From The Desk Of David Schectman

David’s Commentary (In Blue)

This is the third year in a row that Andy and Bill Holter met at the Masters for a three day mini vacation. Zhanna and Kathy stayed at home. This is a boy’s only affair. When Andy left Minneapolis on Tuesday morning the sun was out and it was in the 70s. And this is what it was like in Augusta.

When Andy left Minneapolis on Tuesday, it was 70 and I was sunning on the deck. Wednesday and Thursday, a snowstorm hit the Midwest. This is what my deck looked like below. Next year they will go to for the British Open.

They say that April is the cruelest month of them all. Last year we had a record 21” of snow in April. It’s almost as harsh as the gold and silver markets can be.

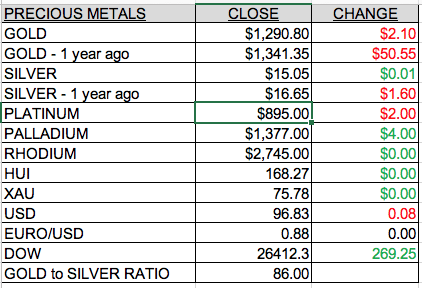

The Boyz never miss an opportunity to take advantage of a major moving average and once again, they pushed gold below the 50-day MA and below the key big number 1300 too. Silver was taken along for the ride and knocked below 15. But this will only last for a day or two, and just like the snow on my deck (above), it will not last – gold will move above 1300 and silver above 15. This is just the paper game, where they take their small profits and re-set to get ready to do it all over again. It’s like tennis or ping pong. Back and forth, back and forth, until finally there is a winner.

Here are Ed Steer’s comments on the price manipulation:

As Ted Butler always points out at times like this, except for the small amount of selling that the commercial traders do to get things started, plus maintain the downside price momentum, the are always, always, always the big buyers on engineered price declines like this…and never big sellers.

Gold was closed not only below $1,300 spot, but also back below its 50-day moving average — and silver was sold back below its 200-day moving average. It was all done for profit and price management purposes — and the Managed Money traders were the patsies once again. You’d think they’d learn after all these years, but they’re slaves to moving averages — and nothing else matters to them

So what have we learned in the last 10 years? We’ve learned that markets are cyclical. They have their peaks and their troughs. Most of our clients are contrarians. They understand that you have to buy low. Lord knows, we given lots of chances and this week is another one.

We have been bullish on silver for several years because the gold/silver ratio tells us that silver, relative to gold, is cheap. But it is not a good “predictive tool” because the ratio can tighten if gold falls and silver remains the same. That’s right, silver doesn’t have to rise for the ratio to fall; it only has to outperform gold. The most bullish case is for gold to rise, and for silver to rise faster. And we are bullish on gold. That is not contradictory, because where gold goes, silver will follow. Silver is more volatile, so if gold is going up, silver will go up more. One cannot be certain, but I do think that 2019 is the year that we finally break out of the trading range that we’ve been in, which in gold’s case is between $1,200 to $1,375. What we do know is that the silver/gold ratio has to normalize so if you are bullish on gold, be even more bullish on silver because it has to rise faster.

We are bullish on gold because gold is a necessary form of insurance versus the US dollar. If you believe that gold trades contra to the dollar, then that is reason enough to be bullish on gold. With $22 trillion in on-balance sheet liabilities and $120 trillion in off-balance sheet liabilities (Social Security, Medicare, etc.) this can only go one of two ways. You can default or you can deflate it away. The odds are that the Fed will continue to take the inflation route, rather than default on the debt, and the debt will be paid back, but with dollars that each year are worth less and less. It’s pretty basic stuff – keep increasing the money supply and watering down the purchasing power of the dollar and the “cost” to pay back the debt is easier to handle. Well, they will never pay back the debt. The struggle is to pay the interest on the debt. There is a saying: you are bankrupt when you can no longer afford to pay the interest on your debt. But since we have (for now) the world’s reserve currency, we can create the money to pay the interest out of thin air. In today’s daily one of the featured articles talks about how China and Russia are moving out of dollars and are the two largest buyers of gold on the planet now, in preparation to end the dollar’s long run as the world’s reserve currency.

Saudis Threaten to End Petrodollar — Jim Rickards

Investors have been speculating for years about the demise of the “petrodollar” deal struck by Henry Kissinger and Treasury Secretary William Simon in 1974.

It was first set up between the U.S. and Saudi princes to prop up the U.S. dollar. At the time, confidence in the dollar was on shaky ground because President Nixon had ended gold convertibility of dollars in 1971.

In 1974, the price of oil was skyrocketing, partly due to inflationary policies pursued by the Federal Reserve, and partly due to an Arab oil embargo in response to U.S. aid to Israel in the Arab-Israeli Yom Kippur War of 1973.

The world economy was under threat unless a way could be found to “recycle” the dollars the Arabs were receiving back into U.S. banks. President Nixon and Henry Kissinger asked Simon to negotiate with Saudi Arabia on this issue.

Kissinger and Simon worked out a plan. If the Saudis would price oil in dollars, U.S. banks would hold the dollar deposits for the Saudis.

Behind this “deal” was a not so subtle threat to invade Saudi Arabia and take the oil by force. I personally discussed these invasion plans in the White House with Kissinger’s deputy, Helmut Sonnenfeldt, at the time. But the petrodollar plan worked brilliantly and the invasion never happened.

The link to it is here.

One of our readers sent me an Email after reading my comments in our Wednesday newsletter. She said, “ I do not believe in coincidences. When I came across/read your article tonight I knew serendipity was afoot.”

The Most Interesting Financial Seminar I Ever Attended

I don’t believe in coincidences either. Let me tell you about “coincidence” – and the most interesting financial seminar I ever attended. Actually, I was one of the featured speakers at the seminar, not just an attendee.

32 years ago I traveled to a financial seminar in Hong Kong to discuss gold and the economy. These offshore events were very popular in the 80s. The conference boasted an impressive cast of speakers, including James Dale Davidson and Doug Casey. All of the speakers predicted that gold was going up – except for one – James Dale Davidson. He was very popular in those days, having just finished co-authoring a book on investing with Lord Reese-Moog in 1987 titled Blood in the Streets. Gold had been moving up for past two years and we all felt the fundamentals indicated that the move up would continue. Davidson emphatically said no, it’s not; it’s going down. At the end of the conference, the attendees are asked to fill out a form and rate the speakers, and Davidson got the lowest ratings! Davidson had the audacity to tell the audience of gold bugs that gold was going down. That’s like a preacher telling the choir that God doesn’t love them anymore. People only want to hear what they already believe. They want affirmation. Turns out that Davidson was right. Gold trended down for the next 13 years.

Outside the main hall, where the speeches are given, booths are set up to promote and sell investment products. In one of the booths something caught my attention. There was a black box that looked kind of like a big telephone sitting on the table. I decided to check it out. “What is this, I asked? It’s a FAX machine. What’s a FAX machine? You can send documents to other people with it”. I asked the salesman, since it’s a brand new technology and so few people have one, “who would you be able to send messages to?” You might say I was shortsighted. And this is how new technology begins.

Susan was with me. How could I even think of going to China and not bring her along. During our free time, we went shopping and one afternoon. We passed a large rather exclusive looking shopping mall. I told Susan that I want to go in. I had an overwhelming urge to go in. This is not at all like me. Shopping is not a big deal to me and never before, or since, did I ever feel such a need to check it out. I ignored Susan’s comment that “There was no reason for you to shop for clothes at a shopping center in Hong Kong”. But I had to do it. I literally grabbed Susan by the arm and pulled her up the stairs. And then, who do I see coming down the stairs directly at me but Morris Gindi. 15 years earlier, when I was a buyer for Target Stores, Morris was one of my suppliers. He sold me beach towels. Susan and I became very close friends with Morris and his wife Jill. We vacationed together and even stayed at their home in Brooklyn whenever I was in New York on a buying trip. After I left my job at Target, our friendship came to an abrupt and awkward end. We hadn’t spoken to the Morris for nearly 15 years. It had bothered me ever since. I hated the way things ended up between us. So here we were, half way around the world and suddenly we were, face to face. What are the odds of this happening? It could not have just been a “coincidence.” My urge to go up those stairs was overwhelming. I had to do it. And there is Morris. This was more like “fate” than a coincidence. I believe to this day that I needed to resolve the issues that ended our friendship and the fate presented me with an opportunity. This was indeed a memorable speaking engagement at a financial seminar.

Do You Believe In Psychics?

Yes, I believe in fate. And I believe that some people have special psychic gifts as well. Daryl Jason told Susan, “You are one of the most psychic people I have ever met.” But I am getting ahead of myself. When Susan was in her late 20s a friend of ours read her palm and told her, “You won’t live to be 30.” I know it is ridiculous, but it bothered her a lot. So on one of my buying trips to New York, I took Susan with me so she could get a second opinion. I mean I thought this was all pretty silly, but Susan didn’t and this was a perfect opportunity to put it all to rest. We stayed with a friend of mine who lived in the Village. He had a girlfriend, Sheri, who we had never met before. Susan asked her if she knew someone who could read her palm? Sheri said, “As a matter of fact, I do.” Sheri was the Director of Publicity for Simplicity Patterns and recently she sponsored an event for Simplicity Patterns for women in New York City who headed up clubs and organizations. After the presentation, as the women were leaving the auditorium, Sheri glanced down at the sheet that listed the attendees, and she came across the name Daryl Jason whose title was president of Taro Cards Of America. She thought to herself, this would be an interesting lady to talk to. Suddenly a woman stopped and said to her, “I am Daryl Jason, the person you wanted to talk to. You are living with a man of your same sign and the stomach problems you have been experiencing will go away. If you ever need me, here is my card.” Sheri was impressed. She is a Pisces and so is her boyfriend. What are the odds of knowing that? (144 to 1) and she was experiencing stomach problems, that no one knew about. So Sheri told Susan, “I’ve got the perfect person for you to see.” The next day Sheri and Susan left to see Daryl Jason, and my friend Dean and I spent the afternoon listening to Cheech and Chong records.

When the girls returned, Susan was pale. She proceeded to tell me about her visit with Daryl. First of all, she reassured Susan that she would live well past 30, which was a relief, and she also told her, “You are married to a Pisces who was born on March 11, and he has dark curly hair.” Correct! She told her, “Your mother died four years ago from cancer.” Correct! She told her, “Your husband is an old soul. He has been here many times before and his purpose in this life is to discover his emotions.” Now this really got my attention because this one sentence really gets to the core of who I am. How could she possibly know this? In fact, that went a long way toward explaining why I was so influenced by Camus’ Meursault (The Stranger) who led a life of “interested indifference.” That was how I led my life too, so if Daryl was correct, and I have been here many times before, then I could be indifferent, since I would have been there and done that countless times before. Well, that’s what I thought. Daryl also told Susan, “You are scheduled to go on a trip very soon, but you will not go.” Susan had won a scholarship to go to Cambridge for two weeks and was supposed to leave next month. Her passport didn’t show up and she never did make the trip. This was all very interesting, but I didn’t think much about it until – some six months later Susan and I were having a terrible fight (we never fight) and our marriage was about to break up. This is the only time that ever happened. Then the phone rang. I picked it up and the operator said, “Collect call for Susan from Daryl Jason.” I handed the phone to Susan, “I know what is going on there now. Stop it! Don’t you know that you and David are meant to be together forever?” This was the only time she ever called and the call came at the exact moment it was necessary. Daryl and Susan had a special psychic link and she understood what was happening at that very moment. She told Susan, “Your are one of the most psychic people I have ever met.” Susan was a sender, and Daryl was the receiver. That is the one phone call in my life I will never forget.

A week later a letter arrived from Daryl and in it she laid out our life for the next several years. The letter was placed on a drawer and forgotten. Three years later we moved, and while packing up, we found the letter….everything she wrote had come to pass, exactly as she said it would. We never spoke with Daryl again, but yes, there are some psychics who are the real deal. I have never forgotten her statement to Susan that life is eternal and we all come back to learn new lessons – until we no longer need to come back again.

Whether through religion or otherwise, it is comforting to think that life is immortal. After that phone call, everything that she told Susan took on an entirely new level of credibility.

This really did happen and I am not embellishing anything here. I wish she were here now to tell me where the precious metals markets are headed.

I have three interesting articles for you today. Check out Bill Bonner’s America’s Real National Emergency, and Egon von Greyerz’ The Biggest Short and The Spectacular Long, and SRSrocco’s Central Banks Buy Up Garbage Assets To Keep The Economy From Collapsing.

By Bill Bonner

America’s Real National Emergency

PARIS – Donald Trump thinks there’s a national emergency on America’s southern border.

Bridgewater’s Ray Dalio was on 60 Minutes over the weekend; he thinks American capitalism is such a mess – and that inequality of wealth is so skewed – that the president should call a national emergency to fix it.

But the real emergency lies elsewhere.

FULL ARTICLE HERE

Egon von Greyerz

THE BIGGEST SHORT & THE SPECTACULAR LONG

The astonishing Fed again proved the consistency of its inconsistency.

Since its creation in 1913, and especially after WWII, the Fed has always been behind the curve. It is hard to believe that this is just incompetence. The recent change of policy hardly seems to be part of a plan but rather another reaction to events. Looking back at the Fed’s policy decisions, it is clear that virtually all are reactive rather than proactive.

Central banks have been totally detrimental to the world economy. They serve no constructive purpose whatsoever. As a matter of fact, they are a menace to the world and actually make things a lot worse than they would be if the laws of nature would rule. The natural rhythm of ebb and flow would regulate markets effortlessly without the need for artificial interference by central banks. If demand for credit is too high, the law of supply and demand would restrict the supply by interest rates going up. And if there was no demand for credit, loans would be cheap with rates going down.

FULL ARTICLE HERE

SRSrocco

Central Banks Buy Up Garbage Assets To Keep The Economy From Collapsing

By purchasing increasingly worthless paper assets, we can thank the central banks for propping up the global economy for the past decade. Since the 2008 financial crisis, the top central bank’s have acquired $13 trillion worth of assets on their balance sheets. While the central banks label these balance sheet items as “Assets,” they are nothing more than glorified Paper IOU’s.

FULL ARTICLE HERE

The Holter Report

China’s “Weight”.

A couple of topics for you today that are connected, obvious, yet not understood or even contemplated at this point. First, have you ever wondered why the names of many fiat currencies refer to “weight”? Such as the Peso, Peseta, Lira, or Pound amongst many others? This is similar to the names of various roads, like “Saw Mill Rd.”. It was named that because years ago there was actually a sawmill down the lane. These fiat currencies with “weighty” names started out as receipts for either gold or silver. They were convertible into a specific amount of metal when presented at a bank.

In essence these currencies were representations of physical metal since they were redeemable but far easier to carry around due to the lack of weight. In today’s jargon, paper currencies that were redeemable in specie were “derivatives” of the metals themselves. Then as time went on, the redeemability was cancelled and the currencies became true fiat, unbacked by anything except the credit worthiness of the issuer.

Over time, ALL currencies have become fiat and these currencies steadily devalued. I would ask, how can anyone have the thought these currencies can gain value versus gold or silver over a long period of time if they were originally spawned as derivatives? Can a derivative ever become more valuable than that it originated from? The answer of course is no and should be followed by another question; can a monetary guarantee from any government ever be more ironclad than that of physical metal itself?

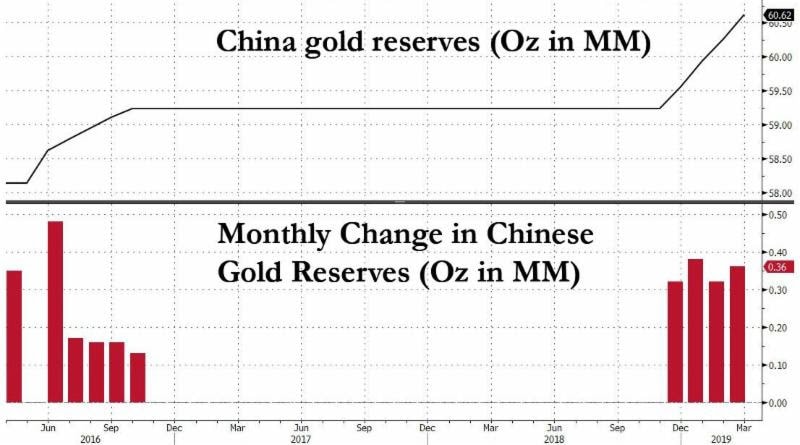

Next, we know for a fact Russia, China and other nations have been accumulating gold for years now. Why? I can assure you it is not to “trade” for profit to accumulate more fiat. They fully understand their own issued fiats and those of other central banks were at best only derivatives historically and not even remotely a derivative of gold now. Now, they are only poor joking derivatives of the various central banks and in no way a store of value.

One of our readers passed this commentary regarding a Zerohedge article along yesterday to us;

“This graph is pure transparency to those who understand the Chinese. Whether in trade agreements, military power, or their economic goals, they never show their hand.

Some estimate they are holding 20,000+ tons of gold.

I believe they will shock the world with twice that (40,000 tons).

That will be the day everything changes and it will be by their design.

Does anyone truly believe Russia doesn’t know this ?”

Think about what is said here and truly what it means? When China does fully announce their gold holdings, they will most likely not make the yuan convertible into gold. Their gold holdings will simply act as a backstop for confidence in the currency. As Jim puts it, the gold hoard will act as the Hope Diamond around a woman’s neck as she walks into the room. No one will really look at the woman, so whether she is homely or not does not matter, only what is around her neck …and this would be China’s gold holdings and to a lesser degree Russia’s.

We are talking about “financial warfare” here. Russia and China fully understand the fraudulent nature of Western fractional reserve banking and finance. They understand how and why the West will fail and have been acting to accumulate gold as buffer against (or in place of) any dollar holdings. They have set up trade deals, lending/credit and clearing facilities, and treaty’s of all sorts with many nations. Put simply, they are making ready for the coming failure of the West!

Putting this together, China will be moving the currency pendulum back toward derivative status. As mentioned, I do not think the yuan will become convertible because if it was convertible …conversion is exactly what will happen. Instead, they will use their gold holdings as a sign of fiscal and monetary responsibility. Though not truly a derivative because no direct connection to their gold, the yuan will be favored versus other fiats because of the held gold. If you understand that we are currently at war, financial war, then you understand “why” foreign nations are accumulating gold. The old saying “he who owns the gold makes the rules” will apply here.

To finish, if you are waiting for gold to break out above the five+ year trading range before you position yourself, good luck! As a nation, we will be completely screwed without gold holdings because our dollar will be shunned internationally as one issued by a central bank with paltry if any actual gold holdings. China will mark up the price of gold making their hoard mighty …and making it very difficult for anyone ever to catch up if trying to pay with fiat and no Hope Diamond around their neck!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

Archived Newsletters

4/10 Watching Gold And Silver Is Like Watching The Grass Grow

4/8 Silver Now-Eight Years Later

4/5 Is This Patriotism? Is This How We Make America Great Again?

4/2 ZIRP and NIRP

4/1 How Many Times Have You Heard “You Can’t Eat Gold” As A Reason NOT To Own Gold?

Market Report April 12, 2019

International Storage

Private Safe Deposit Boxes – Frequently Asked Questions

About Miles Franklin

Miles Franklin was founded in January, 1990 by David MILES Schectman. David’s son, Andy Schectman, our CEO, joined Miles Franklin in 1991. Miles Franklin’s primary focus from 1990 through 1998 was the Swiss Annuity and we were one of the two top firms in the industry. In November, 2000, we decided to de-emphasize our focus on off-shore investing and moved primarily into gold and silver, which we felt were about to enter into a long-term bull market cycle. Our timing and our new direction proved to be the right thing to do.

We are rated A+ by the BBB with zero complaints on our record. We are recommended by many prominent newsletter writers including Doug Casey, Jim Sinclair, David Morgan, Future Money Trends and the SGT Report.

For your protection, we are licensed, regulated, bonded and background checked per Minnesota State law.

Miles Franklin

801 Twelve Oaks Center Drive

Suite 834

Wayzata, MN 55391

1-800-822-8080

www.milesfranklin.com

Copyright © 2019. All Rights Reserved.