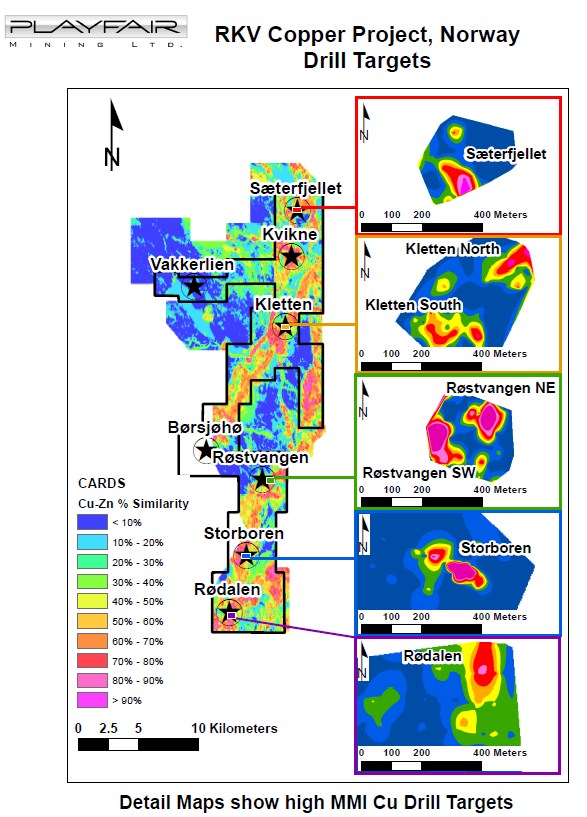

Vancouver, British Columbia–(Newsfile Corp. – August 23, 2021) – Playfair’s (TSXV: PLY) (FSE: P1J1) (OTC Pink: PLYFF) core drilling program on its large (201 square kilometers) 100% owned RKV Copper Project in South Central Norway is expected to start in early September. Playfair has delineated seven drill targets in five areas, Drill Notifications have been made and necessary permits are approved.

Playfair, as a responsible mineral explorer, values protecting the natural environment it works in. Playfair uses new technologies and methods to reduce the impact of its exploration. Playfair’s exploration to date has been in three phases.

The first phase of Playfair’s exploration used non-invasive machine learning algorithms to reinterpret existing geochemical-geological-geophysical data sets and outline potential exploration target areas with similarities to known mineral occurrences.

The second phase of Playfair’s exploration was minimally invasive. In the areas outlined as possibly favourable by the machine learning algorithms small pits were dug by hand, samples of soil were removed, and the pits refilled. There was no off-road driving. Subsequent chemical analysis outlined areas with a high content of copper or other elements of interest.

The third phase of Playfair’s exploration measured the intensity of the earth’s magnetic field in some of the areas where a high copper content was found in soils. Variations in the magnetic field provide important information about the underlying bedrock. The survey was non-intrusive and used an unmanned drone to carry the measuring equipment.

The seven drill targets were previously described: Storboren (November 07, 2019, and December 05, 2019, News Releases), Sæterfjellet, (January 06, 2021, News Release), Kletten North and Kletten South (January 28, 2021, News Release), Røstvangen Northeast and Røstvangen Southwest (February 17, 2021, News Release) and Rødalen (March 11, 2021, News Release).

The drill targets are MMI (Mobile Metal Ion) copper anomalies discovered by sampling target areas generated by Windfall Geotek (TSXV: WIN) (OTCQB: WINKF) using their proprietary Computer Aided Resources Detection System (CARDS).

All seven drill targets show compelling coherent MMI Cu anomalies with multiple MMI Cu values greater than 6,000 ppb. The highest value recorded was 53,300 ppb MMI Cu. A short MMI Report by SGS states that values greater than 6,000 ppb MMI Cu “are likely to be associated with weathering copper sulphides.”

Playfair’s fourth phase of exploration is planned to begin in September 2021. In keeping with Playfair’s intent to minimise the impact of its exploration on the natural environment Playfair will use a lightweight drilling machine which can be disassembled and hand-carried to the drill sites. Playfair’s man-portable drill has now arrived in Norway, cleared customs and has been transported to Tynset, approximately 25 km from Rødalen, the first drill target. With a population of 5,400, Tynset is the municipal centre of the Nord-Østerdalen region. Arctic Drilling As., a local Norwegian Company will carry out the drilling.

A presentation on the drilling plans can be found at this direct link or on Playfair’s website.

The technical contents of this release were approved by Greg Davison, PGeo, a qualified person as defined by National Instrument 43-101.

The road to a cleaner environment includes electric vehicles. Electric vehicles need copper, nickel, and cobalt. There is no green future without minerals.

Forward-Looking Statements: This Playfair Mining Ltd News Release may contain certain “forward-looking” statements and information relating to Playfair which are based on the beliefs of Playfair management, as well as assumptions made by and information currently available to Playfair management. Such statements reflect the current risks, uncertainties and assumptions related to certain factors including, without limitations, exploration and development risks, expenditure and financing requirements, title matters, operating hazards, metal prices, political and economic factors, competitive factors, general economic conditions, relationships with vendors and strategic partners, governmental regulation and supervision, seasonality, technological change, industry practices, and one-time events. Should any one or more of these risks or uncertainties materialize or change, or should any underlying assumptions prove incorrect, actual results and forward-looking statements may vary materially from those described herein.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Vancouver, British Columbia–(Newsfile Corp. – August 19, 2021) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX”) announces that pursuant to the Company’s Stock Option Plan, incentive stock options (the “Options”) to purchase an aggregate of 500,000 common shares, exercisable at a price of $3.66 per share for a period of five years, has been granted to certain directors, and a consultant of the Company.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”; and on the Frankfurt exchange under the symbol “6E9”. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 979-6666 Dave@EMXroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

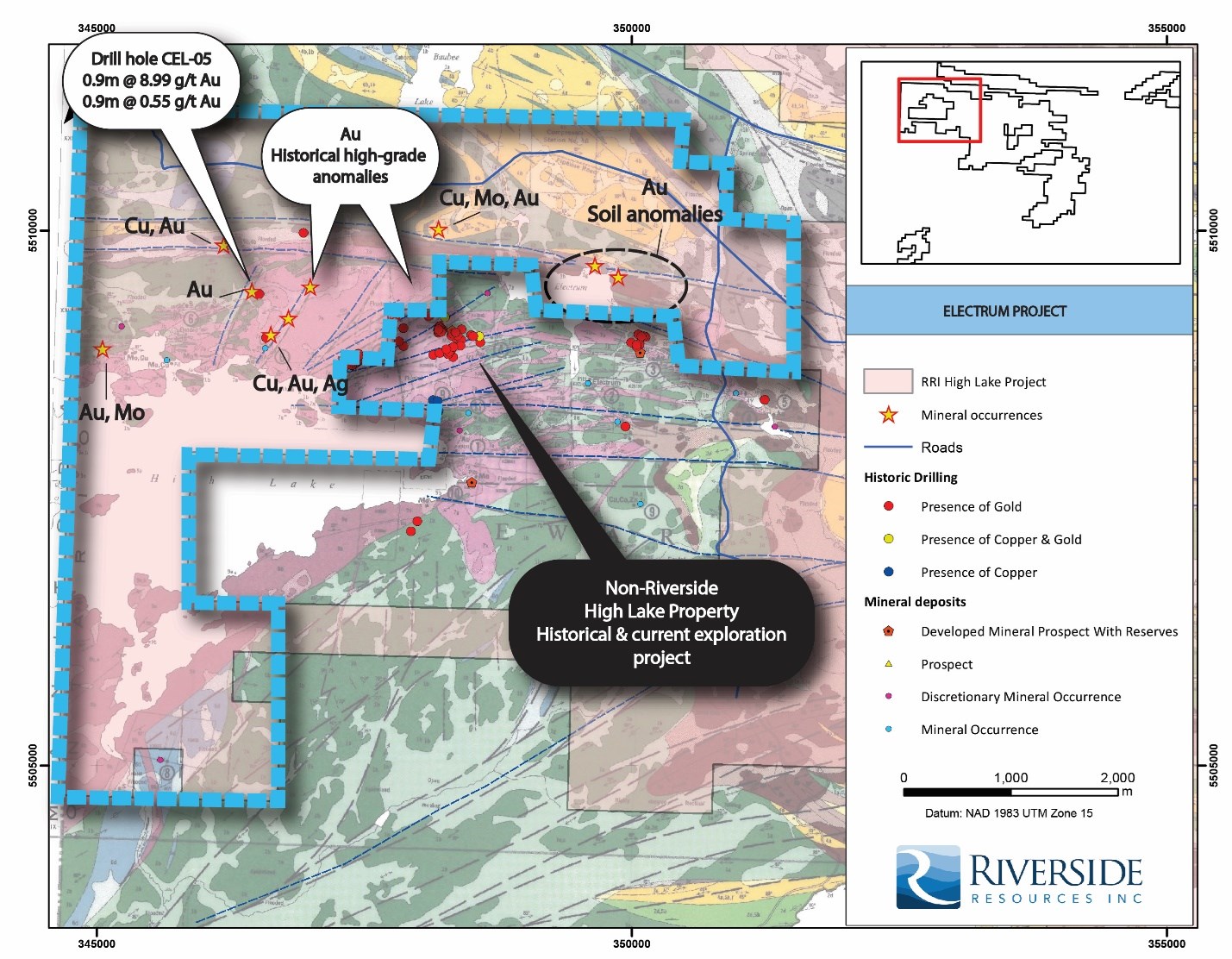

Vancouver, British Columbia–(Newsfile Corp. – August 19, 2021) – Riverside Resources Inc. (TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY) (“Riverside” or the “Company”), is pleased to provide an update on the work program progressing at the High Lake Greenstone Belt in Northwestern Ontario. The company has successfully delineated three (3) projects which are expected to move ahead with more detailed exploration.

Last year Riverside staked a commanding land position of 230 square kilometers within the High Lake-Shoal Lake Greenstone Belt, containing at least two gold mineralization systems with Riverside controlling the structural geologic and intrusion boundary projections of some exploration projects historically defined. This gold-bearing belt is located immediately east of the Ontario-Manitoba border and has good highway infrastructure and extensive favorable age and types of geology. The region hosts multiple discoveries, such as the Shoal Lake deposit which contains over 347,000 ounces of gold (Inferred and Indicated; 2010, NI 43-101[1] of the KPM total). Riverside’s interest in this belt has been triggered by the positive geological settings and extensive occurrences of mineralization found in the area. Recent and past production in Northwestern Ontario includes mines in the Red Lake, Rainy River and Hemlo gold districts, which collectively total over 130Moz gold. All of these active areas are located in similar greenstone belts in western Ontario. New mines and the resurgence of operations in these three gold camps is part of an overall renaissance for new development and integration of the past knowledge with new interpretations and work in this favorable mining Canadian province.

Riverside’s 3 projects in the High Lake – Shoal Lake Greenstone Belt:

Electrum Project: 1,800 hectares

Royal Project: 6,150 hectares

Canoe Project: 4,260 hectares

Figure 1: Riverside’s claim block within the High Lake – Shoal Lake greenstone belt. Highlights of the three defined projects.

Riverside’s President and CEO, John-Mark Staude: “In addition to our active exploration group in Mexico, Riverside is moving forward in Canada not only with the recent deal with iMetal Resources but also with new High Lake Greenstone portfolio of projects that present strong potential for new gold discoveries. Ontario’s greenstone belts have been producing world-class size gold resources and continue to deliver new discoveries like in Red Lake with the Great Bear and Pure Gold companies among a host of others. We are glad to be part of this momentum in northwestern Ontario and to be able to bring three additional 100%-Riverside owned projects with strong discovery potential into our portfolio.“

Electrum Project:

This project has many documented occurrences of gold, copper, and silver at surface, primarily structurally related and hosted within granitoids and at contact with meta-volcanics similar to features in the Manitoba and western Ontario orogenic gold greenstone gold camps. Riverside’s mineral tenure has been previously explored with 4 core drill holes, including an intercept of 0.9 m of 8.99 g/t Au (Internal technical reporting, 2005). Historical soil and rock sampling have reported anomalous grade in gold, copper, molybdenum and silver all of which can be used for vectoring of mineralization and on which Riverside is putting more to. The mineralization on Riverside’s 100% owned property is adjacent and follows the same structures and lithology of the drilled mineralization body found adjacent on the internal concession known as the High Lake Property not on Riverside’s concessions (see Figure 2 below), bringing interest on testing the high-grade targets and system for finding new discoveries associated with this area.

Figure 2: Map Area of Riverside’s Electrum project, showing geology and historical findings across the properties and the adjacent non-compliant Au resource.

Historical exploration of the Royal Project has defined many base metals occurrences with characteristics suggestive of volcanogenic massive sulfide (VMS) mineralization. This project, which lies to the east of the Electrum Project shows variation in geology, including alternating meta-volcanics and meta-sedimentary units folded along a primary E-W axis. Historical data highlights anomalies in base metals and VMS style mineralization at surface and some geophysics surveys by different companies and particularly by Noranda Exploration Company Ltd (1990), which highlighted several strong conductors that have yet to be drill tested. This style of environment has proven favorable in many deposits in Ontario, including the Rainy River Gold deposit located approximately 100 km to the south of the Project.

Figure 3: Focused map for Riverside’s Royal project, showing geology and historical findings across the properties with geological features similar to that of the Rainy River mining area.

The Canoe project is located along the edge of the main pluton bounding the known Shoal Lake gold deposit to the north which host over 347,000 ounces of gold. The area shows noted anomalies at surface and in drill holes of Cu-Zn-Au especially at the contact between the pluton and the meta-volcanics. As with the other two projects, the Canoe project is located along a key structural feature which is oriented NE and merging into EW to the north of the property. Historical work includes drill holes by Teeshin Resources Ltd., (1988), trenching, surface sampling and EM geophysics. Presence of gold to the southwest of the property is particularly abundant and can be traced into Riverside’s property (see Figure 4 below).

Figure 4: Geologic map of Riverside’s Canoe project, showing geology and historical findings across the properties. This is a portion of the full High Lake Greenstone Area controlled by Riverside Resources.

Moving forward, Riverside will be focusing attention on these three projects that all display excellent locations and have the potential to host the geological and structural settings favourable for future discoveries. Field work to date has been positive and the accessibility, favorable geology and presence of large-scale structures makes the High Lake Greenstone Area a key new opportunity for the Company.

Qualified Person & QA/QC:

The scientific and technical data contained in this news release was reviewed and approved by Freeman Smith, P.Geo, a non-independent qualified person to Riverside Resources, who is responsible for ensuring that the geologic information provided this news release is accurate and who acts as a “qualified person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects.

All data represented here from historical reporting, including but not limited to, drill results and resource estimates are historical in nature and require caution readers as the vintage work.

About Riverside Resources Inc.:

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has over $4M in cash, no debt and less than 72M shares outstanding with a strong portfolio of gold-silver and copper assets and royalties in North America. Riverside has extensive experience and knowledge operating in Mexico and Canada and leverages its large database to generate a portfolio of prospective mineral properties. In addition to Riverside’s own exploration spending, the Company also strives to diversify risk by securing joint-venture and spin-out partnerships to advance multiple assets simultaneously and create more chances for discovery. Riverside has properties available for option, with information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

[1]Publication – Technical Report on the Shoal Lake West Project, Northwestern Ontario, Canada Publication Number: 2008 43-101Date: 2008 Author: Valliant, W.W. and Chamois, P., Publisher Name: Scott Wilson Mining for Hays Lake Gold Inc., Reference Location: SEDAR

To purchase the Caserones Royalty, EMX has formed a 50%-50% partnership with Altus Strategies Plc (“Altus” (AIM: ALS) (TSXV: ALTS) (OTCQX: ALTUF) to acquire an effective 0.836% NSR royalty for US$68.2 million (see below for additional acquisition details). EMX and Altus will each control an effective 0.418% royalty interest and will each be responsible for $34.1 million of the purchase price.

Vancouver, British Columbia–(Newsfile Corp. – August 17, 2021) – EMX Royalty Corporation (NYSE American: EMX) (TSX: EMX) (FSE: 6E9) (the “Company“, or “EMX“) is pleased to announce that it has entered into an agreement dated August 16th, 2021 to acquire an effective 0.418% Net Smelter Return (“NSR“) royalty on the operating Caserones Copper-Molybdenum Mine (the “Caserones Royalty“) located in northern Chile for US$34.1 million in cash. Closing is anticipated to take place in two phases with both closings being completed by September 1st, 2021. In completing this transaction, EMX expects immediate and long term cash flow from a large porphyry copper-molybdenum deposit in a top tier mining jurisdiction.

To finance its US$34.1 million portion of the US$68.2 million purchase price, the Company has entered into a Credit Agreement (the “Credit Agreement“) with Sprott Private Resource Lending II (Collector), LP (“Sprott“). The Credit Agreement will increase the Company’s current proposed US$10 million credit facility with Sprott, in connection with the Company’s recently announced transaction with SSR Mining (see Company News Release dated July 29, 2021), to US$44 million (the “Credit Facility“) to include financing for the Caserones Royalty acquisition. Further details of the Credit Agreement are provided below.

The acquisition of the Caserones Royalty represents an important strategic development for EMX, by further enhancing the Company’s royalty cash flow and long-term exposure to copper as a key metal for the global economy. Recognition of the opportunity directly resulted from EMX’s ongoing assessment work in the region and serves as another example of how the Company leverages its regional expertise in various jurisdictions around the world to identify value enhancing business opportunities.

Caserones Mine Overview. The Caserones open pit mine is developed upon a significant porphyry copper-molybdenum deposit in the Atacama Region of the northern Chilean Andean Cordillera, 162 kilometers southeast of the city of Copiapó, at an approximate elevation of 4,300 meters above sea level. The Mine is operated by SCM Minera Lumina Copper Chile SpA, which is indirectly 100% owned by JX Nippon Mining & Metals Corporation (“JX Nippon“).

Caserones is located at the southern end of the well documented Maricunga mineral belt and comprises an Early-Miocene porphyry system associated with a cluster of dacite porphyries and breccias intruding Palaeozoic granitic, volcanic, and metamorphic rocks. Caserones has a well-developed supergene enrichment profile of oxide copper and secondary chalcocite that overlies hypogene sulfide (chalcopyrite-molybdenite) mineralization.

Caserones produces copper and molybdenum concentrates from a conventional crusher, mill and flotation plant, as well as copper cathodes from a dump leach, solvent extraction and electrowinning plant. In 2020 the mine produced 104,917 tonnes of fine copper in concentrate, 2,453 tonnes of fine molybdenum in concentrate, and 22,056 tonnes of fine copper in cathodes. The Caserones open pit has operated with an average waste: ore strip ratio of 0.47, has 17 years remaining in its current mine plan, along with excellent exploration potential. In a news release dated November 9, 2020, JX Nippon announced plans for “stepping up exploration efforts in areas around the mine” in an effort to expand production and extend the mine life.

Acquisition Details. The Caserones Mine is subject to a 2.88% NSR royalty provided for in a 2009 agreement between Minera Lumina Copper Chile S.A. as purchaser, and Compañía Minera Caserones (“CMC“) and Sociedad Legal Minera California Una de la Sierra Peña Negra (“SLM California“) as vendors. CMC and SLM California originally staked the mineral claims that overlie the Caserones deposit, and ownership of the 2.88% NSR royalty is currently divided between CMC (32.5%) and SLM California (67.5%). EMX and Altus will each be indirectly purchasing a portion of the SLM California royalty. Under the 2009 agreement, the NSR interest will be reduced to 2% and 1% if the London Metal Exchange (“LME“) quoted copper price falls below US$1.25 and US$1.00 per pound respectively.

EMX and Altus have formed a Chilean company, Minera Tercero, Spa (“Tercero“), of which the EMX and Altus each own 50%. Tercero will purchase 43% of the issued and outstanding shares of SLM California through a Share Purchase Agreement with 16 shareholders of SLM California (represented by Leonel Polgatti Goycoolea, a shareholder) for US$68.2 million. Tercero will enter into a shareholder’s agreement with the selling shareholders of SLM California, that together with Tercero hold approximately 89% of SLM Californa’s issued and outstanding shares, to govern SLM California. SLM California’s sole purpose is to administer the company, pay Chilean taxes and distribute its royalty proceeds to the shareholders, including Tercero.

Sprott Credit Agreement. In order to finance its US$34.1 million portion of the US$68.2 million purchase price under the Share Purchase Agreement, the Company has entered into the Credit Agreement, which encompasses the previously proposed financing related to EMX’s recent transaction to acquire the SSR Royalty Portfolio. The senior secured Credit Facility is in the principal amount of US$44 million, which includes up to US $10 million which will be used to finance a portion of the purchase price of the SSR Royalty Portfolio.

Under the Credit Agreement, the Credit Facility matures on July 31, 2022, bears interest at a rate of 7% per annum, and is secured by general security agreements over the assets of the Company and certain of its subsidiaries, and pledges of the shares of certain of the Company’s subsidiaries, who will, at Sprott’s election, also be guarantors of the loan. In addition to interest payable, the US$44,000,000 advanced under the Credit Facility was subject to an original issue discount equal to 4.61364% of the amount of the advance. Under the Credit Agreement, the Company will be required to maintain minimum unrestricted cash of USD $1,500,000.

In conjunction with the Credit Agreement, Sprott subscribed for US$1,235,000 of common shares of the Company (“Common Shares“) at a deemed price equal to a 10% discount to the 5-day VWAP of the Common Shares on the NYSE American exchange immediately prior to July 12, 2021 of $US 3.0450, which resulted in the issuance of 450,730 Common Shares.

Summary. The acquisition of the Caserones Royalty provides immediate enhancement to EMX’s royalty cash flow and secures long-term proceeds from copper and molybdenum production in one of the world’s top mining regions. This transaction nicely compliments the Company’s growing portfolio of royalty interests in South America, which has become a recent emphasis in the Company’s growth strategy.

Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and an employee of the Company, has reviewed, verified, and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol EMX. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 979-6666 Dave@EMXroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@EMXroyalty.com

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding completion of the transaction, perceived merits of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential”, “upside” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors. It is possible EMX may not complete the transaction, as a result of failure to fulfill conditions of closing, unavailability of financing or for other reasons EMX cannot anticipate at this time.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended June 30, 2021 and the year ended December 31, 2020 (the “MD&A”), and the most recently filed Revised Annual Information Form (the “AIF”) for the year ended December 31, 2020, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

Vancouver, British Columbia, August 16, 2021 (NYSE American: EMX; TSX Venture: EMX; Frankfurt: 6E9) – EMX Royalty Corporation (the “Company” or “EMX”) is pleased to report results for the quarter ended June 30, 2021 (“Q2-2021”). The Company’s filings for Q2-2021 are available on SEDAR at www.sedar.com, on the U.S. Securities and Exchange Commission’s website at www.sec.gov, and on EMX’s website at www.EMXroyalty.com. Financial results were prepared in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board.

HIGHLIGHTS FOR Q2-2021

Financial Update

Dollar amount are in CDN unless otherwise noted.

EMX ended the three month period at June 30, 2021 with a balance sheet including cash and cash equivalents of $41,979,000, investments, strategic investments, investment in associated entities, and receivables valued at $34,777,000, and no debt.

EMX had revenue of $4,255,000 which includes royalty income, other property income including income from the sale or option of property interests and management fees, and interest and dividends earned on cash and investment balances. Included in revenues was royalty income of $284,000 and $3,801,000 for the fair value of equity positions and cash received on the sale and option of property interests. Revenues for Q2-2021 increased compared to Q2-2020 with an increase in option and other property income and interest income. Royalty income for Q2-2021 was comparable to Q2-2020.

Royalty generation costs totaled $5,378,000 of which the Company recovered $1,689,000 from partners.

General and administrative expenses totaled $979,000 which includes $177,000 in salaries and consultants, $250,000 in administrative costs, $298,000 in professional fees, $71,000 in transfer agent and filing fees, $46,000 in travel, and $137,000 in investor relations costs. General and administrative costs can fluctuate from period to period depending on activity and timing of comparable costs.

For the three months ended June 30, 2021, the Company had a net loss from operations of $2,039,000 including $260,000 in depletion, depreciation, and direct royalty taxes, and $2,845,000 in share-based compensation of which $1,479,000 was included in royalty generation costs. Other items affecting net loss and financial results in Q2-2021 include a gain from the Company’s investment in an associated entity of $158,000, a fair value loss on investments of $425,000, and a foreign exchange adjustment of $1,240,000. The foreign exchange adjustment was a direct result of holding cash and net assets denominated in US dollars.

Operational Update

EMX’s royalty and mineral property portfolio totals over 200 projects on five continents. The following summarizes the work conducted in Q2-2021, as well as subsequent events, by the Company and its partners.

As a subsequent event, EMX entered into an agreement dated July 29, 2021 with SSR Mining Inc., and certain of its subsidiaries (“SSR Mining”), to purchase a portfolio of royalty interests and deferred payments (see EMX news release dated July 29, 2021). The portfolio consists of 18 geographically diverse royalties, with four royalty assets at advanced stages of project development, and also includes US$18 million in future cash payments. The transaction is expected to provide significant near-term cash flow to the Company and establishes a pipeline of quality royalty assets in numerous well-recognized mineral belts around the world. Completion of the transaction is subject to customary closing conditions, including acceptance by the TSX Venture Exchange.

In North America, EMX received provisional payments of approximately US$198,000 from the sale of 110 gold ounces produced at the Leeville royalty property in Nevada’s Northern Carlin Trend. On the royalty generation front, EMX optioned one copper project in Utah while adding new gold and copper projects to the portfolio by staking open ground. Partner companies continued to add value to the portfolio with encouraging drill results for precious metals projects in Nevada (3) and Idaho (1), including Ridgeline Minerals at the Selena royalty property, U.S. Gold at the Maggie Greek royalty property, and Gold Lion Resources at the Robber Gulch project.

EMX’s royalty and mineral asset portfolio in key mining districts of Ontario and Quebec, including the Red Lake camp, generated $392,000 in cash and fair value equity payments.

In Fennoscandia, the Company acquired 37,500 hectares of mineral exploration permits in central Norway that cover the zinc-lead-copper-silver-gold occurrences and historical mines of the Mo-i-Rana district. The transaction with Gold Line Resources and Agnico Eagle closed, by which Gold Line can acquire a 100% interest in Agnico’s Oijärvi gold project in Finland and the Solvik gold project in Sweden for staged cash payments as well as shares of Gold Line and shares of EMX. Agnico will retain a 2% NSR royalty on the projects, 1% (half) of which may be purchased by EMX for US$1,000,000. EMX will receive additional share and cash payments from Gold Line as reimbursement for the EMX shares issued to Agnico. Subsequent to the end of Q2, EMX executed an agreement for the sale of its Svärdsjö polymetallic project in Sweden to District Metals Corp. (TSX-V: DMX) for share equity, annual advance royalty payments, and retained royalty interests to EMX’s benefit. As new acquisitions and deals were completed, partner companies continued to advance EMX’s royalty properties, which included encouraging results from District’s drill program at the Tomtebo polymetallic project in Sweden’s Bergslagen mining district.

In Australia, the Company expanded the land positions at the Yarrol and Mt Steadman gold projects through the acquisition of additional permits covering multiple historical drill defined zones of mineralization. Both projects are located in the goldfields of central-Queensland and are available for partnership.

In Serbia, Timok operator Zijin Mining Group Co. Ltd. continued on an accelerated development pace of the Upper Zone copper-gold project which is covered by an EMX 0.5% NSR royalty. As a subsequent event, EMX filed an amended and restated Technical Report titled “NI 43-101 Technical Report – Timok Copper-Gold Project Royalty, Serbia” on SEDAR authored by Mineral Resource Management LLC with an effective date of December 31, 2020 and report date of July 21, 2021.

CORPORATE UPDATE

EMX is diligently monitoring developments regarding the ongoing coronavirus pandemic (“COVID-19”), with a focus on the jurisdictions in which the Company operates. EMX has implemented COVID-19 prevention, monitoring and response plans following the guidelines of international agencies and the governments and regulatory agencies of each country in which it operates.

EMX’s priority is to safeguard the health and safety of its personnel and host communities, support government actions to slow the spread of COVID-19 and assess and mitigate the risks to business continuity. Although various levels of restrictions remain in place for many jurisdictions where the Company operates (e.g., travel restrictions, etc.), EMX’s field programs are up-and-running principally with in-country based staff.

OUTLOOK

EMX ended Q2-2021 with $42 million in cash, $16 million in tradable securities, $7.7 million in private company equity and warrants, and $4.7 million in strategic investments. The Company continued to complete deals while adding new properties to the royalty generation portfolio, as well as new partners. In addition to the Company’s Q2-2021 successes, as a subsequent event the announcement of the SSR agreement represents an important milestone for the Company, as it seeks to boost its royalty cash flow streams and secure additional long-term optionality in its royalty portfolio.

EMX has been diligently pursuing royalty acquisitions over the last few years in what has been a highly competitive market. EMX has evaluated a large number of royalty purchase opportunities, but has been very selective in its acquisitions, with the Timok, Kaukua, and Gold Bar South royalties being prime examples. EMX sees a similar value proposition with the SSR royalty portfolio acquisition in that it will deliver near-term benefits (i.e. cash flow) as well as long term value to EMX’s shareholders.

The SSR portfolio includes four advanced stage development projects, namely, Gediktepe oxide and sulfide (Turkey), Yenipazar (Turkey), and Diablillos (Argentina), which are complemented by 14 additional royalty interests covering both precious metal and base metal assets in South America, Mexico, the United States (Nevada) and Canada. The SSR royalty portfolio acquisition is well aligned with EMX’s corporate growth strategy, whereby the Company leverages its in-region expertise to identify opportunities in jurisdictions where EMX already has a strategic presence, and hence a competitive advantage. This approach leads to value creation for the Company, as well as synergies with existing EMX initiatives around the world.

Meanwhile the Company’s royalty generation initiatives continued moving forward. EMX’s quick actions led to the acquisition of a 37,500 hectare position covering the historical mines, deposits, and prospects of the Mo-i-Rana polymetallic district in central Norway. This consolidated district-scale package presents enough opportunities to potentially support multiple royalty generation deals. In Australia, EMX expanded its property positions in the goldfields of Queensland at the Yarrol and Mt Steadman projects to yield significantly enhanced property packages available for partnership. In the western U.S., new gold projects were staked in Idaho and Nevada. Fennoscandia, Australia, and the U.S. are stable exploration and mining jurisdictions, and EMX’s royalty generation assets provide prime opportunities for potential partners.

EMX’s established partner companies continued to add value to the portfolio with encouraging drill results. In the western U.S. this included precious metals projects in Nevada (Ridgeline Minerals at Selena and U.S. Gold at Maggie Greek) and in Idaho (Gold Lion at Robber Gulch). In Fennoscandia, most notable were District’s drill success at Tomtebo (Norway) and Norden’s at Gumsberg (Sweden). These drill programs were either conducted with EMX’s technical support, provided on a 100% reimbursed basis, or independently by the partner companies in other cases.

EMX’s value-focused and long-term approach has allowed the Company to maintain its treasury while not overbidding for assets. This strategy allows the company to patiently wait for opportunities like the SSR royalty transaction (and similar future opportunities), which nicely complement its ongoing organic royalty generation. The Company’s progress so far in 2021 signals a number of Company achievements and milestones, and we enter the second half of the year with well-founded optimism for even greater success.

QUALIFIED PERSONS

Michael P. Sheehan, CPG, a Qualified Person as defined by NI 43-101 and employee of the Company, has reviewed, verified and approved the above technical disclosure on the United States, Canada, South America, and Strategic Investments. Eric P. Jensen, CPG, a Qualified Person as defined by NI 43-101 and employee of the Company, has reviewed, verified, and approved the above technical disclosure on EMX Capital (SSR transaction), Serbia, Fennoscandia, Turkey, and Australia.

About EMX. EMX is a precious, base, and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and the TSX Venture Exchange under the symbol EMX. See www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 979-6666 Dave@EMXroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended June 30, 2021 (the ”MD&A”), and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2020, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

Joining us for a conversation is Christian Easterday, the CEO of Hot Chili Limited (ASX: HCH | OTCQB: HHLKF). It’s a pleasure to be speaking with you sir, Hot Chili Limited is having, simply put, a banner year, as throughout the year it’s been one success after another as Hot Chili has released a string of successful press releases to advance the massive Cortadera Copper-Gold Project. Before we delve into the exciting news you have for current and prospective shareholders, Mr. Easterday, please introduce us to Hot Chili Limited and the opportunity the company presents to the market.

Christian Easterday:

Well, it’s been a very exciting time, not just in the copper space, but for Hot Chili, as we really transform ourselves from a corporate exploration company on the coastline of Chile to a full-fledged very significant copper developer and now very pleased to be welcoming Glencore as our largest shareholder through their participation in our recent $40 million capital raising, which was just announced during the week.

Christian Easterday:

None of this has been possible without the string of successes that we’ve had at a world-class Cortaderaporphyry discovery on the coastline, which has allowed us to consolidate a major copper development hub sitting on the Pan-American highway right next to a port 600 kilometers north of Santiago in Chile. We are certainly hitting our straps after announcing our maiden resource last year, where I did my last interview with you Maurice, we now have some three-quarters of a billion tonnes at about half a percent copper equivalent in open-pit and underground resource space.

Christian Easterday:

And that Cortadera discovery, which is one of only two major copper discoveries that the world has seen since 2014 is seeing some significant growth in our drilling. And we’ve been able to put out some further world-class intercepts as we expand that resource base, and look to take our combined asset to over a billion tons. And hopefully, we’ll be looking to put that out later in the year.

Maurice Jackson:

Sounds exciting, sir. You referenced the $40 million funding. Can you go through the details for us on this landmark transaction, along with your new strategic partner Glencore Resources?

Christian Easterday:

We have been very busy in staging the next steps for Hot Chili, as we seek to align ourselves with the rest of the copper porphyry developers in the America’s. Currently, we’re the only major copper porphyry player that is not listed on the TSX and TSX.V and we’re looking to, dual list, the company in the coming months over on the TSX.V in Canada. So, a very exciting time as we transform the company and look to align to a set of copper developers, which are seeing market capitalizations in the range of $500 million to $1.4 billion with some of the leaders over there in Canada being Filo Mining, Solaris, SolGold and several resources that they control, obviously Hot Chili’s resource bases is comparing extremely favorably.

Christian Easterday:

We see a real value gap that exists with the only non-TSX/TSX.V player in our peer space. The $40 million capital raising that we’ve just completed was well supported out of Australia and also overseas with significant support seen from North America. But most importantly, when we put that capital raising together, that was all about taking our last real key milestone, which is the purchase of Cortadera itself. We had one remaining payment that was due in one year of $15 million U.S. or roughly $20 million Australian. And the asset has grown so rapidly and was really sitting on a world-class discovery here that there was significant interest in taking out that final ownership payment, which we’ll be making immediately, and once we close this raising in the coming week or two. So that’s some color on the reason for the raising outside of the purchase of Cortadera, the rest of the money is going in to continue our aggressive resource growth drilling program.

Christian Easterday:

And also now to start stepping out and start testing some very exciting growth potential in what looks like an opportunity to unlock a cluster of high-grade porphyry targets in and around our two key assets at Productora and Cortadera. Part of this raising as you well said, we’ve now attracted the support of one of the largest mining companies in the world in Glencore. And they’re, as is being announced, they’re coming in now as a 9.99% shareholder in Hot Chili, which will make them the largest shareholder in Hot Chili. And we’ll be shortly welcoming their support with a board member coming on to Hot Chili’s board technical steering committee. This will allow us to tap in and utilize that strong capability and experience of Glencore in developing large-scale copper assets in jurisdictions, such as Chile.

Christian Easterday:

And I’m looking forward to the new relationship and our new large shareholder in Glencore. They’ve certainly given the company a significant endorsement of our assets. Effectively, the due diligence by the world has just been completed by one of the largest copper producers in the world, one of the largest mining companies in the world, and a really key aspect of that is where we’re looking forward to negotiating over the coming months, which is an off-take arrangement for the first eight years of our targeted 25 to 30-year mine life that we’re trying to build out on the coastline. That will be for about 60% of the off-take out of our combined Costa Fuego project. And we really look at that as a significant de-risker for the company in terms of actually having a partner there to take a benchmark component on the pricing of our offtake. We view this a strong hedging position. The company is putting in place with the largest global trader of copper concentrates. And now our largest shareholder.

Maurice Jackson:

Having Glencore as a strategic partner is a big, big feather in your cap and puts Hot Chili in the driver’s seat. I would say on the Autobahn, you’ve really, you’ve done several things here for shareholders. That, and again, just this off-take, it’s something that may be minor when you look at all the successes here, but that off-take agreement as well is just another strategic step. And it just demonstrates the business acumen and the leadership here. And I have to just give you a big kudos, sir. Switching gears, let’s look at some numbers. Please provide us the capital structure for Hot Chili Limited.

Christian Easterday:

Look at the moment. Our pre-capital structure was about 3.1 billion shares. We’ll come over the 4 billion mark after this raise, where we have about 1.1 billion shares that we’ll be issuing to Glencore and to other institutional investors. We’ve also been able to give the shareholders a Hot Chili, a slice of the capital rising at 3.2 cents. And I suppose that’s sort of something really important from the board that we wanted all of the shareholders to be able to participate at the same level of investment that Glencore and the institutional investors are coming in at. And that’s certainly seen a very good response day one, day two, day three in the market over here in Australia. We’ve not just a raising that an 11% discount to our closing price pre capital rising, but we’ve been able to get the stock to have a very positive lift after that announcement.

Christian Easterday:

We’re trading at around 40% or 50% higher than the issue price for the rising. We are very pleased to be able to allow all of our shareholders to participate in a share purchase plan. We now have a firm opportunity to rewrite Hot Chili into the billion-dollar-plus market capitalization space. And we believe that we can do that in short order, particularly with our realignment now, and being able to take Hot Chili into the North American market with a dual listing on the TSX/TSX.V and to be able to compare ourselves very favorably with some of the names I’ve mentioned, the Oracles, the Filos, the Solaris’, which have seen spectacular increases in their share prices in association with the lifting copper price environment.

Christian Easterday:

When you have a copper price environment over $4 per pound, and you have an upper-tier copper asset that is rapidly approaching a tier-one asset, and there’s very few of those available in the world to be able to leverage that value and to be able to come into a dual listing and now with Glencore on our register. We believe that we have a significant rewrite ahead of the company. And now the ability in the market’s eyes to be able to execute and transition Hot Chili into a large scale or major copper producer.

Maurice Jackson:

In closing, sir, what would you like to say to shareholders?

Christian Easterday:

I’d like to thank all of our shareholders for ensuring that Hot Chili was one of the survivors of the last downturn in copper, to support our vision, to build out a new copper player of substance globally with the project that we’re positioning in the plus 100,000 tonne per annum, copper production space. Very few of those available in a world where there’s very few major copper discoveries being made.

Christian Easterday:

Now our shareholders, undoubtedly, will start to reap the rewards of what has been a 13 year vision by myself and our founders to build out something that you don’t see very often. And the last time the Australian stock market had anything in this space was, of course, Equinox resources. And we all know knew that a real key element in the rewrite of that company from a $400 million company to a $7.2 billion takeover was their ability to be able to transition into production. And most importantly was to be able to position Equinox into the north American markets at the right time.

Christian Easterday:

They did that in the last copper cycle, and they were able to extract that significant rewrite in valuation. And we were simply following a very well-worn path that has already been done before.

Maurice Jackson:

Last question, sir, what did I forget to ask?

Christian Easterday:

I’m sure we’ll have plenty of time for further questions down the road, Maurice. We’ve got some pretty exciting drilling results coming out of our expansion program that we’ll now be able to start getting out to market now that I’m out of a blackout period following about four or five weeks of no sleep completing the transaction that we’ve just announced.

Christian Easterday:

But most importantly, we’ve got a lot of very exciting news flow in the lead up to our dual listing in the TSX.V, which is scheduled for around late October, and then shortly to follow that hopefully a significant upgrade at our Cortadera porphyry discovery and Chili.

Maurice Jackson:

Mr. Easterday, it’s been an absolute delight to speak with you today, wishing you and Hot Chili Limited the absolute best, sir.

And as a reminder, I am a licensed representative to buy and sell precious metals through Miles Franklin Precious Metals Investments, where we have several options to expand your precious metals portfolio, from physical delivery of gold, silver, platinum, palladium, and rhodium, to offshore depositories, and precious metals IRA’s. Give me a call at 855.505.1900 or you may email: Maurice@MilesFranklin.com. Finally, please subscribe to www.provenandprobable.com, where we provide: Mining Insights and Bullion Sales, subscription is free.

YERINGTON, Nev., Aug. 13, 2021 (GLOBE NEWSWIRE) — Nevada Copper Corp. (TSX: NCU) (OTC: NEVDF) (“Nevada Copper” or the “Company”) today provided an operations update and announced filing of its Q2 2021 financial statements and the related management’s discussion and analysis.

Operations Update

Mining of First Stope: During Q2 2021 the Company successfully mined approximately 9,500 tons at a grade of 1.5% Cu out of the first stope mined since the restart of the mine in the East South area. Tons mined and ore breakage was consistent with the plan, indicating that the mining method was appropriate for the ground conditions where the stope is located, although mining of the stope was later than originally planned. Subsequently, the stope was successfully back-filled and the Company is now preparing to mine the next stope in the East South area.

Mine Infrastructure: Mine infrastructure works were further advanced during the quarter albeit slower than expected, including the final two sets of underground fans installed and commissioned as planned in Q2 2021, allowing for an increase in development rates. Commissioning of the surface ventilation fans continues to be planned for Q4 2021.

Material Hoisting: Following completion of the Main Shaft material handling system in Q4 2020, the Underground Mine achieved a peak daily hoisting rate of over 3,000 tons by February 2021 and has since achieved a hoisting rate equivalent to 5,000 tons per day (“tpd”) on a shift basis, demonstrating capacity of the shaft and associated materials handling system. Due to slower development rates in Q2 2021 through the water-bearing dike structure, the Company now expects to reach sustainable hoisting rates of 3,000 tpd in Q4 2021 and for hoisting rates to continue to ramp-up beyond that.

Lateral Development: Lateral development continued on multiple headings, providing access to ore mining zones in the East South orebody and advancing development towards the East North orebody. During the Q2 2021 the Company continued development of the East North area through a dike structure located between the East South and East North orebodies. A second heading crossing the dike is 90 feet below the first heading. Additional ground support was required to complete dike crossing and the Company is almost through the water-bearing dike structure.

Processing: The process plant maintained average concentrate grade over 21% along with 81% recoveries. While batch processing ore through the processing plant, the Company achieved a weekly average of 3,271 tpd. 87,211 tons of ore was processed through the concentrator in Q2 2021 with an average feed grade of 0.51%. Approximately 1,514 tons of concentrate was produced at a 21% average copper grade for Q2 2021. During June, Sedgman successfully completed C5 testing of the processing plant for grind size and moisture of concentrate and tailings.

Production ramp-up and Mine Planning: The Company continues to advance its mine planning process and has made revisions to the mine plan. The revised mine plan incorporates the recent experiences during mine development, including the geotechnical conditions of the East South area. In light of the impact of the water-bearing dike structure, expected equipment utilization rates and the remaining infrastructure projects to be completed the Company now expects that the Underground Mine will reach a hoisting rate of 3,000 tpd in Q4 2021 and 5,000 tpd in H1 2022.

Property Development Plans

Underground: The Company has progressed its life-of-mine planning aimed at operating its underground mine at an ultimate production rate in excess of the originally contemplated 5,000 tons per day rate. Mine planning work further supports the potential for the mine, once ramped-up to steady-state, to operate at higher long-term rates of 6,500 tons per day milled, increasing long-term annual copper production potential.

Open Pit: The Company reviewed its longer-term development targets for its Pumpkin Hollow property, including a solar power study, electrification and emissions reduction analysis, follow up work on scaling opportunities to improve economics and plans for infill and extension drilling.

Exploration: The Company plans to follow up on new exploration targets added through recent expansion of the Company’s properties to the east and analysis of geophysical surveys.

Corporate

Payroll Protection Program Loan (“PPP Loan”) Forgiveness: on August 6, 2021, the Company received confirmation for the approval of the forgiveness of the PPP Loan in the amount of $2.4 million. The loan was received in 2020 as part of a United States government COVID-19 pandemic program to assist companies to retain their employees.

KfW Credit Facility Amendment Discussions: On June 30, 2021, the Company received a waiver from KfW IPEX-Bank (“KfW”), the lender under its amended and restated senior credit agreement (the “Amended KfW Facility”), which provided for a 60-day extension to the project completion longstop date (the final date to meet the requirements of the project completion test under the Amended KfW Facility) (the “Project Longstop Date”) from June 30, 2021 to August 31, 2021. The Company has requested and expects to receive a further short-term extension of the Project Longstop Date from KfW. The Company is also in discussions with KfW to achieve a longer-term extension of the Project Longstop Date to a date in 2023, the deferral of debt servicing by twelve months and the temporary deferral of compliance with certain financial covenants under the Amended KfW Facility as the Underground Mine continues to ramp-up. The Company expects to have the short-term extension finalized in the next few weeks and the other proposed amendments finalized in the next few months. However, there can be no assurance that such extension and amendments will be finalized by such times or at all. Failure to finalize the extension or these amendments would result in the Company being in default under the Amended KfW Facility.

2021 Promissory Notes: The Company received a loan of $15 million under a promissory note with Pala Investments Limited (“Pala”), the Company’s largest shareholder, in June 2021 (the “2021 Promissory Note”) providing additional liquidity for the ramp-up of the Underground Mine and addressing the reduced development rates associated with crossing the water-bearing dike structure. The 2021 Promissory Note has a maturity date of June 30, 2022, and bears interest at 8% per annum on amounts drawn. Subsequent to the end of Q2 2021, Pala agreed to provide the Company with additional loans of up to $27 million (of which $19 million has been received) pursuant to a series of amendments and restatements of the 2021 Promissory Note (the “Amended and Restated Promissory Note”) on the same terms and conditions as the original 2021 Promissory Note. Further draws by the Company are subject to agreed use of proceeds and regulatory approval of the Amended and Restated Promissory Note.

2021 Credit Facility: On February 3, 2021, the Company entered a credit facility with Pala, for $15 million to be drawn by the Company (the “2021 Credit Facility”). The 2021 Credit Facility also provided $15 million under an accordion feature. The full $30 million has been drawn by the Company.

Senior Management Changes

Mike Ciricillo will be stepping down from the role of President and Chief Executive Officer of the Company, effective August 14, 2021.

Mike Brown will assume the role of Interim President and Chief Executive Officer. Mr. Brown has been a non-executive director of Nevada Copper since 2013 and has over 35 years of underground and open pit mining experience, including as Chief Operating Officer of De Beers Consolidated Ltd., where he was responsible for five operating mines. Mr. Brown has also managed a number of major projects, including the $750 million Finsch block 4 project, the $1.3 billion Venetia underground feasibility study, and a $200 million construction and commissioning of the Voorspoed mine.

Mr. Ciricillo will continue to provide support at the Pumpkin Hollow site for a transition period.

“The board of directors would like to thank Mr. Ciricillo for his contributions to the Company, including execution on ramp-up of the Underground Mine, and look forward to his ongoing support,” stated Chairman Mr. Gill. “The board of directors is pleased to welcome Mr. Brown as interim President and CEO and look forward to his leadership in that role.”

Q2 2021 Financial Statements

The Company has filed on SEDAR its condensed interim financial statements and the related management’s discussion and analysis for the quarter ended June 30, 2021. These documents are available on the Company’s website at www.nevadacopper.com and the Company’s SEDAR profile at www.sedar.com.

Qualified Persons

The technical information and data in this news release was reviewed by Greg French, C.P.G., and Norm Bisson, P.Eng., for Nevada Copper, who are non-independent Qualified Persons within the meaning of NI 43-101.

About Nevada Copper

Nevada Copper (TSX: NCU) is a copper producer and owner of the Pumpkin Hollow copper project. Located in Nevada, USA, Pumpkin Hollow has substantial reserves and resources including copper, gold and silver. Its two fully permitted projects include the high-grade underground mine and processing facility, which is now in the production stage, and a large-scale open pit project, which is advancing towards feasibility status.

NEVADA COPPER CORP. www.nevadacopper.com

Mike Ciricillo, President and CEO

For further information contact: Rich Matthews, Investor Relations Integrous Communications rmatthews@integcom.us +1 604 757 7179

Cautionary Language

This news release includes certain statements and information that constitute forward-looking information and forward-looking statements within the meaning of applicable Canadian and United States securities laws. All statements in this news release, other than statements of historical facts are forward-looking statements. Such forward-looking statements and forward-looking information specifically include, but are not limited to statements and information that relate to: Nevada Copper’s plans for the Project; negotiations with KfW regarding amendments to the Amended KfW Facility and waivers thereunder; the Company’s mine development, production and ramp-up plans and the expected timing, costs and results thereof; the need for additional funding; the resolution of hydrogeological issues; the impacts of the COVID-19 pandemic on the global economy and the Company; future ore and concentrate production rates; expected commencement of positive cash flow from operating activities; the ongoing exploration activities and the objectives and results thereof; and the other plans of Nevada Copper with respect to the exploration, development, construction and commercial production at the Underground Mine.

Forward-looking statements and information include statements regarding the expectations and beliefs of management. Often, but not always, forward-looking statements and forward-looking information can be identified by the use of words such as “plans”, “expects”, “potential”, “is expected”, “anticipated”, “is targeted”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes” or the negatives thereof or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking statements or information should not be read as guarantees of future performance and results. They are subject to known and unknown risks, uncertainties and other factors which may cause the actual results and events to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information.

Such risks and uncertainties include, without limitation, those relating to: the ability of the Company to complete the ramp-up of the Underground Mine within the expected cost estimates and timeframe; requirements for additional capital and no assurance can be given regarding the availability thereof; the impact of the COVID-19 pandemic on the business and operations of the Company; the state of financial markets; history of losses; dilution; adverse events relating to milling operations, construction, development and ramp-up, including the ability of the Company to address underground development and process plant issues and penetrate the dike at the Underground Mine; failure to obtain extensions under and amendments to the Amended KfW Facility; ground conditions; cost overruns relating to development, construction and ramp-up of the Underground Mine; loss of material properties; interest rates increase; global economy; limited history of production; future metals price fluctuations; speculative nature of exploration activities; periodic interruptions to exploration, development and mining activities; environmental hazards and liability; industrial accidents; failure of processing and mining equipment to perform as expected; labour disputes; supply problems; uncertainty of production and cost estimates; the interpretation of drill results and the estimation of mineral resources and reserves; changes in project parameters as plans continue to be refined; possible variations in ore reserves, grade of mineralization or recovery rates from management’s expectations and the difference may be material; legal and regulatory proceedings and community actions; accidents; title matters; regulatory approvals and restrictions; increased costs and physical risks relating to climate change, including extreme weather events, and new or revised regulations relating to climate change; permitting and licensing; volatility of the market price of the Company’s securities; insurance; competition; hedging activities; currency fluctuations; loss of key employees; other risks of the mining industry, as well as those risks discussed in the Company’s Management Discussion and Analysis in respect of the year ended December 31, 2020 and in the section entitled “Risk Factors” in the Company’s Annual Information Form dated March 18, 2021. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements and information. The forward-looking statements and information contained herein are based upon assumptions management believes to be reasonable, including, without limitation: no adverse development in respect of the property at the Project; no material changes to applicable laws; the ramp-up of operations at the Underground Mine in accordance with management’s plans and expectations; no worsening of the current COVID-19 related work restrictions; reduced impacts of the COVID-19 pandemic in the medium-term and long-term; no material adverse change to the price of copper from current levels; and the absence of any other factors that could cause actions, events or results to differ from those anticipated, estimated or intended. The forward-looking information and statements are stated as of the date hereof. Nevada Copper disclaims any intent or obligation to update forward-looking statements or information except as required by law. Readers are referred to the additional information regarding Nevada Copper’s business contained in Nevada Copper’s reports filed with the securities regulatory authorities in Canada. Although the Company has attempted to identify important factors that could cause actual actions, events, or results to differ materially from those described in forward-looking statements, there may be other factors that could cause actions, events or results not to be as anticipated, estimated or intended. For more information on Nevada Copper and the risks and challenges of its business, investors should review Nevada Copper’s filings that are available at www.sedar.com.

Nevada Copper provides no assurance that forward-looking statements and information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements or information. Accordingly, readers should not place undue reliance on forward-looking statements or information.

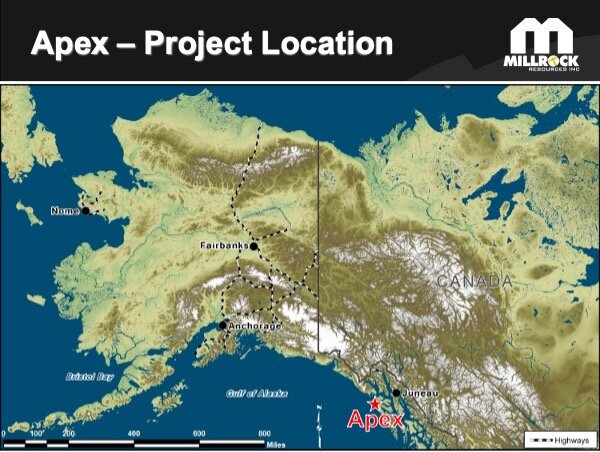

Millrock has executed an agreement with Coeur Explorations, Inc., a wholly-owned subsidiary of Coeur Mining, Inc. concerning claims controlled by Millrock at the Apex gold project, located approximately 70 kilometers from Juneau in Southeast Alaska.

Coeur Explorations may exercise an option to earn a 100% interest in the claims through staged payments and exploration expenditures.

Upon earning 100% interest, a Net Smelter Returns royalty with an advanced minimum royalty provision and buyback option will be granted to Millrock.

Initial exploration is underway; drill permits have been approved.

VANCOUVER, BRITISH COLUMBIA, August 12, 2021 – Millrock Resources Inc. (TSX-V: MRO, OTCQB: MLRKF) (“Millrock” or the “Company”) is pleased to announce that it has entered into an agreement with Coeur Explorations, Inc., a wholly-owned subsidiary of Coeur Mining, Inc. (“Coeur”), concerning the Apex gold project in Southeast Alaska. The project is located on Chichagoff Island, three kilometers north of the village of Pelican and 70 kilometers southwest of Juneau, Alaska.

Millrock President & CEO Gregory Beischer commented: “We are pleased to enter into this agreement with Coeur Explorations and will work diligently with their exploration team to explore the claims. From historic documents, we know that high-grade gold ore was previously mined, but there has never been a single exploratory hole drilled. It seems likely that the known high-grade gold-bearing quartz veins will continue along strike and in the down-dip direction. The claims have been completely dormant since the 1980s. We’ll start with surface geochemical sampling and detailed structural mapping this year and look to drill in 2022.”

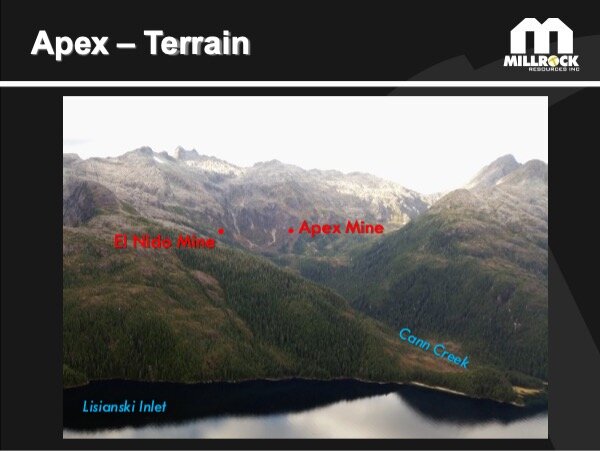

The Apex project targets high-grade, mesothermal, gold-bearing quartz vein deposits. The claims cover the former-producing Apex and El Nido gold mines which operated intermittently from the 1920s through to the 1940s and reportedly produced approximately 34,000 ounces of gold by underground mining methods. Nearly 1,200 meters of workings on four levels were used to extract ore (United States Geological Survey Alaska Resource Data File). Ore was hand-cobbed and milled on site. Surface exploration was done by WGM Inc. in the 1980s, but no drilling was done and the property has been dormant since. Millrock secured an option on the core claim group in 2016 from Apex El Nido Gold Mines Inc. Subsequently, Millrock staked surrounding lands, compiled information, and secured drilling permits. At surface, above the caved portal to the Apex Mine, a swarm of quartz veins can be observed over a width of more than 200 meters. Within the swarm, four thicker veins were the subject of the historic mining efforts. Geological and geochemical features suggest the vein system has continuity along strike to the northeast beneath Cann Creek, toward the tidewater of Lisianski Inlet, two kilometers away. The gold-bearing vein system has never been drill tested along strike or below the historic workings.

Figure 1. Apex Gold Project Location Map

Under the agreement, Millrock will assign its rights under the existing option agreement with Apex El Nido Gold Mines to Coeur Explorations. Coeur Explorations will be responsible for making cash payments and funding exploration expenditures to keep the option agreement with Apex El Nido Gold Mines in good standing. Millrock will execute exploration under a services agreement on behalf of Coeur. Coeur Explorations may determine not to proceed to exercise the option at any time, but if it makes all the payments and expenditures, it will vest with a 100% interest in the underlying claims. Upon exercising the option to purchase the Apex El Nido Gold Mine claims, Millrock will also transfer the claims it owns outright to Coeur Explorations, and the entire project will become subject to a net smelter returns (“NSR”) royalty in favour of Millrock. The royalty payable is a 2.5% NSR with an advanced minimum royalty (“AMR”) provision. Coeur Explorations may reduce the NSR to 1.0% by paying Millrock US$3.0 million. The initial AMR payment will be US$50,000 and will increase by US$50,000 annually until production occurs. AMR payments are deductible from NSR payments. The property will revert to Millrock in the event that Coeur elects to discontinue AMR payments.

Typical of Southeast Alaska, the terrain is steep and challenging, as pictured in Figure 2. The former producing Apex and El Nido mine entries are at tree level, approximately 360 meters above sea level. A soil sampling crew has been mobilized to the project and is presently working out of accommodations in Pelican, using boat access. The goal of the program is to trace the mineralized structure and refine vein locations in anticipation of a 2022 drilling program.

Figure 2. Apex Gold Project Terrain

Qualified Person The scientific and technical information disclosed within this document has been prepared, reviewed, and approved by Gregory A. Beischer, President, CEO, and a director of Millrock Resources. Mr. Beischer is a qualified person as defined in NI 43-101.

About Millrock Resources Inc. Millrock Resources Inc. is a premier project generator to the mining industry. Millrock identifies, packages, and operates large-scale projects for joint venture, thereby exposing its shareholders to the benefits of mineral discovery without the usual financial risk taken on by most exploration companies. The company is recognized as the premier generative explorer in Alaska, holds royalty interests in British Columbia, Canada, and Sonora State, Mexico, is a significant shareholder of junior explorer ArcWest Exploration Inc. and owns a large shareholding in Resolution Minerals Limited. Funding for drilling at Millrock’s exploration projects is primarily provided by its joint venture partners. Business partners of Millrock have included some of the leading names in the mining industry: Coeur Explorations, EMX Royalty, Centerra Gold, First Quantum, Teck, Kinross, Vale, Inmet and, Altius as well as junior explorers Resolution, Riverside, PolarX, and Felix Gold.

ON BEHALF OF THE BOARD “Gregory Beischer” Gregory Beischer, President & CEO

FOR FURTHER INFORMATION, PLEASE CONTACT: Melanee Henderson, Investor Relations Toll-Free: 877-217-8978 | Local: 604-638-3164 Twitter | Facebook | LinkedIn

Some statements in this news release may contain forward-looking information (within the meaning of Canadian securities legislation) including without limitation the intention to mount further exploration including drilling in 2022. These statements address future events and conditions and, as such, involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the statements.

VANCOUVER, British Columbia, Aug. 11, 2021 (GLOBE NEWSWIRE) — Skyharbour Resources Ltd. (TSX-V: SYH) (OTCQB: SYHBF) (Frankfurt: SC1P) (the “Company”) is pleased to announce that partner company Valor Resources Limited (“Valor”) has provided an update on results from the recently completed high-resolution airborne radiometric survey and the commencement of on-ground work at the Hook Lake Project (previously the North Falcon Point Project). The radiometric survey was completed in late July and covered the northeastern third of the Hook Lake Project including the Hook Lake/Zone S historical high-grade uranium occurrence. Numerous anomalies have been identified from the survey (see Figure 1 below). Total count radiometric anomalies were ranked with the highest priority anomalies being strongly correlated with the uranium channel count.

Hook Lake (Formally North Falcon Point) Project: https://skyharbourltd.com/_resources/projects/Falcon-Point-Project.jpg

The survey was flown by Special Projects Inc. (“SPI”) from Calgary, Alberta who are considered an industry-leading provider of high-resolution airborne radiometric surveying. SPI flew the radiometric survey that delineated Fission Uranium’s PLS boulder field which eventually led to the discovery of the high-grade uranium Triple R deposit.

The Hook Lake Project consists of 16 contiguous mining claims covering 25,846 hectares, located 60 km east of the Key Lake Uranium Mine in northern Saskatchewan. Skyharbour signed a Definitive Agreement with Valor Resources on the Hook Lake Uranium Project whereby Valor can earn-in 80% of the Project through $3,500,000 in total exploration expenditures, $475,000 in total cash payments over three years and an initial share issuance of 233,333,333 shares of Valor.

Highlights:

Airborne Radiometric survey highlights several new targets:

North-western area identified as new area of interest with a cluster of Priority 1 and 2 anomalies

Several other Priority 1 and 2 anomalies identified away from known historical occurrences

Hook Lake/Zone S historical high-grade uranium occurrence confirmed as Priority 1 target

On-ground work underway to:

Follow up and confirm historical uranium occurrences

Follow up areas of interest from the recent Airborne magnetic and VLF-EM survey

Follow up anomalies identified in recently completed Radiometric Survey

Of note is the cluster of Priority 1 and 2 anomalies identified in the northwest of the Project area where no uranium occurrences have previously been identified. The historical high-grade uranium occurrence at the Hook Lake (or Zone S) prospect was confirmed as a Priority 1 radiometric anomaly, with a Priority 2 anomaly located approximately 3km to the northeast along strike. There are additional Priority 1 and 2 anomalies away from known occurrences that require on-ground follow- up.

On-ground follow-up work has commenced which is being conducted by Dahrouge Geological Consulting Ltd. This work is focused on validating and developing the geological understanding of the historic uranium occurrences, such as the Hook Lake (or Zone S) prospect. The field crew will also follow-up on the new targets generated from the magnetic/VLF-EM survey completed in April and the priority anomalies identified from the recently completed airborne radiometric survey. A field crew supported by a helicopter is carrying out the field program over a period of 2-3 weeks.