|

|

![]()

From The Desk Of David Schectman

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This article makes the obvious point that a return to a gold standard is the only way nations can contain the interest cost of servicing debt, given the alternative is inflationist policies that can only lead to far higher interest rates and currency destruction. The topic is timely, given the self-harm of American economic and geopolitical policies, which are already leading America into a cyclical slump. Meanwhile, American fears of Asian domination of global economic, monetary and political outcomes have come true. The upcoming credit crisis is likely to kill off the welfare state model in the West by destroying their unbacked paper currencies, while China, Russia and their Asian allies have the means to prosper.

In my last Goldmoney article I explained why the monetary policies of inflationist economists and policy makers would end up destroying fiat currencies. The destruction will come from ordinary people, who are forced by law to use the state’s money for settling their day-to-day transactions. Ordinary people, each one a trinity of production, consumption and saving, will eventually wake up to the fraud of monetary inflation and discard their government’s medium of exchange as intrinsically worthless.

They always have, eventually. This has been proved by experience and should be uncontroversial. For the issuer of a currency, the risk of this happening heightens when credit markets become destabilised and confidence in the full faith and credit, which is the only backing a fiat currency has, begins to be questioned either by its users or foreigners or both. And when it does, a currency starts to rapidly lose purchasing power and the whole interest rate structure moves higher.

The state’s finances are then ruined, because by that time the state will have accumulated a lethal combination of existing unrepayable debt and escalating welfare liabilities. Today, most governments, including the US, are already ensnared in this debt trap, only the public has yet to realise the consequences and the planners are not about to tell them. The difficulty for nearly all governments is the deterioration in their finances will eventually wipe out their currencies unless a solution is found.

There is a solution that if taken allows the state to survive. It could be modelled on Steve Hanke’s (of John Hopkins University) preferred solution of a currency board, that when strictly observed removes the state’s ability to create money out of thin air. He recommends this solution to currency debasement and the evils that come with it for Venezuela and the like, linking a distressed emerging market currency to the dollar. But here we are considering stabilising the dollar itself and all the other currencies linked to it. The currency board in this case can only be linked to gold, which has always been the peoples’ money, free of issuer risk. In former times this was the basis of a gold exchange standard.

Professor Hanke’s currency board is a rule-based system designed to achieve the same thing. Once the system is in place, every currency unit subsequently put into public circulation by the monetary authority must be physically backed by a defined weight of gold bullion. This was the method of the gold exchange standard adopted by the Bank of England under the terms of the Bank Charter Act of 1844. A modern currency board, consisting of digitised currency, effectively works the same way.

A currency board system is not the best mechanism whereby currency is made exchangeable for gold. Its weakness is it relies on the state fulfilling its obligations, so it would be better to use gold directly, either in physical or digitised form. America reneged on its gold exchange standard in 1933/34, when it first banned gold ownership and then devalued the dollar. That was simply theft by the state from its citizens. Therefore, other safeguards for a gold exchange standard must be in place.

A return to a credible gold exchange standard will then put a cap on interest rates and therefore government borrowing costs. Instead of nominal rates of 10% going on 20% and beyond, a gold exchange standard will probably cap long-term government borrowing rates in a two to five per cent range. It also allows businesses with viable investment plans to progress as well. Not only is it an obvious solution, but it is similar to that adopted in the UK following the Napoleonic wars.

Britain had government debt levels in 1815 greater than that of all advanced nations today relative to the size of her economy, with the single exception of Japan. She introduced the gold sovereign coin in 1816, comprised of 0.2354 ounces of gold, as circulating money with a face value of one pound. Over the following nine decades, not only did she pay down her government debt from over 200% of GDP to about 30%, but her economy became the most advanced and wealthy in the world. This was achieved with sound money, whose purchasing power rose significantly over those nine decades, while the quality of life for everyone improved. A sovereign was still one pound, only it bought much more.

Ordinary people were encouraged to work, spend and save. They aspired to make their families better off. The vast majority succeeded, and for those few unfortunates who fell by the wayside, charitable institutions were set up by successful philanthropists to provide both housing and employment. It was never the function of the state to support them. It would be too much to claim that it was a perfect world, or indeed that everyone behaved as gentlefolk with the best of Victorian values, but the difference between the successful laissez-faire economy in Britain with its relatively minor faults compared with the bureaucratic socialism that succeeded it is stark.

The key is in the creation and preservation of personal wealth, contrasting with socialist redistribution and wealth destruction, which has steadily undermined formerly successful economies. The future is coalescing towards an inflationary collapse for all Western governments, the manner of which is described in more detail in the following section. For prescient politicians, it creates the opportunity to reverse out of socialism, because the silent majority, which just wants commercial stability in preference to state handouts, if properly led will support a move away from destructive socialism. It is not a simple task, because all advice that a politician receives today is predicated on the creed of inflationism and socialist imperatives.

Monetarists are fully aware that if a government increases the quantity of money in circulation, its purchasing power declines. Their theory is based on the days when gold was money and describes the effect of imports and exports of monetary gold on the general price level.

Pure monetarists appear to assume the same is basically true of fiat currencies, unbacked by gold. But there is a fundamental difference. When gold is used as money for settling cross-border trade, an arbitrage takes place, correcting price differentials. When prices are generally low in one country, that country would achieve sales of commodities and goods in other countries where prices were higher. Gold then flows to the lower price centre, raising its prices towards those of other countries. With unbacked national currencies, this does not happen.

Instead, national currencies earned through cross-border trade are usually sold in the foreign exchanges, and the determinant of trade flows is no longer an arbitrage based on a common form of money. The pure link between money and trade has gone, and whether foreigners retain or sell currency earned by exports depends mostly on their confidence in it. That is a matter for speculation, not trade.

Domestic users of state-issued currency are divorced from these issues, because foreign currencies do not circulate domestically as a medium of exchange. Instead of being a form of money accepted beyond national boundaries, as gold was formerly, there is no value anchor for domestic use. For this reason, a national currency’s purchasing power becomes a matter of trust, and it is that trust that risks being undermined in a credit crisis. The less trustworthy a government, the more rapidly a currency is in risk of decline.

This is why monetarism, which was based on gold as ubiquitous money, is no longer the sole determinant of currency values. It is true that an increase in the quantity of circulating money devalues the existing stock, but if the population as a whole is prepared to increase its preference for money, usually expressed as a savings ratio, there need be no detrimental effect on its purchasing power.

With fiat currencies we enter a world where statistics reflect the quantity of money, and never the confidence people have in it. Additionally, we should observe that statistics can tell you everything and nothing, but never the truth. It is possible for an economy to collapse, but statistically appear healthy as the following example illustrates.

Imagine, for a moment, that modern statisticians and their methods existed at the time of the Weimar Republic. Government finances were covered by approximately ten per cent taxes and ninety per cent monetary inflation. It was a government whose finances were run on the lines recommended by today’s modern monetary theorists.[i]

There can be no doubt the low level of taxation was an encouragement to business and permitted the redeployment of earnings for investment. A falling exchange rate delivers excess profits for export businesses as well. Interest rates were attractive relative to the rate of price inflation, and the economy, statistically anyway, was expanding rapidly.

This was certainly true measured in nominal GDP, the basic measure of economic activity today. Official prices, which are always the latest gathered and indexed, lag monetary debasement by at least a month, possibly two or even three. To this we must also mention governments always under-record price inflation, which is the natural consequence of earlier debasement. Therefore, even after an official price deflator is applied to nominal GDP, “real” GDP growth in Germany between 1918 and early-1923 would be judged by today’s government economists to be booming.

Interestingly, Joseph Stiglitz and a raft of left-leaning economists and politicians believed Hugo Chavez’s socialist policies were successful in 2007, when statistics revealed a similar interpretation for Venezuela’s inflation-ridden economy. However, instead of Germany being deemed to be in an economic boom, in 1920 economists in the classical and Austrian traditions saw it for what it was. Even Keynes wrote about it in his Tract on Monetary Reform, published coincidentally in late-1923 when the papiermark finally collapsed.

Germany’s inflation may have been a statistical success, but it concealed crippling wealth destruction through the transfer of wealth and wages from private individuals to the state through monetary debasement. As Lenin is reputed to have said, “The way to crush the bourgeoisie is to grind them down between the millstones of taxation and inflation.”

In Germany, inflationary financing started before the First World War to finance a build-up of armaments. At the outbreak of war, gold convertibility was suspended, and the unbacked papiermarkbegan its inflationary drift. Exploiting the facility to issue valueless pieces of paper as currency and for the people to circulate them as legal tender became the principal source of government funds.

This trick worked until approximately May 1923. By then, the purchasing power of the mark had fallen consistently at a relatively even pace. It then took only seven months to lose all its purchasing power, when the public collectively realised what was happening, and manically dumped their marks for anything. It was the katastrophenhausse, or crack-up boom, the end of life for a state’s unbacked currency.

It was the pattern firmly established in all fiat currency collapses, which, besides the currencies in existence today, has happened to all of them throughout the history of post-barter trade, without any known exception. It is the familiar route along which the dollar and other paper currencies are travelling today. Now that we are entering a statistical slowdown in most major economies, Weimar-style financing is set to return to centre-stage. The fate for unbacked state currencies, unless somehow averted, will be the same.

The lesson from Weimar and today’s monetary inflation is that the period before the public cottons on to it can be prolonged. In Germany it was 1914-1923, followed by a swift seven-month collapse. Today it is from 1971 and still counting. But the final collapse could be as rapid as Germany’s between May and November 1923.

Doubtless, we will see rising price inflation later this year, but that statistic will continue to be suppressed. With the gap between the effect of accelerating monetary inflation and the official rate of price inflation widening, we could see for a brief period the statistical recovery in GDP that so badly misled Professor Stiglitz and others observing Venezuela’s economy twelve years ago.

A major problem for governments when price inflation begins to rise is the notional cost of borrowing, because markets alive to the decline in the currency’s purchasing power will drive interest rates higher, despite official attempts to suppress them. So far, the problem has been successfully covered up by central banks rigging government debt markets, and by government statisticians masking the true rate of price inflation through statistical trickery. In future, efforts to keep a lid on reality will presumably intensify as a core feature of monetary and economic policy. In light of another wave of monetary debasement, the question then arises whether markets will permit this market rigging to continue. If not, the purchasing power of unbacked currencies will be visibly undermined by the erosion of public confidence in them.

We cannot know this outcome for sure until it is well on the way. The Lehman credit crisis led to a global explosion in the quantity of money as central banks worked in tandem to rescue the banks and the entire financial world. That injection still circulates in the global blood-stream. A second globally-coordinated monetary debasement is just starting, notably with China leading the way. A realistic assumption must be that this time the purchasing power of state currencies will be the victim of a severe monetary overdose.

This being the case, there is bound to be an upward adjustment in nominal interest rates forced on central banks by the markets. Government financing becomes overtly inflationary, embarking on a modern equivalent of the papiermark route. How else do you describe accelerated quantitative easing?

A loss of confidence in currencies is always reflected in the prices of gold and silver, which by then should be heading considerably higher. Crypto-currencies could compound the problem by becoming an alternative for people no longer content to retain bank deposits.

Governments and their central banks will be at a fork in the road. One direction towards monetary stability is rough, tough, suspension-breaking, but leads to a better place. The other towards accelerating monetary debasement is smoother, more familiar, but just out of sight leads to a cliff-edge of monetary destruction.

Which road will your government take?

Western governments are poorly equipped to make this decision. There are a few people in the political establishment who might understand the choice, but they will have to deliberately put the clock back, and reverse government policy away from socialism and state regulation towards free markets and sound money. They will be fighting the neo-Keynesian economic establishment, the inflationists who form the overwhelming majority of experts and advisers. These neo-Keynesians populate the central banks and government treasury departments almost to the exclusion of all other economic theorists. Spending ministers and secretaries of state will have to be told to reduce their power-bases, which goes against their personal ambitions and political instincts.

It will take an extraordinary feat of leadership to succeed.

In favour of a brave statesman will be the free-market instincts of the silent majority. It is only at times of crisis that a statesman can muster this support. In a different context, Churchill in 1940 comes to mind. The public will not know the solution, but with the right leadership they can be led along the path to economic and monetary salvation. The currency will have to be stabilised by making it convertible into gold bullion, and government spending will have to be slashed, by as much as a quarter or a third in most advanced economies. This means enacting legislation cancelling government responsibilities, something that could require a state of emergency. The message to the electorate must be the government owes you nothing. And so that you can look after yourself, the government must encourage individuals to accumulate personal wealth by removing taxation from savings.

Obviously, the most socialist welfare states will face the greatest challenge. There will be extreme tension between financial reality and entrenched interests. There can be no doubt that their currencies are most likely to fail.

The Eurozone poses a particular challenge, with one currency circulating between nineteen member states. Conventional opinion is that all the troubles visited on the PIGS (Portugal, Italy, Greece and Spain) are due to an inflexible currency. Here, there is likely to be a split, with Germany and perhaps a northern faction gravitating towards the protection of a gold standard, while the PIGS will press for more interest rate suppression and infinite supplies of easy money from the ECB.

The US has a different but more worrying problem. It refuses to accept its decline as the dominant super-power, retreating into trade protection and autarky. Consequently, the US Government is taking destructive decisions. Since President Trump was elected, he accelerated inflationary financing late in the credit cycle in the belief it would lead to greater tax income in due course. He has also replayed the Smoot-Hawley Tariff Act of 1930, in the belief that trade protectionism somehow makes America great again (MAGA). Instead, it has crashed global trade, just as it did in the 1930s. MAGA is a fateful combination of tax cuts and trade protectionism. It is a curious form of self-harm, which backfires badly on American consumers and corporations. And it does not help foster good relations with America’s creditors, who have allowed America to live beyond her means for decades.

Foreigners now own dollars in enormous amounts, for which interpret they are America’s reluctant bankers. They are now beginning to be net sellers as a consequence of a dollar glut in their hands, combined with America’s clumsy geopolitical manoeuvrings. TIC data for December showed foreigners sold a net $91.4bn[ii] – the largest monthly outflow during Trump’s presidency, and this only a few months after everyone believed foreigners were buying yet more dollars to service their own debts.

While ignoring its dependency on foreign finance, America is trying to strangle China’s economic and technical development, but that horse has already bolted. Washington surely knows the jig is up, and that the US, Japan and Britain are merely islands on the periphery of a vitalised Eurasian powerhouse. We were all warned this would happen in one form or another by Halford Mackinder over a hundred years ago.[iii] America, it appears, is prepared to destroy herself rather than see Mackinder’s prophecy come true.

Consequently, the whole world is being thrown into a trade-induced slump, and the American government is central to the problem. We can expect its economy, along with all the others, to decline significantly in the coming months. It will be an encouragement for yet more inflationism. The monetary expansion which is sure to follow is set to lead to an acceleration in the decline in the dollar’s purchasing power, as foreigners turn from dollar bankers to dollar sellers. This will lead to an increase in the value of time-preference set by markets, and unless the Fed counters this increase sufficiently by raising its rates, the dollar will simply slide.

Under current circumstances, the 1980-81 Volcker solution of raising interest rates to 20% to stabilise the currency does not appear to be available. Furthermore, to reverse the Nixon shock of 1971 and reinstate gold backing for the dollar as a means of limiting the rise in interest rates is simply not in the establishment’s DNA. America, which is very much the guilty party in destroying its own Bretton Woods monetary arrangements, will find it very difficult to change its tack with such economic cluelessness at the top.

Things are very different in Asia. The eight members of the Shanghai Cooperation Organisation, together with those seeking to join, represent roughly half the world’s population. It is led by gold-friendly China and Russia. A further two billion people can be said to be directly affected by the way the SCO develops, including the populous nations of South-East Asia, the Middle East, and Sub-Saharan Africa. That leaves America’s questionable sphere of influence reduced to roughly one and a half billion souls out of a global population of seven. It is proof of Halford Mackinder’s foresight.

China and Russia still have significant infrastructure plans, which will stimulate Eurasian economic activity for at least the next decade, perhaps two. If the formerly advanced national economies slump, of course Asia will be adversely affected, but not as much as even China-watchers fear. The upcoming credit crisis is likely to mainly affect America, UK, Western Europe and their military and economic allies. The SCO bloc could escape relatively lightly, if it takes the right avoiding action.

The threat to the SCO’s future is mainly from its current monetary policies, with China in particular using credit expansion to manage the economy. She has sought to control the consequences of domestic monetary policy through strict exchange controls, a strategy which has so far broadly succeeded.

The growing possibility of a dollar collapse will call for a radical change in China’s monetary policy. We know the direction this new policy will take from the actions of Russia, China and increasingly those of other SCO members, and that is to somehow incorporate gold into their paper monies. Furthermore, they are capable of doing it and making it stick.

While it is clear to us that China and Russia understand the importance of gold as true money, it is not clear whether they have a credible plan for its introduction into their monetary systems. The Russians seem to have a good grasp of the issues. China had a good grasp, but many of her economic advisors are now Western-trained in neo-Keynesian inflationary beliefs. Therefore, China is not wholly immune to the faults that are likely to destroy the dollar and other Western currencies. But the central message in China’s successful cornering of the physical gold market is a switch will be made to sound money when it is strategically sensible, despite the neo-Keynesians in it ranks.

Almost none of the SCO nations have significant welfare commitments to their populations. It is therefore possible for them to contain government spending in an economic downturn. Not only can Russia and China introduce a gold exchange standard and make it stick, but fellow SCO members and those nations tied to it can either introduce their own gold exchange standards, or alternatively use gold-backed roubles and yuan to anchor their currencies.

The economic and monetary direction taken by the SCO in the coming years could turn out to be relatively successful, at least compared with the difficulties faced by the welfare states. Such an outcome would be immensely positive for humanity as a whole and be a lifeline for those of us deluded into inflation-funded socialism. You never know, it might even force spendthrift Western governments to reform their ways and return to sound money policies.

The effect on the price of gold should be obvious. It is said that foreign students in Berlin in 1923 were able to buy houses with the spare change from their allowances, sent to them by their parents, usually in dollars or pounds. Dollars at that time were as good as gold. Today, a currency board or gold exchange standard would have to be fixed at a rate significantly higher than current fiat-currency prices. Gold is the ultimate protection from theft by currency debasement.

How quickly things can change. In the four weeks following the December FOMC rate hike, the Fed executed one of its sharpest policy U-turns in memory. Indeed, the Fed’s tonal shift has been so profound, it is difficult to square recent comments from Fed Governors and Regional Bank Presidents with their stated positions just a few weeks prior. What could possibly account for such a dramatic about-face from such a characteristically deliberative body? Is the explanation as simple as the 19.6% decline in the S&P 500 Index (S&P 500)1 between Chairman Powell’s “long way from neutral” comment on 10/3/18 and Secretary Mnuchin’s convening of the President’s Working Group on Financial Markets on Christmas Eve?

In our experience, the contemporary Fed is always hyper vigilant about signs of financial stress with perceived potential to evolve into debt deflation. To us, S&P 500 air pockets are but a symptom of a far more troublesome underlying condition: insufficient credit creation to sustain inflated paper claims. Once equities complete their current Pavlovian bounce, consensus will need to confront the more sobering implications of the Fed’s policy reversal. The Fed is far too tight and has already tripped the switch on long overdue debt rationalization.

Of course, this is precisely the juncture for which we have long prepared.

Similar to early 2016, when global financial markets were destabilized by the Fed’s initial 12/16/15 rate hike, the gold price responded quickly to market fallout from Chairman Powell’s early October overreach, and has remained in steady uptrend ever since. Importantly, gold’s advance has not been derailed by the S&P 500’s 18.1% bounce from Christmas Eve through 2/15/19. To us, gold’s performance clearly signals Fed policy error, and we believe spot gold is coiling for spirited advance as global central banks pivot back toward easing. For gold investors, this is the mix of real-deal fundamentals on which spectacular gains are based.

Given the seminal nature of catalysts now in play for precious metals, we felt the timing appropriate for a comprehensive review of factors driving the gold price. In this report, we have compiled our Top 10 List of fundamentals supporting a portfolio allocation to gold in 2019. Because our gold investment thesis rests on epic global imbalances, our first few sections review underpinnings of our long-term gold thesis.

We often marvel at investor apathy towards gold’s investment merits. Especially in institutional circles, gold is generally viewed as an archaic asset offering negligible portfolio utility. To us, it is remarkable that gold could remain such an institutional outcast after posting the single best performance of any global asset for eighteen years running. Since 2000, not only has bullion outperformed traditional investment assets in cumulative total return, but gold’s ongoing bull market has also proved to be highly consistent in its annual progression. As shown in the rightmost column of Figure 1, the average of gold’s annual performance in nine prominent currencies has been positive in 16 of the past 18 years.

Figure 1: Annual Performance of Spot Gold in Prominent Global Currencies (2001-2018)

Source: Bloomberg.

Given gold’s fringe standing in much of the investment world, it is interesting to note that gold bullion’s cumulative performance since 2000 has trounced the S&P 500. As shown in Figure 2, gold’s cumulative gain from 12/31/00 through 2/15/19 totaled 385.42%, versus a 110.23% advance in the S&P 500 price level, and a 201.15% gain in S&P 500 total return.

Figure 2: Spot Gold2 vs. S&P 5001 (Price and Total Return Indices) (12/29/00-2/15/19)

Source: Bloomberg.

(Note to Reader: Items 2-9 have been condensed. The full 28-page Gold Report can be found here.)

Synopsis: Greenspan, Bernanke and Yellen Feds have facilitated trillions of dollars of credit creation atop a fairly consistent GDP denominator. Why is debt-to-GDP analysis important and what does it have to do with gold’s portfolio merits? While timing is uncertain, it is inevitable that the U.S. financial system will eventually rebalance to the degree that GDP can productively support total debt levels. There are only two possible routes for the U.S. debt burden to be recalibrated to underlying GDP: default or debasement. Because gold can neither default nor be debased, it is an ideal portfolio component until such time as the U.S. financial system rebalances.

Synopsis: Since the Fed’s about-face on rates, the biggest riddle in financial markets is what could possibly have served as the underlying trigger. Was it the S&P 500 swoon, pressure from President Trump or some signal of financial stress not yet publically disseminated? We suspect it was a combination of all three. Whatever the true mix of catalysts, the message has been received, not only by the Fed, but by all global central banks, which have discarded in unison their collective resolve for policy tightening.

Synopsis: In unison, global central banks are swinging quickly and hard back towards an easing posture. The world is quickly refocusing on the likelihood and utility of negative interest rates. The global total of negative yielding sovereign bonds has exploded 56% from $5.733 trillion on 10/3/18 to $8.944 trillion on 2/15/19. Already within $1 trillion of its September 2017 high, how large will the ultimate supply of negative-yielding sovereigns become in the unfolding cycle? While just one of many factors influencing the gold price, correlations confirm that gold is taking notice of the global pivot to negative rates.

Synopsis: While we recognize U.S. Fed power borders on the divine, we have always found the proposition that 19 individuals, no matter how capable and well-supported, might possibly price the world’s reserve currency more efficiently than free markets to be a fairly absurd notion. Sidestepping our perceptions of Fed Governors and Regional Bank Presidents, both individually and as a deliberative body, we have detected since early 2018 distinct erosion in the Fed’s factual credibility.

Synopsis: One of the least kept secrets in global financial markets is the deteriorating fiscal position of the United States. Everyone knows the Trump Administration’s Office of Management and Budget (OMB) now forecasts $1 trillion-plus budget deficits in fiscal 2019, 2020 and 2021. Everyone knows OMB assumptions for GDP growth in those years are likely a bit optimistic (3.2%, 3.1% and 3.0%). And everyone knows post-tax-cut federal receipts are already lagging advertised projections.

Synopsis: Central bank demand for gold soared to a multi-decade high in 2018, rising 74% YOY – the highest level of CB net purchases since the dissolution of Bretton Woods (1968-1973). There is no question that President Trump’s penchant for sanctions has energized longstanding rancor towards the dollar-standard system. As recently as 2000, 72.7% of global foreign-exchange (FX) reserves were denominated in U.S. dollars. By year-end 2018, the U.S. dollar had shrunk to 61.9%. We believe that the declining use of dollar-denominated assets by global central banks has less to do with direct supply/demand impacts in currency markets than with the symbolic impact on the U.S. dollar’s hegemonic status.

Synopsis: Since 2016, the twin shocks of Brexit and the Trump Presidency have bookended near continuous political turmoil in global markets. Investors have become inured to the daily twists and turns of President Trump’s seemingly erratic decision-making and Prime Minister May’s Sisyphean negotiations with both the EU and her own Parliament. Indeed, investors’ increasingly thick skin to political headline risk may be leading to underestimation of potential black swans forming on the horizon.

Synopsis: Important components of our 2019 gold investment thesis are the lingering imbalances from eight years of QE (quantitative easing) and ZIRP (zero-interest-rate-policy). Artificially depressed interest rates always distort time preferences and foster malinvestment. In the instance of the post-GFC (Great Financial Crisis) Fed, these imbalances have become epic in size and scope. At Sprott, we adhere to the theory that volatility generally signals change. We believe isolated outbreaks of volatility during 2018 served as early signposts of profound change in financial markets (the unwinding of eight years of volatility-suppressing QE and ZIRP). What is being vastly underestimated by investor consensus is the stored force of volatility suppression during these past eight years.

In documenting an objective record of gold’s portfolio utility, one logically begins with gold’s traditional profile as safe-harbor asset. It goes without saying that gold’s safe-haven reputation accrues from bullion’s established history of relative outperformance during periods of financial stress. As shown in Figure 18, gold has done a masterful job of insulating portfolio capital from sharp declines in U.S. equities during the past three decades of financial crises.

Figure 18: S&P 500 Index versus Spot Gold During “Crisis” Periods (1987-Present)

Source: World Gold Council. Dates used: Black Monday: 9/1987-11/1987; LTCM: 8/1998; Dot-Com: 3/2000-3/2001; September 11: 9/2001; 2002 Recession: 3/2002-7/2002; Great Recession: 10/2007-2/2009; Sovereign Debt Crisis I: 1/2010-6/2010; Sovereign Debt Crisis II: 2/2011-10/2011; Greek Default: 6/2015-9/2015.

Institutional focus on non-correlating assets has directed trillions-of-dollars of investment capital towards hedge funds and specialized investment partnerships in disciplines such as real estate, private equity and venture capital. A more recent trend, however, has been mounting investor backlash against elevated fees charged by alternative managers in the context of mediocre investment returns (not to mention onerous liquidity and lockup provisions). In short, a marquee consideration for today’s pension and endowment stewards has become whether the fees, lockups and obfuscation of alternative investments are truly worth their while.

Even more challenging to the industry status quo, gold bullion has rivaled the performance of alternative asset indices while simultaneously displaying far lower correlation to these vehicles than either stocks or bonds. As shown in Figure 23, the correlation between prominent alternative asset indices and the S&P 500 Index has averaged 80% over the decade through 2018. By way of comparison, the 10-year correlation between these same indices and spot gold has averaged just 9%. At an 80% correlation-rate with U.S. equities, high-priced and unwieldy alternative vehicles seem hardly worth their freight.

Figure 23: Correlations between Alternative Asset Indices and S&P 500 Index, U.S. Treasuries and Spot Gold (Monthly Data Trailing 10-years through 2018)

Source: World Gold Council.

We thank you for your diligence in reviewing our fundamentals supporting a portfolio allocation to gold in 2019. We expect gold’s 2019 performance to more than justify the effort.

Download Report PDF – Short Version (7 pages)

Download Report PDF – Long Version (28 pages)

Trey Reik

Senior Portfolio Manager

Sprott Asset Management USA, Inc

203.656.2400

| 1 | S&P 500® Index represents 505 stocks issued by 500 large companies with market capitalizations of at least $6.1 billion. This Index is viewed as a leading indicator of U.S. equities and a reflection of the performance of the large-cap universe. The SPX Index represents price only, and SPXT Index represents total return with dividends reinvested. |

| 2 | Spot gold is measured by the Bloomberg GOLDS Comdty sub-index. |

The information contained herein does not constitute an offer or solicitation to anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada or the United States should contact their financial advisor to determine whether securities of the Funds may be lawfully sold in their jurisdiction.

The information provided is general in nature and is provided with the understanding that it may not be relied upon as, nor considered to be, the rendering or tax, legal, accounting or professional advice. Readers should consult with their own accountants and/or lawyers for advice on the specific circumstances before taking any action.

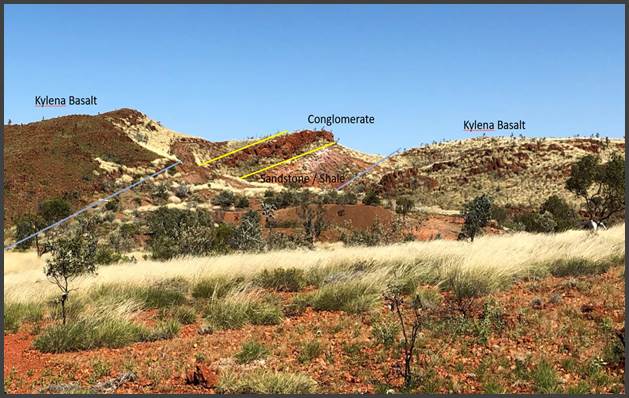

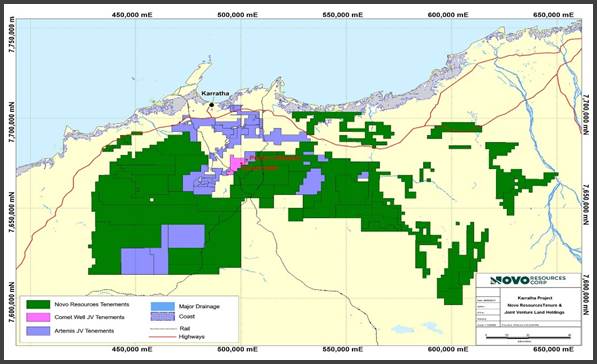

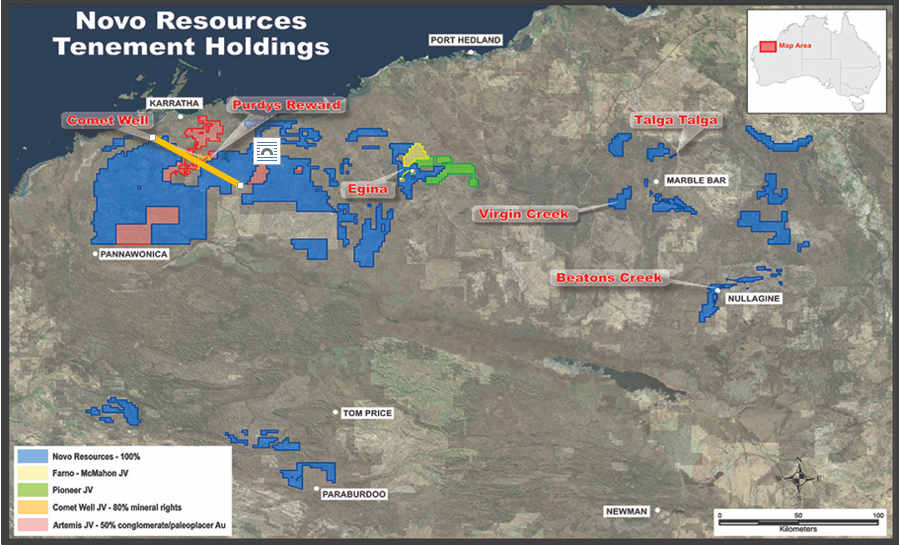

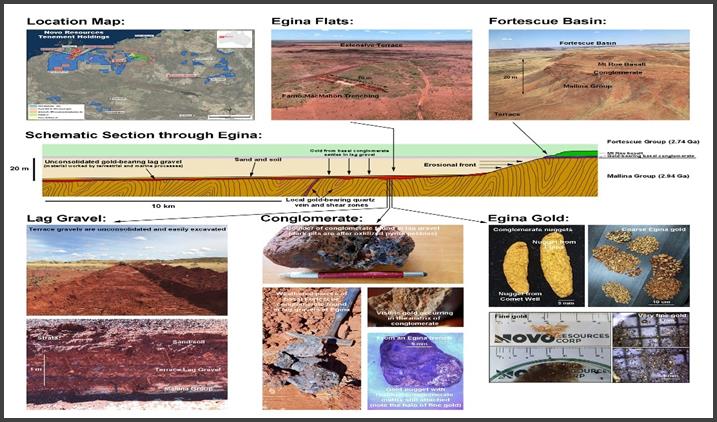

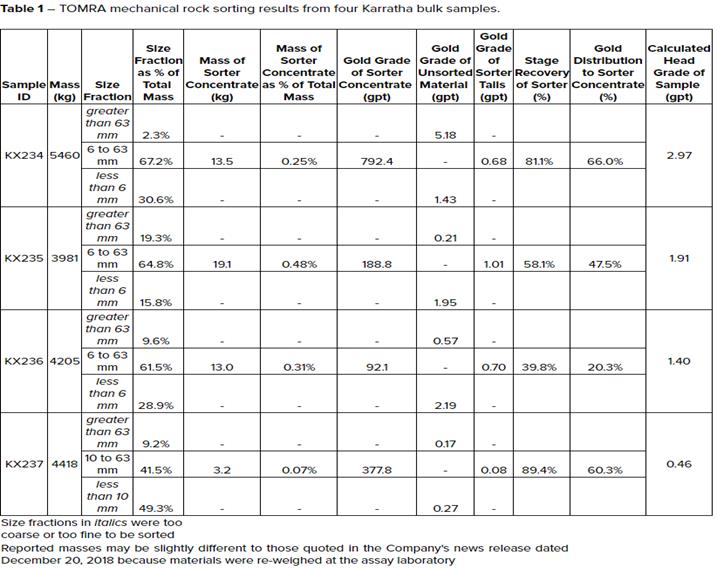

Dr. Quinton Hennigh the President and Director of Novo Resources (TSX: NVO | OTCQX: NSRPF) sits down with Maurice Jackson of Proven and Probable to discuss the companies road to production. Current and prospective shareholders will be introduced to the thesis and unique value proposition that Novo Resources provides to the market. We shall address a number of fronts from expanding the project portfolio from 7,000 sq km to 12,000 sq km, bulk sample results, mechanical rock sorting with TOMRA, and DTC Eligibility for U.S. investors just to name a few. Dr. Hennigh shall provide a thorough comprehensive update on each project in the Novo portfolio.

Source: Maurice Jackson for Streetwise Reports (2/23/19): https://www.streetwisereports.com/article/2019/02/23/companys-quest-to-become-an-established-gold-producer-in-australia.html

Dr. Quinton Hennigh, chairman and president of Novo Resources, sits down with Maurice Jackson of Proven and Probable to discuss how the road to production looks.

Dr. Quinton Hennigh, chairman and president of Novo Resources, sits down with Maurice Jackson of Proven and Probable to discuss how the road to production looks.

Since that time, we have focused efforts more to the northwest and acquired this vast land package by Karratha. This was based on a discovery roughly two-and-a-half years ago of gold being found by prospectors in areas like Comet Well and Purdy’s Reward, as well as others around the marsh and the basin, including Egina and some other select locals.

Since that time, we have focused efforts more to the northwest and acquired this vast land package by Karratha. This was based on a discovery roughly two-and-a-half years ago of gold being found by prospectors in areas like Comet Well and Purdy’s Reward, as well as others around the marsh and the basin, including Egina and some other select locals.

1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Novo Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Novo Resources is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click herefor important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Images provided by the author.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VANCOUVER, British Columbia, Feb. 21, 2019 (GLOBE NEWSWIRE) — Group Ten Metals Inc. (TSX.V: PGE; US OTC: PGEZF; FSE: 5D32) (the “Company” or “Group Ten”) announces results from the Chrome Mountain and East Boulder target areas on the west side of the Stillwater West Project in Montana, USA. This is the second in a series of planned news releases to report results of 2018 exploration programs, on-going historical data compilation, and modeling work at the Company’s flagship PGE-Ni-Cu project adjacent to Sibanye-Stillwater’s high-grade PGE mines in the Stillwater Igneous Complex. With more than 41 million ounces of past production and current M&I resources, plus another 49 million ounces of inferred resources at over 16 g/t palladium and platinum, the Stillwater Complex is recognized as one of the top regions in the world for PGE-Ni-Cu mineralization1,2.

Michael Rowley, President and CEO, commented, “We are pleased to report results of our work to date in the Chrome Mountain and East Boulder target areas at the middle-west portion of the 25-km-long Stillwater West project (see Figure 1). Mineralization including platinum group elements (PGE), nickel, copper and cobalt at these target areas is associated with two major electro-magnetic geophysical conductors that are approximately 2.9 and 2.6 km in length respectively, and correspond with broad coincident soil and rock geochemical anomalies. The scale of these targets demonstrates the potential for discovery of a major new bulk-tonnage “Platreef-style” PGE-Ni-Cu deposit in the Stillwater Complex, geologically similar to those in the Bushveld Complex of South Africa.”

“Chrome Mountain, in particular, is one of our highest priority target areas and has advanced very rapidly with the discovery of a new style of platinum and palladium mineralization associated with nickel and copper sulphides at the Hybrid Zone (see December 17, 2018 news release). This discovery has attracted significant interest in the Stillwater West project with wide intervals of platinum, palladium, nickel, copper, and cobalt mineralization starting at surface, including nine intervals of over 100 meters in thickness with grade-thickness values of more than 100 gram-meter Total Platinum Equivalent (TotPtEq), including six holes which returned composite mineralization of over 200 meters with grade-thickness values of 200 to 294 gram-meter TotPtEq (see Table 1). Grade-thickness values of 25 gram-meter or more are considered economically significant, with the grade-thickness values at the adjacent J-M Reef mines averaging approximately 34 gram-meter palladium and platinum1. Values of 100 to 300 gram-meter are exceptional, highlighting the strength of the Stillwater West system.”

“Rock sampling programs at Chrome Mountain in 2018 returned up to 16 g/t 3E (8.72 g/t Pt, 7.25 g/t Pd and 0.03 g/t Au) (see Table 2) in previously unrecognized areas, confirming the underexplored nature of the lower Stillwater Complex, and the substantial potential for new discoveries of both higher-grade and bulk tonnage deposits in this famously metal-rich district.”

Chrome Mountain – Overview

As shown in Figure 1, the Chrome Mountain target area is one of eight major bulk tonnage target areas identified by Group Ten Metals across the Ultramafic and Basal Series of the Stillwater Complex. These target areas are highlighted by strong, multi-kilometer electro-magnetic conductive signatures that are characteristic of large bodies of interconnected to strongly disseminated sulphides. These conductive geophysical targets have overlapping highly elevated platinum, palladium, gold, nickel, copper, and chromium values in soils and rock sampling. The limited drilling completed to date on these large geophysical and geochemical targets confirms the presence of corresponding PGE-Ni-Cu mineralization within the 31 holes drilled across the broad Chrome Mountain target area. In addition, the Company has obtained most of the core samples drilled on the property since 2001 for re-logging and sampling as part of the ongoing modeling work, which has allowed the Group Ten team to identify and confirm the potential for Platreef-style deposits in the Stillwater Complex.

Figure 1 – 14 Target Areas Across the 25-Kilometer Width of the Stillwater West Project

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/76f412d3-e608-4b20-9643-a6111b4f3c57

The Chrome Mountain target area covers an area of approximately 2.9 km by 2.3 km that includes bulk tonnage “Platreef-style” PGE-Ni-Cu targets within the Hybrid Zone (the Discovery, Dunite Ridge, Bald Hills, and Tarantula Targets), as well as potential bulk tonnage PGE-enriched Ni and Cu sulphide mineralization targets within the basal portion of the complex. Potential also exists for higher-grade PGE “reef-type” targets. Comprehensive soil geochemical data has been collected across Chrome Mountain with high levels of PGE, Ni, Cu and Cr in soils shown across kilometer-scale areas coincident with high level electro-magnetic conductors shown in geophysical survey results (see Figures 2, 3 and 4).

Chrome Mountain – Hybrid Zone

The Hybrid Zone is characterized by broad intervals of highly anomalous PGE levels associated with chromite and nickel and copper sulfides with complex pegmatoidal and magmatic breccia textures in the Ultramafic Series lithologies. The complexly textured host rocks, together with broadly disseminated chromite and sulphide, are geologically similar to the Platreef setting in South Africa’s Bushveld Complex.

Table 1 presents highlight intercepts from ten holes drilled in the Discovery target where nine separate intercepts exceeded 100 meters thickness with continuous highly elevated PGE, Ni, Cu and Co mineralization, starting at surface, including 118 m at 1.73 g/t TotPtEq (0.36 Pt, 0.56 Pd, and 0.09 Au for 1.0 g/t 3E along with 0.12% Ni, 0.03% Cu and 0.01% Co for 0.17% NiEq). In addition, six holes returned composite mineralization of over 200 meters in thickness that occurs over a strike length of approximately 600 meters which remains open in all directions and occurs within a broader one kilometer wide area of highly anomalous metals in soils. These holes were targeted on highly elevated platinum and palladium values in soils that characterize the entire Hybrid Zone (see Figure 3). Along with the untested additional soil targets and geophysical conductors, these drill results demonstrate the potential for significant bulk tonnage mineralization at the Chrome Mountain target area.

Chrome Mountain – Dunite Ridge and Bald Hills Targets

Several intrusive dunite targets have been identified in the core of the Hybrid Zone (see cross section CM-6 in Figure 7). Work at Chrome Mountain in 2018 led to the discovery of the Dunite Ridge and Bald Hill targets where mapping of olivine chromite-rich intrusive returned chip samples of up to 16.0 g/t 3E (as 8.72 g/t Pt, 7.25 g/t Pd, and 0.03 g/t Au) at Dunite Ridge. A second sample at Dunite Ridge returned 7.45 g/t 3E as 2.32 g/t Pt, 5.10 g/t Pd, and 0.02 g/t Au (see Table 2). These samples occur within a highly elevated PGE, Ni and Cu soil anomaly covering at least 750 meters of strike. Intrusive dunites can have spectacular grades in the Bushveld Complex, but have not been systematically explored for in the Stillwater Complex. The intrusive dunites identified at the Chrome Mountain target area are one of several occurrences across the overall Stillwater West Project. Dunite Ridge and Bald Hills are priority targets for follow-up work in 2019.

| TABLE 1 – Highlight mineralized drill intercepts from the Chrome Mountain Target Area | ||||||||||||||

| INTERVAL | PRECIOUS METALS | BASE METALS | TOTAL METAL EQUIVALENTS | GRADE THICKNESS | ||||||||||

| HOLE ID | From | To | Width | Pt | Pd | Au | 3E | Ni | Cu | Co | NiEq | TotPtEq | TotNiEq | Grade x Width |

| (m) | (m) | (m) | (g/t) | (g/t) | (g/t) | (g/t) | (%) | (%) | (%) | (%) | (Pt g/t) | (Ni %) | (gram-meters) | |

| CM2007-01 | 3.1 | 148.1 | 145.1 | 0.24 | 0.21 | 0.01 | 0.46 | 0.07 | 0.01 | 0.009 | 0.10 | 0.89 | 0.22 | 129.5 |

| including | 7.9 | 25.9 | 18.0 | 0.46 | 0.54 | 0.02 | 1.02 | 0.08 | 0.01 | 0.010 | 0.12 | 1.52 | 0.37 | 27.4 |

| including | 56.7 | 77.4 | 20.7 | 0.34 | 0.35 | 0.01 | 0.70 | 0.07 | 0.00 | 0.010 | 0.11 | 1.15 | 0.28 | 23.8 |

| AND | 261.5 | 448.1 | 186.5 | 0.04 | 0.04 | 0.01 | 0.08 | 0.12 | 0.02 | 0.014 | 0.18 | 0.82 | 0.20 | 153.9 |

| including | 294.4 | 362.7 | 68.3 | 0.07 | 0.07 | 0.02 | 0.17 | 0.16 | 0.04 | 0.016 | 0.24 | 1.15 | 0.28 | 78.5 |

| including | 305.4 | 334.7 | 29.3 | 0.10 | 0.10 | 0.02 | 0.22 | 0.18 | 0.06 | 0.018 | 0.27 | 1.34 | 0.33 | 39.2 |

| CM2007-02 | 0.0 | 210.6 | 210.6 | 0.20 | 0.28 | 0.02 | 0.49 | 0.10 | 0.01 | 0.011 | 0.14 | 1.08 | 0.26 | 227.4 |

| including | 13.4 | 109.4 | 96.0 | 0.37 | 0.56 | 0.03 | 0.96 | 0.12 | 0.02 | 0.012 | 0.17 | 1.65 | 0.40 | 158.5 |

| including | 38.7 | 68.6 | 29.9 | 0.60 | 1.25 | 0.09 | 1.93 | 0.19 | 0.04 | 0.014 | 0.26 | 3.03 | 0.74 | 90.4 |

| AND | 300.8 | 387.7 | 86.9 | 0.04 | 0.03 | 0.01 | 0.08 | 0.10 | 0.02 | 0.010 | 0.14 | 0.66 | 0.16 | 57.0 |

| CM2007-03 | 0.0 | 47.5 | 47.5 | 0.30 | 0.44 | 0.13 | 0.87 | 0.13 | 0.05 | 0.010 | 0.19 | 1.68 | 0.41 | 79.9 |

| including | 0.0 | 17.7 | 17.7 | 0.33 | 0.42 | 0.16 | 0.92 | 0.14 | 0.06 | 0.011 | 0.21 | 1.82 | 0.44 | 32.1 |

| including | 23.5 | 41.8 | 18.3 | 0.38 | 0.62 | 0.13 | 1.13 | 0.15 | 0.06 | 0.010 | 0.21 | 2.03 | 0.49 | 37.1 |

| CM2007-04 | 1.5 | 119.5 | 118.0 | 0.36 | 0.56 | 0.09 | 1.00 | 0.12 | 0.03 | 0.010 | 0.17 | 1.73 | 0.42 | 204.3 |

| including | 1.5 | 18.9 | 17.4 | 0.40 | 0.52 | 0.15 | 1.06 | 0.12 | 0.04 | 0.010 | 0.17 | 1.81 | 0.44 | 31.5 |

| including | 33.5 | 51.8 | 18.3 | 0.52 | 0.91 | 0.10 | 1.54 | 0.16 | 0.06 | 0.011 | 0.22 | 2.48 | 0.60 | 45.3 |

| including | 34.8 | 43.3 | 8.5 | 0.55 | 0.94 | 0.14 | 1.63 | 0.22 | 0.10 | 0.012 | 0.31 | 2.94 | 0.71 | 25.1 |

| including | 71.3 | 118.3 | 46.9 | 0.45 | 0.71 | 0.11 | 1.27 | 0.13 | 0.04 | 0.011 | 0.18 | 2.04 | 0.50 | 95.9 |

| AND | 151.2 | 242.6 | 91.4 | 0.21 | 0.21 | 0.02 | 0.44 | 0.12 | 0.02 | 0.012 | 0.17 | 1.15 | 0.28 | 105.1 |

| CM2007-05 | 1.2 | 239.3 | 238.1 | 0.14 | 0.22 | 0.04 | 0.40 | 0.12 | 0.03 | 0.011 | 0.17 | 1.12 | 0.27 | 267.4 |

| including | 64.6 | 128.3 | 63.7 | 0.19 | 0.33 | 0.07 | 0.60 | 0.15 | 0.05 | 0.012 | 0.22 | 1.51 | 0.37 | 96.4 |

| including | 85.3 | 107.6 | 22.3 | 0.26 | 0.41 | 0.10 | 0.77 | 0.18 | 0.07 | 0.012 | 0.25 | 1.84 | 0.45 | 40.9 |

| CM2007-06 | 0.0 | 128.0 | 128.0 | 0.15 | 0.18 | 0.06 | 0.40 | 0.19 | 0.07 | 0.014 | 0.27 | 1.52 | 0.37 | 194.1 |

| including | 8.8 | 119.5 | 110.6 | 0.16 | 0.20 | 0.07 | 0.43 | 0.20 | 0.08 | 0.015 | 0.29 | 1.64 | 0.40 | 180.9 |

| CM2007-07 | 1.5 | 227.1 | 225.6 | 0.15 | 0.32 | 0.05 | 0.52 | 0.13 | 0.04 | 0.011 | 0.19 | 1.30 | 0.32 | 293.2 |

| including | 42.1 | 55.5 | 13.4 | 0.19 | 0.45 | 0.06 | 0.70 | 0.14 | 0.05 | 0.010 | 0.20 | 1.54 | 0.37 | 20.7 |

| including | 68.3 | 172.5 | 104.2 | 0.19 | 0.36 | 0.06 | 0.61 | 0.16 | 0.06 | 0.013 | 0.24 | 1.60 | 0.39 | 166.5 |

| including | 76.2 | 93.3 | 17.1 | 0.22 | 0.34 | 0.06 | 0.62 | 0.16 | 0.04 | 0.015 | 0.23 | 1.60 | 0.39 | 27.2 |

| including | 121.3 | 137.8 | 16.5 | 0.17 | 0.19 | 0.06 | 0.42 | 0.18 | 0.09 | 0.012 | 0.27 | 1.53 | 0.37 | 25.2 |

| including | 148.7 | 172.5 | 23.8 | 0.26 | 0.70 | 0.08 | 1.04 | 0.18 | 0.08 | 0.013 | 0.27 | 2.15 | 0.52 | 51.2 |

| CM2007-08 | 0.0 | 209.7 | 209.7 | 0.20 | 0.26 | 0.07 | 0.52 | 0.14 | 0.04 | 0.013 | 0.21 | 1.38 | 0.34 | 290.4 |

| including | 18.3 | 143.9 | 125.6 | 0.27 | 0.38 | 0.10 | 0.75 | 0.16 | 0.05 | 0.013 | 0.23 | 1.72 | 0.42 | 216.6 |

| including | 52.1 | 75.6 | 23.5 | 0.21 | 0.32 | 0.13 | 0.66 | 0.19 | 0.07 | 0.013 | 0.27 | 1.79 | 0.43 | 41.9 |

| including | 81.5 | 100.6 | 19.1 | 0.30 | 0.48 | 0.10 | 0.88 | 0.21 | 0.06 | 0.018 | 0.30 | 2.13 | 0.52 | 40.5 |

| including | 123.1 | 142.7 | 19.5 | 0.54 | 0.78 | 0.07 | 1.39 | 0.14 | 0.04 | 0.013 | 0.20 | 2.23 | 0.54 | 43.6 |

| CM2007-09 | 3.7 | 22.9 | 19.2 | 0.37 | 0.60 | 0.10 | 1.07 | 0.14 | 0.04 | 0.011 | 0.20 | 1.92 | 0.47 | 36.9 |

| including | 9.5 | 22.9 | 13.4 | 0.45 | 0.75 | 0.13 | 1.32 | 0.17 | 0.06 | 0.012 | 0.23 | 2.31 | 0.56 | 31.0 |

| CM2007-10 | 3.4 | 255.7 | 252.4 | 0.14 | 0.18 | 0.02 | 0.34 | 0.14 | 0.02 | 0.013 | 0.20 | 1.16 | 0.28 | 293.8 |

| including | 9.5 | 44.8 | 35.4 | 0.39 | 0.58 | 0.06 | 1.04 | 0.15 | 0.05 | 0.012 | 0.22 | 1.94 | 0.47 | 68.6 |

| including | 92.4 | 108.2 | 15.9 | 0.35 | 0.48 | 0.07 | 0.91 | 0.24 | 0.08 | 0.016 | 0.33 | 2.29 | 0.56 | 36.4 |

Intercepts with grade thickness values over 25 gram-meter TotPtEq are presented above. Total Platinum Equivalent (TotPtEq g/t) and Total Nickel Equivalent calculations reflect total gross metal content using metals prices as follows (all USD): $6.00/lb nickel (Ni), $3.00/lb copper (Cu), $20.00/lb cobalt (Co), $1,000/oz platinum (Pt), $1,000/oz palladium (Pd) and $1,250/oz gold (Au). Values have not been adjusted to reflect metallurgical recoveries. Total metal equivalent values include both base and precious metals, where available. Results labelled ‘n/a’ were not assayed for that metal. Total platinum equivalent grade thickness was determined by multiplying the thickness (in meters) by the Total Platinum Equivalent grade (in grams/tonne) to provide gram-meter values (g-m) as shown. All holes were conducted by Group Ten’s QP and are not considered historic.

Chrome Mountain – Tarantula Target

In the eastern area of the Hybrid Zone, work in 2018 identified the Tarantula Target, where highly anomalous PGE mineralization occurs in the Ultramafic Series. Host rocks are pegmatoidal bronzitite; disseminated chromite, sulphide and magmatic breccia textures have been described over an approximate strike length of at least 500 meters.

Table 2 presents select rock sample results from reconnaissance prospecting and geological mapping programs at the Chrome Mountain and East Boulder target areas in 2018 which confirm the presence of significant platinum, palladium, nickel, copper and cobalt mineralization with grades up to 3.56 g/t Pd, 0.618% Ni, and 0.049% Co outside of the Dunite Ridge Target discussed above (see Table 2). High chromium levels were also noted with 14 samples returning grades of 10 to 26.8% Cr. In addition, test work indicates a consistent ratio of rhodium content relative to platinum values. Neither chromium nor rhodium values have been included in the calculation of metal equivalents in the tables above and below.

| TABLE 2 – Highlight 2018 rock sample results from the Chrome Mountain Target Area | |||||||||||

| PRECIOUS METALS | BASE METALS | TOTAL METAL EQUIVALENTS | |||||||||

| SAMPLE ID | LOCATION | Pt | Pd | Au | 3E | Ni | Cu | Co | NiEq | TotPtEq | TotNiEq |

| (g/t) | (g/t) | (g/t) | (g/t) | (%) | (%) | (%) | (%) | (Pt g/t) | (Ni %) | ||

| 337388 | Dunite Ridge | 8.72 | 7.25 | 0.03 | 16.00 | 0.106 | 0.020 | 0.016 | 0.17 | 16.70 | 4.06 |

| 1409950 | Dunite Ridge | 2.32 | 5.10 | 0.02 | 7.45 | 0.093 | <0.005 | 0.012 | 0.13 | 8.00 | 1.94 |

| 337391 | Dunite Ridge | 0.38 | 1.23 | 0.05 | 1.67 | 0.112 | 0.058 | 0.026 | 0.23 | 2.62 | 0.64 |

| 337392 | Dunite Ridge | 0.41 | 1.00 | 0.08 | 1.49 | 0.157 | 0.056 | 0.019 | 0.25 | 2.53 | 0.61 |

| 3190364 | Discovery | 0.99 | 3.56 | 0.06 | 4.61 | 0.084 | 0.000 | 0.011 | 0.12 | 5.12 | 1.24 |

| 3190372 | Discovery | 1.53 | 2.34 | 0.01 | 3.88 | 0.088 | 0.000 | 0.018 | 0.15 | 4.49 | 1.09 |

| 3190368 | Discovery | 1.78 | 1.42 | 0.01 | 3.21 | 0.156 | 0.000 | 0.017 | 0.21 | 4.08 | 0.99 |

| 3190351 | Discovery | 0.87 | 2.15 | 0.06 | 3.09 | 0.139 | 0.019 | 0.019 | 0.21 | 3.97 | 0.97 |

| 3190375 | Discovery | 0.78 | 2.00 | 0.06 | 2.84 | 0.111 | 0.032 | 0.022 | 0.20 | 3.68 | 0.89 |

| 3190373 | Discovery | 0.47 | 1.17 | 0.04 | 1.68 | 0.104 | 0.000 | 0.020 | 0.17 | 2.39 | 0.58 |

| 3190362 | Discovery | 0.28 | 0.80 | 0.15 | 1.23 | 0.193 | 0.083 | 0.009 | 0.26 | 2.35 | 0.57 |

| 3190363 | Discovery | 0.21 | 0.79 | 0.05 | 1.04 | 0.182 | 0.085 | 0.020 | 0.29 | 2.25 | 0.55 |

| 3190461 | Bald Hills | 1.04 | 1.81 | 0.24 | 3.09 | 0.336 | 0.027 | 0.030 | 0.45 | 5.00 | 1.22 |

| 337378 | Bald Hills | 0.10 | 0.08 | 0.06 | 0.23 | 0.618 | 0.094 | 0.049 | 0.83 | 3.66 | 0.89 |

| 3190467 | Bald Hills | 0.97 | 1.47 | 0.10 | 2.53 | 0.170 | 0.000 | 0.021 | 0.24 | 3.54 | 0.86 |

| 3190464 | Bald Hills | 1.02 | 0.72 | 0.05 | 1.78 | 0.233 | 0.000 | 0.030 | 0.33 | 3.16 | 0.77 |

| 337381 | Bald Hills | 0.44 | 1.77 | 0.07 | 2.28 | 0.107 | 0.000 | 0.024 | 0.19 | 3.07 | 0.75 |

| 337380 | Bald Hills | 1.09 | 0.64 | 0.03 | 1.76 | 0.137 | 0.018 | 0.029 | 0.24 | 2.77 | 0.67 |

| 3190394 | Bald Hills | 1.28 | 0.40 | 0.03 | 1.71 | 0.086 | 0.063 | 0.024 | 0.20 | 2.53 | 0.61 |

| 3190390 | Bald Hills | 0.72 | 0.62 | 0.17 | 1.50 | 0.050 | 0.034 | 0.017 | 0.12 | 2.05 | 0.50 |

| 3190471 | Tarantula | 0.71 | 2.48 | 0.06 | 3.25 | 0.243 | 0.030 | 0.020 | 0.32 | 4.60 | 1.12 |

| 3190397 | Tarantula | 1.44 | 1.88 | 0.14 | 3.46 | 0.100 | 0.007 | 0.010 | 0.14 | 4.05 | 0.99 |

| 3190306 | Tarantula | 0.92 | 2.16 | 0.01 | 3.09 | 0.111 | 0.000 | 0.016 | 0.16 | 3.77 | 0.92 |

| 3190376 | Tarantula | 0.97 | 0.41 | 0.01 | 1.39 | 0.101 | 0.000 | 0.018 | 0.16 | 2.05 | 0.50 |

| 1409933 | East Boulder | 0.68 | 2.58 | 0.15 | 3.41 | 0.212 | 0.152 | 0.015 | 0.34 | 4.84 | 1.18 |

| 3190452 | East Boulder | 0.44 | 1.06 | 0.01 | 1.51 | 0.162 | 0.000 | 0.016 | 0.22 | 2.39 | 0.58 |

| 337365 | Lindgren | 0.00 | 0.10 | 0.04 | 0.14 | 0.315 | 0.976 | 0.030 | 0.90 | 3.87 | 0.94 |

| 337368 | Lindgren | 0.03 | 0.21 | 0.08 | 0.32 | 0.342 | 0.054 | 0.034 | 0.48 | 2.32 | 0.56 |

| 3190389 | Hybrid Zone | 1.73 | 0.42 | 0.01 | 2.16 | 0.081 | 0.036 | 0.019 | 0.16 | 2.83 | 0.69 |

Results over 2 g/t TotPtEq are presented above. Total Platinum Equivalent (TotPtEq g/t) and Total Nickel Equivalent were determined as per Table 1.

Figures 6 and 7 present cross sections representing the Company’s current understanding of the Hybrid Zone and surrounding stratigraphy. The Hybrid Zone is open in all directions, and is a priority target for follow-up in 2019.

Chrome Mountain – Basal Zone Targets

The Company is also targeting potential bulk-tonnage sulphide mineralization in the Basal Series of the complex at Chrome Mountain where mineralization may be associated with interaction between the layered basal magmatic system and the basement country rocks. Interaction and assimilation of basement country rocks is an important component of the Platreef deposits in the Bushveld Complex, where the country rocks may be in place as the footwall or occur as large rafts within the layered magmatic stratigraphy. Kilometer-scale geophysical, geochemical and geological signatures present compelling bulk-tonnage targets in this type of setting for PGE-enriched Ni/Cu sulfides in the lower Stillwater Complex stratigraphy.

The potential for deposits of this type in the Chrome Mountain area has been confirmed by reconnaissance rock chip samples and geological mapping work by Group Ten in 2018, as well as in limited historic drilling, which targeted nickel and copper sulphides in the Basal and lowest Ultramafic Series. These drill holes were relatively shallow, and were only selectively assayed where base metal sulphide levels were high. A few of these high-sulphide intercepts were assayed for PGEs confirming that the nickel and copper sulphides in these areas are highly enriched in PGEs. Notably, this historic drill sampling did not assay areas enriched in chromite, which typically exhibit higher-grade PGE mineralization. Data from the 355 series drill holes by AMAX in the 1960s and 1970s, shown on cross sections in Figures 6 and 7, confirm the presence of net-textured to massive sulphide hosted mineralization proximal to the strongest electro-magnetic conductive signatures.

2018 rock sample results from the historic Lindgren Target in the basal series at Chrome Mountain are particularly compelling as they confirm the presence of significant PGE, Ni and Cu mineralization with results of 0.315% Ni, 0.976% Cu, and 0.030% Co (0.94% Ni Eq) in sample 337365 and 0.342% Ni, 0.054% Cu and 0.034% Co (0.56% Ni Eq) in sample 337368 (see Table 2). Basal zone sulphide targets will be a priority for follow-up work in 2019 at Chrome Mountain.

East Boulder Target Area

As shown in Figure 2, the East Boulder target area centers on a highly conductive geophysical anomaly with coincident highly elevated levels of PGE, Ni, Cu and Cr metals in soils (Figures 3 and 4) covering an area approximately 2.6 km x 1.9 km. The East Boulder target area has less outcrop exposure than the adjacent Chrome Mountain target area (Figure 5) and, as a result, remains much less explored despite historic placer mining in the area. Two drill holes from 2008 confirm the presence of Pt, Pd and Au mineralization adjacent to the EM conductive high anomaly but were not tested for base metals.

Work in 2018 included surface mapping and limited sampling with results up to 3.4 g/t 3E, 0.21% Ni, and 0.15% Cu (4.84 g/t TotPtEq) (see Table 2) providing support that similar mineralized stratigraphic horizons continue into the East Boulder target area.

Future work at the East Boulder target area will include detailed mapping and rock sampling to develop and refine drill targets in the area of the electro-magnetic conductors and coincident soil anomalies.

Amendment to the Catalyst Property Agreement

Group Ten announces that it has amended the terms of the agreement for the Catalyst Project within the Company’s Kluane PGE-Ni-Cu Project in Canada’s Yukon Territory, as announced on August 16, 2017. The amendment allows the Company to meet the $10,000 cash payment requirement by the issuance of 200,000 common shares, and is subject to regulatory approval.

Upcoming Events

Group Ten will be exhibiting in the Investor’s Exchange at booth #3018 at the PDAC convention in March in Toronto, among other upcoming shows. The Company looks forward to releasing further results from the adjacent target areas in the coming weeks.

About Stillwater West

The Stillwater West PGE-Ni-Cu project positions Group Ten as the second largest landholder in the Stillwater Complex, adjoining and adjacent to Sibanye-Stillwater’s world-leading Stillwater, East Boulder, and Blitz platinum group elements (PGE) mines in south central Montana, USA. With more than 41 million ounces of past production and current M&I resources, plus another 49 million ounces of Inferred resources1,2, the Stillwater Complex is recognized as one of the top regions in the world for PGE-Ni-Cu mineralization, alongside the Bushveld Complex and Great Dyke in southern Africa, which are similar layered intrusions. The J-M Reef, and other PGE-enriched sulphide horizons in the Stillwater Complex, share many similarities with the highly prolific Merensky and UG2 Reefs in the Bushveld Complex, while the lower part of the Stillwater Complex also shows the potential for much larger scale disseminated and high-sulphide PGE-nickel-copper type deposits, possibly similar to Platreef in the Bushveld Complex3. Group Ten’s Stillwater West property covers the lower part of the Stillwater Complex along with the Picket Pin PGE Reef-type deposit in the upper portion, and includes extensive historic data, including soil and rock geochemistry, geophysical surveys, geologic mapping, and historic drilling.

Note 1: Report on Montana Platinum Group Metal Mineral Assets of Sibanye-Stillwater, November 2017, Measured and Indicated Resources of 57.2 million tonnes grading 17.0 g/t Pt+Pd containing 31.3 million ounces and 92.5 million tonnes grading 16.6 g/t containing 49.4 million ounces. Grade thickness was determined by applying the reported minimum mining width of 2.0 meters to the M&I grade of 17 g/t Pt+Pd for an average grade thickness of approximately 34 gram-meter (g-m).

Note 2: Public production records from Stillwater Mining Company from 1992 to present.

Note 3: Magmatic Ore Deposits in Layered Intrusions—Descriptive Model for Reef-Type PGE and Contact-Type Cu-Ni-PGE Deposits, Michael Zientek, USGS Open-File Report 2012–1010.

About Group Ten Metals Inc.

Group Ten Metals Inc. is a TSX-V-listed Canadian mineral exploration company focused on the development of high-quality platinum, palladium, nickel, copper, cobalt and gold exploration assets in top North American mining jurisdictions. The Company’s core asset is the Stillwater West PGE-Ni-Cu project adjacent to Sibanye-Stillwater’s high-grade PGE mines in Montana, USA. Group Ten also holds the high-grade Black Lake-Drayton Gold project in the Rainy River district of northwest Ontario and the highly prospective Kluane PGE-Ni-Cu project on trend with Nickel Creek Platinum’s Wellgreen deposit in Canada‘s Yukon Territory.

About the Metallic Group of Companies

The Metallic Group is a collaboration of leading precious and base metals exploration companies, with a portfolio of large, brownfields assets in established mining districts adjacent to some of the industry’s highest-grade producers of platinum & palladium, silver and copper. Member companies include Group Ten Metals (PGE.V) in the Stillwater PGM-Ni-Cu district of Montana, Metallic Minerals (MMG.V) in the Yukon’s Keno Hill silver district, and Granite Creek Copper (GCX.V) in the Yukon’s Carmacks copper district. The founders and team members of the Metallic Group include highly successful explorationists formerly with some of the industry’s leading explorer/developers and major producers and are undertaking a systematic approach to exploration using new models and technologies to facilitate discoveries in these proven historic mining districts. The Metallic Group is headquartered in Vancouver, BC, Canada and its member companies are listed on the Toronto Venture, US OTC, and Frankfurt stock exchanges.

FOR FURTHER INFORMATION, PLEASE CONTACT:

| Michael Rowley, President, CEO & Director | |

| Email: info@grouptenmetals.com | Phone: (604) 357 4790 |

| Web: http://grouptenmetals.com | Toll Free: (888) 432 0075 |

Quality Control and Quality Assurance

2018 rock chip samples were analyzed by Bureau Veritas Mineral Laboratories in Vancouver, B.C. Samples were crushed and split, and a 250 g split pulverized with 85% passing 200 mesh. Gold, platinum, and palladium were analyzed by fire assay (FA350) with ICP finish. Selected major and trace elements were analyzed by peroxide fusion with ICP-EB finish to insure complete dissolution of resistate minerals. Following industry QA/QC standards, blanks, duplicate samples, and certified standards were also assayed.

2007 drilling was conducted by Group Ten’s QP while working for Beartooth Platinum. Pre-2001 drill results are considered historic and have not been independently verified by Group Ten. Mr. Mike Ostenson, P.Geo., is the qualified person for the purposes of National Instrument 43-101, and he has reviewed and approved the technical disclosure contained in this news release.

Forward-Looking Statements

Forward Looking Statements: This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Group Ten believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Group Ten and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Photos accompanying this announcement are available at:

http://www.globenewswire.com/NewsRoom/AttachmentNg/19ab82a2-8538-49c0-a4ab-d53d9560507a

http://www.globenewswire.com/NewsRoom/AttachmentNg/3b1a32c4-124a-49f2-9131-91d308c90693

http://www.globenewswire.com/NewsRoom/AttachmentNg/8bd53d6b-5b65-4b05-b79d-6ec897cd91a3

http://www.globenewswire.com/NewsRoom/AttachmentNg/7500e218-8fb5-4f03-9f58-9ecb52ff8863

http://www.globenewswire.com/NewsRoom/AttachmentNg/f17abd16-0599-4991-b6c7-d6ddb73c1e5f

http://www.globenewswire.com/NewsRoom/AttachmentNg/0812e521-afe4-4be1-944e-d109e1f3db6f

![]()