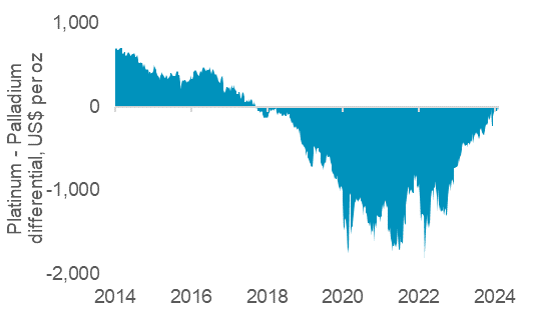

The fall in the palladium price has closed the differential with platinum, with the sister metals now priced near parity for the first time since 2018. As this fall has been long-expected, due to forecasts of palladium moving into surplus from 2025, investors are net short palladium, leaving it vulnerable to short covering rallies. In contrast, platinum’s fundamentals are much more attractive, with the current market deficit expected to continue until at least 2028, which should be reflected in the price after automaker inventory management has run its course.

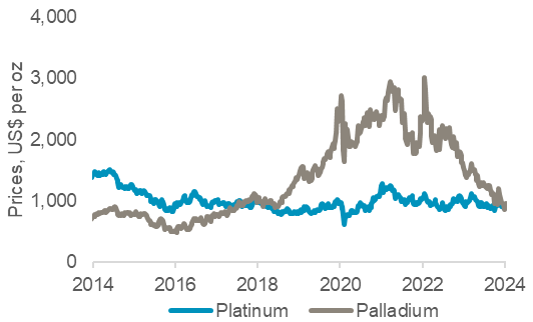

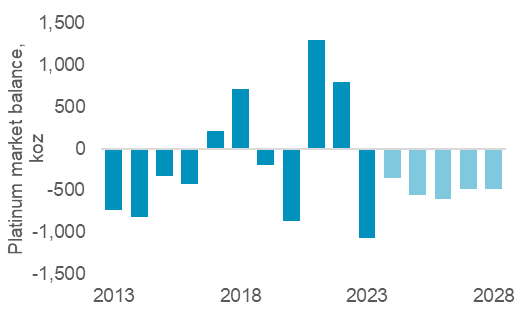

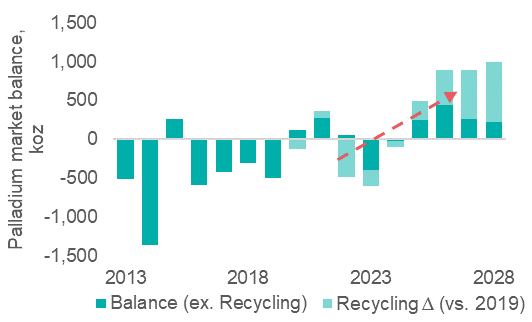

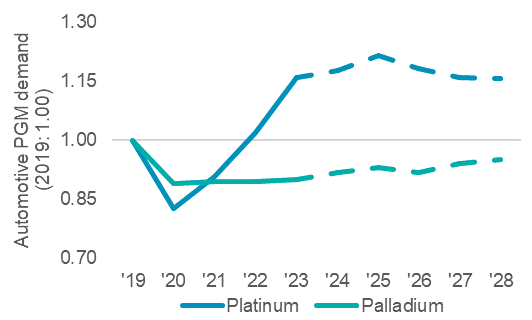

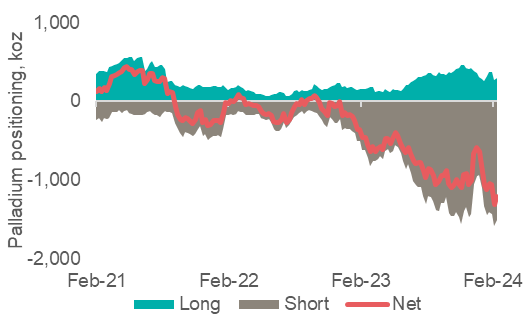

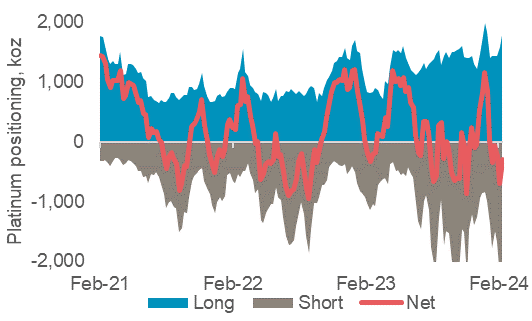

Palladium’s price rose above platinum’s in 2018, after multi-year palladium market deficits, and remained at a premium to platinum of over $1,000/oz for nearly three years. This incentivised significant automotive 1:1 substitution of platinum for palladium (2023, >600 koz). Palladium prices peaked in March 2022 at US$3,012/oz (Fig. 1), a record US$1,883/oz premium to platinum (Fig. 3), following Russia’s invasion of Ukraine, providing a further boost to substitution. Since then, the outlook for platinum and palladium have diverged. Palladium is weighed upon by automotive substitution (Fig. 5), overreliance on ICE autocatalyst demand, and expected growth in recycling supply. Conversely, substitution benefits platinum as do more diverse end-markets (Pt auto demand ~40%, vs. ~80% for Pd). WPIC expects platinum deficits from 2023 to at least 2028 (Fig. 2), but palladium is forecast to transition to a surplus from 2025 (Fig. 4). Net managed money positions highlight a build of investor short positions on palladium (Fig 6) while platinum’s average positioning has been less consistently directional (Fig. 7).

In the near-term palladium prices are likely to be volatile as investors continue to cover short positions, with two short squeezes since December 2023 alone. In addition, there are some supply risks to palladium’s move into surplus; palladium recycling supply is expected to grow by ~1 Moz p.a., but with the recycling industry facing a number of challenges, should this supply not materialise in full it could make palladium markets much more balanced or even keep them in deficit. However, it is more pertinent to understand why platinum, with its better outlook, did not see prices converge upwards towards palladium. From a sentiment perspective, platinum, as a non-yielding asset, was hampered by tightening monetary policy undertaken by central banks to contain inflation through 2022 and 2023. While physical platinum purchases were impacted by reduced automaker purchases after a period of large inventory accumulation as a result of under-producing vehicles during COVID and the semiconductor shortage. There are early signs that automakers are returning to normalised purchasing patterns. This comes as platinum is forecast to enter the second year of a protracted period of market deficits, arguably boding well for upward pressure on prices and investor returns.

Platinum’s attraction as an investment asset arises from:

- WPIC research indicates the platinum market entering a period of consecutive deficits from 2023

- Platinum supply remains challenged, both from primary mining and secondary recycling

- Automotive platinum demand growth should continue into 2024f due principally to substitution of platinum for palladium in gasoline vehicles

- Platinum is a critical mineral in the global energy transition underpinning a key role in the hydrogen economy

- The platinum price remains historically undervalued and significantly below both gold and palladium

IMPORTANT NOTICE AND DISCLAIMER: This publication is general and solely for educational purposes. The publisher, The World Platinum Investment Council, has been formed by the world’s leading platinum producers to develop the market for platinum investment demand. Its mission is to stimulate investor demand for physical platinum through both actionable insights and targeted development: providing investors with the information to support informed decisions regarding platinum; working with financial institutions and market participants to develop products and channels that investors need.

This publication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. With this publication, the publisher does not intend to transmit any order for, arrange for, advise on, act as agent in relation to, or otherwise facilitate any transaction involving securities or commodities regardless of whether such are otherwise referenced in it. This publication is not intended to provide tax, legal, or investment advice and nothing in it should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. The publisher is not, and does not purport to be, a broker-dealer, a registered investment advisor, or otherwise registered under the laws of the United States or the United Kingdom, including under the Financial Services and Markets Act 2000 or Senior Managers and Certifications Regime or by the Financial Conduct Authority.

This publication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your investment objectives, financial circumstances and risk tolerance. You should consult your business, legal, tax or accounting advisors regarding your specific business, legal or tax situation or circumstances.

The information on which this publication is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information. This publication contains forward-looking statements, including statements regarding expected continual growth of the industry. The publisher notes that statements contained in the publication that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect actual results. The logos, services marks and trademarks of the World Platinum Investment Council are owned exclusively by it. All other trademarks used in this publication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks

WPIC Research MiFID II Status

The World Platinum Investment Council -WPIC- has undertaken an internal and external review of its content and services for MiFID II. As a result, WPIC highlights the following to the recipients of its research services, and their Compliance/Legal departments:

WPIC research content falls clearly within the Minor Non-Monetary Benefit Category and can continue to be consumed by all asset managers free of charge. WPIC research can be freely shared across investment organisations.

- WPIC does not conduct any financial instrument execution business. WPIC does not have any market making, sales trading, trading or share dealing activity. (No possible inducement).

- WPIC content is disseminated widely and made available to all interested parties through a range of different channels, therefore qualifying as a “Minor Non-Monetary Benefit” under MiFID II (ESMA/FCA/AMF). WPIC research is made freely available through the WPIC website. WPIC does not have any permissioning requirements on research aggregation platforms.

- WPIC does not, and will not seek, any payment from consumers of our research services. WPIC makes it clear to institutional investors that it does not seek payment from them for our freely available content.

More detailed information is available on the WPIC website:

https://www.platinuminvestment.com/investment-research/mifid-ii