Tim Johnson, Granite Creek CEO stated: “Granite Creek management strongly believes that the value of the combined project is significantly greater than the sum of the parts, especially in terms of the potential for expansion of existing high-grade copper-gold resources in this productive yet underexplored district. At Carmacks many zones remain open along trend and at depth especially in the sulfide domain and the work done at Carmacks North has laid the groundwork for resource development. This is a major milestone for the Company, and we look forward to unlocking the potential of the southern half of the high-grade Minto Copper Belt.”

About the Minto Copper Belt

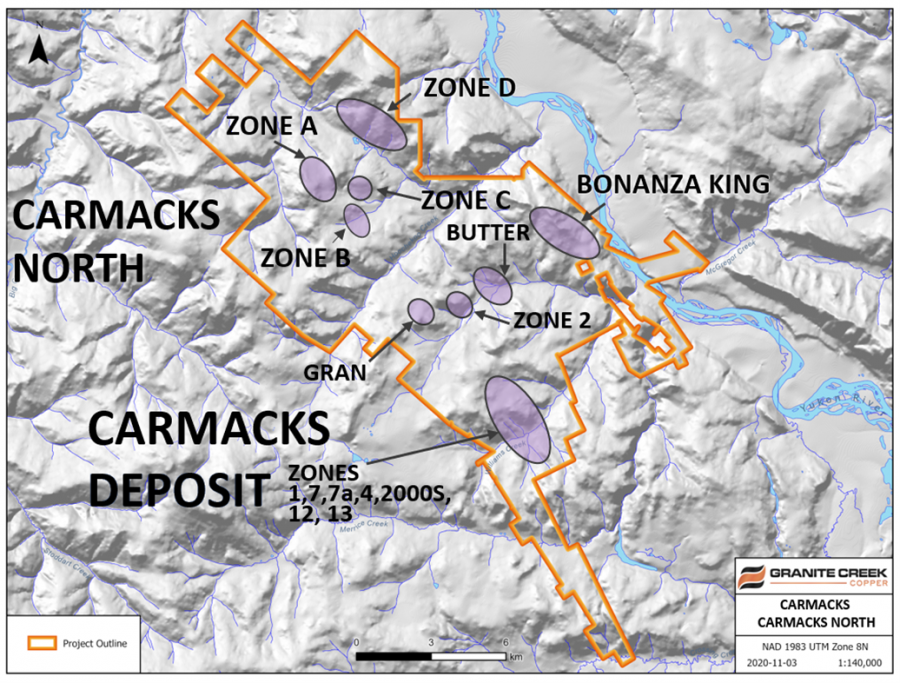

The Minto Copper Belt is a 180-kilometer-long by 60-kilometer-wide belt of intrusion-related, high-grade Cu-Au-Ag deposits within the Dawson Range in the central Yukon Territory of Canada. The District is host to Pembridge’s operating Minto Mine and Granite Creek’s Carmacks and Carmacks North Project. At Carmacks copper mineralization is contained in foliated to gneissic material, generally similar to the Minto mine.

FOR FURTHER INFORMATION PLEASE CONTACT:

Granite Creek Copper Ltd. Timothy Johnson, President & CEO Telephone: 1 (604) 235-1982 Toll Free: 1 (888) 361-3494 E-mail: info@gcxcopper.com Website: www.gcxcopper.com

Nevada Copper (TSX: NCU) is a copper producer and owner of the Pumpkin Hollow copper project. Located in Nevada, USA, Pumpkin Hollow has substantial reserves and resources including copper, gold and silver. Its two fully permitted projects include the high-grade underground mine and processing facility, which is now in the production stage, and a large-scale open pit project, which is advancing towards feasibility status.

“The collection of this data and refinement of conductor locations within the identified corridors will ensure that our highest priority targets are being targeted and tested effectively,” said Azincourt Exploration Manager, Trevor Perkins.

To find out more about Skyharbour Resources Ltd. (TSX-V: SYH) visit the Company’s website at www.skyharbourltd.com.

Bob Moriarty the founder of http://www.321gold.com/ sits down with Maurice Jackson to discuss politics, precious metal investing, and resource stocks in a common-sense approach that can literally increase your chances of success financially. If your willing to hear a perspective on politics that doesn’t favor Democrats or Republicans this interview is for you. Bob pulls no punches and requires the listener to engage, research, and question. We will also discuss the gold price, silver price, and Basel 3 along with the Bank of International Settlements. If you are a first-buyer or a gold, silver stacker, and you want to find out which is the best precious metal purchase right now among gold, silver, or platinum then this interview is for you! Do you enjoy speculating in resource stocks? Bob will address several value propositions that his attention and deserve consideration for your portfolio.

What to learn more about the companies we referenced today? Find out right here!

Novo Resources: (TSX.V: NVO | OTCQX: NSRPF) Website: https://www.novoresources.com/ Our Interview with Novo Resources: https://youtu.be/C_bWxp1cCLs

Lion One Metals: (TSX.V: LIO | OTCQX: LOMFL) Website: https://liononemetals.com/

Are you interested in investing in gold, silver, or platinum? Do you enjoy silver stacking? At Miles Franklin, we offer Junk Silver, Silver Bullion in Private Minted, and Government Minted Bullion Coins directly from the US Mint. Place an order: 855.505.1900 or email: maurice@milesfranklin.com

*Silver Stacking should not be a religion, use the ratio’s to your advantage*

Proven and Probable Where we deliver Mining Insights & Bullion Sales. I’m a licensed broker for Miles Franklin Precious Metals Investments (https://www.milesfranklin.com/contact/) Where we provide several options to expand your precious metals portfolio, from physical delivery, offshore depositories, and precious metals IRA’s. Call me directly at (855) 505-1900 or you may email: maurice@milesfranklin.com.

Proven and Probable provides insights on mining companies, junior miners, gold mining stocks, uranium, silver, platinum, zinc & copper mining stocks, silver and gold bullion in Canada, the US, Australia, and beyond.

No, we will not cover technical analysis or uranium stocks in this interview.

Tim Johnson, President and CEO, stated, “We are pleased to be welcoming the Copper North shareholders to Granite Creek and look forward to delivering details on the expanded potential of the south portion of the high grade Minto District once the transaction is closed. Additional updates with respect to the 2020 field exploration and drilling programs are expected over the coming weeks.”

Dolly Varden Silver Corporation is a mineral exploration company focused on exploration in northwestern British Columbia. Dolly Varden has two projects, the namesake Dolly Varden silver property and the nearby Big Bulk copper-gold property. The Dolly Varden property is considered to be highly prospective for hosting high-grade precious metal deposits, based on its similar structural and stratigraphic setting to other high-grade deposits (Eskay Creek, Brucejack) in the region. The Big Bulk property is prospective for porphyry and skarn style copper and gold mineralization similar to other such deposits in the region (Red Mountain, KSM, Red Chris).

Mike Ciricillo, Chief Executive Officer of Nevada Copper, stated: “We are pleased with our operations progress in Q3 following recommencement of concentrate production in August. The Processing Plant performance continues to deliver on-spec concentrate with increased throughput rates, concentrate grade, recovery, and volume. By the end of Q4 we look forward to continuing our operations improvements and completing the materials handling system, a key to accelerating ramp-up to commercial production in Q1 2021.”

For further information contact: Rich Matthews, Investor Relations Integrous Communications rmatthews@integcom.us +1 604 355 7179