Digital Transformation Initiative Establishes Operational Foundation for Innovation in Diagnostics, Prevention and Precision Medicine

DALLAS, TX / ACCESS Newswire / July 1, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announced that its portfolio company, MediGuide International, has launched a new enterprise digital platform.

MediGuide’s digital platform is an API-first, interoperable layer that connects insurers, payors, and digital health partners to MediGuide’s clinical services, Medical Second Opinion, virtual urgent/primary/behavioral/specialty care, and chronic condition programs, through a single, configurable integration. Built to be channel-agnostic, it can be embedded into existing member portals, apps or insurer platforms via API, and is designed and configured to meet GDPR, HIPAA, and local data-protection requirements across every market MediGuide operates in.

“MediGuide represents exactly the type of business we believe can benefit from the practical application of Transformational AI,” said Todd A. Furniss, Chief Executive Officer of AIAI Holdings. “When we launched Ai2, we committed to creating value by partnering with experienced management teams and applying technology that improves operational efficiency and positions businesses for long-term growth. Today’s announcement represents a step towards the implementation of that strategy. By modernizing core operations, the digital transformation initiative lays the foundation for innovation in diagnostics, preventive care, and precision medicine.”

Founded in 1999, MediGuide is a global medical intelligence company providing Medical Second Opinions (MSO), Medical Treatment Abroad coordination and digital healthcare solutions through an international network serving clients across more than 160 countries. The company works with leading insurers, employers and healthcare organizations to help patients access expert medical guidance and improve healthcare outcomes through world-class specialist expertise.

“For more than 25 years, MediGuide has helped people make informed healthcare decisions by serving as a trusted clinical gatekeeper for high-complexity healthcare spending,” said Vera Guerreiro, Chief Executive Officer of MediGuide International. “As MediGuide expands its global footprint, investing in a modern digital operating platform has become essential to supporting scalable growth and delivering the high-quality service our clients rely on. As part of Ai2, we now have access to exceptional technology capabilities and expertise that will help accelerate our product roadmap, drive innovation, and position us for the next stage of growth.”

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai2) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai2 is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries.

About MediGuide

MediGuide is a global medical intelligence company dedicated to helping individuals make informed healthcare decisions when they matter most. Founded in 1999, the Company provides Medical Second Opinions, Medical Treatment Abroad, Digital Health, and Preventive Health solutions through an integrated healthcare platform that connects members with world-renowned medical centers and leading specialists around the globe.

Operating across more than 160 countries with a network spanning five continents, MediGuide partners with insurers, employers, financial institutions, and healthcare organizations to deliver expert clinical guidance, personalized care navigation, and innovative digital health services. By combining world-class medical expertise with advanced technology and AI-enabled healthcare solutions, MediGuide empowers patients with greater confidence, improved clinical outcomes, and access to the highest standards of care worldwide. Learn more at MediGuide.

MediGuide is a portfolio company of AIAI Holdings Corporation (NASDAQ:AIAI).

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

The forward-looking statements in this press release are based on information available to us as of the date hereof, and we disclaim any intention to, and, except as may be required by law, undertake no obligation to, update or revise forward-looking statements to reflect events or circumstances that subsequently occur or of which the Company hereafter become aware. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

South Jordan, Utah and Vancouver, British Columbia–(Newsfile Corp. – June 24, 2026) – Sage Potash Corp. (TSXV: SAGE) (OTCQB: SGPTF) (“Sage Potash” or the “Company”) is pleased to announce that site preparation and mobilization activities for its 2026 drilling program are underway at the Company’s flagship Sage Plain Potash Project (the “Project”), located in the Paradox Basin of southeastern Utah, USA.

Site preparation is underway, including access road construction, topsoil removal, site levelling, perimeter berm construction, storm water management preparations, and construction of an aggregate platform to create a stable rig base, all in preparation for rig setup activities. Drilling operations are expected to commence approximately two weeks from current site preparations.

Figure 1 – Representative drilling rig and equipment similar to that planned for use during the Company’s 2026 drilling program.

“Receiving final approvals and commencing construction of the drill site is an important event for our team, in anticipation of the start of the Drill program and the advancement of the Sage Plain Potash Project toward its next stage of development,” stated J. Patricio Varas, Chief Executive Officer of Sage Potash Corp. “With potash recently designated as a critical mineral in the United States and approximately 95% of domestic demand supplied through imports, we believe Sage Plain is uniquely positioned to contribute to long-term U.S. fertilizer security. We anticipate the successful completion of this drill program to be a valuable milestone for our shareholders”.

The Company will be drilling a 1.275 km (3/4 mile) step out hole to the NNE from the maiden hole from which the Company’s current resource is calculated.

Historical drillhole data has identified significant potash mineralization within the Cycle 18 Upper and Lower beds at depths of approximately 2,100 metres (6,890 feet): a thickness of 7.26 m (24 ft) at 46% KCl in the Upper bed and a thickness of 5.46 m (18 ft) at 35.8% KCl in the Lower bed. The grades at Sage Plain are amongst the highest tenor or potash grades seen in the USA and indeed the world. The objective of the current drill program is to intersect the two beds of Cycle 18 in the 1.275 m step-out hole and test for substantially the same grades and thicknesses. Achieving this should allow the Company to expand the inferred resource and upgrade a portion of the overall mineralization to the measured and indicated categories. The Company anticipates releasing an updated resource estimate for Sage Plain in late Q3, 2026.

In addition to confirming potash mineralization, the drilling program will include a comprehensive hydrogeological assessment. The Company plans to conduct targeted Drill Stem Tests (“DSTs”) in formations exhibiting sufficient water flow in order to evaluate yield rates and water quality (primarily targeting saline non-potable aquifers) for future solution mining operations. Fluid sampling and detailed water analysis will also be undertaken to support future processing design and cavern development.

Qualified Person

The scientific and technical information contained in this news release has been reviewed and approved by Greg Vogelsang, P.Geo, P.Eng, the Qualified Person as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects. Mr, Vogelsang is Vice President Project Development for the Company.

About Sage Potash Corp.

Sage Potash Corp. (TSXV: SAGE) (OTCQB: SGPTF) is dedicated to the development of its flagship Sage Plain Potash Project, located in the Paradox Basin, Utah. With a large and high-grade resource base, the Company is advancing toward its goal of establishing a secure and sustainable domestic potash production platform in the United States. Sage Potash is committed to food security, environmental stewardship, and creating value for shareholders and stakeholders alike.

Marcus van der Made, Investor Relations IR@sagepotash.com 1 (236) 521-1521

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities legislation. The forward-looking statements herein are made as of the date of this news release only, and the Company does not assume any obligation to update or revise them to reflect new information, estimates or opinions, future events or results or otherwise, except as required by applicable law. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects”, “is expected”, “budgets”, “scheduled”, “estimates”, “forecasts”, “predicts”, “projects”, “intends”, “targets”, “aims”, “anticipates” or “believes” or variations (including negative variations) of such words and phrases or may be identified by statements to the effect that certain actions “may”, “could”, “should”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking information in this news release includes, but is not limited to, statements with respect to future events or future performance of Sage Potash, including: the objective of the current drill program is to intersect the two beds of Cycle 18 in the 1.275 m step-out hole and test for substantially the same grades and thicknesses; achieving this should allow the Company to expand the inferred resource and upgrade a portion of the overall mineralization to the measured and indicated categories; the Company anticipates releasing an updated resource estimate for Sage Plain in late Q3 2026; fluid sampling and detailed water analysis will also be undertaken to support future processing design and cavern development; we anticipate this drill programs’ successful completion to be a valuable milestone for our shareholders. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including, but not limited to, the risk factors set out under the heading “Risk Factors and Uncertainties” in the Company’s Management’s Discussion & Analysis available for review under the Company’s profile at www.sedarplus.ca. Such forward-looking information represents management’s best judgement based on information currently available. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Toronto, Ontario–(Newsfile Corp. – June 23, 2026) – Coyote Copper Mines Inc. (TSXV: CCMM) (“CCMM” or the “Corporation”) announces that further to its news releases dated May 13, 2026, May 25, 2026, June 2, 2026 and June 15, 2026 it has closed the final tranche (the “Final Tranche“) of its previously announced non-brokered private placement financing of up to 34,353,483 Units issued at a price of CAD$0.25 per Unit with each Unit consisting of one (1) fully-paid Common Share (a “CommonShare“) and one half (½) Common Share purchase warrant (a “HalfWarrant“) in the capital of the Corporation, for aggregate gross proceeds of $8,588,370.75 to be used for exploration and general corporate purposes (the “Offering“).

Two Half Warrants will entitle the holder thereof to purchase one common share of the Corporation. Each Warrant will expire thirty six (36) months from the date of issue and will entitle the holder thereof to purchase one Common Share at a price of CAD$0.50 per Warrant Share within 36 months from the date of issue.

An aggregate of 20,956,830 Units was sold under the First Tranche for total gross proceeds of C$5,239,207.50

An aggregate of 13,396,313 Units was sold under the Final Tranche for total gross proceeds of C$3,349,163.25

In connection with closing of the financing, the Company paid aggregate finder’s fees consisting of (i) C$528,085.00 (the “Cash Consideration”) and (ii) 1,836,260 compensation warrants (the “Compensation Warrants”) to eligible finders. Each Compensation warrant entitles the holder to acquire one Common Share at a price of C$0.50 per Common Share for a period of 36 months from the date of issuance of the Compensation Warrant.

The closing of the Financing is subject to the receipt of all necessary regulatory approvals, including the final approval of the TSX Venture Exchange. All securities issued and issuable pursuant to the First Tranche of the Offering are subject to a four-month plus one day hold period commencing on the date of issuance.

Neither the Exchange nor its Regulation Services Provider (as that term is defined in the policies of the Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in the United States. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“) or any state securities laws and may not be offered or sold within the United States or to U.S. persons unless registered under the U.S. Securities Act and applicable state securities laws or an exemption from such registration is available.

information is based on currently available competitive, financial and economic data and operating plans, strategies or beliefs as of the date of this news release, but involve known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, performance or achievements of the Corporation to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors may be based on information currently available to the Corporation including information obtained from third-party industry analysts and other third-party sources, and are based on management’s current expectations or beliefs. Any and all forward-looking information contained in this news release is expressly qualified by this cautionary statement.

as of the date of this news release and, other than as required by law, the Corporation disclaims any obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information.

Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking information prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected. Although the Corporation has attempted to identify important risks, uncertainties and factors which could cause actual results to differ materially, there may be others that cause results not to be as anticipated, estimated or intended. The Corporation does not intend, and does not assume any obligation, to update this forward-looking information except as otherwise required by applicable law.

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

Yahoo Finance

M

ADVERTISEMENT

This is a paid press release. Contact the press release distributor directly with any inquiries.

AIAI Holdings Unveils AI Integration Playbook for Portfolio Companies

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

“Transformational AI is intelligence grounded in a business’s actual operations, acting as a core driver of value rather than an add-on,” said Todd Furniss, Chief Executive Officer and Co-founder of AIAI Holdings Corporation. “At Ai2 we don’t sell this technology, we buy companies then bake it into their DNA, converting complex services into durable cash flows. This requires meeting each portfolio company where it is today, understanding its workflows and data environment, and then building the appropriate foundation for AI-enabled value creation. Disorganized or incomplete data is not a weakness; it is the norm. Identifying, organizing, and analyzing that information is a critical part of the transformation process. Once that foundation is in place, we can implement targeted AI and operational strategies designed to drive both revenue growth and EBITDA expansion wherever the greatest opportunities exist.”

The framework provides Ai² with a disciplined, repeatable process for assessing newly acquired and existing portfolio companies, identifying practical AI-enabled value creation opportunities, evaluating operational and data readiness, and developing phased implementation plans that can be executed responsibly over time.

The Company is also pleased to announce that C.C. Carlton Industries (“CCCI”), a wholly owned subsidiary of Ai² and a Central Texas construction company with more than 30 years of operating history, is among the first Ai2 portfolio companies to move through the Company’s structured Transformational AI assessment and onboarding process.

“C.C. Carlton Industries is excited to be an initial benefactor of Ai²’s Transformational AI integration framework,” said Ben Lyon, CEO of C.C. Carlton Industries. “As an operating business with established workflows, project complexity, customer requirements, safety considerations, and opportunities for process improvement, we believe TAI assessment process can help identify practical opportunities to improve efficiency, quality, safety, speed to completion, and decision-making over time.”

The Company expects that early implementation work will help establish repeatable processes and reusable AI tools that can support future acquisitions and additional portfolio company integrations. Over time, Ai² intends to build a portfolio-wide Transformational AI playbook that can support faster assessment, improved execution and scalability across diverse industries.

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

“Transformational AI is intelligence grounded in a business’s actual operations, acting as a core driver of value rather than an add-on,” said Todd Furniss, Chief Executive Officer and Co-founder of AIAI Holdings Corporation. “At Ai2 we don’t sell this technology, we buy companies then bake it into their DNA, converting complex services into durable cash flows. This requires meeting each portfolio company where it is today, understanding its workflows and data environment, and then building the appropriate foundation for AI-enabled value creation. Disorganized or incomplete data is not a weakness; it is the norm. Identifying, organizing, and analyzing that information is a critical part of the transformation process. Once that foundation is in place, we can implement targeted AI and operational strategies designed to drive both revenue growth and EBITDA expansion wherever the greatest opportunities exist.”

The framework provides Ai² with a disciplined, repeatable process for assessing newly acquired and existing portfolio companies, identifying practical AI-enabled value creation opportunities, evaluating operational and data readiness, and developing phased implementation plans that can be executed responsibly over time.

The Company is also pleased to announce that C.C. Carlton Industries (“CCCI”), a wholly owned subsidiary of Ai² and a Central Texas construction company with more than 30 years of operating history, is among the first Ai2 portfolio companies to move through the Company’s structured Transformational AI assessment and onboarding process.

“C.C. Carlton Industries is excited to be an initial benefactor of Ai²’s Transformational AI integration framework,” said Ben Lyon, CEO of C.C. Carlton Industries. “As an operating business with established workflows, project complexity, customer requirements, safety considerations, and opportunities for process improvement, we believe TAI assessment process can help identify practical opportunities to improve efficiency, quality, safety, speed to completion, and decision-making over time.”

The Company expects that early implementation work will help establish repeatable processes and reusable AI tools that can support future acquisitions and additional portfolio company integrations. Over time, Ai² intends to build a portfolio-wide Transformational AI playbook that can support faster assessment, improved execution and scalability across diverse industries.

The Company emphasized that the framework is not intended to represent a complete enterprise-wide transformation of each acquired business. Rather, the objective is to ensure that meaningful Transformational AI integration begins early in the ownership cycle, with selected use cases identified, prioritized, tested, and moved into active implementation during the initial post-acquisition period.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai2) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai2 is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries.

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

Yahoo Finance

M

ADVERTISEMENT

This is a paid press release. Contact the press release distributor directly with any inquiries.

AIAI Holdings Unveils AI Integration Playbook for Portfolio Companies

Strategic framework meets businesses where they are today, identifying Transformational AI enabled value creation opportunities

DALLAS, TX / ACCESS Newswire / June 23, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai2” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI (TAI) to enhance portfolio performance, today announces its strategic and comprehensive post-acquisition AI integration framework, pursuant to which it will identify, design, and implement AI-enabled value creation opportunities across the Company’s portfolio businesses. This disciplined, repeatable playbook is expected to move portfolio companies from initial operational assessment to active Transformational AI implementation, fundamentally redefining their financial potential.

“Transformational AI is intelligence grounded in a business’s actual operations, acting as a core driver of value rather than an add-on,” said Todd Furniss, Chief Executive Officer and Co-founder of AIAI Holdings Corporation. “At Ai2 we don’t sell this technology, we buy companies then bake it into their DNA, converting complex services into durable cash flows. This requires meeting each portfolio company where it is today, understanding its workflows and data environment, and then building the appropriate foundation for AI-enabled value creation. Disorganized or incomplete data is not a weakness; it is the norm. Identifying, organizing, and analyzing that information is a critical part of the transformation process. Once that foundation is in place, we can implement targeted AI and operational strategies designed to drive both revenue growth and EBITDA expansion wherever the greatest opportunities exist.”

The framework provides Ai² with a disciplined, repeatable process for assessing newly acquired and existing portfolio companies, identifying practical AI-enabled value creation opportunities, evaluating operational and data readiness, and developing phased implementation plans that can be executed responsibly over time.

The Company is also pleased to announce that C.C. Carlton Industries (“CCCI”), a wholly owned subsidiary of Ai² and a Central Texas construction company with more than 30 years of operating history, is among the first Ai2 portfolio companies to move through the Company’s structured Transformational AI assessment and onboarding process.

“C.C. Carlton Industries is excited to be an initial benefactor of Ai²’s Transformational AI integration framework,” said Ben Lyon, CEO of C.C. Carlton Industries. “As an operating business with established workflows, project complexity, customer requirements, safety considerations, and opportunities for process improvement, we believe TAI assessment process can help identify practical opportunities to improve efficiency, quality, safety, speed to completion, and decision-making over time.”

The Company expects that early implementation work will help establish repeatable processes and reusable AI tools that can support future acquisitions and additional portfolio company integrations. Over time, Ai² intends to build a portfolio-wide Transformational AI playbook that can support faster assessment, improved execution and scalability across diverse industries.

The Company emphasized that the framework is not intended to represent a complete enterprise-wide transformation of each acquired business. Rather, the objective is to ensure that meaningful Transformational AI integration begins early in the ownership cycle, with selected use cases identified, prioritized, tested, and moved into active implementation during the initial post-acquisition period.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai2) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai2 is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries.

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

The forward-looking statements in this press release are based on information available to us as of the date hereof, and we disclaim any intention to, and, except as may be required by law, undertake no obligation to, update or revise forward-looking statements to reflect events or circumstances that subsequently occur or of which the Company hereafter become aware. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

West Point Gold CEO Derek Macpherson breaks down the latest high-grade drill results and what they mean for the company future. See why this 66.2 meter intercept at 6.57 GPT Au is a critical indicator for the project’s potential. Netting a 435 Gram/Meter is exceptional!

This update is designed for investors tracking West Point Gold who want a clear view of the company capital structure, ownership, and current analyst coverage. We review the specific technical data from the recent drilling program to provide a grounded perspective on the robust vein system currently being tested.

By evaluating these high-grade drill results, viewers will better understand how the company is positioning its assets within the broader gold mining stocks market. We focus strictly on the data provided by the CEO to help you assess the operational progress and the strategic outlook for the site.

Subscribe for weekly mining investment analysis updates, and comment below on which exploration project you want us to cover next.

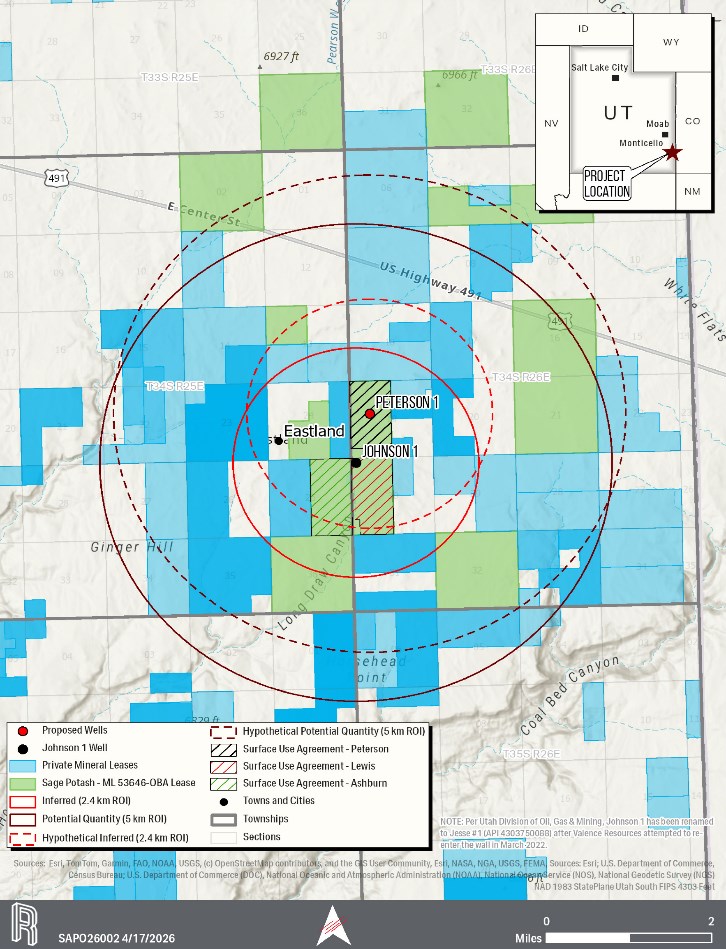

South Jordan, Utah and Vancouver, British Columbia–(Newsfile Corp. – June 18, 2026) – Sage Potash Corp. (TSXV: SAGE) (OTCQB: SGPTF) (“Sage Potash” or the “Company”) is pleased to announce the Company has now received all required approvals and permits from both the local County and the State of Utah to proceed with drilling operations at its Sage Plain project in San Juan County in Utah. Final approvals were granted following a customary site inspection conducted on May 28, 2026, by representatives of the Utah Division of Oil, Gas and Mining (“DOGM”), accompanied by personnel from Sage Potash and its contractors, along with posting of drilling related bonds.

As previously announced, the Company has engaged Westrock Energy Services (USA) Inc. to oversee and coordinate all aspects of the drilling program, alongside Drake Well Service Inc. as drilling contractor. The Company will be drilling a 1.275 km (3/4 mile) step out hole to the NNE from the maiden hole from which the Company’s current resource is calculated.

Figure 1 – Peterson 1 drill hole location relative to Johnson 1 and hypothetical resource expansion radius at the Sage Plain Potash Project, Utah

Historical drillhole data has identified significant potash mineralization within the Cycle 18 Upper and Lower beds at depths of approximately 2,100 metres (6,890 feet), demonstrating strong economic potential across the Project area. As outlined in the Company’s April 7, 2026 news release, the current drilling program is specifically designed to target these potash-bearing horizons and expand and upgrade the resource confidence levels for what management believes to be one of the most prospective and high-grade solution mining potash targets in the United States.

In addition to confirming potash mineralization, the drilling program will include a comprehensive hydrogeological assessment. The Company plans to conduct targeted Drill Stem Tests (“DSTs”) in formations exhibiting sufficient water flow in order to evaluate yield rates and water quality (primarily targeting saline non-potable aquifers) for future solution mining operations. Fluid sampling and detailed water analysis will also be undertaken to support future processing design and cavern development.

Following completion of coring operations, the open borehole will undergo an extensive suite of geophysical wireline logs. Recovered potash horizon core samples will then be transported to an independent analytical laboratory for detailed geological logging, geochemical sampling, and assaying under strict QA/QC protocols to confirm the grade, continuity, and thickness of the sylvinite mineralization.

“Receiving final approvals marks a major milestone in the advancement of the Sage Plain Potash Project,” stated J. Patricio Varas, Chief Executive Officer of Sage Potash Corp. “Our technical team has designed a focused multi-purpose drill program aimed at generating the critical geological and hydrogeological data required to potentially upgrade the resource and advance the Project toward feasibility studies and detailed engineering. We are confident this program will further demonstrate the quality and scale of the Project while being executed safely and efficiently.“

The Company expects to release an updated resource estimate in Q3 2026, incorporating results from the current drilling campaign and historical drilling data. The updated estimate is expected to support the next stage of project advancement, including feasibility studies, detailed engineering, and broader development planning.

The Company and its contractors intend to mobilize for this drill program in short order.

About Sage Potash Corp.

Sage Potash Corp. (TSXV: SAGE) (OTCQB: SGPTF) is dedicated to the development of its flagship Sage Plain Potash Project, located in the Paradox Basin, Utah. With a large and high-grade resource base, the Company is advancing toward its goal of establishing a secure and sustainable domestic potash production platform in the United States. Sage Potash is committed to food security, environmental stewardship, and creating value for shareholders and stakeholders alike.

On Behalf of the Board of Directors, J. Patricio Varas, CEO and Director 1 (236) 521-1521 Website: www.sagepotash.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities legislation. The forward-looking statements herein are made as of the date of this news release only, and the Company does not assume any obligation to update or revise them to reflect new information, estimates or opinions, future events or results or otherwise, except as required by applicable law. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects”, “is expected”, “budgets”, “scheduled”, “estimates”, “forecasts”, “predicts”, “projects”, “intends”, “targets”, “aims”, “anticipates” or “believes” or variations (including negative variations) of such words and phrases or may be identified by statements to the effect that certain actions “may”, “could”, “should”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking information in this news release includes, but is not limited to, statements with respect to future events or future performance of Sage Potash, including the satisfactory design and supervision of the Company’s upcoming drill program, the achievement of positive results of the drill program, the achievement of targeting Cycle 18 horizons and continuous core recovery, the achievement of satisfactory potash evaluation and hydrogeological testing in the drill program, the timing of the mobilization and the commencement of the drill program and potentially upgrading the resource and advancing the Project toward feasibility studies, detailed engineering and broader development planning. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including, but not limited to, the risk factors set out under the heading “Risk Factors and Uncertainties” in the Company’s Management’s Discussion & Analysis available for review under the Company’s profile at www.sedarplus.ca. Such forward-looking information represents management’s best judgement based on information currently available. No forward-looking statement can be guaranteed and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Edmonton, Alberta–(Newsfile Corp. – June 19, 2026) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) announces that, between June 16 and June 19, 2026, it closed on a private placement originally announced on May 13, 2026 (the “Offering”) by the issuance of 4,525,292 Units, 562,500 FT Units, and 110,000 CMFT Units for gross proceeds of $349,044.

Each Unit, priced at $0.065 per Unit, consisted of one common share of the Company (“Common Share”) and one Common Share purchase warrant entitling the warrant holder to purchase an additional Common Share for $0.12 and expiring on the earlier of a) 30 days following written notice by the Company to the warrant holder that the volume-weighted average trading price of the Common Shares on the TSX Venture Exchange is at or greater than CA$0.18 per Common Share for 10 consecutive trading days; and (b) 36 months (3 years) from the date of issuance (“Warrant”). Each FT Unit, priced at $0.08 per FT Unit, consisted of one Common Share and one half of one Warrant, each issued as a “flow through share” for the purposes of the Income Tax Act (Canada). Each CMFT Unit, priced at $0.09 per CMFT Unit, consisted of one Common Share and one half of one Warrant, each issued as a “flow through share” for the purposes of the Income Tax Act (Canada).

The Offering was offered to qualified subscribers in the Provinces of Alberta, British Columbia and Ontario and in other jurisdictions as the Company in its discretion determined, in reliance upon exemptions from the registration and prospectus requirements of applicable securities legislation. The Offering is now closed.

The Company intends to use the proceeds of the sale of the Units for mineral property acquisition, exploration, and general working capital; the proceeds from the sale of FT Units for mineral property exploration, and the proceeds from the sale of the CMFT Units for mineral property exploration specifically targeting Critical Minerals (as defined in the Income Tax Act (Canada))

In connection with the sale of 600,000 Units, the Company paid a cash finders fee of $2,340 and issued 36,000 Finder Warrants (with each Finder Warrant having the same terms as the Warrants included in the Units) to Canaccord Genuity Corp. In connection with the sale of 437,500 FT Units and 110,000 CMFT units, the Company paid a cash finders fee of $2,694 and issued 32,850 Finder Warrants to Raymond James Limited. In connection with the sale of 384,000 Units, the Company paid a cash finders fee of $1,498 and issued 23,040 Finder Warrants to Leede Financial Inc. In connection with the sale of 315,000 Units, the Company paid a cash finders fee of $1,229 and issued 18,900 Finder Warrants to Haywood Securities Inc.

Following closing of the Offering, the Company has 232,838,034 common shares issued and outstanding. The Common Shares and any Common Shares issued on exercise of the Warrants and Finder Warrants are subject to restrictions on trading for four months from the date of issuance, expiring on dates ranging from October 17, 2026 to October 20, 2026. The Offering is subject to final acceptance of the TSX Venture Exchange.

ABOUT GRIZZLY DISCOVERIES INC.

Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and base metals properties in southeastern British Columbia. Grizzly is run by a highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.

On behalf of the Board,

GRIZZLY DISCOVERIES INC. Brian Testo, CEO, President

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Caution concerning forward-looking information

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward-looking information. Such forward-looking information and statements are frequently identified by words such as “may,” “will,” “should,” “anticipate,” “plan,” “expect,” “believe,” “estimate,” “intend” and similar terminology, and reflect assumptions, estimates, opinions and analysis made by management of Grizzly in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Grizzly’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon.

Risks and uncertainties that may cause actual results to vary include but are not limited to the availability of financing; fluctuations in commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedarplus.ca. Grizzly disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

NOT FOR DISSEMINATION IN THE UNITED STATES OF AMERICA

DALLAS, TX / ACCESS Newswire / June 18, 2026 / AIAI Holdings Corporation (NASDAQ:AIAI) (“Ai²” or the “Company”), an AI-enabled diversified holding company utilizing Transformational AI to enhance portfolio performance, today announced that John P. Rochon, Chairman of Ai² and entities controlled by the family of Mr. Rochon, collectively, have acquired approximately $100 million of Ai² shares at $20.00 per share through a privately negotiated transaction with an existing large shareholder.

This transaction represents a significant incremental investment by the Rochon family, further increasing their already substantial ownership position in Ai². The purchase underscores a deep and continuing conviction in the Company’s long-term strategy, its differentiated position in Transformational AI, and the proven ability of its Board and management team to execute at scale. The Rochon family has been a longstanding supporter of Ai², and this latest investment further aligns their interests with the Company’s long-term value creation objectives. This transaction reinforces a stable and strategically aligned shareholder base.

“This is not simply a financial investment; it is a statement of belief in where Ai² is going and how we intend to get there,” added John P. Rochon, Sr. “We are building something enduring, with a focus on disciplined execution, durable growth and long-term value creation.”

Ai² continues to execute against a robust pipeline of AI-driven initiatives across multiple sectors, focusing on enterprise-grade psychometric intelligence, scalable deployment architectures, and high-value commercial applications. The Rochon family believes it is well-positioned to capitalize on accelerating demand for applied AI solutions that deliver measurable business outcomes.

The Company was not involved in negotiating this transaction and will not receive any proceeds. Additionally, the Company expects to file its Quarterly Report on Form 10-Q for the quarter ended March 31, 2026 with the Securities and Exchange Commission next week. The Company notes that the period covered by the 10-Q predates both its direct listing and the acquisition of its Portfolio Companies and therefore will not reflect the consolidated financial results of those subsidiaries. The financial results to be presented in the forthcoming Form 10-Q will reflect only the historical operations of the Company’s predecessor entity and will include transaction-related expenses incurred in connection with the business combination, as well as the effects of operational disruptions arising from, among other factors, closing the transaction, adverse weather conditions and military hostilities in the Middle East, each of which impacted performance during the first quarter. As a result, the Company believes the financial results that will be reported in the forthcoming Form 10-Q will not be representative of the Company’s normalized operating performance.

About AIAI Holdings Corporation

AIAI Holdings Corporation (Ai²) (NASDAQ:AIAI) is an AI-enabled diversified holding company that acquires and grows companies across multiple industries. We expect to drive revenue and earnings growth throughout our portfolio by applying exclusively licensed Transformational AI to enhance operational efficiency and financial performance.

Ai² is building a next-generation model for technology-enabled business operations, which is expected to create sustainable value for shareholders through the strategic integration of artificial intelligence across diverse industries. More information can be found at www.aiaiholdings.com.

This press release contains “forward-looking statements” or “forward-looking information” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the plans, intentions, beliefs, and current expectations of the Company with respect to future business activities and plans of the Company. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including without limitation statements regarding our expectations, intentions, beliefs, plans, objectives, goals, strategies, future events or performance, and underlying assumptions. Forward-looking statements are often identified by the use of words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “would,” “could,” “should”, “estimate,” “plan,” “predict,” “project,” “estimate”, or “continue,” or similar expressions, including the negative of these terms or other comparable terminology.

Forward-looking statements are based on the Company’s current expectations regarding its strategy, plans, intentions, performance, or future occurrences or results, the information on which such expectations were based may change. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of known and unknown risks, uncertainties, and other factors, many of which are outside of the Company’s control, that could cause actual results, performance, or achievements to materially differ from any future results, performance, or achievements expressed or implied by the forward-looking statements. Such risks, uncertainties and other factors include, but are not limited to our lack of operating history, our ability to attract new investments, our failure to manage growth effectively, our acquisition activities may pose risks that could harm our business, and our licensed AI may not perform up to the expected standards, as well as general business and economic conditions, competitive pressures, regulatory changes, technological developments, and other factors identified in the Company’s most recent filings with the U.S. Securities and Exchange Commission, including our Registration Statement on Form S-1, which are available for review at www.sec.gov. Furthermore, the Company operates in a competitive environment where new and unanticipated risks may arise. Accordingly, investors should not place any reliance on forward-looking statements as a prediction of actual results.

The forward-looking statements in this press release are based on information available to us as of the date hereof, and we disclaim any intention to, and, except as may be required by law, undertake no obligation to, update or revise forward-looking statements to reflect events or circumstances that subsequently occur or of which the Company hereafter become aware. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

Denver, Colorado–(Newsfile Corp. – June 17, 2026) – Elemental Royalty Corporation (NASDAQ: ELE) (TSX: ELE) (“Elemental” or the “Company“) is pleased to announce the Company has been included in the list of additions to the Russell 3000®, Russell 2000® and S&P/TSX Global Gold Index.

S&P/TSX Global Gold Index Elemental is expected to be added to the S&P/TSX Global Gold Index, effective prior to the open of trading on Monday, June 22, 2026, as disclosed by S&P Dow Jones Indices on June 5, 2026. The S&P/TSX Global Gold Index is designed to provide investors with exposure to global gold securities and is widely followed by market participants seeking diversified exposure to the gold sector.

Russell 3000® and Russell 2000® Indexes Elemental is also expected to join the broad-market Russell 3000® Index and the small-cap Russell 2000® Index at the conclusion of the June 2026 Russell Reconstitution, effective after the U.S. market close on June 26, 2026.

The June reconstitution of the Russell US indexes captures up to the 4,000 largest U.S. stocks as of April 30, ranking them by total market capitalization. Membership in the Russell 2000® Index, which remains in place for half a year beginning 2026, is based on membership of the broad-market Russell 3000® Index. The Company will also automatically be added to the appropriate growth and value indexes.

S&P and Russell indexes are widely used by investment managers and institutional investors for index funds and as benchmarks for active investment strategies. According to data as of the end of June 2025, about $12.2 trillion in assets are benchmarked against the Russell US indexes, which belong to FTSE Russell, the global index provider.

Elemental’s inclusion in these indexes marks another important milestone in the Company’s continued growth as an emerging mid-tier, gold-focused royalty company.

Elemental Chief Executive Officer, David M. Cole, commented: “Our inclusion in these indexes is recognition of Elemental’s growth and relevance within the global gold sector. These milestones broaden Elemental’s visibility with both Canadian and U.S. institutional and index-oriented investors. We remain focused on building a high-quality royalty platform that delivers immediate cash flow, diversified growth, and long-term discovery upside for shareholders.”

NASDAQ: ELE | TSX: ELE | ISIN: CA28620K1066 | CUSIP: 28620K106

About Elemental Royalty Corporation. Elemental is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 18 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental trades on Nasdaq and on the Toronto Stock Exchange under the ticker Symbol “ELE”.

Vancouver, British Columbia–(Newsfile Corp. – June 17, 2026) – Riverside Resources Inc. (TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY0) (“Riverside” or the “Company”) is pleased to announce the appointment of Marco Strub as an Independent Director of the Company, effective immediately.

Marco is a long-time shareholder of Riverside and has worked with major European investment firms with vast connections in mining networks. He is principal of Sircon AG, a consulting and investment research company based in Zurich, Switzerland, and was formerly a partner of Exulta AG, a portfolio management company from 1997 to 2003. He is an Independent Director of Triumph Gold Corp., and Canada Zinc Metals Corp. (Formerly: Mantle Resources Inc.). He has also been a Director of Open Gold Corp (aka, Range Capital Corp) since 2009 and Mexigold Corp. (formerly, BCY Resources Inc.) since 2011. He served as a Director at Margaret Lake Diamonds, Inc. (JDV Capital Corp.) from 2011 to 2014, and as a Director of MVE Capital Corp. since 2007. He received a Master of Arts degree from the University of St. Gallen, Switzerland in 1982.

“We are pleased to welcome Marco to the Board,” commented John-Mark Staude, CEO of Riverside Resources. “His deep background in investment research, portfolio management, and capital markets, combined with his extensive experience serving on the boards of public mining companies, brings valuable perspective as Riverside continues to advance its project portfolio and partnership model. We look forward to his contributions and counsel.”

“Riverside has built a disciplined approach to project generation and value creation in the resource sector,” said Mr. Strub. “I am pleased to join the Board and to support the Company and its shareholders as it advances its exploration and partnership initiatives.”

Riverside would like to thank James Ladner for his service as a director. After choosing not to stand for re-election, James leaves behind a legacy of meaningful contribution where his deep expertise in accounting, mining finance, and the broader mineral business has been invaluable to the Company. While Mr. Ladner will no longer serve as a formal director, he will continue to share his insights and provide input to Riverside going forward.

Results of Annual General Meeting of Shareholders

The Company is pleased to provide the results of its Annual General Meeting of Shareholders which was held on June 4, 2026.

At the Annual General Meeting of shareholders, 6,365,550 shares were voted, representing 6.81% of the total 93,443,464 issued and outstanding shares, and the Company received majority shareholder approval for the following:

1. To set the number of directors at five (5):

2. Elected one new and re-elected four incumbent directors, total of five directors for the ensuing year as follows:

Director

Votes For

%

John-Mark Staude

6,358,050

99.88%

James Clare

6,358,050

99.88%

Walter Henry

6,358,050

99.88%

Bryan Wilson

6,358,050

99.88%

Marco Strub

6,358,050

99.88%

3. Appointment of Auditor: To appoint Davidson & Company LLP, Chartered Professional Accountants, as auditors of the Company for the ensuing year and to authorize the directors to fix their remuneration.

4. To consider, and if deemed advisable, pass an ordinary resolution, substantially in the form set out in the accompanying management information circular (the “Information Circular”), re-approving the continued use of Riverside’s stock option plan.

Details of the matters approved at the meeting are set out in the Company’s Information Circular dated April 20, 2026 and available under the Company’s profile on SEDAR+ at www.sedarplus.ca.

About Riverside Resources Inc.

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has a solid balance sheet with no debt and 93M shares outstanding with a strong portfolio of gold-silver and copper assets and royalties in North America. Riverside has extensive experience and knowledge operating in Mexico and Canada and leverages its large database to generate a portfolio of prospective mineral properties. Riverside has properties available for option, with information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information, contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Corporate Communications Riverside Resources Inc. Eric@rivres.com Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the risk that the Transaction will not be completed as contemplates, or at all, availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.