Denver, Colorado–(Newsfile Corp. – March 2, 2026) – Elemental Royalty Corporation (TSXV: ELE) (NASDAQ: ELE) (“Elemental” or “the Company“) notes the announcement by Quilla Resources Inc. (“Quilla”) on the successful production of first copper cathode from the Chapi Copper Project (“Chapi”) in southern Peru. Elemental holds a 2.0% Net Smelter Return (“NSR”) royalty on the project.

Highlights

- First production of copper cathode at the Chapi Copper Project following Quilla’s acquisition in December 2024

- Ramp-up underway toward plant nameplate capacity of approximately 10,000 tonnes per annum of copper cathode

- Elemental expects first royalty payment from Chapi in Q1 2026

Chief Executive Officer and Director of Elemental Royalty, David M. Cole, commented: “Quilla has made phenomenal progress at Chapi with first copper cathode produced, and ramp-up underway toward nameplate capacity. This rapid progression through key de-risking milestones underscores the project’s meaningful value and significant upside potential.”

Details

Quilla has announced first production of copper cathode at Chapi following the acquisition of the brownfield asset in December 2024. Quilla undertook a comprehensive technical review, engineering evaluation, and operational planning before commencing refurbishment at the mine and solvent extraction and electrowinning (SX-EW) plant facilities. The restart was achieved within the originally stated schedule and budget, reflecting management’s strong execution, operational discipline, and reaffirming Elemental’s confidence in Quilla, and in-country subsidiary Minera Pampa de Cobre S.A.C., as operators.

Following the successful commissioning of the SX-EW the plant, Quilla have stated their intention to progressively increase operating rates toward an initial 10,000 tonnes of copper cathodes per year, while completing remaining capital projects and site optimization initiatives to support stable, long-term operations.

Elemental Royalty on Chapi

Acquired in January 2025, the royalty comprises a 2% NSR on minerals produced from the approximately 26,000-hectare property, as well as a 2% NSR royalty on any minerals produced from properties acquired by Quilla within a two-kilometer area of interest (“AOI”). In addition, the agreement includes an additional 2% NSR royalty from any minerals that are produced from outside the Property Royalty area, but that are processed at the Chapi Solvent Extraction Electro-Winning (“SX-EW”) plant.

Background on the Chapi Mine

The Chapi Mine is located in southern Peru’s Moquegua and Arequipa Departments at an elevation of approximately 2,750 meters, and has ready access approximately 50 kilometers south-southeast from the city of Arequipa. Historical, small-scale copper production, which is poorly documented, occurred intermittently from the 1930s through the early 1980s. Subsequently, between 2006 and 2012 the Chapi Mine produced approximately 5,000 to 8,500 tonnes per annum, initially of copper sulphates from open-pit and underground mining and heap leaching, and later copper cathodes from open-pit mining, heap leaching, and SX-EW (solvent extraction-electrowinning) processing. The grades mined during 2006-2012 were reported as 0.59% – 1.04% copper. The operations were halted in 2012 due to declining copper prices and operational challenges that were mainly related to insufficient ore control on materials delivered to the leach pads.

The historical Chapi Mine is comprised of two principal open pits, underground workings, a crushing and agglomeration circuit, heap leach pads, a solvent extraction plant, an electrowinning copper cathode plant, and related infrastructure including mine camp, office facilities, water supply, and power. Since 2012, Chapi has been under care and maintenance with the principal permits for mining operations remaining in place under a temporary suspension.

For further information contact:

David M. Cole

CEO and Director

For more information, please contact:

| David M. Cole | Tara Vivian-Neal |

| CEO info@elementalroyalty.com | Investor Relations investor@elementalroyalty.com |

www.elementalroyalty.com

Phone: +1 (604) 688-6390

(TSXV: ELE) (NASDAQ: ELE) (ISIN: CA28620K1066) (CUSIP: 28620K)

About Elemental Royalty Corporation.

Elemental Royalty is a new mid-tier, gold-focused streaming and royalty company with a globally diversified portfolio of 18 producing assets and more than 200 royalties, anchored by cornerstone assets and operated by world-class mining partners. Formed through the merger of Elemental Altus and EMX, the Company combines Elemental Altus’s track record of accretive royalty acquisitions with EMX’s strengths in royalty generation and disciplined growth. This complementary strategy delivers both immediate cash flow and long-term value creation, supported by a best-in-class asset base, diversified production, and sector-leading management expertise.

Elemental Royalty trades on the TSX Venture Exchange and on NASDAQ under the ticker symbol “ELE”.

Cautionary note regarding forward-looking statements and financial outlook

This news release contains certain “forward looking statements” and certain “forward-looking information” as defined under applicable United States and Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “believe”, “continue”, “plans” or similar terminology (including negative and grammatical variations thereof).

Forward-looking statements and information include, but are not limited to, statements regarding future royalties and future consideration payments or issuances of shares, or other statements that are not statements of fact. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies.

Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of Elemental to control or predict, that may cause Elemental’s actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the impact of general business and economic conditions, the absence of control over the mining operations from which Elemental will receive royalties, risks related to international operations, government relations and environmental regulation, the inherent risks involved in the exploration and development of mineral properties; the uncertainties involved in interpreting exploration data; the potential for delays in exploration or development activities; the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results will not be consistent with Elemental’s expectations; accidents, equipment breakdowns, title matters, labour disputes or other unanticipated difficulties or interruptions in operations; fluctuating metal prices; unanticipated costs and expenses; uncertainties relating to the availability and costs of financing needed in the future; the inherent uncertainty of production and cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations; currency fluctuations; regulatory restrictions, including environmental regulatory restrictions; liability, competition, loss of key employees and other related risks and uncertainties. For a discussion of important factors which could cause actual results to differ from forward-looking statements, refer to the annual information form of Elemental for the year ended December 31, 2024. Elemental undertakes no obligation to update forward-looking statements and information except as required by applicable law. Such forward-looking statements and information represent management’s best judgment based on information currently available. No forward-looking statement or information can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements or information.

Neither the TSX-V, its Regulation Service Provider (as that term is defined in the policies of the TSX-V) or the Nasdaq Stock Market LLC accepts responsibility for the adequacy or accuracy of this press release.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/285993

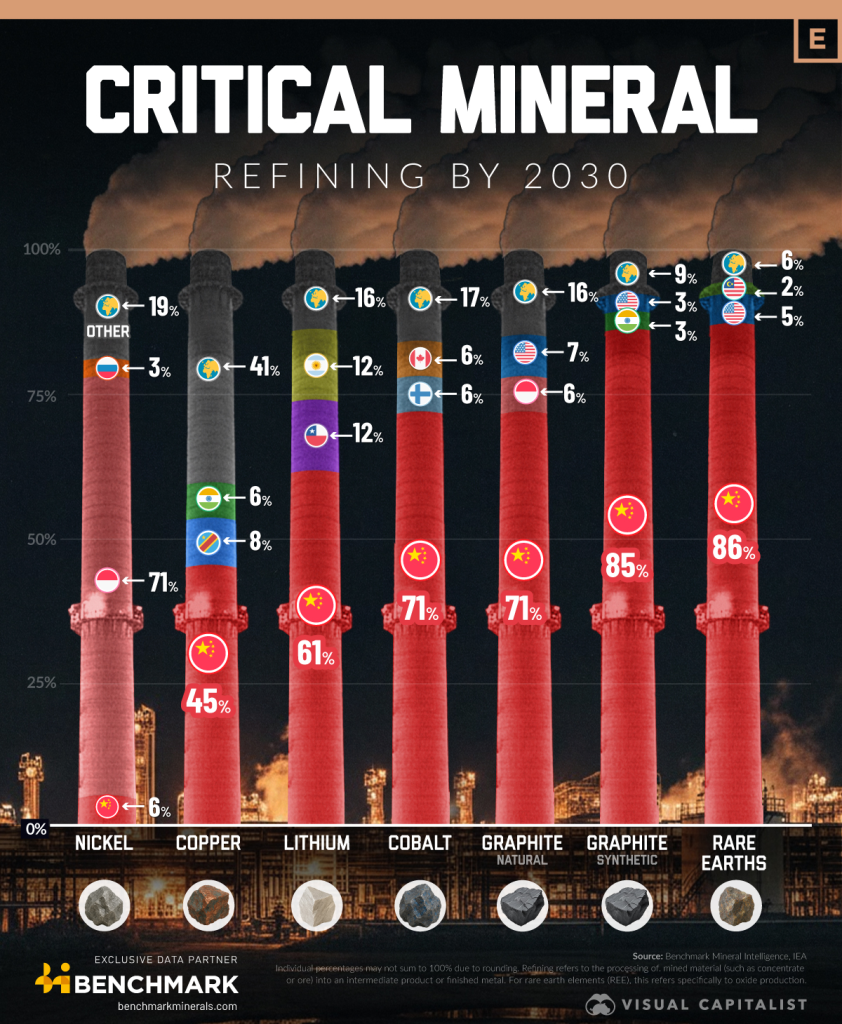

China

China Indonesia

Indonesia Russia

Russia DRC

DRC India

India Chile

Chile Argentina

Argentina United States

United States Malaysia

Malaysia Finland

Finland Canada

Canada South Korea

South Korea Australia

Australia Sweden

Sweden Morocco

Morocco Saudi Arabia

Saudi Arabia Uganda

Uganda Tanzania

Tanzania