Would Black Lives Matter, affirmative action policies, multi-culturalism and the demand for diversity have emerged had the concept of honor still been a part of the backbone of the West? Here are my thoughts:

On Investments

Recently, I had a linked conversation with Cory Fleck and Shad Marquitz about three companies that had not gone up with the general resources market.

Here are some more names with my limit buy-prices:

Gran Colombia Warrants (GCM.WT.B; C$3)

Silver Dollar (SLV; C$0.66)

Baru Gold (BARU; C$0.09)

Irving Resources (IRV; C$0.92)

Signature Resources (SGU; C$0.065)

Maritime Resources (MAE; C$0.13)

Aztec Minerals (AZT; C$0.27)

Montage Gold (MAU; C$0.65)

Newcore Gold (NCAU; C$0.54)

Valterra Resources (VQA; C$0.03)

You cannot have liberty in a society where a critical mass of people is not morally conscious. A society lacking moral consciousness will invariably produce goons and tyrants. Your perfect constitution will come to naught in such a society. So, the first step should always be to develop a critical mass of morally conscious people. That is what Capitalism & Morality strives to achieve, which, if our rulers allow, will be held on 30th July 2022.

Vancouver, British Columbia–(Newsfile Corp. – November 12, 2021) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX”) is pleased to report results for the quarter ended September 30, 2021 (“Q3-2021”). The Company’s filings for Q3-2021 are available on SEDAR at www.sedar.com, on the U.S. Securities and Exchange Commission’s website at www.sec.gov, and on EMX’s website at www.EMXroyalty.com. Financial results were prepared in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board.

HIGHLIGHTS FOR Q3-2021

Significant Acquisitions

EMX closed the acquisition of a portfolio of royalty interests and deferred payments from SSR Mining Inc. and certain of its subsidiaries (“SSR Mining“) (see EMX news release dated October 21, 2021). The Portfolio consists of 16 geographically diverse base and precious metals royalties, with four royalty assets at advanced stages of project development, and also includes US $18 million in future cash payments. EMX has paid US $33 million in cash and issued 12,323,048 common shares of the Company valued at US $32.5 million to SSR Mining. SSR Mining now owns an approximate 12% undiluted equity interest in EMX. EMX will also make deferred and contingent payments to SSR Mining of up to US $34 million if certain project advancement milestones are achieved.

EMX completed the acquisition of an effective 0.418% NSR royalty on the Caserones Copper-Molybdenum Mine located in northern Chile for US$34.1 million in cash (see EMX news release dated September 3, 2021). Caserones is a significant porphyry copper-molybdenum mining operation in a top tier mining jurisdiction. The Caserones acquisition brings immediate cashflow to EMX’s portfolio. Through the quarter end, EMX has realized an initial payment of US $951,000 from the second quarter (i.e., April – June) royalty distributions.

Financial Update

Dollar amounts are in CDN unless otherwise noted.

As at September 30, 2021, EMX ended the quarter with a working capital balance of $13,889,000 including cash and cash equivalents of $46,735,000, investments, strategic investments, and receivables and loan receivables totaling $27,034,000, and debt of $54,134,000.

To facilitate the Caserones and SSR royalty acquisitions, as well as to supplement working capital, the Company has entered into three financing transactions including a US$44,000,000 credit facility with Sprott Private Resource Lending II (Collector), LP, a Vendor-take-back note of US$7.85 million with SSR Mining, and the closing of the first tranche of a private placement for gross proceeds of $20,913,000.

For the three months ended September 30, 2021, EMX had revenue and other income of $1,504,000. EMX also received or accrued from its effective royalty interest on the Caserones mine its first quarterly payment of approximately US$950,000.

Royalty generation costs for the three months ended September 30, 2021 totaled $3,882,000 including share-based compensation of $45,000, of which the Company recovered $1,792,000 from partners.

General and administrative expenses totaled $1,807,000. The increase from Q3-2020 is largely the result of increased due diligence costs related to the Caserones acquisition and other prospective royalty assets.

For the three months ended September 30, 2021, the Company had a net loss from operations of $10,866,000. In addition to operating items noted above, included in net loss from operations was $759,000 in depletion, depreciation, and direct royalty taxes, and $1,206,000 in share-based compensation. Other items affecting net loss in Q3-2021 include a gain from the Company’s investments in associated entities of $1,138,000 primarily related to its effective royalty interest in the Caserones mine, a fair value loss on investments of $3,731,000, and a foreign exchange gain of $1,301,000. The Company also recorded impairment charges of $4,178,000 including $4,022,000 related to its investment in Rawhide Acquisition Holding LLC (“RAH” or “Rawhide”). The foreign exchange gain was primarily related to the Company holding cash and net assets denominated in US.

Operational Update

EMX’s royalty and mineral property portfolio totals over 280 projects on five continents. The following summarizes the work conducted in Q3-2021, as well as subsequent events, by the Company and its partners.

In North America, EMX received provisional payments of approximately US$641,000 from the sale of 364 gold ounces produced at the Leeville royalty property in Nevada’s Northern Carlin Trend. Leeville’s Q3 performance ensures that 2021 will be a year of increased payments due to robust production contributions from Carlin East and Four Corners. On the royalty generation front, EMX continued to evaluate and add new gold and copper projects to the portfolio by staking open ground. Partner companies continued to build value in the portfolio with their summer field exploration programs. In particular, partner Ridgeline Minerals’ successes at Swift resulted in the Carlin-type gold project being optioned to Nevada Gold Mines. Ridgeline also reported additional encouraging drill results from the Selena sediment-hosted silver-gold project.

EMX’s royalty and mineral asset portfolio in key mining districts of Ontario and Quebec, including the Red Lake camp, generated $75,000 in cash and fair value equity payments. EMX’s initiatives in Canada included staking prospective open ground, as well as expanding land positions at several existing properties.

In Serbia, Timok operator Zijin Mining Group Co. Ltd. (“Zijin”) received the final operating licenses and is in the trial production stage at the Upper Zone copper-gold project, which is covered by an EMX 0.5% NSR royalty. The Company filed an amended and restated Technical Report titled “NI 43-101 Technical Report – Timok Copper-Gold Project Royalty, Serbia” on SEDAR dated July 21, 2021 authored by Mineral Resource Management LLC.

In Fennoscandia, EMX executed an agreement for the sale of its Svärdsjö polymetallic project in Sweden to District Metals Corp. (TSX-V: DMX) for share equity, AAR payments, and retained royalty interests to EMX’s benefit. Subsequently EMX executed an option agreement for the sale of five battery metals projects in Sweden to Swedish Nickel Pty. Ltd. for share equity, AAR payments, retained royalty interests in the projects, work commitments and other consideration. As these six new deals were completed, partner companies continued to advance EMX’s royalty properties, which included further encouraging results from District’s drill program at the Tomtebo polymetallic project in Sweden’s Bergslagen mining district.

In Australia, the Company was granted the Copperhole Creek exploration license in the Georgetown Region of North Queensland. The Copperhole Creek project is available for partnership.

Corporate Update

EMX is monitoring developments regarding the ongoing coronavirus pandemic (“COVID-19”), with a focus on the jurisdictions in which the Company operates. EMX has implemented COVID-19 prevention, monitoring and response plans following the guidelines of international agencies and the governments and regulatory agencies of each country in which it operates. EMX’s priority is to safeguard the health and safety of its personnel and host communities, support government actions to slow the spread of COVID-19, and assess and mitigate the risks to business continuity. Although various levels of restrictions remain in place for some jurisdictions where the Company operates (e.g., travel restrictions, etc.), EMX’s field programs are up-and-running with in-country based staff.

Outlook

With the closing of the SSR and Caserones acquisitions, EMX continues to significantly strengthen its global portfolio of royalties. Gediktepe is one of several EMX royalty properties that are expected to commence production during late Q4, 2021 and early 2022. The others include the Timok development project in Serbia, where the Cukaru Peki high grade copper-gold deposit is being put into production by Zijin Mining Group Co. Ltd., and Balya North, a polymetallic Carbonate Replacement Deposit (“CRD”) in western Turkey being developed by Esan Eczacibaşi Endüstriyel Hammaddeler San. ve Tic. A.Ş., a private Turkish company.

EMX’s Leeville royalty in Nevada has delivered increased cash flows in recent months, with royalty production proceeds now being received from the Four Corners and Carlin East mining areas in addition to other areas on the royalty property. Together with cash flow already being received from its recently purchased Caserones copper-molybdenum royalty in Chile, EMX anticipates a significant increase in royalty revenue in 2022 from multiple assets that span four continents. See the EMX website (www.EMXroyalty.com) for further project and portfolio details.

The SSR royalty portfolio acquisition is an example of EMX’s corporate growth strategy, whereby the Company leveraged its in-region expertise to identify opportunities in jurisdictions where EMX already has a strategic presence, and hence a competitive advantage. This approach leads to value creation for the Company as well as synergies with existing EMX initiatives around the world. The Company is continuing with its assessments of royalty acquisition opportunities to continue growing the portfolio.

Meanwhile the Company’s royalty generation initiatives continued moving forward during Q3, which provided deal flow momentum moving into Q4. EMX partnered six projects in Fennoscandia for retained royalty interests, cash payments, and equity interests while continuing with field programs to add new projects to the royalty generation portfolio. In Australia, despite the challenges of COVID-19 lockdowns, the Company was successful in its efforts to add the Copperhole Creek project to the royalty generation portfolio. In the southwestern U.S., Regional Strategic Alliance (“RSA”) generative funds from South32 paid for identifying new copper properties for potential acquisitions. Elsewhere, multiple new precious-metals projects were staked by the Company in Idaho and Nevada which are now available for partnership. EMX is steadily building its generative portfolio in key mineral belts of the western U.S. and is now the third largest holder of mineral rights in Arizona and the second largest in Idaho. Fennoscandia, Australia, and the U.S. are stable exploration and mining jurisdictions, and EMX’s royalty generation assets provide prime opportunities for new partnerships.

EMX’s established partner companies continue to add value to the portfolio with encouraging drill results and other important advancements. In Fennoscandia, most notable were District’s drill success at Tomtebo (Norway) and further expansion of PGE-Ni-Cu mineralized zones at the Kaukua South project by Palladium One. In the western U.S. advancements included Ridgeline Minerals’ encouraging drill results from the Selena precious metals project on the Carlin Trend, and a joint venture agreement with Nevada Gold Mines for the Cortez Trend’s Swift gold project. EMX’s partners continued creating value on these assets, as well as others, at no cost to the Company. This trend of ongoing partner funded work expenditures is expected to carry forward, if not increase, going into Q4.

The Company will continue to strengthen its balance sheet through increased cashflows from royalties, deferred royalty payments, sale of investments, and other income. As part of this effort to strengthen working capital, in November 2021, the Company completed the first tranche of a $21.45 million private placement by the issuance of 6,337,347 units at $3.30 each for gross proceeds of $20.9 million. Increases to EMX’s treasury will allow it to continue project generation and royalty acquisition activities, thereby further building shareholder value (See Liquidity and Capital discussions below).

QUALIFIED PERSONS

Michael P. Sheehan, CPG, a Qualified Person as defined by NI 43-101 and employee of the Company, has reviewed, verified, and approved the above technical disclosure on North America. Eric P. Jensen, CPG, a Qualified Person as defined by NI 43-101 and employee of the Company, has reviewed, verified, and approved the above technical disclosure on Significant Acquisitions, Serbia, Fennoscandia, and Australia.

ABOUT EMX

EMX is a precious, base, and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and the TSX Venture Exchange under the symbol EMX, as well as on the Frankfurt exchange under the symbol 6E9. See www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 979-666 Dave@EMXroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended September 30, 2021 (the “MD&A”), and themost recently filed Annual Information Form (“AIF”) for the year ended December 31, 2020, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

Thunder Bay, Ontario–(Newsfile Corp. – November 12, 2021) – Kesselrun Resources Ltd. (TSXV: KES) (OTC Pink: KSSRF) (“Kesselrun” or the “Company“) is pleased to announce a non-brokered private placement for gross proceeds of up to C$3,000,000 from the sale of any combination of flow-through units of the Company (the “FT Units“) at a price of C$0.175 per FT Unit and FT Units to be sold to charitable purchasers (the “Charity FT Units“) at a price of C$0.21 per Charity FT Unit (collectively, the “Offering“). The FT Units and Charity FT Units shall be collectively referred to as the “Offered Securities“. Red Cloud Securities Inc. is acting as a finder in connection with the Offering.

Each FT Unit and Charity FT Unit shall be comprised of one common share of the Company to be issued as a “flow-through share” within the meaning of the Income Tax Act (Canada) (each, a “FT Shares“) and one half of one common share purchase warrant (each full warrant, a “Warrant“). Each Warrant shall be exercisable into one common share of the Company (each, a “Warrant Share“) at a price of C$0.23 at any time on or before the date which is 24 months after the closing date of the Offering.

The Company intends to use the proceeds from the offering for the exploration of the Company’s Huronian Gold Project in northwestern Ontario. Proceeds from the sale of FT Shares will be used to incur “Canadian exploration expenses” as defined in subsection 66.1(6) of the Income Tax Act and “flow through mining expenditures” as defined in subsection 127(9) of the Income Tax Act (“Qualifying Expenditures“). Such proceeds will be renounced to the subscribers with an effective date not later than December 31, 2021, in the aggregate amount of not less than the total amount of gross proceeds raised from the issue of Offered Securities.

The Offering is scheduled to close on or about November 30, 2021 and is subject to certain conditions, including, but not limited to, the receipt of all necessary regulatory and other approvals, including the approval of the listing of the FT Shares and Warrant Shares on the TSX Venture Exchange (the “TSXV“). The FT Shares and Warrant Shares will be subject to a hold period of four months and one day in accordance with applicable securities laws.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy the Offered Securities, nor shall there be any sale of the Offered Securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction. The Offered Securities being offered will not be, and have not been, registered under the United States Securities Act of 1933, as amended, and may not be offered or sold within the United States or to, or for the account or benefit of, a U.S. person.

About Kesselrun Resources Ltd.

Kesselrun Resources is a Thunder Bay, Ontario-based mineral exploration company focused on growth through property acquisitions and discoveries. Kesselrun’s management team possesses strong geological and exploration expertise in Northwest Ontario. For more information about Kesselrun Resources, please visit www.kesselrunresources.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Forward-Looking Statements – Certain information set forth in this news release may contain forward-looking statements that involve substantial known and unknown risks and uncertainties. These forward-looking statements are subject to numerous risks and uncertainties, certain of which are beyond the control of Kesselrun, including, but not limited to the impact of general economic conditions, industry conditions, volatility of commodity prices, dependence upon regulatory approvals, the execution of definitive documentation, the availability of financing and exploration risk. Readers are cautioned that the assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be placed on forward-looking statements.

NOT FOR DISTRIBUTION TO UNITED STATES NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

Battery metal demand is rising, and the trend will continue

New properties are in demand- Producers provide leverage to the metal prices, and exploration companies turbocharge the gearing- Location is critical

Lithium Americas (LAC) looks to pick up a property

Nevada Copper (NEVDF)- The trend is your friend, and increasing demand for EVs supports a continuation of the rally

Noram Lithium (NRVTF)- An undervalued battery metal play in Nevada, a desirable jurisdiction

In real estate, a property’s value always reflects its location. Any real estate professional understands that the three leading value factors are location-location-location.

Commodity producers face many regional issues. Raw materials can occur in local regions where political or economic forces make extraction challenging. The cost of production reflects local tax, royalty, logistical, and other factors.

Over the past year, the ascent of metals prices has caused many of the world’s leading producers to scramble to find new mining projects to meet the growing demand. One of the world’s leading diversified commodity producers, BHP is currently in talks with Ivanhoe Mines to acquire part of the Western Foreland exploration area in the Democratic Republic of the Congo (DRC). While DRC is the largest copper producer in Africa with the most substantial reserves, the country has a long history of corruption that has impeded its growth. The DRC is not an ideal location for mining companies, but the growing need for new output has put BHP in a position to consider the project. It takes up to ten years to bring a new copper mine into production, and producers are scouring the earth for projects that will meet the increasing demand.

Goldman Sachs called copper “the new oil” because of its role in decarbonization. Three-month LME copper was trading at the $9,518 per ton level on November 5, with the December COMEX copper futures at the $4.3430 per pound level. Goldman projects that copper prices could rise to the $15,000 per ton level by 2025, putting COMEX copper futures north of the $6.80 per pound level.

Meanwhile, lithium is another commodity that is experiencing growing demand. The success of addressing climate change through decarbonization relies on ample supplies of battery metals that can replace fossil fuels.

While BHP is looking to the DRC for new copper deposits, other mining and exploration companies are developing battery metal deposits. Friendlier and less challenging jurisdictions are likely to attract significant premiums over the coming months and years.

In the US, Nevada, the silver state, has a long history as one of the most favorable mining jurisdictions on the earth. When it comes to location, it does not get much better than Nevada.

Battery metal demand is rising, and the trend will continue

Climate change is not a US issue; it is a worldwide trend. Addressing climate change involves replacing the hydrocarbons that currently power the world with alternative, renewable energy sources. While batteries power only around one percent of the cars on roads today, the demand for EVs is growing by leaps and bounds. Hertz recently announced they are purchasing 100,000 Tesla model-3 EVs in a $4.2 billion deal. EVs will make up 20% of the Hertz fleet by the end of 2022. Hertz will also install thousands of charging stations in its locations in the US and Europe.

EV’s require twice the copper as internal combustion engines. The batteries require other metals and minerals including, lithium, nickel, cobalt, zinc, aluminum, manganese, graphite, and potassium. Tesla’s batteries currently use lithium-nickel-cobalt-aluminum chemistry. However, the company is working on a set of cobalt-free or reduced batteries drawing on lithium-iron-phosphate technology and chemistries that rely more heavily on nickel. The three-month nickel price on the London Metals Exchange closed 2020 at the $16,600 per ton level. As of November 4, the price was over $19,400 after reaching over $20,500 during the year. Copper futures on COMEX may have corrected from the May 2021 all-time high at nearly $4.90 per pound, but they remain appreciably higher than at the end of 2020.

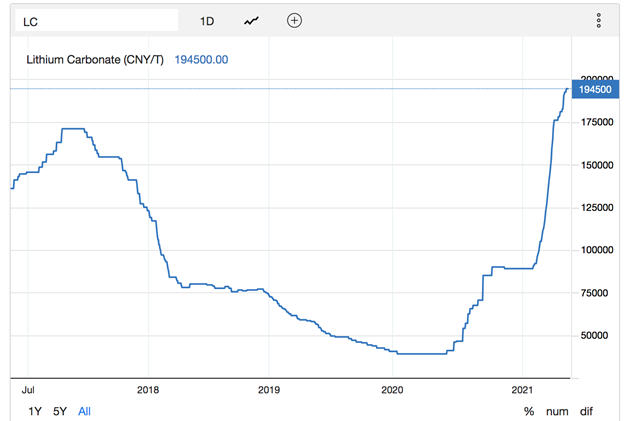

Source: CQG

The monthly chart shows that copper closed 2020 at the $3.52 level. At the $4.3430 per pound level in early November 2021, copper futures were over 23% higher. The price action in the lithium carbonate market has been even more bullish.

The chart shows the rise from below $33,000 per ton in 2020 to the current price at the $194,500 level, an increase of nearly six times. Lithium’s ascent is more like a cryptocurrency than a commodity as the demand for the metal for EV production grows.

New properties are in demand- Producers provide leverage to the metal prices, and exploration companies turbocharge the gearing- Location is critical

Mining companies make substantial capital investments to extract raw materials from the earth’s crust. The leading mining companies profit handsomely when market prices exceed production costs, creating leverage. Mining companies often outperform the commodities they produce on the upside but underperform when prices decline.

Meanwhile, exploration companies provide even more leverage. Since rewards are always a function of the risks, companies that search for commodities tend to experience incredible gains when they find them and begin production or sell the properties to the more established mining companies that can take projects to the next production and processing levels.

The mining industry reflects economies of scale. The leading companies like BHP, Rio Tinto, Anglo American, Glencore, and others have made significant capital investments and spread production risks over a diversified portfolio of mining properties. They tend to allow exploration companies to make the finds and then take the mining properties to the next steps.

When it comes to investing, exploration companies can offer attractive returns that often outpace the underlying commodity and the established miners on a percentage basis. If the BHP’s offer leverage, exploration companies turbocharge that gearing.

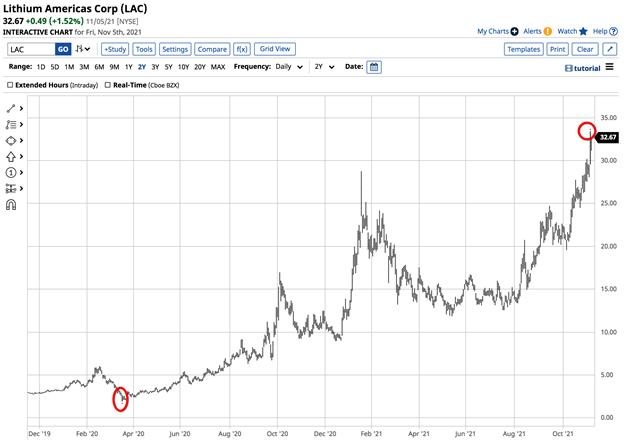

Lithium Americas (LAC) looks to pick up a property

Lithium Americas Corporation (LAC) operates as a resource company in the United States. The company explores for lithium deposits. LAC owns interests in the Cauchari-Olaroz Project in the Jujuy province of Argentina and the Thacker Pass project in north-western Humboldt County, Nevada. Thacker Pass recently increased its Phase 1 capacity to target 40,000 tpa lithium carbonate.

LAC announced it submitted an unconditional offer to Millennial Lithium Corporation to acquire all of the outstanding shares for approximately $400 million.

Source: Barchart

The chart shows LAC’s ascent from a low of $1.92 per share in March 2020 to its most recent high of $33.42 on November 4. At the $32.67 per share level, LAC’s market cap was over $3.919 billion. An average of over five million shares changes hands each day. Lithium has been a hot commodity that has moved nearly six times since 2020. LAC shares have moved over seventeen times higher over the period as the successful mining company turbocharged the commodity’s percentage gain.

Nevada Copper (NEVDF)- The trend is your friend, and increasing demand for EVs supports a continuation of the rally

Nevada Copper is an exploration company in the silver state of Nevada. The company owns a 100% interest in the Pumpkin Hollow property that contains copper, gold, and silver reserves. The most recent operations update highlighted accelerated stope turnover rates, management team changes that strengthened the company, productivity improvements, and processing of ore averaging approximately 1.5% copper delivered to the mill. Since the May high, copper’s price has dropped at nearly $4.90 per pound on the nearby COMEX futures contract. NEVDF is an exploration company, so its share performance tends to outperform the commodity on the upside and underperform on the downside. Copper rose from $3.52 per pound at the end of 2020 to a high of $4.8985 in May or 39.2%. On November 5, the price was at the $4.3430 level, 11.3% below the May peak. NEVDF shares closed 2020 at the $1.14 level.

Source: Barchart

The chart highlights that NEVDF shares reached a high of $2.71 when copper peaked and traded at 67.00 cents per share on November 5. NEVDF shares rallied by 137.7% and from the end of 2020 to the May 2021 high and were 75.3% lower than the peak as of November 5. Like many exploration companies, NEVDF turbocharged the price action in copper, outperforming the metal on the upside and underperforming on the downside.

As the demand for copper will rise over the coming years, and Goldman Sachs expects the price to increase dramatically, now could be the perfect time to consider this exploration company.

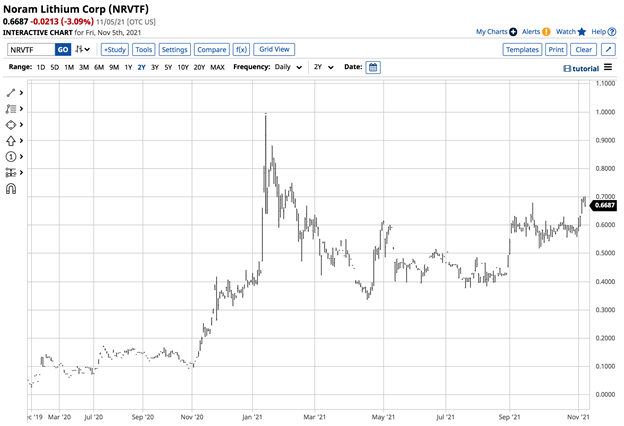

Noram Lithium (NRVTF)- Another battery metal play in Nevada, a desirable jurisdiction

Norman Lithium (NRVTF) is an exploration company that develops mineral properties in the United States. The company owns interests in the Zeus Lithium Project in Clayton Valley, Nevada. Noram’s property is next door to Albemarle Corporation’s (ALB) Silver Peak Lithium Mine in Nevada.

A 70% increase in measured and indicated resources

A 369% increase in inferred resources

Deposits near the surface, reducing production costs

The potential to increase the deposit size via deeper drilling

An environmentally friendly footprint

A Preliminary Economic Assessment (PEA) in the coming weeks – Advancing the project closer to its’ production target

At the 67.15 cents per share level, NRVTF has a market cap at the $50.701 million level. An average of 56,780 shares changes hands each day.

Source: Barchart

The chart shows NRVTF shares closed at the 40.26 cents level on December 31, 2020. At 66.87 on November 5, they were 66.1% higher. NRVTF shares reached a high of 98.78 cents on January 14, 2021, which is the stock’s current technical target. The shares have traded in a bullish trend since mid-April 2021.

With the spotlight on lithium, Norman could be an excellent exploration company to consider. Success in the Zeus project could attract interest from companies like Lithium Americas Corporation (LAC) that is currently buying Millennial Lithium Corporation’s shares for $400 million, nearly eight times higher than NRVTF’s current market cap.

Exploration companies are risky, but the potential for substantial rewards always involves an elevated risk level. Meanwhile, Nevada Copper and Noram Lithium have location on their sides as Nevada is a highly desirable mining jurisdiction in a world hungry for copper and lithium supplies.

Written By: Andrew Hecht, on behalf of Maurice Jackson of Proven and Probable.

Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein, or any security in any jurisdiction in which such an offer would be unlawful under the securities laws of such jurisdiction.

Vancouver, British Columbia – (November 11, 2021) – Rover Metals Corp. (TSXV: ROVR) (OTCQB: ROVMF) (“Rover” or the “Company”) has received an update from ALS Canada and expects to be fully reported on the results of its Summer 2021 Phase 2 Drill Program, at its Cabin Gold Project, by the end of November. The Company anticipates issuing a news release on the results in early December.

About the Cabin Gold Project In September 2020, Rover kicked-off its first exploration drilling program at the historic Cabin Gold Project. The exploration program included both confirmation and expansion drilling of historical high grade gold drill intercepts in the “Arrow Zone” area of the historic Bugow Iron Formation. The Bugow Iron Formation is the controlling structure for the gold mineralization on the property and is over 15 km in at or near surface length. In Q4-2020, the Company reported an intersection of 32 meters of continuous gold averaging 13.6 grams per ton Au from the Arrow Zone. Rover’s 2020 expansion drilling included the discovery of what it believes to be a primary gold bearing ore shoot at the Arrow Zone. The Arrow Zone remains open at depth, underneath Cabin Lake, and is only accessible for expansion drilling in the winter months. Rover’s 2020 drill program was the initial step towards confirming and expanding the historic 100,000 tons at 0.30 Oz/ton Au* historic resource estimate, reported for the Arrow Zone, towards a NI 43-101 compliant mineral resource estimate. The Arrow Zone will see expansion drilling commencing in Q1-2022, as soon as the ice drill pads and ice road to site have been constructed.

In July 2021, Rover commenced a Phase 2 Exploration Program at the Cabin Gold Project. The goal of the Phase 2 Exploration Program was the discovery and definition of new, near surface, gold bearing zones along the Bugow Iron Formation. The Company focussed on five known historic targets areas: (1) the Beaver; (2) the Andrew South; (3) the Andrew North; (4) the Camp South; and (5) Camp North. As of the date hereof, the Company is still waiting on results of its summer exploration program. Any new discoveries will form part of the Company’s Phase 3 Winter Exploration Program slated to begin in Q1-2022.

(*) As per Section 2.4 of NI 43-101, Aber Resources Ltd. reported a mineral inventory (that does not compare to the current CIM Definitions Standards mineral resource categories) of 100,000 tons at 0.30 ounces per ton gold at the Cabin Lake Gold Zone on the north limb of the folded Bugow Iron Formation in their 1986 and 1987 annual reports. The parameters used for the resource calculation are unknown. These results are relevant as to delineate a larger zone of gold mineralization at the Cabin Lake Gold Zone, but further drilling is needed to bring that up to CIM Definition Standards. The reader is cautioned that a Qualified Person has not done sufficient work to classify the historical estimates as current mineral resources and Rover Metals is not treating the historical estimates as current mineral resources. Technical information in this news release has been approved by Raul Sanabria, M.Sc., P.Geo., Technical Advisor and shareholder of Rover Metals Corp. and a Qualified Person for the purposes of National Instrument 43-101.

About Rover Metals Rover is a precious metals exploration company specialized in North American precious metal resources, that is currently advancing the gold potential of its existing projects in the Northwest Territories of Canada (60th parallel). The Company commenced Phase 2 Exploration at its Cabin Gold Project in the summer of 2021, and is planning to commence Phase 3 Exploration in Q1-2022.

ON BEHALF OF THE BOARD OF DIRECTORS “Judson Culter” Chief Executive Officer and Director

For further information, please contact: Email: info@rovermetals.com Phone: +1 (778) 754-2617

Statement Regarding Forward-Looking Information This news release contains statements that constitute “forward-looking statements.” Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Rover’s actual results, performance or achievements, or developments in the industry to differ materially from the anticipated results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. There can be no assurance that such statements be prove to be accurate. Actual results and future events could differ materially from those anticipated in such statements, and readers are cautioned not to place undue reliance on these forward-looking statements. Any factor could cause actual results to differ materially from Rover’s expectations. Rover undertakes no obligation to update these forward-looking statements in the event that management’s beliefs, estimates or opinions, or other factors, should change.

THE FORWARD-LOOKING INFORMATION CONTAINED IN THIS NEWS RELEASE REPRESENTS THE EXPECTATIONS OF THE COMPANY AS OF THE DATE OF THIS NEWS RELEASE AND, ACCORDINGLY, IS SUBJECT TO CHANGE AFTER SUCH DATE. READERS SHOULD NOT PLACE UNDUE IMPORTANCE ON FORWARD-LOOKING INFORMATION AND SHOULD NOT RELY UPON THIS INFORMATION AS OF ANY OTHER DATE. WHILE THE COMPANY MAY ELECT TO, IT DOES NOT UNDERTAKE TO UPDATE THIS INFORMATION AT ANY PARTICULAR TIME EXCEPT AS REQUIRED IN ACCORDANCE WITH APPLICABLE LAWS.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OF THIS RELEASE.

VANCOUVER, BC / ACCESSWIRE / November 10, 2021 / Granite Creek Copper Ltd. (TSXV:GCX)(OTCQB:GCXXF) (“Granite Creek” or the “Company“) is pleased to announce the retention of SGS Geological Services (‘SGS”) to provide an updated National Instrument 43-101 mineral resource estimate on the Company’s Carmacks copper-gold-silver deposit in the Minto Copper Belt located in central Yukon, Canada.

Granite Creek will be incorporating drilling completed in 2017, 2020 and 2021 into an updated resource estimate which will build on the existing NI 43-101 compliant resources last published in 20171,2. Resource expansion drilling completed in 2021 consisted of 22 diamond drill holes primarily targeted at sulfide mineralization in Zones 1, 2000S and 13 and is expected to add to the existing sulfide resource (see news release dated October 28, 2021).

Table 1. Current Mineral Resource Estimate on the Carmacks Copper Project

Category

Tonnes (000)

Cu (%)

Au (g/t)

Ag (g/t)

Oxide & Transition Mineralization

Measured

6,484

0.86

0.41

4.24

Indicated

9,206

0.97

0.36

3.80

M&I

15,690

0.94

0.38

3.97

Inferred

913

0.45

0.12

1.90

Sulphide Mineralization

Measured

1,381

0.64

0.19

2.17

Indicated

6,687

0.69

0.17

2.34

M&I

8,068

0.68

0.18

2.33

Inferred

8,407

0.63

0.15

1.99

About SGS Geological Services

SGS Geological services has a very strong team, with valuable experience, known, renown and respected in the international mining industry. The team has considerable experience in estimation and modeling of deposits of all types and practical and theoretical experience having realized hundreds of assessments for clients. A multidisciplinary group of qualified persons with a strong understanding of the disclosure requirements for Mineral Resources set out in the NI 43-101 Standards of Disclosure for Mineral Projects (2016), CIM Definition Standards – For Mineral Resources and Mineral Reserves (2014) and a strong understanding of the CIM Estimation of Mineral Resources & Mineral Reserves Best Practice Guidelines 2019.

Resource Road Update

On November 8th the Yukon government announced the following road construction update that directly effects Granite Creek’s Carmacks Project.

“Whitehorse based company Pelly Construction has been awarded the contract for the Carmacks Bypass Project, a $29.6 million investment to construct a new road and bridge near Carmacks. This project is a key component under the Yukon Resource Gateway Program and a collaborative effort between the Government of Yukon and Little Salmon/Carmacks First Nation.

The project, which is anticipated to be complete in 2024, will allow industrial vehicles to bypass the community of Carmacks, creating an enhanced and safer flow of traffic for residents. It will also improve access to mining activities while enabling the Little Salmon/Carmacks First Nation to benefit from contracting, education and training benefits associated with the project.

The Yukon Resource Gateway Program improves infrastructure to Yukon’s most mineral-rich areas. The Carmacks Bypass project is jointly funded by Canada and the Yukon and is the first project to be awarded under the program.”

Granite Creek President & CEO, Tim Johnson, commented, “We are very pleased to have engaged with a top calibre firm like SGS on this key milestone in the Company’s relatively short history. With the amount of highly targeted new drilling we have completed, we anticipate a robust update to the existing resource estimate and that this, along with the mine planning and trade-off studies being developed by Sedgman and Mining Plus, will have a significant impact on the project economics. In our continuing development of Carmacks, the recent announcement by the Yukon government of the start of construction on the Carmacks Bypass is extremely good news. The incremental improvement in access represented by this road upgrade is welcomed and this, combined with an updated resource estimate, will pave the way for and even more extensive exploration program in 2022.”

[1] JDS Energy and Mining. Feb 9, 2017. NI 43-101 Preliminary Economic Assessment Technical Report on the Carmacks Project, Yukon, Canada. Contained metal based on 23.76 million tonnes of NI 43-101 compliant resources in the Measured and Indicated categories grading 0.85% Cu, 0.31 g/t Au, 3.14 g/t Ag.

[2] Arseneau Consulting Services, 2016 Independent Technical Report on the Carmacks Copper Project, Yukon, Canada.

About Granite Creek Copper

Granite Creek, a member of the Metallic Group of Companies, is a Canadian exploration company focused on the 176 square kilometer Carmacks project in the Minto copper district of Canada’s Yukon Territory. The project is on trend with the high-grade Minto copper-gold mine, operated by Minto Explorations Ltd, to the north, and features excellent access to infrastructure with the nearby paved Yukon Highway 2, along with grid power within 12 km. More information about Granite Creek Copper can be viewed on the Company’s website at www.gcxcopper.com.

Ms. Debbie James, P.Geo., a qualified person for the purposes of National Instrument 43-101, has reviewed and approved the technical disclosure contained in this news release.

Forward-Looking Statements

This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Granite Creek Copper believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Granite Creek Copper and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

YERINGTON, Nev., Nov. 10, 2021 (GLOBE NEWSWIRE) — Nevada Copper Corp. (TSX: NCU) (OTC: NEVDF) (FSE: ZYTA) (“Nevada Copper” or the “Company”) is pleased to announce that it has filed a preliminary short form prospectus with the securities commissions in all provinces of Canada, except Quebec, in connection with a marketed public offering (the “Offering”) of units (the “Units”) of the Company seeking to raise aggregate gross proceeds of approximately C$75,000,000. The Company’s largest shareholder, Pala Investments Limited (“Pala”), has committed to purchase, on a private placement basis, an aggregate number of Units to maintain its current shareholding percentage in the Company (the “Private Placement”) after giving effect to both the Offering and the Private Placement (the “Purchased Units”) at the price per Purchased Unit determined in connection with the Offering.

Each Unit will consist of one common share of the Company (each a “Common Share”) and one-half of one common share purchase warrant (each full warrant, a “Warrant” and collectively the “Warrants”). Each Warrant will be exercisable for one Common Share at any time for a period of 18 months following closing of the Offering. Final pricing of the Units, the Warrant exercise price and the determination of the number of Units to be sold pursuant to the Offering will be determined following marketing. The Offering will be conducted on an overnight marketed “best efforts” basis by a syndicate of underwriters to be formed and led by Scotiabank, as lead underwriter and sole-bookrunner (collectively, the “Underwriters”).

The Company intends to grant the Underwriters an option, exercisable in whole or in part, at the sole discretion of the Underwriters, at any time for a period of 30 days from and including the closing of the Offering, to purchase from the Company up to an additional 15% of the Units sold under the Offering, on the same terms and conditions of the Offering to cover over-allotments, if any, and for market stabilization purposes (the “Over-Allotment Option”). The Over-Allotment Option may be exercised by the Underwriters to purchase additional Units, Common Shares, Warrants or any combination thereof.

As announced on October 12, 2021, the Company entered into amendments to its amended and restated credit facility (the “KfW Facility”) with its senior project lender, KfW-IPEX Bank, for a significant deferral and extension of its debt facilities, providing substantially greater balance sheet flexibility and support for the completion of the ramp-up of its underground mining operations and subsequent advancement of its open pit project and broader property exploration targets. The Company expects the effectiveness of the deferral and extensions agreed under the KFW Facility to occur upon the closing of the Offering and the Private Placement.

Additionally, in connection with the Offering, the Company and Pala have agreed to amend the existing non-binding term sheet as previously announced on October 12, 2021 to provide for a binding commitment (the “Binding Term Sheet”) in respect of certain amendments to the credit facility entered into between Company and Pala on February 3, 2021 (as amended, the “Amended Credit Facility”). The Amended Credit Facility will consolidate all outstanding loans owing to Pala and the maturity date will be extended by two years from 2024 to 2026. Net proceeds raised in the Offering will replace the new tranche of up to US$41 million that was contemplated by the non-binding term sheet, which will be a significant improvement to the Company’s balance sheet. See the Company’s October 12, 2021 news release for additional details on the terms of the Amended Credit Facility.

The Company intends to use the net proceeds of the Offering for: (i) the development and ramp-up of the underground mine at the Company’s Pumpkin Hollow project (the “Underground Mine”); (ii) the repayment of bridge loans advanced under the promissory note issued by the Company to Pala on October 1, 2021, as amended and restated on November 1, 2021; and (iii) general corporate purposes. The net proceeds from the Private Placement will be utilized to retire and prepay an equivalent portion of the existing loans outstanding under the promissory note issued by the Company to Pala on June 10, 2021, as amended and restated (the “JunePromissory Note”), such that Pala will continue to maintain its current shareholding percentage in the Company after giving effect to the Offering and the Private Placement. The balance of the June Promissory Note will be consolidated and extended under the Amended Credit Facility in accordance with the Binding Term Sheet.

The Offering is expected to close on or about November 29, 2021, or such other date as the Company and the Underwriters may agree. Closing of the Offering is subject to customary closing conditions, including, but not limited to, the execution of an underwriting agreement and the receipt of all necessary regulatory approvals, including the approval of the securities regulatory authorities and the Toronto Stock Exchange. The Private Placement is conditional on the closing of the Offering.

The preliminary short form prospectus is available on SEDAR at www.sedar.com. The Company has also today filed on SEDAR its condensed interim financial statements and the related management’s discussion and analysis for the quarter ended September 30, 2021.

This news release does not constitute an offer to sell or a solicitation of an offer to buy any of securities in the United States. The securities have not been and will not be registered under the U.S. Securities Act or any state securities laws and may not be offered or sold within the United States or to U.S. Persons unless registered under the U.S. Securities Act and applicable state securities laws or an exemption from such registration is available.

About Nevada Copper

Nevada Copper (TSX: NCU) is a copper producer and owner of the Pumpkin Hollow copper project. Located in Nevada, USA, Pumpkin Hollow has substantial reserves and resources including copper, gold and silver. Its two fully permitted projects include the high-grade Underground Mine and processing facility, which is now in the production stage, and a large-scale open pit project, which is advancing towards feasibility status.

NEVADA COPPER CORP. www.nevadacopper.com

Randy Buffington, President and CEO

For further information contact: Rich Matthews, Investor Relations Integrous Communications rmatthews@integcom.us +1 604 757 7179

Cautionary Language

This news release includes certain statements and information that constitute forward-looking information within the meaning of applicable Canadian securities laws. All statements in this news release, other than statements of historical facts are forward-looking statements. Such forward-looking statements and forward-looking information specifically include, but are not limited to, statements that relate to the completion of the Offering and the Private Placement and the timing in respect thereof, the entering into of the Amended Credit Facility and the use of proceeds of the Offering and the Private Placement.

Forward-looking statements and information include statements regarding the expectations and beliefs of management. Often, but not always, forward-looking statements and forward-looking information can be identified by the use of words such as “plans”, “expects”, “potential”, “is expected”, “anticipated”, “is targeted”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes” or the negatives thereof or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking statements or information should not be read as guarantees of future performance and results. They are subject to known and unknown risks, uncertainties and other factors which may cause the actual results and events to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information.

Such risks and uncertainties include, without limitation, those relating to: the ability of the Company to complete the ramp-up of the Underground Mine within the expected cost estimates and timeframe; requirements for additional capital and no assurance can be given regarding the availability thereof; the impact of the COVID-19 pandemic on the business and operations of the Company; the state of financial markets; history of losses; dilution; adverse events relating to milling operations, construction, development and ramp-up, including the ability of the Company to address underground development and process plant issues; failure to obtain the effectiveness of extensions under and amendments to the KfW Facility; failure to enter into the Amended Credit Facility; ground conditions; cost overruns relating to development, construction and ramp-up of the Underground Mine; loss of material properties; interest rates increase; global economy; limited history of production; future metals price fluctuations; speculative nature of exploration activities; periodic interruptions to exploration, development and mining activities; environmental hazards and liability; industrial accidents; failure of processing and mining equipment to perform as expected; labor disputes; supply problems; uncertainty of production and cost estimates; the interpretation of drill results and the estimation of mineral resources and reserves; changes in project parameters as plans continue to be refined; possible variations in ore reserves, grade of mineralization or recovery rates from management’s expectations and the difference may be material; legal and regulatory proceedings and community actions; accidents; title matters; regulatory approvals and restrictions; increased costs and physical risks relating to climate change, including extreme weather events, and new or revised regulations relating to climate change; permitting and licensing; volatility of the market price of the Company’s securities; insurance; competition; hedging activities; currency fluctuations; loss of key employees; other risks of the mining industry as well as those risks discussed in the Company’s Management’s Discussion and Analysis in respect of the year ended December 31, 2020 and in the section entitled “Risk Factors” in the Company’s Annual Information Form dated March 18, 2021. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements or information. The forward-looking information or statements are stated as of the date hereof. Nevada Copper disclaims any intent or obligation to update forward-looking statements or information except as required by law. Readers are referred to the additional information regarding Nevada Copper’s business contained in Nevada Copper’s reports filed with the securities regulatory authorities in Canada. Although the Company has attempted to identify important factors that could cause actual actions, events, or results to differ materially from those described in forward-looking statements, there may be other factors that could cause actions, events or results not to be as anticipated, estimated or intended. For more information on Nevada Copper and the risks and challenges of its business, investors should review Nevada Copper’s filings that are available at www.sedar.com.

Nevada Copper provides no assurance that forward-looking statements and information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements or information. Accordingly, readers should not place undue reliance on forward-looking statements or information.

Vancouver, British Columbia–(Newsfile Corp. – November 10, 2021) – Playfair’s (TSXV: PLY) (FSE: P1J1) (OTC Pink: PLYFF) extensive drill program on its large (201 square kilometers) 100% RKV Copper Project in South Central Norway has successfully completed seven short holes totaling 385.1 metres to test the Storboren target identified by using a combination of Artificial Intelligence (CARDS) and Mobile Metal Ion (MMI) geochemistry. Drilling at Rødalen was reported in Playfair’s October 8, 2021 News Release.

At Storboren drillhole STB-21-07 encountered at least 6 sulphide zones ranging from 20 cm to 1.5 metres wide within a previously unknown ultramafic intrusive. Sulphides are mostly pyrrhotite with lesser pyrite and chalcopyrite.

NQ core with sulphides in drillhole STB-21-007 at Storborenhttps://s.yimg.com/rq/darla/4-9-0/html/r-sf-flx.html

Samples have been cut and sent for analysis. Preparation will be at the Malå, Sweden ALS laboratory with analysis at the Loughrea, Ireland ALS laboratory. ALS Minerals is internationally recognized as the global leader in providing geochemical sample preparation, analytical procedures, and data management solutions, with its European hub lab based in Loughrea, Co. Galway.

A total of 99 samples have been submitted and comprised 36 core samples from Rødalen, 60 core samples from Storboren and 3 rock samples.

Playfair will consider future exploration at Rødalen and Storboren once analytical results have been received. Drill testing of the remaining five targets will resume in the Spring.

Promin AS, a Trondheim-based consultancy with extensive experience in the Norwegian Mining industry, provides logistical support and experienced geologists. Helge Rushfeldt assisted greatly in the start-up of the drill program. Kjell Nilsen, one of Norway’s most experienced field geologists who discovered Nussir, Norway’s largest known copper deposit, and Jonas Dombrowski are directly supervising the drilling, core logging and analysis.

Geologists Kjell Nilsen and Jonas Dombrowski examining drillcore

The man portable drill team is supervised by Canadian drillers (No Limit Diamond Drilling) for Arctic Drilling (based in Finnmark). Local “Muskelgutta” (Muscle Guys) have risen to the challenge of moving the man portable drill. Local community support is greatly appreciated.

In keeping with Playfair’s intent to minimise the impact of its exploration on the natural environment Playfair is using a lightweight drilling machine which can be disassembled and hand-carried to the drill sites. Although lightweight the drill is capable of drilling to 150m depth using BQ sized rods (36.5 mm or 1.437 inches core diameter) and to 100m depth using NQ sized rods (47.8mm or 1.872 inches core diameter).

All seven drill targets show compelling coherent MMI Cu anomalies with multiple MMI Cu values greater than 6,000 ppb. The highest value recorded was 53,300 ppb MMI Cu. A short MMI Report by SGS states that values greater than 6,000 ppb MMI Cu “are likely to be associated with weathering copper sulphides”.

Hillside drill collar location for SB-21-07 at Storboren

Overall management and execution of Playfair’s RKV drilling program is provided by Ronacher McKenzie Geoscience Inc., an independent consulting group, who, as part of their supervision, will ensure that appropriate quality assurance/quality control (QA/QC) protocols are in place. RMG follows the Canadian Institute of Mining, Metallurgy and Petroleum’s (CIM) Best Practices.

In Norway, Reidar Gaupås, Playfair’s representative, continues to assist Playfair within the local community and enhance Playfair’s profile in Norway.

The drill targets are MMI (Mobile Metal Ion) copper anomalies discovered by sampling target areas generated by Windfall Geotek (TSXV: WIN) (OTCQB: WINKF) using their proprietary Computer Aided Resources Detection System (CARDS).

The seven drill targets were described previously: Storboren (November 07, 2019, and December 05, 2019, News Releases), Sæterfjellet, (January 06, 2021, News Release), Kletten North and Kletten South (January 28, 2021, News Release), Røstvangen Northeast and Røstvangen Southwest (February 17, 2021, News Release) and Rødalen (March 11, 2021, News Release).

A presentation on the drilling plans can be found at this direct link or on Playfair’s website.

The technical contents of this release were approved by Greg Davison, PGeo, a qualified person as defined by National Instrument 43-101.

The road to a cleaner environment includes electric vehicles. Electric vehicles need copper, nickel, and cobalt. There is no green future without minerals.

Forward-Looking Statements: This Playfair Mining Ltd News Release may contain certain “forward-looking” statements and information relating to Playfair which are based on the beliefs of Playfair management, as well as assumptions made by and information currently available to Playfair management. Such statements reflect the current risks, uncertainties and assumptions related to certain factors including, without limitations, exploration and development risks, expenditure and financing requirements, title matters, operating hazards, metal prices, political and economic factors, competitive factors, general economic conditions, relationships with vendors and strategic partners, governmental regulation and supervision, seasonality, technological change, industry practices, and one-time events. Should any one or more of these risks or uncertainties materialize or change, or should any underlying assumptions prove incorrect, actual results and forward-looking statements may vary materially from those described herein.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

VANCOUVER, BC, Nov. 9, 2021 /PRNewswire/ – Dolly Varden Silver Corporation (“Dolly Varden” or the “Company“) (TSXV: DV) (OTC: DOLLF), is pleased to announce that Andrew Hamilton, P.Geo. has joined the Company as Senior Geologist.

Dolly Varden Silver Corp Logo (CNW Group/Dolly Varden Silver Corp.)

Mr. Hamilton is an exploration geologist with over 30 years of mineral exploration experience, primarily in British Columbia, Nunavut, the Yukon and Mexico, with a focus on gold and copper-gold projects. He brings additional grass roots to advanced stage mineral exploration experience to Dolly Varden with a focus on drill program design and management, mineral resource modelling and estimation, QAQC and data management.

Andrew has been part of technical teams of multiple successful explorers that have transitioned from exploration to production as well as company sale, including Wheaton River Minerals’ Golden Bear Mine, Cumberland Resources’ Meadowbank Project and IDM Mining’s Red Mountain Project. He was mostly recently the Exploration Manager for White Gold Corp. for their Yukon projects.

As an Independent Qualified Person, he has co-authored numerous NI 43-101 Reports and Resource Estimates, as well as audits and reviews of producing Companies Mineral Resources and Reserves and QA/QC. Mr. Hamilton has been lauded in the mining industry for his conservative and balanced approach.

Shawn Khunkhun, Dolly Varden’s CEO, commented: “I am pleased to welcome Andrew to Dolly Varden. His advanced exploration experience in the Golden Triangle, expertise in the design of drill programs for resource delineation and expansion, as well as critical project evaluation skills will complement our current technical team and benefit the Company as we look to dramatically grow in the next two years.”

Mr. Hamilton holds a Bachelor of Science degree in geological sciences from the University of British Columbia and a Bachelor of Arts degree in anthropology from the University of Victoria. He is a registered professional geoscientist (P.Geo.) in the province of British Columbia.

About Dolly Varden Silver Corporation

Dolly Varden Silver Corporation is a mineral exploration company focused on exploration in northwestern British Columbia. Dolly Varden has two projects, the namesake Dolly Varden silver property and the nearby Big Bulk copper-gold property. The Dolly Varden property is considered to be highly prospective for hosting high-grade precious metal deposits, since it comprises the same structural and stratigraphic setting that host numerous other high-grade deposits (Eskay Creek, Brucejack). The Big Bulk property is prospective for porphyry and skarn style copper and gold mineralization similar to other such deposits in the region (Red Mountain, KSM, Red Chris).

Forward Looking Statements

This release may contain forward-looking statements or forward-looking information under applicable Canadian securities legislation that may not be based on historical fact, including, without limitation, statements containing the words “believe”, “may”, “plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”, “expect”, “potential” and similar expressions. Forward-looking statements involve known and unknown risks, uncertainties, and other factors which may cause the actual results, performance, or achievements of Dolly Varden to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. Forward looking statements or information relates to, among other things, completion of the Offering, Exchange approval of the Offering, the use of proceeds with respect to the Offerings, the results of previous field work and programs and the continued operations of the current exploration program, interpretation of the nature of the mineralization at the project and that that the mineralization on the project is similar to Eskay and Brucejack, results of the mineral resource estimate on the project, the potential to grow the project, the potential to expand the mineralization, the planning for further exploration work, the ability to de-risk the potential exploration targets, and our beliefs about the unexplored portion of the property. These forward-looking statements are based on management’s current expectations and beliefs but given the uncertainties, assumptions and risks, readers are cautioned not to place undue reliance on such forward-looking statements or information. The Company disclaims any obligation to update, or to publicly announce, any such statements, events or developments except as required by law.

For additional information on risks and uncertainties, see the Company’s most recently filed annual management discussion & analysis (“MD&A”), which is available on SEDAR at www.sedar.com. The risk factors identified in the MD&A are not intended to represent a complete list of factors that could affect the Company.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this news release.