and core samples have been prepared and analyzed at SGS laboratory facilities in Medellin, Colombia and Lima, Peru. Blanks, duplicates, and certified reference standards are inserted into the sample stream to monitor laboratory performance. Crush rejects and pulps are kept and stored in a secured storage facility for future assay verification. No capping has been applied to sample composites. The Company utilizes a rigorous, industry-standard QA/QC program.

Information Contact:

Follow Executive Chairman Ari Sussman (@Ariski) and Collective Mining (@CollectiveMini1) on Twitter

FORWARD-LOOKING STATEMENTS

This news release contains certain forward-looking statements, including, but not limited to, statements about the drill programs, including timing of results, and Collective’s future and intentions. Wherever possible, words such as “may”, “will”, “should”, “could”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict” or “potential” or the negative or other variations of these words, or similar words or phrases, have been used to identify these forward-looking statements. These statements reflect management’s current beliefs and are based on information currently available to management as at the date hereof.

Forward-looking statements involve significant risk, uncertainties, and assumptions. Many factors could cause actual results, performance, or achievements to differ materially from the results discussed or implied in the forward-looking statements. These factors should be considered carefully, and readers should not place undue reliance on the forward-looking statements. Although the forward-looking statements contained in this news release are based upon what management believes to be reasonable assumptions, Collective cannot assure readers that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this news release, and Collective assumes no obligation to update or revise them to reflect new events or circumstances, except as required by law.

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this news release.

The Best Video on Why and When to Buy and Sell Physical Precious Metals:

I’m a licensed broker for Miles Franklin Precious Metals Investments, The Only Online Dealer that is Licensed and Bonded Period! Where we provide unlimited options to expand your precious metals portfolio, from:

Silver ETFs** (Total Known Holdings ETSITOTL Index Bloomberg)

760.17

749.00

11.18

1.49%

1.49%

First real uptick since summer selling

Gold ETFs** (Total Known Holdings ETFGTOTL Index Bloomberg)

93.17

93.75

(0.58)

(0.62)%

(0.62)%

Last positive month was April 2022

Source: Bloomberg and Sprott Asset Management LP. Data as of January 31, 2023. *Mo % Chg and YTD % Chg for this Index are calculated as the difference between the month end’s yield and the previous period end’s yield, instead of the percentage change. BPS stands for basis points. **ETF holdings are measured by Bloomberg Indices; the ETFGTOTL is the Bloomberg Total Known ETF Holdings of Gold Index; the ETSITOTL is the Bloomberg Total Known ETF Holdings of Silver Index.

January Review

Gold had another strong month and the best start to a year since 2015 as spot gold rose $104.34 (or 5.72%) to close January at $1,928.36. While the gold price was supported by the decline in the U.S. dollar (USD) and real yields in January, the magnitude and persistence of the bid for gold were high. Gold bullion trading desks have confirmed this strong interest is a continuation of flow demand from China since early November 2022, and the estimated tonnages bought would align with the most significant numbers since 2017. Price action and trading desk anecdotes denote large buying from China’s “official sector” (possibly any combination of People’s Bank of China, central bank-related entities or state banks) for undisclosed reasons.

January was a solid month for risk assets as investment funds were underexposed for a positive, right-tail8 outcome. The significant left-tail risks of 2022 quickly faded or reversed as we headed toward the new year. In the U.S., fears of hyperinflation and additional Federal Reserve (“Fed”) rate hikes ended abruptly as the Fed signaled it would slow its rate hikes just as inflation data finally moderated. In Europe, a far warmer-than-expected winter prevailed, allowing the EU to dodge the worst of an energy-spiking-induced hard landing and associated stress events. After years of a strict zero-COVID policy, China quickly reversed to a full re-opening, instantly giving the world an unexpected growth shock. With all three major economic regions experiencing a sudden reversal from left-tail (negative) to right-tail (positive) outcomes, massive forced buying was triggered.Gold has outperformed U.S. Treasuries over the past two decades despite the bond market having the advantages of a dovish accommodative Fed.

Furthermore, with the pause in Fed rate hikes in sight, both the USD and interest rates declined sharply, easing financial conditions and paving the way for a rebound in many financial assets. Whether this rally is the beginning of the consensus-desired soft landing or yet another bear market rally remains to be seen. We expect that macro volatility will likely remain high in the months ahead.

Gold Bullion Update

Gold bullion since the autumn lows, based on a three-month rate of change, had the most significant increase since 2011. Since the lows, the gold price has broken through technical resistance levels and Fibonacci retracement levels9 with remarkable ease, reinforcing the evidence that the buyer(s) are not likely financial market types. From gold’s early November lows of approximately $1,625 to $1,775, the price action has the look and feel of short covering in the face of an aggressive buyer. But since gold has reached the $1,775 level, the narrow up-channel and low bid-ask dispersion indicate a persistent large bid in gold that is not concerned with market-related overbought conditions. Lastly, the weekly Relative Strength Index (RSI)10 put in a positive divergence during the autumn lows and has broken above the RSI downtrend line (lower panel of Figure 1).

Figure 1. Gold Bullion Rally with Technical Strength

Source: Bloomberg. Data as of 1/31/2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

Gold Investment Positioning Remains Low

Despite the rise in gold, the long gold CFTC(Commodity Futures Trading Commission) net non-commercial positions and ETF holdings remain muted, like a deer caught in a headlight (Figure 2). Gold held in ETFs (mainly retail and smaller funds) remain near +2.5-year lows and has not shown any buying indication yet. CFTC non-commercial long gold positioning, too, remains near the low end of its 10-year range. Neither of these two sources of investment “longs” is likely to sell off further as they are more trend-following than leading. The last source of investment flows, short positions, are even less likely to add to selling flows. Firstly, there is no overriding primary bearish macro driver (interest rate hikes are near the end, and the USD is weakening); secondly, shorting into massive buying is outright dangerous. The combined CFTC gold longs plus ETF gold holdings are now at their -2 standard deviation lows (lower panel, Figure 2) with macro drivers positive and massive buying from China and central banks. The risk from long positioning remains skewed to increasing longs, not divestment.

Figure 2. Gold Investment Demand Remains Muted

Source: Bloomberg. Data as of 1/31/2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

U.S. Dollar Strength and U.S. Treasury Liquidity Functioning

The US Dollar Index (DXY) reached the upper end of its 16-year-long uptrend and has now fallen at a remarkable pace last seen in the volatile years of 2008 to 2010. The 3-month rate of change of DXY has recorded its second sharpest decline in the past 20 years. This dramatic fall in the USD has also eased financial conditions, creating a powerful tailwind for gold and other risk assets. Typically, policy coordination comes to mind when currencies sharply reverse from levels detrimental to market functioning quickly, with such high correlations. Unfortunately, if policymakers have decided on a coordinated USD strength reduction policy, we won’t know until much later when it becomes evident in hindsight.

The Bloomberg US Government Securities Liquidity Index (a measure of liquidity condition for U.S. Treasuries) surpassed the crisis levels of March 2020, the last time the Fed was forced to intervene to restore market functioning with interest rate cuts, liquidity injections, swap facilities, etc. Generally, a strong USD reduces systematic market liquidity, and Figure 3 highlights this relationship. The U.S. Treasury Market is the world’s largest and most liquid market. If it were to cease functioning properly, the spillover effects could be catastrophic in an overleveraged financial system under the wrong conditions. We would expect the days of runaway USD strength will not be allowed due to liquidity functioning alone.

Figure 3. U.S. Dollar Index and U.S. Treasury Liquidity Index

Source: Bloomberg. Data as of 1/31/2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

Foreign Selling of U.S. Treasuries is Accelerating

Foreign holdings of U.S. Treasuries as a percentage of total holdings peaked in 2013, a decade ago. Most of this time, the Fed provided QE (quantitative easing) programs, negating the need for foreign funding of Treasuries. In Figure 4, we highlight foreign ownership of U.S. Treasuries and the rapidly decreasing percentage of foreign ownership of U.S. Treasuries. In March 2022, foreign holders saw notable selling (~$516 billion). There were several reasons, including 1) the Fed ending its latest QE program; 2) geopolitics (the Russia-Ukraine war and intensifying de-globalization; 3) the start of an aggressive string of Fed rate hikes along with tightening by other central banks; 4) USD weaponization had been occurring for several years, but the seizure of Russia’s foreign exchange (FX) reserves was likely the final straw. After these events, U.S. Treasury Liquidity began to deteriorate, even worse than in March 2020. Without liquidity support for U.S. Treasuries, the probability of another QE program (or a variation built around YCC, i.e., yield curve control) within the next few years is no longer remote, even in the face of high inflation.

Figure 4. Foreign Buyers are Dumping U.S. Debt

Source: Bloomberg. Data as of 1/31/2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

China Replacing U.S. Treasuries with Gold?

Since 2008, China has been the largest foreign holder of U.S. Treasuries. Though the peak has been in place since 2013, China has recently accelerated its selling of Treasuries. The reason for China selling U.S. Treasury securities are varied and not disclosed. Still, since the U.S. sanctioned Russia’s FX reserves, China has a tremendous incentive to diversify its foreign exchange reserves. Figure 5 highlights the cumulative change in China’s gold imports and U.S. Treasures since 2018, measured in USD. 2018 was the first year of the U.S.-China trade war. The recent accelerated selling in U.S. Treasuries occurred at the start of the Russia-Ukraine war and in response to sanctions on Russia’s FX reserves. We expect China to continue reducing its U.S. Treasuries holdings as the economic war extends and intensifies, and the risk of future U.S. sanctions on China’s FX reserves remains present.

Since 2018, we estimate that China has sold $310 billion of U.S. Treasuries ($199 billion in 2022 alone) and has imported $230 billion of gold. China is estimated to have the seventh-largest global bond market, with the top six positions held by the U.S. and its allies. The list of the most liquid tradeable currencies has the same size ranking. In terms of market liquidity, safety as outside money and convertibility (sanctions resistant), gold remains a highly desirable asset for China.

Figure 5. China Buys Gold and Sells U.S. Bonds

Source: Bloomberg. Data as of 11/30/2022. Included for illustrative purposes only. Past performance is no guarantee of future results.

Japan Yield Curve Control (YCC) and Selling U.S. Treasuries

The Bank of Japan (BoJ) began yield curve control in 2016 (0.25% cap on its 10-year yield) to achieve an inflation target of 2% and stimulate economic growth by controlling long-term interest rates. By late 2022, the BoJ did “technically” achieve its goals, although not the hoped-for “virtuous growth cycle” outcome. However, the costs were enormous as global yields soared while Japanese government bond (JGB) yields were capped at 0.25% by the BoJ. The yen had fallen in value by 22.5%, driving import cost inflation so high that the Ministry of Finance had to intervene in the currency market to defend the yen, while at the same time, the BoJ continued with YCC weakening the yen. If this makes no sense, then you have read this correctly.

In December 2022, in a surprise move, the BoJ lifted the YCC cap to 0.50% from 0.25%, signaling to the market that the BoJ YCC had likely reached its best-before date. Since then, the yen has strengthened by ~15%, contributing to USD weakness. Capping JGB yields in the second half of 2022 as global yields soared required massive purchases of JGBs via quantitative easing. This 2H 2022 QE event was a monetary stimulus of 76 trillion yen or $550 billion (~14% of GDP, i.e., gross domestic profit). The end of this stimulus is likely to act as a defacto global tightening. Raising the yield cap also removed a global “low-yield anchor” on global rates. Not only is this yield anchor fading, but Japanese institutional investors, one of the world’s largest foreign bond buyers, are returning to JGBs. Year to date as of this writing, U.S. Treasury holdings in Japan have declined ~$220 billion since the start of 2022. For various reasons, the two largest holders of U.S. Treasuries have sold $420 billion, or 17.5% of their combined holdings, in 2022.

Foreign selling of U.S. Treasuries is increasing, and the Fed in quantitative tightening (QT )mode leaves U.S. domestic investors as the primary buyers for U.S. Treasuries. Maintaining U.S. Treasury liquidity is now more critical than ever, and the looming debt ceiling standoff will be the next challenge. For gold, the immediate bullish catalyst is a weaker USD and lower real yields. Rising JGB yields will lead to higher U.S. nominal yields but lower breakeven yields (removal of stimulus weakens growth), resulting in lower real yields.

Figure 6. U.S. Treasuries Held by Japan and China, $Billions

Source: Bloomberg. Data as of 1/31/2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

Gold vs. Bonds, Heresy Anyone?

Thus far in 2023, there have been near-record capital inflows into the bond market after 2022 recorded the worst year for bond returns in 48 years of available data. In Figure 7a, we update the gold bullion to the U.S. Treasury Index ratio, highlighting that gold has outperformed over the past several years since 2016 and even over the past 20 years. The gold-Treasury ratio is testing the upper resistance level, and we expect an eventual break higher. Figure 7b highlights the performance of gold versus U.S. equities and U.S. bonds over the past five and 20 years, with performance and portfolio metrics highlighting how well gold has performed and behaved.

Despite these positive metrics, gold is still not widespread in investment portfolios. In the past five years, gold compared to both equities and bonds, has a better Sharpe ratio (risk-adjusted return), a better Sortino ratio (lower downside volatility) and the lowest market correlation (increased diversification).

Gold has outperformed U.S. Treasuries over the past two decades despite the bond market having the advantages of a dovish accommodative Fed (QE, ZIRP, NIRP)11 with volatility-destroying practices (forward guidance, Fed put). Furthermore, most of the past 20 years were dominated by low inflation, low macro volatility, negative stock-bond correlations, etc., all favoring bond performance. In our 2023 Top 10 Watch List, we highlighted several significant macro changes underway, all pointing to higher inflationary pressures and increasing volatility. If gold outperformed U.S. Treasuries in the past decades, we believe the chances are excellent that it is likely to do so in the next several years.

Figure 7a. Gold to U.S. Treasury Index Ratio: Gold Significantly Outperforming U.S. Treasuries

Source: Bloomberg. Data as of 1/31/2023. Included for illustrative purposes only. Past performance is no guarantee of future results.

Figure 7b. Gold vs. Equities and Bonds: 5 & 20-Year Returns and Metrics

Dec. 2017 to Dec. 2022

5 YR CAGR*

Standard Deviation

Max Drawdown

Sharpe Ratio

Sortino Ratio

Market Correlation

U.S. Stock Market

8.67%

19.06%

-24.94%

0.46

0.68

1.00

Total U.S. Bond Market

0.02%

5.09%

-17.57%

-0.23

-0.29

0.34

Gold

6.86%

13.45%

-18.06%

0.47

0.85

0.16

Dec. 2002 to Dec. 2022

20 YR CAGR*

Standard Deviation

Max Drawdown

Sharpe Ratio

Sortino Ratio

Market Correlation

U.S. Stock Market

9.52%

15.29%

-50.89%

0.59

0.87

1.00

Total U.S. Bond Market

3.06%

3.95%

-17.57%

0.48

0.7

0.12

Gold

8.65%

16.87%

-42.91%

0.51

0.83

0.08

*CAGR refers to compound annual growth rate.

1

Gold bullion is measured by the Bloomberg GOLDS Comdty Spot Price.

2

Silver bullion is measured by Bloomberg Silver (XAG Curncy) U.S. dollar spot rate.

3

The NYSE Arca Gold Miners Index (GDM) is a rules-based index designed to measure the performance of highly capitalized companies in the Gold Mining industry.

4

The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index distributed by Bloomberg Indices.

5

The U.S. Dollar Index (USDX, DXY, DX) is an index (or measure) of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners’ currencies.

6

The S&P 500 or Standard & Poor’s 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies.

7

Any event that is extremely rare, beyond the sixth standard deviation in a normal distribution, is known as a six sigma event.

8

Source: Investopedia. Tail risk is the chance of a gain/loss occurring due to a rare event, as predicted by a probability distribution. Right-tail risks are associated with substantial investment gains, while left-tail risks are associated with unexpected losses.

9

Source: Investopedia. Fibonacci retracement levels are horizontal lines that indicate where support and resistance are likely to occur. They are based on Fibonacci numbers. Each level is associated with a percentage. The percentage is how much of a prior move the price has retraced. The Fibonacci retracement levels are 23.6%, 38.2%, 61.8% and 78.6%. While not officially a Fibonacci ratio, 50% is also used. The indicator is useful because it can be drawn between any two significant price points.

10

Source: Investopedia. The Relative Strength Index (RSI) is a momentum indicator that measures the magnitude of recent price changes to analyze overbought or oversold conditions.

11

QE-ZIRP-NIRP is Fed speak and refers to “quantitative easing”, “zero interest rate policy” and “negative interest rate policy”.

Paul Wong, CFA, Market Strategist Paul has held several roles at Sprott, including Senior Portfolio Manager. He has more than 30 years of investment experience, specializing in investment analysis for natural resources investments. He is a trained geologist and CFA holder. Read Bio

Country* United States Canada Argentina Australia Austria Belgium Brazil China Denmark Finland France Germany India Ireland Italy Japan Netherlands New Zealand Norway South Africa Spain Sweden Switzerland United Kingdom Other

Past performance is no guarantee of future results. You cannot invest directly in an index. Investments, commentary and statements are that of the author and may not be reflective of investments and commentary in other strategies managed by Sprott Asset Management USA, Inc., Sprott Asset Management LP, Sprott Inc., or any other Sprott entity or affiliate. Opinions expressed in this commentary are those of the author and may vary widely from opinions of other Sprott affiliated Portfolio Managers or investment professionals.

This content may not be reproduced in any form, or referred to in any other publication, without acknowledgment that it was produced by Sprott Asset Management LP and a reference to sprott.com. The opinions, estimates and projections (“information”) contained within this content are solely those of Sprott Asset Management and are subject to change without notice. SAM LP makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, SAM LP assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. SAM LP is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Sprott Asset Management LP. These views are not to be considered as investment advice nor should they be considered a recommendation to buy or sell.

The information provided is general in nature and is provided with the understanding that it may not be relied upon as, nor considered to be, the rendering or tax, legal, accounting or professional advice. Readers should consult with their own accountants and/or lawyers for advice on their specific circumstances before taking any action.