VANCOUVER, March 1, 2019 /PRNewswire/ – Pacton Gold Inc. (TSXV: PAC, OTC: PACXF) (the “Company” or “Pacton“) is pleased to announce that it has entered into a binding letter of intent (“LOI“) to acquire a 100% interest in the Tardarinna Gold Project. The acquisition of this strategic and prospective property, significantly enhances Pacton’s exposure to high-grade, shear-hosted gold within the Pilbara in Western Australia. Exploration targeting is underway and will be followed by field-based exploration across the property.

Tardarinna Gold Project Acquisition Highlights:

Up to 328 g/t Au has been reported by historical surface samples

Shallow eluvial gold workings identified in the south eastern quadrant of Project

Large target locations: Pegmatoidal-quartz veins have been delineated within a shear zone with >1 km strike and ranging between 10 to 50 m wide

Underexplored: property has never been drill tested

Tier one jurisdiction: Located in the Pilbarra region of Western Australia

Alec Pismiris, Interim President and CEO, of Pacton Gold, commented, “Acquiring the Tardarinna gold project will greatly enhance our exposure to high-grade, shear-hosted gold mineralization. This is a property with considerable advantages: it has historical samples of impressively high-grade gold, it is underexplored and has never been drill-tested and it is located in a stable jurisdiction with superb access to infrastructure. We look forward to defining the potential scale of Tardarinna.”

Under the terms of the LOI, which will be formalized by a definitive agreement, the Company will acquire a 100% interest in Tardarinna by the issuance of 1,250,000 common shares.

This transaction is subject to the acceptance of the TSX Venture Exchange.

About Pacton Gold

Pacton Gold is a Canadian exploration company with key strategic partners focused on the exploration and development of high grade conglomerate and orogenic gold properties located in the district-scale Pilbara gold rush in Western Australia and the Red Lake District, Ontario.

The technical content of this news release has been reviewed and approved Peter Caldbick, P.Geo., a director of the Company and a Qualified Person pursuant to National Instrument 43-101. The qualified person has not yet verified the data disclosed, including sampling, analytical, and test data underlying the information or opinions contained in the written disclosure.

On Behalf of the Board of Pacton Gold Inc.

R. Dale Ginn

Executive Chairman

This news release may contain or refer to forward-looking information based on current expectations, including, but not limited to the Company achieving success in exploring its properties and the impact on the Company of these events, including the effect on its share price. Forward-looking information is subject to significant risks and uncertainties, as actual results may differ materially from forecasted results. Forward-looking information is provided as of the date hereof and we assume no responsibility to update or revise such information to reflect new events or circumstances. References to other issuers with nearby projects is for information purposes only and there are no assurances the Company will achieve similar results.

Tesla – The Next Enron?

As the Austrian economists have long pointed out, one of the things that commonly happens during periods of credit expansion is that the easy money leads to malinvestment. Which is usually revealed later on when the credit is removed and the excesses are exposed.

Of which there is growing evidence that Tesla may turn out to fit this profile. To the degree that some analysts are suggesting it might even be the next Enron.

Certainly one of the challenges in today’s financial markets (and perhaps this has always been the case) is not just in analyzing the numbers. But also in evaluating the integrity of the numbers. Because remember that the Enron numbers looked great. Except that they were never real.

And now as Tesla approaches a key financial event where its $920 million dollar bond payment is coming due, not only is there uncertainty as to how CEO Elon Musk is going to make that payment, but also increasing concerns around his actions and the veracity of the financial data the company provides.

In an interview with Tesla analyst Dave Kranzler of Investment Research Dynamics, Kranzler pointed out how not only did Musk break the law in sending his “420 secured” tweet, but that “Tesla’s Q3 GAAP “Net Income” numbers are highly misleading, if not outright fraudulent”.

Aside from concerns about the quality of the financial statements, Mark Tepper, president and CEO of Strategic Wealth Partners mentions how “there are stories of people not getting their vehicles, and then not getting their refunds for months.” While another concern being echoed among Tesla bears is in regards to the company’s growing reputation for being unable to deliver on the promises Musk makes. “He hasn’t hit on any target or deliverable with any sort of reliability for years now. Why should I believe him now? Remember in 2016 when he said they’d be profitable and didn’t need any more money? Or when they said that in 2017? He’ll probably be saying the same thing at the bankruptcy hearing.” -Harris Kupperman of Praetorian Capital

In addition to the red flags surrounding management is the latest news that January sales are down significantly, as the tax incentives have begun phasing out.

(chart courtesy of @teslashcarts)

Which makes it even more interesting to see what will happen in the next few days as the bond payment comes due. Especially with Musk creating a new round of suspense on Wednesday with a tweet that “some Tesla news” will be delivered on Thursday.

So if Musk is going to convince investors that the company is on solid footing, under good management, and that the data is accurate, he has some work to do. Because simply based on the events of the past year, as well as growing skepticism in the investment community, the possibility that Tesla will be exposed as an Enron is becoming a more real view in the marketplace.

To date the company has been able to navigate these issues. Yet especially if the Fed were to ever remove the unprecedented amount of credit it has injected into the system over the past decade, if the concerns regarding Tesla are indeed accurate, it may well in time rival Enron as one of the biggest financial scandals in history.

Chris Marcus

Arcadia Economics

“Helping You Thrive While We Watch The Dollar Die”

www.ArcadiaEconomics.com

Company Production Hits an All-Time Yearly Record, Reduced Operating Expenses by 30%

TULSA, Okla., Feb. 28, 2019 (GLOBE NEWSWIRE) — Jericho Oil Corporation (“Jericho”) (TSX-V: JCO; OTC PINK: JROOF) announces that preliminary 2018 full-year partnership production totaled approximately 297,000 barrels of oil equivalent (“BOE”) up 33% from 2017 full-year partnership production of 222,000 BOE. The Company’s 2018 partnership production is an all-time yearly high.

In addition to record production, the Company continued to drive down production operating expenses with an approximately $17.00 / BOE cost in 2018, a reduction of 30% from the last year. A combination of lower absolute expenses and efficient production growth from our STACK asset produced outstanding per unit results for Jericho shareholders further demonstrating the dedication of our team and the quality of our world-class STACK asset.

In 2019, Jericho is committed to maintaining balance sheet and capital spend flexibility (with low leverage and a prudent hedging program), allocating capital based on strategic and rate-of-return metrics, prioritizing the Company’s high-return STACK asset and potential acquisition opportunities near our concentrated position. A continued improvement in commodity prices through the remainder of Q1 2019 will see Jericho move back into a development mode and also accelerate its return to production program for shut-in wells in its existing fields.

Industry activity has focused on the low-cost, high-return Osage and Meramec formations within the STACK play of Oklahoma. Deep-pocketed public operators including ExxonMobil, Chesapeake Energy, Sandridge Energy and Chaparral Energy continue to put considerable capital resources in and around Jericho’s largely held-by-production STACK acreage position. To-date, the Company has participated in multiple successful STACK wells with many of our offset operators, gleaning valuable information that drives our confidence in the underlying value of our investment.

“These outstanding and record results confirm our 2018 strategy to successfully prove and develop our premier STACK acreage position,” stated Brian Williamson, CEO of Jericho Oil, adding, “the resulting production growth provides our shareholders confidence in the exceptional quality of our high-impact STACK resource. Looking forward to 2019, we are excited in our unique ability to drive further competitive performance through the quality of our investments and our capital and operating discipline. While we are pleased with our 2018 results, we were just starting to see our patience be rewarded as we began to drill our STACK asset, return existing shut-in wells to production and move to develop some of our other high potential assets when oil prices turned down 40% in the end of 2018. We are hopeful that oil prices will continue their upward trend and provide us the opportunity to expand upon 2018’s success.”

In addition to Jericho’s steady base of low-decline production, its STACK JV has an interest in four currently producing Osage and Meramec formation wells.

Jericho also announces that effective March 1, 2019, Brian Williamson, CEO, assumes the additional position of President and Ben Holman, CFO, assumes the additional position of Secretary. The roles of President and Secretary were previously held by Allen Wilson, Jericho’s founder, who continues with the Company as a director, consultant and shareholder.

About Jericho Oil Corporation

Jericho Oil (www.jerichooil.com) is focused on domestic, liquids-rich unconventional resource plays, located primarily in the Anadarko basin STACK Play of Oklahoma. Jericho’s primary business objective is driving long-term shareholder value through the growth of oil and gas production, cash flow and reserves. Jericho has assembled an interest in 55,000 net acres across Oklahoma, including an interest in ~16,000 net acres in the STACK Play. Jericho owns a 26.5% interest in STACK JV.

Jericho’s current operations are focused on the oil-prone Meramec and Osage formations in the STACK. The Jericho team applies advanced engineering analyses and enhanced geological techniques to under-developed resource areas.

Jericho, with operational headquarters in Tulsa, Oklahoma, trades publicly on the TSX Venture Exchange (JCO) and OTC Markets (JROOF). Jericho owns its net acre position in Oklahoma through, and participates in the STACK JV through, one or more wholly owned subsidiaries.

Cautionary Note Regarding Forward-Looking Statements: This news release includes certain “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and Canadian securities laws. There can be no assurance that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual events and results to differ materially from Jericho’s expectations include risks related to the exploration stage of Jericho’s project; market fluctuations in prices for securities of exploration stage companies; and uncertainties about the availability of additional financing.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

VANCOUVER, British Columbia, Feb. 28, 2019 (GLOBE NEWSWIRE) — Metallic Minerals Corp. (TSX-V: MMG; US OTC: MMNGF) (“Metallic Minerals” or the “Company”) announces that company representatives will be attending the Prospectors & Developers Association of Canada (PDAC) International Convention to be held at the Metro Toronto Convention Centre in Toronto, Canada from Sunday March 3rd to Wednesday March 6th. Metallic Minerals will be exhibiting in the Investors Exchange throughout the conference at booth #3018 as a member of the Metallic Group of Companies. The PDAC Convention is the most-attended event for the world’s mineral exploration and mining sector and promotes a globally responsible and sustainable minerals industry.

Metallic Minerals also announces that it has granted 2,500,000 incentive stock options (the “Options”) to directors, officers, employees and consultants of the Company. The Options are exercisable for up to five years, expiring on February 28, 2024, and each Option will allow the holder to purchase one common share of the Company at a price of $0.18 per share based on the closing price of the previous trading day. The Options are subject to certain vesting requirements in accordance with the Company’s Long-Term Performance Incentive Plan.

About Metallic Minerals Corp.

Metallic Minerals Corp. is a growth stage exploration company, focused on the acquisition & development of high-grade silver and gold in under-explored districts of mining-friendly jurisdictions proven to produce top-tier assets. Our objective is to create value through a systematic, entrepreneurial approach to exploration. The Company’s core Keno Silver project is located in the historic Keno Hill silver district of Canada’s Yukon Territory, with over 300 million ounces of high-grade silver in past production and current resources, and excellent existing infrastructure, including grid power, highway & road access. Metallic Minerals is led by a team with a track record of discovery and exploration success, including large scale development, permitting and project financing.

About the Metallic Group of Companies

The Metallic Group is a collaboration of leading precious and base metals exploration companies, with a portfolio of large, brownfields assets in established mining districts adjacent to some of the industry’s highest-grade producers of platinum & palladium, silver and copper. Member companies include Group Ten Metals (PGE.V) in the Stillwater PGM-Ni-Cu district of Montana, Metallic Minerals (MMG.V) in the Yukon’s Keno Hill silver district, and Granite Creek Copper (GCX.V) in the Yukon’s Carmacks copper district. The founders and team members of the Metallic Group include highly successful explorationists formerly with some of the industry’s leading explorer/developers and major producers and are undertaking a systematic approach to exploration using new models and technologies to facilitate discoveries in these proven historic mining districts. The Metallic Group is headquartered in Vancouver, BC, Canada and its member companies are listed on the Toronto Venture, US OTC, and Frankfurt stock exchanges.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this release.

VANCOUVER, British Columbia, Feb. 28, 2019 (GLOBE NEWSWIRE) — Group Ten Metals Inc. (TSX.V: PGE; US OTC: PGEZF; FSE: 5D32) (the “Company” or “Group Ten”) announces that company representatives will be attending the Prospectors & Developers Association of Canada (PDAC) International Convention to be held at the Metro Toronto Convention Centre in Toronto, Canada from Sunday March 3rd to Wednesday March 6th. Group Ten will be exhibiting in the Investors Exchange throughout the conference at booth #3018 as a member of the Metallic Group of Companies. The PDAC Convention is the most-attended event for the world’s mineral exploration and mining sector and promotes a globally responsible and sustainable minerals industry.

Group Ten also announces that it has granted 545,000 incentive stock options (the “Options”) to directors, officers, employees and consultants of the Company. The Options are exercisable for up to five years, expiring on February 28, 2024, and each Option will allow the holder to purchase one common share of the Company at a price of $0.20 per share, based on the closing price of the previous trading day. The Options are subject to certain vesting requirements in accordance with the Company’s Long-Term Performance Incentive Plan.

About Group Ten Metals Inc.

Group Ten Metals Inc. is a TSX-V-listed Canadian mineral exploration company focused on the development of high-quality platinum, palladium, nickel, copper, cobalt and gold exploration assets in top North American mining jurisdictions. The Company’s core asset is the Stillwater West PGE-Ni-Cu project adjacent to Sibanye-Stillwater’s high-grade PGE mines in Montana, USA. Group Ten also holds the high-grade Black Lake-Drayton Gold project in the Rainy River district of northwest Ontario and the highly prospective Kluane PGE-Ni-Cu project on trend with Nickel Creek Platinum’s Wellgreen deposit in Canada‘s Yukon Territory.

About the Metallic Group of Companies

The Metallic Group is a collaboration of leading precious and base metals exploration companies, with a portfolio of large, brownfields assets in established mining districts adjacent to some of the industry’s highest-grade producers of platinum & palladium, silver and copper. Member companies include Group Ten Metals (PGE.V) in the Stillwater PGM-Ni-Cu district of Montana, Metallic Minerals (MMG.V) in the Yukon’s Keno Hill silver district, and Granite Creek Copper (GCX.V) in the Yukon’s Carmacks copper district. The founders and team members of the Metallic Group include highly successful explorationists formerly with some of the industry’s leading explorer/developers and major producers and are undertaking a systematic approach to exploration using new models and technologies to facilitate discoveries in these proven historic mining districts. The Metallic Group is headquartered in Vancouver, BC, Canada and its member companies are listed on the Toronto Venture, US OTC, and Frankfurt stock exchanges.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

ANCOUVER , Feb. 28, 2019 /CNW/ – Pacton Gold Inc. (TSXV: PAC, OTC: PACXF) (the “Company” or “Pacton“) is pleased to announce its participation in the following events in March: Redcloud Pre-PDAC Mining Showcase, Metals Investor Forum and PDAC 2019 convention in Toronto, Canada .

Pacton Gold Inc. (CNW Group/Pacton Gold Inc.)

Redcloud Pre-PDAC Mining Showcase Event Details

Date and Time: Friday, March 1, 2019 ( 8.00 am – 5.00 pm )

Location: Omni King Edward Hotel, 37 King Street East, Toronto

Metals Investor ForumEvent Details

Date and Time: Saturday, March 2 (9. 00 am to 6:00 pm ) and Sunday, March 3, 2019 ( 9.00 am – 4.00 pm )

Location: 3rd floor, Delta Hotel, 75 Lower Simcoe Street, Toronto

Pacton Presentation: Dale Ginn , Chairman and Director will present on Sunday, March 3 at 10:40 am

PDAC Event and Booth Details

Event: PDAC 2019

Date: March 3 – 6, 2019

Location: Investors Exchange, Metro Toronto Convention Centre, Toronto, Canada

Booth Number: 3142

Booth Hours Sunday, March 3 , 10:00 am – 5:00 pm

Monday, March 4 , 10:00 am – 5:00 pm

Tuesday, March 5 , 10:00 am – 5:00 pm

Wednesday, March 6 , 9:00 am – 12:00 pm

Pacton Gold is a Canadian exploration company with key strategic partners focused on the exploration and development of high grade conglomerate and orogenic gold properties located in the district-scale Pilbara gold rush in Western Australia and the Red Lake District, Ontario. Pacton’s Red Lake mineral claims are strategically located between Pure Gold’s Madsen property, including the Wedge Zone, and Great Bear Resource’s Dixie discovery. The property geology is made up of two key packages known to host significant gold mineralization in the district. The Confederation

Assemblage and the Balmer Assemblage hosts the high-grade gold mineralization at Great Bear Resources’ Dixie Project and Pure Gold’s Madsen property, respectively. A high-resolution helicopter magnetics survey is underway to identify D2 structures and folding that are proposed to have significant control on gold mineralization in the district.

On Behalf of the Board of Pacton Gold Inc.

R. Dale Ginn

Executive Chairman

Neither TSX Venture Exchange, the Toronto Stock Exchange nor their Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Vancouver, British Columbia–(Newsfile Corp. – February 28, 2019) – Sojourn Exploration Inc. (TSXV: SOJ) (OTC Pink: SJRNF) (“Sojourn” or the “Company“) announces that it will change its name to ArcWest Exploration Inc. (“ArcWest“) effective February 28, 2019.

The Company will trade on the TSX Venture Exchange under the new stock symbol “AWX” and under the new CUSIP/ISIN numbers 03969H105/CA0369H1055.

For further information please contact Tyler Ruks, President and CEO AT 1 (604) 638-3695.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

TORONTO , Feb. 28, 2019 /CNW/ – Anaconda Mining Inc. (“Anaconda” or the “Company”) (ANX.TO) (ANXGF) is pleased to announce the final results from the 10,000-metre drill program that began in July 2018 at the Goldboro Gold Project in Nova Scotia (“Goldboro”). Anaconda drilled four holes (BR-18-64 to 67), totaling 1,456 metres (the “EG Drill Program”) to extend the existing Goldboro Deposit towards the east along strike. The EG Drill Program successfully intersected the host fold structure, alteration and mineralization 100 metres east of the current Mineral Resource within the East Goldbrook Gold System (“EG Gold System”). Anaconda also encountered five occurrences of visible gold (Exhibit A, B).

The EG Drill Program intersected a high-grade mineralized zone which included 25.70 grams per tonne (“g/t”) gold over 1.5 metres and 8.00 g/t gold over 3.2 metres up plunge from very high-grade historic assays including 215.74 g/t gold over 3.7 metres (the “High-Grade Zone”) (See photo in Exhibit C). The High-Grade Zone plunges moderately to the east and is located on the south dipping limb of the host fold structure. It extends for at least 150 metres and is open down plunge. High-grade plunging chutes are common at Goldboro , having been intersected elsewhere in the deposit. Furthermore, numerous other mineralized zones were intersected along the south limb of the EG Gold System outside of the High-Grade Zone, with further drilling planned to confirm the geological model for these zones.

A table of selected intersections from both recent and historical drilling are shown in the table below.

“These drill results continue to demonstrate the expansion potential of the Goldboro Deposit as well as the ability to locate pockets of very high-grade continuous mineralized zones. The results from the EG Drill Program, taken together with historical drilling in the East Goldbrook area, indicate that there is a very high-grade zone of at least 150 metres in plunge length, which remains open for expansion down plunge. In our upcoming 5,000-metre drill program, we will take a closer look at this high-grade area to see if we can define it better. With all results received from the 10,000-metre drill program, we are incorporating them into an updated Mineral Resource estimate currently underway by WSP Canada Inc. We expect to publish a new estimate by the third quarter.”

~ Dustin Angelo , President and CEO, Anaconda Mining Inc.

Initiation of a 5,000-metre drill program at Goldboro

The Company will initiate a 5,000-metre drill program at Goldboro beginning in March. The drill program will focus on expansion drilling in the EG Gold System with the goal of growing resources and better defining the extents of the high-grade plunging chutes intersected in the recent EG Drill Program. The drill program will also focus on infill drilling portions of the Boston Richardson Gold System with the goal of converting high-grade Inferred Resources to Indicated Resources. The 5,000-metre diamond drill program will be funded using the proceeds of a flow-through financing completed in July of 2018.

Table of selected composited assays from drill holes reported in this press release:

Hole ID

From

(m)

To

(m)

Interval

(m)

Au

(g/t)

Gold

System

Visible

Gold

Section

BR-18-64

147.8

148.6

0.8

1.17

EG

9750E

Current

and

255.3

256.0

0.7

1.45

EG

and

267.2

267.7

0.5

0.54

EG

VG

and

387.5

388.0

0.5

1.33

EG

and

451.5

452.0

0.5

2.05

EG

BR-18-65

133.6

134.1

0.5

5.69

EG

and

190.0

191.0

1.0

3.37

EG

and

317.7

318.3

0.6

6.41

EG

and

321.5

322.1

0.6

2.53

EG

VG

BR-18-66

61.0

62.5

1.5

25.70

EG

including

61.0

61.6

0.6

63.33

EG

VG

and

90.0

92.0

2.0

6.37

EG

including

90.0

91.0

1.0

12.08

EG

and

183.6

185.0

1.4

1.22

EG

and

229.0

230.0

1.0

1.36

EG

BR-18-67

51.2

52.2

1.0

2.42

EG

9850E

and

53.8

54.4

0.6

5.94

EG

and

75.0

77.5

2.5

1.57

EG

and

116.6

118.0

1.4

1.48

EG

and

125.5

128.0

2.5

2.24

EG

and

136.6

139.2

2.6

4.86

EG

including

137.6

138.2

0.6

16.89

EG

and

142.6

145.8

3.2

8.00

EG

including

145.0

145.8

0.8

30.66

EG

VG

and

189.8

190.4

0.6

12.33

EG

VG

BR-18-16

23.5

24.0

0.5

0.73

EG

9650E

Previous

and

189.1

189.7

0.6

11.59

EG

VG

and

315.6

318.5

2.9

2.23

EG

including

315.6

316.1

0.5

8.88

EG

OSK11-01

36.0

37.0

1.0

1.82

EG

9650E

Historic

and

43.9

46.0

2.2

0.96

EG

and

61.0

62.0

1.0

0.76

EG

and

86.0

88.0

2.0

1.81

EG

and

128.0

130.0

2.0

0.58

EG

OSK11-02

117.0

118.5

1.5

137.77

EG

VG

including

117.0

117.5

0.5

412.00

EG

VG

and

127.0

128.5

1.5

0.65

EG

and

174.0

175.0

1.0

1.28

EG

and

179.5

183.0

3.5

1.76

EG

VG

including

182.0

183.0

1.0

4.55

EG

and

199.5

200.5

1.0

0.77

EG

and

235.5

236.5

1.0

2.28

EG

OSK11-03

17.0

18.0

1.0

0.54

EG

9900E

and

38.0

39.0

1.0

1.28

EG

and

46.0

47.0

1.0

2.87

EG

and

49.0

50.5

1.5

2.02

EG

and

143.0

143.7

0.7

4.28

EG

OSK11-04

42.0

43.0

1.0

0.69

EG

and

140.0

140.5

0.5

35.10

EG

VG

and

193.9

197.5

3.7

215.74

EG

VG

including

193.9

194.4

0.5

1570.00

EG

VG

and

205.0

206.0

1.1

2.00

EG

and

213.0

224.5

11.5

1.24

EG

VG

including

223.0

224.5

1.5

6.23

EG

and

230.3

231.5

1.2

0.58

EG

This news release has been reviewed and approved by Paul McNeill , P. Geo., VP Exploration with Anaconda Mining Inc., a “Qualified Person”, under National Instrument 43-101 Standard for Disclosure for Mineral Projects.

All samples and the resultant composites referred to in this release are collected using QA/QC protocols including the regular insertion of standards and blanks within the sample batch for analysis and check assays of select samples. All samples quoted in this release were analyzed at Eastern Analytical Ltd. in Springdale, NL , for Au by fire assay (30 g) with an AA finish.

Samples analyzing greater than 0.5 g/t Au via 30 g fire assay were re-analyzed at Eastern via total pulp metallic. For the total pulp metallic analysis, the entire sample is crushed to -10mesh and pulverized to 95% -150mesh. The total sample is then weighed and screened to 150mesh. The +150mesh fraction is fire assayed for Au, and a 30 g subsample of the -150mesh fraction analyzed via fire assay. A weighted average gold grade is calculated for the final reportable gold grade. Anaconda considers total pulp metallic analysis to be more representative than 30 g fire assay in coarse gold systems such as the Goldboro Deposit.

Reported mineralized intervals are measured from core lengths. Intervals are estimated to be approximately 80-100% of true widths.

A version of this press release will be available in French on Anaconda’s website (www.anacondamining.com) in two to three business days.

ABOUT ANACONDA

Anaconda Mining is a TSX and OTCQX-listed gold mining, development, and exploration company, focused in the prospective Atlantic Canadian jurisdictions of Newfoundland and Nova Scotia . The Company operates the Point Rousse Project located in the Baie Verte Mining District in Newfoundland , comprised of the Stog’er Tight Mine, the Pine Cove open pit mine, the Argyle Mineral Resource, the fully-permitted Pine Cove Mill and tailings facility, and approximately 10,150 hectares of prospective gold-bearing property. Anaconda is also developing the Goldboro Gold Project in Nova Scotia , a high-grade Mineral Resource, subject to a 2018 a preliminary economic assessment which demonstrates a strong project economics. The Company also has a wholly owned exploration company that is solely focused on early stage exploration in Newfoundland and New Brunswick .

FORWARD-LOOKING STATEMENTS

This news release contains “forward-looking information” within the meaning of applicable Canadian and United States securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects”, or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “does not anticipate”, or “believes” or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur”, or “be achieved”. Forward-looking information is based on the opinions and estimates of management at the date the information is made, and is based on a number of assumptions and is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Anaconda to be materially different from those expressed or implied by such forward-looking information, including risks associated with the exploration, development and mining such as economic factors as they effect exploration, future commodity prices, changes in foreign exchange and interest rates, actual results of current production, development and exploration activities, government regulation, political or economic developments, environmental risks, permitting timelines, capital expenditures, operating or technical difficulties in connection with development activities, employee relations, the speculative nature of gold exploration and development, including the risks of diminishing quantities of grades of resources, contests over title to properties, and changes in project parameters as plans continue to be refined as well as those risk factors discussed in the annual information form for the fiscal year ended December 31, 2017 , available on www.sedar.com. Although Anaconda has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. Anaconda does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

Exhibit A. A map showing the location of recent drilling and highlights from the EG Gold System at Goldboro. Four holes, drilled for metallurgical testing, pending assays are also shown (holes BR-18-68 to -71). (CNW Group/Anaconda Mining Inc.)

Exhibit B. A long section through the EG Gold System showing the location of high-grade drill intersections along a 150-metre plunge and other interpreted zones of mineralization. Further drilling is required to create a geological model of these mineralized zones. All zones remain open for expansion down plunge. (CNW Group/Anaconda Mining Inc.)

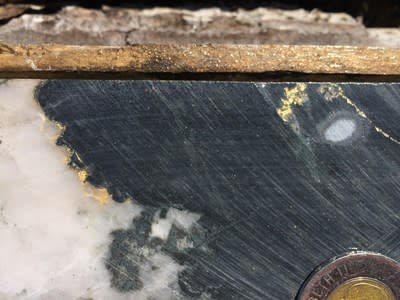

Exhibit C. A photograph of NQ core from diamond drill hole OSK-11-04 from the High-Grade Zone showing visible gold associated with a composited assay of 215.7 g/t over 3.7 metres. Canadian two-dollar coin for scale. (CNW Group/Anaconda Mining Inc.)

I’m not focused on what gold does tomorrow, or next week, or even next year. It will be what it will be. But it is my belief that there are so many unresolved issues that have to be addressed that it is highly probable that at least one or more will end up badly and that will be the spark that sets gold free to rise to a new all-time high. Among the issues are interest rates, the bond market, inflation, the economy, the stock market, the Middle East plus whatever new excitement Trump gets us involved in. Take your pick. What do you think the odds are that all of these items work out favorably? I wonder what odds Vegas would give?

Gold started the last bull market at $272 and powered all the way up to $1,900. Starting from the recent bottom at $1,174 it is not being unrealistic to expect gold to rise far above $2,000 this time. If it matches the gain from 2000 until 2008, gold would rise to $8,200. I’d be fine with just $2,000.

Silver is currently selling for about what it did 10-years ago.

David’s Commentary:

But look at the 20-year silver chart.

Silver is also turning up off major support at the $15 area and now setting up to break $20 and make the slow move up to $27.50 where major resistance sits.

This chart pattern is going to be one for the record books when it’s setup to break into new highs above $50.

David’s Commentary:

Gold and silver are insurance, not investments. Catch the bull market wave and the results can be stunning. Or heartbreaking on the way down. We’ve survived the way down and now, the metals are turning back up and just biding their time to break strongly out to the upside.

What is holding them back and how will it change? The Federal Reserve, JPMorgan and friends are holding it back. Many people think that JPMorgan is working side by side with the Fed to keep the prices in check. The government’s regulatory agencies are sitting on the sidelines and allowing massive interventions and manipulation without saying boo!

But – when one or more of the topics I mentioned in the opening unfolds and the price starts to move up rapidly, the computer-driven algorithms that buy and sell will all switch over to the buy mode, the big money hedge funds will enter the party and it will be impossible to slow down the Gold and Silver Express. They couldn’t stop it from increasing 7-fold (gold) or 10-fold (silver) from 2000 to 2011. They won’t be able to stop it this time either. All it needs is a bit of momentum to get the hedge funds buying again. They all follow the price and if gold and silver are the “go to” investments, the big money will be there in the forefront.

Kimble Charting Solutions thinks we are right on the cusp of a breakout. The mining shares traditionally lead the physical metals on the way up, and down. They are about to issue a buy signal…

Mining stocks are facing an opportunity they haven’t seen many times in the past 8-years!

This 2-pack looks at the Gold Bugs Index (HUI) and the Gold & Silver Miners (XAU) Index over the past 12-years. Since the highs in 2011, both have created a series of lower highs and lower lows along each (1) line. The counter-trend rally the past couple of months has each mining index facing long-term falling resistance at each (2).

These resistance tests have happened a few times over the past 8-years, where breakout attempts have failed. If they would do something different this time and succeed in breaking out at each (2), both should attract new buying pressure and quality rallies should follow.

What mining stocks do here is one of the most important price tests in years!

David’s Commentary:

Craig Hemke, is an analyst I follow and one whose views are very similar to mine. Here is what he has to say about the precious metals market and why he is convinced that gold and silver will reach all-time highs in the next 18 months.

The Make Believe Gold and Silver Scheme Is Going to Collapse

Was gold ever “fixed” or is the “fix” coming? We have to remember, this has been one massive experiment for the last 10-years. The Fed has been flying by the seat of their pants, and they have been ever since the market collapsed 10-years ago. The Fed began with QE-1, and that was supposed to be a one-of a kind event. That led to QE-2 and QE-3. For the past four years, they have been playing the “confidence game” – telling people that now things are just going to get back to “normal.” The interest rates are going to go back to normal, the Fed’s balance sheet is going to go back to normal, and they are playing that game to create “confidence.” We are about to find out this year and next that this was just an “experiment” and they are going to have to go back to cutting rates and they will go back to QE. The world is living off of money printing and liquidity. They can’t stop; you saw a little bit of what happened in December. They tried to stop and they tried to liquidate some of their balance sheet. The result was that the stock market plunged. The Fed had to reverse course. This is the new “normal” and this confidence scheme the Fed has been trying to implement the last four or five years is falling apart. That’s what’s driving gold. Read Full Article Here

About Miles Franklin

Miles Franklin was founded in January, 1990 by David MILES Schectman. David’s son, Andy Schectman, our CEO, joined Miles Franklin in 1991. Miles Franklin’s primary focus from 1990 through 1998 was the Swiss Annuity and we were one of the two top firms in the industry. In November, 2000, we decided to de-emphasize our focus on off-shore investing and moved primarily into gold and silver, which we felt were about to enter into a long-term bull market cycle. Our timing and our new direction proved to be the right thing to do.

We are rated A+ by the BBB with zero complaints on our record. We are recommended by many prominent newsletter writers including Doug Casey, Jim Sinclair, David Morgan, Future Money Trends and the SGT Report.

For your protection, we are licensed, regulated, bonded and background checked per Minnesota State law.