Kelowna, British Columbia–(Newsfile Corp. – September 10, 2024) – Strathmore Plus Uranium Corporation (TSXV: SUU) (OTCQB: SUUFF) (“Strathmore” or “the Company“) is pleased to announce that it has received the final Drill Notice permit from the State of Wyoming to perform exploratory drilling at the Beaver Rim project in the Gas Hills Uranium District of Wyoming. The permit allows for 10,000 feet of drilling, planned to begin the week of September 16th to confirm historical results and extend mineralization into areas sparsely explored in the past.

Mr. Terrence Osier, VP Exploration of Strathmore said, “We are excited to start exploring our Beaver Rim claims. I previously drilled at Beaver Rim in 2012, as project geologist for Strathmore Minerals. We encountered stacked roll-fronts at the West Diamond area at depths of 700 to 1,000 feet. The entire mineralized host-sandstone is present, giving us multiple targets across our properties. Many of the claims were previously explored by American Nuclear and Cameco. The potential to define uranium deposits at Beaver Rim is very promising based on the information we have, and areas of close-spaced drilling noted in the field. We’ve contracted with two Wyoming companies, Lou’s Drilling of Riverton and Hawkins CBM Logging of Cody. I have extensive experience with both contractors over the years and expect a successful exploration campaign that we can build on in 2025 and beyond.”

About the Beaver Rim Project

The Beaver Rim project consists of 131 wholly owned mining claims totaling 2,706 acres. The Gas Hills uranium district is the largest producer in the State of Wyoming; more than 100 million pounds of uranium was mined. Historical and recent reports suggest 50-100 million pounds of uranium remain in the Gas Hills, with significant discovery potential in the lesser drilled areas to the south, notably atop Beaver Rim. The project area was previously explored by American Nuclear in the 1970s, Cameco in the 1990-2000’s, and most recently by Strathmore Minerals in 2012, where uranium mineralization was encountered at depths of 700-1,000 feet, contained in stacked, Wyoming-type roll front deposits within arkosic-rich sandstones of the Eocene-age Wind River Formation.

The Beaver Rim project lies immediately south and adjacent to Cameco’s fully permitted Gas Hills in-situ recovery project. The West Diamond claim group lies south of Cameco’s Peach deposit, for which Cameco reported (2002 Annual Report) mineral reserves and resources of 7.0 million and 2.6 million pounds of uranium, respectively (tonnage and grade % not stated). Additional, historically defined resources controlled by Cameco are noted to trend from their property south beneath the Beaver Rim claims including the East Diamond, North Sage, and South Sage properties. Strathmore is reviewing the greater Beaver Rim area and past exploration as part of its intent to acquire additional properties with the potential to contain uranium mineralization.

About Strathmore Plus Uranium Corp.

Strathmore has three permitted uranium projects in Wyoming: Agate, Beaver Rim, and Night Owl. The Agate and Beaver Rim properties contain uranium in typical Wyoming-type roll front deposits based on historical and recent drilling data. The Night Owl property is a former producing surface mine that was in production in the early 1960s.

Cautionary Statement: “Neither the TSX Venture Exchange nor its Regulation Services Provider (as the term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release”.

Certain information contained in this press release constitutes “forward-looking information”, within the meaning of Canadian legislation. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur”, “be achieved” or “has the potential to”. Forward looking statements contained in this press release may include statements regarding the future operating or financial performance of Strathmore Plus Uranium Corp. which involve known and unknown risks and uncertainties which may not prove to be accurate. Actual results and outcomes may differ materially from what is expressed or forecasted in these forward-looking statements. Such statements are qualified in their entirety by the inherent risks and uncertainties surrounding future expectations. Among those factors which could cause actual results to differ materially are the following: market conditions and other risk factors listed from time to time in our reports filed with Canadian securities regulators on SEDAR at www.sedarplus.ca. The forward-looking statements included in this press release are made as of the date of this press release and Strathmore Plus Uranium Corp. disclaim any intention or obligation to update or revise any forward-looking statements, whether a result of new information, future events or otherwise, except as expressly required by applicable securities legislation.

Qualified Person

The technical information in this news release has been prepared in accordance with the Canadian regulatory requirements set out in National Instrument 43-101 and reviewed on behalf of the company by Terrence Osier, P.Geo., Vice President, Exploration of Strathmore Plus Uranium Corp., a Qualified Person.

Vancouver, British Columbia–(Newsfile Corp. – September 9, 2024) – Dolly Varden Silver Corporation (TSXV: DV) (OTCQX: DOLLF) (FSE: DVQ1) (the “Company” or “Dolly Varden“) is pleased to announce results from the Wolf Vein high-grade silver plunge expansion directional drilling. Drill hole DV24-416, averaged 654 g/t Ag, 0.47% Pb and 0.57% Zn over 21.48 meters and drill hole DV24-408, averaged 513g/t Ag, 2.95% Pb and 1.82% Zn over 27.19 meters. Both holes are located on the same vertical section and are separated by 44m vertically. The intersections demonstrate consistent thicknesses and indicate an increased vertical extent to the mineralized zone as it plunges to the southwest. The 2024 exploration drill program on the Kitsault Valley Project has been expanded to 32,000 m from the initial planned 25,000 m based on the successful drilling and supported by the recently completed financing. Currently, 3 drills continue expansion drilling at the Homestake Silver Deposit.

Wolf Vein Extension Drilling

Highlights include:

DV24-416: 654g/tAg, 0.47% Pb and 0.57% Zn over 21.48 meters, including 1,000 g/t Ag, 0.11 g/t Au, 0.62% Pb and 0.64% Zn over 7.70 meters.

DV24-408: 513 g/tAg, 2.95% Pb and 1.82% Zn over 27.19 meters, including 2,520 g/t Ag, 0.34 g/t Au, 0.18% Pb and 0.88% Zn over 2.80 meters.

* intervals shown are core length. Estimated true widths vary depending on intersection angles and range from 55% to 70% of core lengths, further modelling of the new intersections is needed before true widths can be estimated.

“The Wolf Vein continues to deliver exceptional silver grades, often with significant base metal values and strong native silver mineralization over potentially bulk-mineable widths. The extended drill program will prioritize lateral and vertical step-outs from these new Wolf results and follow up at other exploration targets including the silver zone at Moose. Resource expansion and exploration drilling efforts at the Homestake Silver Deposit continues within the projection of wider higher-grade gold and silver plunge zone defined in 2023,” said Shawn Khunkhun, CEO of Dolly Varden Silver.

This release includes results for three directional drill holes drilled from the same pad and intersecting the Wolf Vein on the same section, approximately 80 meters to the northeast of previously released (August 18, 2024) that documents step-out holes DV24-404, 409, 412 and 414. Directional drilling technology from this second drill pad was used to precisely target areas for vertical extension. Drill holes DV24-416 and DV24-408 intersected wide and high-grade silver mineralization in Wolf Vein breccias and coliform grey silica and carbonate approximately 14 meters above and 30 meters below, respectively from previously reported (September 11, 2023) drill hole DV23-368 that graded 381 g/t Ag, 0.46% Pb and 0.39% Zn over 29.34 meters including 583 g/t Ag, 0.13 g/t Au, 0.66% Pb and 0.45%Pb over 16.97 meter with 1,898 g/t Ag over 1.00 meter (Figure 1).

Figure 1. Section of Wolf Vein showing extended vertical expression of the Wolf vein silver mineralization and consistent wide zones of silica and carbonate vein and vein breccia with native silver, and silver sulphonate mineralization.

Drill hole DV24-416 confirms that high grade silver mineralization extends further up dip than expected, increasing the potential for a broader mineralized zone. There is also an increase in gold associated with higher grade silver as seen in a 0.60 meter interval from 676.04 to 676.64 meters grading 4,350 g/t Ag and 0.47 g/t Au. The mineralized vein remains open towards the sediment cap above it (Figure 3). Step out drilling along the upper portion of the plunge has been prioritized for late season.

Drill hole DV24-408 intersected the wider central portion of the higher-grade silver plunge and shows that in the southwestern drilling on the Wolf Vein, as the exploration approaches the projection of the intersection of the mid-valley north-northwest structures there is an increase in gold values associated with the higher grades of silver and the vein and vein breccias occur within a wide consistent structure.

Figure 2. Plan of Wolf Vein mineralized zone (in red) with all drilling to date. Lithology shown on drill trace- grey: sedimentary rock, green: volcanic rock, pink/red: mineralization. DV24-408, 410 and 416 are drilled from a collar location 80 meters northeast of the previously released step out holes.

Drill hole DV24-410 intersected the lower projection of the high-grade plunge, approximately 43 meters vertically below DV24-408. The vertical expression of the Wolf vein shows increased base metals at depth and on section, increased silver values into the high-grade plunge. This hole intersected 20.22 meters length of vein breccias that had a mix of low grade and high-grade silver, lead and zinc mineralization averaging 198 g/t Ag, 1.68% Pb and 3.42% Zn overall, with a higher-grade interval attributed to more sulphide-rich breccias, grading 823g/t Ag, 6.64% Pb and 1.55% Zn over 2.80 meters (table 1).

Figure 3. Longitudinal Section of Wolf Vein with mineralization envelope in red. Plunge of high-grade silver mineralization expanded vertically over 100m height. Drill traces in this release with bold font.

The Wolf Vein is hosted in Jurassic-age Hazelton Formation volcanic rocks and is interpreted as a structurally controlled, multi phased, epithermal vein and vein breccias that occur along a southwest plunging zone of wider, higher grade silver mineralization. Native silver, pyargerite, argentite and argentiferous galena are hosted in multiple phases of silica and iron carbonate veins and breccias. The extention of the mineralization discovered underneath the sedimentary rock cap and the outcropping Wolf deposit has a plunge extent of over 950 meters at -45 to the southwest.

Figure 4. Whole core of Wolf Vein and Vein Breccia in DV24-416 showing interval 674.30m to 682.00m (7.70 meters) with grades highlighted within broader vein intersect.

Figure 5. Cut core sample face of Wolf Vein silver mineralization in DV24-408 @ 698.10m consisting of coarse native silver in epithermal grey silica vein breccia fragments, local coliform texture open space fill. From an individual sample length of 0.78 meters grading 3,760 g/t Ag, 0.18 g/t Au, 10.60% Pb, 4.72%Zn. Field of view is 5cm across.

Table 1: Completed Drill Hole Assays from Wolf Vein (hole order in vertical sequence from top)

Target

Hole ID

From (m)

To (m)

Length (m)*

Ag (g/t)

Pb (%)

Zn (%)

Au (g/t)

Wolf

DV24-416

662.52

684.00

21.48

654

0.47

0.57

0.11

including

664.75

666.00

1.25

1,614

1.27

0.22

0.49

including

674.30

682.00

7.70

1,000

0.62

0.64

0.11

including

676.04

676.64

0.60

4,350

1.92

2.10

0.47

Wolf

DV24-408

688.26

715.45

27.19

513

2.95

1.82

–

including

688.78

689.28

0.50

2,010

1.45

1.18

–

including

697.22

700.02

2.80

2,520

13.16

6.28

0.34

including

708.94

712.07

3.13

712

11.36

4.65

–

Wolf

DV24-410

726.98

747.20

20.22

250

1.68

3.43

–

including

730.05

733.27

3.22

354

1.23

1.34

–

including

742.35

747.20

4.85

402

2.79

2.58

–

including

742.35

744.36

2.01

823

6.64

1.55

–

*All intervals shown are core length. Estimated true widths vary depending on intersection angles and range from 55% to 70% of core lengths, further modelling of the new interpretation is needed before true widths can be calculated.

Table 2: Drill hole data for Wolf Vein holes reported in this release

Hole ID

Easting UTM83 (m)

Northing UTM83 (m)

Elev. (m)

Azimuth

Dip*

Length (m)

DV24-408

466839

6173616

449

130.5

-63

759

DV24-410

466839

6173616

449

130.5

-63

795

DV24-416

466839

6173616

449

130.5

-63

726

*Directional drilling mother hole orientation; daughter holes directed at variable orientations downhole to reach target locations

Quality Assurance and Quality Control

The Company adheres to CIM Best Practices Guidelines for exploration related activities conducted on its property. Quality Assurance and Quality Control (QA/QC) procedures are overseen by the Qualified Person.

Dolly Varden QA/QC protocols are maintained through the insertion of certified reference material (standards), blanks and field duplicates within the sample stream. Drill core is cut in-half with a diamond saw, with one-half placed in sealed bags and shipped to the laboratory and the other half retained on site. Third party laboratory checks on 5% of the samples are carried out as well. Chain of custody is maintained from the drill to the submittal into the laboratory preparation facility.

Analytical testing was performed by ALS Canada Ltd. in North Vancouver, British Columbia. The entire sample is crushed to 70% minus 2mm (10 mesh), of which a 500 gram split is pulverized to minus 200 mesh. Multi-element analyses were determined by Inductively Coupled Plasma Mass Spectrometry (ICP-MS) for 48 elements following a 4-acid digestion process. High grade silver testing was determined by Fire Assay with either an atomic absorption, or a gravimetric finish, depending on grade range. Au is also determined by fire assay on a 30g split with either atomic absorption, or gravimetric finish, depending on grade range. Metallic screen on a 1.0kg sample may be completed on high-grade gold samples.

Qualified Person

Rob van Egmond, P.Geo., Vice-President Exploration for Dolly Varden Silver, the “Qualified Person” as defined by NI43-101 has reviewed, validated and approved the scientific and technical information contained in this news release and supervises the ongoing exploration program at the Dolly Varden Project.

About Dolly Varden Silver Corporation

Dolly Varden Silver Corporation is a mineral exploration company focused on advancing its 100% held Kitsault Valley Project (which combines the Dolly Varden Project and the Homestake Ridge Project) located in the Golden Triangle of British Columbia, Canada, 25kms by road to tide water. The 163 sq. km. project hosts the high-grade silver and gold resources of Dolly Varden and Homestake Ridge along with the past producing Dolly Varden and Torbrit silver mines. It is considered to be prospective for hosting further precious metal deposits, being on the same structural and stratigraphic belts that host numerous other, on-trend, high-grade deposits, such as Eskay Creek and Brucejack. Five kilometers to the East of the Kitsault Valley Project is the Big Bulk property which is prospective for porphyry and skarn style copper and gold mineralization, similar to other such deposits in the region (Red Mountain, KSM, Red Chris).

Forward Looking Statements

This release may contain forward-looking statements or forward-looking information under applicable Canadian securities legislation that may not be based on historical fact, including, without limitation, statements containing the words “believe”, “may”, “plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”, “expect”, “potential”, and similar expressions. Forward-looking statements involve known and unknown risks, uncertainties, and other factors which may cause the actual results, performance, or achievements of Dolly Varden to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. Forward looking statements or information in this release relates to, among other things, the 2022 drill program at the Kitsault Valley Project, the results of previous field work and programs and the continued operations of the current exploration program, interpretation of the nature of the mineralization at the project and that that the mineralization on the project is similar to Eskay and Brucejack, results of the mineral resource estimate on the project, the potential to grow the project, the potential to expand the mineralization and our beliefs about the unexplored portion of the property.

These forward-looking statements are based on management’s current expectations and beliefs and assume, among other things, the ability of the Company to successfully pursue its current development plans, that future sources of funding will be available to the company, that relevant commodity prices will remain at levels that are economically viable for the Company and that the Company will receive relevant permits in a timely manner in order to enable its operations, but given the uncertainties, assumptions and risks, readers are cautioned not to place undue reliance on such forward-looking statements or information. The Company disclaims any obligation to update, or to publicly announce, any such statements, events or developments except as required by law.

For additional information on risks and uncertainties, see the Company’s most recently filed annual management discussion & analysis (“MD&A“) dated March 27, 2024, and management information circular dated May 28, 2024 (the “Circular“), both of which are available on SEDAR at www.sedar.com. The risk factors identified in the MD&A and the Circular are not intended to represent a complete list of factors that could affect the Company.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this news release.

Vancouver, British Columbia–(Newsfile Corp. – September 6, 2024) – Riverside Resources Inc.(TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY) (“Riverside” or the “Company”), is pleased to announce that on September 4, 2024, it entered into a Letter of Intent with Questcorp Mining Inc. (CSE: QQQ) (“Questcorp”), whereby the Company will grant an option (the “Transaction”) to Questcorp for the acquisition of a one-hundred percent (100%) interest in the La Union project (the “Project”) located in Sonora, Mexico. Riverside will receive $100,000 and 19.9% in the ownership of Questcorp upon Questcorp investing $5,500,000 into the Project over a period of 4 years from the date of completing the Definitive Agreement.

Union is a large, carbonate-hosted gold district with high grade gold-zinc and a former mining operation of the Penoles Mining Company of Mexico. The Project has drive up access, private ranch surface ownership, and geologic features similar to the major carbonate replacement deposits located in Arizona and further east in Mexico. Union has past drilling and mining at multiple production centers which have been consolidated over the past 5 years by Riverside. Riverside now controls over 22 sq km with favorable limestone host rocks, large alteration footprint and many small mine workings which provide more than 8 drill ready target areas with the central former Union Mine and the Famosa Mine as two key immediate target areas.

“We are excited to partner this top-quality Project, consolidated and worked up by Riverside. To now work with Questcorp to go forward with the exploration program and continued development is an excellent collaboration and fits both companies’ business models.” said John Mark Staude, President and CEO of Riverside. “Riverside has extensive operational capacity in Mexico and can rapidly move ahead with Questcorp to unlock the value of La Union Project. Riverside being a significant shareholder of Questcorp with an initial 9.9% on signing the Definitive Agreement aligns our interests to see success for Union and the companies.”

Transaction Details:

In accordance with the terms of the Transaction, Questcorp can acquire a one-hundred percent (100%) interest in the Project in consideration for completion of a series of cash payments totaling $100,000, the issuance of 19.9% of the outstanding common shares of the Questcorp, and the incurrence of no less than $5,500,000 of exploration expenditures on the Project by Questcorp, as follows:

Deadline

Cash Payment

Share Issuance

Exploration Expenditures

Entering into Letter of Intent

(Paid) $12,500

Nil

N/A

Closing of the Transaction (Signing of the Definitive Agreement and conditions)

$12,500

*9.9%

N/A

First Anniversary of Closing

Nil

*14.9%

$1,000,000

Second Anniversary of Closing

$25,000

*19.9%

$1,250,000

Third Anniversary of Closing

$25,000

*19.9%

$1,500,000

Fourth Anniversary of Closing

$25,000

*19.9%

$1,750,000

Total

$100,000

*19.9%

$5,500,000

*Expressed as a cumulative total percentage of the undiluted issued and outstanding common shares of the Company

as of the applicable payment date, and assuming Riverside has not previously disposed of any common shares

**All dollar amounts in this news release are in Canadian dollars

Riverside will remain the program operator for the Project during the term of the option using its local team based in Hermosillo, Sonora and with support from the Vancouver, Canada exploration office. Following exercise of the option, Riverside will retain a two-and-one-half percent (2.5%) net smelter returns royalty on commercial production from the Project.

Exploration work by Riverside over the past 12 months has improved the geologic and structural contextual understanding of the past mines and overall potential areas of mineralization including possibilities for a deeper Laramide age porphyry Cu-Au target as found to the north at Ajo and eastward along the abundant Cu porphyry belt of Sonora- Arizona. Surface sampling recently completed by Riverside has continued to find gold and the tailings from the past mine operators, located in a number of locations on the property, have shown extensive gold zones in oxide ores.

Completion of the Transaction remains subject to a number of conditions, including the finalization of definitive documentation, completion of the Concurrent Financing by Questcorp for gross proceeds of no less than $1,500,000, receipt of any required regulatory, shareholder and third-party consents, approval of the Canadian Securities Exchange, and the satisfaction of other customary closing conditions. Riverside has been paid the initial $12,500 and will be paid the second $12,500 upon signing the Definitive Agreement.

Readers are cautioned that the Letter of Intent does not bind Questcorp to complete the Transaction. Should the Definitive Agreement not be done then the Letter of Intent will automatically terminate after forty-five days. The Transaction cannot close until the required approvals are obtained and the foregoing conditions satisfied. There can be no assurance that the Transaction will be completed as proposed or at all.

Qualified Person:

This news release was reviewed and approved by Freeman Smith, P.Geo., a non-independent qualified person to Riverside Resources, who is responsible for ensuring that the geologic information provided within this news release is accurate and who acts as a “qualified person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects.

About Riverside Resources Inc.:

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has over $5 million in cash, no debt and less than 75 million shares outstanding with a strong portfolio of gold-silver and copper assets and royalties in North America. Riverside has extensive experience and knowledge operating in Mexico and Canada and leverages its large database to generate a portfolio of prospective mineral properties. In addition to Riverside’s own exploration spending, the Company also strives to diversify risk by securing joint-venture and spin-out partnerships to advance multiple assets simultaneously and create more chances for discovery. Riverside has properties available for option, with information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Investor Relations Riverside Resources Inc. Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Over the years as an advisor and investor, I’ve spoken to hundreds of mainly natural resource investors. A topic I’ve always found difficult to explain, which is vitally important to understanding a stock, is the different between ‘share price’ and ‘market capitalization’ (also known as ‘market cap’).

In this article we’ll discuss why these two items are important and different from each other, and explore how knowing the difference will allow one to determine the true ‘price paid’ for a stock (or business). Knowing the true price of a business will provide one with a competitive edge, which is particularly important when investing in natural resource shares.

Countless times we’ve been part of investment discussions, where the question of buying a stock comes up. Invariably, the question “How much did you pay?” is asked. Ten out of ten investors will tell you, “I paid $100 per share for Apple (or Barrick Gold)”.

If we then ask, “How much did you pay for the business”? Ninety-nine out of one hundred investors will repeat themselves, and say, “I paid $100 per share.” The odd man out, or the 100th investor would instead say, “I paid $100 per share, at a market capitalization of $100 billion”. In other words, this rare fellow understands that while he paid $100 per share, he actually paid $100 billion, notionally, for the business itself.

How does this compute?

The share price represents the price of a single fractional share of a business. If we wanted to purchase the entire business, we would need to purchase every share issued by the company. If the company has issued 100 million shares (referred to as ‘shares outstanding’) – we would need to purchase all 100 million, in order to purchase the business in its entirety.

How do we calculate how much money is needed to purchase an entire business?

This is where market capitalization comes into play. Market cap is simply the total number of shares issued, multiplied by the share price.

To use our earlier example – if we bought Apple stock at $100 per share, and if (hypothetically speaking) there were 100 million shares outstanding – that would imply a market cap of $10 billion. Therefore, $10 billion would be needed to ‘notionally’ purchase the entire company.

In reality, there are other moving parts involved in purchasing an entire company, but this is a simplified explanation of ‘market cap’.

The best place to find the outstanding share count of a company is the most recent quarterly or annual report. This report can usually be found on the investor relations page of the company’s website, or through the stock exchange or regulatory filing website for the country in question.

When investing in natural resource shares, one must pay extra close attention to market capitalization and outstanding share count. The reason is that outstanding share count can change rapidly over time, and in most cases the number only grows in size.

In the natural resource and mining sector, there are four asset categories: 1. Major producers, 2. Junior producers, 3. Development stage companies, and 4. Exploration stage companies.

Most companies in the bottom three asset categories are ‘negative cash flowing.’ Meaning, they lose money from year to year just staying in business. “How can a company remain in business if it loses money?” you might ask.

Well, the approach taken for most natural resource companies is to issue more stock (shares) and sell it to investors privately in the form of a private placement, or ‘equity offering’.

(Side note: Some investors jokingly refer to profligate junior resource issuers who ‘over-issue’ shares, as “Mining the Stock Market” as opposed to mining anything from the ground.)

When the process of share issuance continues over time, it causes outstanding share count to grow, and when multiplied by the market price – causes market cap to continually grow. Therefore, while the share price of a company may remain the same or decline over time, the expansion or contraction of outstanding share count may cause the market cap (or ‘price paid for the business’) to increase or decrease.

Given that most companies in the bottom three asset classes of the natural resource space are negative cash-flowing, investors need to anticipate share count expansion over time.

The brutal fact, is that each additional share issued by the company represents a ‘slice of the pie’ taken from your plate, as the investor. Your interest in the company is diluted, unless you continue to purchase additional shares, as they are issued.

Why would a company issue more shares – isn’t that a form of theft, and are they cheating me out of my investment?

In defense of management teams, there are many ways in which a share issuance may be helpful to investors (the term we might use is ‘accretive’). For example, let’s say a management team wishes to purchase a strip of property adjacent to their own company’s operating gold mine.

If they issue shares and exchange them for the strip of property, the transaction may be deemed beneficial to shareholders, despite the share dilution. Whether or not the transaction is beneficial would be a separate set of calculations – namely, deciding what the shares exchanged are ‘worth’, and what the strip of property is worth – and whether there is a reasonable rate of return, on the ‘notional’ value spent on the property.

A company may also issue additional shares, with the intended use of funds going toward purchasing complimentary assets which may reduce the cost of operations. As an example – purchasing a fleet of vehicles or other machinery, versus leasing the same. Whether or not the transaction is beneficial would be determined by the details – comparing the value of the shares issued, versus the cost savings gained.

Quite often in the natural resource space, and nearly always by the exploration stage companies – share issuances generate funds to pay employee salaries and ‘keep the lights on’ (also known as general & administrative expense). Many exploration companies survive by continuous financings, year after year, without assurance of continued survival – throughout which, share count continually grows.

A common term for describing the rate of annual consumption of funds of negative cash flowing resource companies, is called ‘Burn Rate’. As an example, a company may have a $2 million cash balance on hand, with an expected expense or Burn Rate of $2 million per annum. Therefore, we know the company will run out of money within 12 months or less, and will need to conduct a financing.

The odds of an exploration company exploring a project on their own, funded solely by their shareholders, and discovering a Tier 1 (highly profitable) deposit, is akin to the odds of winning the lottery. When such a remote set of survival odds are combined with a negative cash flowing business model, it becomes clear, that ‘sole-funded’ exploration companies are among the riskiest market sectors on the planet.

Let’s take a look at a hypothetical example of market cap expansion, via share count:

Beaverbrook Gold Exploration Company (a fictitious company) – has an outstanding share count of 100,000,000 as of its most recent annual report. The market price is $.10 per share. If we multiply this share price against the outstanding share count, we arrive at a market cap (or price to buy the business as a whole), of $10,000,000.00.

The company has $2 million cash on hand, which they estimate will cover exploration expenditures and general & administrative expense for 1 year – a $2 million per annum Burn Rate, in other words.

With that knowledge, we know the company will need to raise additional funds within 12 months or less, and if they expect another year of $2 million in expenditures – then we know it will likely be a $2 million financing (assuming they wish to ask the market for that amount).

A common financing practice to attract investors is to offer shares at a discount to the market price. If our hypothetical company offers a $2mm share issuance, let’s assume they offer the shares at a price of $.08 per share – a 20% discount to market. This would imply issuance of an additional 25,000,000 shares, bringing the total share count up to 125,000,000 – diluting existing shareholders’ interests by 20%.

In response to seeing the offering, some shareholders decide to sell their shares, and the market price drops to $.08, matching the recent offering price. However, since the share count grew – the market cap, using the new share price of $.08 – comes out to $10,000,000 – matching precisely the prior market cap, when there were fewer shares outstanding priced at $.10.

In this circumstance the share price dropped by 20%, but the ‘price of the business’ – market cap in other words, stayed the same. This is an incredibly important dynamic to keep track of when investing in the junior resource space, or any negative cash flowing sectors for that matter. The negative cash flows, year after year, accumulate in the form of ballooning share structures (rising share counts), diluting one’s interest in the underlying company fairly quickly.

The process resembles a musical accordion, expanding to enormous proportions as the music is played:

Original Image Credit: Richard Brandao, Creative Commons.

For many ‘sole-funded’ exploration companies, the speed of annual share issuance is so rapid, that within just a few years – say 3-5 – hundreds of millions of additional shares are issued. The speed and size of share issuance may cause the ‘accordion’ share structure to bloat beyond recognition.

After blowing out the share structure, many companies carry out share consolidations (also known as ‘rollbacks’ or ‘reverse share splits’). A share consolidation might entail 10, 20, 50, or even 100 shares, being condensed and replaced by as few as 1 single post-consolidation share.

Other instances may see shareholders completely wiped out through bankruptcy or other reorganization, with subsequent launching of a new separate company under a different name (in order to shed stigma associated with the prior corporate failure).

There are however a few segments of the junior resource space which generate mildly lower speeds of share dilution. Conservatively run ‘Prospect Generator’ and ‘Optionality Deposit’ companies may meet this criterion. We will discuss ‘Prospect Generator’ model companies at a later date.

Optionality companies typically possess one or more large resource deposits that exhibit ‘leverage’ to a higher commodity price. In simple terms, this means a deposit that is not economic to extract at today’s commodity pricing, but could potentially become economic should the price of a commodity such as gold, silver or copper, double or triple in price – with assumed production costs remaining the same.

The hoped-for strategic intent (from an investor’s viewpoint) of optionality strategy company management teams, is to spend as little money as possible on development, and general & administrative expense, while preserving the deposit’s good & marketable condition. Preserving capital helps preserve the share structure of the company – ie. decelerating share expansion as much as possible.

There are a few optionality companies that engage in exploratory drilling to increase the resource base of an existing deposit, advance feasibility study work, and/or acquire additional optionality deposits over time. ‘Active’ optionality deposit companies of this type will consequently produce share expansion at a faster speed.

Let’s take a look at a few examples of optionality companies, and inspect share price, share count, and market cap over time, of each.

Please note however – this exercise is meant to observe changes over time related to share price, share count, and market cap only. The examples used here do not represent an endorsement of quality or investment ‘attraction’.

For a snapshot of corporate development changes over time, and changes to what a business is ‘worth’ from an intrinsic standpoint – that would be a separate exercise outside the scope of this article.

The following statistical displays are one of many information gathering processes. Inspection of corporate developments over time would require review of the balance sheet, asset and resource base of the company, and income (or loss) statement.

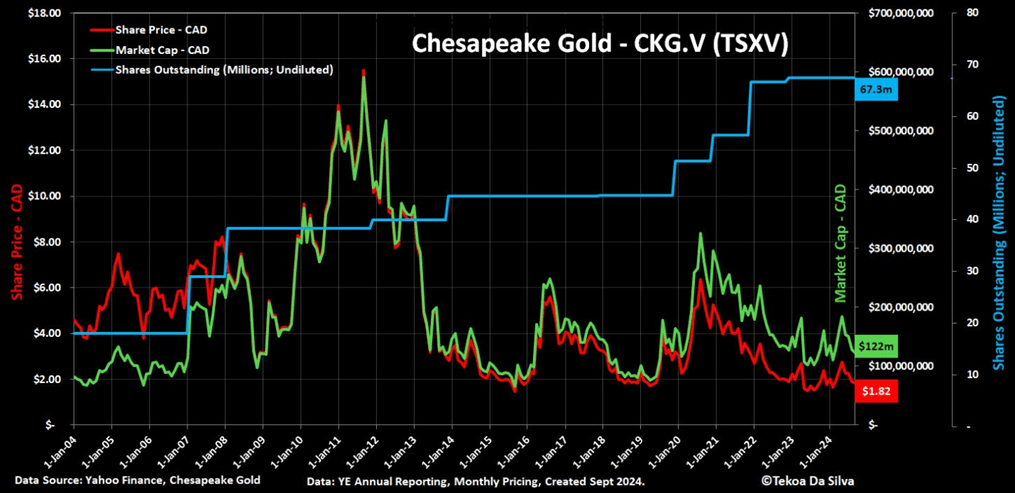

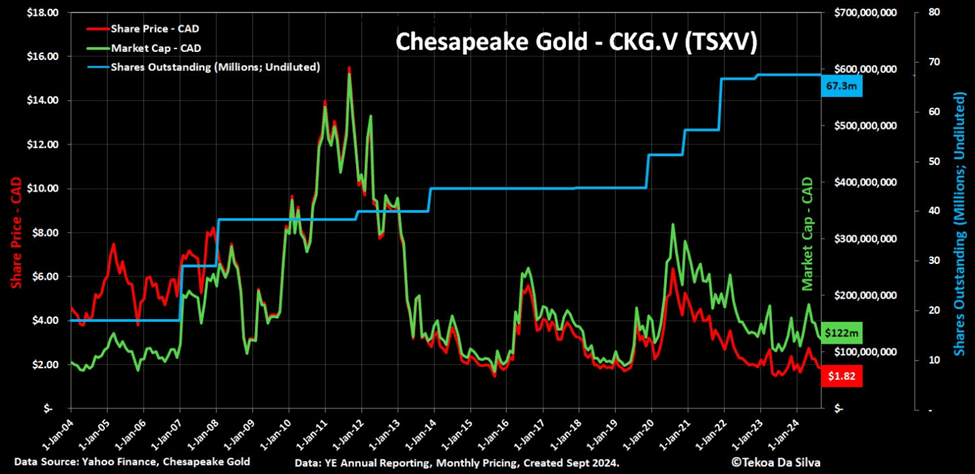

The first company we’ll look at is Chesapeake Gold. As illustrated by the red line below – the share price declined from CAD $4.60 to approximately CAD $1.82 over the last 20 year period, from January 2004 to September 2024. This is over a 50% decline:

As illustrated by the blue line above, the outstanding share count increased from about 17 million to over 67 million during the same 20 year period; nearly a 4x increase.

This resulted in a market cap (price of the business) increase, as illustrated by the green line, which over the same 20 year period grew from about CAD $81 million to over CAD $122 million – an increase of over 50%.

In this example, over the 20 year period, shareholders experienced a 50%+ share price decline, while the price of the business itself rose by over 50% – due to expansion of share count, and consequently, market cap.

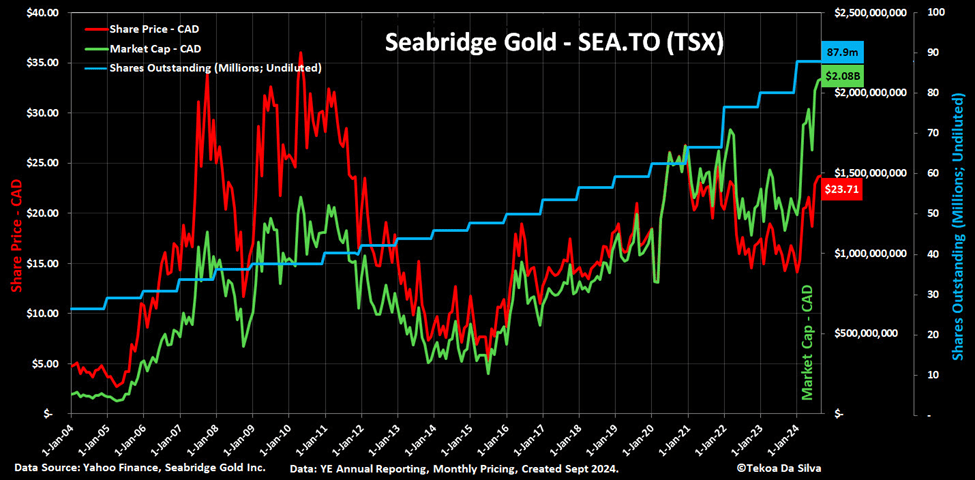

The second company we’ll look at is Seabridge Gold. As illustrated by the red line below – the share price increased from CAD $4.75 to approximately CAD $23.71 over the last 20 year period, from January 2004 to September 2024. This is roughly a 5x move higher:

As illustrated by the blue line above, the outstanding share count increased from about 26 million to over 87 million during the same 20 year period; over a 3x increase.

This resulted in a market cap (price of the business) increase, as illustrated by the green line, which over the same 20 year period grew from about CAD $124 million to a recent high over CAD $2.08 billion – an increase of over 16x.

In this example, over the 20 year period, shareholders experienced nearly a 400% gain on their shares, while the price of the business itself rose by over 16x – due to expansion of share count, and consequently, market cap.

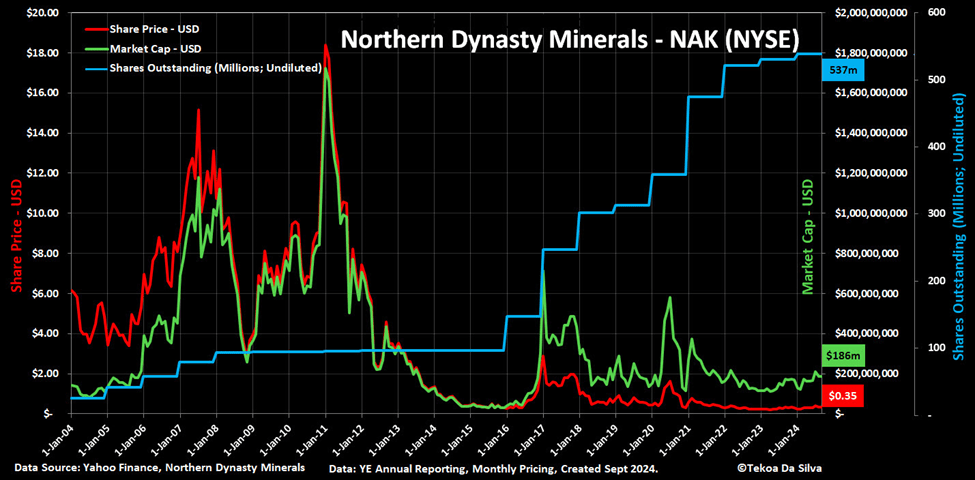

The last company we’ll look at is Northern Dynasty. As illustrated by the red line below – the share price decreased from USD $6.15 to approximately USD $0.35 over the last 20 year period, from January 2004 to September 2024. This is nearly a 95% decline:

As illustrated by the blue line above, the outstanding share count increased from about 23 million to over 537 million during the same 20 year period; over a 23x increase.

This resulted in a market cap (price of the business) increase, as illustrated by the green line, which over the same 20 year period grew from about USD $143 million to over USD $186 million – an increase of over 30%.

In this example, over the 20 year period, shareholders experienced nearly a 95% share price decline, while the price of the business itself rose by over 30% – due to expansion of share count, and consequently, market cap.

To further dampen this picture – a common assumption made by nonprofessional investors when looking at a 20-year price chart of Northern Dynasty – is that the USD $18.00 per share price peak generated in 2011, as a matter of course, should be recovered during the next precious metal equity ‘bull market’. From the current USD $.35 share price this would imply a 50x move higher.

When looking at the price of the business – the 2011 market cap peaked around USD $1.7 billion. The current market cap is roughly USD $186 million. Recovering the prior market cap high from here, would imply a 9x move higher – not a 50x move. A 9x move higher in the share price and market cap from here (assuming no further expansion of share count), would imply a share price of USD $3.15 – a far cry, from the majestic heights of USD $18.00 per share, exhibited at the 2011 peak.

The reason the market cap revisitation multiple is lower than some expect, is explained by the blue line in the Northern Dynasty chart above – outstanding share count ballooned by over 23x, during the 20 year period.

A counterargument for a higher Northern Dynasty (or any other company) market cap might rest in the real fact that ‘2011’ US dollars are not the same as ‘2024’ US dollars. The US dollar has weakened to the extent that in January 2011 only 1,360 US dollars were required to purchase an ounce of gold, whereas in September 2024 it takes 2,513 US dollars to purchase an ounce of gold – nearly a 50% loss of purchasing power, during the period.

If we measure Northern Dynasty’s January 2011 market cap peak in gold terms – it would indicate an approximate 1,266,705 gold ounce market cap. If Northern Dynasty today revisited that same market cap peak, in gold ounce terms – at USD $2513 per oz. gold, it would imply a USD market cap of $3.183 billion. A market cap increase to that size would imply about a 17x move higher, from here.

There is speculative prospect of further USD devaluation, which offers the potential of driving market caps higher for all ‘hard asset’ businesses. It is up to individual investors and speculators, to decide if they wish to factor currency devaluation into their approach.

The difference between ‘share price’ and ‘market capitalization’ is stark. Without knowing the quantity and difference between the two, an investor will not know how much he or she is paying for a business.

Many investors discuss share price, but not many engage market cap discussions. Market cap is determined by outstanding share count, which like a musical accordion, can expand and contract greatly over time.

To increase survival odds, investors and speculators should consider visiting with company financial statements over time. The statements will indicate whether share count has been expanding or contracting. It is an especially important metric to follow in the junior natural resource space.

This tool (market cap monitoring) will contribute to your competitive edge. And most investors are unaware of it.

To reach or follow the author, Tekoa Da Silva, visit:

Ottawa, Ontario–(Newsfile Corp. – September 4, 2024) – Gold79 Mines Ltd. (TSXV: AUU) (OTCQB: AUSVF) (“Gold79” or the “Company”) and Bullet Exploration Inc. (TSXV: AMMO) (“Bullet”) are excited to have entered into a definitive amalgamation agreement (the “Agreement”) dated September 3, 2024, whereby Gold79 has agreed to acquire all of the issued and outstanding common shares of Bullet (the “Transaction”). The Transaction will create a well-funded gold exploration company focused on the southwest United States. The Company will be focused on delivering a maiden resource at its Gold Chain project in Arizona; exploring the newly acquired Jefferson North Gold-Silver project in Nevada to define its scale potential; and continue to work with Kinross to get the maiden drill program at Jefferson Canyon in Nevada underway.

Under the terms of the Transaction and subject to Bullet shareholder approval, Bullet shareholders will receive one (1) common share of Gold79 (each whole share, a “Gold79 Share”) for every three (3) common shares of Bullet (“Bullet Share”) held (the “Exchange Ratio”). In addition, each common share purchase warrant and stock option of Bullet outstanding immediately prior to completion of the Transaction shall be adjusted in accordance with the Exchange Ratio and replaced with common share purchase warrants and stock options of Gold79, respectively. Existing shareholders of Gold79 and Bullet will hold approximately 54% and 46%, respectively, of the outstanding Gold79 Shares on closing of the Transaction, on a fully diluted, in-the-money basis (but prior to the completion of the planned equity financing described below). In connection with the Transaction Gold79 plans to raise C$4,000,000 (or such other amount as may be agreed by the parties).

Derek Macpherson, President and CEO of Gold79 stated, “The Transaction between Gold79 and Bullet is a unique opportunity to consolidate exploration companies in the Southwest U.S. The combined entity is going to have multiple projects at various stages of exploration, be well-funded and have improved access to capital. Importantly for shareholders, the planned equity financing should provide the Company the capital necessary to deliver a maiden resource at Gold Chain. We are excited to bring together the teams of these two companies that have complementary skill sets, which we expect to bear fruit as we move the combined Company forward.”

Ehsan Agahi, President and CEO of Bullet stated, “This merger is a transformative step for Bullet shareholders, offering immediate exposure to a diverse portfolio of high-potential gold projects in the Southwest U.S. By joining forces with Gold79, we strengthen our ability to advance these assets and unlock their full value. The combined expertise and resources should accelerate our growth trajectory and create substantial value for all stakeholders.”

Strategic Rationale for the Transaction

Creation of a multi-project SW US Gold Explorer (Figure 1)

Gold Chain Project, Arizona

Recent drilling returned 9.1m of 51.09 g/t Au (GC23-28) and 44.2m of 2.01 g/t Au (GC23-23).

Recently defined a from-surface exploration target of 15.6 to 31.2 million tonnes (Mt) grading 1.5 to 2.5 g/t Au. The potential quantity and grades are conceptual in nature. There has been insufficient exploration drilling to define a mineral resource and it is uncertain if further exploration will result in the exploration target being delineated as a mineral resource.

Short path to a maiden resource.

Jefferson North Gold-Silver Project, Nevada

Recent sampling returned 56.7 g/t Au and 29.9 g/t Au from the East Adit #1 Underground Drive.

Maiden drill program scheduled to be completed in the Fall of 2024.

Approximately 30 kilometres from Gold79’s Jefferson Canyon project providing regional synergies.

Jefferson Canyon Gold-Silver Project, Nevada

Historical results include 41.2m of 6.4 g/t Au and 402 g/t Ag (drill hole GJ-081, CR Exploration Company (CREC), 1983 to 1985).

Partnered with Kinross, operator of the adjacent Round Mountain Mine and a Top Ten Global Gold producer.

Permitting advanced for a maiden drill program.

Tip Top Gold-Silver Project, Nevada

Historical results include 9.14m at 14.42 g/t Au (drill hole T98-14, Dos Amigos 1998, reverse circulation drilling).

Financial Strength to deliver a Maiden Resource: The planned C$4,000,000 equity financing should provide the necessary funds to deliver a maiden resource at the Gold Chain project, while also allowing the Company to advance its other projects.

Increased scale: The combined entity is expected to have a larger market capitalization.

Multiple Exploration Projects: The combined entity will have four exploration stage projects in the southwest United States.

Operational Synergies: The synergy of the combined exploration and management teams of the combined entity is expected to reduce costs and result in a higher percentage of capital raised being used for exploration.

Better Access to Capital: Bullet’s management and directors along with its existing shareholders are expected to improve the Company’s access to capital as it works to deliver a maiden resource at Gold Chain.

Adding a Quality Project in a well understood district: Bullet’s Jefferson North project is close to Gold79’s existing Jefferson Canyon project. Gold79’s understanding of the geology of this area is expected to allow the Company to quickly advance this project.

Increased Scale: The combined entity is expected to have a larger market capitalization.

Improved Team: Management and directors from Bullet are expected to be selectively added to Gold79’s management team and board of directors. These additions are expected to improve the skill set of the combined team.

Benefits to Bullet Shareholders

Exposure to Gold Chain: Bullet shareholders gain exposure to the Gold Chain project which is expected to have a short path to a maiden resource.

Gold79 Management Team: Bullet shareholders should benefit from the technical expertise of the Gold79 team, which has had exploration success over the last three years with limited budgets.

Exposure to Partner Funded Project: Bullet shareholders gain exposure to the Jefferson Canyon project, where the next round of drilling is expected to be funded by Kinross and the potential exists for a US$5 million payment to the Company if Kinross exercises their option.

Increased Scale: The combined entity is expected to have a larger market capitalization.

Transaction Details

Under the terms of the Transaction and subject to Bullet shareholder approval, Bullet shareholders will receive one (1) Gold79 Share for every three (3) Bullet Shares held. In addition, each common share purchase warrant and stock option of Bullet outstanding immediately prior to completion of the Transaction shall be adjusted in accordance with the Exchange Ratio and replaced with common share purchase warrants and stock options of Gold79, respectively. Existing shareholders of Gold79 and Bullet will hold approximately 54% and 46%, respectively, of the outstanding Gold79 Shares on closing of the Transaction on a fully diluted, in-the-money basis (but prior to the completion of the planned equity financing).

The Transaction will be effected by way of a three-cornered amalgamation whereby Gold79, through its wholly-owned subsidiary, 1492834 B.C. Ltd. (“Subco”), will amalgamate with Bullet forming Amalco. Amalco will become a wholly-owned subsidiary of Gold79. Bullet will cease to be a reporting issuer and the Bullet Shares will be delisted from the TSXV.

On the effective date of the Transaction, the Board of Directors (the “Board”) of Gold79 will be reconstituted such that three current directors of Gold79 will remain on the Board, and Gold79 will appoint two additional director nominees provided by Bullet. The Company plans to provide additional details on the composition of the go-forward management team, Board and advisory board at a later date.

In addition to the requisite Bullet shareholder approval, the Transaction is subject to applicable regulatory approvals, including the approvals of the TSX-V and the satisfaction of certain other closing conditions customary in transactions of this nature as well as customary interim period covenants regarding the operation of each of the companies’ respective businesses. The Agreement also provides for a mutual condition of the parties that a C$4,000,000 equity financing (or such other amount as may be agreed by the parties) be completed immediately following, and contingent upon, the closing of the Transaction. The Agreement contains customary provisions including fiduciary-out provisions in favour of both Gold79 and Bullet, non-solicitation and the right to match alternate proposals for each party. A C$200,000 termination fee may be payable to Gold79 or Bullet under certain circumstances.

Subject to the satisfaction of these conditions, Gold79 and Bullet expect that the Transaction will be completed on or before November 30, 2024. Details regarding these and other terms of the Transaction are set out in the Agreement, which will be available under the SEDAR+ profiles of Gold79 and Bullet at www.sedarplus.ca.

None of the securities to be issued pursuant to the Transaction have been or will be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“), or any securities laws of any state of the United States (as defined in Regulation S under the U.S. Securities Act), and any securities issuable in the Transaction are anticipated to be issued in reliance upon available exemption from such registration requirements pursuant to Section 3(a)(10) of the U.S. Securities Act and similar exemptions under applicable securities laws of any state of the United States. This press release does not constitute an offer to sell or the solicitation of an offer to buy any securities.

Additional Information

Further details about the Transaction, including further particulars of the business of Gold79, Bullet and the combined entity, will be provided in in the management information circular of Bullet to be prepared and filed in respect of the annual and special meeting of the Bullet shareholders to be held in Q4 2024.

All information contained in this press release with respect to Gold79 and Bullet was supplied for inclusion herein by the respective parties and each party and its directors and officers have relied on the other party for any information concerning the other party.

Completion of the Transaction is subject to a number of conditions, including but not limited to, TSX-V acceptance and the requisite Bullet shareholder approval. The Transaction cannot close until the required Bullet shareholder approval is obtained. There can be no assurance that the Transaction will be completed as proposed or at all.

Investors are cautioned that, except as disclosed in the Agreement or in the management information circular of Bullet to be prepared in connection with the annual and special meeting of the Bullet shareholders, any other information released or received with respect to the Transaction may not be accurate or complete and should not be relied upon. Trading in the securities of Gold79 and Bullet should be considered highly speculative.

The TSX-V has in no way passed upon the merits of the proposed Transaction and has neither approved nor disapproved the contents of this press release.

Qualified Person / Quality Control and Quality Assurance

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration for Gold79 is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release related to the Gold Chain, Jefferson Canyon, and Tip Top projects. The QP has not verified the historical analytical data or the quality control or quality assurance procedures of previous operators related to historical drill hole intercepts at the Jefferson Canyon and Tip Top projects.

Garry Clark, P. Geo., is a qualified person as defined in National Instrument 43-101 and has reviewed and approved the technical content of this press release related to the Jefferson North project. Mr. Clark is a director of Bullet.

About Gold79 Mines Ltd.

Gold79 Mines Ltd. is a TSX Venture listed company focused on building ounces in the Southwest USA. Gold79 holds 100% earn-in option to purchase agreements on three gold projects: the Jefferson Canyon Gold Project and the Tip Top Gold Project both located in Nevada, USA, and, the Gold Chain Project located in Arizona, USA. In addition, Gold79 holds a 32.3% interest in the Greyhound Project, Nunavut, Canada under JV by Agnico Eagle Mines Limited.

About Bullet Exploration Inc.

Bullet Exploration Inc. is a TSX Venture listed company focused on high-potential gold and silver projects in the Southwest United States. The flagship Jefferson North Gold-Silver project in Nevada, near major producers like Kinross’s Round Mountain, spans 1,068 hectares and 132 claims, offering significant exploration potential. Bullet also holds the Copper Canyon Property in British Columbia, targeting a copper-gold porphyry deposit. With a tight capital structure and a long-term vision for growth, Bullet is committed to advancing its projects and creating lasting shareholder value.

For further information regarding this press release contact:

This press release may contain forward looking statements that are made as of the date hereof and are based on current expectations, forecasts and assumptions which involve risks and uncertainties associated with our business including the proposed Transaction and proposed private placement or any future private placements, the uncertainty as to whether further exploration will result in the target(s) being delineated as a mineral resource, capital expenditures, operating costs, mineral resources, recovery rates, grades and prices, estimated goals, expansion and growth of the business and operations, plans and references to the Company’s future successes with its business and the economic environment in which the business operates. All such statements are made pursuant to the ‘safe harbour’ provisions of, and are intended to be forward-looking statements under, applicable Canadian securities legislation. Any statements contained herein that are statements of historical facts may be deemed to be forward-looking statements. By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties. We caution readers of this news release not to place undue reliance on our forward-looking statements as a number of factors could cause actual results or conditions to differ materially from current expectations. Please refer to the risks set forth in the Company’s most recent annual MD&A and the Company’s continuous disclosure documents that can be found on SEDAR at www.sedar.com. Gold79 does not intend, and disclaims any obligation, except as required by law, to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Edmonton, Alberta–(Newsfile Corp. – September 3, 2024) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) Is pleased to announce the appointment of Mr. Phil B. Acton of Hayward, CA as an Advisor to the Board of Directors.

Mr. Acton is a Certified Public Accountant and a member of the American Institute of Certified Public Accountants and the Utah Association of Certified Public Accountants and has extensive business experience in various industries. This includes ownership of multiple businesses, providing tax, audit and other attestation services, portfolio and cash management for a Private Trust, and co-managing 20-80 trucks transporting uranium ore in Utah. Since 2000, Mr. Acton has been a shareholder and General Manager of East Bay Motorsports, Inc. in Hayward, California, guiding significant growth of the business through acquisitions and marketing and increasing sales from US$8.0 million to over US$26 million.

Brian Testo, President and CEO of Grizzly Discoveries, stated, “We continue to strengthen our Advisory Board with motivated and qualified individuals with diverse skillsets. We are thrilled to welcome Mr. Acton to the Grizzly team as his business acumen and strategic insight will be instrumental as we position ourselves for the inevitable improvement in market conditions for the junior mineral exploration industry in Canada.”

In conjunction with his appointment, the Board has authorized the grant of 1,000,000 stock options of Grizzly with an exercise price of $0.05 per option to Mr. Acton, expiring on September 3, 2029 or earlier in accordance with the Company’s stock option plan. The grant of options is subject to acceptance by the TSX Venture Exchange.

ABOUT GRIZZLY DISCOVERIES INC.

Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and base metals properties in southeastern British Columbia. Grizzly is run by a highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.

On behalf of the Board,

GRIZZLY DISCOVERIES INC. Brian Testo, CEO, President

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Caution concerning forward-looking information

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward-looking information. Such forward-looking information and statements are frequently identified by words such as “may,” “will,” “should,” “anticipate,” “plan,” “expect,” “believe,” “estimate,” “intend” and similar terminology, and reflect assumptions, estimates, opinions and analysis made by management of Grizzly in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Grizzly’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon.

Risks and uncertainties that may cause actual results to vary include but are not limited to the availability of financing; fluctuations in commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available under the Company’s SEDAR+ profile at www.sedarplus.ca. Grizzly disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

Gold futures (GC=F) have been surfing record highs, with Monday’s prices hitting $2,555.2 per ounce, sending the value of a 400 troy ounce gold bar to $1,022,080.

The yellow metal has forged meteoric gains this year, emerging as the world’s second-best-performing asset next to crypto. Its 23% year-to-date gain edges out the megacap-loaded Nasdaq Composite (^IXIC) — itself up a healthy 18%. (A proxy for the crypto market writ large, the Bitwise 10 Crypto Index Fund (BITW), is up 47% this year.)

According to BofA Global Research, gold funds just absorbed the largest inflows in four weeks, attracting $1.1 billion. Yet, the broader trend has actually seen $2.5 billion in outflows year to date, suggesting that underlying strength is coming from outside traditional fund flows.

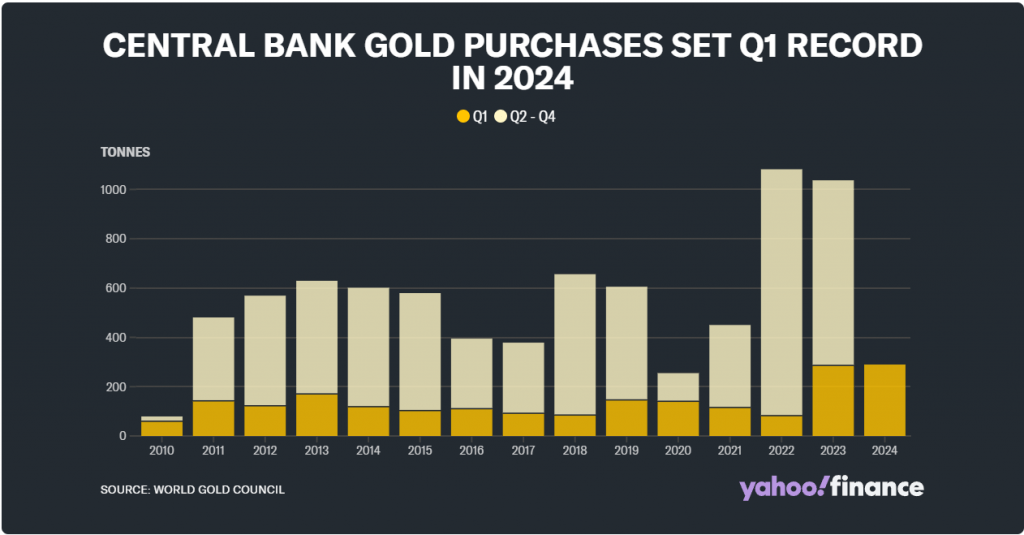

Central banks — especially those of developing countries — have been buying the barbarous relic at a record clip. According to the World Gold Council, central banks have purchased 290 tonnes in the first quarter alone, beating out the prior Q1 record from 2023 and setting CBs on a path to record gold purchases in 2024 that are estimated to easily eclipse 1,000 tonnes.

“Not only is the long-standing trend in central bank gold buying firmly intact, it also continues to be dominated by banks from emerging markets,” wrote the Gold Council.

In that regard, Turkey tops the buy list this year with 30 tonnes purchased in the first quarter — lifting its gold reserves to 570 tonnes. China bought 27 tonnes in Q1, making it the 17th consecutive quarter of purchases and also bringing its holdings to 2,262 tonnes. Other notable purchasers include India, Kazakhstan, the Czech Republic, Oman, and Singapore.

The central bank buying spree has solidified gold’s status as a reserve asset. According to BofA, gold has now surpassed the euro to become the world’s largest reserve asset second only to the US dollar, representing 16% of the reserve pool.

The precious metal’s performance can be attributed to its unique position as a real asset with one of the lowest correlations to stocks across asset classes, making it a safe haven from market swings and inflation.

This embedded content is not available in your region.

According to Tom Bruni, head of market research at StockTwits, in a recent episode of Stocks in Translation, “We’re seeing gold being used as an uncertainty hedge.”

Bruni also emphasized gold’s appeal to traders due to its price action. “With gold breaking out above its 2011 highs, it’s drawing significant attention from trend followers and technical analysts alike.”

Investors looking for deep, liquid gold markets have a robust choice of futures markets, ETFs, and gold miner stocks and ETFs, which tend to be even more volatile than the underlying metal.

“The volatility in gold prices has made it a prime trading vehicle, whether through gold ETFs or mining stocks,” said Bruni.

BofA separately highlighted how this latest gold rally isn’t like the other advances this century, offering a tantalizing glimpse of future bullish potential.

The bank noted this is the third major gold advance in two decades, yet “households have missed this rally.” The first two rallies — from 2004 to 2011, and from 2015 to 2020 — attracted big fund flows into gold ETFs. But over the last year, gold bullion and gold miner ETFs have shed $6.4 billion in assets, according to Bloomberg data and Yahoo Finance calculations.

But if last week’s large gold inflows were to gain momentum, that trend could signal a perfect storm of retail, institutional, and central bank gold buying is brewing. Why?

Bruni said it best: “Gold is kind of one of these things that operates on vibes.”

Ottawa, Ontario–(Newsfile Corp. – August 27, 2024) – Gold79 Mines Ltd. (TSXV: AUU) (OTCQB: AUSVF) (“Gold79” or the “Company”) has received an Acceptance Letter from the United States Forest Service (“USFS”) for its Plan of Operations (“POO”) to explore the Jefferson Canyon Project in Nevada.

The Acceptance Letter indicates that the USFS believes that the POO submitted is acceptable based upon studies and documentation submitted to date. The next steps include consultation with both the public and state heritage agency, along with other reviews, which are expected to be followed by a Record of Decision and bonding, before drilling can commence.

Derek Macpherson, President and CEO of Gold79, states, “This is a positive step forward in the Jefferson Canyon permitting process; and, while we are not yet able to start drilling, we continue to make progress towards that end.” Mr. Macpherson continued, “It is important to note that while there is still a possibility that drilling could occur this year, the most likely scenario emerging is that the permitting process will not be completed in-time to drill in 2024.”

The original Plan of Operations for Jefferson Canyon was submitted in July 2021 and the cultural and biological studies were completed and submitted in Q2 2022. Gold79 received feedback on the proposed areas of disturbance relative to identified cultural sites in March 2023. After multiple revisions to the plan, it was resubmitted on December 12, 2023. After some additional minor revisions, the Acceptance Letter was received on August 26, 2024. The application is for 20 drill sites and associated roads to service them.

The Jefferson Canyon project in Nye County, Nevada is located 7 kilometres from Kinross’s Round Mountain operations. The project has 145 historical drill holes, including 41.2m at 6.4 g/t gold and 402 g/t silver (GJ-81). In 2022, Gold79 entered into an Exploration and Option agreement with Kinross. Kinross has made all the required payments associated with the agreement to date and has been working with Gold79 on completing the permitting process.

Gold Chain share payment

Further to its press release dated July 27, 2023, the Company announces that it has issued 306,396 common shares of the Company in connection with a US$48,000 (C$66,024) share payment due under the option agreement covering a portion of the Company’s landholdings for the Gold Chain project. The common shares issued have a statutory hold period until December 16, 2024.

Qualified Person / Quality Control and Quality Assurance

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release.

About Gold79 Mines Ltd.

Gold79 Mines Ltd. is a TSX Venture listed company focused on building ounces in the Southwest USA. Gold79 holds 100% earn-in option to purchase agreements on three gold projects: the Jefferson Canyon Gold Project and the Tip Top Gold Project both located in Nevada, USA, and, the Gold Chain Project located in Arizona, USA. In addition, Gold79 holds a 32.3% interest in the Greyhound Project, Nunavut, Canada under JV by Agnico Eagle Mines Limited.

For further information regarding this press release contact: Derek Macpherson, President & CEO Phone: 416-294-6713 Email: dm@gold79mines.com Website: www.gold79mines.com

This press release may contain forward-looking statements that are made as of the date hereof and are based on current expectations, forecasts and assumptions which involve risks and uncertainties associated with our business including any proposed private placement or any future private placements, the uncertainty as to whether further exploration will result in the target(s) being delineated as a mineral resource, capital expenditures, operating costs, mineral resources, recovery rates, grades and prices, estimated goals, expansion and growth of the business and operations, plans and references to the Company’s future successes with its business and the economic environment in which the business operates. All such statements are made pursuant to the ‘safe harbour’ provisions of, and are intended to be forward-looking statements under, applicable Canadian securities legislation. Any statements contained herein that are statements of historical facts may be deemed to be forward-looking statements. By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties. We caution readers of this news release not to place undue reliance on our forward-looking statements as a number of factors could cause actual results or conditions to differ materially from current expectations. Please refer to the risks set forth in the Company’s most recent annual MD&A and the Company’s continuous disclosure documents that can be found on SEDAR+ at www.sedarplus.ca. Gold79 does not intend, and disclaims any obligation, except as required by law, to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Lundin Mining logo (CNW Group/Lundin Mining Corporation)

VANCOUVER, BC, Aug. 24, 2024 /CNW/ – (TSX: LUN) (Nasdaq Stockholm: LUMI) Lundin Mining Corporation (“Lundin Mining” or the “Company”) is pleased to announce today that an agreement has been reached with the union at Caserones and accepted by the majority of the union members through a vote. Further to the press release dated August 12, 2024 entitled “Lundin Mining Provides Update on Labour Negotiations at its Caserones Mine”, a new collective bargaining agreement will be signed imminently. The Company will now focus on a safe back-to-work plan and an efficient ramp-up of operations which has been running at approximately 50% capacity during the labour action. View PDF version

About Lundin Mining

Lundin Mining is a diversified Canadian base metals mining company with operations and projects in Argentina, Brazil, Chile, Portugal, Sweden and the United States of America, primarily producing copper, zinc, gold and nickel.

The information was submitted for publication, through the agency of the contact persons set out below on August 24, 2024 at 17:00 Vancouver Time.

Cautionary Statement on Forward-Looking Information

Certain of the statements made and information contained herein are “forward-looking information” within the meaning of applicable Canadian securities laws. All statements other than statements of historical facts included in this document constitute forward-looking information, including but not limited to statements regarding the Company’s plans, prospects and business strategies; the Company’s approach to resolution and procedures regarding the strike and its expectations regarding the return to normal operations; the Company’s guidance on the timing and amount of future production and its expectations regarding the results of operations; expected costs; permitting requirements and timelines; timing and possible outcome of pending litigation; the results of any Preliminary Economic Assessment, Pre-Feasibility Study, Feasibility Study, or Mineral Resource and Mineral Reserve estimations, life of mine estimates, and mine and mine closure plans; anticipated market prices of metals, currency exchange rates, and interest rates; the development and implementation of the Company’s Responsible Mining Management System; the Company’s ability to comply with contractual and permitting or other regulatory requirements; anticipated exploration and development activities at the Company’s projects; expansion projects and the realization of additional value; expectations regarding, and ability to complete, the acquisition of Filo Corp. and the 50/50 joint venture with BHP; the anticipated development and other plans with respect to the acquisition and joint venture; the Company’s integration of acquisitions and expansions and any anticipated benefits thereof; and expectations for other economic, business, and/or competitive factors. Words such as “believe”, “expect”, “anticipate”, “contemplate”, “target”, “plan”, “goal”, “aim”, “intend”, “continue”, “budget”, “estimate”, “may”, “will”, “can”, “could”, “should”, “schedule” and similar expressions identify forward-looking information.