ST. LOUIS, Oct. 12, 2023 /PRNewswire/ — On Thursday, October 26, 2023, Peabody (NYSE: BTU) will announce results for the quarter ended September 30, 2023. A conference call with management is scheduled for 10 a.m. CT on Thursday, October 26, 2023.

Instructions for the conference call participation and accessing a replay, as well as other investor data will be available at PeabodyEnergy.com prior to the call.

Participants may also access the call using the following phone numbers:

U.S. Toll Free 1 833 816 1387 Canada Toll Free 1 866 284 3684 International Toll 1 412 317 0480

Peabody (NYSE: BTU) is a leading coal producer, providing essential products for the production of affordable, reliable energy and steel. Our commitment to sustainability underpins everything we do and shapes our strategy for the future. For further information, visit PeabodyEnergy.com.

ST. LOUIS, July 27, 2023 /PRNewswire/ — Peabody (NYSE: BTU) announced today that its Board of Directors has declared a quarterly dividend on its common stock of $0.075 per share, payable on August 30, 2023 to stockholders of record on August 10, 2023.

Peabody is a leading coal producer, providing essential products for the production of affordable, reliable energy and steel. Our commitment to sustainability underpins everything we do and shapes our strategy for the future. For further information, visit PeabodyEnergy.com.

Contact: Karla Kimrey 314.342.7890

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the securities laws. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include words or variation of words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “projects,” “forecasts,” “targets,” “would,” “will,” “should,” “goal,” “could” or “may” or other similar expressions. Forward-looking statements provide management’s current expectations or predictions of future conditions, events or results. All statements that address operating performance, events, or developments that Peabody expects will occur in the future are forward-looking statements. They may include estimates of sales and other operating performance targets, cost savings, capital expenditures, dividends, share repurchases, other expense items, actions relating to strategic initiatives, demand for the company’s products, liquidity, capital structure, market share, industry volume, other financial items, descriptions of management’s plans or objectives for future operations and descriptions of assumptions underlying any of the above. The declaration and payment of future quarterly dividends remains at the discretion of the Board of Directors and will depend on the Company’s financial results, cash flow and cash requirements, future prospects, and other factors deemed relevant by the Board. All forward-looking statements speak only as of the date they are made and reflect Peabody’s good faith beliefs, assumptions and expectations, but they are not guarantees of future performance or events. Furthermore, Peabody disclaims any obligation to publicly update or revise any forward-looking statement, except as required by law. By their nature, forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. Factors that might cause such differences include, but are not limited to, a variety of economic, competitive and regulatory factors, many of which are beyond Peabody’s control, that are described in Peabody’s Annual Report on Form 10-K for the fiscal year ended Dec. 31, 2022 and Quarterly Report on Form 10-Q for the quarter ended March 31, 2023, and other factors that Peabody may describe from time to time in other filings with the SEC. You may get such filings for free at Peabody’s website at www.peabodyenergy.com. You should understand that it is not possible to predict or identify all such factors and, consequently, you should not consider any such list to be a complete set of all potential risks or uncertainties.

In this interview, we sit down with Bob Moriarty to discuss: ‘Moriarty’s First Law of Unintended Consequences‘ We discuss a broad range of topics ranging from the War in Ukraine, the importance of oil (fossil fuels), precious metals, and resource stocks! We also highlight the value thesis of contrarian investing/speculation.

Bob Moriarty is a renown for insights on junior mining and precious metals markets, as well as the common sense. This video is a great way to learn about the resource stocks tips, precious metals, how to analyze and exploit market conditions as a contrarian. Bob Moriarty the founder of 321gold.com visits us for an exclusive, one of a kind, interview to discuss a number of topics ranging from the War in Ukraine, Precious Metals (Bullion investments, and select junior mining companies (exploration stocks) that have his attention. If you are easily offended, this may not be for you. Bob Moriarty is a straight shooter that has the guts to say what others are afraid to say. We hope you enjoy!

A Christmas Treat for Aviation Lovers Bob Moriarty (No Guts, No Glory):https://bit.ly/3jap3mo

WATCH THE VIDEO!!!!

The Best Video on Why and When to Buy and Sell Physical Precious Metals:

I’m a licensed broker for Miles Franklin Precious Metals Investments, The Only Online Dealer that is Licensed and Bonded (Period)! Where we provide unlimited options to expand your precious metals portfolio, from:

Global oil prices could reach a “stratospheric” $380 a barrel if US and European penalties prompt Russia to inflict retaliatory crude-output cuts, JPMorgan Chase & Co. analysts warned.

The Group of Seven nations are hammering out a complicated mechanism to cap the price fetched by Russian oil in a bid to tighten the screws on Vladimir Putin’s war machine in Ukraine. But given Moscow’s robust fiscal position, the nation can afford to slash daily crude production by 5 million barrels without excessively damaging the economy, JPMorgan analysts including Natasha Kaneva wrote in a note to clients.

For much of the rest of the world, however, the results could be disastrous. A 3 million-barrel cut to daily supplies would push benchmark London crude prices to $190, while the worst-case scenario of 5 million could mean “stratospheric” $380 crude, the analysts wrote.

“The most obvious and likely risk with a price cap is that Russia might choose not to participate and instead retaliate by reducing exports,” the analysts wrote. “It is likely that the government could retaliate by cutting output as a way to inflict pain on the West. The tightness of the global oil market is on Russia’s side.”

Integrous- Oil & Gas- Drilling & Exploration- The Answer to Supply-Side Inflation

Crude oil at the highest price since 2008- Inventories and product prices support higher highs

Natural gas is also at a fourteen-year high- Inventories, and European prices support the continuation of a very volatile bull market

The four reasons for higher fossil fuel prices- SPR releases are a temporary band-aid

Drilling and exploration are the answer to supply-side economic woes

XOP outperforming the stock market in 2022- The trend is your best friend

Throughout most of 2021, the US Federal Reserve called the rising inflationary pressures “transitory.” Late last year, increasing consumer and producer price data convinced the central bank that the economic condition was not a temporary event. The Fed told markets it was preparing to shift to a more hawkish approach to monetary policy to address the economy’s demand-side pressures. The artificially low interest rates, liquidity, and government stimulus in 2020 and 2021 planted the inflationary seeds which sprouted during the second half of 2020, throughout 2021, and into early 2022.

In early 2022, the geopolitical landscape threw a curveball at the central bank when Russia invaded Ukraine, launching the first major war in Europe since WW II. Sanctions on Russia and Russian retaliation began to cause even more upside pressure on commodity prices as Russia is a leading producer of energy and other raw materials. China and Russia’s “no-limits” support agreement complicated matters, setting the stage for the invasion.

Crude oil and natural gas prices had already been rising by the end of 2021. The leading benchmark crude oil futures are the Brent and WTI contracts. After falling to a record low below zero in April 2020, nearby WTI crude oil futures at $75.21 per barrel. Brent futures fell to $16 per barrel, the lowest price of this century in April 2020, and closed 2021 at the $77.78 level.

Meanwhile, nearby natural gas futures dropped to $1.44 per MMBtu in June 2020 and were at the $3.73 level on December 31, 2021. The oil and gas futures markets had been rising, making higher lows and higher highs throughout the second half of 2020 and in 2021. In 2022, they took off on the upside, reaching fourteen-year highs.

Increasing inflation and post-pandemic demand created a bull market in crude oil and natural gas that turned into a perfect bullish storm in 2022. The war and a dramatic geopolitical shift made dynamics shift from demand to supply-side concerns. The Fed has few if any tools to deal with supply-side economic events, and the only answer could be increasing supplies, which is a challenge in the current environment.

Just as the Fed mischaracterized inflation as “transitory,” US and European policies addressing climate change have played a role in the ascent of hydrocarbon prices. Since energy prices are inflation’s root cause, exploration and drilling could be the only answer to address the economic condition. Fossil fuels continue to power the world, and the price action is screaming that monetary policy has taken a backseat to the energy debacle.

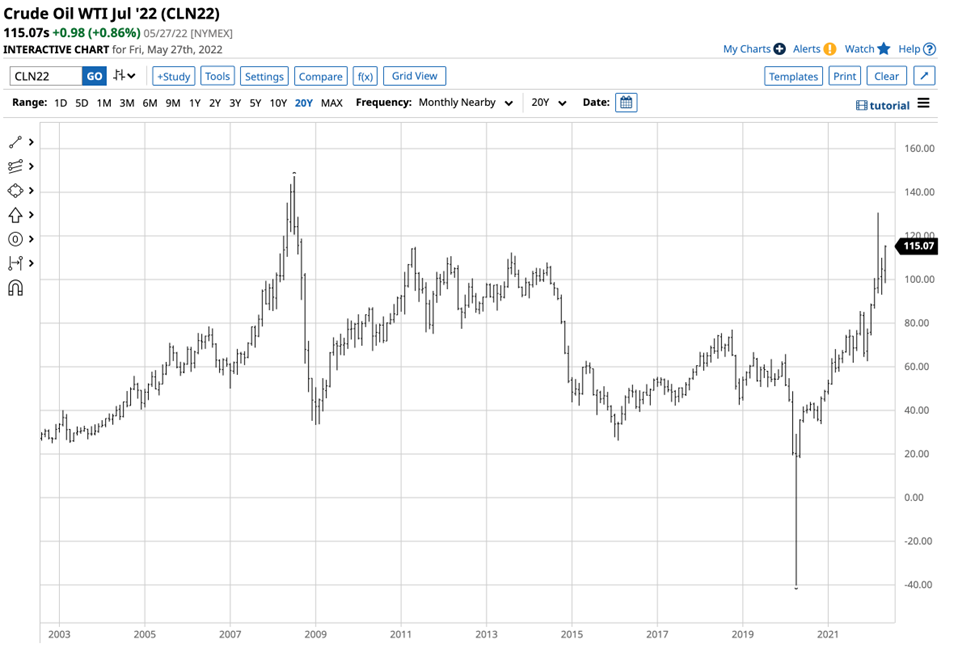

Crude oil at the highest price since 2008- Inventories and product prices support higher highs

Nearby NYMEX WTI futures rose to $130.50 per barrel on March 7 after Russia invaded Ukraine on February 24, and the war escalated.

Source: Barchart

The chart highlights that the WTI futures were sitting at just above the $115 level on May 27. Brent crude oil hit a high of $139.13 in early March.

Source: Barchart

The chart shows the price was at around the $119.43 per barrel level in late May 2022. The all-time 2008 peaks in WTI and Brent were at $147.27 and $147.50.

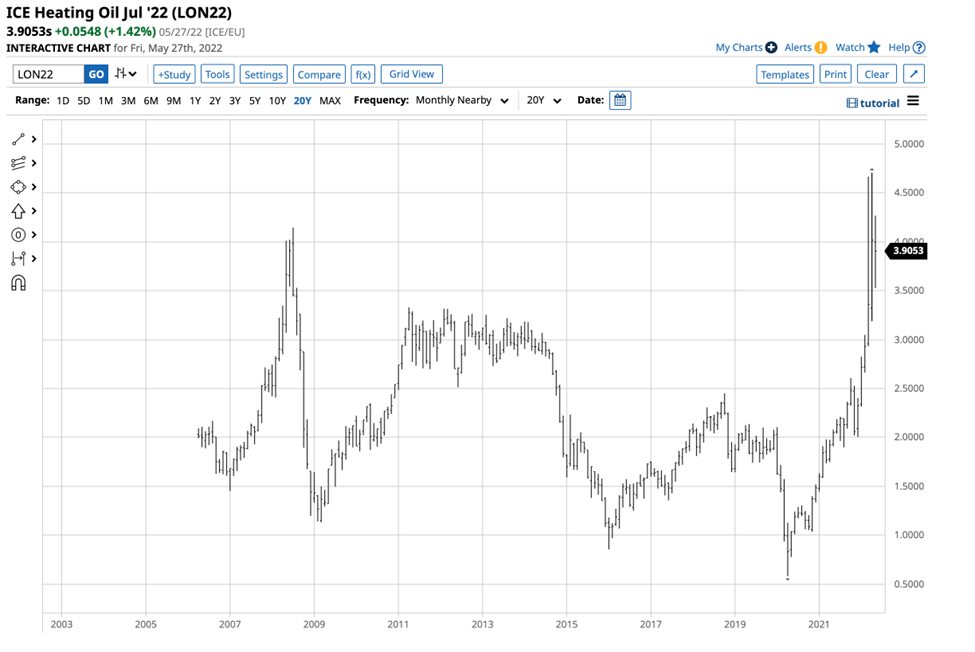

While crude oil missed an all-time high, gasoline and heating oil hit record prices in 2022.

Source: Barchart

The chart shows that gasoline futures prices reached $4.0640 per gallon wholesale in May, an all-time high. July gasoline was sitting at over the $3.90 level on May 27.

Source: CQG

Heating oil is also a proxy for distillates like diesel and jet fuels. The chart shows the spike to a record peak in distillate in April at $4.7072 per gallon wholesale. Heating oil was also over the $3.90 per gallon level on May 27.

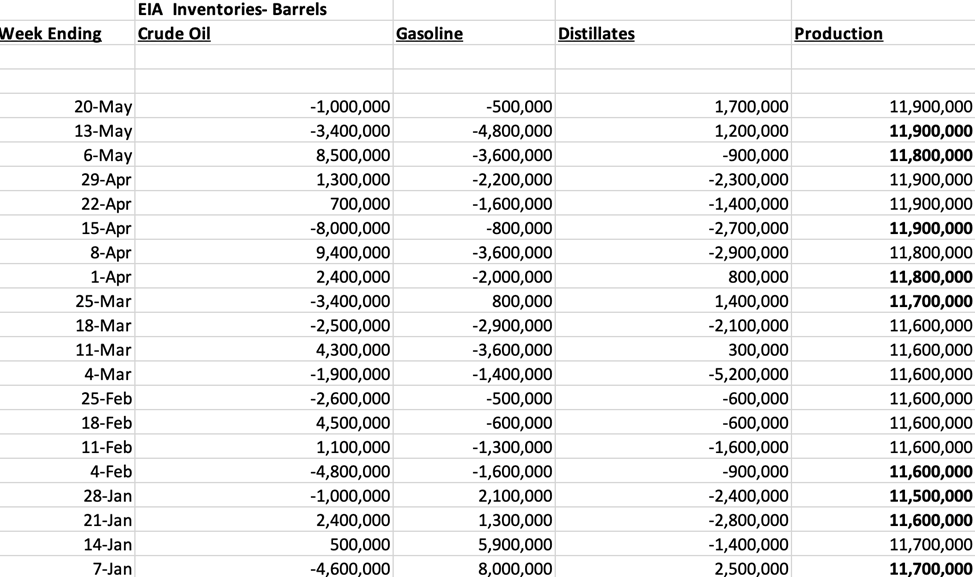

Inventories and US production have supported prices:

Source: US Energy Information Administration

So far, in 2022, US crude oil stockpiles rose by 1.9 million barrels, but the data includes strategic stockpile releases. Meanwhile, gasoline inventories declined by 12.9 million barrels, and distillate stocks fell by 19.9 million barrels from the beginning of 2022 through May 20. Consumers require oil products, and the data supports higher prices. While US daily output rose from 11.7 to 11.9 million barrels per day in 2022, they remain below the March 2020 13.2 mbpd record peak.

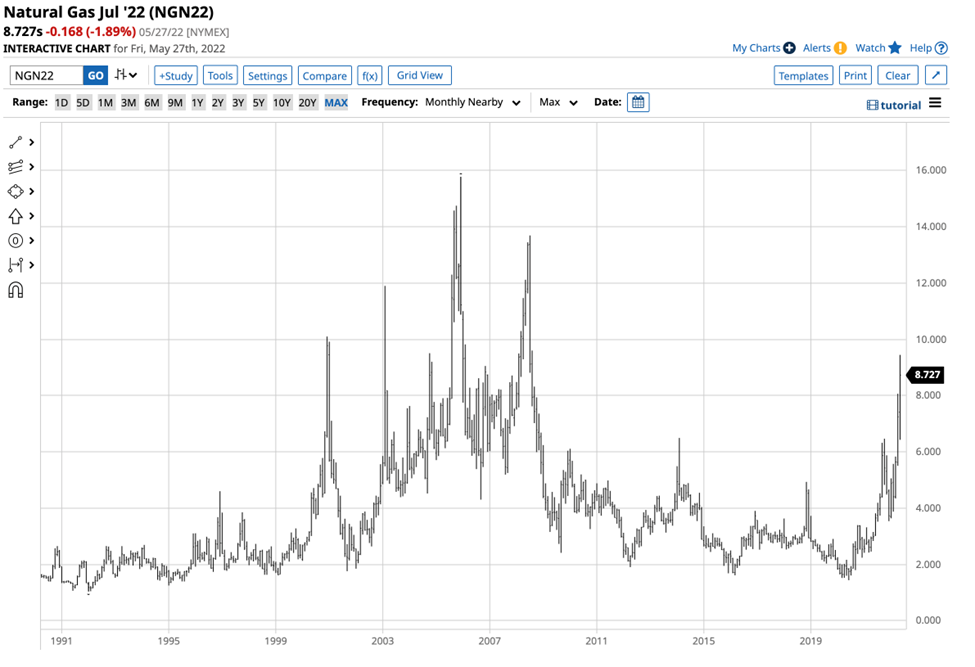

Natural gas is also at a fourteen-year high- Inventories, and European prices support the continuation of a very volatile bull market

NYMEX natural gas futures fell to a twenty-five-year low in June 2020, reaching $1.432 per MMBtu.

Source: CQG

The long-term chart shows that natural gas futures moved over six times higher by May 2022, reaching a high of $9.447 per MMBtu and sitting at over the $8.70 level on May 27.

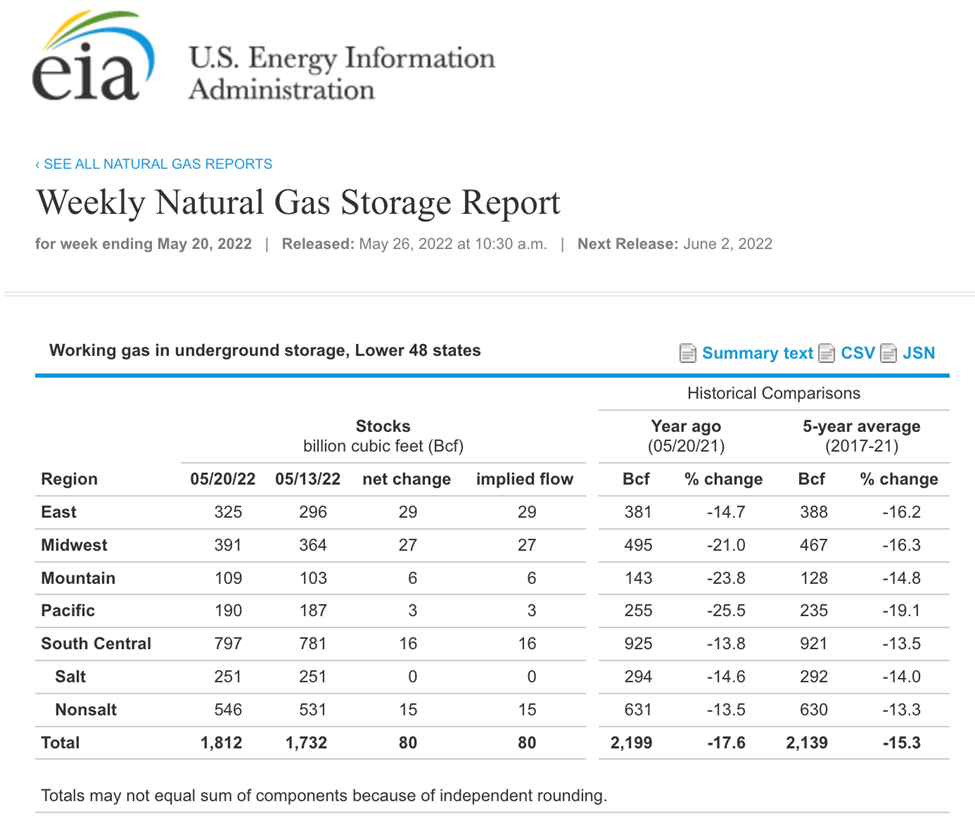

Natural gas inventories are at low levels, with the price at a fourteen-year high.

Source: EIA

At the 1.812 trillion cubic feet level on May 20, natural gas in storage across the US was 17.6% below last year’s level and 15.3% under the five-year average.

Over the past years, natural gas liquefication opened a burgeoning export market for the US energy commodity as it now travels worldwide via ocean vessels. Natural gas’s addressable market expanded far beyond the US pipeline network.

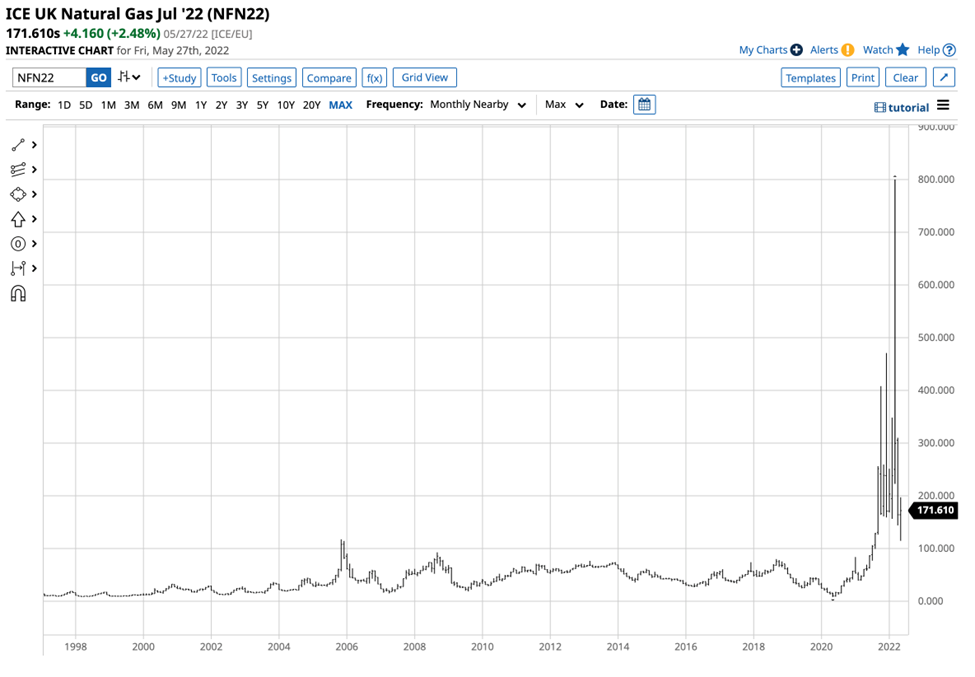

While US natural gas exports have sold LNG to Asian consumers under long-term contracts, the war in Europe and Russian retaliation for sanctions have sent European natural gas prices to record levels.

Source: Barchart

The chart shows that ICE UK natural gas futures rose to the 800 pounds per 1,000 thermals level in March 2022. Before 2021, the all-time high was at the 117 level, and at the 171.61 level on May 27, the price was well above the pre-2021 record peak. Russian natural gas travels by pipeline to European consumers. The Russians have demanded payment in rubles and have cut off “unfriendly” countries that support Ukraine. Moreover, Sweden and Finland’s plans to join NATO only increase Russian export bans, and European consumers are turning to the US for supplies. The bottom line is that

US natural gas has become an international energy market, and the supply shortage is lifting worldwide prices.

In the US, natural gas is heading into the volatile hurricane season. In 2005 and 2008, Hurricanes Katrina and Rita wreaked havoc along the Louisiana coast. The NYMEX futures delivery point is the Henry Hub in Erath, Louisiana, along the Gulf Coast hurricane corridor. Storms in 2008 and 2005 lifted the price to $13.694, and $15.65per MMBtu, respectively. Even if the natural gas market makes it through the annual hurricane season without category four or five storms, the 2022/2023 winter season in worn-torn Europe will likely push prices higher, with $10+ NYMEX futures prices on the horizon.

The four reasons for higher fossil fuel prices- SPR releases are a temporary band-aid

At least four factors favor higher oil and gas prices in late May 2022:

The Biden administration’s green energy initiative favors alternative and renewable fuels while inhibiting fossil fuel production. The US energy policy since early 2021 handed the pricing power to OPEC, the international oil cartel, and Russia. After years of suffering under low prices and lower US demand because of US shale oil and gas production, OPEC+ now controls supplies and owes the US and European consumers no favors. US requests for production increases fell on deaf ears in Riyadh, Moscow, and other production capitals.

The February 4 “no-limits” agreement between China and Russia creates a bifurcation of the world’s nuclear powers, with the US and Europe on the other side. Russia’s invasion of Ukraine could lead to Chinese reunification attempts with Taiwan. Hostilities and geopolitical tensions make hydrocarbons a political tool for the Russians and allied world oil and gas producers.

The crude oil and natural gas prices have been rising despite a COVID-19 lockdown in China. When the Chinese economy reopens, the global energy demand will likely rise, putting more upside pressure on oil and gas prices. Meanwhile, a historic heatwave in India is causing increased energy demand in the world’s second-most populous country. India has not cooperated with the US and Europe with sanctions on Russia.

Even if the US were to shift back to a drill-baby-drill and frack-baby-frack approach to traditional energy production, labor shortages and higher input and equipment prices put upside pressure on production costs. Moreover, the Biden administration has doubled down on its green initiatives, so the potential for production increases remains low.

Instead of increasing production over the past months, President Biden released a historical level of crude oil from the strategic petroleum reserve. Past SPR releases have not weighed on the price in challenging times. Moreover, the US will eventually need to replace its resources, leading to buying in the oil market. The administration released 30 million barrels in early 2022 and has been releasing one million barrels per day from the SPY. The price remains around the $115 per barrel level as the SPR sales have been a short-term, ineffective band-aid. Meanwhile, crack spreads, a real-time demand indicator rose to new all-time highs in May. The level of refining margins are a warning sign that higher crude oil prices are on the horizon.

Drilling and exploration are the answer to supply-side economic woes

The Fed is increasing interest rates and reducing its balance sheet to address the highest inflation in over four decades. The central bank’s toolbox contains monetary policy tools that deal with the economy’s demand-side. In 2020, slashing interest rates and government stimulus encouraged borrowing and spending and inhibited saving.

The Fed now faces supply-side economic factors caused by the war in Ukraine, sanctions, and geopolitical bifurcation. There are few, if any, tools that can deal with the supply-side issues that will continue to fuel inflation. While core inflation data excludes food and energy, food and energy are critical inflationary factors that impact individuals and businesses. Moreover, energy is a crucial cost of goods sold input in all sectors of the economy. Therefore, the only answer to dealing with supply-side inflationary pressures in the current environment is to increase supplies. Just as the Fed woke up from its “transitory” trance, the administration will likely realize that encouraging fossil fuel exploration and drilling is the only route out of the current inflationary spiral. The US is blessed with rich oil reserves in the shale regions, Alaska, and other oil-producing areas. The Marcellus and Utica shale contains quadrillions of cubic feet of natural gas. A hostile Russia and China could cause a reversal of the current path of US energy policy. Rising oil and gas prices will eventually choke all economic growth, and the administration may have no choice but to put climate change initiatives to the side while it deals with the inflationary spiral.

XOP outperforming the stock market in 2022- The trend is your best friend

The war, rising interest rates, a strong US dollar, increasing geopolitical turmoil, and other factors have weighed on the stock market in 2022.

Source: Barchart

The S&P 500 is the most diversified US stock market index. After closing at 4,766.18 on December 31, 2021, the index was 12.8% lower at 4,158.24 on May 27.

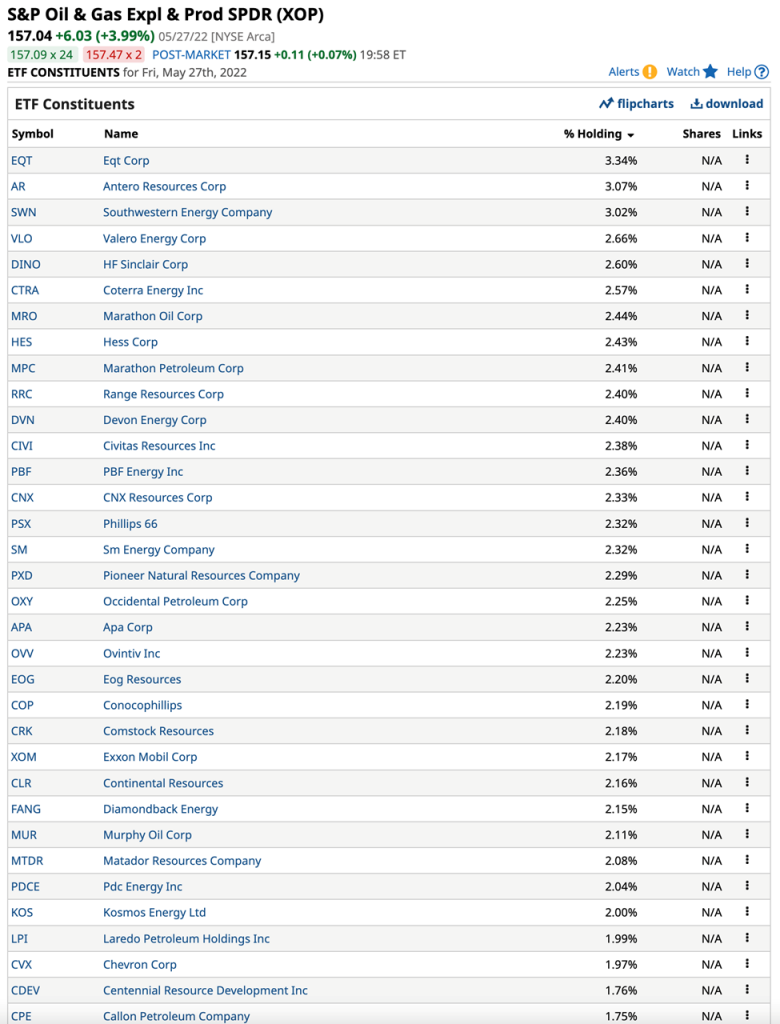

The S&P Oil & Gas Exploration and Production ETF product (XOP) holds many of the top US companies that explore, drill, and produce crude oil and natural gas, including:

While the S&P 500 is 12.8% lower in 2022, the XOP performance has been impressive:

Source: Barchart

The XOP closed at $95.87 at the end of 2021. At the $157.04 level on May 27, the ETF was over 63.8% higher this year.

Existing oil and gas exploration, drilling, and production companies have experienced a profit bonanza in 2022, but they are struggling to meet the growing worldwide hydrocarbon requirements. The bull market in oil and gas opens the door for newcomers in exploration and drilling. Dealing with inflation requires addressing the root cause, energy shortages, and high prices. An epiphany that shifts US energy policy is the path of fighting inflation. The supply-side problems are beyond the Fed’s reach, and SPR releases are only a band-aid on a worldwide gapping ax wound.

Written By: Andrew Hecht, on behalf of Maurice Jackson of Proven and Probable.

Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.

NEWTOWN, PA and VANCOUVER, BC / ACCESSWIRE / August 4, 2021 /Jericho Energy Ventures (TSXV:JEV)(FRA:JLM0)(OTC PINK:JROOF) (“Jericho” or “JEV” or the “Company”) is pleased to announce its wholly owned subsidiary, Hydrogen Technologies (“HT”), has filed for a series of new provisional patents associated with the advancements of its second generation hydrogen boiler with the US Patent and Trademark Office.

On May 26, 2021, JEV announced the launch of HT’s newest Generation 2.0 cleanH2steam Dynamic Combustion Chamber™ (DCC™) Boiler 3000 Series design. The second generation DCC™ Boiler has an improved and streamlined fuel delivery system featuring high precision mass flow meters, increased process monitoring and remote management options. Improvements were also made to the ignitor design providing optimum combustion resulting in higher thermal efficiencies.

The enhanced engineering design was also accompanied by an active procurement strategy which led to metallurgy changes that address the current high cost and long lead time of stainless steel in global supply chains.

There is no pathway to Net Zero targets without a robust, efficient, zero-emission boiler. Currently, 37 percent of the fossil fuels burned by US industry alone is to produce steam. HT’s DCC™ is the only zero-emissions, closed-loop hydrogen boiler, which produces clean process steam without generating any air pollutants or emissions. The DCC™ system is designed to replace existing boilers that burn coal, natural gas, diesel, or fuel oil, which are estimated to account for over 20 percent of all global greenhouse gasses emitted each year.

“Our Hydrogen Technologies team has made significant advances with the DCC™ boiler, leveraging Jericho’s financial and strategic capabilities to drive innovation,” said CEO Brian Williamson. “The DCC™, designed without a smokestack for energy dissipating heat and gasses, is the only hydrogen-based boiler with ZERO greenhouse gas emissions. Our disruptive technology enables meaningful GHG emissions reduction for large users of heat and steam. With the filing of our recent patent application, we are preparing a broader marketing campaign targeting users with large thermal loads worldwide.”

About Jericho Energy Venture

Jericho Energy Ventures (JEV) is focused on advancing the low-carbon energy transition with investments in hydrogen technologies, energy storage, carbon capture and new energy systems. JEV’s wholly owned subsidiary, Hydrogen Technologies, delivers patented, zero-emission boiler technology to the $30 Billion Commercial & Industrial heat and steam industry in addition to its investment in H2U‘s electrocatalyst and low-cost electrolyser platform. JEV also owns and operates producing oil and gas assets in the US Mid-Continent, predominantly in Oklahoma.

This news release contains certain “forward-looking information” within the meaning of applicable Canadian securities legislation and may also contain statements that may constitute “forward-looking statements” within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995. Such forward-looking information and forward-looking statements are not representative of historical facts or information or current condition, but instead represent only Jericho’s beliefs regarding future events, plans or objectives, many of which, by their nature, are inherently uncertain and outside of Jericho’s control. Generally, such forward-looking information or forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or may contain statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “will continue”, “will occur” or “will be achieved”. Although Jericho believes that the assumptions and factors used in preparing, and the expectations contained in, the forward-looking information and statements are reasonable, undue reliance should not be placed on such information and statements, and no assurance or guarantee can be given that such forward-looking information and statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information and statements. Forward-looking information and statements are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those anticipated in the forward-looking information and statements which include, but are not limited to: the effects of and risks associated with the ongoing COVID-19 pandemic, the impact of general economic conditions, industry conditions and current and future commodity prices including sustained low oil prices, significant and ongoing stock market volatility, currency and interest rates, governmental regulation of the oil and gas industry, including environmental regulation; geological, technical and drilling problems; unanticipated operating events; competition for and/or inability to retain drilling rigs and other services; the availability of capital on acceptable terms; the need to obtain required approvals from regulatory authorities; liabilities inherent in oil and gas exploration, development and production operations; and the other factors described in our public filings available at www.sedar.com. Readers are cautioned that this list of risk factors should not be construed as exhaustive.The forward-looking information and forward-looking statements contained in this news release are made as of the date of this news release, and Jericho does not undertake to update any forward-looking information and/or forward-looking statements that are contained or referenced herein, except in accordance with applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

H2U has developed a high throughput screening process for discovering electrocatalysts

Millions of elemental compositions screened and tested daily for their catalytic value

Low-cost catalysts enable the Hydrogen Economy

H2U to develop its own proprietary electrolyser technology

NEWTOWN, PA and VANCOUVER, BC / ACCESSWIRE / July 22, 2021 /Jericho Energy Ventures (TSXV:JEV)(Frankfurt:JLM0)(OTC PINK:JROOF) (“Jericho” or “JEV” or the “Company”) is pleased to announce it has led a Series A financing for H2U Technologies, Inc. (“H2U”), a Company focused on developing its proprietary ultrahigh throughput, AI-driven, electrocatalyst discovery process for electrolyser and fuel cell applications.

Jericho’s USD$1.5 million Co-Lead investment is joined by Dolby Family Ventures, Hess Corporation (NYSE: HES) and Motus Ventures – with a total Series A raise of approximately USD$7 million. Each of the Co-Leads, including Jericho, will have board representation. The Board of H2U will also be joined by independent director, Tom Werner, former CEO (2003-2021) and current Chairman of SunPower (NASDAQ: SPWR).

H2U intends to use this funding to support the start-up and development of its proprietary electrocatalyst discovery process and machinery. H2U will also develop its own PEM electrolyser technology utilizing its proprietary catalysts, breakthrough sub-component innovations and manufacturing processes.

H2U’s low-cost electrolyser is being developed in partnership with Southern California Gas Co. (“SoCalGas”) – the cost target of which is half that of current PEM electrolysers. SoCalGas, who recently announced its commitment to reach Net Zero carbon emissions in its operations and delivery by 2045, will conduct demonstration testing of the new low-cost electrolyser, as well as validation testing on the performance of new non-precious metal catalysts, materials used in small quantities to initiate and accelerate the chemical process of splitting water into hydrogen and oxygen.

Disruptive Solution and Background

H2U is a commercialization of technology, exclusively licensed to H2U by Caltech, developed under a $122 million Joint Center for Artificial Photosynthesis (“JCAP”) program established by the Department of Energy and a group of universities including the California Institute of Technology, University of California, Berkley, Stanford University, UC Irvine, and UC San Diego. The mission of JCAP was to find cost-effective methods to produce fuels using only sunlight, water, and CO2. This program produced over 30 patents to which H2U has the exclusive worldwide IP-rights.

H2U’s disruptive solution to replace precious metal catalysts with cheap, stable, and effective electrocatalysts will be a required step in the adoption of green hydrogen, globally. The resulting electrocatalyst discovery pipeline is an unprecedented, proprietary, end-to-end, ultra-high throughput data-driven process focused on the discovery of new catalysts for hydrogen electrolysis, fuel cells and batteries. The process is capable of preparing, characterizing, and quantifying the catalytic activity of over 1 million compositions per day, which is orders of magnitude beyond the current state-of-the-art. Critically, the Company has already developed, lab tested and has patents pending on two potential catalysts that will be the focal point of commercialization efforts in the near-term.

H2U will initially be led by some of the leading scientists in the field of photo-and-electrocatalysis, many of whom led and directed the JCAP program at the California Institute of Technology including H2U’s Chief Scientific Advisor, Dr. Nathan Lewis (Scientific Director, Principal Investigator for JCAP and Professor of Chemistry at Caltech).

Ryan Breen, Head of Corporate Strategy at JEV, states, “Critical to any pathway towards Net Zero targets will be the low-cost, efficient and stable electrocatalysts developed by H2U for the rapidly growing Hydrogen Economy. H2U’s catalyst discovery process is a distinct advantage over traditional catalyst companies looking to serve the hydrogen market. Driving down the cost of green hydrogen is of vital importance to its adoption and JEV seeks to play a market-leading role in that pursuit. Moreover, we are thrilled to be joined by like-minded investors in recognizing the value of H2U’s proprietary technology and world-class Caltech team.”

Hydrogen Generation and Utilization: Electrolysers, Fuel Cells and Catalysts

The market to produce and utilize green hydrogen as a fuel, feedstock and means of energy storage is slated to reach a total addressable market size of $2.5 trillion per annum by 2050. Today, electrolysers and fuel cells rely on expensive and supply-constrained precious metals for electrocatalysts, particularly, platinum and iridium whose prices have risen 25% and 240%, respectively over the last twelve months.

According to the Renewable Energy Agency (IRENA) and Bloomberg New Energy Finance (BNEF), required electrolyser capacity needs to reach 270GW and 1700GW by 2030 and 2050 respectively to meet global decarbonization targets. The current global pipeline is 3GW. The growth prospects of green hydrogen and its electrolysis production process will produce an inevitable supply pull on currently utilized precious metal catalysts. In fact, the Henry Royce Institute (UK) identified the reduction of precious metals in PEM electrolyser and fuel cells as one of its top five priorities for materials research enabling the hydrogen economy.

Jericho’s Hydrogen Platform

Jericho Energy Ventures investment in H2U follows on its hydrogen-based boiler acquisition of HTI earlier in 2021. JEV’s hydrogen investment platform offers shareholders full spectrum exposure to critical parts enabling the hydrogen economy.

About Jericho Energy Ventures

Jericho Energy Ventures (JEV) is focused on advancing the low-carbon energy transition with investments in hydrogen technologies, energy storage, carbon capture and new energy systems. JEV’s wholly owned subsidiary, Hydrogen Technologies, delivers patented, zero-emission boiler technology to the $30 Billion Commercial & Industrial heat and steam industry in addition to its investment in H2U’s electrocatalyst and low-cost electrolyser platform. JEV also owns and operates producing oil and gas assets in the US Mid-Continent, predominantly in Oklahoma.

This news release contains certain ‘forward-looking information’ within the meaning of applicable Canadian securities legislation and may also contain statements that may constitute ‘forward-looking statements’ within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995. Such forward-looking information and forward-looking statements are not representative of historical facts or information or current condition, but instead represent only Jericho’s beliefs regarding future events, plans or objectives, many of which, by their nature, are inherently uncertain and outside of Jericho’s control. Generally, such forward-looking information or forward-looking statements can be identified by the use of forward-looking terminology such as ‘plans’, ‘expects’ or ‘does not expect’, ‘is expected’, ‘budget’, ‘scheduled’, ‘estimates’, ‘forecasts’, ‘intends’, ‘anticipates’ or ‘does not anticipate’, or ‘believes’, or variations of such words and phrases or may contain statements that certain actions, events or results ‘may’, ‘could’, ‘would’, ‘might’ or ‘will be taken’, ‘will continue’, ‘will occur’ or ‘will be achieved’. Although Jericho believes that the assumptions and factors used in preparing, and the expectations contained in, the forward-looking information and statements are reasonable, undue reliance should not be placed on such information and statements, and no assurance or guarantee can be given that such forward-looking information and statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information and statements. Forward-looking information and statements are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those anticipated in the forward-looking information and statements which include, but are not limited to: the effects of and risks associated with the ongoing COVID-19 pandemic, the impact of general economic conditions, industry conditions and current and future commodity prices including sustained low oil prices, significant and ongoing stock market volatility, currency and interest rates, governmental regulation of the oil and gas industry, including environmental regulation; geological, technical and drilling problems; unanticipated operating events; competition for and/or inability to retain drilling rigs and other services; the availability of capital on acceptable terms; the need to obtain required approvals from regulatory authorities; liabilities inherent in oil and gas exploration, development and production operations; and the other factors described in our public filings available at www.sedar.com. Readers are cautioned that this list of risk factors should not be construed as exhaustive.The forward-looking information and forward-looking statements contained in this news release are made as of the date of this news release, and Jericho does not undertake to update any forward-looking information and/or forward-looking statements that are contained or referenced herein, except in accordance with applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Jericho Energy Ventures (www.jerichoenergyventures.com) (JEV) is focused on advancing the low-carbon energy transition with investments in hydrogen technologies, energy storage, carbon capture and new energy systems. JEV’s wholly owned subsidiary, Hydrogen Technologies, delivers patented, zero-emission, boiler technology to the $30 Billion Commercial & Industrial heat and steam industry.JEV also owns and operates producing oil and gas assets in the US Mid-Continent, predominantly in Oklahoma.

Ryan Breen, Head of Corporate Strategy at JEV & HTI, commented, “Our growing customer pipeline is a testament to our unique zero-emissions hydrogen-based boiler. Intensifying efforts by large steam consuming corporations to achieve their Net-Zero goals, in addition to supportive public policy, provide strong tailwinds to our business fundamentals. We look forward to further educating the market about our new hydrogen-based solution and converting robust customer interest into repeatable sales.”

About Jericho Energy Ventures

Jericho Energy Ventures (https://jerichoenergyventures.com) is focused on advancing the low-carbon energy transition with investments in hydrogen technologies, energy storage, carbon capture and new energy systems.