Silver Hammer Mining is focused on building a multi mine silver production company. Its growing asset portfolio includes the recently acquired past-producing Silver Strand and Burnt Cabin mines located in the renowned Coeur d’Alene mining district in Idaho, USA, one of the most prolific silver districts in the world and the earlier stage Lacy Gold-Silver project in British Columbia, Canada.

Labrador Gold is a Canadian-based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada. The Company is advancing the Kingsway Gold Project, located in the Gander Gold District of Newfoundland. The project is strategically located contiguous to New Found Gold’s Queensway Project and lies along strike to the northeast of their recent discovery of 92.86g/t Au over 19.0 meters.

Metallic Minerals Corp. (TSX-V: MMG / US OTC: MMNGF) is a growth stage exploration company focused on the acquisition and development of high-grade silver and gold projects within underexplored districts proven to produce top-tier assets. Our objective is to create value through a disciplined, systematic approach to exploration, reducing investment risk and maximizing probability of long-term success. Our core Keno Silver Project is located in the historic Keno Hill Silver District of Canada’s Yukon Territory, a region which has produced over 200 million ounces of silver and currently hosts one of the world’s highest-grade silver resources. The Company’s La Plata silver-gold-copper project is located in the high-grade La Plata district of the prolific Colorado Mineral Belt and our McKay Hill project northeast of Keno Hill is a high-grade historic silver-gold producer. Metallic Minerals is also building a portfolio of gold royalties in the historic Klondike Gold District. Metallic Minerals is led by a team with a track record of discovery and exploration success, including large scale development, permitting and project financing.

Russia causes a dramatic change in the global diamond market

Mountain Province Diamonds- a top-tier company with significant scale

Diamcor Mining- A junior diamond miner with potential

A potential bottom in DMI/DMIFF shares

A diamond is a pure solid form of the element carbon with its atoms arranged in a crystal structure, a diamond cubic. At room temperature and pressure, another solid form of carbon is graphite, a chemically stable form of the element. Diamonds form under high temperatures and pressure that cause the carbon atoms to bond and form crystals.

It takes carbon up to 650 million years to become fossil fuels. Transforming carbon into a diamond takes one to 3.3 billion years, approximately 25% to 75% of the earth’s age.

Diamonds occur in greater number and quality in the ocean, but the extraction process is expensive and challenging. Ocean miners dredge the ocean floor, bring the material onto mining ships, and sift it for diamonds. Mining diamonds from the earth’s crust involves releasing igneous emplace rocks with explosives as the encased diamonds are carried up with intrusive rocks from the earth’s mantle. Most diamond mines are around one hundred miles below the earth’s surface.

Rough diamonds look like shiny pebbles. Experts cut and polish the rocks that become the centerpiece of jewelry cherished worldwide. Only 20-30% of mined diamonds have a suitable quality for jewelry; the remainder goes to industrial applications. The industrial diamonds are too badly flawed, irregularly shaped, poorly colored, or too small for gems. However, they are critical for cutting, grinding, drilling, and polishing procedures because of a diamond’s hardness and heat conductivity.

The first Soviet leader, Vladimir Lenin, once said, “There are decades where nothing happens, and there are weeks where decades happen.”

The international diamond business is experiencing that phenomenon in early 2022, courtesy of his successor.

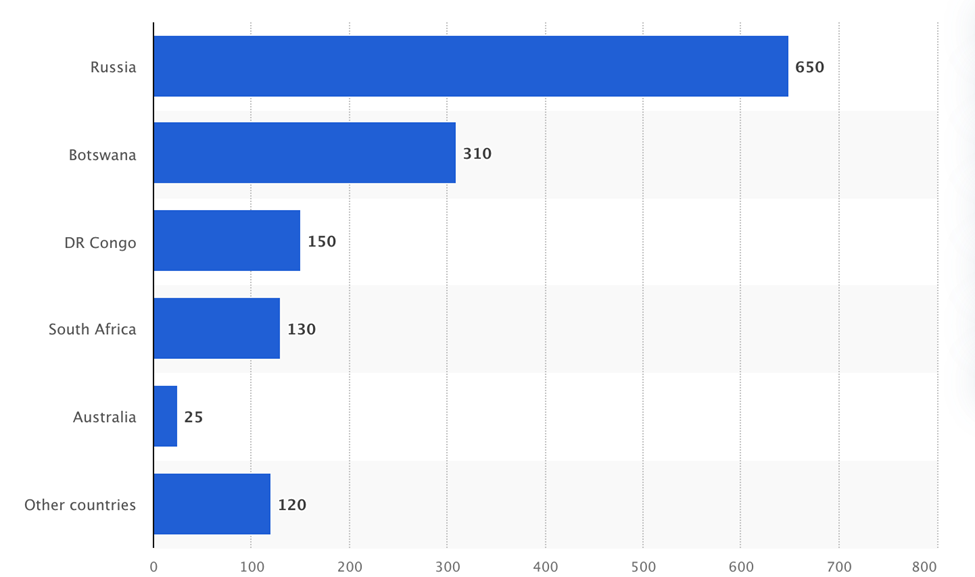

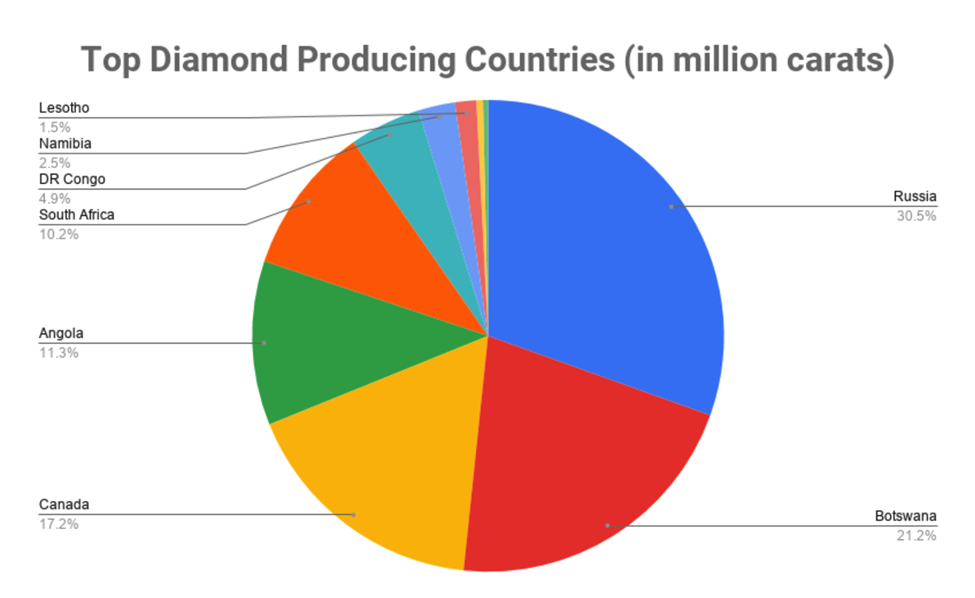

Russia is the leading producer- Canada is third Like many commodities, diamond production occurs in regions where the earth contains minable reserves.

The chart highlights that Russia has the largest diamond reserves with approximately 650 million carats, over double the country with the second-most reserves, Botswana. While diamonds are synonymous with South Africa, the nation is home to the fourth leading reserves behind Russia, Botswana, and the Democratic Republic of Congo. While the DR Congo has the third most reserves, Canada is the third-leading diamond-producing country.

As the chart illustrates, in 2020, Canada produced 17.2% of the worlds’ diamonds.

Russia causes a dramatic change in the global diamond market

On February 24, 2022, the world changed as the Russian military invaded Ukraine. President Vladimir Putin does not consider Ukraine a country but a part of Western Europe. Meanwhile, the watershed event occurred on February 4, 2022, when President Putin and Chinese President Xi signed a $117 billion trade agreement and shook hands on “no-limits” support. The Chinese-Russian alliance paved the way for Russia’s invasion of the country that the US, Europe, Canada, Australia, Japan, and allies worldwide consider a sovereign country in Eastern Europe. Russian success in Ukraine could pave the way for China’s reunification with Taiwan.

Sanctions on Russia leading to retaliatory measures are likely to choke off commodity supplies to the west. Russia is a leading producer and exporter of diamonds, oil, nickel, wheat, fertilizer, and a host of other raw materials.

The geopolitical landscape has deteriorated to the most dangerous level since World War II. War, sanctions, and trade embargos distort market prices, impacting the global supply chain and creating fundamental supply and demand imbalances. The dark cloud of war and tensions between Russia-China and the West may have a diamond lining for companies producing commodities to fill the gaps created by supply shortages and rising prices.

On February 24, the diamond market underwent a substantial change.

Mountain Province Diamonds- a top-tier company with significant scale

The DeBeers Group controls companies in the diamond mining, diamond processing, and diamond trading sectors. Still, it is the second-leading diamond company behind Alrosa, the Russian mining giant that distributed 38.5 million carats in 2021. De Beers distributed 30.78 million carats.

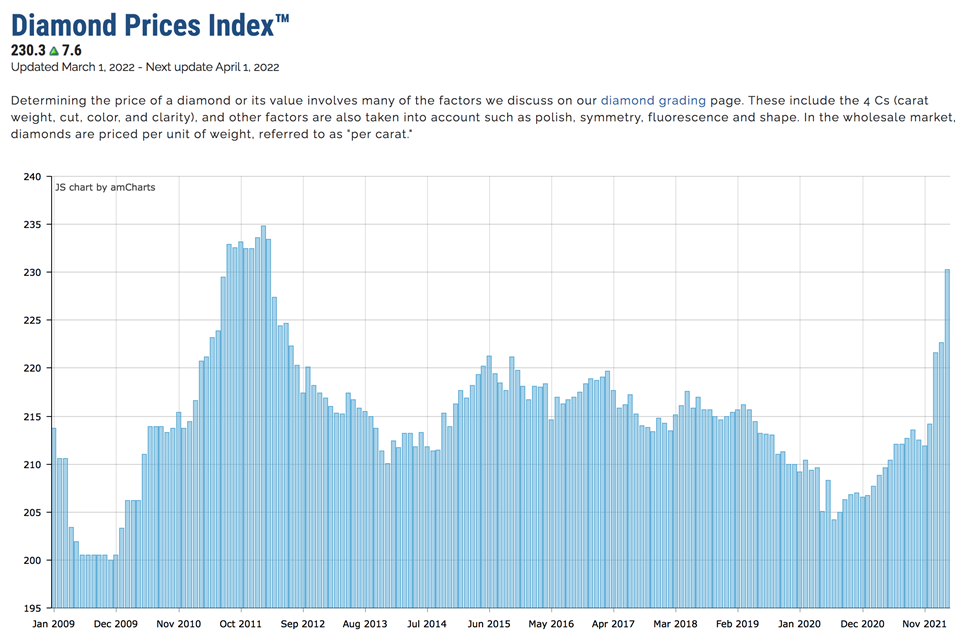

When most people think of diamonds, De Beers is the brand name that glistens like the stones. De Beers has been around since 1888 with South African roots. Today, the company calls London home, with the mining giant Anglo American (NGLOY)owning 85%. While price transparency in the diamond market can be opaque, prices have appreciated.

The price index rose from 204.20 in July 2020 to 230.30 in March 2022, a 12.8% increase.

Mountain Province Diamonds is a Canadian diamond producer that operates a joint venture with De Beers, owning the world’s fifth-largest diamond mine, Gahcho Kue, in Canada’s Northwest Territories. Mountain Province Diamonds also owns 100% of the Kennady North Project and explores for diamonds in the Northwest Territories through targeted drill programs with 13.6 million carat reserves and inferred resources of 7.35 million carats ten kilometers from the Gahcho Kue mine. A summary of some of the company’s other highlights includes:

The highest-grade diamonds in the De Beers portfolio at 1.55 carats per ton of reserves.

The second most favorable mining jurisdiction in Canada.

A commitment to sustainability through environmental stewardship.

Exploration territory of 107,000 hectares of 100% owned claims/leases surrounding Gahcho Kue.

Mountain Province Diamonds traded on the TSX in Canadian dollars under MPVD.TO. The company trades in the over-the-counter market in the US under the symbol MPVDF.

Source: Barchart

As the chart highlights, MPVDF shares fell to a low of 17.41 cents in March 2020 as the global pandemic gripped markets across all asset classes. The stock has moved higher with diamond prices and production success, making higher lows and higher highs with the price at 62.83 cents on March 16, over 3.6 times higher than the March 2020 low.

Diamcor Mining- A junior diamond miner with potential

Diamcor Mining Inc. is a junior diamond mining company that identifies, acquires, and operates unique projects with “near-term production potential.”

While many people think of De Beers synonymously with diamonds, the other name that comes to mind is Tiffany & Company. Diamcor established a long-term strategic alliance and the first right of refusal with Tiffany & Co, Canada, a subsidiary of Tiffany & Co in the US, for the purchase of up to 100% of the future production of rough diamonds from the Krone-Endora at Venetia Project at current market prices. Tiffany & Co. provides financing for the project. Diamcor acquired the Krone-Endora at Venetia project from DeBeers. The mine is co-located directly adjacent to the De Beers Venetia Diamond Mine in the Limpopo province of the Republic of South Africa. The project is a rare eluvial deposit, a direct shift of material from the higher grounds of the Venetia Kimberlite clusters onto the lower surrounding areas of Krone-Endora. The property is approximately 500 kilometers north-northeast of Johannesburg. The Venetia mine is the world’s third-largest diamond mine and South Africa’s leading mining, accounting for over 50% of annual production.

Some of Diamcor’s highlights include:

Accelerated phase two of a three-phase processing upgrade to increase volumes as the demand for rough diamonds has continued to be robust.

Diamcor’s most recent rough diamond sale yielded an average price of over $300 per carat, a 60% increase from the December 2021 price.

The project has revenue flows with demonstrated profitability.

The project has $70 million in development to date with significant infrastructure in place and a 30-year mining right.

A high percentage of the project’s diamonds are gem quality and can be found just 50 feet below surface.

Diamond reserves are likely on 95% of the project area that has not been defined, leading to significant growth potential.

US and European sanctions will limit the number of industrial and gem-quality diamond flows from Russia, pushing prices higher and availability lower. The world will be looking for new sources, and Diamcor’s project is far enough along and positioned to meet the increasing demand.

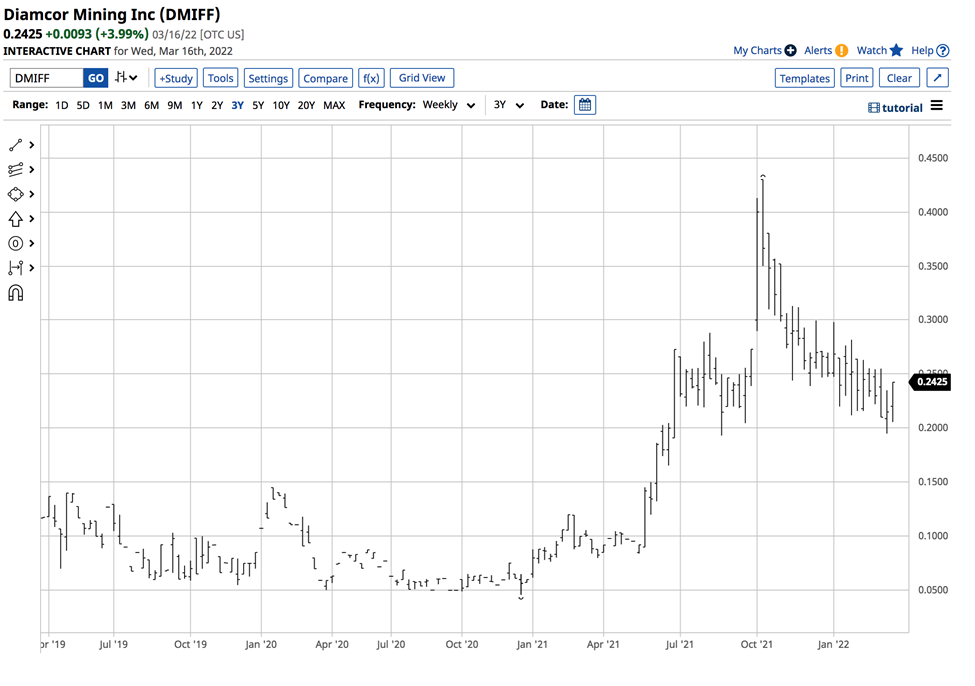

A potential bottom in DMI/DMIFF shares Diamcor Mining Inc trades on the TSX under the symbol DMI.VN. On the Us over-the-counter market, the symbol is DMIFF. The shares have moved appreciably higher since the late 2020 low.

Source: Barchart

As the chart highlights, DMIFF shares rose from a low of $0.046 in late December 2020 to $0.2425 on March 16, over five times higher. In October 2021, the shares peaked at 43.0 cents, over nine times higher than the late 2020 low. DMIFF returned a higher percentage gain than Mountain Province Diamonds (MPVDF) since its 2020 low.

It takes over a billion years for a diamond to form, making the stones a forever asset. Meanwhile, sanctions on Russia will limit the precious stones supplies, which could create an exciting opportunity for Diamcor, a mining company with lots of upside potential.

Written By: Andrew Hecht, on behalf of Maurice Jackson of Proven and Probable.

Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.

ABOUT GRANITE CREEK COPPER Granite Creek Copper is a Canadian junior mining, exploration company focused on the advancement of its 100%-owned Stu Copper-Gold project located in the Yukon’s Minto Copper District. This 115-square-kilometer property is between, and on trend with, Pembridge Resources’ high-grade Minto Copper-Gold Mine and, to the south, the Carmacks Copper-Gold-Silver project held by Copper North of which Granite Creek holds a 30% interest. The Stu project has excellent access to infrastructure with the nearby paved Yukon Highway 2, along with grid power within 12 km. Granite Creek Copper is one of top junior mining stocks and copper stocks 2021.

Joining us for a conversation is John Carter to share the value proposition of Silver Bullet Mines, which hosts the Black Diamond Property, Buckeye Mine, McMorris Mine in Arizona and the recently acquired Washington Mine in Idaho. Silver Bullet Mines is a high-grade silver company with blue sky potential in porphyry copper. Silver Bullet Mines is going into production on the Buckeye Mine in Arizona, and the Washington Mine in Idaho! Both of these are past producing high-grade silver mines. In addition, Silver Bullet Mines owns a 100% Pilot Processing Plant. Watch now!

Labrador Gold is a Canadian-based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada. The Company is advancing the Kingsway Gold Project, located in the Gander Gold District of Newfoundland. The project is strategically located contiguous to New Found Gold’s Queensway Project and lies along strike to the northeast of their recent discovery of 92.86g/t Au over 19.0 meters.