Buy Precious Metals Here

Visit Bob Moriarty’s work at 321gold.com.

Proven Probable

Proven ProbableFrom CNN’s David Goldman

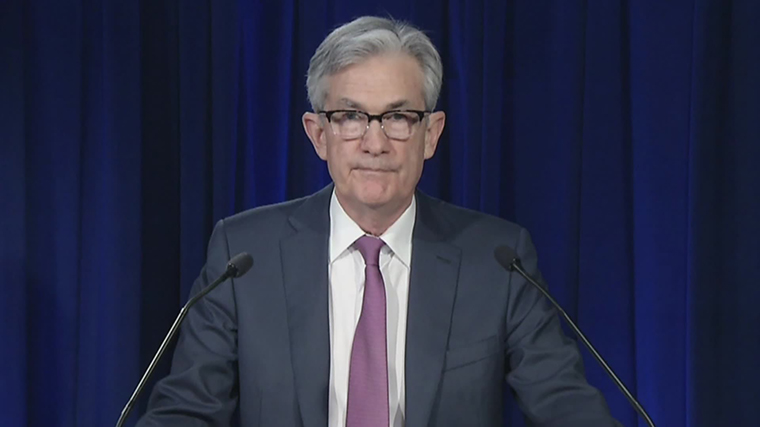

How bad is the coronavirus economy? The worst ever, says Fed Chairman Jerome Powell.

“We are going to see economic data for the second quarter that is worse than any data we have seen for the economy,” Powell said. “There are direct consequences of the disease and measures we are taking to protect ourselves from it.”

The recovery will be long and painful, but the economy could begin to bounce back significantly in the third quarter as businesses reopen, he added. While we won’t go back to pre-coronavirus levels for quite some time, the third quarter could provide some economic relief.

“We will enter the new phase — and we are just beginning to maybe do that — where we will begin formal measures that require social distancing will be rolled back, gradually, and at different paces in different parts of the country. And in time, during this period, the economy will begin to recover,” Powell said.

Powell also noted that unemployment shot higher for minorities in the United States —much faster than it has for white Americans.

Just a few months ago, the US labor market was the best-ever for minorities, Powell noted. Now, minorities are among the first to lose their jobs as stay-at-home orders have shuttered restaurants, movie theaters, retailers and many other businesses.

“It is heartbreaking, frankly, to see that all threatened now,” Powell said. “All the more need for our urgent response and also that of Congress, which has been urgent and large, and to do what we can to avoid longer run damage to the economy.”

Powell noted that people “who are least able to bear it have been the first to lose their jobs, and they have little cushion to protect themselves.

“That is a very big concern,” Powell said.

Transcript

https://youtu.be/j_vp9YyU9ck

Gregory Beischer the CEO of Millrock Resources sits down with Maurice Jackson of Proven and Probable to discuss the initial assay results on 64 North Project, which was temporarilty suspended due to the COVID-19. The initial findings produced all of the indicators that Millrock was seeking to identify with the exception of high-grade gold. The assay results represent approximately 25% of the proposed drill campaign. Find out why speculators, including ourselves, believe the value proposition of Millrock Resources has the potential to increase significantly.

INVESTOR INQUIRIES

Melanee Henderson

Investor Relations

Direct: 604-638-3164

Toll Free: 877-217-8978

Email: mhenderson@millrockresources.com

David Schectman, the founder of Miles Franklin Precious Metals Investments, has just released his latest musing that is a great reminder of why one should have an allocation towards physical precious metals. We are buying Silver and Platinum bullion, along with Numismatic Gold.

Contact me, Maurice Jackson, before you make your next physical precious metals purchase at 855.505.1900 or email maurice@milesfranklin.com

Transcript

https://youtu.be/ijMKSLRqTjI

In this exclusive interview Byron King of the Agora Finanical and newletter writer of “Whiskey and Gunpowder’ along with Dr. John-Mark Stuade of Riverside Resources, sit down with Maurice Jackson of Proven and Probable to discover the true price of gold and silver and the best value propositions in mining. We will address a number topics ranging from mining, bullion, exploration, currency creation, devaluation of the Federal Reserve Note, oil, and gas. Find out if gold will reach a new high!

Proven and Probable Where we deliver Mining Insights & Bullion Sales. I’m a licensed broker for Miles Franklin Precious Metals Investments. Where we provide unlimited options to expand your precious metals portfolio, from physical deliver, offshore depositories, and precious metals IRA’s. Call me directly at (855) 505-1900 or you may email maurice@milesfranklin.com.

Proven and Probable provides insights on mining companies, junior miners, gold mining stocks, uranium, silver, platinum, zinc & copper mining stocks, silver and gold bullion in Canada, the US, Australia and beyond.

David Schectman, the founder of Miles Franklin Precious Metals Investments, has just released his latest musing that is a great reminder of why one should have an allocation towards physical precious metals. We are buying Silver and Platinum bullion, along with Numismatic Gold.

Contact me, Maurice Jackson, before you make your next physical precious metals purchase at 855.505.1900 or email maurice@milesfranklin.com