Vancouver, British Columbia–(Newsfile Corp. – September 4, 2025) – Elemental Altus Royalties Corp. (TSXV: ELE) (OTCQX: ELEMF) (“Elemental Altus“) and EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (“EMX“, and together with Elemental Altus, the “Companies“) are pleased to announce that the Companies have entered into a definitive arrangement agreement dated September 4, 2025 (the “Arrangement Agreement“) whereby Elemental Altus will acquire all of the issued and outstanding common shares of EMX (the “EMX Shares“) pursuant to a court-approved plan of arrangement (the “Transaction“). The Merged Company (the “Merged Company“) will continue under the new name Elemental Royalty Corp.

Concurrently with and in support of the Transaction, Tether Investments S.A. de C.V. (“Tether“) and Elemental Altus have entered into a subscription agreement dated September 4, 2025 (the “Tether Subscription Agreement“) pursuant to which, among other things, Tether has agreed to purchase approximately 75 million Elemental Altus Shares at a price of C$1.84 per share for aggregate gross proceeds of US$1001 million (the “Tether Concurrent Financing“).

The Merged Company will have 16 producing royalties contributing to a projected approximate adjusted revenue2 of US$80 million in 2026, positioning the Merged Company as a new mid-tier streaming and royalty company.

Transaction Highlights and Strategic Rationale:

- Top Quality, Globally Diversified Portfolio:

- Creation of peer-leading revenue generating royalty company: combined revenue guidance of US$70 million in 2025 and analyst consensus revenue of US$80 million in 20263, underpinned by strong growth visibility;

- Gold focused portfolio: adjusted revenue relating to a commodity split of 67% precious metals and 33% base metals on a latest quarter revenue basis providing exposure to record gold prices;

- Strengthened asset portfolio: anchored by four cornerstone royalties with world-class operators;

- Enhanced portfolio diversification: exposure to 16 paying royalties and 200 total royalties providing a balanced foundation of immediate cash flow and long-term upside;

- Meaningful scale:

- Larger, well capitalized entity: with lower cost of capital, positioned to pursue further accretive royalty opportunities in the market;

- Graduating to the mid-tier: materially higher combined revenue than the junior royalty companies, filling a gap in the market left by recent industry consolidation;

- Increased trading liquidity: combined trading liquidity and expected indexation demand to help close valuation gap with peers;

- Poised for Future Growth:

- Complementary management expertise: unites Elemental Altus’ proven track record of accretive royalty acquisitions with EMX’s disciplined royalty generation and acquisition capabilities to create a best-in-class leadership team;

- Royalty generation business: a unique differentiator offering low cost, organic growth;

- Demonstrated shareholder support: Certain shareholders of EMX (including management) who hold approximately 23% of the outstanding EMX Shares have entered into voting support agreements and the Tether Concurrent Financing emphasizes strong confidence in the strategy and long-term vision of the Merged Company, and provides significant financial capacity to the Merged Company; and

- Clear path forward: the Merged Company will be listed on the TSX Venture Exchange (“TSX-V“) under the ticker “ELE” with plans to pursue a US listing prior to the closing of the Transaction.

Elemental Altus and EMX will hold a joint conference call and webcast for investors and analysts on September 5, 2025, at 8am PT/11 am ET to discuss the Transaction. Details are provided at the end of this press release.

Frederick Bell, CEO of Elemental Altus, commented:

“This transaction establishes one of the world’s premier gold focused emerging streaming and royalty companies, bringing together two complementary portfolios in a compelling combination. Elemental Altus’ portfolio, with a strategic emphasis on royalty acquisition, and with more than 75% of revenue associated with gold producing mines, is complemented by EMX’s revenue generating portfolio paired with their royalty generation business. The combination of two business that have each delivered over 17% compound annual growth rates in share price since their inception creates an enlarged company that is exceptionally well-placed to continue to grow in an accretive manner for shareholders. The support from Tether in the form of a US$100 million placement as well as the existing cashflow generation, provides the ability to pursue further valuable growth through acquisitions of the best opportunities in the sector. Both Elemental Altus’ and EMX’s shareholders will benefit from our cornerstone assets, greater scale, diversification, growth profile and trading liquidity.”

David Cole, CEO of EMX, commented:

“The merger of Elemental Altus and EMX represents a superb opportunity to combine two royalty companies with accelerating revenue streams and a shared mindset of financial discipline in the pursuit of growth. The ethos of EMX from the founding of the company has been to expose shareholders to the ever increasing value of mineral rights around the world. We believe that growing a diverse portfolio of royalties is the most effective way to accomplish this goal. Royalties are phenomenal financial instruments that leverage commodity price exposure and the asymmetric upside of exploration success. The integration of EMX and Elemental’s portfolios are expected to greatly enhance shareholder value through increased liquidity, capital availability and importantly, discovery optionality across an expanded portfolio.”

Juan Sartori, Executive Chairman of Elemental Altus, commented:

“Tether’s recent investment in Elemental Altus was based on its strategy of increasing gold exposure. We believed Elemental Altus was the ideal vehicle to execute on this strategy due to the company’s strong foundation of assets and disciplined approach to investments. We are even more excited about the Merged Company’s future following the combination with EMX, creating a platform for growth that is unmatched in the junior royalty space and allowing us to accelerate into the mid-tier royalty space. The Merged Company will have the cashflow generation and expertise to deploy capital on royalties and streams that continue to add value for all shareholders.”

Concurrently with the Transaction, Elemental Altus will complete the previously-approved consolidation of all of the issued and outstanding common shares of Elemental Altus (the “Elemental Altus Shares“) at a ratio of one (1) post-consolidation Elemental Altus Share for every 10 pre-consolidation Elemental Altus Shares (the “Consolidation“). Additional details of the timing for the Consolidation will be provided by Elemental Altus in a subsequent press release.

Under the terms of the Arrangement Agreement, shareholders of EMX will receive (a) 0.2822 Elemental Altus Shares for each EMX Share held immediately prior to the effective time of the Transaction (the “Effective Time“) if the Consolidation is completed prior to the Effective Time; or (b) 2.822 Elemental Altus Shares for each EMX Share, if the Consolidation is not completed prior to the Effective Time (the “Consideration“). Upon completion of the Transaction, including the Tether Concurrent Financing, existing Elemental Altus shareholders and former EMX shareholders will own approximately 51% and 49% of the outstanding common shares of the Merged Company, respectively, on a fully diluted basis. The implied market capitalization of the Merged Company is estimated at US$933m4.

Benefits for EMX Shareholders

- Immediate upfront premium to near all-time high closing share price of 21.5% based on 20-day volume-weighted average prices and 9.8% based on spot prices5

- Accretive to near term cash flow per share

- Offers material ownership in combined larger cash flowing company with near term cash contributions from Elemental Altus’ portfolio

- Diversification to Tier-1 Australian gold producing and near-producing assets

- Exposure to gold focused royalty revenue from cornerstone assets, including Karlawinda

- Optionality through Elemental Altus’ development royalty portfolio

- Continued financial support of Tether for further acquisitions

Benefits for Elemental Altus Shareholders

- Immediately accretive to net asset value (NAV) on a per share basis6

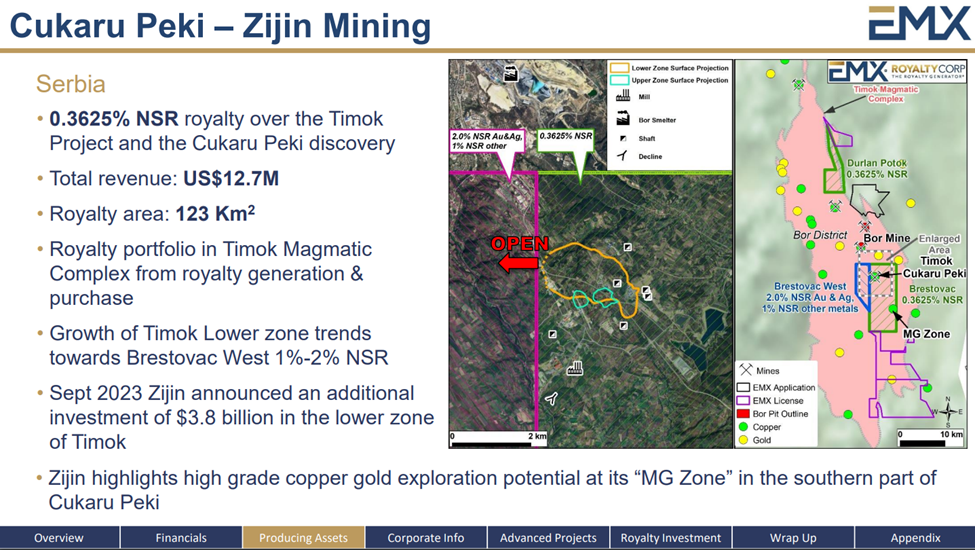

- Provides exposure to unique long-life Timok royalty

- Triples ownership of flagship Caserones royalty

- Diversifies risk profile adding cornerstone assets in North America, South America and Europe

- Combination with high-quality technical team will improve deal sourcing and organic origination of new royalties for low cost

- Enhanced trading liquidity and capital markets exposure through size and planned US listing, providing access to new investors including index inclusion

Transaction Details

Pursuant to the terms and conditions of the Arrangement Agreement, EMX shareholders will receive (a) 0.2822 Elemental Altus Shares for each EMX Share held immediately prior to the Effective Time if the Consolidation is completed prior to the Effective Time; or (b) 2.822 Elemental Altus Shares for each EMX Share, if the Consolidation is not completed prior to the Effective Time as the Consideration.

The Consideration implies a premium of 9.8% based on the closing prices of the Elemental Altus Shares and EMX Shares, respectively, on the TSX-V on September 4, 2025, and a premium of 21.5% based on the 20-day volume-weighted average price of the Elemental Altus Shares and EMX Shares, respectively, on the TSX-V and US Exchanges as of September 4, 2025. The Consideration implies a total equity value for EMX of US$4567 million on a basic basis.

The Transaction will be effected by way of a court-approved plan of arrangement under the Business Corporations Act (British Columbia). The Transaction will require the approval of at least (i) 66 2/3% of the votes cast at a special meeting of shareholders of EMX (the “EMX Special Meeting“); and (ii) if, and to the extent, required under applicable Canadian securities laws, a majority of the votes cast at a the EMX Special Meeting, excluding the votes attached to EMX Shares held by persons required to be excluded pursuant to Multilateral Instrument 61-101 – Protection of Minority Security Holder in Special Transactions (“MI 61-101“).

Upon completion of the Transaction, including the Tether Concurrent Financing, existing Elemental Altus and former EMX shareholders are expected to own approximately 51% and 49% of the Merged Company, respectively, on a basic basis.

Certain officers and directors and shareholders of EMX who hold approximately 23% of the outstanding EMX Shares have entered into voting support agreements pursuant to which they have agreed, among other things, to vote their EMX Shares in favour of the Transaction.

Upon completion of the Transaction, the Merged Company will be renamed Elemental Royalty Corp. and remain headquartered in Vancouver, British Columbia. The Board of Directors will be comprised of three representatives from Elemental Altus and two representatives from EMX. Juan Sartori will continue as Executive Chairman and David Cole will serve as CEO of the Merged Company, while Frederick Bell will assume the role of President and COO.

In addition to approval of the EMX shareholders, completion of the Transaction is subject to approval of the Elemental Altus shareholders for the Tether Concurrent Financing (as described below), TSX-V, regulatory and court approvals and other customary closing conditions for Transactions of this nature. Further, the completion of the Transaction is subject to the conditional approval of the listing of the Elemental Altus Shares on a US stock exchange and the completion of the Tether Concurrent Financing. Any such US listing of the common shares of the Merged Company is subject to the Merged Company meeting the quantitative and qualitative requirements to list on a US stock exchange. The Arrangement Agreement includes customary deal protection provisions, including reciprocal non-solicitation and right to match provisions, and an approximately C$15.8 million termination fee, payable under certain circumstances.

None of the securities to be issued pursuant to the Transaction have been or will be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any state securities laws, and any securities issuable in the Transaction are anticipated to be issued in reliance upon available exemptions from such registration requirements pursuant to Section 3(a)(10) of the U.S. Securities Act or other available exemptions and applicable exemptions under state securities laws. This press release does not constitute an offer to sell or the solicitation of an offer to buy any securities.

The full details of the Transaction will be described in the Companies’ respective management information circulars to be prepared in accordance with applicable securities legislation and made available in connection with the special meetings.

Tether Concurrent Financing

Concurrently with and in support of the Transaction, Elemental Altus has entered into the Tether Subscription Agreement, pursuant to which, among other things, Elemental Altus and Tether have agreed to complete the Tether Concurrent Financing. Proceeds from the Tether Concurrent Financing will be used to repay EMX’s credit facility, fund royalty acquisitions (including to pay the purchase price for Elemental Altus’ two recently announced royalty acquisitions, or to repay its credit facility to the extent drawn for that purpose) and provide capital for the Merged Company so that it is fully unlevered post-completion.

Tether is an insider and control person of the Company, and therefore the Tether Concurrent Financing constitutes a related party transaction as defined under MI 61‐101. The shareholders of Elemental Altus must approve each of (a) the Tether Concurrent Financing pursuant to the requirements of MI 61-101 (the “Elemental Altus Financing Resolution“), (b) Tether as a “Control Person” of Elemental Altus pursuant to policies of the TSX-V (the “Elemental Altus Control Person Resolution“); and (c) the change of Elemental Altus’ name to Elemental Royalty Corp. (the “Elemental Altus Name Change Resolution” and collectively, the “Elemental Altus Resolutions“).

The Elemental Altus Financing Resolution will require the approval of at least a simple majority of the votes cast at a special meeting of shareholders of Elemental Altus (the “Elemental Altus Special Meeting“), excluding the votes attached to Elemental Altus Shares held by Tether and any other persons required to be excluded pursuant to MI 61-101. The Elemental Altus Control Person Resolution will require the approval of at least a simple majority of the votes cast at the Elemental Altus Special Meeting, excluding votes attached to Elemental Altus Shares held by the Tether and its associates and affiliates. The formal valuation requirement under MI 61-101 does not apply to the Tether Concurrent Financing as Elemental Altus has relied on the exemption therefrom contained at section 5.5(b) of MI 61-101.

Certain officers and directors and shareholders of Elemental Altus who hold approximately 40% of the outstanding Elemental Altus Shares have entered into voting support agreements pursuant to which they have agreed, among other things, to vote their Elemental Altus Shares in favour of the Elemental Altus Resolutions.

The Tether Concurrent Financing is conditional on the approval of the Transaction at the EMX Special Meeting. The Tether Concurrent Financing is also subject to approval of the TSX-V, including Elemental Altus fulfilling the requirements of the TSX-V. The Elemental Altus Shares issued under the Tether Concurrent Financing will be subject to a four month and one day hold period, pursuant to securities laws in Canada, and have not been and will not be registered under the U.S. Securities Act of 1933, as amended, or any applicable securities laws of any state of the United States and may not be offered or sold in the United States absent registration or an applicable exemption from such registration requirements. This press release shall not constitute an offer to sell or the solicitation of an offer to buy any securities of Elemental Altus, nor shall there be any offer or sale of any securities of Elemental Altus in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

The Tether Concurrent Financing will close concurrently with the closing of the Transaction, and such concurrent closing is a condition to the completion of closing the Transaction.

The full details of the Tether Concurrent Financing will be described in Elemental Altus’ management information circular to be prepared in accordance with applicable securities legislation and made available in connection with the special meeting.

The Elemental Altus Name Change Resolution will require the approval of at least 66 2/3% of the votes cast at the Elemental Altus Special Meeting. The Elemental Altus Name Change Resolution is not a condition to close the Transaction.

Timing

Subject to receiving the requisite court, regulatory and shareholder approvals as described above, the Transaction and the Tether Concurrent Financing are expected to close in the fourth quarter of 2025. In connection with and subject to closing of the Transaction and the Tether Concurrent Financing, it is expected that the EMX Shares will be delisted from the TSX-V and NYSE American, and that EMX will cease to be a reporting issuer under Canadian and U.S. securities laws.

Board of Directors Recommendations

The Board of Directors of Elemental Altus has unanimously approved the Transaction and (subject to the abstention of any conflicted director) the Tether Concurrent Financing and recommends that the shareholders of Elemental Altus vote in favour of the Elemental Altus Resolutions.

The Board of Directors of EMX (subject to the abstention of any conflicted director) and a special committee comprised solely of independent directors of EMX (the “EMX Special Committee“) have each unanimously determined that the Transaction is in the best interests of EMX and have approved the Transaction and recommend that the shareholders of EMX vote in favour of the Transaction.

Financial Advisors and Legal Counsel

National Bank Financial is acting as financial advisor to Elemental Altus. Fasken Martineau DuMoulin LLP is acting as legal advisor to Elemental Altus. Greenberg Traurig, LLP is acting as U.S. legal counsel to Elemental Altus. Bennett Jones LLP is acting as legal advisor to Tether.

GenCap Mining Advisory Ltd. has provided a fairness opinion to the Elemental Altus Board of Directors, stating that, as of the date of such opinion, and based upon and subject to the assumptions, limitations and qualifications stated in such opinion, the Consideration to be paid is fair, from a financial point of view, to Elemental Altus shareholders excluding Tether.

CIBC World Markets Inc. is acting as financial advisor to EMX. CIBC World Markets Inc. has provided a fairness opinion to the EMX Board of Directors, stating that, as of the date of such opinion, and based upon and subject to the assumptions, limitations and qualifications stated in such opinion, the Consideration under the Transaction is fair, from a financial point of view, to the shareholders of EMX.

Haywood Securities Inc. is acting as financial advisor to the EMX Special Committee. Haywood Securities Inc. has provided a fairness opinion to the EMX Special Committee, stating that, as of the date of such opinion, and based upon and subject to the assumptions, limitations and qualifications stated in such opinion, the Consideration to be received is fair, from a financial point of view, to the shareholders of EMX.

Cassels Brock & Blackwell LLP is acting as Canadian legal advisor to EMX. Crowell & Moring LLP is acting as U.S. legal advisor to EMX. Blake, Cassels & Graydon LLP is acting as legal advisor to the EMX Special Committee.

Conference Call and Webcast

Elemental Altus and EMX will hold a joint conference call and webcast for investors and analysts on September 5, 2025, at 8am PT/11 am ET to discuss the Transaction. Questions can be asked through a chat function.

Participants may join using the webcast link:

- Audience URL: https://my.demio.com/ref/qKUUovbX1KWgKjoT

The webcast will be archived on both the Elemental Altus and EMX websites until the Transaction closes.

On Behalf of Elemental Altus,

Frederick Bell

CEO

Corporate & Media Inquiries:

Tel: +1 604 646 4527

info@elementalaltus.com

www.elementalaltus.com

TSX-V: ELE | OTCQX: ELEMF | ISIN: CA28619K1093 | CUSIP: 28619K109

On Behalf of EMX,

David Cole

CEO

For further information, contact:

| David M. Cole President and CEO Phone: (303) 973-8585 Dave@EMXroyalty.com | Stefan Wenger Chief Financial Officer Phone: (303) 973-8585 SWenger@EMXroyalty.com | Isabel Belger Investor Relations Phone: +49 178 4909039 IBelger@EMXroyalty.com |

About Elemental Altus

Elemental Altus is an income generating precious metals royalty company with 10 producing royalties and a diversified portfolio of pre-production and discovery stage assets. The Company is focused on acquiring uncapped royalties and streams over producing, or near-producing, mines operated by established counterparties. The vision of Elemental Altus is to build a global gold royalty company, offering investors superior exposure to gold with reduced risk and a strong growth profile. The Elemental Altus Shares are listed on the TSX-V and OTCXQ under the symbol “ELE” and “ELEMF”, respectively. Please see www.elementalaltus.com for more information.

About EMX

EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The EMX Shares are listed on the NYSE American Exchange and TSX-V under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

Neither the TSX-V nor its Regulation Service Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this press release.

Cautionary note regarding forward-looking statements

This press release may contain “forward-looking information” within the meaning of applicable Canadian securities laws and “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995, (collectively, “forward-looking statements”) that reflect the Companies’ current expectations and projections about their future results. These forward-looking statements may include statements regarding guidance and long-term outlook, including future revenue, which are based on public forecasts and other disclosure by the third-party owners and operators of our assets or on the ‘Elemental Altus’ or EMX’s assessments thereof, including certain estimates based on such information; expectations regarding financial strength, trading liquidity, and capital markets profile of the Merged Company; the completion of the Tether Concurrent Financing; the completion of the Transaction and the timing thereof; the realization of synergies and expected premiums in connection with the Transaction, the identification of future accretive opportunities, permitting requirements and timelines; the value the Transaction will add for shareholders of the Companies; the future price of the common shares of the Merged Company; the receipt of required approvals for the Transaction and the Tether Concurrent Financing; the completion of the name change of Elemental Altus; the completion of the Consolidation and the timing thereof; the benefits of the Transaction to shareholders of Elemental Altus; the benefits of the Transaction to shareholders of EMX; the availability of the exemption under Section 3(a)(10) of the U.S. Securities Act to the securities issuable pursuant to the Transaction; the listing of the Merged Company on a US stock exchange and the timing thereof; the timing and amount of estimated future royalty guidance; and the future price of gold. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects,” “anticipates,” “believes,” “plans,” “projects,” “estimates,” “assumes,” “intends,” “strategy,” “goals,” “objectives,” “potential,” “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are based on a number of material assumptions, including those listed below, which could prove to be significantly incorrect, including that no material disruption to production at any of the mineral properties in which the Companies’ have a royalty or other interest; that the Companies will receive all required approvals for the Transaction and the Tether Concurrent Financing in a timely manner; that synergies are realizable as between the Companies; estimated capital costs, operating costs, production and economic returns; estimated metal pricing; metallurgy, mineability, marketability and operating and capital costs; the expected ability of any of the properties in which the Companies hold a royalty, or other interest to develop adequate infrastructure at a reasonable cost; assumptions that all necessary permits and governmental approvals will remain in effect or be obtained as required to operate, develop or explore the various properties in which the Companies hold an interest; and the activities on any on the properties in which the Companies hold a royalty, or other interest will not be adversely disrupted or impeded by development, operating or regulatory risks or any other government actions.

Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward-looking statements include, amongst others, failure to obtain any required regulatory and shareholder approvals with respect to the Transaction and the Tether Concurrent Financing; the inability to satisfy the conditions to closing the Transaction and the Tether Concurrent Financing; the inability to satisfy the listing requirements to be listed on a US stock exchange; volatility in the price of gold or other minerals or metals, discrepancies between anticipated and actual production with respect to portfolio assets; the accuracy of the mineral reserves, mineral resources and recoveries set out in the technical data published by the owners of portfolio assets; the absence of control over mining operations from which the Companies receive royalties, and risks related to those mining operations, including risks related to international operations, government and environmental regulation, actual results of current exploration activities, conclusions of economic evaluations and changes in project parameters as plans continue to be refined, activities by governmental authorities (including changes in taxation); currency fluctuations; the global economic climate; dilution; share price volatility and competition.

Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors that may cause the actual results, level of activity, performance or achievements of the Companies to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: the impact of general business and economic conditions, the absence of control over mining operations from which the Companies will receive royalties from, and risks related to those mining operations, including risks related to international operations, government and environmental regulation, actual results of current exploration activities, conclusions of economic evaluations and changes in project parameters as plans continue to be refined, risks in the marketability of minerals, fluctuations in the price of gold and other commodities, fluctuation in foreign exchange rates and interest rates, stock market volatility, as well as those factors discussed in (A) the Elemental Altus’ Annual Information Form dated August 18, 2025, filed under the Elemental Altus’ profile on SEDAR+ at www.sedarplus.ca; and (B) the EMX risk factors listed in EMX’s Management’s Discussion and Analysis for the six months ended June 30, 2025 and its Annual Information Form dated March 12, 2025 filed under EMX’s profile on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov. Although the Companies have attempted to identify important factors that could cause actual results to differ materially from those Companies in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The Companies do not undertake to update any forward-looking statements that are contained or incorporated by reference, except in accordance with applicable securities laws.

Cautionary Statements to U.S. Securityholders

The financial information included or incorporated by reference in this press release or the documents referenced herein has been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, which differs from US generally accepted accounting principles (“US GAAP”) in certain material respects, and thus are not directly comparable to financial statements prepared in accordance with US GAAP.

This press release and the documents incorporated by reference herein, as applicable, have been prepared in accordance with Canadian standards for the reporting of mineral resource and mineral reserve estimates, which differ from the previous and current standards of the United States securities laws. In particular, and without limiting the generality of the foregoing, the terms “mineral reserve”, “proven mineral reserve”, “probable mineral reserve”, “inferred mineral resources,”, “indicated mineral resources,” “measured mineral resources” and “mineral resources” used or referenced herein and the documents incorporated by reference herein, as applicable, are Canadian mineral disclosure terms as defined in accordance with Canadian National Instrument 43-101 — Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) — CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended (the “CIM Definition Standards”).

The definitions of these terms, and other mining terms and disclosures, differ from the definitions of such terms, if any, for purposes of the United States Securities and Exchange Commission (“SEC”) disclosure rules for domestic United States Issuers (the “SEC Rules”), including the requirements of the SEC in Regulation S-K Subpart 1300 under the United States Securities Exchange Act of 1934, as amended. As a foreign private issuer that is eligible to file reports with the SEC pursuant to the multijurisdictional disclosure system, EMX is not required to provide disclosure on its mineral properties under the SEC Rules and provides disclosure under NI 43-101 and the CIM Definition Standards. Accordingly, mineral reserve and mineral resource information and other technical information contained or incorporated by reference herein or documents incorporated by reference may not be comparable to similar information disclosed by United States companies subject to the SEC’s reporting and disclosure requirements for domestic United States issuers. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Under Canadian rules, estimates of inferred mineral resources are considered too speculative geologically to have the economic considerations applied to them to enable them to be categorized as mineral reserves and, accordingly, may not form the basis of feasibility or pre-feasibility studies, or economic studies except for a preliminary economic assessment as defined under NI 43-101. Investors are cautioned not to assume that part or all of an inferred mineral resource exists or is economically or legally mineable. In addition, United States investors are cautioned not to assume that any part or all of the EMX’s measured, indicated or inferred mineral resources constitute or will be converted into mineral reserves or are or will be economically or legally mineable.

The Elemental Altus shares to be issued to EMX shareholders pursuant to the Transaction have not been or will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any state securities laws, and such securities are anticipated to be issued in reliance upon the exemption from such registration requirements provided by Section 3(a)(10) of the U.S. Securities Act and similar exemptions under applicable U.S. state securities laws.

Non-IFRS Measures

Adjusted Revenue

Adjusted revenue is a non-IFRS financial measure, which is defined as including gross royalty revenue from associated entities holding royalty interests related to Elemental Altus’ and EMX’s effective royalty on the Caserones copper mine. Management uses adjusted revenue to evaluate the underlying operating performance of the Company for the reporting periods presented, to assist with the planning and forecasting of future operating results, and to supplement information in its financial statements. Management believes that in addition to measures prepared in accordance with IFRS such as revenue, investors may use adjusted revenue to evaluate the results of the underlying business, particularly as the adjusted revenue may not typically be included in operating results. Management believes that adjusted revenue is a useful measure of the Company performance because it adjusts for items which management believes reflect the Company’s core operating results from period to period. Adjusted revenue is intended to provide additional information to investors and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. It does not have any standardized meaning under IFRS and may not be comparable to similar measures presented by other issuers.

1 Exchange rate of C$1.00 = US$0.7231 (the “Exchange Rate“), being the indicative exchange rate for Canadian dollars in terms of the United States dollar, as quoted by the Bank of Canada on September 4, 2025.

2 Adjusted revenue is a non-IFRS measure. Please refer to the “Non-IFRS Measures” section of this press release and Elemental Altus’ discussion of non-IFRS performance measures in its Management’s Discussion and Analysis for the quarter ended June 30, 2025

3 Based on figures (i) with respect to EMX from National Bank Financial Inc. and as of August 12, 2025, and (ii) with respect to Elemental Altus from each of Raymond James Ltd. And National Bank Financial Inc. as of August 19, 2025 and from Canaccord Genuity Corp. as of May 26, 2025.

4 Assuming approximately 629.4 million outstanding common shares of the Merged Company on the completion of the Transaction and the Tether Concurrent Financing, and based on the closing price of the Elemental Altus Shares on September 4. 2025 of C$2.05 per share, converted to US$ at the Exchange Rate

5 As at September 4, 2025

6 Average of available consensus NAV estimates as of September 4, 2025.

7 Assuming approximately 108.9 million outstanding EMX Shares as of the Effective Time and based on the closing price of the Elemental Shares on September 4. 2025 of C$2.05 per share, converted to US$ at the Exchange Rate.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/265192