Federal Reserve Fireworks This Wednesday According to Q?

After watching Federal Reserve chairman Jerome Powell change his tone in regards to Fed tightening over the last few months, the financial markets are largely expecting no action out of the central bank on Wednesday.

Although one potential wild-card has emerged, that could possibly make this week’s meetings one of the more memorable ones in recent times.

Certainly after watching the way the stock market started to really run into trouble last fall as interest rates were rising, it was hardly surprising to see the reversal by Powell and the Fed.

President Donald Trump even joined the action by criticizing the Fed for raising rates too quickly. Even though we’re a decade after the last crisis, and the Fed funds rate is still only at 2.5%.

Which is in direct contradiction to the notion that both Trump and the Fed have attempted to promote of the economy being strong and healthy. Because if that’s the case, why isn’t it time to normalize the rates and balance sheet yet?

However we live in a world where bankers and politicians don’t always do as they say, and don’t always say what they truly mean. During Trump’s election campaign he was talking about a gold standard, auditing the Fed, and how the stock market was a bubble. Now he’s done a 180 since then, and it’s a bit of a mystery what many of the key players might actually be thinking and planning.

Which is even more interesting now with the growing attention centered around the internet voice known as Q (or Qanon). Who many believe is a source of intelligence coming from within the White House.

To be clear, I am happy to admit that while I have been following the story, I am still discerning how much confidence I feel in the veracity of the posts. Yet with that said, I continue to hear from intelligent analysts who I trust and respect who have been completely won over and believe the messages are legitimate.

Which makes Q post 2575 rather intriguing. Especially ahead of this week’s Federal Reserve meeting.

(image courtesy of qanon.pub)

Whether this will manifest on Wednesday will be darn fascinating to watch. I have one reader who suggested to me that a 50-basis point hike may be coming this week. Which if that were to occur, especially given the context, would represent one of the more stunning events I can remember in financial history.

As not only would it serve as a confirmation of the messages Q has been sending, but also of the battle going on behind the scenes that many analysts and commentators have been talking about since before Trump took office.

Such a hike would also be significant in that it would be an indication towards the Fed really being prepared to let the bubbles pop. Which I was not sure they would ever really do, although if there is a 25-basis point hike, let alone a 50-basis point increase, the stock market conditions witnessed back in September and October could well end up looking like an appetizer compared to what would come next.

If nothing else, you can never argue that what’s going on is not more interesting than your average TV show. As Trump has essentially created the most fascinating reality show ever out of the Oval Office of the White House. And perhaps even regardless of what the Fed does this week, seeing how these bubbles are ultimately deflated will be some of the most stunning financial history the world has ever witnessed.

On Wednesday we get the next clue on how that path ultimately unfolds. Chris Marcus

Arcadia Economics

“Helping You Thrive While We Watch The Dollar Die”

www.ArcadiaEconomics.com

First pass drill program returns encouraging results TSX VENTURE SYMBOL: FUU

KELOWNA, BC, March 20, 2019 /CNW/ – FISSION 3.0 CORP. (“Fission 3” or “the Company“) is pleased to announce results from the first pass drill program at its Key Lake South properties (Karpinka Lake and Hobo Lake projects) in the south-east Athabasca Basin region of Saskatchewan, Canada. A total of ~1300m was drilled in eight completed holes, all of which encountered variably intense hydrothermal alteration and six holes with anomalous radioactivity. Of note, holes KL19-005, KL19-006 and KL19-007, drilled in the northern part of the extensive land package, encountered the most significant hydrothermal alteration and paleoweathering, which are considered important factors for hosting high-grade uranium mineralization and will be prioritized for follow up. With $6M in the treasury, Fission 3 is well poised to continue to explore on its extensive property portfolio.

Winter program at Key Lake complete: Eight holes in 1300.8m in the Key Lake South projects (Karpinka Lake and Hobo Lake) – located on the south-east region of theAthabasca Basin, 40 km south of the basin margin in a geological setting analogous to Fission Uranium’s Triple R deposit at PLS.

Drilling intercepted multiple anomalous and narrow radiometric anomalies and strong alteration: drill holes located in the northern area of the property (holes KL19-005, KL19-006 and KL19-007) have exhibited the strongest hydrothermal alteration and paleoweathering profile.

Prospective for high-grade mineralization: KL19-005 intersected over 100m of strong clay alteration and faulted rock, which is interpreted to represent a major structural dilation zone. Such settings are important in the genesis of structurally hosted uranium deposits as they provide a pathway for large amount of hydrothermal fluid flow and can develop traps for localizing mineralized fluids. Most of the Athabasca Basin’s major uranium deposits are situated in similar geological settings.

Cree Bay exploration upcoming: Fission 3.0’s ongoing portfolio exploration program will now move to Cree Bay, conducting ground geophysics surveys to assist with the planned summer drill program.

Ross McElroy, COO, and Chief Geologist for Fission, commented, “The drill program at Key Lake is the latest step in the ongoing exploration of our prospective uranium projects. With radioactivity and strong alteration in multiple holes, we are looking at very encouraging first pass results that warrant follow up drilling. The winter program will now progress with a ground geophysics DC resistivity survey on our Cree Bay property in the northeast basin area, as we focus on developing high-priority drill targets to be tested during the summer exploration program.” About Key Lake South: The Key Lake area is an important historic mining district. The Key Lake operations is owned by Cameco Corp. (83%) and Orano Canada Inc. (17%) and hosted the former Key Lake mine, which produced 208 million pounds of uranium between 1975 to 1997 and is home to one of the largest uranium mills in the world. The Key Lake mill processed ore from the McArthur River uranium deposit, until Cameco announced in 2018 that McArthur River mining would be suspended indefinitely due to low uranium prices. The area is considered highly prospective to discover significant new uranium occurrences.

The 100% owned Key Lake South Projects consist of two projects (Karpinka Lake and Hobo Lake) covering 19,377 ha in 42 mineral claims. The properties are located approximately 40km south of the historic Key Lake mine. The projects are geologically situated within the extremely prolific Wollaston-Mudjatic Transition Zone “WMTZ”, notable for hosting the majority of the major high-grade uranium deposits on the eastern side of the Athabasca Basin. To the north, the Key Lake Deposit is hosted within the northern portion of northeast-southwest trending litho-structural feature known as the Key Lake Shear Zone “KLSZ”. The KLSZ continues southward through the Karpinka Lake and Hobo Lake projects. Together the properties cover approximately 50km of trend of the KLSZ, where a number of geochemical uranium anomalies have been discovered and where a network of EM conductors exhibit structural complexity including off-sets, breaks, folding and other geophysical features such as gravity and resistivity lows. These features are often associated with uranium mineralization occurrences. Key Lake South Projects – Drilling Summary Table 1: Winter 2019 Key Lake South Drill Hole Summary

Property

Target

EM Conductor

Hole ID

Collar

* Down-hole Radiometric Highlights

with Mount Sopris 2PGA-1000 Natural

Gamma Probe

Overburden

Depth (m)

Total

Depth (m)

Azimuth

Dip

From (m)

To (m)

Width (m)

CPS Peak

Karpinka

Lake

Key Lake Shear Zone

FOR-B-2220

KL19-001

79

-75

99.9

100.2

0.3

743

18.0

149.0

111.3

111.9

0.6

884

114.9

115.3

0.4

984

126.5

126.8

0.3

948

129.4

131.8

2.4

1431

FOR-2

KL19-002

274

-50

53.5

53.8

0.3

1344

2.1

101.0

79.1

80.2

1.1

985

FOR-B-2220

KL19-003

257

-63

217.2

218.1

0.9

1492

15.3

251.0

220.3

220.6

0.3

693

KAR-3160

KL19-004

277

-54

69.1

70.0

0.9

1302

37.6

125.0

KL19-005

86

-61

No anomalous radioactivity

39.0

128.8

KL19-006

90

-52

No anomalous radioactivity

57.0

101.0

KL19-007

86

-67

113.7

114.3

0.6

840

29.0

152.0

118.7

119

0.3

595

N/A

KL19-008

271

-55

212.3

212.5

0.2

550

7.3

293.0

TOTAL

1300.8

KL19-001 KL19-001 was an angled drill hole oriented parallel to the intermittent, weak, calc-silicate hosted radioactivity intersected in historic hole RO-01. The purpose of KL19-001 was to test the radioactive calc-silicate from the top of bedrock down to a depth of approximately 150m. Bedrock was intersected at a depth of 18.0m down hole and was comprised of variably clay, hematite, graphite and chlorite altered schist, cataclasite and calc-silicate. A strongly hematized calc-silicate was cored from 126.8m to 132.5m down hole which returned weak radioactivity up to 590 cps on a RS-125 handheld scintillometer. No other anomalous radioactivity was intersected, and the hole was terminated at a depth of 149.0m in weakly altered graphitic schist. KL19-002 KL19-002 was an angled drill hole targeting the Key Lake Shear zone (KLSZ) approximately 950m south of KL19-001. Bedrock was intersected at a depth of 43.0 m down hole and was comprised of weakly altered orthogneiss and calc-silicate gneiss to a depth of 72.9m. From 72.9m to 80.3m a strongly sheared biotite-garnet gneiss was cored with a central 5.2mwide graphitic brittle-ductile fault zone. The hole was terminated at a depth of 101.0m in fresh orthogneiss. KL19-003 KL19-003 was an angled drill hole targeting the weakly radioactive calc-silicate approximately 75m below that intersected in KL19-001. The drill hole aimed to assess the variability in previously intersected calc-silicate thickness and radioactivity with depth, and to test for parallel radioactive calc-silicate lenses. Bedrock was intersected at a depth of 15.3m down hole and was comprised of a thick sequence of biotite schist to a depth of 182.5m where a sheared, graphitic schist was intersected. A weakly radioactive calc-silicate lens was cored from 222.2m to 224.5m which returned up to 410 cps on a RS-125 handheld scintillometer. The hole was terminated at a final depth of 251.0m in fresh orthogneiss. KL19-004 KL19-004 was an angled drill hole testing the southern extent of a large left stepping electromagnetic conductor trace ~7km north of KL-001. This flexure is interpreted to reflect a dilational zone in the KLSZ caused by sinistral strike-slip movement. Bedrock was intersected at a depth of 37.0m down hole and was comprised primarily of weakly hematite altered orthogneiss. An intercalacted sequence of weakly graphitic biotite-garnet schist and cataclasite was cored from 42.7m to 66.9m down hole. No anomalous radioactivity was intersected, and the hole was terminated at a depth of 125.0m in fresh orthogneiss. KL19-005 KL19-005 was an angled drill hole testing the same large, left stepping KLSZ VTEM conductor trace as KL19-004, approximately 1 km further to the north. Bedrock was intersected at a depth of 39.0m down hole as was comprised of moderately to extremely bleached, clay, hematite, chlorite and graphite altered orthogneiss. A strongly graphitic, clay and chlorite altered cataclasite was intersected from 85.5m to 94.5m down hole. Thin limonitic fractures in the graphite altered orthogneiss at approximately 78m down hole returned elevated radioactivity up to 200 cps on the RS-125 handheld scintillometer. The hole was lost due to ground conditions at a depth of 128.8m in strongly chlorite and graphite altered orthogneiss. KL19-006 KL19-006 was an angled drill hole testing the up-dip projection of the graphitic cataclasite in hole KL19-005. Bedrock was intersected at depth of 56.0m down hole and was comprised of weakly clay and chlorite altered orthogneiss. The drill hole is interpreted to have overshot the graphitic cataclasite which down-dropped the bedrock surface to the east (normal faulting). No anomalous radioactivity was intersected and the hole was terminated at a depth of 101.0m in weakly chlorite and clay altered orthogneiss. KL19-007 KL19-007 was an angled drill hole testing the down-dip projection of the structural damage zone and strong alteration in KL19-005. Bedrock was intersected at a depth of 29.0m down hole and was comprised of extremely clay and chlorite altered graphitic cataclasite, variably altered graphitic schist, biotite schist and orthogneiss. Weak elevated radioactivity up to 160 cps was recorded on the RS-125 handheld scintillometer at 119.0m hosted in intercalated quartzitic and graphitic schist. Apart from the upper cataclasite no structural damage zone was intersected below KL19-005 and the hole was terminated at a depth of 152.0m in fresh orthogneiss. KL19-008 KL19-008 was an angled drill hole testing for the northern extension of the historic DD-Zone where previous historic drilling returned up to 0.78% U3O8 over 0.5m. Bedrock was intersected at a depth of 7.3m down hole and was comprised of a thick intercalated sequence of graphite altered amphibolite and calc-silicate to a depth of 136.8m. Below 136.8m, the hole encountered weakly altered to fresh biotite-garnet schist and graphitic schist. A 0.20m granite intrusion at 90.5 m depth returned elevated radioactivity up to 540 cps. The hole was terminated at a depth of 293.0m in fresh biotite-garnet schist.

Natural gamma radiation in drill core that is reported in this news release was measured in counts per second (cps) using a Mount Sopris PGA-1000 Natural Gamma Probe and a hand-held RS-125 Scintillometer manufactured by Radiation Solutions. The reader is cautioned that scintillometer readings are not directly or uniformly related to uranium grades of the rock sample measured and should be used only as a preliminary indication of the presence of radioactive materials.

Samples from the drill core are split in half sections on site. Where possible, samples are standardized at 0.5m down-hole intervals. One-half of the split sample will be sent to SRC Geoanalytical Laboratories (an SCC ISO/IEC 17025: 2005 Accredited Facility) in Saskatoon, SK. Analysis will include a 63 element ICP-OES, and boron.

All depth measurements reported, including radioactivity and mineralization interval widths are down-hole, core interval measurements and true thickness are yet to be determined. Cree Bay Exploration: In 2017 a ground DC Resistivity survey was completed in 2 separate grids centered on sections of strong conductivity interpreted from a historic airborne GEOTEM electromagnetic survey on what was then the Cree Bay property. Fission 3 subsequently staked additional ground to cover the most conductive part of this anomaly. The winter 2019 exploration work will thus continue to extend the ground geophysics survey over the anomaly, to determine the highest priority drill targets. The program will consist of a winter 21 line-km ground DC Resistivity survey and 2 lines of Moving Loop TDEM survey will be conducted during April to cover the most geophysically prospective area identified from a historic GEOTEM electromagnetic survey. About Cree Bay: The Cree Bay property, located 20km south of the town of Stony Rapids, consists of 16 claims totaling 14,080 ha and sits on the inside edge of the north-eastern Athabasca Basin. The property is located along the major SW-NE trending Virgin River Shear Zone. Locally the conductive corridor is bound by the Black Lake Fault to the north and East Channel Fault to the south. The historic Nisto uranium mine, is located ~7.5km to the northeast, along the Black Lake fault.

The technical information in this news release has been prepared in accordance with the Canadian regulatory requirements set out in National Instrument 43-101 and reviewed on behalf of the company by Ross McElroy, P.Geol. Chief Geologist and COO for Fission 3.0 Corp., a qualified person. About Fission 3.0 Corp.

Fission 3.0 Corp. is a Canadian based resource company specializing in the strategic acquisition, exploration and development of uranium properties and is headquartered in Kelowna, British Columbia. Common Shares are listed on the TSX Venture Exchange under the symbol “FUU.” ON BEHALF OF THE BOARD “Ross McElroy” Ross McElroy, COO Cautionary Statement: Certain information contained in this press release constitutes “forward-looking information”, within the meaning of Canadian legislation. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur”, “be achieved” or “has the potential to”. Forward looking statements contained in this press release may include statements regarding the future operating or financial performance of Fission 3.0 Corp. which involve known and unknown risks and uncertainties which may not prove to be accurate. Actual results and outcomes may differ materially from what is expressed or forecasted in these forward-looking statements. Such statements are qualified in their entirety by the inherent risks and uncertainties surrounding future expectations. Among those factors which could cause actual results to differ materially are the following: market conditions and other risk factors listed from time to time in our reports filed with Canadian securities regulators on SEDAR at www.sedar.com. The forward-looking statements included in this press release are made as of the date of this press release and Fission 3 Corp. disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by applicable securities legislation.

SOURCE Fission 3.0 Corp.

For further information: Investor Relations, Ph: 778-484-8030, TF: 844-484-8030, ir@fission3corp.com, www.fission3corp.com

Matt Gili the CEO, President, and Director of Nevada Copper (TSX: NCU | OTC: NEVDF) sits down with Maurice Jackson of Proven and Probable to discuss the value proposition of Nevada Copper, which is on target for U.S. production in Q4 2019. Mr. Gili, provides updates on the flagship Pumpkin Hollow Project, which hosts both an underground and open-pit deposits. We provide an overview on the supply an demand fundamentals on Copper, where a prudent speculator may position themselves to take advantage of the copper supply deficit.

VIDEO

AUDIO

TRANSCRIPT

Source: Maurice Jackson for Streetwise Reports (3/18/19)

Matt Gili, CEO of Nevada Copper, talks with Maurice Jackson of Proven and Probable about his company’s progress in beginning copper production by the end of the year.

Pumpkin Hollow

Maurice Jackson: Joining us for a conversation is Matt Gili, president, CEO and director of Nevada Copper Corp. (NCU:TSX), which is on target to U.S. copper production by Q4 2019.

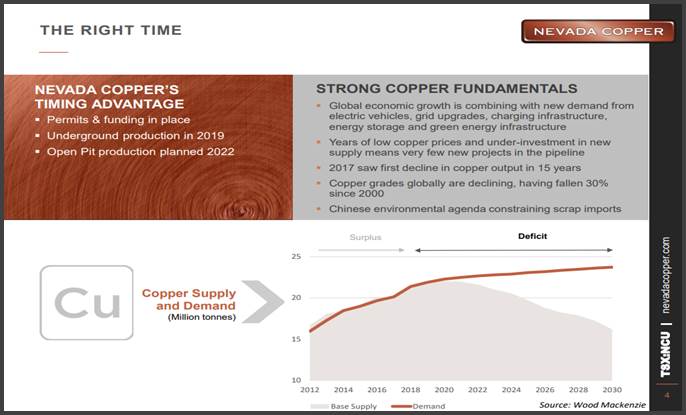

Nevada Copper has a number of successes to share with reader. But, before you share the unique value preposition of Nevada Copper, Mr. Gili, for readers who may not be familiar with the supply and demand fundamentals regarding copper, please provide us with a 10,000-foot overview. Matt Gili: When you look at the copper fundamentals, we see a very steady and predictable increase in demand of copper, modest amount, 1.5% per year. We see the move towards electrification of vehicles consuming more copper. We see other things that are offsetting that, but overall, a steady predictable 1.5% increase in the global demand for copper. Where the story really gets exciting, from the Nevada Copper standpoint, is with regards to the supply for copper. What we’re seeing is a lot of restrictions in future supply. We’re seeing a lot of difficulties on bringing on a future supply and backed up by work done by Wood Mackenzie and others, we’re projecting that by 2025, the world will be in a supply deficit of upwards of 6 million tonnes of copper per year. This just really supports what we’re doing in Nevada Copper in setting up the next copper mine. Maurice Jackson: Now that we have an overview of the supply and demand fundamentals for copper, Matt, let’s discuss how someone listening may position himself prudently as a beneficiary. For someone new to the story, can you give us a very quick overview of Nevada Copper? Matt Gili: Certainly. Nevada Copper, who’s Nevada Copper? We have an asset in Nevada called Pumpkin Hollow. This is our chief asset. It consists of two deposits: an underground deposit and an open-pit deposit for copper. We’re currently in the construction phase for the underground project with production from that underground project coming online later this year. I think we’ll talk more about that later. Regarding the open pit, we’re currently in the process of wrapping up the prefeasibility study for the open pit. You’ll see that being published in April of this year. Then, we have a regional land package of well over 15,000 acres that we are looking at really understanding, really unlocking the full value from that land package. That’s really Nevada Copper, building a copper mine coming into production later this year, with a lot of expansion into an open-pit mine, as well as regional exploration. Maurice Jackson: Let’s provide readers the latest updates on Nevada Copper, as the company has been very proactive on a number of fronts. Please provide us with an update on the construction progress. I would like to begin with the multi-million dollar question, are we on track to enter production in Q4 of this year? Matt Gili: Yes, Maurice, we are on track to enter production in Q4 of this year. We are very proud of that. The team’s doing a fantastic job. We have construction activities both on surface with Sedgman building the process plants, as well as underground cementation, both sinking shaft and doing lateral development on our main shaft. All that’s coming together very nicely. We are absolutely on track for commissioning of the plant in the fourth quarter of this year. Maurice Jackson: As Nevada Copper is preparing for production this year, have you increased your staffing to meet the growing demands? Matt Gili: That’s a really good question and yes, we have. We’ve increased our staffing. It’s an operational readiness question that you’re asking. This is where I want to stress to you and readers that this concept of operational readiness is foremost in our thoughts and how we’re planning for really becoming, not just building a great mine, but operating a great mine. When you look at the staffing, so far, our staffing, by design, is quite modest. We’re looking at a total workforce of Nevada Copper employees of around 30. That is because this is our model, a very lean, efficient operation. We utilize high-quality, expert service providers as necessary, to make sure that we are operating very efficiently. Maurice Jackson: Is Nevada Copper still actively recruiting and if so, what positions? Matt Gili: Yes, we are actively recruiting. Most of our positions open are technical and specialist positions, and would be part of the management team. I absolutely encourage anyone interested in what we’re recruiting for to contact the Nevada Copper website. You’ll see the complete listing of opening jobs there, as well as information on how to apply for any of these positions if you’re interested. Maurice Jackson: Pumpkin Hollow is unique in that you have both an underground and an open-pit mine. Let’s discuss exploration and expansion potential. What initiatives is Nevada Copper taking to optimize the full potential of the Pumpkin Hollow project? Matt Gili: We are in the process of constructing the underground, which has a large amount of upside potential. We’ll really only explore that upside potential when we’re underground, after we’re in production. We really look forward to updates on that front in 2020, and the reason for that is very simple. It’s just much more efficient to drill out the prospective areas of the underground from the underground; the holes are shorter. It’s just much easier. That’s really where the underground sits right now, in a holding pattern as far as expansion potential. When you look at the open pit, that’s where a lot of great energy is going into expanding the open pit, understanding the open pit better, really getting that ore body knowledge to allow you to build a world-class operation. That is part of the PFS, which is coming out in April of this year.

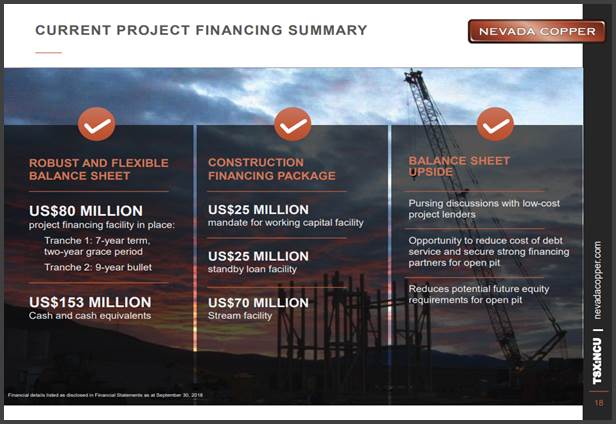

That PFS will include the drilling campaign that we completed in 2018, the 26 hole drilling campaign. It will include those results in the resource model. That’s going to give you an even better idea of the full potential of the open pit. The real excitement that we have is with regards to the region itself, a large region, relatively unexplored, but with large amounts of historical copper production, as well as great physical outcroppings of copper mineralization. This is really where we’re going to focus our efforts during 2019, to really get a chance, now that we’ve tied up this land package, to understand what we have. Maurice Jackson: Speaking of the region, there was a regional survey conducted that led you to staking more land. Can you share the results with us? Matt Gili: We staked a section a land that we refer to as the Teddy Boy Claims. This is about 5,700 acres of land to our northeast. We are very glad to have this in our portfolio. The criteria for that selection was we brought together experts on this region and experts in copper mineralization. They identified that as a really prospective area and where we should be really focused on. We’ve staked that land, secured it for our ability to explore over the next several years. Maurice Jackson: Does Nevada Copper plan to drill the new area at some point this year? Matt Gili: We plan on drilling this year. I really haven’t put out the entire drill program for 2019. We’re still pulling that together and analyzing where to best spend the monies we have available for exploration. We would like to drill that this year. Some more prospective holes, really not an in-depth blanket campaign, but probe a few really interesting areas over there and get a better idea for the drill campaign. Maurice Jackson: It’s one thing to have tonnage and grade, but you must equally have astute business acumen to make the numbers work. Now, Nevada Copper is in discussions regarding an ECA-backed project finance facility to further optimize the balance sheet, as well as lining up a working capital facility and further offtake agreements to improve the economics of Pumpkin Hollow. Please provide us with the details. Matt Gili: You kind of said it all. I can’t really provide you with any more details, but I can surely stress what you’ve just said, Maurice. We are in discussions with this export, credit agency style backed project financing. This is going to provide us the opportunity to substantially reduce the cost of our debt service, as well as attract strong and robust financial partners for potential future open-pit developments. Something we’re very excited about and it’s part of really creating Nevada Copper as a world-class company. Maurice Jackson: Let’s get into some numbers. Please share your capital structure. Matt Gili: The capital structure is well defined. We have $8 million in long-term debt. We have $153 million of cash or cash equivalents. When you look at the financing package specifically for the underground, we’re fully financed, including the working capital facility to take us through operation ramp up. The inputs into that are an equity raise that we did in the middle of last year, as well as a streaming deposit with regards to a stream arrangement on the precious metals strictly from the underground deposit. We also have a $25-million subordinated debt package. Really a standby loan facility that we can use if necessary. Maurice Jackson: In closing, I have a multilayered question. What is the next unanswered question for Nevada Copper? When can we expect a response? What determines success? Matt Gili: I would not classify our successful completion of underground construction and bringing them in operation as an unanswered question. That is going to happen, and I’m very proud of the activities that have happened so far. The real unanswered question for the investors out there, is what is the true potential of the open pit? There’s been a lot of great work done, a lot of exploration done, last year. That’s all been incorporated. I’m really going to be excited when the PFS is released and we can share the details of the open pit potential with the public. They are going to be very impressed and they’re going to see the picture. They’re going to see what we see when we get so excited about Nevada Copper. Maurice Jackson: Speaking of the prefeasibility study, give us a timeline on that, sir. Matt Gili: We’ll release that in April. I’m being careful. I don’t want to be too specific. It will be in April of this year. Next month. Maurice Jackson: Mr. Gili, last question. What did I forget to ask? Matt Gili: Maurice, forget to ask? You’re always very thorough, so I wouldn’t say you forgot to ask anything. What I would say is I want to reiterate something that we at Nevada Copper have been thinking about over the last month. Unfortunately, for the world, the last month has been a month marred with tragedies, with risk and with unexpected events. What we’re really stressing, with Nevada Copper, is the risk management of Nevada Copper. We are an operation that is on private land. We’re not waiting for any permits. We’re not waiting for records of decision. We’re utilizing EPC contractors, who have that fixed price nature, reduced risks. We’re building a dry stack tailing facility. We’ll never have a wet tailing storage facility at Pumpkin Hollow. We’re doing this all with a proven, experienced team of mine builders and operators. Really wrapping that up, that concept of low risk, risk mitigation. We are going to build and operate the next mine and there’s very little risk to that execution. Maurice Jackson: Matt, if investors want to get more information about Nevada Copper, please share the website address.

Matt Gili: Absolutely, www.nevadacopper.com. We love to get your input. You’ll see our investor presentationsthere in our latest news. Let us know what you think. Maurice Jackson: For our audience, we wish to remind you that Nevada Copper trades on the TSX symbol, NCU, and on the OTC symbol NEVDF. For additional inquiries, please contact Richard Matthews at (877) 648-8266 or you may email RMatthews@nevadacopper.com. Nevada Copper is a sponsor and we are proud shareholders for the virtues conveyed in today’s message.

Last but not least, please visit our website, provenandprobable.com, for mining insights and bullion sales. You may reach us at contact@provenandprobable.com.

Matt Gili of Nevada Copper, thank you for joining us today on Proven and Probable. Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world. Disclosure:

1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Nevada Copper. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Nevada Copper is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click herefor important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734. The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Images provided by the author.

Lance Roberts listed James Montier’s 7-Immutable Laws of Investing. They are:

Always insist on a margin of safety.

This time is never different.

Be patient and wait for the fat pitch.

Be contrarian.

Risk is the permanent loss of capital, never a number.

Be leery of leverage.

Never invest in something you don’t understand.

Those sensible rules apply to gold and silver.

ALWAYS INSIST ON A MARGIN OF SAFETY: Don’t buy gold or silver on margin. Always take physical possession personally or in non-bank storage vaults. Trust that governments and the banking cartel will drive nominal prices far higher as they devalue currencies.

Problem: The gold and silver paper markets (COMEX and LBMA) are managed markets. The managers are incented to maintain low prices. This will change. I believe prices will rise, slowly and then rapidly in 2019 and 2020.

THIS TIME IS NEVER DIFFERENT: The banking cartel will “print” fiat currency units until they can’t. Governments will spend in excess of revenues until they can’t. The only question is how rapidly fiat currency units fall in value.

BE PATIENT AND WAIT FOR THE FAT PITCH. Trust the banking cartel to push fiat currency units lower and gold and silver prices higher. Central banks (not the Fed) are buying gold. Individuals should buy gold and silver.

BE CONTRARIAN: When others proclaim gold and silver are dead, then buy. When gold or silver prices have increased by a factor of five or ten, reconsider the risk and reward profile.

RISK IS THE PERMANENT LOSS OF CAPITAL, NEVER A NUMBER: Gold and silver coins and bars will always stay valuable. There is risk of permanent loss of capital with COMEX paper gold and silver, buying on margin, or trusting banks to hold your metals. Minimize risk!

BE LEERY OF LEVERAGE: The COMEX creates leverage with paper gold and silver contracts. Assets can disappear but debt remains.

NEVER INVEST IN SOMETHING YOU DON’T UNDERSTAND:

All fiat currency units devalue.

Many currency units have turned into waste paper and are no longer used.

The almighty dollar is now a mini-dollar, and soon will become a micro-dollar.

Propaganda and government statistics may delay the inevitable, but they cannot prevent an implosion or reset.

The banking cartel created too much debt. That debt will be repaid in devalued fiat currency units or defaulted.

Gold and silver do not default and have no counter-party risk.

Gold and silver stored in a non-bank vault are boring. Sometime boring is good. History will show that 2018 – 2025 was one of those times when boring investments in gold and silver were necessary.

These sensible rules apply to debt-based fiat currencies.

ALWAYS INSIST ON A MARGIN OF SAFETY: With fiat currencies a supposed margin of safety is automatic. The government makes pieces of paper legal tender and prints more paper as needed. Governments and central banks encourage fiat currencies because controlling the currencies benefits them.

Problem: Politicians, governments and central banks inevitably print too many pieces of paper. The currency loses value and is replaced, shunned or becomes worthless. The “bad money” drives out the good money (gold and silver) because few people want to exchange valuable gold and silver coins for soon-to-be-worthless paper currencies. Zimbabwe, Venezuela, Argentina and the list goes on…

THIS TIME IS NEVER DIFFERENT: Most unbacked currencies have disappeared into the trash heap of history. Remaining fiat currencies – dollars, euros, pounds and yen – are devaluing every year toward worthlessness. This time will not be different regarding the demise of fiat currencies.

BE PATIENT AND WAIT FOR THE FAT PITCH: A “fat pitch” in the fiat currency world is a profit mania from speculative trades. Buy Amazon stock at $6 in 2001 and watch it run past $2,000 in 2018 – a huge win for fiat currencies invested in Amazon.

Problem: How do you find the next Microsoft, Netflix or Amazon?

Problem: Don’t overstay the party. Remember Enron, Global Crossing, and hundreds of other high fliers that crashed into the dirt. The investment landscape is littered with debris from winners that turned into losers. Deutsche Bank and General Electric sell for small fractions of their earlier highs.

Problem: When you cash out, how much will the fiat currency units buy? The banking cartel and government deficit spending guarantee further devaluation of fiat currency units.

BE CONTRARIAN: A contrarian buys when “blood is in the streets” and sells when everything looks rosy. Remember the “permanently high plateau” story before the 1929 crash. A contrarian knows propaganda from government accountants and central bank Ph.D.’s has limited usefulness. The cheerleaders sell their story and hope the public will keep their misguided faith in fiat currencies.

Problem: The contrarians in the fiat currency world want to escape. They buy hard assets including gold and silver. The managers of fiat currencies discourage opting out.

Problem: People might abandon fiat banks and only use cash. Their solution: Make cash illegal and force people to use digital currencies.

Problem: People might lose faith in stock and bond markets after multiple scandals and crashes. Solution: Force interest rates to near zero or negative levels and discourage parking cash in banks.

RISK IS A PERMANENT LOSS OF CAPITAL, NOT A NUMBER: The real risk is that the managers will abuse fiat currencies, print too much, and devalue the currency so far that people rebel. It has happened in many countries and will occur again. What is your capital worth if you measure your paper assets in dollars or euros and both currencies fall to near zero value?

BE LEERY OF LEVERAGE: Leverage results from investment debt. Buy stocks on margin and watch profits soar in a bull market or shudder as bankruptcies expand in the inevitable bear market.

NEVER INVEST IN SOMETHING YOU DON’T UNDERSTAND: Advisors encourage buying for the long term. Did they explain the inevitable loss of purchasing power of fiat currencies?

Problem: Fiat currencies must devalue. People hope the nominal gains from paper investments offset the devaluation of the currency.

Problem: If people realized how rapidly currencies devalue, they would object to rampant price inflation. Solution: create a Consumer Price Index (CPI) and “manage” the results.

Problem: Devaluation and inflation run in cycles. Inflation was high throughout the 1970s while hard assets soared, and the stock market stagnated. During the “age of paper” from the early 1980s to 2000, the stock market soared, and hard assets languished. Stocks have bubbled higher since 2011 while the COMEX crushed silver prices. Cycles favor hard assets for the next several years.

Solution: If we use unbacked debt-based fiat currencies, the stock markets, gold, silver and real estate will rise exponentially over many decades. After extended moves, the risk – reward profile changes. Now is a risky time for stocks and a high reward time for gold and silver.

Miles Franklin was founded in January, 1990 by David MILES Schectman. David’s son, Andy Schectman, our CEO, joined Miles Franklin in 1991. Miles Franklin’s primary focus from 1990 through 1998 was the Swiss Annuity and we were one of the two top firms in the industry. In November, 2000, we decided to de-emphasize our focus on off-shore investing and moved primarily into gold and silver, which we felt were about to enter into a long-term bull market cycle. Our timing and our new direction proved to be the right thing to do.

We are rated A+ by the BBB with zero complaints on our record. We are recommended by many prominent newsletter writers including Doug Casey, Jim Sinclair, David Morgan, Future Money Trends and the SGT Report.

For your protection, we are licensed, regulated, bonded and background checked per Minnesota State law.

Original Source: https://ceo.ca/@mickeymantle/march-madness

For those who follow College Basketball, the next few weeks are some of the most enjoyable and exciting months on the sports calendar. For those new to sports or living under a rock, March Madness brings together 64 teams in a single elimination tournament . The brackets get tighter with each round 64/ 32/ 16/ 8/ 4/ and finally a duke out between the 2 last remaining teams. As the brackets dwindle down the contests have sub names ” The Sweet 16 ” / “Elite Eight ” / ” Final Four ” and the ” Championship Game “.

The games are usually very exciting often coming down to the last possession and consequently there are usually quite a few upsets on the Road to the Final Four. In this spirit I have decided to make my own March Madness Tournament with my favorite Juniors participating.

This list was comprised of 12 stocks that I have been following closely and own shares in. The list has been pared down to The Elite Eight for the brackets to work out. I am using the share price of the companies (on 12-24-18) when article was published as a benchmark. I have attempted to put companies with similar share prices paired against one another. After each round the companies that have the highest %gain will move on to the next round. Simple enough now without any further ado … Lets’ meet the Elite Eight.

Bracket 1) MUX vs. IRV

McEwen Mining – this under valued producer striving to get a listing on the S&P. It’s share price is at the mercy of the price of Gold. It’s CEO, Rob McEwen draws a dollar a year salary. If the shareholders do well so does its leader. What a novel concept !!I It was recommended on 12-24-2018 @ $1.79/ MUX

Irving Resources- this tightly held sleeper is headed up by Quinton Hennigh ,which almost guarantees big things. Permitting is now in place and this one time huge producing mine in Japan is now drill ready and ready to rock. “Q” knows how and where to position the the Truth Meter to get it to confess vehemently. Price when recommended was $1.80/IRV

Bracket 2) JCO vs. FVAN

Jericho Oil – with steadily rising OIL prices… up over 30% in two months and located in the very friendly Oil state of Oklahoma in the prolific STACK region. It boasts having some mighty titans of the Oil industry as neighbors. It is only a matter of time before this gets legs and gains some well deserved attention. JCO/ 43 cents

First Vanadium – with a just released PFS report with staggering numbers, this tightly held stock needs to be revisited. The company just added 1.5 Billion pounds of Vanadium in very mining friendly Nevada which is currently going for close to $18 a pound. You do the math. Your head will spin. !!! FVAN /77 cents

Bracket 3) SIR vs. ANX

Serengeti Resources – A newly released PFS revealed an overall increase in contained metal from the 2016 Indicated Resource estimate. Which included increases of 44% for copper, 32% for gold, and 52% for silver in the M+I categories. This stock was hammered mysteriously on these fantastic results. Somebody wants this stock on the cheap and for good reason. Rick’s Cafe lives on in the Junior Sector. !!! SIR/17 cents

Anaconda Resources– this stock was once the darling of PDAC in 2018. My how much changed in a year. The company keeps putting out great news … to crickets. Perhaps new blood at the top would pump new life into this sleeper and get it back on track. There has been a buzz about M&A’s in the maritime and COB, Jonathan Fitzgerald is a cagey deal maker who makes great things happen. ANX/ 22 cents

Bracket 4) AZS vs. PRG

Arizona Silver Exploration – continues to amaze. It is slowly coming back to life and I believe still has plenty of upside. Sharp management who put their money where their mouth is. Share structure remains super tight, as they know how and when to finance without warrants. They have added 2 new highly prospective properties which are drill ready awaiting final permitting. This company is a blueprint for success on how to run a Junior Miner !!! AZS/ 8 cents

Precipitate Gold – this is run by a very sharp , intelligent ,savvy CEO , Jeff Wilson. They have smartly recently acquired a property in the Dominican Republic which butts up next to Barrick’s Pueblo Viejo Mine. This acquisition and the highly anticipated future drill results could make Jeff Wilson a legend. It seems new government in the DR is much easier to work with than previous scoundrels. Having savant Quinton Hennigh on the board adds to the allure. PRG/ 12 cents

A reminder we will check highest % gainers for my 12 Days of Christmas article and the price of each stock from the 12-24-18 benchmark to determine their performance in the tournament.

I am a fan of all of these companies and hold shares in each, some in great quantity in my own portfolio. So there are no losers among these companies only winners but somebody will prove to be a worthy champion in a months time !!!

This article is for informational purposes only. It is certainly not investment advise. It is also not encouraging any gambling or betting in any way. Please consult Gamblers Anonymous if you feel the need to waver on my tournament 🙂 Kevin Dougan (aka The Mick) runs a website Blue Sky Marketing which finds and promotes under valued and out of favor companies with much upside and potential growth. Many of these companies are clients and sponsors and I own shares in all of the companies mentioned in this article. Please sign up for my free newsletter on my website for monthly picks and updates. www.kdblueskymarketing.com

Ross McElroy the COO and Chief Geologist for Fission 3.0 (TSX.V: FUU | OTCQB: FISOF) sits down with Maurice Jackson of Proven and Probable to discuss the value proposition of Fission 3.0 and their Property Bank. In this interview Mr. McElroy provides the macro economics for uranium and how one may allocate their uranium holdings in a Uranium Project Generator with a Property Bank with projects located in high-grade uranium districts, with proven management and technical team that has a 20 year history of delivering success to shareholders.

VIDEO

AUDIO

TRANSCRIPT

Original Source: https://www.streetwisereports.com/article/2019/03/16/prospect-generator-in-position-for-uranium-turnaround.html Maurice Jackson: Joining us for a conversation is Ross McElroy, the COO and chief geologist for Fission 3.0 Corp. (FUU:TSX.V; FISOF:OTC.MKTS): A Uranium Project Generator and Property Bank. Ross McElroy, glad to have you back on the program to share the value proposition of Fission 3.0. Before we begin, Ross, I’d like to begin with some basic fundamentals regarding uranium. For someone new to the uranium sector, what is uranium, and where is it used? Ross McElroy: Uranium is really all about energy. The way we use uranium is for nuclear fuel. That’s basically the fuel that runs reactors.

Globally nuclear power constitutes between 15% and 20% of the electrical requirements. That’s really where the majority of the uranium is used. There is some uranium that’s used for strategic purposes on a country by country basis, more for the Department of Defense reasons. But really, the vast, vast majority of uranium is used to fuel nuclear reactors. Maurice Jackson: Provide us with some metrics on how abundant uranium is in the Earth’s crust, and correlate that to the average grade that is found versus the grade that is needed to define an ore deposit in a future mine? Ross McElroy: Well, uranium is actually one of the most abundant elements in the Earth. It’s kind of ubiquitous. You’ll see it throughout the Earth’s crust; there is trace amounts of uranium present primarily in volcanic and igneous rocks and sedimentary rocks.

On a deposit level, there’s actually a number of uranium deposits around the world, in every continent on the planet and in many countries. On a global basis, the average grade of a uranium deposit worldwide is around 0.1 to 0.15% U308.

Now, if you compare that to say, the deposits in Canada, they’re orders of magnitude higher grade in Canada. We’re talking orders of magnitude that are 10 to 20 times that of the global grade.

Although I’ve given you the average grade, most of those deposits at those lower grades, the average grades are really uneconomic deposits. We need grades that are generally much higher than the 0.1%–0.15% if it’s going to be an economic deposit. And that’s what Canada has. Canada has very high-grade deposits, so the economic metrics are just that much more attractive in Canada. Maurice Jackson: Now that we’ve identified uranium’s utility, what can you share with us from a supply and demand perspective? Ross McElroy: Well, it’s fairly simple to understand what the demand for nuclear energy is, in other words, uranium. We can just multiply the number of reactors around the world that are currently operating, and the known fuel consumption rate for a 1000 megawatt reactor is just under 500,000 pounds of uranium a year. If we look at the global reactors, there are around 450 reactors around the world. You can see that the need for uranium on an annual basis is around the realm of almost 200 million pounds of uranium. Maurice Jackson: How does the nuclear plant in Fukushima, Japan, fit into this narrative? Ross McElroy: Japan historically, up until the Fukushima event in 2011, was one of the main users on a country basis worldwide. Japan I think consumed almost 20% of the world’s nuclear power, in other words, 20% of the world’s annual production of uranium was used to run the Japanese reactors.

In 2011, of course, we had the magnitude 9 earthquake followed by a tsunami, and that’s what damaged the Fukushima facility. Interestingly enough, even with that magnitude of an earthquake and the soon-to-follow tsunami, the reactor still did not breach. The housing that surrounded the reactor was damaged, and this is where some of the radiation leaks came from, but the reactor itself actually held, and so the damage was actually very, very limited and manageable.

What happened is overnight, Japan shut down all of its nuclear reactors, in other words, all 52 reactors I think they had working at that time, went offline. That caused disruption to the supply/demand situation globally.

What’s happened since then is Japan is slowly coming back on. Japan’s alternatives for power are pretty limited as the country doesn’t have very much of its own resources, if any at all. It imports whatever energy that it needs, be it in natural gas now, in nuclear.

It’s important for Japan to be able to operate these factories that they’re running. I mean, it’s an exporting country around the world, so it does have high energy requirements. It also has the requirements for inexpensive power.

Japan is coming back on to the scene as far as nuclear power. There are eight reactors that are currently back up and operating, and 17 reactors that are in the near-term licensing for approval to get them restarted again.

I think the bottom line is, prior to Fukushima, Japan depended on nuclear energy for at least 25% of its electricity demands. I think by the time 2030 approaches, Japan is supposed to be right back up to those same levels. The country is coming back on, it has always been an important major consumer of nuclear power. I think we’ll see it right back to the equation again in the very near future. Maurice Jackson: Uranium, next to gold, is known as the other yellow metal, and here’s why. Ross, let’s step back to the bull market in uranium. If one was selective with the uranium holdings, they would’ve had generational changes in their portfolio. What was the spot price during the last bull market? Ross McElroy: Well, in 2002, uranium was around, I don’t know, about $15 a pound. This is on the spot market. That’s what uranium was trading for.

In 2003–2004, we really saw the lift off of the price of uranium. In fact, it peaked at 2007 to around $140 a pound. It went almost a 10-fold increase in the price of the commodity between 2003 and 2007. The peak at 140 didn’t last particularly long, but it had a slower decline until about 2008—2009, it stabilized, and then it peaked back up again.

Really, it was holding steady. I guess this is the point I would want to make, is that we were starting to see a steady state price of between $50 to $70 a pound, and then the Fukushima event hit that we talked about in 2011, and that really threw the whole pricing structure right out the window. We’ve been working on our recovery ever since. Maurice Jackson: What is the spot price for uranium today? Ross McElroy: Currently we’re about $28 a pound for uranium. It has recovered; we’re off the bottoms of $17, $18 a pound just a couple of years ago. Uranium is making its way back.

Maybe the important point here to note is we’re still at prices that the majority of mines around the world are not profitable. Even the lowest cost producers are really not operating in an environment where they can make money with uranium prices what they’re at right now.

What we’ve seen is that the supply is starting to be restricted as the producers are taking a lot of that uranium off market; they’re not supplying it to the utilities at this cheap price, because it’s not a working business model to lose money in the long run on the mining of the commodity.

We are seeing an improvement in the price of uranium, and it’s been about a year and a half in the making. It’s gone up from the $18 that I mentioned to about $28 a pound, but it certainly has a lot more room to move upwards even before we can start to get production back online to meaningful levels. Maurice Jackson: What is that spot price that companies right now, uranium companies I should say, for them to earn their cost of capital? Is the number around $60 for a spot price of uranium? Ross McElroy: I believe you are correct. We’re seeing prices that globally, they have to be in the $60 to $70 a pound really to bring on any meaningful production.

One of the clues that I look at when we look at the best uranium mines out there, the lowest cost producers, those would be McArthur River deposit in Canada’s Athabasca Basin in Northern Saskatchewan. That is one of the best uranium mines in the world, certainly the largest highest-grade operating mine. Cameco took that offline because of the prices of uranium where they were at, they weren’t making any money on the mining of this deposit.

There are some indications that Cameco won’t turn that mine back on into being a producer until the price of uranium is somewhat north of $40, maybe $45. Something in that realm.

I don’t have an exact number there, but it does tell you that if you’re going to even bring back the best of those deposits, you really need prices that are something of $40 to $45. As we mentioned earlier, the price for many of the other deposits around the world are probably closer to $60 or $70. You can see, there’s still lots of room for improvement. Maurice Jackson: The current price of uranium does not support the fundamentals. What correlations do you see today that may exceed the returns from the last bull market? Ross McElroy: Well, it’s sort of an elastic situation. I think that the longer that we keep depressed prices, yet the demand is still there and growing, reactors are being built, the need to fuel these reactors, that’s not stopping.

In fact, it’s growing. You have the primary suppliers of uranium, i.e., the mines that are not supplying it, the longer that the prices are low, the more rapid that climb will be in the price of uranium when it does correct.

I think there’s a possibility, as I’ve heard some analysts call it, a violent reaction upwards to the price of uranium. I think we’re going to see some substantial price increases within some short vision of time, maybe a year or two or three. Something in that realm that I think will be quite meaningful.

We’ll see what happens, but the longer it stays depressed, the more likely and quicker the rise will be when it does come. Maurice Jackson: Ross, you’ve provided a compelling case on the fundamentals for uranium. I know readers may be asking, how will all of this demand for uranium be met? Mr. McElroy, please introduce us to Fission 3.0. Ross McElroy: Fission 3.0 is a uranium explorer. This is a company that we spun out of Fission Uranium Corp. (FCU:TSX; FCUUF:OTCQX; 2FU:FSE), our larger company, back in 2014 when we bought out our partner on the Patterson Lake project, and in so doing with that process from that arrangement, we spun out our non-core assets, the more grassroots exploration projects.

We’ve been able to build up an exploration portfolio, primarily focused in the Athabasca Basin. Remember, the Athabasca Basin is Canada’s only producing uranium field. That’s where the McArthur River deposit is, this is where Fission Uranium has the Triple R deposit. There’s some fantastic deposits out there.

That’s what we’re exploring for in Fission 3.0. We’re looking for the next high-grade uranium deposit in the Athabasca Basin. Maurice Jackson: You referenced that you’re a project generator. There’s a lot of ambiguity regarding project generators. Please share the virtues and why Fission 3.0 took on the project generator business model? Ross McElroy: Project generators are really all about sharing the risk. In our case, what we do very well is pick ground. We’ve been able to strategically stake ground in the Athabasca Basin, we’ve made discoveries on two of our properties, the first one in the company called Fission Energy that we made the discovery at our Waterbury Lake property, and later on in Fission Uranium Corp on our PLS property.

That have been situations where we’ve had joint-venture partners sharing the risks, sharing the costs with others. To use the model, what we do is we use our brands and other peoples’ money. That’s really what we’re good at, that’s basically the model that we have.

We have a very highly trained technical team that’s exceptional at picking out high-quality projects. We attract other people who are looking to get into the uranium business, looking to partner up with a team such as ours and join us for the ride to make a discovery.

It’s really all about sharing risk. That’s really what the project generator model does. It’s our land, and we partner with good quality people that can fund a project, and that’s how they earn into it as well. Maurice Jackson: Do you currently have a joint-venture partner? If yes, who and what are the terms of the relationship? Ross McElroy: We have had joint-venture partners in the past, and very successful ones. As I mentioned earlier on our Waterbury project, we had a partner with the Korean utility called KEPCO. It earned in by spending a certain amount of money on the property each year over the course of a three-year period.

What we did with that, we were able to make a discovery, using the money in that project, we made a discovery, built up the resource estimate on there, and eventually sold that asset. That was how our shareholders were able to take advantage of our monetizing on the property.

I guess we could say the same at the PLS project, which we now own 100% of it, but that was also a partnership. We shared in the risk early on and in the money early on with our partner. We eventually bought them out in 2014. That was another example of a successful joint venture partnership.

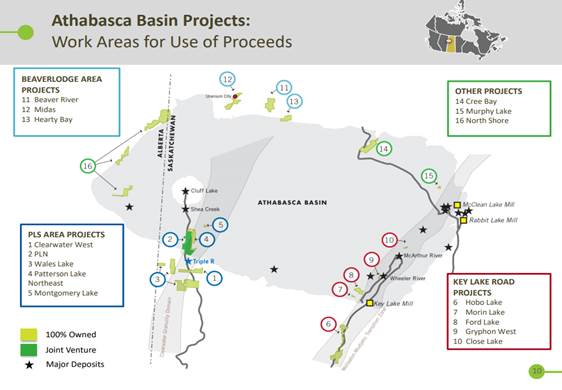

Each one of the deals would be a little bit different from each other. It is a model that we think works very well. I will note that in our property down in Peru as well, we have a partnership that we’re still looking to finalize the deal. This is one where another group has approached us, said it’s interested in the potential of a property down in Peru. It will spend a significant amount of money having us as the operator. Hopefully we’ll make a discovery down in Peru as well. Maurice Jackson: Well, you’ve just alluded to my next question. Fission 3.0 has 18 projects in its project bank. Now, it is strategically located in premier, high-grade uranium districts in Canada and Peru. Mr. McElroy, introduce us to the Fission 3.0 Project Bank (click here). Ross McElroy: We have 18 properties in the Athabasca Basin. Our properties, we think that everywhere in the Athabasca Basin has the potential to host high-grade uranium projects.

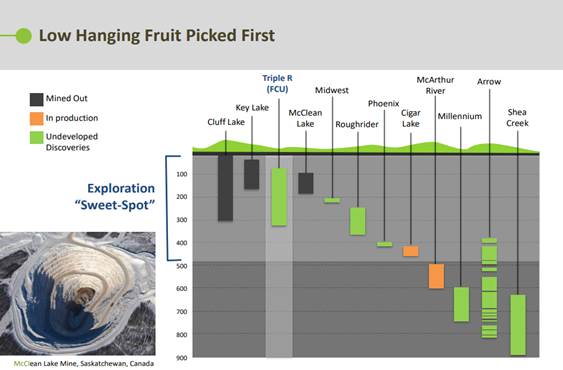

One of the keys that we seek to identify are deposits that will be shallow. In other words, the closer a deposit is to surface, the easier it is to build a case that this could be a project that could go into production. It’s an easier mine to develop the closer it is to the surface.

Really deep deposits are challenging. They still exist, but they’re challenging. Eventually they cost more money to find and cost more money to get out of the ground. They’re just another level of challenge.

If you look at our 18 properties, they’re all in and around the edge of the Athabasca Basin, where we’ve had a great deal of success finding near-surface mineralization.

Our PLS project that hosts the Triple R deposit in Fission Uranium is a great example of a near-surface deposit. The mineralization starts at 50 meters below the surface, so 150 feet below the present-day surface is where the high-grade mineralization starts. That makes it a potentially open-pit deposit, which is generally low cost and gives you a lot of flexibility.

This is the sort of thing that we’re looking for in Fission 3.0. We’ve got very good properties that are in known mining districts, conversely, we have a good portfolio of ground around the southwest side of the basin where our PLS project in Fission Uranium is hosted, and also NexGen’s Arrow deposit, it’s all in that same area. We have the significant land package that surrounds that area.

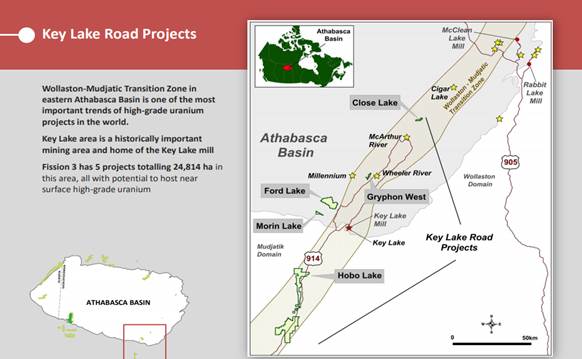

We also have a good strategic land package in and around the Key Lake area on the southeast side of the basin. This has been, and still currently is the hot bed of uranium mining in Canada right now. This is the side of the basin where the McArthur River and Cigar Lake deposits are located.

McArthur shut down for economic reasons waiting for higher uranium prices. It was an operating mine up until about a year ago, and Cigar still is in operation. You’ve also got the Key Lake mine.

It’s a strategic area to have a good land package. We think there’s lots of opportunities in and around land in that area to make a new discovery.

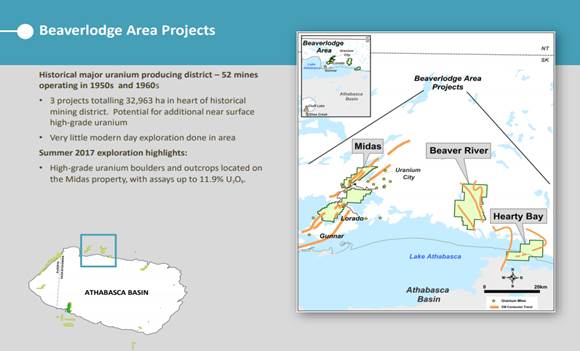

And probably third for us is the land package that’s up in the northwest side of the basin, in the old uranium city Beaverlodge district where uranium mining in Saskatchewan first got started back in the 1950s and was the going concern back in the ’50s and the ’60s, I think there were about 52 operating mines up in that area, pretty small scale most of them, but still lots of high-grade uranium. That’s an area where we think that there’s still plenty of exploration potential.

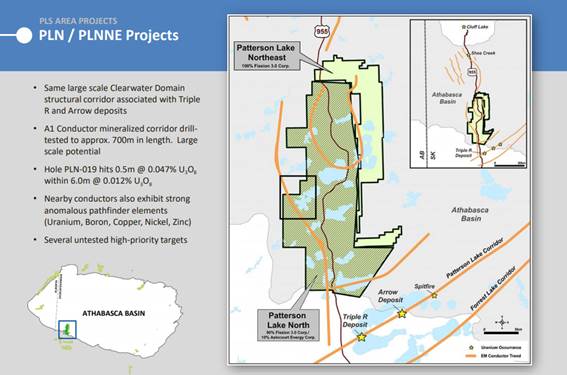

Between all those areas, we’re going to be active and we’re going to be looking for the next high-grade uranium deposit in Saskatchewan. Maurice Jackson: Speaking of being active, is there active drilling going on right now in these projects? Ross McElroy: There is active drilling. We did drill in the southwest side of the basin. We were drilling in January on our PLN project. That project is just immediately north of Fission Uranium’s PLS project.

You’re really talking about the same area where the latest discoveries have been found, where you’ve got the Triple R deposit, you’ve got NexGen’s Arrow deposit. These are two of the best new deposits that have been found in the Athabasca Basin in the last 15 years.

We have a package around there called PLN, and we did drill six holes in there earlier this year. It has the potential to host another one of these fantastic deposits, so we are going to continue looking there. We see all the signs present that tell us that this is where we’ll make that discovery.

As we’re speaking right now, we’re drilling over in the Key Lake area that I described earlier. This is over on the southeast side of the basin, about 200 kilometers to the east of the PLS drilling. That is a program where we’ll drill probably eight or nine holes, just south of the Key Lake Mill and the old historical Key Lake deposits. There’s areas of activity there. We’ll continue drilling throughout the rest of 2019 on a number of our projects.

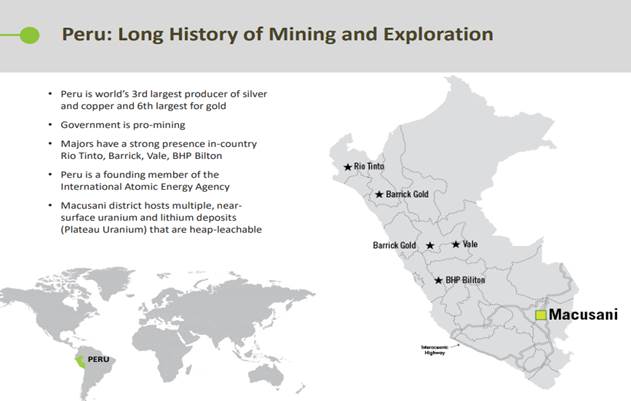

Fission 3.0 is active. We were able to raise some significant money early in the year, in late 2018. We’re going to be active. This is how we’ve been successful in the past, is by being aggressive, looking in places where people probably haven’t looked for a while or never even thought to look, and putting our technical team to work. Yes, you’ll see pretty good news flow out of Fission 3 this year. Maurice Jackson: Ross, let’s expand the narrative on the project bank portfolio and go south into Peru. What can you share with us there? Ross McElroy: Peru is a really interesting area. Where our projects are is called the Macusani Plateau, located in southern Peru, near the Bolivian border. The Macusani Plateau has shown at least over 100 million pounds in near-surface uranium deposits.

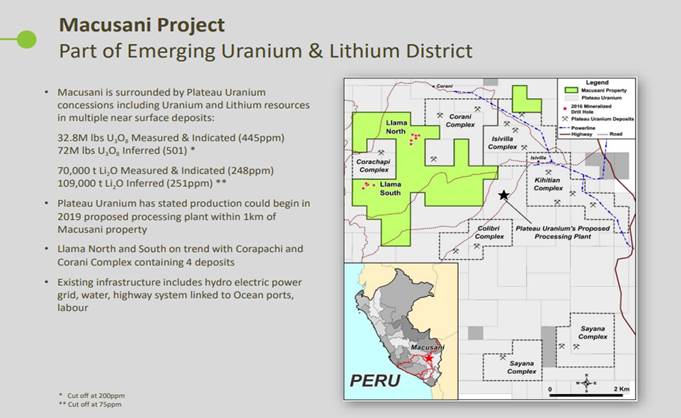

There’s a company down there that’s quite dominant called Plateau Energy. Plateau has been able to stake a lot and consolidate a land package in the area, and consolidated all these old deposits. It has amassed around 100 million pounds of uranium in these uranium deposits.

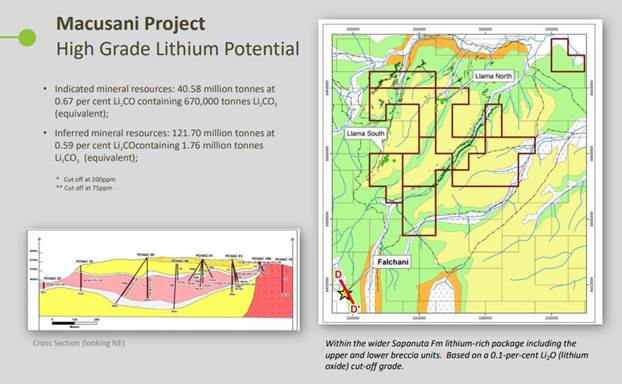

However, even more significant, Plateau made a discovery of high-grade lithium in the same area, and in fact, that’s within five kilometers of our southern property boundary on our Macusani plains. Not only do we have the potential now to host near-surface uranium deposits, and we have shown in fact that we do have mineralization on our property for uranium, we’ve mapped it, we’ve drilled, we’ve trenched and found high-grade uranium, but now the potential’s there for hosting high-grade lithium.

This is really a new dimension that we have down in that area, that we wouldn’t have had say, two or three years ago when we were last down drilling. You’ve got uranium, and now we have lithium. It’s a very interesting up-and-coming area as well. Maurice Jackson: Switching gears, Fission 3.0 has the right projects in the right place at the right time. But that’s only part of the story. Equally important are the people that are responsible for increasing shareholder value. Mr. McElroy, please introduce us to your board of directors. Ross McElroy: Thank you, and I appreciate that. We do have a very successful team. Our founder of Fission 3.0 is also the same CEO and founder of Fission Uranium, and previously Fission Energy before that, and Strathmore.

Dev Randhawa has been involved in this company right from the get-go in its first iteration back in 1996, and also heading up Fission 3.0. Dev is the longest running CEO in the uranium sector.

Myself, I’ve been involved with Dev 12, 13 years now. We’ve had a great successful relationship. We’re able to raise money, raise attention, put that money to work, make discoveries, and basically build shareholder value right from the bottom up.

This is the group that I think, we’ve been able to deliver in the past, and we’re going to be able to deliver shareholder value as we move forward in this much improving uranium sector.

A lot of the same players that we’ve had all the way along, still keep also in the Fission 3 group. Maurice Jackson: Who is on your management team? Ross McElroy: The management team is composed of our CEO Dev Randhawa and chairman. I am the chief operating officer, and also the chief geologist. We have maintained the same structure that we have in Fission Uranium, is the same that we have in Fission 3.0. It’s a fairly lean team. Phil Morehouse is president of Fission 3.0. We kept a pretty lean mean machine in Fission 3.

Don’t forget, we’ve had up until just recently in the last six months, it’s been a very quiet company, there hasn’t been a lot of exploration activities in the uranium sector. I think as we start to ramp up, with our level of activity increasing, we’ll start to draw more and more people into roles and developing roles within the company as we begin to be active, get out and start marketing the story more, get on the ground and back that up with real results, we’re going to continue to build our team. Maurice Jackson: Before we move on to your impressive technical team, in the natural resource basis, why is it wise to follow proven winners? Ross, you alluded to it earlier, you and CEO Dev Randhawa have a proven pedigree of success. How were shareholders rewarded as far as returns for their loyalty to sticking with your team? Ross McElroy: Well, if you owned the original company at the beginning, which would’ve been Strathmore Minerals, and you’d held on it to all the way throughout, over the last 20 years since about 1996, 97, you’d probably own about five different companies right now.

What’s happened is we’ve moved on to a new phase, we’ve made discoveries, advanced projects, sold different projects to different groups. What we’ve been able to do is form new companies, split off new companies in what they call a butterfly transaction.

You have shares in the new company, still maintain your shares in the old company, so you would’ve received essentially what would look like dividends in the way of different shares for five different companies since that time. The shareholders that have been loyal and sticking with us would’ve succeeded quite handsomely all the way along. Maurice Jackson: Your technical team is exceptional. I had an opportunity to meet them in the summer of 2016 at the site visit there. Please, introduce us to them. Ross McElroy: We’re very, very proud of this group. This has been the team we’ve had, the same core group of people with us since 2010. With that same group, we were able to make our discovery on the Waterbury Lake project, and then followed up in 2012 with the discovery of PLS. It’s the same group that is very core and important to us in Fission 3.0.

I do head up the team and the technical group, so I would be the team leader or chief geologist for the technical team. My right hand guy is Raymond Ashley, he’s the VP of exploration. Ray is an excellent geoscientist who I’ve had the pleasure to work with for over 30 years in this sector, so we’ve been working pretty close together. Definitely a proven mine finder.

We’ve basically held the same group of people together on the project managers, all the structural scientists, geochemists. We’ve kept the same core group together over the last almost 10 years or so.

To me, that’s really the key. You want a team that works together well, good chemistry with each other, the ability and the environment to think outside of the box. Really, the goal for each and every one of us is to responsibly make world-class discoveries. That’s what we’re all about.

We’ve got an excellent team. All the key people are listed on the website. You’ll be able to go there and see the roles of the various groups there in the technical team, but there’s about seven or eight of us that have been able to be what I consider the core team for the last decade or so. Maurice Jackson: Let’s get into some numbers. Please share your capital structure. Ross McElroy: In Fission 3.0, we have 142 million shares outstanding. We were able to raise a significant amount. We have just under $7 million in the treasury right now, that’ll allow us to be active over the next two years or so. Maurice Jackson: What is your burn rate? Ross McElroy: The burn rate, because it’s exploration, it’s pretty discretionary spending. We have $7 million that we have in the treasury right now, that’ll certainly carry us over the next two to three years of pretty aggressive exploration spending on our key projects. We can dial that kind of number up, and we can dial it back as conditions warrant. That’s the benefit of being in exploration.

The burn rate is actually pretty minimal. In other words, we run a pretty lean shop as far as the number of management and corporate costs. Really, the majority of the costs are exploration spending, which is really entirely discretionary. Maurice Jackson: How much debt do you have? Ross McElroy: We have no debt. We’ve not taken on any debt. Basically, the money that we raise have been through equity share offerings. No debt in Fission 3.0. Maurice Jackson: Who are your major shareholders? What is their level of commitment? Ross McElroy: When we spun off Fission 3.0 back in December of 2014, it was the same shareholders that were shareholders of Fission Uranium, were the same shareholders in Fission 3.0. We would’ve had a lot of the same loyal, large shareholders, including JP Morgan, even investment from others that we’ve had along the way. It’s been the same loyal group.

We have significant new shareholders now with the financing that we did back in 2018, which was led by the Sprott Global Resources Group out of California. I think we have some new players back to the game, but we have a lot of shareholders that have been with us over the long haul.

These are people that have a good vision of the uranium sector. They know that the good times are around the corner. It’s a point that we believe really strongly, and we think that the sector is improving a great deal.