Proven Probable

Proven ProbableCategory: Base Metals

Press Release

Corporate Presentation

https://youtu.be/4qbyvnu_Bhw

About EMX. EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and the TSX Venture Exchange under the symbol EMX.

For further information contact:

David M. Cole

President and Chief Executive Officer

Phone: (303) 979-6666

Dave@EMXroyalty.comScott Close

Director of Investor Relations

Phone: (303) 973-8585

SClose@EMXroyalty.comIsabel Belger

Investor Relations (Europe)

Phone: +49 178 4909039

IBelger@EMXroyalty.com

Press Release

Corporate Presentation

https://youtu.be/HwXHWNC3-nc

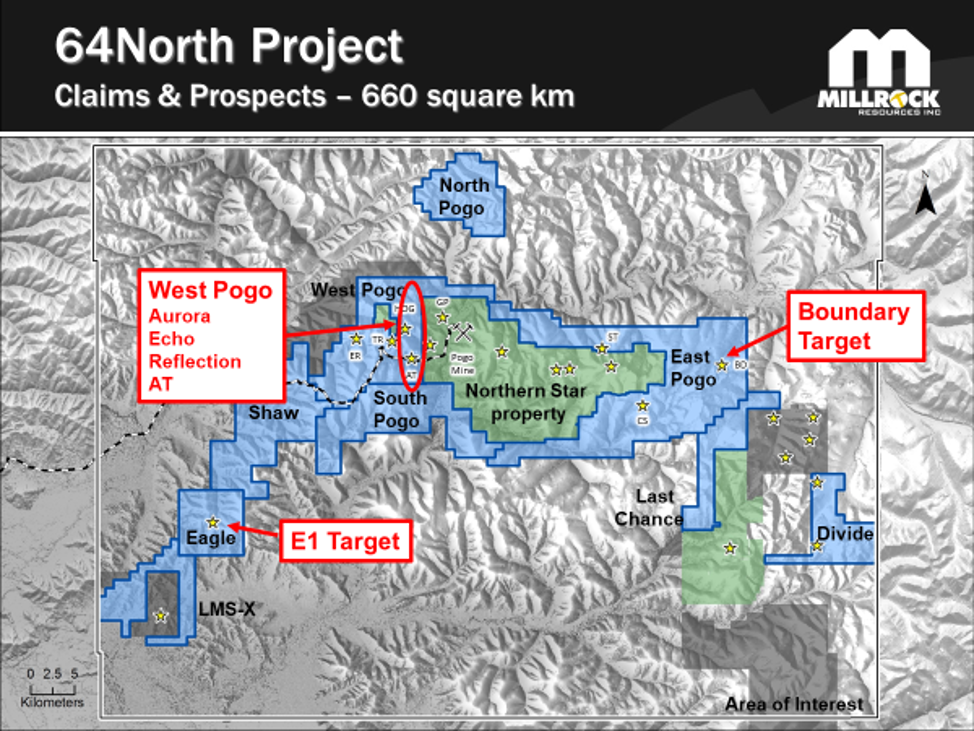

Millrock President & CEO Gregory Beischer commented, “We are pleased to have been able to execute this exploration program despite the additional risks and challenges posed by COVID. A strong initial drill test of the West Pogo prospects was completed, and new drill targets were defined at other prospects on this district-scale gold project. We look forward to pending assay results and developing exploration plans for 2021.”

FOR FURTHER INFORMATION, PLEASE CONTACT:

Melanee Henderson, Investor Relations

(604) 638-3164

Transcript

https://youtu.be/wXUfft9sSvg

Steve Todoruk the 2019 Murray Pezmin Award Winner and World Renowned Investment Executive for Sprott USA sits down with Maurice Jackson of Proven and Probable to discuss the Natural Resources Space and his thesis on how he finds ‘The Next Big Discovery’, as too many companies trick investors with their nomenclature when their deposit is actually a different underlying asset in the ground. The is a reason Rick Rule hand-picked Steve Todoruk and the results are in the returns. Website: https://sprottusa.com/ Phone: 800.477.7853 Contact: stodoruk@sprottglobal.com – Subject Line: Proven and Probable

Press Release

Corporate Presentation

https://youtu.be/EV13Ds-AqX4

“We’re eager to continue drilling East Preston,” said Alex Klenman, President & CEO of Azincourt Energy. “We know the area is target rich and we’ve only drill tested a handful to date. The additional geophysics will add to the targeting and help refine priority areas. In addition, this round of work will allow us to meet the spend threshold of the option agreement with Skyharbour and Dixie. It’s a significant milestone for the company,” continued Mr. Klenman.

For further information contact

Spencer Coulter

Corporate Communications

Skyharbour Resources Ltd.

Telephone: 604-687-3800

Email: info@skyharbourltd.com

About Nevada Copper

Nevada Copper (TSX: NCU) is a copper producer and owner of the Pumpkin Hollow copper project. Located in Nevada, USA, Pumpkin Hollow has substantial reserves and resources including copper, gold and silver. Its two fully permitted projects include the high-grade underground mine and processing facility, which is now in the production stage, and a large-scale open pit project, which is advancing towards feasibility status.

NEVADA COPPER CORP.

www.nevadacopper.comFor further information contact:

Rich Matthews, Investor Relations

Integrous Communications

rmatthews@integcom.us

+1 604 355 7179

Press Release

Corporate Presentation

https://youtu.be/EV13Ds-AqX4

Skyharbour’s President and CEO, Jordan Trimble commented: “We are thrilled to have this Definitive Agreement signed as we continue to execute on our business model by adding value to our project base in the Athabasca Basin through strategic partnerships as well as focused mineral exploration at our flagship Moore Lake Project. We are excited to have the opportunity to work with new partners in Pitchblende and Valor led by experienced management and technical teams at our North Falcon Point Project while maintaining a 100% interest at the Frasers Lakes Uranium and Thorium Deposit at the South Falcon Point Project. News will be forthcoming on exploration plans and the timing is excellent given the recent upward momentum in the uranium market.”

For further information contact :

Spencer Coulter

Corporate Development and Communications

Skyharbour Resources Ltd.

Telephone: 604-687-3376

Email: info@skyharbourltd.com

Click here

https://youtu.be/EV13Ds-AqX4

Jordan Trimble, President and CEO of Skyharbour Resources, stated: “Drill hole ML20-09 is a breakthrough hole for us at the Maverick East Zone as it is the longest continuously mineralized drill intercept the Company has reported and it is one of the best basement-hosted zones of mineralization discovered at the project. We are successfully increasing the size of the high grade uranium zones at the Maverick corridor and these results illustrate the notable discovery upside potential at the project especially in the basement rock feeder-zones which have had limited drill-testing historically. The remaining assay results from the program are pending with planning for additional drilling at Moore Lake currently underway.”

Spencer Coulter

Corporate Development and Communications

Skyharbour Resources Ltd.

Telephone: 604-639-3850

Toll Free: 800-567-8181

Facsimile: 604-687-3119

Email: info@skyharbourltd.com