Edmonton, Alberta–(Newsfile Corp. – March 17, 2026) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) announces that, on March 17, 2026, it closed on the sale of 2,030,000 Units and 13,430,000 FT Units, at $0.035 per Unit and FT Unit, for gross proceeds of $541,100 as an initial tranche of a non-brokered private placement originally announced on February 27, 2026 (the “Offering”).

The Offering consists of up to 7,142,856 Units and up to 21,428,574 of any combination of Units and FT Units. Each Unit consists of one common share of the Company (“Common Share”) and one Common Share purchase warrant entitling the warrant holder to purchase an additional Common Share for $0.055 and expiring on the earlier of a) 30 days following written notice by the Company to the warrant holder that the volume-weighted average trading price of the Common Shares on the TSX Venture Exchange is at or greater than CA$0.10 per Common Share for 10 consecutive trading days; and (b) 60 months (5 years) from the date of issuance (“Unit Warrant”). Each FT Unit consists of one Common Share and one half of one Common Share purchase warrant (“FT Unit Warrant”), each of which shall be issued as a “flow through share” for the purposes of the Income Tax Act (Canada). Each whole FT Unit Warrant shall entitle the holder to purchase an additional Common Share for $0.055 and expiring on the earlier of a) 30 days following written notice by the Company to the warrant holder that the volume-weighted average trading price of the Common Shares on the TSX Venture Exchange is at or greater than CA$0.10 per Common Share for 10 consecutive trading days; and (b) 36 months (3 years) from the date of issuance.

The Offering remains open, with up to 5,112,856 Units and up to 7,998,574 of any combination of Units and FT Units, pursuant to closing of this first tranche. The Units and the FT Units are being offered at $0.035 per Unit or FT Unit. The Offering is being offered to qualified subscribers in the Provinces of Alberta, British Columbia and Ontario and in other jurisdictions as the Company may in its discretion determine, in reliance upon exemptions from the registration and prospectus requirements of applicable securities legislation.In connection with the sale of an aggregate 2,030,000 Units and 12,430,000 FT Units, the Company paid cash finder’s fees of $29,463 and issued 841,800 non-transferable finder’s warrants, with equivalent terms to the FT Unit Warrants (“Finder Warrants”) as follows:

FinderFinder WarrantsCash Finder FeeVentum Financial Corp.36,000$1,260Hampton Securities Inc.60,000$2,100GloRes Securities Inc.685,800$24,003Raymond James Limited60,000$2,100 Following closing, the Company has 221,925,956 common shares issued and outstanding. The Common Shares and any Common Shares issued on exercise of the Unit Warrants, FT Unit Warrants, and Finder Warrants are subject to restrictions on trading until July 18, 2026. The Offering is subject to final acceptance of the TSX Venture Exchange.

ABOUT GRIZZLY DISCOVERIES INC.Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and base metals properties in southeastern British Columbia. Grizzly is run by a highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.On behalf of the Board,GRIZZLY DISCOVERIES INC.Brian Testo, CEO, PresidentSuite 363-9768 170 Street NWEdmonton, Alberta T5T 5L4Email: info@grizzlydiscoveries.comFor further information, please visit our website at www.grizzlydiscoveries.com or contact:

On behalf of the Board,GRIZZLY DISCOVERIES INC.Brian Testo, CEO, PresidentSuite 363-9768 170 Street NWEdmonton, Alberta T5T 5L4Email: info@grizzlydiscoveries.comFor further information, please visit our website at www.grizzlydiscoveries.com or contact:Nancy MassicotteCorporate DevelopmentTel: 604-507-3377Email: nancy@grizzlydiscoveries.comNeither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedarplus.ca. Grizzly disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

March 18, 2026 – Vancouver, BC: Riverside Resources Inc. (“Riverside” or the “Company”) (TSX-V: RRI) (OTCQB: RVSDF) (FSE: 5YY0), is pleased to announce the successful consolidation of the Famosa Area with three mineral concessions within the Union Project district in Sonora, Mexico, through the completion of the final payment and transfer of mineral title from Pacific Comox S.A. de C.V. to Riverside’s wholly owned Mexican subsidiary, RRM Exploración S.A.P.I. de C.V.. This provides the Company with clear ownership and the ability to advance exploration and, potentially, move toward mining based on future development results.

The transaction completes the acquisition of three mineral concessions: La Famosa, Dana 7, and Dana 7 which form an important portion of the southern part of the Union Project district. These concessions are mineral titles 199006, 220840, and 220841, with validity extending from 1994 through 2044 and 2003 through 2053, respectively. This long-term validity and fully titled status fit with the rest of the district mineral titles that the Company is advancing through its spring 2026 mineral exploration program.

The concessions were originally secured through an exploration agreement signed in August 2021 between RRM Exploración S.A.P.I. de C.V. and Pacific Comox S.A. de C.V., which provided Riverside with an option to purchase the claims within a five-year period (2021–2026). With the completion of the final payment of US$125,000, Riverside has now exercised the purchase option, and the titles have been formally transferred to Riverside. The total consideration for the acquisition amounts to US$175,000, and notably no net smelter royalty (“NSR”) or any other type of royalty is attached to this transaction.

“We are pleased to complete the consolidation of the Famosa area within the Union Project, securing full ownership with no royalty burden for the transaction on these key concessions,” said John-Mark Staude, President and CEO, Riverside Resources Inc. “This strengthens our district-scale land position and provides greater flexibility as we continue advancing exploration at Union with our partner Questcorp.”

The Famosa Area hosts carbonate replacement deposit (CRD) style mineralization and structurally controlled gold mineralization within dolomite and quartzite units, located in the southern portion of the broader Union Project district. The consolidation strengthens Riverside’s land position within the Union district and supports ongoing exploration efforts targeting CRD-style gold–silver–polymetallic mineralization.

This transaction represents another step in the systematic advancement of the Union Project, where Riverside has been working in partnership with Questcorp under an option agreement that provides for up to C$5.5 million in exploration expenditures funded by Questcorp while Riverside retains equity exposure and a 2.5% net smelter royalty on the project. Previous exploration programs at Union have included geological mapping, geophysics, diamond drilling, and high-grade rock chip channel sampling that have confirmed the presence of gold- and polymetallic-bearing CRD-style and sediment hosted gold-style mineralization across multiple targets within the district. By securing the Famosa concessions outright, Riverside further consolidates its district-scale land position and enhances the exploration potential across the southern portion of the Union Project. The expanded control of mineral titles provides increased flexibility for future exploration programs and supports the continued advancement of the project with partner-funded exploration.

Further technical updates related to exploration activities at the Union Project will be provided as programs progress.

About the Union Project

The Union Project is a district-scale carbonate replacement deposit (CRD) exploration project located in Sonora, Mexico. The project hosts historical mining areas and multiple exploration targets associated with gold, silver, zinc, and lead mineralization within carbonate and structurally controlled settings. Riverside operates the project through its Mexican subsidiary while advancing exploration in partnership with Questcorp.

Qualified Person

The technical content of the news release has been reviewed and approved by Freeman Smith, P.Geo. (British Columbia), a qualified person under National Instrument 43-101 who is non-independent and the Vice President Exploration for the Company.

About Riverside Resources Inc.: Riverside is a well-funded exploration company driven by value generation and discovery. The Company has a strong balance sheet with over C$5,000,000 cash, no debt and tight share structure with a strong portfolio of gold-silver, copper, and REE assets and royalties in North America. Further information about Riverside is available on the Company’s website at www.rivres.com.

ON BEHALF OF THE BOARD OF RIVERSIDE RESOURCES INC.

Eric Negraeff Investor Relations Riverside Resources Inc. Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the risk that the Transaction will not be completed as contemplates, or at all, availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This video features a deep-dive interview with Derek MacPherson, President and CEO of West Point Gold ($WPG), regarding the significant new gold discovery at the Black Dyke target within the Gold Chain Project in Arizona. Below is a detailed breakdown of the discussion with associated timestamps:

“Check out the timestamp links below to jump directly to the detailed technical analysis of the new Black Dyke discovery zone!”

0:00 – Introduction & Company Overview 1:30 – The Oatman District & Walker Lane Trend 3:15 – Black Dyke Target: 36.6m of Surface Gold Breakdown 5:45 – Validating a Potential Deeper System: Deeper Drill Hits 8:00 – 15,000m Program: Where are the Next 24 Drill Hole Assays Pending? 10:30 – Key Milestones defining a ‘Successful’ 2026 12:45 – Capital Structure & Financial Discipline 15:00 – CEO’s Closing Message & How to Invest

Vancouver, Canada – March 17, 2026 – West Point Gold Corp. (“West Point Gold” or the “Company”) (TSX.V: WPG) (OTCQB: WPGCF) (FSE: LRA0) is pleased to announce the intersection of shallow gold mineralization at the Black Dyke target located four kilometres (“km”) west of the Tyro Main Zone, at the Company’s Gold Chain Project in Arizona. The initial six reverse circulation (“RC”) drill holes at Black Dyke, suggest it is a highly prospective area where additional resources could be defined at the Gold Chain Project. Recent drilling results from the Black Dyke prospect have further prioritized the target for follow-up drilling in early 2026. To date, 10,255m of the ongoing 15,000m drill program at the Gold Chain project have been completed. Results are pending for 24 holes representing 5,361m from the Tyro Main Zone, South Tyro, Sheep Trail, and Bull 8 targets.

Highlights:

Black Dyke hosts a shallow-dipping body of quartz veinlets and breccia ranging in estimated thickness between 7.6 and 36.6m over a strike length of at least 200m and from surface to approximately 250m down-dip

The zone remains open along strike to the west and down-dip to the southwest

Alteration and textures observed in near surface drill results suggest the presence of a potentially deeper gold system associated with this shallow mineralization.

4 km west of Tyro, Black Dyke now represents a second area for potential resource development; follow-up drilling is planned to expand the limits of the shallow oxidized gold mineralization

“Black Dyke is now a potential second resource development area at Gold Chain, which is a meaningful milestone for the project. Shallow, oxidized gold from the surface, with the zone open in multiple directions, gives us a well-defined path to expand this target. Equally compelling is that West Point Gold found this by applying modern methods to a historically underexplored prospect, and the Company is taking that same approach across the property. With results pending from multiple step-out targets, it appears that the potential of the Gold Chain Project is still being defined”, stated Derek Macpherson, President and CEO.

Table 1: Drill Results

Holes

From(m)

To(m)

Width(m)

Grade(g/t Au)

GC25-095

0

36.6

36.6

1.04

GC25-097

4.6

15.2

10.6

0.80

GC26-098

21.3

42.7

21.3

0.92

GC26-099

62.5

70.1

7.6

1.56

GC26-100

No Significant Intercepts

GC26-101

114.3

126.5

12.2

1.09

Note: All widths shown are downhole; true widths are greater than 80% of downhole widths.

Figure 1: Plan view of the Gold Chain project showing geology, historical mines and/or current prospects. Note the location of the Black Dyke prospect.

Figure 2. Geologic map of the Black Dyke prospect showing drill holes and surface samples.

Drilling Summary

Holes GC26-95 and GC26-97 through GC26-101 (Table 1) confirm the presence of gold in the subsurface over meaningful grades and widths. The mineralized zone is part of the historical Black Dyke structure and confirms the presence of gold identified in previous exploration efforts. Figure 3 provides a preliminary view of this newly drilled zone and reveals that the gold-bearing holes cut the surface breccia a short distance, up to 250m, down-dip. Given that other NE-trending structures in the district have served as gold-bearing conduits, such as Tyro, Figure 2 suggests that a similar relationship exists at Black Dyke. A short distance into the hanging wall, volcanic rocks deposited upon the Precambrian granite are strongly altered (kaolinite-silica-iron oxide) and brecciated (Figure 3).

The geologic section provided in Figure 3 reveals a sub-horizontal ‘blanket’ of quartz-calcite breccia and veins at shallow depths. Hole GC26-95 contains 36.6m of 1.04 g/t Au and GC26-98 intersected 21.3m of 0.92 g/t Au. It appears that the holes closest to the intersection of the ‘Black Dyke’ breccia and the suspected NE-trending structure are thicker and point to the importance of this structural intersection. The southward continuation of this mineralized zone is likely and supported by the projection of mineralized, regional structures (Roadside Mine fault) and hydrothermal alteration in the overlying volcanics (Figure 1).

West Point Gold plans to return to the area to expand the gold zone by drilling to depth and laterally. The gold-bearing vein occurs as fragments in a calcite-cemented breccia. It is anticipated that these fragments emanated from a discrete vein or breccia body at depth.

Figure 3. Geologic section along Holes GC26-95, -98 and -101 revealing shallow gold mineralization above the water table (oxidized) extending beneath strongly altered and brecciated volcanics. Fault offsets are postulated, and irregularities in the breccia may, instead, reflect fault refractions or bends.

Project Geology

The northern limit of the Black Dyke prospect is defined by a northwest-trending low-lying ridge composed of coarsely crystalline calcite cementing up to 80+% chalcedony vein and vein (hydrothermal) breccia (Figure 4). The calcite is commonly banded and can be correlated to other calcite veins across the Gold Chain project, which are considered to have been deposited late in the gold system’s history and after the gold events.

Historical reports and mapping suggested a southward dip between 30 and 60 degrees. Drilling now indicates a shallow, southerly dip of less than 30 degrees. The western and eastern limits of the low-angle breccia are defined by north- to northeast-trending faults (Figure 2). In the surface exposures both the footwall (“FW”) and hangingwall (“HW”) rocks are composed of Precambrian granite. The FW contact is sharp with weak propylitic alteration in the underlying Precambrian rocks. The HW is strongly replaced by chlorite and invaded by abundant low-angle calcite veins (<1m) and veinlets. Surface weathering, which extends down to the footwall contact, is evidenced by strong iron and manganese oxides in the gold-bearing zones. Gold mineralization in these initial holes is associated with quartz-chalcedony-calcite veinlets, vein and vein breccia.

This entire south-dipping package passes beneath intensely altered (kaolinite-silica-iron oxides) Miocene dikes and volcanic breccias and tuffs. These rocks comprise distinct low-lying hills surrounded by alluvial deposits composed of gravel and sand. It is suspected that this high-level alteration is related to the gold events operative at Black Dyke.

Figure 4. Photograph of the Black Dyke ‘vein breccia’ showing the dark ‘desert varnish’ patina on quartz vein and vein breccia hosted in white-gray, massive to banded coarsely crystalline late-stage calcite.

Project History

The Black Dyke mine, which consists of a backfilled shaft, several small pits and dumps, and extensive roads, is located 4.8km east of the Katherine mine and 4.0km west of the Tyro Main Zone. The Katherine vein, like the Tyro vein (West Point Gold), trends northeast and consists of a broad zone of sub-parallel quartz-chalcedony-adularia-calcite veins and veinlets developed along ancestral shears and Miocene rhyolite dikes. Shortly after the discovery of the Katherine vein in 1900, prospectors discovered a broad, easterly trending gold-bearing ridge referred to as a “dyke”. It was later described as a vein breccia, up to 30 meters wide, composed of broken chalcedony vein and breccia cemented by a massive to banded, coarsely crystalline gray calcite with elevated manganese (Figure 4). Weathering of the siliceous vein fragments resulted in a dark patina (desert varnish) and, hence, the Black Dyke (dike).

There is no reported gold production from the Black Dyke mine although a two-compartment shaft was open in 1940 which was sunk to 150 feet (45.7m) in the hanging wall of the south-dipping breccia complex. Several hundred feet of drifting was conducted from the bottom of the shaft with much of it reported to be in mineralized rock. Historical assays reveal low gold grades over broad widths up to 30m. Intermittent exploration and development activities continued up through the 1930s but without recorded production.

In the 1980s, several RC/rotary drilling campaigns were conducted with up to 12 holes drilled across the prospect (see Figure 2). One hole, RSM15, drilled 20m of 0.65 g/t Au at 41m. Although the historical (pre-2020) database is considered incomplete, the holes plotted in Figure 2 appear to have been too shallow. Aside from these few holes, there does not appear to have been additional exploration until West Point Gold optioned the property in 2019.

Table 2: Drill hole locations and descriptions

Hole No.

Azimuth (degrees)

Inclination (degrees)

Easting

Northing

Length

GC25-095

0

-45

727932

3901658

62.5

GC25-097

45

-60

728006

3901621

74.7

GC26-098

0

-70

727952

3901592

86.9

GC26-099

330

-50

727838

3901632

106.7

GC26-100

50

-70

728038

3901472

144.8

GC26-101

280

-50

728033

3901471

150.9

Qualified Person

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration, is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for overseeing all phases of the drilling program, including logging, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Drillholes have a diameter of about 10cm, and samples have an approximate weight of 5 to 10kg. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, and over-limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), and over-limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. The results summarized above have been carefully reviewed with reference to the QA/QC results. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

About West Point Gold Corp.

West Point Gold is an exploration and development company focused on unlocking value across four strategically located projects along the prolific Walker Lane Trend in Nevada and Arizona, USA, providing shareholders with exposure to multiple discovery opportunities across one of North America’s most productive gold regions. The Company’s near-term priority is advancing its flagship Gold Chain Project in Arizona.

For further information regarding this press release, please contact:

Certain statements contained in this press release constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements in this press release include statements with respect to Black Dyke representing a second area for potential resource development, that follow-up drilling is planned to expand the limits of the shallow oxidized gold mineralization, that near surface drill results suggest the presence of a potentially deeper gold system associated with this shallow mineralization and include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures. The Company cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete any payments or expenditures required under the Company’s various option agreements for its projects; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainties related to resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data; the potential for delays in exploration or development activities; uncertainty related to the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results may vary from those expected; statements about expected results of operations, royalties, cash flows, financial position may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions. The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; fluctuating gold prices; possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR made by the Company with securities regulators. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate press release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

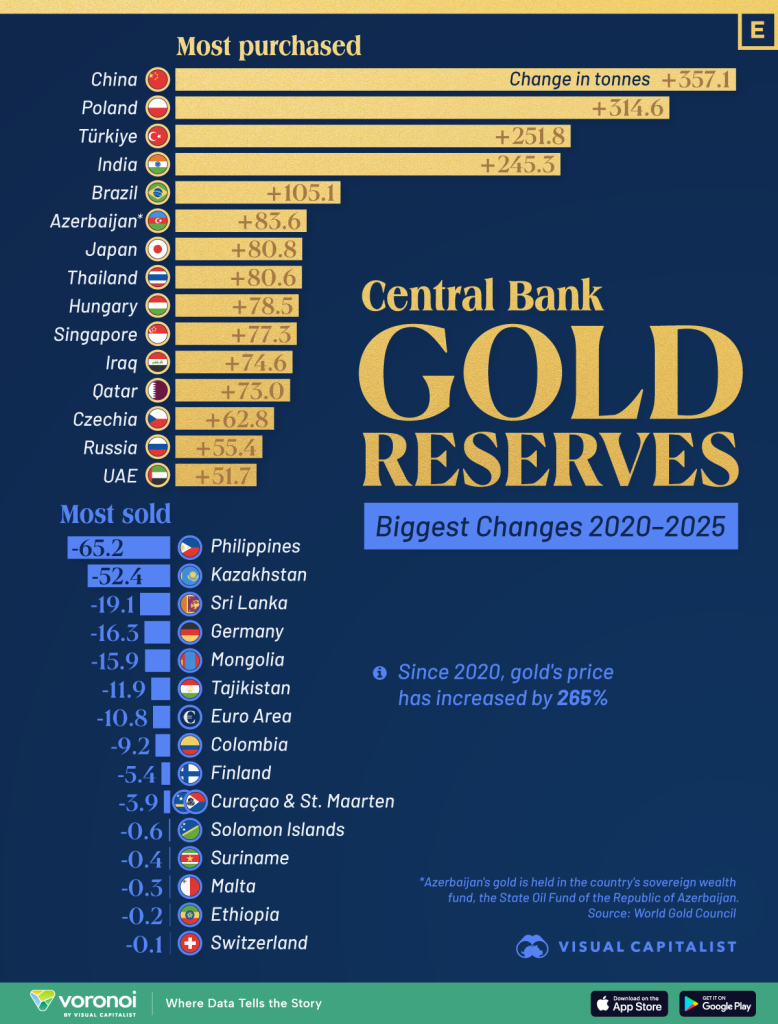

Central Bank Gold Reserves: Biggest Changes (2020–2025)

See visuals like this from many other data creators on our Voronoi app. Download it for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Key Takeaways

China, Poland, and Türkiye led global gold buying among central banks between 2020 and 2025.

Rising gold prices and currency risk pushed many countries to boost gold reserves, while a smaller group reduced holdings.

Gold prices soared past $5,500 an ounce in late January as weakness in the U.S. dollar continued to steer investors toward hard assets. Since 2020, gold prices have risen by more than 230%, increasing the appeal of bullion for central banks seeking stability during a volatile economic period.

This visualization highlights which central banks made the biggest changes to their gold reserves between 2020 and 2025. The data for this visualization comes from the World Gold Council.

China and Eastern Europe Lead Gold Buying

China recorded the largest increase in gold reserves over the period, adding more than 350 tonnes. This reflects a broader strategy to diversify reserves away from the U.S. dollar and strengthen financial independence. Poland followed closely, increasing its gold holdings by over 300 tonnes as part of a long-term push to bolster monetary security.

Türkiye and India also ranked among the top buyers. Both countries face persistent inflation pressures and currency volatility, making gold an attractive hedge within official reserves.

Most gold purchased

2020-2025 (tonnes)

Most gold sold

2020-2025 (tonnes)

China

357.1

Philippines

-65.2

Poland

314.6

Kazakhstan

-52.4

Türkiye

251.8

Sri Lanka

-19.1

India

245.3

Germany

-16.3

Brazil

105.1

Mongolia

-15.9

Azerbaijan

83.6

Tajikistan

-11.9

Japan

80.8

Euro Area (average)

-10.8

Thailand

80.6

Colombia

-9.2

Hungary

78.5

Finland

-5.4

Singapore

77.3

Curaçao & St. Maarten

-3.9

Iraq

74.6

Solomon Islands

-0.6

Qatar

73

Suriname

-0.4

Czech Rep.

62.8

Malta

-0.3

Russia

55.4

Ethiopia

-0.2

United Arab Emirates

51.7

Switzerland

-0.1

Emerging Markets Step Up Accumulation

Beyond the largest buyers, several emerging markets made notable additions. Brazil added more than 100 tonnes, while Azerbaijan’s increase came through its sovereign wealth fund, the State Oil Fund of the Republic of Azerbaijan.

Japan, Thailand, Hungary, and Singapore also expanded reserves, signaling broader global interest in gold as a stabilizing asset during periods of economic uncertainty.

Who Reduced Gold Holdings?

On the selling side, the Philippines recorded the largest reduction, cutting reserves by over 65 tonnes. Kazakhstan and Sri Lanka also saw significant declines, often linked to domestic liquidity needs or reserve rebalancing.

Several European countries, including Germany and Finland, posted modest reductions. Switzerland’s change was minimal, underscoring its generally stable approach to gold management compared with more active buyers elsewhere.

Forecast 240 koz deficit for 2026 follows deep 1,082 koz deficit in 2025

Depleted above ground stocks projected to remain at just over four months’ worth of global demand through 2026

Total bar and coin investment demand to jump 35% to 725 koz, with gains expected across all markets and India emerging as a new growth market

While exchange traded fund (ETF) and exchange stocks are expected to remain at elevated levels, the significant inflows seen in 2025 are not expected to repeat, resulting in total demand coming in 8% lower than in 2025 at 7,619 koz

Industrial demand to rebound, increasing 11% to 2,124 koz as glass capacity expansion resumes, helping to offset respective 3% and 12% reductions in automotive and jewellery demand

Total platinum supply to increase by 2% as recycling supply grows 10%, incentivised by higher prices, while mine supply is projected to be flat

LONDON, March 4, 2026 /PRNewswire/ — The World Platinum Investment Council – WPIC® – today publishes its PlatinumQuarterly for the fourth quarter of 2025 and full year 2025, with a revised forecast for 2026.

Trevor Raymond, CEO of the World Platinum Investment Council, comments:

“The key drivers of platinum’s price rally in 2025, namely strong supply/demand fundamentals, a depletion of above ground stocks, and macropolitical uncertainty-driven precious metals demand, are expected to persist in 2026. Consequently, market tightness is likely to continue, maintaining investor interest in platinum, and further supporting bar and coin and ETF demand throughout the year. One item not yet captured in the supply/demand balance is any exchange stocks warehoused with the Guangzhou Futures Exchange, which could potentially deepen the deficit versus current projections once these are made publicly available.”

Neither the World Platinum Investment Council nor Metals Focus is authorised by any regulatory authority to give investment advice. Nothing within this document is intended or should be construed as investment advice or offering to sell or advising to buy any securities or financial instruments and appropriate professional advice should always be sought before making any investment.

Denver, Colorado–(Newsfile Corp. – March 2, 2026) – Elemental Royalty Corporation (TSXV: ELE) (NASDAQ: ELE) (“Elemental” or “the Company“) notes the announcement by Quilla Resources Inc. (“Quilla”) on the successful production of first copper cathode from the Chapi Copper Project (“Chapi”) in southern Peru. Elemental holds a 2.0% Net Smelter Return (“NSR”) royalty on the project.

Highlights

First production of copper cathode at the Chapi Copper Project following Quilla’s acquisition in December 2024

Ramp-up underway toward plant nameplate capacity of approximately 10,000 tonnes per annum of copper cathode

Elemental expects first royalty payment from Chapi in Q1 2026

Chief Executive Officer and Director of Elemental Royalty, David M. Cole, commented: “Quilla has made phenomenal progress at Chapi with first copper cathode produced, and ramp-up underway toward nameplate capacity. This rapid progression through key de-risking milestones underscores the project’s meaningful value and significant upside potential.”

Details Quilla has announced first production of copper cathode at Chapi following the acquisition of the brownfield asset in December 2024. Quilla undertook a comprehensive technical review, engineering evaluation, and operational planning before commencing refurbishment at the mine and solvent extraction and electrowinning (SX-EW) plant facilities. The restart was achieved within the originally stated schedule and budget, reflecting management’s strong execution, operational discipline, and reaffirming Elemental’s confidence in Quilla, and in-country subsidiary Minera Pampa de Cobre S.A.C., as operators.

Following the successful commissioning of the SX-EW the plant, Quilla have stated their intention to progressively increase operating rates toward an initial 10,000 tonnes of copper cathodes per year, while completing remaining capital projects and site optimization initiatives to support stable, long-term operations.

Elemental Royalty on Chapi Acquired in January 2025, the royalty comprises a 2% NSR on minerals produced from the approximately 26,000-hectare property, as well as a 2% NSR royalty on any minerals produced from properties acquired by Quilla within a two-kilometer area of interest (“AOI”). In addition, the agreement includes an additional 2% NSR royalty from any minerals that are produced from outside the Property Royalty area, but that are processed at the Chapi Solvent Extraction Electro-Winning (“SX-EW”) plant.

Background on the Chapi Mine The Chapi Mine is located in southern Peru’s Moquegua and Arequipa Departments at an elevation of approximately 2,750 meters, and has ready access approximately 50 kilometers south-southeast from the city of Arequipa. Historical, small-scale copper production, which is poorly documented, occurred intermittently from the 1930s through the early 1980s. Subsequently, between 2006 and 2012 the Chapi Mine produced approximately 5,000 to 8,500 tonnes per annum, initially of copper sulphates from open-pit and underground mining and heap leaching, and later copper cathodes from open-pit mining, heap leaching, and SX-EW (solvent extraction-electrowinning) processing. The grades mined during 2006-2012 were reported as 0.59% – 1.04% copper. The operations were halted in 2012 due to declining copper prices and operational challenges that were mainly related to insufficient ore control on materials delivered to the leach pads.

The historical Chapi Mine is comprised of two principal open pits, underground workings, a crushing and agglomeration circuit, heap leach pads, a solvent extraction plant, an electrowinning copper cathode plant, and related infrastructure including mine camp, office facilities, water supply, and power. Since 2012, Chapi has been under care and maintenance with the principal permits for mining operations remaining in place under a temporary suspension.

For further information contact: David M. Cole CEO and Director

About Elemental Royalty Corporation. Elemental Royalty is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 18 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental Royalty trades on the TSX Venture Exchange and on NASDAQ under the ticker symbol “ELE”.

Cautionary note regarding forward-looking statements and financial outlook This news release contains certain “forward looking statements” and certain “forward-looking information” as defined under applicable United States and Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar terminology (including negative and grammatical variations thereof).

Forward-looking statements and information include, but are not limited to, statements regarding future royalties and future consideration payments or issuances of shares, or other statements that are not statements of fact. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental to control or predict, that may cause Elemental’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions, the absence of control over the mining operations from which Elemental will receive royalties, risks related to international operations, government relations and environmental regulation, the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results will not be consistent with Elemental’s expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental for the year ended December 31, 2024. Elemental undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represent management’s best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Neither the TSX-V, its Regulation Service Provider (as that term is defined in the policies of the TSX-V) or the Nasdaq Stock Market LLC accepts responsibility for the adequacy or accuracy of this press release.

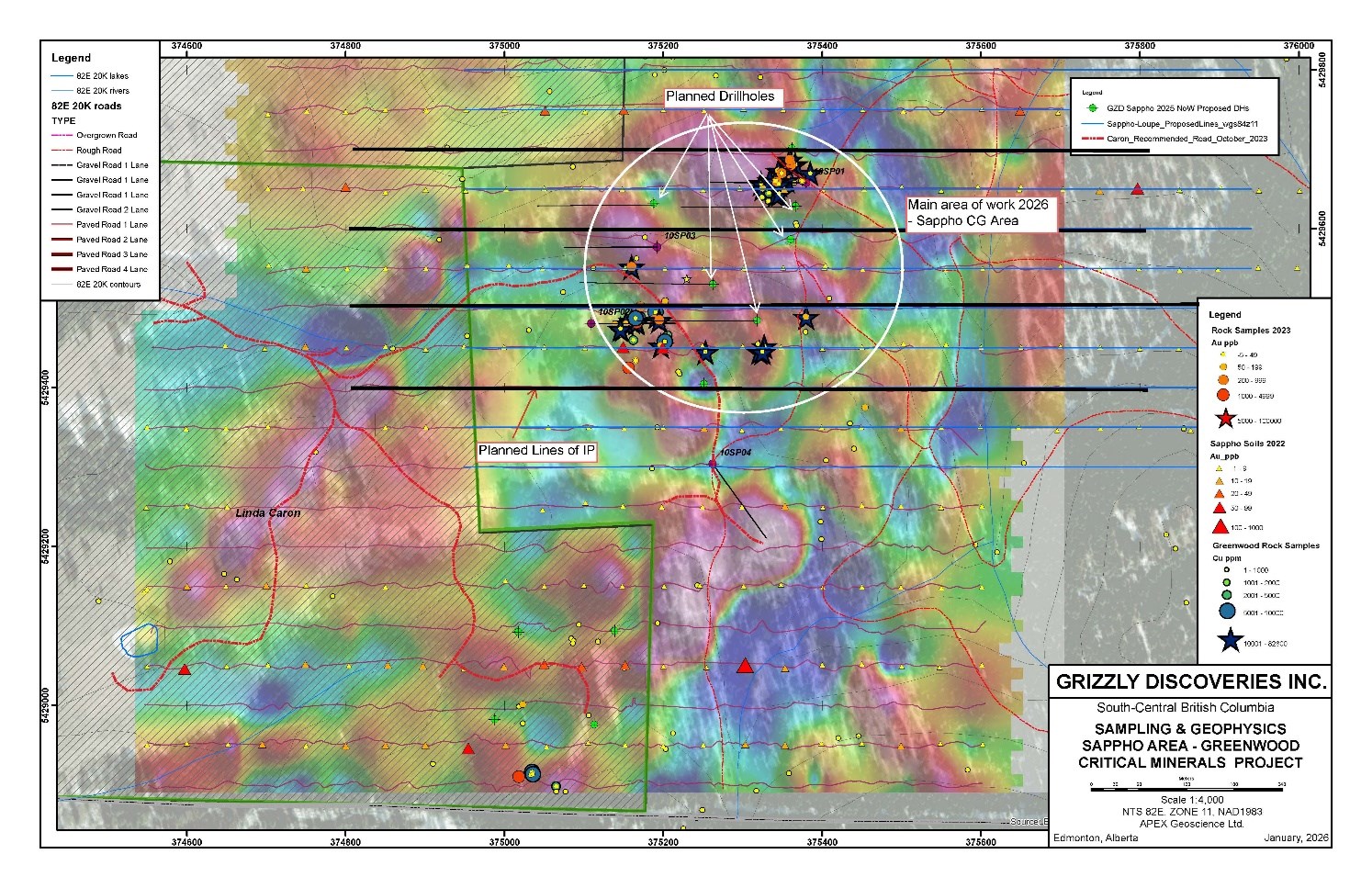

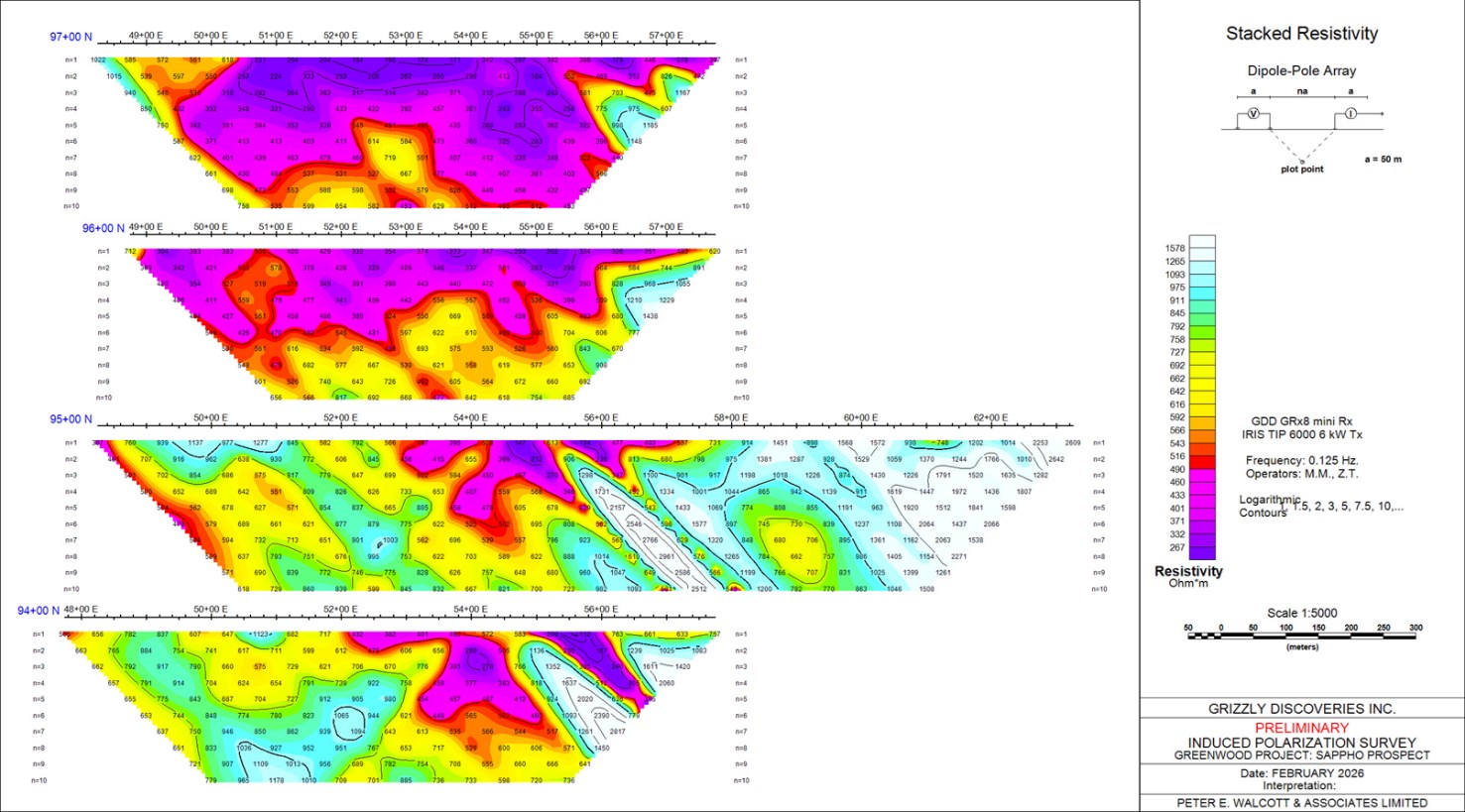

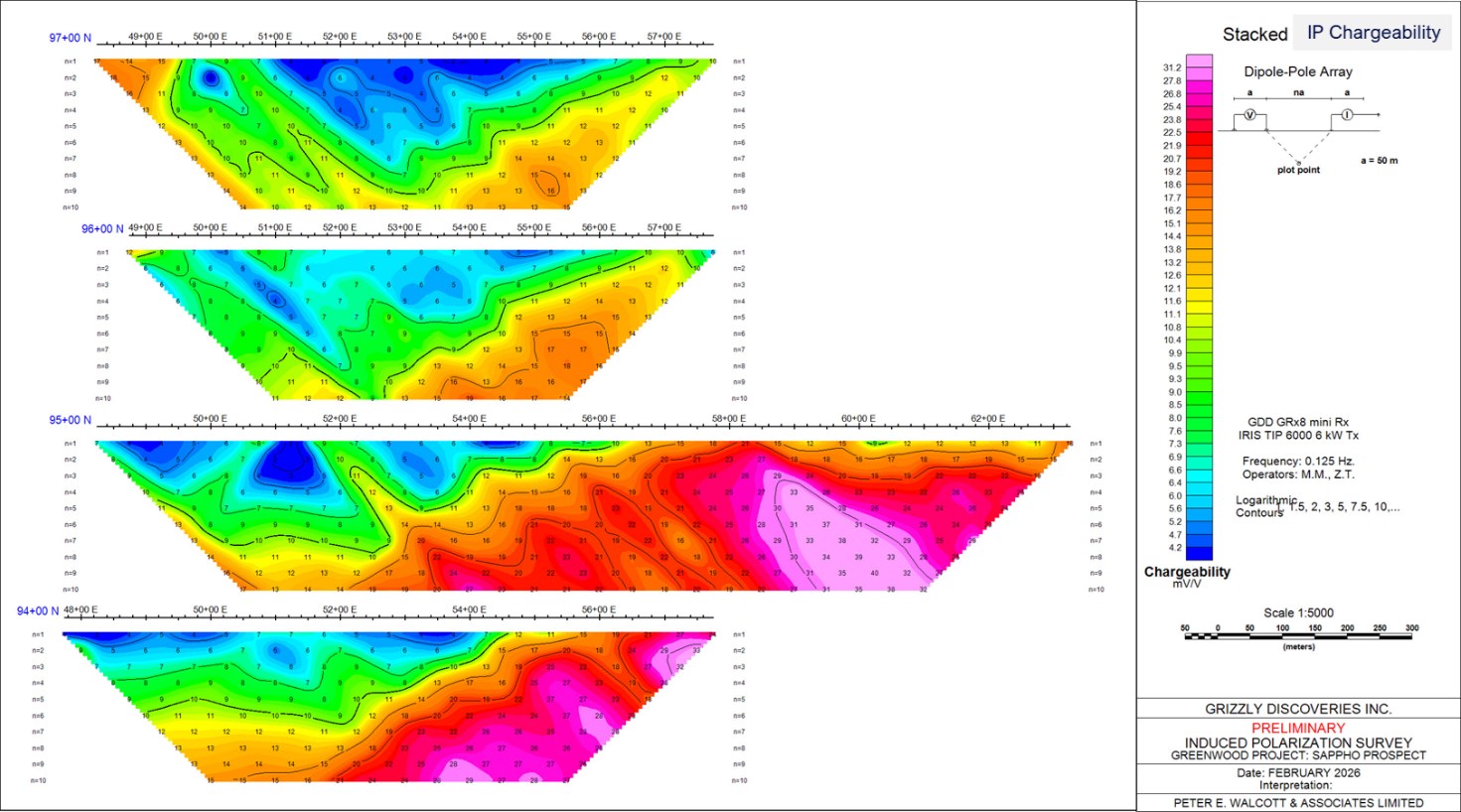

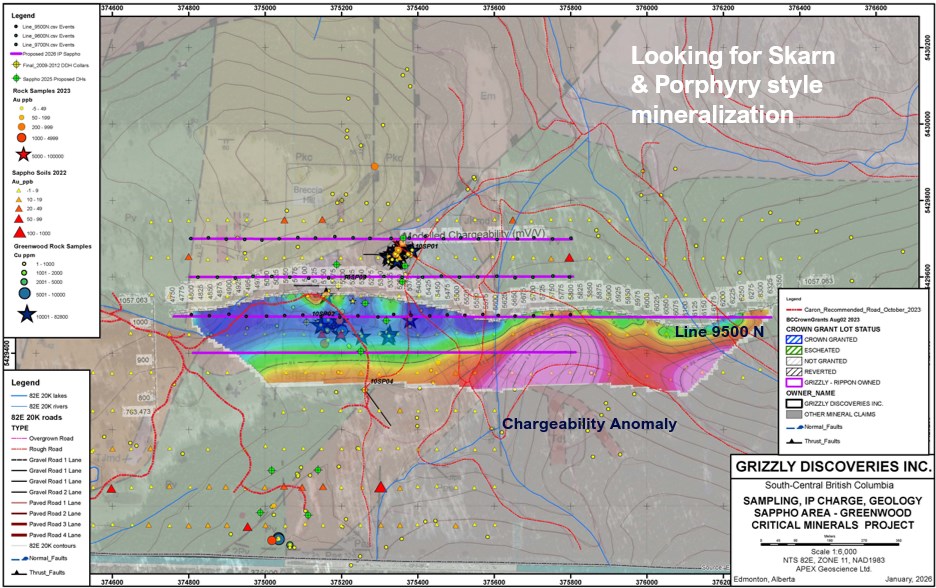

Edmonton, Alberta–(Newsfile Corp. – February 26, 2026) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) is pleased to announce that preliminary results have been received from Peter E. Walcott and Associates from an Induced Polarization (IP) program conducted in February 2026 to follow up excellent prior results from both surface sampling and historical drilling at the Sappho Critical Minerals Target (Figure 1). In light of the current escalating metal prices for critical minerals/metals including copper (Cu), platinum (Pt), palladium (Pd), gold (Au) and silver (Ag), the Sappho Skarn/Porphyry Target warrants follow-up exploration including drilling. A total of four lines of IP for 4.5 line-kms were completed. Further IP work is being planned prior to the commencement of drilling. Due to current weather conditions and the desire to complete more IP, the fully funded drilling of 4 to 6 drillholes and about 1,500 to 2,000 m at Sappho is slated to commence approximately early to mid-April.

Highlights

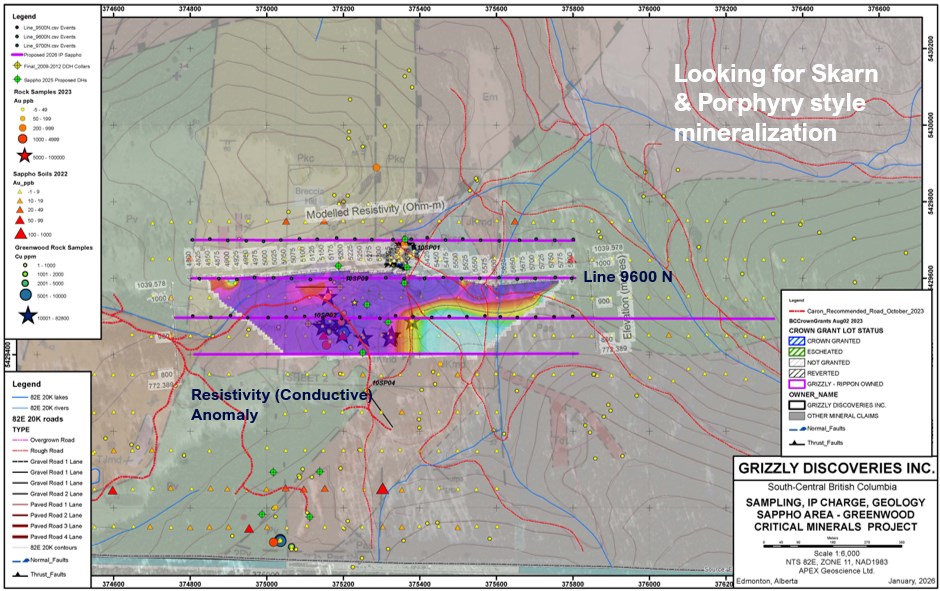

The IP survey has yielded a significant near surface conductivity anomaly on Lines 9600 and 9700 North coincident with Main Showings and the Skarn intersected in drilling in holes 10SP02 and 10SP03 in 2010 (Figures 2 and 3).

Follow-up drilling (fully funded) is planned to test the conductive zone this April.

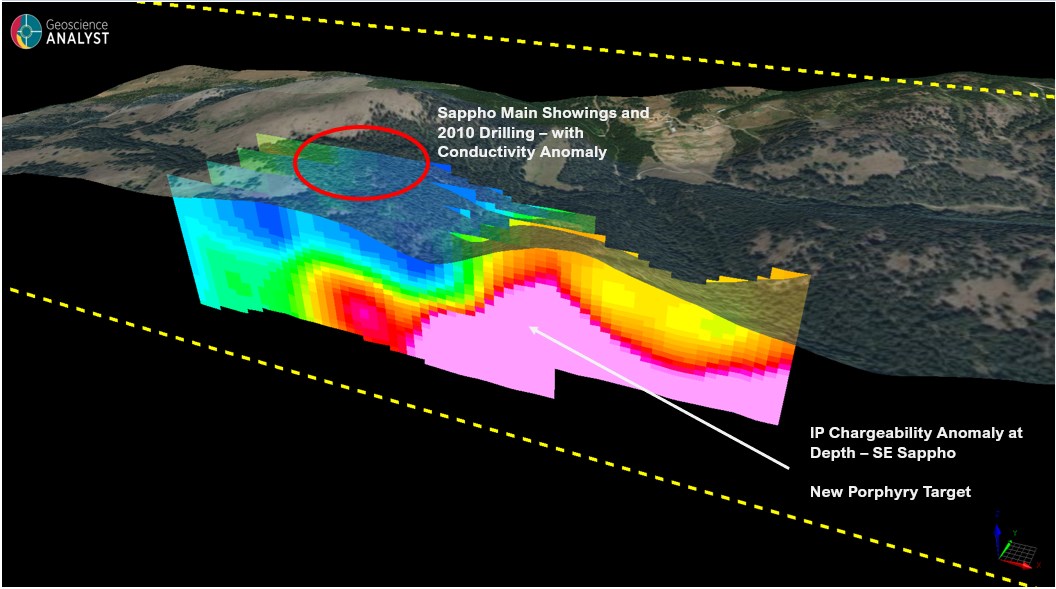

The IP Survey has detected a new significant deeper chargeability anomaly on the southeast part of the grid – likely up against one of the Main Sappho faults (Figures 4 to 6). The chargeability anomaly is not closed off and is on the order of 20 to 30 millivolts per volt and is consistent with a number of porphyry targets that have yielded new discoveries in BC recently.

Five (5) new sulphide showings were discovered during 2022 field work, with 4 of the 5 showings yielding rock grab samples with >1% copper (Cu) up to as high as 7.25% Cu (Figure 1 and see Grizzly news release dated November 3rd, 2022).

A total of 17 rock grab samples returned values >1% Cu up to 9.06% Cu, many also with anomalous gold (Au), silver (Ag), platinum (Pt) and palladium (Pd).

A total of 11 samples have yielded >500 parts per billion (ppb) Pt and Pd up to 4.64 grams per tonne (g/t) Pt and up to 2.28 g/t Pd.

The Geological Setting is the East Fault Contact of the Toroda Graben with numerous pyroxenite-monzonite-diorite (older) and younger QFP-diorite (Tertiary) intrusions into intermediate-mafic volcanics along with a complex magnetic feature at the Sappho CG area (Figure 1).

The East and West Faults of the Toroda Graben likely played a role in controlling the Au-Ag mineralization for the Buckhorn Skarn and Mine to the southwest and the Cu-Au-Ag mineralization for the Motherlode/Greyhound skarns to the north (Figure 2).

Skarn and porphyry style alteration and mineralization along with Cu-PGE’s-Au-Ag are observed in outcrop and drill core along with a complex magnetic signature in the Main Sappho CG area.

The Sappho area is being targeted for copper-gold skarn and porphyry type targets associated with a Jurassic alkalic intrusive complex and several younger diorite intrusions (Figure 1). A total of five new showings of copper oxide mineralization were found during the 2022 program (Figure 1). Previous surface sampling and drilling by Grizzly has yielded significant anomalous copper, gold, silver along with platinum and palladium. Numerous historical and new rock grab samples have yielded greater than 1% Cu, 1 g/t Au, 1 g/t Ag, 1 g/t Pt and 1 g/t Pd (Figure 1).

Historical 2010 drilling by the Company (4 core holes) yielded up to 0.31% Cu, 0.75 g/t Au, 0.34 g/t Pt, 0.39 g/t Pd and 6.57 g/t Ag over 6.5 m core length in skarn at Sappho (in hole 10SP03), including a 1 m core length intersections of 3.82 g/t Au and 199 g/t Ag, and in a separate sample 1.83 g/t Pt and 2.09 g/t Pd across 1 m – these results all are associated with >1% Cu in those samples. These higher grade zones were contained within a 63.5 m core length zone logged as a pyroxene – sulphide skarn with a grade approaching 0.7% copper equivalent derived from current metal prices for Cu, Au, Ag, Pt and Pd. Drillhole 10SP03 targeted a magnetic anomaly and had no indications of surface mineralization at the time of drilling. One of the new 2022 showings has been found proximal to drillhole 10SP03 and the targeted magnetic anomaly.

Figure 1: Sappho Rock Sampling Summary 2026 and Planned IP and Drillhole Locations.

Brian “Griz” Testo, President & CEO of Grizzly Discoveries, states: “Anomalous ground magnetics and now IP has outlined multiple new targets across the Sappho Project. I am excited to see what the next phase of IP work and drilling might show us – Grizzly will continue to refine these targets to the drill ready stage for drilling in the next couple of months and I look forward to identifying some new discoveries.”

Figure 2: Sappho IP Results Showing Conductivity Anomaly Lines 9600 and 9700.

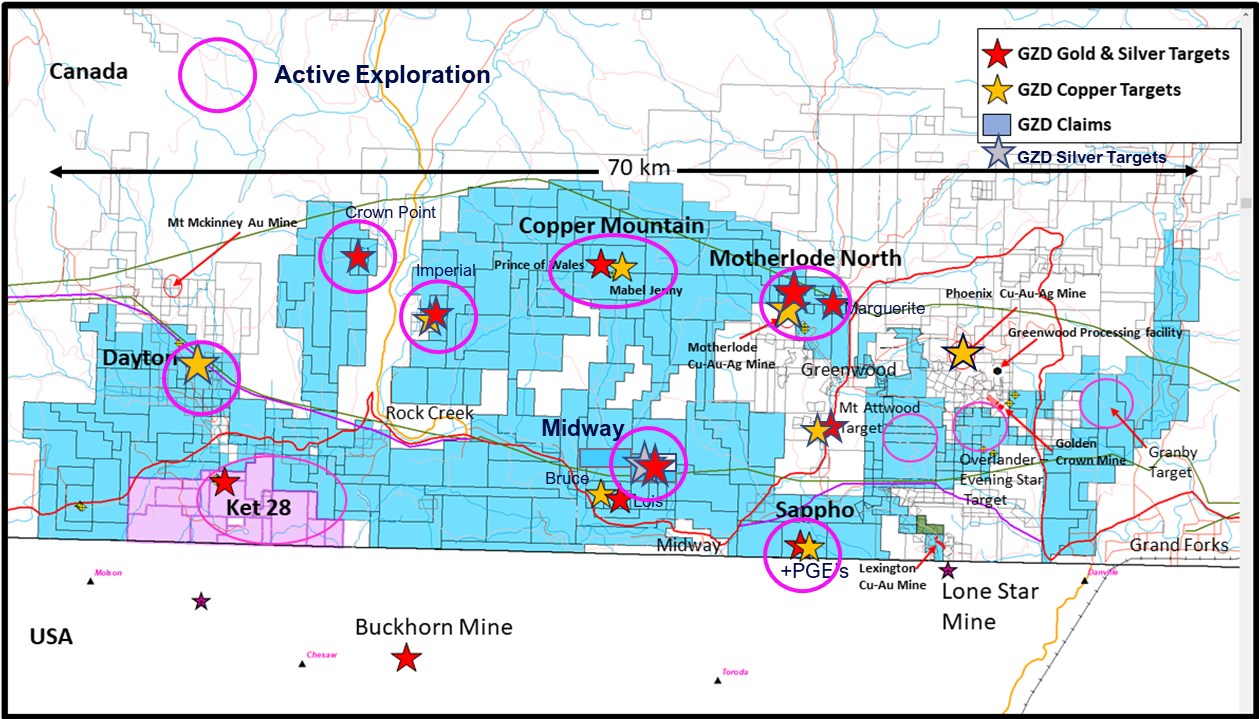

The Company is continuing with surface exploration in the Greenwood area. Crews from APEX Geoscience Ltd. completed rock sampling in August through to November and again in January. The exploration work is ongoing and includes prospecting and rock sampling at targets in the Rock Creek area, the Midway area, the Copper Mountain area, the Overlander-Attwood area and the Sappho (Figure 7). Additional groundwork including ground geophysical surveys are being planned and will comprise IP, magnetics and Loupe electromagnetics (EM) for the Sappho, the Midway and Motherlode areas (Figure 7). Rock sampling results (>220 samples) from the 2025 fieldwork are pending and will be released as they are received.

Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and base metals properties in southeastern British Columbia. Grizzly is run by a highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.

QUALIFIED PERSON STATEMENT

The technical content of this news release and the Company’s technical disclosure has been reviewed and approved by Michael B. Dufresne, M. Sc., P. Geol., P.Geo., who is a non-independent Qualified Person as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects.

On behalf of the Board,

GRIZZLY DISCOVERIES INC. Brian Testo, CEO, President

Suite 363-9768 170 Street NW Edmonton, Alberta T5T 5L4

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Caution concerning forward-looking information

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward-looking information. Such forward-looking information and statements are frequently identified by words such as “may,” “will,” “should,” “anticipate,” “plan,” “expect,” “believe,” “estimate,” “intend” and similar terminology, and reflect assumptions, estimates, opinions and analysis made by management of Grizzly in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Grizzly’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon.

Risks and uncertainties that may cause actual results to vary include but are not limited to the availability of financing; fluctuations in commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedarplus.ca. Grizzly disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

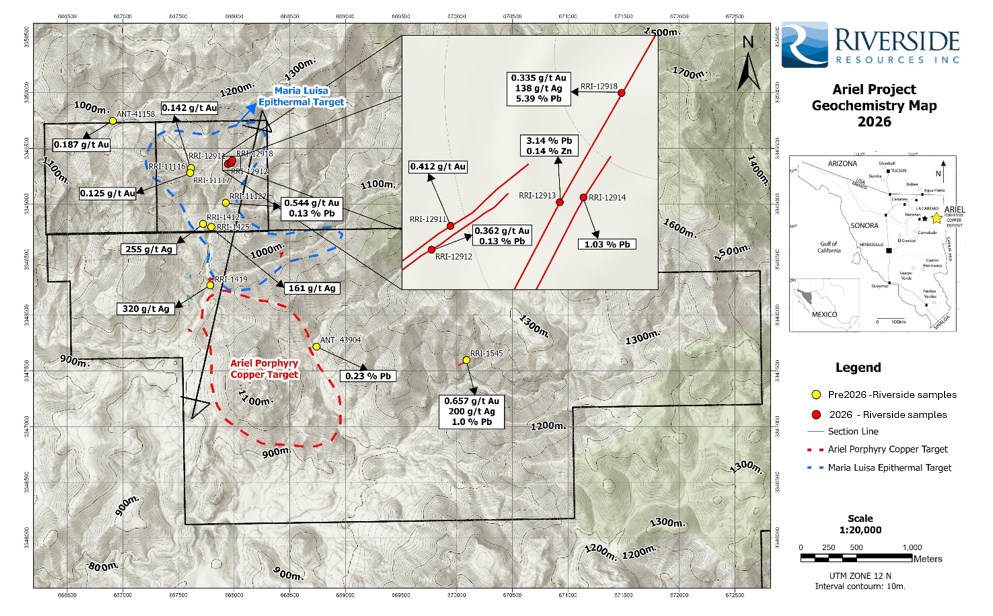

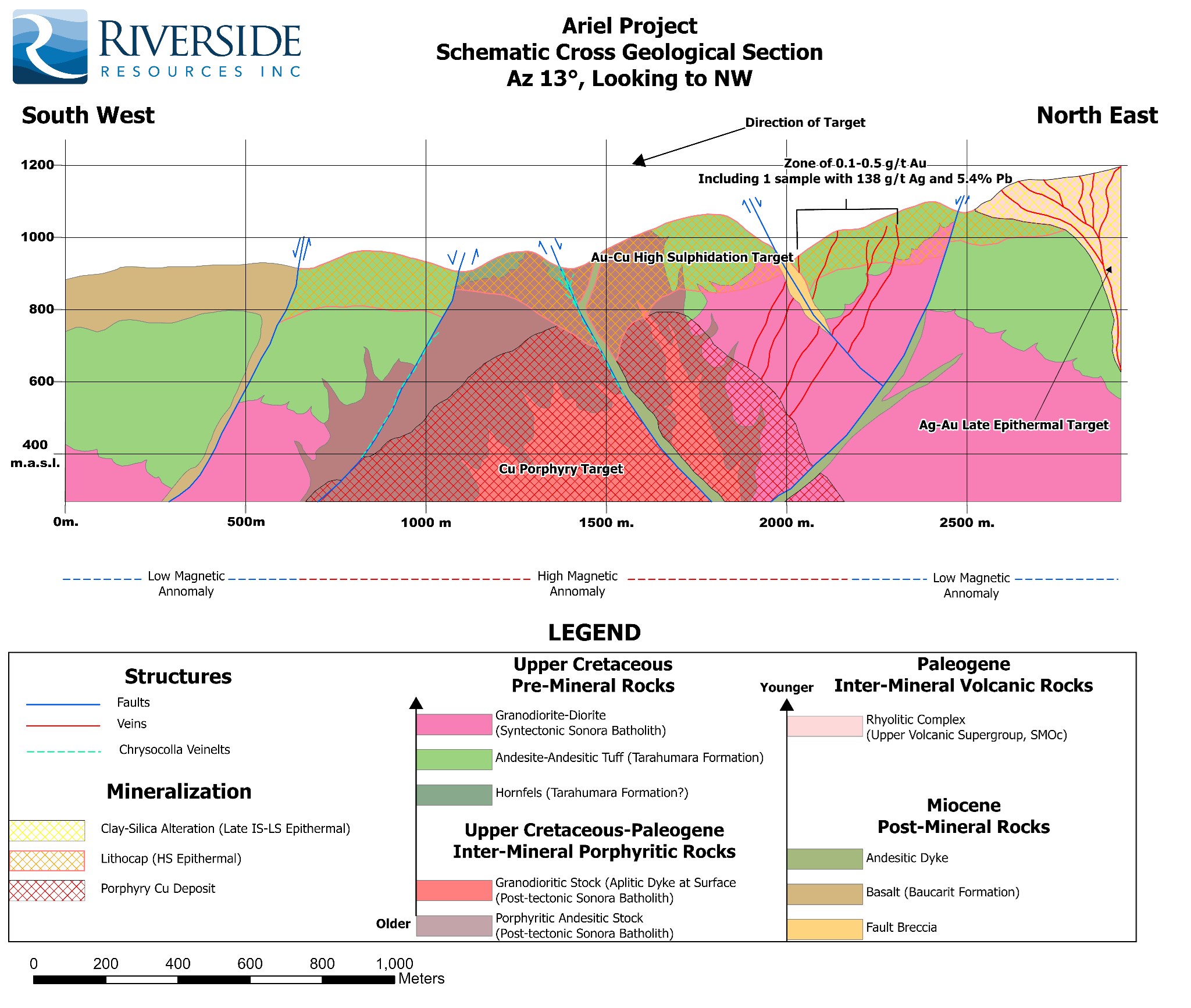

Vancouver, British Columbia–(Newsfile Corp. – February 26, 2026) – Riverside Resources Inc. (TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY0) (“Riverside” or the “Company“), is pleased to announce early 2026 assay and porphyry Cu exploration results at the 100%-owned Ariel Copper Project (the “Ariel Project” or “Ariel”) in Sonora, Mexico. Ariel is a drill-permitted, district-scale porphyry copper-gold set of targets located approximately 18 km east-southeast of the La Caridad copper mining complex in the highly productive Laramide-age Arizona-Sonora copper mining belt.

2026 Exploration Highlights

High-grade base metals with 5.4% Pb, 320 g/t Ag in veins both as targets and high-level, lateral indicators for the Ariel Porphyry Cu target

Sampling of veins in the north as shown on maps and cross section below link for the upgrade porphyry Cu target linking Maria Luisa and Ariel targets

Age dating at Ariel provides similar age to La Caridad and Cananea Mine host rocks further linking the geologic comparisons for the project to major copper districts

Applying spectral mineral analysis (near-infrared/short-wave infrared methods) to map alteration minerals commonly associated with porphyry and high-sulphidation systems, including advanced argillic assemblages and breccia-related alteration styles documented at Ariel.

Integrating mapping, alteration interpretation, and regional geophysical datasets to prioritize drill collars within permitted areas with full drive-up easy access.

Riverside sees the project ready for partnering and moving ahead as it has multiple partnerships with diverse companies on the Riverside portfolio, Ariel is now ready for partnering and drilling toward making a major copper discovery.

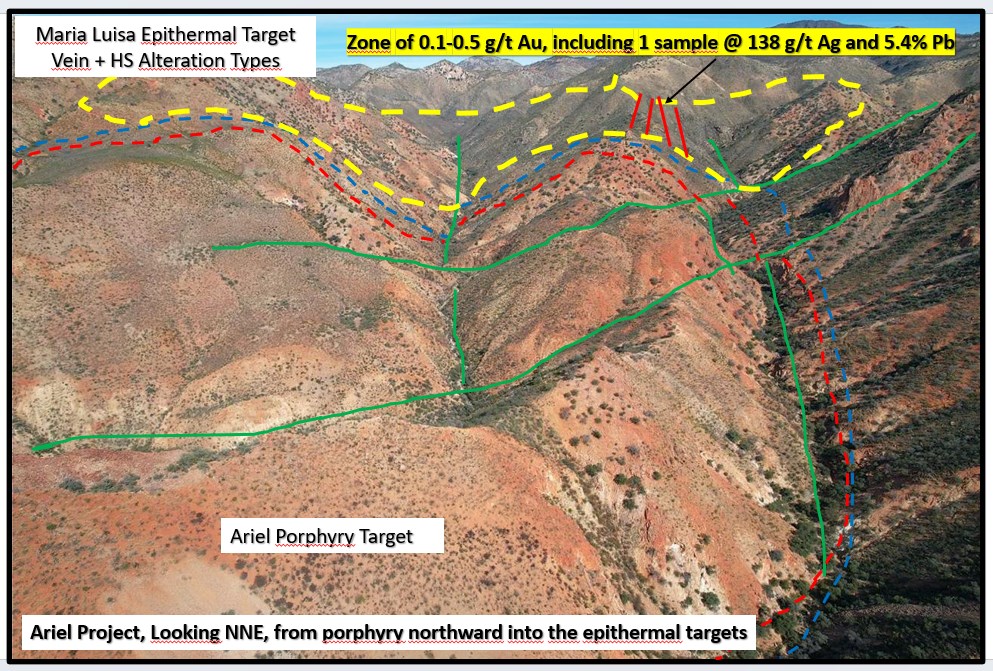

Building on Riverside’s consolidation of the Ariel Project through acquisition of the adjacent Maria Luisa concessions, the Company has now conducted expanded early 2026 field work and has received high grade silver and lead samples from veins, porphyry style alterations, and turquoise mines that are all part of the advancing target definition work with detailed mapping, sampling, alteration mineral studies summarized in the graphics below. These high grades are significant because they are comparable to those seen in other major Arizona-Sonora mining camps, where early mining of silver veins later evolved into major copper discoveries at more than a dozen large mines, including Cananea, La Caridad, Bisbee, Resolution, Morenci, and Ray, to name a few.

“Riverside early 2026 field program at the Ariel and Maria Luisa mineral concessions now consolidated into a single, fully permitted drill-ready project area found high grade precious and base metals typical of the major copper mines in the region and now the targets at Ariel continue to improve as the Company derisks the project with systematic fieldwork to sharpen targeting and prepare it for partnering and immediate drilling,” said John-Mark Staude, CEO of Riverside Resources. “The combination of geologic mapping, geochemistry, alteration mineral studies, and integrated geophysics is providing stronger vectors into the most prospective zones. Ariel remains a compelling, undrilled copper district target in a premier belt, with excellent access, safety and infrastructure. The recent geochemistry continues to enhance the porphyry Cu target potential at Ariel.”

Exploration Work and Targeting Progress

Riverside has full mineral title for the Ariel property and has advanced copper exploration through database compilations, field mapping, sampling, remote sensing, mineral concession consolidation and regional geophysical data interpretation, leading to the definition of two principal porphyry target areas (Ariel and Maria Luisa). The project has seen limited to no historical drilling to Riverside’s knowledge, and the Company considers Ariel a high-quality, drill-stage copper district target with extensive exposed targets and additional areas masked by shallow post-mineral cover. The Project is available for partnership per the Company’s business model of project generation; however, the Company could choose to drill the project given the quality exploration district.

Project Highlights

District-scale, consolidated footprint: Ariel totals 1,640 hectares (16 km²) across five fully titled concessions in good standing, including the Maria Luisa area, providing multiple priority target zones for drill testing.

Two priority target styles defined: Ongoing work continues to refine (1) a porphyry copper target with near surface copper sulphides and oxides, and (2) an epithermal arget interpreted as the upper portion of a porphyry system, consistent with alteration, veining and breccia styles with walk up safe, easy access on private ranch land.

Modern scientific exploration tools improving vectoring: Riverside is applying portable geochemical and mineralogical tools (including portable XRF and short-wave/infrared spectral mineral scanning) to distinguish vein and alteration assemblages and prioritize drill-ready areas.

Strategically located in the Sonora, Mexico Laramide copper belt and less than 20km from the La Caridad Cu-Mo porphyry mining complex, with additional regional porphyry prospects in the district.

Ariel is underlain by Late Cretaceous volcanic rocks of the Tarahumara Formation intruded by Paleocene (ca. 57 Ma) porphyritic intrusions comparable in age to regional porphyry mineralization events similar to many of the mines in the Arizona- Sonora Belt which includes over 10 significant copper operations.

2026 Sampling North Area – “Maria Luisa” Epithermal Target

New exploration geochemistry results from the early 2026 program for the Maria Luisa part of the Ariel Project have high grade Ag and Pb typical of lateral expressions of porphyry copper like those in Arizona at Resolution, Globe-Miami and Bingham in Utah. Here, silver values reach up to >10 oz/t Ag and Pb values reach up to 5.4%, along with gold anomalies of up to 0.4 g/t Au, as shown in the Table, Summary Map, and Cross Section figures in this news release. The sampling showed multiple sets of parallel veining consistent with what is common in major copper districts. Chip samples ranging from 0.5 to 1.5 m were taken by cutting the veins perpendicularly. Some select sample results include:

Sample Number

Assays

RRI-12911

0.42 g/t Au, 0.07%Pb

RRI-12912

1.36% Pb, 0.36 g/t Au,

RRI-12913

3.14% Pb, 0.14% Zn

RRI-12914

1.03% Pb

RRI-12918

138 g/t Ag, 5.39% Pb, 0.34 g/t Au

RRI-1412

225 g/t Ag

RRI-1419

320 g/t Ag

RRI-1425

161 g/t Ag

RRI-1545

200 g/t Ag, 0.657 g/t Au, 1% Pb

RRI-11122

0.5 g/t Au, 0.131% Pb

Table 1. Highlights of rock sampling in the northern zone of the Ariel project at Maria Luisa target with high silver and lead typical of the Arizona Sonora major copper operating districts by Riverside.

Figure 1. Drone photo looking NNE up the cross-section line from Ariel porphyry in the south toward the yellow loop and the Maria Luisa epithermal shown in blue loop in the north with epithermal Ag-Pb veins and overall distal parts of the drill ready porphyry target.

Figure 2: Map of the rock chip assays and sampling locations of recent results and other Riverside assay exploration data with expanded area showing some detail of the Maria Luisa high grade veins. Rock chip geochemical samples collected in 2026 (red) and similar results from previous sampling (yellow) part of epithermal target in the north and porphyry copper target of Ariel in the south.

Figure 3. Schematic section showing copper porphyry in red and epithermal in yellow cross hatch color to the north and over top with assays of >5% Pb and >130 gpt Ag typical for the high sulfidation veins potentially emanating from a related porphyry copper

Rock chip sampling at Ariel was taken generally of 1.5m chip channel and select pieces of rock materials from outcrops. Samples were then shipped for analysis by ACT Labs in Zacatecas, Mexico. Samples were analyzed for by gold fire assay, with pulps analyzed with Inductively Coupled Plasma-Mas Spectrometry (“ICP-MS”) following four-acid digestion to determine silver, base metals, and pathfinders. Samples were maintained in chain of custody being delivered to the laboratory in sealed bags. Standards and blanks were inserted every 20 samples and the laboratory also did duplicates every 20 samples as additional check on the quality control. The QA/QC was analyzed with a check for any variations in the standards beyond 2 standard deviations and the standards passed. Historic samples were analyzed using the same procedures with samples delivered to Bureau Veritas (Hermosillo, Sonora) for gold fire assay, with pulps forwarded to Vancouver, Canada for Inductively Coupled Plasma-Mas Spectrometry (“ICP-MS”) following four-acid digestion to determine silver, base metals, and pathfinders.

Qualified Person

The technical content of the news release has been reviewed and approved by Freeman Smith, P.Geo. (British Columbia), a qualified person under National Instrument 43-101 who is non-independent and the Vice President Exploration for the Company.

About Riverside Resources Inc.:

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has a strong balance sheet with over C$5,000,000 cash, no debt and tight share structure with a strong portfolio of gold-silver, copper, and REE assets and royalties in North America. Further information about Riverside is available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Investor Relations Riverside Resources Inc. Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

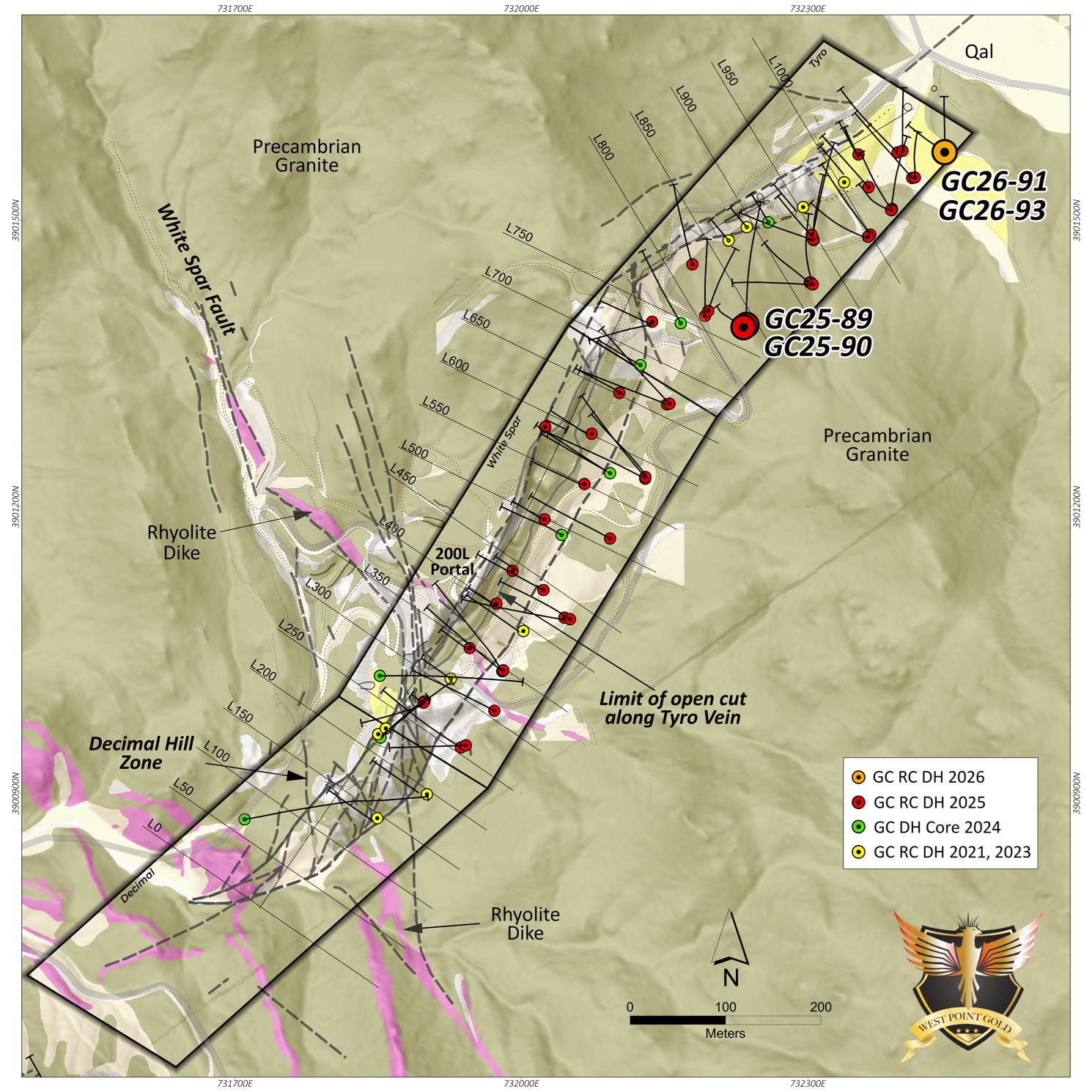

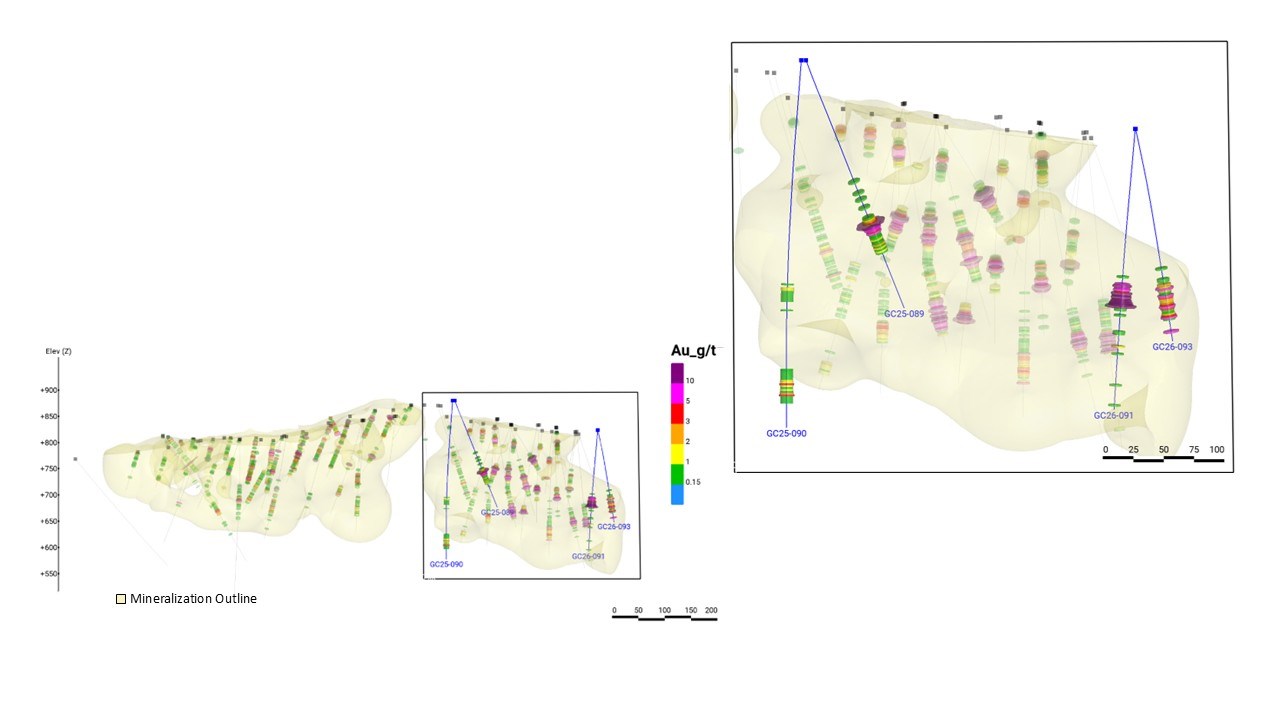

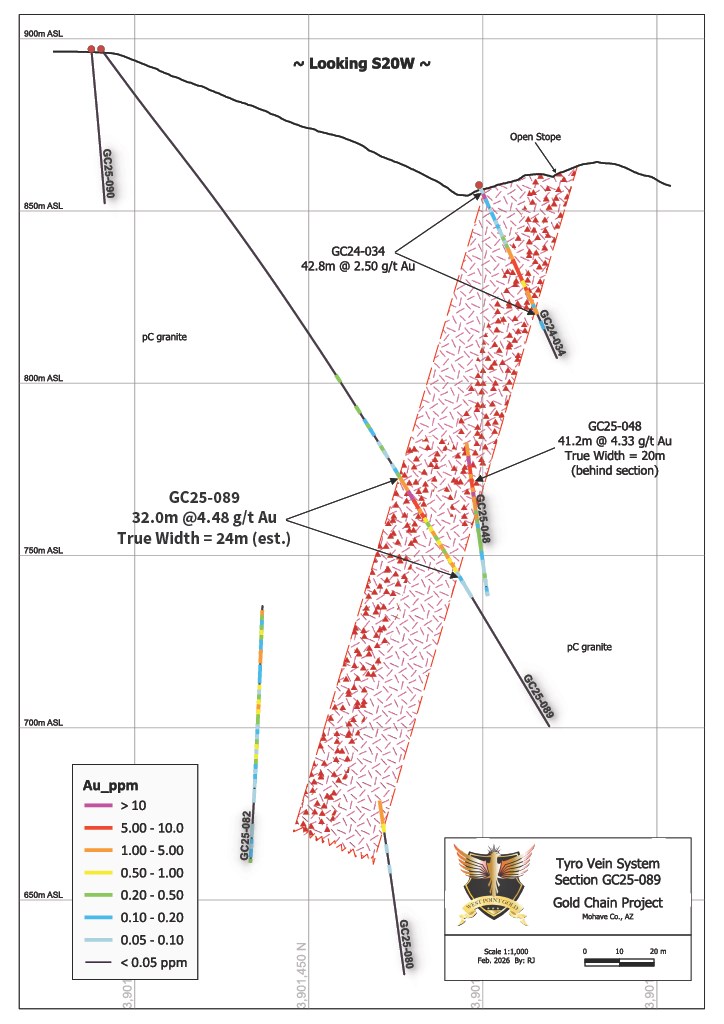

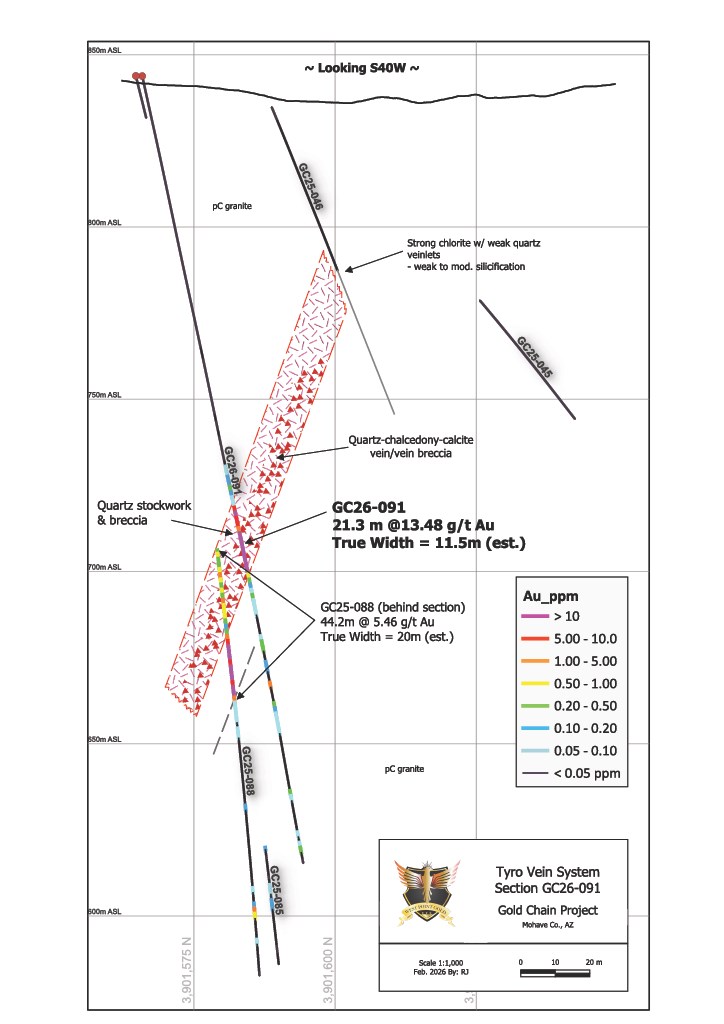

Vancouver, British Columbia–(Newsfile Corp. – February 25, 2026) – West Point Gold Corp. (TSXV: WPG) (OTCQB: WPGCF) (FSE: LRA0) (“West Point Gold” or the “Company”) is pleased to announce the results for four holes from the high-grade zone at Northeast (NE) Tyro, part of the ongoing 15,000 metre (m) drill program at its flagship Gold Chain Project in Arizona. The Company is reporting assay results for four drill holes (954m), GC25-89, GC25-90, GC26-91 and GC26-93.

Highlights:

These holes have extended the strike length of the high-grade zone at NE Tyro to more than 300m (Figure 2).

Hole GC26-91 returned 21.34m of 13.48 g/t Au from 128.0m to 149.4m, expanding the highest portion of the high-grade zone at NE Tyro to the northeast.

Hole GC25-89 returned 32.0m of 4.48 g/t Au from 152.4m to 184.4m, about 30m south of GC25-48 (41.2m at 4.33 g/t Au) and about 100m below surface vein exposures.

Hole GC26-93 returned 30.5m of 3.09 g/t Au from 132.6 to 163.1m, expanding the high-grade zone at NE Tyro along strike to the northeast.

Hole GC25-90 returned 25.9m of 1.23g/t Au from 256.0m to 281.9m and expands the mineralized zone at NE Tyro along strike to the southwest into an area previously considered to be weakly mineralized.

To date, 9,898m of the ongoing 15,000m drill program at the Gold Chain project have been completed, with assays released for 4,194m of drilling. Results are pending from the Tyro Main Zone, South Tyro, Red Hill Ledge, Black Dyke and Sheep Trail targets, representing 30 holes.

A third drill rig (core) will commence drilling at Gold Chain in early March, focused on increasing our understanding of the high-grade NE Tyro zone and extending the Tyro Main Zone to depth.

“The continuity and consistent high grades at NE Tyro, along with our ability to continue expanding the zone, are positive indicators for the scale potential of this zone. Drilling continues at Gold Chain, as we are well funded to deliver on our dual exploration goals for 2026, of delivering a maiden resource for the Tyro Main Zone and making a discovery at one of the multiple step-out targets we are testing,” stated Derek Macpherson, President and CEO.

Table 1: Drill Results

Holes

From (m)

To (m)

Width (m)

Grade (g/t Au)

GC25-89

152.4

184.4

32.0

4.48

GC25-90

256.0

281.9

25.9

1.23

GC26-91

128.0

149.4

21.3

13.48

GC26-93

132.6

163.1

30.5

3.09

Note: All widths shown are downhole; true widths are approximately 50-75% of downhole widths.

Figure 1: Plan view of the Main Tyro vein showing geology and drilling conducted in 2021, 2023, 2024, 2025, and 2026. Note the location of Hole Nos. GC25-89, GC25-90, GC26-91, and GC26-93.

Figure 2: Longitudinal perspective of the Tyro Main and NE Zones Showing Core and RC Drilling to Date. Holes GC25-89, GC25-90, GC26-91, and GC26-93 are highlighted and described below.

Summary Holes GC25-89, GC25-90, GC26-91, and GC26-93 continue to expand and provide improved definition of the high-grade gold mineralization in the NE Tyro zone at the Company’s Gold Chain project in Arizona. The four holes comprising this release represent 954.1m of the 9,898m drilled to date in the current 15,000m program.

The hole descriptions below briefly highlight the most recently completed holes across the NE Tyro vein, including the last two holes of the 2025 campaign and the first two holes of 2026. The high-grade Northeast Tyro zone is anchored by a higher-grade core. The entire zone remains open to depth and to the northeast along strike.

West Point Gold will commence core drilling of both the Northeast and Main Tyro zones in early March. With the anticipated receipt of the Plan of Operations (POO) in early March, drilling will continue to track the vein to the northeast toward the Frisco Graben and to depth. Results to date (Figure 2) reveal that high-grade gold mineralization extends below 200m (below surface) and over a strike length in excess of 300m. Receipt of the POO will permit drilling both core and RC holes outside the controlled patented claims, allowing deeper tests and further exploration to the northeast and toward the Frisco Graben target area.

Holes GC25-89 and GC25-90 Hole GC25-89 was designed to provide additional definition of the emerging high-grade zone at its southern end. The hole traversed the vein breccia/stockwork zone at 152.4m to 184.4m (32.0m) containing 4.48 g/t Au. This intersection is about 25m south of hole GC25-48, which contains 41.2m of 4.33 g/t Au, revealing good grade correlation between the two holes. Figure 3 suggests a true width of about 20m for the mineralized zone and a dip of about 74 degrees to the southeast. The intercept’s midpoint is about 100m below the surface.

Hole GC25-90 was designed to explore a portion of the vein system that hosts lower grades over broader intervals. GC25-60 encountered 33m (true width) of 1.29 g/t Au in a quartz-calcite stockwork zone, to connect the gold mineralization to the Main Tyro Zone (Figure 2). Hole GC25-90 (this PR) crossed the mineralized zone about 75m down-dip from GC25-60 and traversed 25.9m (apparent width) of 1.23 g/t Au (Figure 2). Additional drilling is warranted in this area but must be conducted at greater depths and collared outside of the patented claims.

Figure 3: Geologic section drawn along GC25-89 showing vein and spatial relation to GC25-48, GC24-34 and the surface.

Holes GC26-91 and GC26-93 Hole GC26-91 was drilled from the northeast corner of the Tyro patent and oriented perpendicular to the NE-trending Tyro structure. The goal was to traverse the high-grade zone at a higher elevation than hole GC25-88 (44.2m of 5.46 g/t Au) but beneath hole GC25-46, which encountered a broad zone of quartz-chlorite alteration with only minor quartz veinlets and negligible gold values. Hole GC26-91 traversed a distinct quartz-adularia vein and vein breccia from 128.0m to 149.4m (21.3m) containing 13.48 g/t Au with an estimated true width of 11.5m (Figure 4). Geologic interpretation, provided in Figure 4, indicates that the vein dips about 70 degrees. Hole GC25-88 crossed the vein about 30m down-dip.

Hole GC25-93 was drilled to the north from the same site as -91 to test the northeast extent of the high-grade zone. The hole encountered the vein at 132.6m to 163.1m (30.5m), which contained 3.09 g/t Au at about 120m below the surface. This intercept supports West Point Gold’s belief that the NE Tyro high-grade zone projects toward the Frisco Graben target area and plunges to depth beneath a broad alluvium-filled wash. This area will be the initial target for the deep drilling program to commence upon the receipt of the Plan of Operations.

Figure 4: Cross Sectional View of Hole GC26-91 between Holes GC25-46 and -88.

Qualified Person Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration, is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for overseeing all phases of the drilling program, including logging, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Drillholes have a diameter of about 10cm, and samples have an approximate weight of 5 to 10kg. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, and over-limit samples were determined by fire assay and gravimetric finish. Silver plus 15 other elements were determined by Aqua Regia ICP-AES (IM-2A16), and over-limit samples were determined by fire assay and gravimetric finish. Both certified standards and blanks were inserted on site along with duplicates, standards and blanks inserted by American Assay. The results summarized above have been carefully reviewed with reference to the QA/QC results. Standard sample chain of custody procedures were employed during drilling and sampling campaigns until delivery to the analytical facility.

About West Point Gold Corp. West Point Gold is an exploration and development company focused on unlocking value across four strategically located projects along the prolific Walker Lane Trend in Nevada and Arizona, USA, providing shareholders with exposure to multiple discovery opportunities across one of North America’s most productive gold regions. The Company’s near-term priority is advancing its flagship Gold Chain Project in Arizona.

For further information regarding this press release, please contact: Aaron Paterson, Corporate Communications Manager Phone: +1 (778) 358-6173 Email: info@westpointgold.com

FORWARD-LOOKING STATEMENTS: Certain statements contained in this press release constitute forward-looking information. These statements relate to future events or future performance. Forward-looking statements include estimates and statements that describe the Company’s future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. The use of any of the words “could”, “intend”, “expect”, “believe”, “will”, “projected”, “estimated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward-looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events including, among others, assumptions about future prices of gold, silver, and other metal prices, currency exchange rates and interest rates, timing of the Company’s maiden resource estimate, favourable operating conditions, political stability, obtaining government approvals and financing on time, obtaining renewals for existing licenses and permits and obtaining required licenses and permits, labour stability, stability in market conditions, availability of equipment, availability of drill rigs, and anticipated costs and expenditures. The Company cautions that all forward-looking statements are inherently uncertain, and that actual performance may be affected by a number of material factors, many of which are beyond the Company’s control. Such factors include, among other things: risks and uncertainties relating to West Point Gold’s ability to complete any payments or expenditures required under the Company’s various option agreements for its projects; and other risks and uncertainties relating to the actual results of current exploration activities, the uncertainties related to resources estimates; the uncertainty of estimates and projections in relation to production, costs and expenses; risks relating to grade and continuity of mineral deposits; the uncertainties involved in interpreting drill results and other exploration data; the potential for delays in exploration or development activities; uncertainty related to the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results may vary from those expected; statements about expected results of operations, royalties, cash flows, financial position may not be consistent with the Company’s expectations due to accidents, equipment breakdowns, title and permitting matters, labour disputes or other unanticipated difficulties with or interruptions in operations, fluctuating metal prices, unanticipated costs and expenses, uncertainties relating to the availability and costs of financing needed in the future and regulatory restrictions, including environmental regulatory restrictions. The possibility that future exploration, development or mining results will not be consistent with adjacent properties and the Company’s expectations; operational risks and hazards inherent with the business of mining (including environmental accidents and hazards, industrial accidents, equipment breakdown, unusual or unexpected geological or structural formations, cave-ins, flooding and severe weather); metal price fluctuations; environmental and regulatory requirements; availability of permits, failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; fluctuating gold prices; possibility of equipment breakdowns and delays, exploration cost overruns, availability of capital and financing, general economic, political risks, market or business conditions, regulatory changes, timeliness of government or regulatory approvals and other risks involved in the mineral exploration and development industry, and those risks set out in the filings on SEDAR+ made by the Company with securities regulators. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this corporate press release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, other than as required by applicable securities legislation.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

China

China Philippines

Philippines Poland

Poland Kazakhstan

Kazakhstan Türkiye

Türkiye Sri Lanka

Sri Lanka India

India Germany

Germany Brazil

Brazil Mongolia

Mongolia Azerbaijan

Azerbaijan Tajikistan

Tajikistan Japan

Japan Euro Area (average)

Euro Area (average) Thailand

Thailand Colombia

Colombia Hungary

Hungary Finland

Finland Singapore

Singapore Curaçao & St. Maarten

Curaçao & St. Maarten Iraq

Iraq Solomon Islands

Solomon Islands Qatar

Qatar Suriname

Suriname Czech Rep.

Czech Rep. Malta

Malta Russia

Russia Ethiopia

Ethiopia United Arab Emirates

United Arab Emirates Switzerland

Switzerland