Register Here: https://jayantbhandari.com/capitalism-morality/capitalism-morality-2025/

Proven Probable

Proven ProbableBlog sub category

Dear Friend and Investor,

We’re pleased to share that EMX has sold its Moroccan portfolio and entered into a strategic exploration alliance with Avesoro Holdings. This partnership allows EMX to retain long-term upside through royalties, while Avesoro fully funds the advancement of projects in one of North Africa’s most prospective mineral regions.

Here is the link to the German Translation:

EMX-NR Morocco Alliance-Ff-FINAL (clean)_DE.pdf

Please feel free to reach out if you have any questions.

NEWS RELEASE

EMX Sells its Moroccan Portfolio and Forms Exploration Alliance with Avesoro

Vancouver, British Columbia, July 8, 2025 (NYSE American: EMX; TSX Venture: EMX) – EMX Royalty Corporation (“EMX”) is pleased to announce the execution of an exploration alliance agreement (the “Agreement”) in the country of Morocco with Avesoro Morocco LTD (“Avesoro”), a wholly owned subsidiary of Avesoro Holdings LTD, a privately owned, West Africa-focused mid-tier gold producer. The Effective date of the Agreement is March 19, 2025, and key conditions precedent for closing have now been completed. Avesoro Holdings, through its subsidiaries, operates gold mines in the country of Liberia and is looking to expand its operations elsewhere in the region. As such, Avesoro brings high levels of operational and exploration experience in western Africa to the alliance. In Morocco, EMX and Avesoro will work together to advance a portfolio of exploration projects that EMX has assembled and to cooperatively explore for new opportunities.

Avesoro will fully fund the alliance activities, which will include the advancement of certain projects in the EMX Moroccan portfolio, as well as new projects identified by the alliance for acquisition. Under the Agreement, Avesoro will acquire EMX’s operating entity in Morocco (“EMX Corp Morocco”, a wholly owned subsidiary of EMX) that currently domiciles EMX’s exploration projects and its Moroccan exploration staff. Projects slated for advancement under the alliance will be initially designated as Alliance Exploration Projects (“AEP’s”). These will be funded from an annual budget agreed upon by Avesoro and EMX. Once a project reaches an appropriate stage of advancement, it can be converted to a Designated Project (“DP”) and advanced from an independent pool of funding provided by Avesoro.

The initial term of the alliance will be two years but can be extended by mutual agreement. At the end of the alliance term, any AEP’s that have not become DP’s will revert to EMX.

Strategic rationale. The sale of EMX’s Moroccan business unit is the latest example of efficient execution of our Royalty Generation business. The exploration alliance with Avesoro will perpetuate EMX’s upside royalty exposure across a large portfolio of exploration assets in a highly prospective region, while reducing ongoing operational expenses.

Commercial Terms Overview. (all terms in USD)

Alliance stage:

Designated project stage:

Overview of EMX’s Moroccan Portfolio. EMX has been active in Morocco since 2021, conducting reconnaissance exploration programs that have resulted in the acquisition of 18 exploration projects in Morocco, comprising 860 square kilometers (see Figure 1). These include a combination of gold, copper and other base metal projects that are strategically located in several of Morocco’s key mineral belts, with three projects in the highly underexplored Moroccan Sahara region, 14 projects in the well-endowed Anti-Atlas belt, home to several of Morocco’s most significant mineral deposits, and one project in the High-Atlas belt.

Morocco is emerging as an attractive jurisdiction for mineral exploration and mineral resource development, benefiting from a stable regulatory framework, well-developed infrastructure, and highly prospective geological settings. The country hosts significant precious and base metal mines yet remains underexplored compared to other mining regions.

In advance of signing the Alliance, EMX and Avesoro have agreed upon extensive follow-up programs to continue to advance the projects. Nine of the existing EMX projects will be designated as AEP’s at the onset of alliance activities.

More information on the Projects can be found at www.EMXroyalty.com.

Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

About Avesoro. Avesoro Resources Inc. is a leading West Africa-focused, privately owned mid-tier gold producer. Deeply committed to sustainable and responsible mining practices, Avesoro strives to create a diverse and inclusive workforce that adheres to strict environmental, social, and governance standards. Avesoro is recognized for its exceptional technical expertise and broad commercial and financial capabilities that span exploration, engineering, construction, and mine operations. Please see www.avesoro.com for more information.

For further information contact:

| David M. ColePresident and CEOPhone: (303) 973-8585Dave@EMXroyalty.com | Stefan WengerChief Financial OfficerPhone: (303) 973-8585SWenger@EMXroyalty.com | Isabel BelgerInvestor Relations Phone: +49 178 4909039IBelger@EMXroyalty.com |

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this

news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended March 31, 2025 (the “MD&A”), and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2024, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedarplus.ca and on the SEC’s EDGAR website at www.sec.gov.

Figure 1: location map for EMX exploration projects in Morocco

Kind regards,

Isabel Belger

Investor Relations Manager

Email: ibelger@emxroyalty.com

Mobile: +49 178 4909039

From the offices of Jayant Bhandari:

The program for the next seminar on 23rd August 2025 is linked here.

This is a friendly reminder that seats for Friday dinner with Albert Lu are limited. Only the first eighty people who register will be invited. Of course, the price of the ticket will increase as the event date approaches.

If you are already registered, I will email you in two weeks to ask if you will be attending the Friday dinner with Albert Lu.

You may use coupon code PPC2025 for a 10% discount.

While I quite liked our usual room for the seminar, we had audio problems there. So, the new location will be a couple of blocks away. Please make a note of the seminar room location from the webpage.

The playlists of all the past Capitalism & Morality seminars are linked here.

Regards,

Jayant Bhandari

www.jayantbhandari.com

Skype: jayantbh (voicemail)

Telephone: +1-206-317-1236 (voicemail)

email: contact@jayantbhandari.com

Subscribe to my free musings here

Vancouver, British Columbia–(Newsfile Corp. – June 2, 2025) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (the “Company” or “EMX”) is pleased to announce the sale of its Nordic operational platform to First Nordic Metals Corporation (TSXV: FNM) (“FNM”), a current partner of EMX and operator on multiple EMX royalty properties in Sweden and Finland. This strategic divestment will include EMX’s infrastructure, exploration equipment and employees in the Nordic countries. EMX views this transaction as highly synergistic, as it will reduce EMX’s operational and administrative expenses while providing additional operational capacity for FNM to advance its Gold Line interests in Sweden and its Oijärvi gold project in Finland, where EMX holds royalty interests. EMX will also be granted future royalty interests on projects organically generated by FNM for a period of five years.

Strategic Rationale and Long-Term Benefits

This transaction is part of a broader initiative to streamline EMX’s global operations and reduce administrative costs while maintaining upside royalty exposure in partner-funded generative exploration efforts. EMX has been conducting generative exploration in the Nordic Countries for over 15 years and has generated a broad portfolio of royalties in the region, which will be retained by EMX. In addition, EMX will be granted future royalty interests on projects organically generated by FNM for a period of five years. This transaction fits EMX strategic objectives and provides an operational boost to an existing partner and operator.

Commercial Terms

As consideration for the sale, EMX will receive staged payments totaling 3.25 million SEK (approximately US$335,000) over a period of two years. The payments will be made in equal proportions of cash and the equivalent value in shares of FNM.

Additionally, FNM will grant EMX a 1% net smelter return (NSR) royalty on any newly generated projects in Sweden and Finland during the next five years.

Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

About EMX. EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

About FNM. First Nordic Metals Corp. is a Canadian-based gold exploration company, with precious metals assets in Sweden and Finland. The Company’s flagship asset is the Barsele gold project in northern Sweden, a joint venture project with Agnico Eagle Mines Limited. Immediately surrounding the Barsele project, First Nordic is 100%-owner of a district-scale license position comprised of two additional target areas (Paubäcken, Storjuktan, also EMX royalty properties), which combined with the Barsele project, total ~100 km of strike coverage of the Gold Line greenstone belt. Additionally, in northern Finland, First Nordic is the 100%-owner of the underexplored Oijärvi greenstone belt, including the Kylmäkangas deposit, the largest known gold occurrence on this belt. EMX also controls various royalty interests over FNM projects in the Oijärvi belt.

For further information contact:

| David M. Cole President and CEO Phone: (303) 973-8585 Dave@EMXroyalty.com | Stefan Wenger Chief Financial Officer Phone: (303) 973-8585 SWenger@EMXroyalty.com | Isabel Belger Investor Relations Phone: +49 178 4909039 IBelger@EMXroyalty.com |

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended March 31, 2025 (the “MD&A”), and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2024, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedarplus.ca and on the SEC’s EDGAR website at www.sec.gov.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/254041

Vancouver, British Columbia–(Newsfile Corp. – June 2, 2025) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (the “Company” or “EMX“) is pleased to report that all proposed resolutions were approved at the Company’s Annual General Meeting of shareholders held on June 2, 2025, in Vancouver, British Columbia (the “Meeting”). The number of directors was set at 6 and all director nominees, as listed in the Management Information Circular dated April 15, 2025 (the “Information Circular”), were elected as directors of the Company at the Meeting to serve for a one-year term and hold office until the next annual meeting of shareholders. According to the proxy votes received from shareholders, the results were as follows:

| Director | Votes FOR | Votes WITHHELD |

| Dawson C. Brisco | 99.41% | 0.59% |

| David M. Cole | 99.55% | 0.45% |

| Sunny S.C. Lowe | 96.88% | 3.12% |

| Henrik K.B. Lundin | 99.34% | 0.66% |

| Geoff G. Smith | 99.52% | 0.48% |

| Michael D. Winn | 99.51% | 0.49% |

Shareholders voted 99.14% in favour of setting the number of directors at six, 99.10% in favour of appointing Davidson & Company LLP, Chartered Accountants as auditors, and 96.76% in favour of ratifying and approving the Company’s Stock Option Plan.

Voting results for all resolutions noted above are reported in the Report on Voting Results as filed under the Company’s SEDAR+ profile on June 2, 2025.

About EMX. EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

For further information contact:

| David M. Cole President and CEO Phone: (303) 973-8585 Dave@EMXroyalty.com | Stefan Wenger Chief Financial Officer Phone: (303) 973-8585 SWenger@EMXroyalty.com | Isabel Belger Investor Relations Phone: +49 178 4909039 IBelger@EMXroyalty.com |

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release

🚨✨ NEW OFFER: American Silver Eagles – Junk Silver! ✨🚨

📢 While supplies last, Miles Franklin Precious Metals Investments is thrilled to offer American Silver Eagle coins at just $4.98 OVER SPOT! 🦅💰

🌟 Why choose Silver Eagles?

• 1 oz. .9993 fine silver 📏

• Iconic “Walking Liberty” design 🇺🇸

• Perfect for diversifying your portfolio 📊

• Backed by an A+ BBB–accredited business 🏅

📞 Call us today: 855.505.1900 ☎️

🔗 Ready to secure your coins? Don’t wait—get yours before they’re gone!

🔖 #PreciousMetals #SilverInvesting #AmericanSilverEagle #WealthPreservation #PortfolioDiversification #MilesFranklin #InvestSmart #SafeHavenAssets #MauriceJackson #ProvenAndProbable #InvestmentOpportunity

Vancouver, British Columbia–(Newsfile Corp. – May 12, 2025) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (the “Company” or “EMX”) is pleased to report results for the three months ended March 31, 2025 (in U.S. dollars unless otherwise noted). EMX delivered revenue and other income of $8.4 million, adjusted royalty revenue1 of $10.8 million and adjusted EBITDA1 of $7.1 million.

Dave Cole, EMX CEO, commented, “For the first quarter of 2025 we achieved exceptional growth in adjusted royalty revenue and adjusted EBITDA, completed the acquisition of an additional royalty interest in the Chapi Mine, and strengthened our financial position through disciplined capital management, and opportunistic share buybacks. With rising commodity prices, growing revenue and a strong balance sheet, including a $10.0 million debt repayment made subsequent to the end of the quarter, we have great momentum as we continue into the second quarter of 2025.”

Q1 2025 Financial Highlights

| Three months ended March 31, | ||||||

| (In thousands) | 2025 | 2024 | ||||

| Statement of Income (Loss) | ||||||

| Revenue and other income | $ | 8,422 | $ | 6,240 | ||

| General and administrative costs | (2,170 | ) | (2,148 | ) | ||

| Royalty generation and project evaluation costs, net | (2,502 | ) | (2,934 | ) | ||

| Net income (loss) | $ | 1,260 | $ | (2,227 | ) | |

| Statement of Cash Flows | ||||||

| Cash flows from operating activities | $ | 1,289 | $ | 1,027 | ||

| Non-IFRS Financial Measures1 | ||||||

| Adjusted revenue and other income | $ | 11,428 | $ | 8,293 | ||

| Adjusted royalty revenue | $ | 10,751 | $ | 7,657 | ||

| Adjusted cash flows from operating activities | $ | 2,906 | $ | 2,661 | ||

| EBITDA | $ | 4,892 | $ | 1,249 | ||

| Adjusted EBITDA | $ | 7,101 | $ | 3,223 | ||

| GEOs sold | 3,756 | 3,696 | ||||

Summary of Financial Highlights for the Quarter Ended March 31, 2025 and 2024:

Key Strategic Developments

During the three months ended March 31, 2025, and the period subsequent to quarter end, EMX has completed several key transactions that demonstrate our strategy of incremental revenue growth and disciplined capital management as we move into 2025. These key developments include:

Outlook

The Company is maintaining its 2025 guidance2 of GEOs sales of 10,000 to 12,000, adjusted royalty revenue of $26,000,000 to $32,000,000 and option and other property income of $1,000,000 to $2,000,000.

Capital Management

For 2025, EMX has established the following capital allocation goals for 2025:

Portfolio Growth

The drivers for near and long term growth in cash flow will come from the material producing assets at Caserones in Chile and Timok in Serbia. At Caserones, Lundin Mining Corporation (“Lundin”) has initiated an exploration program which is intended to expand mineral resources and mineral reserves while at the same time looking to increase throughput at the plant. At Timok, Zijin Mining Group Co. (“Zijin”) continues to develop the Lower Zone copper porphyry block cave project while continuing to produce from the high-grade Upper Zone. Zijin also announced the recently discovered high-grade Malka Golaja Copper-Gold Deposit south of the Cukaru Peki mine and within EMX’s royalty footprint. Analysis of recent satellite imagery over the Brestovac license, which contains the Cukaru Peki Mine and is covered by EMX’s royalty, shows substantial development of new drill pads with numerous drill rigs visible in the images in the southeast corner of the license where Malka Golaja is located.

We anticipate the recently announced $10,000,000 acquisition of a royalty on the Chapi Copper Mine property in Peru will begin contributing to royalty revenue in 2026. We are excited by the addition of a high-quality copper royalty to the portfolio that has excellent upside development and exploration potential located in the prolific Paleocene-Eocene copper-molybdenum porphyry belt of Southern Peru.

In Türkiye, at Gediktepe, ACG Metals announced that the Sulphide Expansion Project remains on schedule for commissioning in Q1 2026, with no delays or cost overruns, reinforcing Gediktepe’s transition into a long-life, low-cost copper producer.

AbraSilver Resource Corp. continues to advance Diablillos in Argentina and announced that it expects to complete its definitive feasibility study by Q1 2026 and make a construction decision in the second half of 2026. At the Viscaria copper-iron-silver development project in Sweden, the Supreme Court of Sweden announced in April 2025 it will not grant leave to appeal Viscaria’s environmental permit. This decision means that Viscaria’s environmental permit can no longer be appealed and thus gains legal force. Viscaria now has all permits in place to start the construction of the industrial area including the enrichment plant, and to start operations in the mine. These developments are all examples of the upside optionality that exists throughout EMX’s global royalty portfolio.

EMX is well positioned to identify and pursue new royalty and investment opportunities, while continuing to grow a pipeline of royalty generation properties for partnership. As the Company continues to generate revenues from its producing royalty assets as well as from other option, advance royalty and pre-production payments across its global asset portfolio, various opportunities for capital redeployment will be evaluated. Such opportunities may include the direct acquisition of royalties, continued organic generation of royalties through partner funded projects and select strategic investments.

First Quarter Results for 2025

In Q1 2025, the Company recognized $11.4 million and $10.8 million in adjusted revenue and other income3 and adjusted royalty revenue3, respectively, which represented a 38% and 40% increase, respectively, compared to Q1 2024. The increase is largely due to a $1.3 million increase in royalty revenue from Gediktepe and a $1.0 million increase in royalty revenue from Caserones when compared to Q1 2024.

The following table is a summary of GEOs3 sold and adjusted royalty revenue3 for the three months ended March 31, 2025 and 2024:

| 2025 | 2024 | |||||||||||

| (In thousands) | GEOs Sold | Revenue (in thousands) | GEOs Sold | Revenue (in thousands) | ||||||||

| Gediktepe | 1,504 | 4,305 | 1,443 | 2,990 | ||||||||

| Caserones | 1,050 | $ | 3,006 | 991 | $ | 2,053 | ||||||

| Timok | 553 | 1,583 | 612 | 1,267 | ||||||||

| Leeville | 318 | 910 | 417 | 864 | ||||||||

| Other Producing Assets | 290 | 830 | 131 | 272 | ||||||||

| Advanced royalty payments | 41 | 117 | 102 | 211 | ||||||||

| Adjusted royalty revenue | 3,756 | $ | 10,751 | 3,696 | $ | 7,657 | ||||||

Shareholder Information – The Company’s filings for the year are available on SEDAR+ at www.sedarplus.ca, on the U.S. Securities and Exchange Commission’s EDGAR website at www.sec.gov, and on EMX’s website at www.EMXroyalty.com. Financial results were prepared in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board.

About EMX – EMX is a precious, and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

For further information contact:

| David M. Cole President and CEO Phone: (303) 973-8585 Dave@EMXroyalty.com | Stefan Wenger Chief Financial Officer Phone: (303) 973-8585 SWenger@EMXroyalty.com | Isabel Belger Investor Relations Phone: +49 178 4909039 IBelger@EMXroyalty.com |

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release

Forward-Looking Statements

This news release may contain “forward looking information” or “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding the future price of copper, gold and other metals, the estimation of mineral reserves and mineral resources, realization of mineral reserve estimates, the timing and amount of estimated future production, the Company’s growth strategy and expectations regarding the guidance for 2025 and future outlook, including revenue and GEO estimates, anticipated reductions in operating expenditures, repayment of outstanding debt and the timing thereof, the acquisition of additional royalty and royalty generation interests and other investment opportunities, the purchase of securities pursuant to the Company’s NCIB, exploration and development plans at the Company’s royalty properties and the expected timing thereof or other statements that are not statements of fact. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects,” “anticipates,” “believes,” “plans,” “projects,” “estimates,” “assumes,” “intends,” “strategy,” “goals,” “objectives,” “potential,” “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are based on a number of material assumptions, including those listed below, which could prove to be significantly incorrect, including disruption to production at any of the mineral properties in which the Company has a royalty, or other interest; estimated capital costs, operating costs, production and economic returns; estimated metal pricing (including the estimates from the CIBC Global Mining Group’s Consensus Commodity Price Forecasts published on March 3, 2025), metallurgy, mineability, marketability and operating and capital costs, together with other assumptions underlying the Company’s resource and reserve estimates; the expected ability of any of the properties in which the Company holds a royalty, or other interest to develop adequate infrastructure at a reasonable cost; assumptions that all necessary permits and governmental approvals will remain in effect or be obtained as required to operate, develop or explore the various properties in which the Company holds an interest; and the activities on any on the properties in which the Company holds a royalty, or other interest will not be adversely disrupted or impeded by development, operating or regulatory risks or any other government actions.

Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward-looking statements include, amongst others, failure to maintain or receive necessary approvals, changes in business plans and strategies, market conditions, share price, best use of available cash, copper, gold and other commodity price volatility, discrepancies between actual and estimated production, mineral reserves and resources and metallurgical recoveries, mining operational and development risks relating to the parties which produce the gold or other commodity the Company will purchase, regulatory restrictions, activities by governmental authorities (including changes in taxation), currency fluctuations, the global economic climate, dilution, share price volatility and competition.

Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: the impact of general business and economic conditions, the absence of control over mining operations from which the Company will receive royalties from, and risks related to those mining operations, including risks related to international operations, government and environmental regulation, actual results of current exploration activities, conclusions of economic evaluations and changes in project parameters as plans continue to be refined, risks in the marketability of minerals, fluctuations in the price of gold and other commodities, fluctuation in foreign exchange rates and interest rates, stock market volatility, as well as those factors discussed in the Company’s MD&A for the quarter ended March 31, 2025, and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2024, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR+ at www.sedarplus.ca and on the SEC’s EDGAR website at www.sec.gov. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. The Company does not undertake to update any forward-looking statements that are contained or incorporated by reference, except in accordance with applicable securities laws.

Future-Oriented Financial Information

This news release may contain future-oriented financial information (“FOFI”) within the meaning of Canadian securities legislation, about prospective results of operations, financial position, GEOs and anticipated royalty payments based on assumptions about future economic conditions and courses of action, which FOFI is not presented in the format of a historical balance sheet, income statement or cash flow statement. The FOFI has been prepared by management to provide an outlook of the Company’s activities and results and has been prepared based on a number of assumptions including the assumptions discussed under the headings above entitled “Outlook” and “Forward-Looking Statements” and assumptions with respect to the future metal prices, the estimation of mineral reserves and resources, realization of mineral reserve estimates and the timing and amount of estimated future production. Management does not have, or may not have had at the relevant date, or other financial assumptions which may have been used to prepare the FOFI or assurance that such operating results will be achieved and, accordingly, the complete financial effects are not, or may not have been at the relevant date of the FOFI, objectively determinable.

Importantly, the FOFI contained in this news release are, or may be, based upon certain additional assumptions that management believes to be reasonable based on the information currently available to management, including, but not limited to, assumptions about: (i) the future pricing of metals, (ii) the future market demand and trends within the jurisdictions in which the Company or the mining operators operate, and (iii) the operating cost and effect on the production of the Company’s royalty partners. The FOFI or financial outlook contained in this news release do not purport to present the Company’s financial condition in accordance with IFRS, and there can be no assurance that the assumptions made in preparing the FOFI will prove accurate. The actual results of operations of the Company and the resulting financial results will likely vary from the amounts set forth in the analysis presented in any such document, and such variation may be material (including due to the occurrence of unforeseen events occurring subsequent to the preparation of the FOFI). The Company and management believe that the FOFI has been prepared on a reasonable basis, reflecting management’s best estimates and judgments as at the applicable date. However, because this information is highly subjective and subject to numerous risks including the risks discussed under the heading above entitled “Forward-Looking Statements” and under the heading “Risk Factors” in the Company’s public disclosures, FOFI or financial outlook within this news release should not be relied on as necessarily indicative of future results.

Non-IFRS Financial Measures

The Company has included certain non-IFRS financial measures in this press release, as discussed below. EMX believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provide investors an improved ability to evaluate the underlying performance of the Company. These non-IFRS financial measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These financial measures do not have any standardized meaning prescribed under IFRS, and therefore may not be comparable to other issuers.

Non-IFRS financial measures are defined in National Instrument 52-112 – Non-GAAP and Other Financial Measures Disclosure (“NI 52-112”) as a financial measure disclosed that (a) depicts the historical or expected future financial performance, financial position or cash flow of an entity, (b) with respect to its composition, excludes an amount that is included in, or includes an amount that is excluded from, the composition of the most directly comparable financial measure disclosed in the primary financial statements of the entity, (c) is not disclosed in the financial statements of the entity, and (d) is not a ratio, fraction, percentage or similar representation. A non-IFRS ratio is defined by NI 52-112 as a financial measure disclosed that (a) is in the form of a ratio, fraction, percentage or similar representation, (b) has a non-IFRS financial measure as one or more of its components, and (c) is not disclosed in the financial statements.

The following table outlines the non-IFRS financial measures, their definitions, the most directly comparable IFRS measures and why the Company use these measures.

| Non-IFRS financial measure | Definition | Most directly comparable IFRS measure | Why we use the measure and why it is useful to investors | |||

| Adjusted revenue and other income | Defined as revenue and other income including the Company’s share of royalty revenue related to the Company’s effective royalty on Caserones. | Revenue and other income | The Company believes these measures more accurately depict the Company’s revenue related to operations as the adjustment is to account for revenue from a material asset | |||

| Adjusted royalty revenue | Defined as royalty revenue including the Company’s share of royalty revenue related to the Company’s effective royalty on Caserones. | Royalty revenue | ||||

| Adjusted cash flows from operating activities | Defined as cash flows from operating activities plus the cash distributions related to the Company’s effective royalty on Caserones. | Cash flows from operating activities | The Company believes this measure more accurately depicts the Company’s cash flows from operations as the adjustment is to account for cash flows from a material asset. | |||

| Gold equivalent ounces (GEOs) | GEOs is a non-IFRS measure that is based on royalty interests and calculated on a quarterly basis by dividing adjusted royalty revenue by the average gold price during such quarter. The gold price is determined based on the LBMA PM fix. For periods longer than one quarter, GEOs are summed for each quarter in the period. | Royalty revenue | The Company uses this measure internally to evaluate our underlying operating performance across the royalty portfolio for the reporting periods presented and to assist with the planning and forecasting of future operating results. | |||

| Earnings before interest, taxes, depreciation and amortization (EBITDA) and adjusted EBITDA | EBITDA represents net earnings or loss for the period before income tax expense or recovery, depreciation and amortization, finance costs. Adjusted EBITDA adds all revenue from the Caserones Royalty less any equity income from the equity investment in SLM California (Caserones Royalty holder). Additionally, it removes the effects of items that do not reflect our underlying operating performance and are not necessarily indicative of future operating results. These may include: share based payments expense; unrealized and realized gains and losses on investments; write-downs of assets; impairments or reversals of impairments; foreign exchange gains or losses; and other non-cash or non-recurring expenses or recoveries. | Earnings or loss before income tax | The Company believes EBITDA and adjusted EBITDA are widely used by investors and analysts as useful indicators of our operating performance, our ability to invest in capital expenditures, our ability to incur and service debt and also as a valuation metric. | |||

| Working capital | Defined as current assets less current liabilities. Working capital does not include assets held for sale and liabilities associated with assets held for sale | Current assets, current liabilities | The Company believes that working capital is a useful indicator of the Company’s liquidity. |

Reconciliation of Adjusted Revenue and Other Income and Adjusted Royalty Revenue:

During the three months ended March 31, 2025 and 2024, the Company had the following sources of revenue and other income:

| (In thousands of dollars) | Three months ended March 31, | |||||

| 2025 | 2024 | |||||

| Royalty revenue | $ | 7,745 | $ | 5,604 | ||

| Option and other property income | 303 | 188 | ||||

| Interest income | 374 | 448 | ||||

| Total revenue and other income | $ | 8,422 | $ | 6,240 | ||

The following is the reconciliation of adjusted revenue and other income and adjusted royalty revenue:

| Three months ended March 31, | ||||||

| (In thousands of dollars) | 2025 | 2024 | ||||

| Revenue and other income | $ | 8,422 | $ | 6,240 | ||

| SLM California royalty revenue | $ | 7,035 | $ | 4,805 | ||

| The Company’s ownership % | 42.7 | 42.7 | ||||

| The Company’s share of royalty revenue | $ | 3,006 | $ | 2,053 | ||

| Adjusted revenue and other income | $ | 11,428 | $ | 8,293 | ||

| Royalty revenue | $ | 7,745 | $ | 5,604 | ||

| The Company’s share of royalty revenue | 3,006 | 2,053 | ||||

| Adjusted royalty revenue | $ | 10,751 | $ | 7,657 | ||

Reconciliation of Adjusted Cash Flows from Operating Activities:

| Three months ended March 31, | ||||||

| (In thousands of dollars) | 2025 | 2024 | ||||

| Cash provided by operating activities | $ | 1,289 | $ | 1,027 | ||

| Caserones royalty distributions | 1,617 | 1,634 | ||||

| Adjusted cash flows from operating activities | $ | 2,906 | $ | 2,661 | ||

Reconciliation of EBITDA and Adjusted EBITDA:

| Three months ended March 31, | ||||||

| (In thousands of dollars) | 2025 | 2024 | ||||

| Income (loss) before income taxes | $ | 1,882 | $ | (2,235 | ) | |

| Finance expense | 681 | 1,065 | ||||

| Depletion, depreciation, and direct royalty taxes | 2,329 | 2,419 | ||||

| EBITDA | $ | 4,892 | $ | 1,249 | ||

| Attributable revenue from Caserones royalty | 3,006 | 2,053 | ||||

| Equity income from investment in SLM California | (1,680 | ) | (797 | ) | ||

| Share-based payments | 1,227 | 189 | ||||

| Gain on revaluation of investments | (746 | ) | (84 | ) | ||

| Loss on sale of marketable securities | 346 | 411 | ||||

| Foreign exchange (gain) loss | (207 | ) | 116 | |||

| Loss on revaluation of derivative liabilities | 162 | 41 | ||||

| Impairment charges | 101 | 45 | ||||

| Adjusted EBITDA | $ | 7,101 | $ | 3,223 | ||

Reconciliation of GEOs:

| Three months ended March 31, | ||||||

| (In thousands of dollars) | 2025 | 2024 | ||||

| Adjusted royalty revenue | $ | 10,751 | $ | 7,657 | ||

| Average gold price per ounce | $ | 2,863 | $ | 2,072 | ||

| Total GEOs | 3,756 | 3,696 | ||||

1 Refer to the “Non-IFRS financial measures” section below and on page 23 of the Q1 2025 MD&A for more information on each non-IFRS financial measure. These non-IFRS measures are not standardized financial measures under the financial reporting framework used to prepare the financial statements to which the measures relates and might not be comparable to similar financial measures disclosed by other issuers.

2 Assumed commodity prices of $2,668/oz gold and $4.26/lb copper based on CIBC Global Mining Group’s Consensus Commodity Price Forecasts (“Consensus Pricing”) published on March 3, 2025, which the Company believes to be reliable for the purposes of guidance.

3 Refer to the “Non-IFRS financial measures” section below and on page 23 of the Q1 2025 MD&A for more information on each non-IFRS financial measure.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/251664

Dear Friend and Investor,

We are pleased to invite you to an upcoming webinar hosted by John Tumazos Very Independent Research, featuring a presentation and Q&A with Dave Cole, President and CEO of EMX Royalty Corporation.

Mr. Cole will provide an update on the Company’s recent developments, portfolio performance, and strategic outlook, while addressing investor questions in conversation with John Tumazos.

Event Details:

Date: Thursday, May 15, 2025

Time: 11:00 AM EDT

Location: Online Webinar

Registration Link: https://attendee.gotowebinar.com/register/2949394207632879964

We encourage you to register in advance and mark your calendar. This is an excellent opportunity to stay informed about EMX’s progress and plans for the remainder of 2025.

Should you have any questions ahead of the webinar, please don’t hesitate to reach out.

Kind regards,

Isabel Belger

Investor Relations Manager

Email: ibelger@emxroyalty.com

Mobile: +49 178 4909039

Is Gold Still Underpriced?

We believe the next leg up for gold will be driven by a loss of confidence in mainstream positioning in equities, high-yield bonds and private equity. Concerns over tariffs may well have become a contributing factor to the gathering deflation of the financial asset bubble, but overanalyzing their possible impact obscures focus on market forces that were in motion long before “Liberation Day.”

The run to record gold bullion prices in 2024 and year-to-date 2025 has been mainly driven by official sector investment motivated in part by the gradual disintegration of the U.S. dollar-based system of international trade and the shakeup of the geopolitical landscape. Official sector demand has been augmented by record Asian and especially Chinese investment buying. These developments have been all but ignored by American and European retail and institutional investors captivated instead by overvalued technology and artificial intelligence (AI) stocks. We believe investor exposure to gold, by several measures, is at historic lows.

As capital flees overvalued assets, gold’s scarcity and safe-haven appeal could drive its price higher.

The essence of a bear market1 is overvaluation and incorrect positioning. The shift in psychology that results from bear market losses may lead to a search for investment alternatives. We believe safe-haven assets, including gold, will capture resulting capital flows.

Gold’s capacity to absorb new inflows is limited by its tiny “float”2 relative to the scale of financial markets denominated in U.S. dollars. Gold-backed exchange traded funds (ETFs) are likely recipients of the shift in capital flows we anticipate. Expanded flows into most gold ETFs must be accommodated by the purchase of physical metal. The migration of capital to gold and possibly other monetary metals could result in a price that is multiples of the current price of $3,000 per ounce.

We believe gold mining equities remain significantly undervalued and stand to benefit from further advances in metal prices. Mining profitability is leveraged to changes in gold prices, which move more quickly than costs. Therefore, in our view, mining shares offer significant torque potential relative to physical gold.

Even as the Trump administration walks back its stance on tariffs, the contraction in equity market valuations likely has further to run. On April 6, 2025, veteran market analyst and technician Stan Weinstein stated:

“While many traders and investors incorrectly think that this devastating selloff is simply the result of ‘the tariffs,’ as we showed you in detail in last weekend’s update, ‘termites’ have been at work, weakening the market’s technical structure, for the past few months, even as several of the indexes (such as the S&P 500 Index3) were making new highs (and this was being ‘camouflaged’ by the narrow strength of the ‘Magnificent 7,’4 just as was the case in late 1999-early 2000, before the internet bubble ‘popped,’ and in 1973 when the ‘Nifty Fifty’ 5 of that era was ‘all the rage’ – but, in each and every case, the Advance-Decline Line6 had topped out well before the market reached those respective peaks). So what is really happening is that the upsetting fundamental ‘news’ is colliding with an already-weakened technical structure that was getting ready to collapse (so it most definitely couldn’t handle the added ‘worries’) – and, very simply, that ‘perfect storm’ combination has resulted in this ‘crash’!”

Market strategist Michael Belkin, who has correctly called major turning points in the stock market over many decades, noted in his report on March 24, 2025, that the fuel for a market decline could be seen in the record level of margin debt.

“The January margin debt level was $937 billion, equal to the Oct 2021 peak of $936 billion…. Margin debt is a great indication of animal spirits… It’s not what people think about the market (like the AAII Individual Investor Sentiment Index), it’s a measure of how much stock market risk they are willing to take on with leverage.”

You can access more insights from Michael Belkin by listening to our Sprott Radio podcast, The New Sector Rotation.

Carter Worth, a savvy market analyst and eponym of Worth Charting, noted in an April 6, 2025, commentary that the typical stock in the Russell 3000 Index, representing 98% of all investible capital in U.S. equity markets, peaked in October well before “tariffs” was on the tip of everyone’s tongue. Roughly 50% of the stocks in that Index are down 35% or more (as of March 31, 2025), giving the lie to Treasury Secretary Bessent’s recent comment that the market carnage was confined mainly to the “Magnificent 7” names. The bear market is pervasive throughout all market sectors based on Worth’s analysis.

In our opinion, the current generation of investors has never experienced a genuine bear market. The notion that a bear market is simply a decline of 20% or more from the trading peak is overly superficial. The bear market of the 1970s was a grinding multi-year affair whose duration was sufficient to suffocate speculative psychology well into the 1980s.

It remains to be seen whether the current bear market will resemble one of the 1970s or of the post-2000 variety, which were mostly ended by Federal Reserve bailouts. History demonstrates that either outcome will be positive for gold.

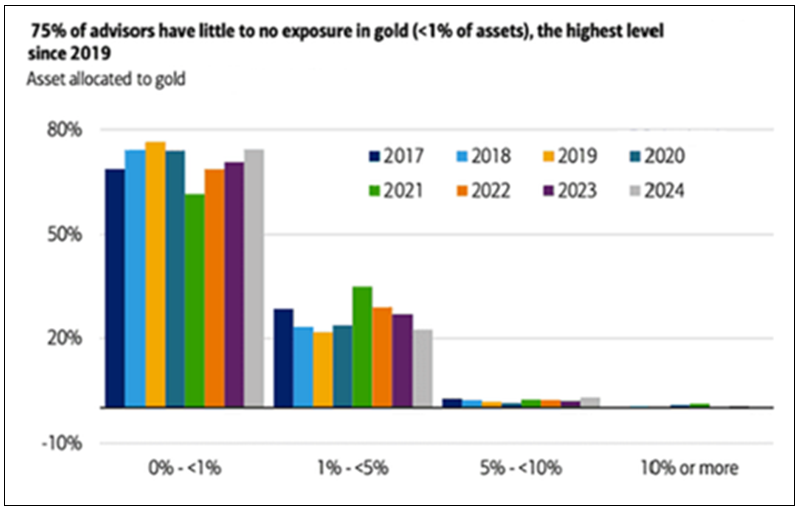

As of year-end 2024, financial advisors recorded the lowest exposure to gold since 2019.

Figure 1: Financial Advisor Allocations to Gold

Source: BofA Global Research. Data as of 2/26/2024.

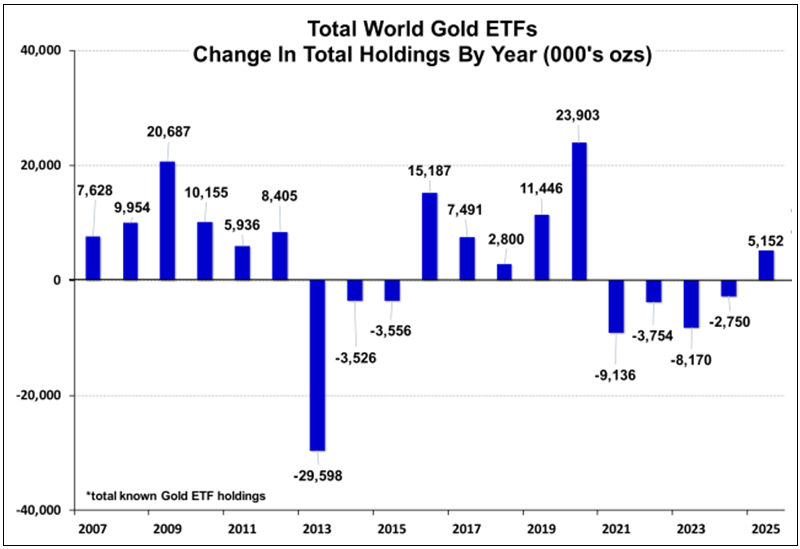

Since 2020, holdings of gold-backed ETFs have declined by 585 metric tonnes, or 17.51% of total assets at year-end 2020. In 2024, holdings rose by 159 tonnes, leaving aggregate AUM by weight nearly 20% below the 2020 peak.

Figure 2: Gold-Backed ETF Holdings Have Declined Since 2019 Peak

Source: Meridian Macro Research. Data as of 3/31/2025.

Figure 3. Total World Gold ETFs, Change in Total Holdings by Year

Source: Meridian Macro Research. Data as of 3/31/2025.

Gold, long a Wall Street pariah, has only recently become popular as major investment firms jump on the bandwagon to make gold price forecasts undreamed of only six months ago. Bullion’s newfound popularity may have resulted in a short-term overbought condition, but we believe it has been remedied by the market meltdown.

On Saturday, April 5, 2025, the Financial Times reported that hedge funds had been hit with the largest margin calls since the 2020 COVID crisis. Gold may be temporarily caught up in this “sell everything” scenario. We believe gold’s checkback will prove to be temporary and will serve to correct recent overbought sentiment readings.

A bullish outlook7 for gold is still contrarian. The longer-term consensus forecast among investment firms polled by Bloomberg is for gold prices to decline steeply to $2,100 in 2028 (see Figure 4). We regard this groupthink as a positive sign that strategists see no appeal for metal exposure other than a tactical one beyond the very short term. Another way to put this bearish gold forecast into perspective is the unanimity of bullish calls from leading brokerage firms for the stock market at the beginning of 2025. Example forecasts for the S&P 500 Index include Deutsche Bank (7100), BMO and HSBC (6700), and Goldman Sachs, Morgan Stanley, JP Morgan and Citi (all at 6500).

Figure 4. Consensus Forecasts on Gold Prices to 2028

Source: Bloomberg. Data as of March 31, 2025.

With Trump’s detonation of the “pax Americana” liberal world order in place since the end of World War II, “the U.S. dollar becomes a choice, not a necessity, and debt issuance on everything and everywhere — not just by the U.S. Treasury — becomes more risky and expensive” (from “Crashing the Car of Pax Americana Epsilon Theory”). The potential scope for reallocation to gold is suggested by the chart below:

Figure 5. Gold’s Share of Global Equity and Bond Securities

Source: BIS, ICE Benchmark Administration, Metals Focus, Refinitiv GFMS, World Bank, World Federation of Exchanges, World Gold Council.

Figure 6.

Source: Bloomberg and World Gold Council as of 2024.

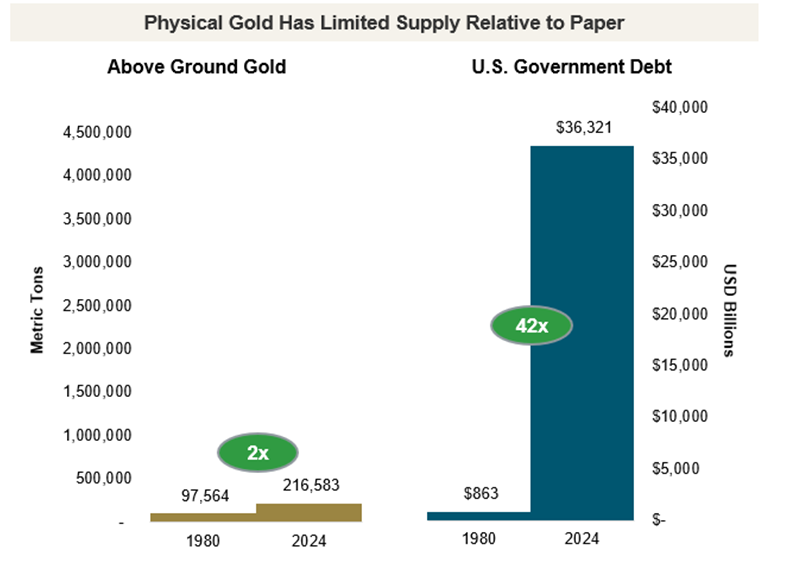

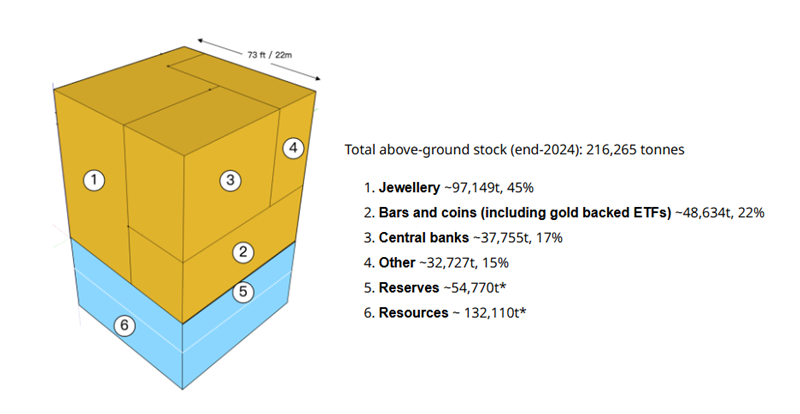

The apocryphal tale that every molecule of gold ever mined remains above ground as potential supply (due to recycling, preservation in works of art, high-end jewelry, coins, hoarding and storage as a monetary reserve by central banks) is deeply flawed. As calculated and shown in the gold cube illustration in Figure 7, that quantity is 216,583 metric tonnes, which, for the sake of this exercise, equals $22 trillion at $3,000/oz.

However, only a small fraction of that quantity is potentially in play as “supply”. The gold cube illustration suggests the application of a 72% haircut to arrive at a number for physical gold that could be quasi-tradeable. That would include coins, low-end jewelry (think Middle Eastern souks) and assorted shapes and units not acceptable as good delivery by the London Bullion Market Association (LBMA), Commodity Exchange (COMEX) or Shanghai Gold Exchange (SGE). A tally of metal stored in London, COMEX or Shanghai Gold Exchange inventories results in a tradeable float of approximately $1 trillion.

Figure 7. Estimated Above-Ground Gold Holdings by Demand Categories

Source: Data as of 2/11/2025. Financial investment includes over-the-counter (OTC) and gold ETFs. World Gold Council, Metals Focus, Refinitiv GFMS.

First, the dollar amount of all gold is a small fraction of wealth denominated in U.S. dollars (USD), $100 trillion in global equities and $315 trillion of debt (Source: Institute of International Finance) as of year-end 2024. A small reallocation from liquid financial assets into gold, most easily accessed via gold-backed ETFs, could significantly increase the USD gold price.

Second, the recent scramble to relocate physical gold from London to New York ahead of tariffs illustrated the stark illiquidity of even the tradeable gold float. Following Trump’s victory, COMEX inventories rose 2.6x from approximately 17,000 to 40,000 ounces within a few months. The premium of New York versus London gold prices rose as high as $45 (1.5%) during that period as bullion banks and their clients hurried to withdraw London 400 ounce gold bars to be refined into 100 ounce COMEX good delivery, hardly the indication of a liquid market.

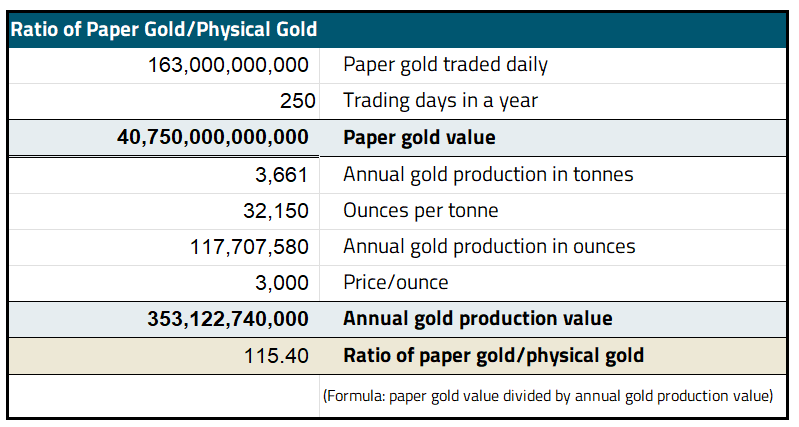

Third, the highly liquid paper gold trade rests on a shaky foundation, best imagined by John Exter*, as an inverted pyramid (see Figure 8). Paper gold includes all contracts traded between bullion banks and their clients in the form of swaps, options, futures and other derivatives. According to the LBMA, the daily trading volume of gold in 2024 was 33 million ounces or $80 billion compared to annual gold production of 120,000,000 ounces or $324 billion (2024 prices).

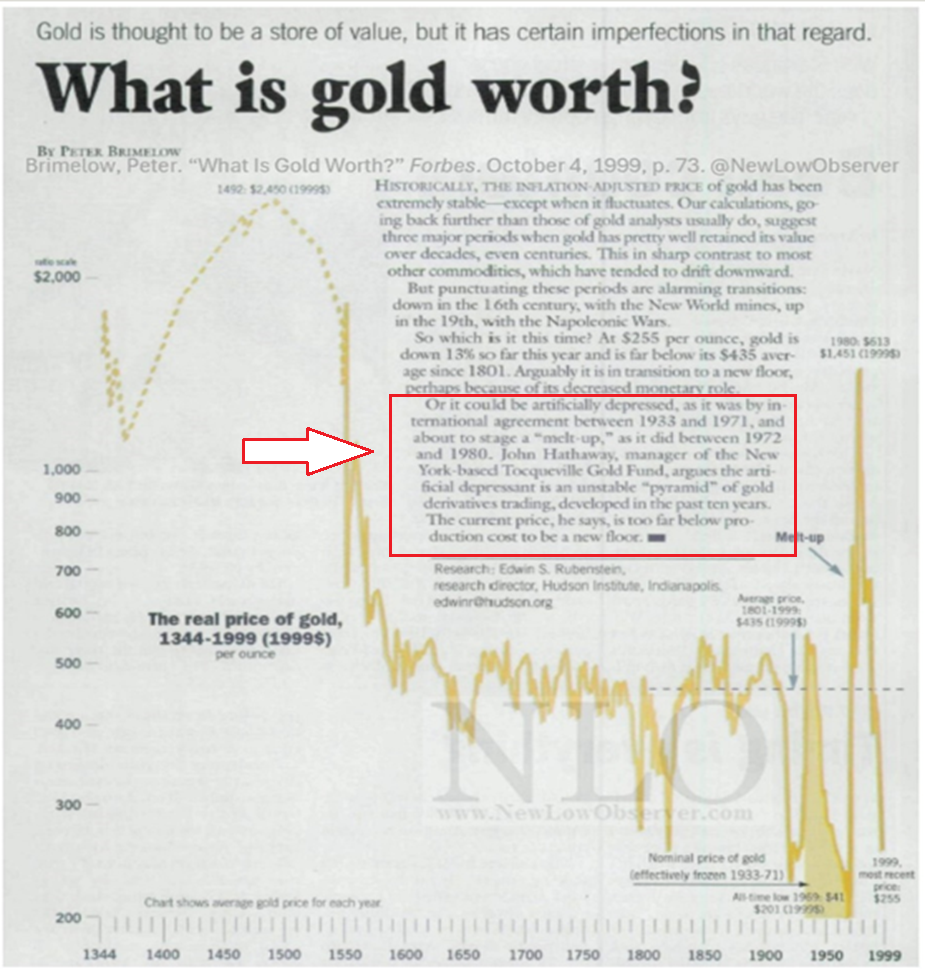

We reckon that the ratio of paper to physical trading is approximately 115 to 1 (based on LBMA and COMEX futures; see Figure 9). It is unclear, but unlikely, that the opaque LBMA market statistics include unreported over-the-counter derivative trades. The tariff scare illustrates the fragility of arrangements underlying the paper gold trade. In our opinion, the extension of credit among bullion banks and their clients will be more cautious following this episode. Our long-held belief (almost 30 years, as shown by my 1999 quote in the Appendix) is that any diminution of the paper gold trade will lead to improved price discovery for physical metal.

Figure 8. Exter’s Pyramid in the 21st Century

Source: Antiquesage.com.

Figure 9.

Source: LMBA, COMEX and the World Gold Council.

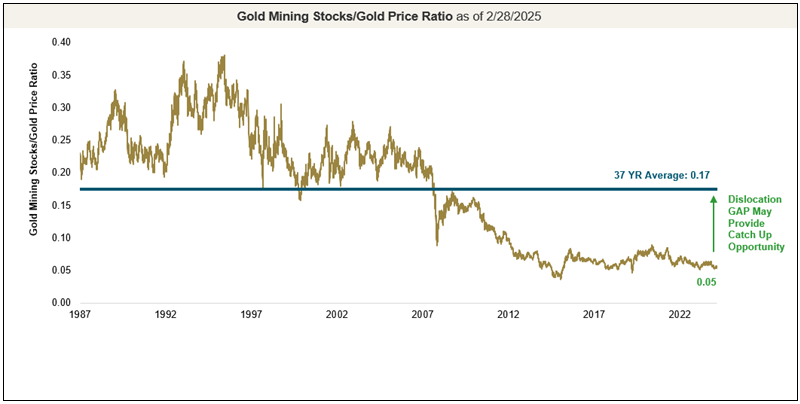

During Q1 2025, gold stocks (using GDX8 as a proxy) outperformed gold bullion with a gain of 35.56% compared to 19.02% for the metal. For many years, miners have underperformed the metal:

Figure 10. Gold Miners Offering Deep Value versus Gold Bullion

Source: Bloomberg as of 2/28/2025 (reflects past 37 years). Gold is measured by the GOLDS Comdty Spot Price and gold equities by the Philadelphia (PHLX) Stock Exchange Gold and Silver Sector Index (XAU). The Philadelphia (PHLX) Stock Exchange Gold and Silver Index (XAU) is used versus the Philadelphia (PHLX) Stock Exchange Gold and Silver Sector Total Return Index (XXAU) for its longer historical track record. You cannot invest directly in an index.

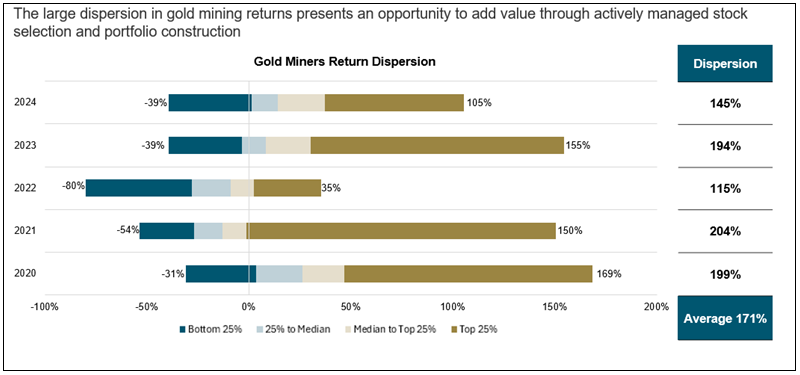

However, value investors and stock pickers, please take note: it would be ill-advised to take a jaundiced view of each and every gold stock. There are many success stories within the sector. A better perspective can be seen from the wide dispersion of returns:

Figure 11. Gold Miners: A Dispersion of Returns

Source: Bloomberg and FactSet as of 12/31/2024. Gold Miners (GDM) represents the NYSE Arca Gold Miners Index (GDMNTR INDEX) and the constituents of GDX US Equity, which tracks the GDMNTR Index. You cannot invest directly in an index.

While not universal, we see growing evidence of intelligent deployment of capital, resistance to the siren call of investment bankers that “bigger is better” and recognition of the need to return capital to shareholders during this period of prosperity for the industry. More enlightened management teams are beginning to think in terms of returns on invested capital (see Figure 12), accountability in terms of per-share metrics and judicious deal making.

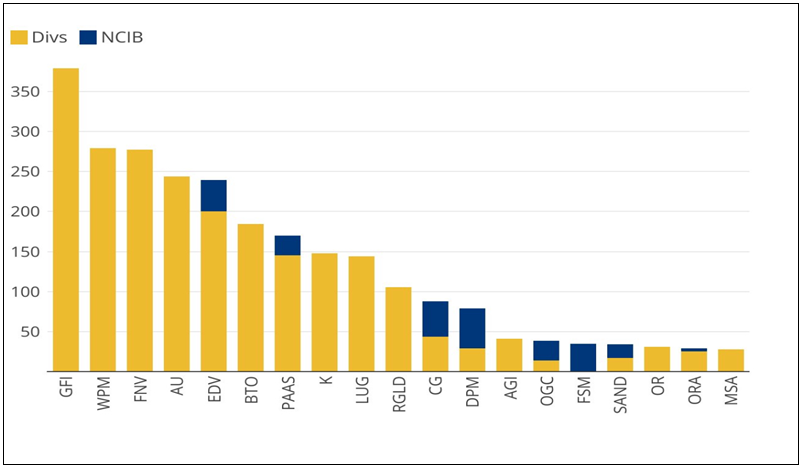

Figure 12. Gold Mining Companies Returns to Shareholders, Ex Big 3 (US$M)

Source: Mining Journal. Data as of 12/31/2024. “Ex Big 3” refers to Newmont, Barrick Gold and Agnico Eagle Mines. A Normal Course Issuer Bid (NCIB), also known as a stock repurchase program, is a company’s plan to buy back its own outstanding shares from the market, usually over an extended period, and is subject to regulatory approval.

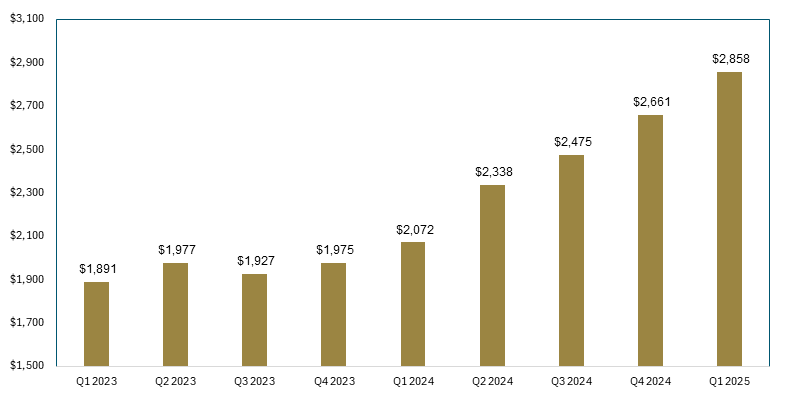

While many investors trade mining stocks according to every twitch and jiggle in the daily price, we believe a better guide is the average gold price received on a quarterly basis.

Figure 13. Average Gold Price (2023-2025)

Source: Bloomberg. Data as of March 31, 2025.

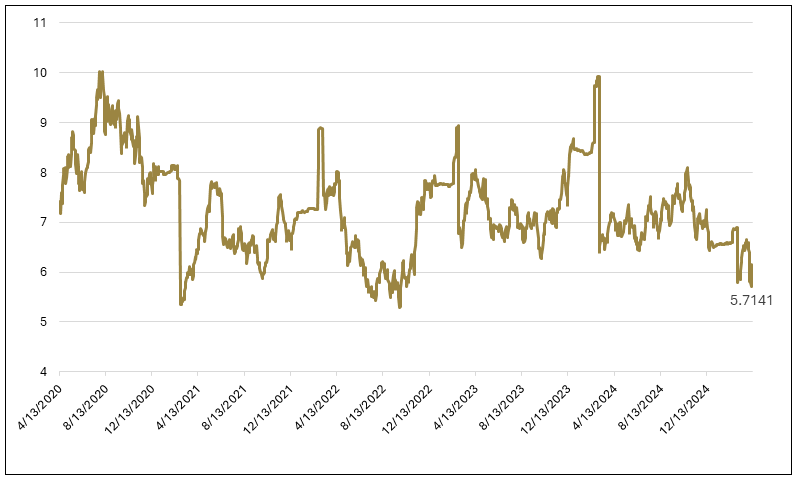

And for die-hard value investors, as we are, it is hard to find a more enticing sector in terms of EV/EBITDA9. What is especially appealing is that mining fundamentals, the main component of which is future gold prices, have fared relatively well in periods of recession and inflation.

Figure 14: Gold Miners Appear Undervalued Based on EV/EBITDA (2019-2025)

Source: Bloomberg. Data as of March 31, 2025.

We concluded our 2024 commentary with the same heading as above. We hypothesized that the catalysts for a step change in the advance of gold prices would be: “a bear market; a steep, lengthy retreat in cryptocurrencies; bond market disruption with interest rate risk morphing into credit risk; and unwanted, persistent U.S. dollar strength that threatens economic instability.”

We are batting about 75% on those calls. The retreat in cryptocurrencies has been steep, but it is too early to call it lengthy. Treasuries have thus far failed to serve as a safe haven and credit risk seems to be furiously springing leaks. The U.S. dollar has weakened instead of strengthening as a corollary of the “Trump trade” that we envisioned. However, an entrenched bear market and spreading credit risk are enough, in our opinion, to drive the gold price substantially higher. Mining stocks, especially those well-managed and positioned, stand to benefit most from the step change in the rate of gold’s advance that we envision.

From the dustbin.

For illustrative purposes only.

| 1 | A bear market is often characterized by negative investor sentiment, leading to a downward trend in market performance over time. |

| 2 | The gold “float” is the amount of gold readily available for trading in the market. |

| 3 | The S&P 500 Index (Standard & Poor’s 500) is a stock market index that tracks the performance of 500 of the largest publicly traded companies in the United States. |

| 4 | The Magnificent 7 refers to a group of seven major tech companies known for their significant stock growth and market influence. |

| 5 | The term Nifty Fifty was an informal designation for a group of roughly fifty large-cap stocks on the New York Stock Exchange during the 1960s and 1970s, known for their consistent earnings, considered solid buy-and-hold growth stocks. |

| 6 | The advance-decline line (A/D line) is a technical indicator used in stock market analysis to measure market breadth. It tracks the difference between the number of stocks that are rising in price (advancing) and the number of stocks that are falling in price (declining) on a given day. |

| 7 | A bull market is characterized by rising prices and investor optimism. |

| 8 | VanEck Gold Miners ETF (GDX®) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the NYSE Arca Gold Miners Index (GDMNTR), which is intended to track the overall performance of companies involved in the gold mining industry. |

| 9 | EV/EBITDA, a popular valuation metric, compares a company’s enterprise value (EV) to its earnings before interest, taxes, depreciation, and amortization (EBITDA) to assess its value and profitability. |

Source: https://sprott.com/insights/the-return-of-exter-s-inverted-pyramid/

Vancouver, British Columbia–(Newsfile Corp. – April 10, 2025) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (the “Company” or “EMX”) is pleased to announce that it has received an early final property payment from AbraSilver Resource Corp. (“AbraSilver”) totaling US$6.85 million. This payment, originally due by July 31, 2025, was completed ahead of schedule in exchange for a reduced total obligation from the original US$7.0 million.

EMX retains a 1% NSR on AbraSilver’s Diablillos project, an advanced silver and gold project in Argentina. EMX congratulates AbraSilver on its recent C$58.5 million equity financing to accelerate advancement of Diablillos.

EMX will use the proceeds of the early property payment, together with cash on hand, to make a US$10 million principal payment toward its senior secured term loan facility due to Franco-Nevada Corporation. Following this early principal payment, EMX’s total long-term debt outstanding will be reduced from US$35 million to US$25 million.

About EMX – EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and TSX Venture Exchange under the symbol “EMX”. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole

President and CEO

Phone: (303) 973-8585

Dave@EMXroyalty.com

Stefan Wenger

Chief Financial Officer

Phone: (303) 973-8585

SWenger@EMXroyalty.com

Isabel Belger

Investor Relations

Phone: +49 178 4909039

IBelger@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward-looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended December 31, 2024 (the “MD&A”), and the most recently filed Annual Information Form (“AIF”) for the year ended December 31, 2024, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedarplus.ca and on the SEC’s EDGAR website at www.sec.gov.

SOURCE: EMX Royalty Corp.