Burlington, Ontario–(Newsfile Corp. – January 23, 2024) – Silver Bullet Mines Corp. (TSXV: SBMI) (OTCQB: SBMCF) (‘SBMI’ or ‘the Company’) is pleased to announce as part of its ongoing transformation to a silver producing company, it has submitted and received approval for its mine training program from the Mine Safety and Health Association (“MSHA”), part of the United States Department of Labor. This MSHA approval covers the training program for both SBMI’s underground and surface operations. The approval process included three onsite inspections by MSHA and the completion by SBMI of a detailed safety operations program.

The field team in Arizona is currently attending the annual training program which will be completed this week, following which the field team intends to address any outstanding safety-related items, develop the silver higher-grade Zone1, and commence commercial operations.

For further information, please contact:

John Carter Silver Bullet Mines Corp., CEO cartera@sympatico.ca +1 (905) 302-3843

Peter M. Clausi Silver Bullet Mines Corp., VP Capital Markets pclausi@brantcapital.ca +1 (416) 890-1232

Cautionary and Forward-Looking Statements

This news release contains certain statements that constitute forward-looking statements as they relate to SBMI and its subsidiaries. Forward-looking statements are not historical facts but represent management’s current expectation of future events, and can be identified by words such as “believe”, “expects”, “will”, “intends”, “plans”, “projects”, “anticipates”, “estimates”, “continues” and similar expressions. Although management believes that the expectations represented in such forward-looking statements are reasonable, there can be no assurance that they will prove to be correct.

By their nature, forward-looking statements include assumptions, and are subject to inherent risks and uncertainties that could cause actual future results, conditions, actions or events to differ materially from those in the forward-looking statements. If and when forward-looking statements are set out in this new release, SBMI will also set out the material risk factors or assumptions used to develop the forward-looking statements. Except as expressly required by applicable securities laws, SBMI assumes no obligation to update or revise any forward-looking statements. The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: the impact of SARS CoV-2 or any other global virus; reliance on key personnel; the thoroughness of its QA/QA procedures; the continuity of the global supply chain for materials for SBMI to use in the production and processing of ore; shareholder and regulatory approvals; activities and attitudes of communities local to the location of the SBMI’s properties; risks of future legal proceedings; income tax matters; fires, floods and other natural phenomena; the rate of inflation; availability and terms of financing; distribution of securities; commodities pricing; currency movements, especially as between the USD and CDN; effect of market interest rates on price of securities; and, potential dilution. SARS CoV-2 and other potential global pathogens create risks that at this time are immeasurable and impossible to define.

People aren’t messing with their 401(k)s enough, according to the The Wall Street Journal. It used to be “Set it and forget it.” Now, according to the Wall Street Journal’s Jon Sindreu, if you forget it, you might miss it.

Inspired by a BlackRock thought experiment which included perfect knowledge, Sindreu looked backward between 2020 and the present at a person making yearly changes (moving funds to the previous year’s strongest sector) which would have generated a compound annual return of 55 percent, nearly four times more than buying and holding the Standard and Poor’s 500 (or setting and forgetting). For the period of 2016 through 2019, the gain would have been 30 percent, twice the index.

Basing a new strategy on back-of-the-envelope testing back just seven years seems dubious. It also requires discipline and market knowledge that the vast majority of 401(k) investors just don’t have. Most people with 401(k)s just plain have no interest in, let alone knowledge of, financial markets.

At least one company understands that its employees are not cut out to be investors. IBM, starting this year, will “provide a defined benefit plan that will save for an employee’s retirement automatically, with no contribution required from the employee. The result will be a stable and predictable benefit that professionally invests every retirement saving dollar to maximize risk-adjusted rates of return,” summarizes Teresa Ghilarducci in an article for Forbes.

Ghilarducci makes the point that small businesses may go back to defined benefit plans because “the permitted tax-qualified contributions are larger in [defined benefit] than [defined contribution].”

IBM dropped their pension plan fifteen years ago and went to a 401(k) plan. The United Auto Workers did the same, as did many other large and small companies. These moves shifted “the risk of mistakes onto the employees.”

IBM has now declared its 401(k) plan a failure, as has the Mercer/CFA Institute Global Pension Index, which flunks the US model for not “providing enough accumulation, stable investment, and reliable lifetime benefits.”

Ghilarducci says 401(k) participants are stuck with investment options that are high-priced and inefficient. Plus, what happens when that lump sum of accumulated wealth is staring a retiree in the face? Some take distributions slowly and carefully and likely will live below their means and pass what remains to their heirs. Others, however, will buy expensive toys, what Ghilarducci calls the “red truck syndrome—a term coined when newly retired workers with lumps [buy] something they have always wanted—a shiny new truck.”

Defined benefit plans are A-OK if fully funded, but many government employee defined benefit plans are not. In fact, an academic study finds there are incentives for government defined benefit plans to be underfunded. Not to give away the punchline, but government employee pensioners know it’s the law for them to be paid their pension, and the government will force taxpayers to cover any shortfall.

Another basic feature of pension politics is that public workers and their unions have incentives to support the chronic underfunding of their own pensions. Due to state statutes, constitutions, and judicial decisions, pensions promised by state politicians are backed by strong legal protections almost everywhere; and public workers thus know they will eventually get what they are promised even if their pension plans are currently underfunded. Indeed, because full funding on a regular schedule would be tremendously costly for state (and local) budgets—crowding out other services, forcing higher taxes, making the true costs of pensions painfully transparent to citizens—public workers and their unions have incentives to prefer that their pension plans be underfunded. Underfunding enables the fiscal illusion that pension benefits are much less expensive than they really are. If public workers and their unions want increasingly generous benefits in future years, they need to convince the public that these benefits are not costly to provide. At the same time, underfunding keeps employee contributions to their own pension funds at low levels; and by keeping contributions by their employers down, they are freeing up public money for other government services, keeping public workers employed—and providing funds for their own salaries and raises.

Employees in the private sector must spend time researching investment options and hope their investment selections and market timing are right. Meanwhile, government employees can relax and count on taxpayers to make their golden years stress free.

Ottawa, Ontario–(Newsfile Corp. – January 22, 2024) – Gold79 Mines Ltd. (TSXV: AUU) (OTCQB: AUSVF) (“Gold79” or the “Company”) is pleased to announce that it has defined an exploration target at the Tyro Main Zone, the first potential resource area, on the Gold Chain Project in Arizona (the “Exploration Target”).

Gold79 believes that the Tyro Main Zone has the potential for 15.6 to 31.2 Mt grading 1.5 to 2.5 g/t Au. This is based on previous exploration on the property, including 685.7 metres of drilling along with surface sampling (95 samples), sampling of historical underground workings (56 samples) and detailed mapping. The Exploration Target was derived by modeling the Tyro Vein System within the Tyro Main Zone. The volume of the modeled areas determines the potential tonnage statement in the Exploration Target. The grade range given in the Exploration Target is determined with consideration to the drill results within the modeled Exploration Target area and consideration of the geological setting in an established gold camp where mineralization typically extends to a depth of at least 300 metres. See the heading below “Tyro Main Zone Exploration Target” for additional details. The potential quantity and grades are conceptual in nature. There has been insufficient exploration drilling to define a mineral resource and it is uncertain if further exploration will result in the Exploration Target being delineated as a mineral resource.

The highlights in this update include:

To generate a potential maiden resource at the Tyro Main Zone, additional core and reverse circulation (RC) drilling is proposed along with mechanized sampling of surface vein exposures.

The Tyro Main Zone Exploration Target is limited to only 1 kilometre of the 3.4 kilometre strike length of the full Tyro vein system (Figure 4).

The initial target at the Tyro Main Zone excludes the adjacent targets identified at the historic Banner and Sheep Trail Mines (previous drilling at Banner by Gold79 returned 10.7 grams per tonne Au over 3.1 metres in drill hole GC21-08, see press release dated November 2, 2021).

The Tyro Main Zone Exploration Target also excludes the Frisco Graben to the northeast, where continuing work indicates the upper levels of a potential low sulfidation epithermal gold system over an extent of 4 kilometres.

Derek Macpherson, President and CEO stated, “In the second half of 2023, Gold79 undertook a review of all the data collected from the Company’s work at the Gold Chain project over the last 3 years. Our conclusion continues to be that the Gold Chain project has the potential to host multiple, plus million-ounce gold targets. The Tyro Main Zone represents a portion of the potential we see at the project and has become a priority for the Company given the potential to define a higher-grade open-pittable resource that would start from surface with a relatively small amount of additional exploration work.”

Mr. Macpherson continued, “This Exploration Target, if converted to a resource, would have the potential to be one of the higher-grade open-pit deposits in the camp, and has the potential to be moved into production quickly given that it is on patented claims and given the existing underutilized infrastructure in the surrounding district.”

Figure 1. Geologic map of the Katherine district and the Gold Chain project.

The Tyro Main Zone consists of the historic Tyro Mine (with production from two-levels of underground workings and a small slot pit) and the Decimal Hill area. The 1,000-metre extent considered in this Exploration Target is contained within 15.6 to 31.2 Mt grading 1.5 to 2.5 g/t Au and is located entirely on 3 patented claims controlled by Gold79.

The work completed to date by Gold79 at the Tyro Main Zone includes:

685.7 metres of RC drilling (Table 1).

95 surface rock chip samples (Figure 2).

56 chip channel samples from the underground workings (Table 2).

Detailed geologic mapping of the mine workings, patented claims and surrounding BLM claims.

Using this data, Gold79 has defined the Exploration Target over the 1,000-metre strike length of the Tyro Main Zone and down to a depth of 300 metres. The Exploration Target effectively excludes the potential high-grade zone intersected with drill hole GC23-28 (which included 9.1 metres at 51.09 grams per tonne gold, see press release dated February 28, 2023). This potential high-grade zone was excluded since it has only been intersected in one drill hole to date and would materially skew the potential grade range higher. It should be noted that similar grades in line with GC23-28 were documented to have been mined historically (pre-1940) at the Tyro underground mine.

The dimensions of the Exploration Target are based on surface sampling, detailed mapping, and drilling for strike length and width. The 300-metre depth is consistent with the depth of mineralization encountered in neighboring veins (i.e. Katherine, Arabian and the Oatman district) shown in Figure 1.

The potential quantity and grades estimated for the Tyro Main Zone Exploration Target are conceptual in nature, and there has been insufficient exploration completed to date to define a mineral resource. It is uncertain if further exploration will result in the Tyro Main Zone Exploration Target being delineated as a mineral resource.

Figure 2. Tyro Mine area geologic map showing sections, drill holes and sampling results.

Figure 3. Three-dimensional view looking north across the mineralized domain (red) of the Tyro vein system. Historical holes (black dots) and holes proposed for 2024 (blue poles).

Gold79 believes it has a unique opportunity to define a gold resource with minimal additional investment over a short period of time. Modelling of the existing database (Figure 3) has identified areas where additional exploration is needed to support a maiden inferred resource estimate. Gold79 believes that to define a maiden resource at the Tyro Main Zone to a depth of approximately 150m the following work is required.

Trenching – 24 trenches (~1,100 metres)

Core Drilling – 750 to 1,250 metres

RC Drilling – 1,500 to 2,500 metres

The planned trenching program is expected to help define widths and gold grade in mine and surface exposures. The accessible mine workings have already been sampled (Table 2). Many of the roads required for this work were constructed in the 1980s and surface access/disturbance should not require a permit. It is important to note that each step in the exploration process will define the scale required at the subsequent step.

The potential quantity and grade estimated for the Tyro Main Zone Exploration Target is conceptual in nature, and there has been insufficient exploration completed to date to define a mineral resource. It is uncertain if further exploration will result in the Tyro Main Zone Exploration Target being delineated as a mineral resource.

Table 1. Selected Intercepts from Tyro Main Zone Drilling.

Figure 5. Exploration model for low-sulfidation epithermal gold-silver vein systems illustrating vertical variations in quartz textures, structure, alteration and geochemistry along with the estimated vertical positions of the several structural segments of the Tyro vein system. Diagram adapted from: Buchanan (1980), Hollister (1985), Berger & Eimon (1983), Anaconda Corp. (1983), Guoyi (1992) and Corbett & Leach (1996).

Further Updates Planned on the Frisco Graben and North Oatman Trend

Gold79 has completed a review of the exploration data collected over the last three years at Gold Chain. Given that the upper extent of the “boiling zone” of this low sulphidation epithermal gold system is effectively at surface for the Tyro Main Zone (Figure 5), this has become Gold79’s priority exploration target at Gold Chain. However, based on this review of exploration data, Gold79 also believes that other targets at the Gold Chain project have the potential to yield large gold deposits. Besides the Tyro Vein system, discussed in our May 9, 2023 press release, the North Oatman Trend and Frisco Graben represent large scale targets, with the “bonanza zones” partially exposed or blind to the surface (Figure 5). The Company plans to provide future updates on these other large-scale targets at its Gold Chain project in northwest Arizona.

Qualified Person / Quality Control and Quality Assurance

Robert Johansing, M.Sc. Econ. Geol., P. Geo., the Company’s Vice President, Exploration is a qualified person (“QP”) as defined by NI 43-101 and has reviewed and approved the technical content of this press release. Mr. Johansing has also been responsible for all phases of drilling programs including sample collection, labelling, bagging and transport from the project to American Assay Laboratories of Sparks, Nevada. Samples were then dried, crushed and split, and pulp samples were prepared for analysis. Gold was determined by fire assay with an ICP finish, over limit samples were determined by fire assay and gravimetric finish. Silver plus 34 other elements were determined by Aqua Regia ICP-AES, over limit samples were determined by fire assay and gravimetric finish. Standard sample chain of custody procedures were employed during field work and the drilling campaigns until delivery to the analytical facility.

About Gold79 Mines Ltd.

Gold79 Mines Ltd. is a TSX Venture listed company focused on building ounces in the Southwest USA. Gold79 holds 100% earn-in option to purchase agreements on three gold projects: the Jefferson Canyon Gold Project and the Tip Top Gold Project both located in Nevada, USA, and, the Gold Chain Project located in Arizona, USA. In addition, Gold79 holds a 32.3% interest in the Greyhound Project, Nunavut, Canada under JV by Agnico Eagle Mines Limited.

For further information regarding this press release contact:

This press release may contain forward-looking statements that are made as of the date hereof and are based on current expectations, forecasts and assumptions which involve risks and uncertainties associated with our business including any future private placement financing, the uncertainty as to whether further exploration will result in the target(s) being delineated as a mineral resource, capital expenditures, operating costs, mineral resources, recovery rates, grades and prices, estimated goals, expansion and growth of the business and operations, plans and references to the Company’s future successes with its business and the economic environment in which the business operates. All such statements are made pursuant to the ‘safe harbour’ provisions of, and are intended to be forward-looking statements under, applicable Canadian securities legislation. Any statements contained herein that are statements of historical facts may be deemed to be forward-looking statements. By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties. We caution readers of this news release not to place undue reliance on our forward-looking statements as a number of factors could cause actual results or conditions to differ materially from current expectations. Please refer to the risks set forth in the Company’s most recent annual MD&A and the Company’s continuous disclosure documents that can be found on SEDAR at www.sedar.com. Gold79 does not intend, and disclaims any obligation, except as required by law, to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Edmonton, Alberta–(Newsfile Corp. – January 22, 2024) – Grizzly Discoveries Inc. (TSXV: GZD) (FSE: G6H) (OTCQB: GZDIF) (“Grizzly” or the “Company”) is pleased to announce that, on January 19, 2024, it closed on a private placement (the “Offering”) by the issuance of 2,975,500 Units (as defined below) at a price of $0.05 per Unit for gross proceeds of $148,775.

Under the terms of the Offering, each Unit consisted of one common share of the Company (“Common Share”) and one half of one warrant (“Warrant”). Each whole Warrant entitles the holder to acquire one additional Common Share at an exercise price of $0.07 per Common Share and shall expire on the earlier of: (a) 30 days following written notice by the Issuer to the Subscriber that the volume-weighted average trading price of the Common Shares on the TSX Venture Exchange is at or greater than CA$0.10 per Common Share for 10 consecutive trading days; and (b) January 19, 2026.

The Company intends to use the proceeds from the Units for general working capital.

The Common Shares and any Common Shares issued on exercise of the Warrants are subject to restrictions on trading until May 20, 2024 in accordance with the policies of the TSX Venture Exchange.

Following closing of the Offering, the Company has 152,669,619 Common Shares issued and outstanding. The Offering is subject to Final Acceptance by the TSX Venture Exchange.

ABOUT GRIZZLY DISCOVERIES INC.

Grizzly is a diversified Canadian mineral exploration company with its primary listing on the TSX Venture Exchange focused on developing its approximately 72,700 ha (approximately 180,000 acres) of precious and base metals properties in southeastern British Columbia. Grizzly is run by a highly experienced junior resource sector management team, who have a track record of advancing exploration projects from early exploration stage through to feasibility stage.

On behalf of the Board, GRIZZLY DISCOVERIES INC. Brian Testo, CEO, President

Suite 363-9768 170 Street NW Edmonton, Alberta T5T 5L4

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

North Vancouver, British Columbia–(Newsfile Corp. – January 18, 2024) – Lion One Metals Limited (TSXV: LIO) (OTCQX: LOMLF) (ASX: LLO)(“Lion One” or the “Company”) is pleased to provide an update on ongoing operations at the company’s 100% owned Tuvatu Alkaline Gold Project in Fiji.

Lion One Metals’ Chairman and CEO Walter Berukoff stated:“2023 was a year of noteworthy accomplishments for Lion One Metals. Within one year we have gone from pouring concrete to pouring gold. We built the entire processing plant at Tuvatu within one year, completed over 2,000 m of underground mine development, drilled over 40,000 m of core, completed Stage 1 of our Tailings Storage Facility, and on October 10th we celebrated with over 1,000 community members, employees, and government officials as we poured our first gold at Tuvatu. We’re very proud of our technical team’s ability to achieve these significant milestones, especially in such a short period of time.”

“In 2024 we expect another watershed year for Lion One Metals. During the 300 TPD pilot plant phase of operations we will be focusing on the development of the mine and the expansion of the processing plant to 500 TPD. We are pursuing a staged increase in development and the 300 TPD pilot plant stage is a critical step in the continuous improvement of mining and milling at Tuvatu. The knowledge and experience gained during the pilot plant stage of operations will be crucial in achieving long-term success and in optimizing performance at the 500 TPD stage. The goal for 2024 is to have the 500 TPD processing plant in operation by the end of Q3. We will then use the cash flow from our 500 TPD operations to fund the next stage of growth for Lion One, which includes the development of the 500 Zone at Tuvatu, and the advancement of our regional exploration program throughout the Navilawa Caldera, where we intend to discover and develop the next Tuvatu.”

Mine Operations

The focus of mining activities during the 300 TPD pilot plant phase of operations is the development of the underground mine, with the goal of advancing the main decline to the 500 Zone as quickly as is safely possible. A secondary goal during this phase of operations is the development of as many stope access points as feasible in advance of the plant expansion to 500 TPD. A significant portion of the material mined during the 300 TPD pilot plant phase of operations is therefore expected to be development material.

As mine development has progressed at Tuvatu, additional mineralization has been discovered in areas in Zone 2 that were not previously expected to be mineralized. This includes mineralization associated with stockwork veining as well as entirely new mineralized lodes. Many of the development headings at Tuvatu have been found to contain low-grade gold mineralization. This low-grade development material is ideal for use as feed stock to test the different gold recovery circuits during the initial stages of plant operation. Processing the development material also serves to offset costs during mine development as this material needs to be removed regardless of whether it is mineralized. Most of the mill feed during the start-up of the 300 TPD pilot plant has therefore consisted of low-grade development material. The first production material was extracted on December 13th, 2023, from the URW1 leading edge stope in Zone 2. This stope is located outside the original PEA resource and represents an expansion of the resource.

Mining activities at Tuvatu in 2024 will consist of a mix of handheld and mechanized mining methods. Handheld mining is ideal for narrow vein mining as it is precise and enables the effective development of narrow drives, thereby minimizing dilution. Mechanized mining produces wider voids and results in a considerably higher production rate. It is therefore the preferred alternative for wider zones of mineralization that are not sensitive to dilution. At Tuvatu there are areas more suitable for handheld mining and others more suitable for mechanized mining. The mining method employed will be tailored to the style of mineralization being extracted. Mine development is proceeding in a manner designed to preserve the optionality of switching between mining methods as appropriate. To date, development mining at Tuvatu has progressed using both handheld and mechanized mining, yet production mining has been limited to handheld methods. Mechanized production is scheduled to start in Q1 2024. Production mining refers to the mining of production stopes through which most of the mineralized material will be extracted, whereas development mining refers to all the supporting development required to access the production stopes, such as the declines, access drives, crosscuts, ventilation rises, and so on. While the primary mining objective during the 300 TPD pilot plant stage is development, mine production is anticipated to steadily increase as production mining is introduced and as the number of available production areas increases ahead of the plant expansion to 500 TPD.

Mill Operations

The focus of mill operations during the 300 TPD pilot plant stage is on determining the best methods and parameters required to maximize gold recovery from each type of gold mineralization at Tuvatu. Mill operations to date have consisted of a start-up period and a campaign period with feed from different areas within Zone 2 and Zone 5.

During the start-up period of operations from late October to early December 2023, predominantly low-grade material was put through the mill. This is typical of mill start-ups and is done while identifying and resolving any start-up issues that may be present before ramping up production. It also serves to build the in-process store of gold that is retained within the plant. During the subsequent campaign periods of operation, the focus changed to the metallurgical variability of the gold mineralization. Several different types of mineralization have been identified at Tuvatu, including three different types within Zone 2 and Zone 5. Due to the complexity of the deposit, additional variability in mineralization is anticipated as development progresses deeper into the mine. The campaign period of operations, which began in mid-December, has consisted of processing separate batches of material from specific parts of Zone 2 and Zone 5 to determine how the plant responds in each case. The knowledge gained from these campaigns will be applied to maximize gold recovery from the larger production stopes in these areas. Gold recovery rates during the start-up and campaign periods have been in line with expectations.

In addition to the start-up and campaign activities, mill commissioning and upgrading has been carried out. Commissioning of both the continuous gravity concentrator and the intensive leach circuit has been on hold due to a delayed shipment of component parts from suppliers. Both circuits are expected to be brought on-line by early February. Similarly, the blowers supplied to aerate the CIL tanks and cyanide detoxification circuit were found to be undersized by the supplier. New blowers will be installed, along with new air spargers and diffusion cones to improve the performance of the CIL circuit.

The mill expansion to 500 TPD is scheduled to be complete by the end of Q3 2024. The expansion consists of three main components: a tower mill, a flotation circuit, and a third ball mill. The purpose of the tower mill is to produce a finer grind of concentrates from the continuous gravity concentrator, thereby further increasing recoveries. The tower mill is expected to be on site in February. The flotation circuit is also being added to maximize recoveries, while the third ball mill is required to increase the milling capacity of the plant. Site preparations for both the flotation circuit and the third ball mill are already complete and construction is pending. All three mill components are on schedule for completion and commissioning by the end of Q3 2024, which is a year ahead of the originally scheduled completion date of Q3 2025.

Figure 1. Aerial Views of Tuvatu Processing Plant and Mine Portal, December 2022 and January 2024. Top image: Aerial view in December 2022 shortly after plant construction started. Bottom image: Aerial view in January 2024 after construction is complete and the 300 TPD pilot plant is in operation. These views highlight some of the substantial progress made at Tuvatu throughout 2023.

The Company also announces it has granted stock options pursuant to its 10% rolling stock option plan to an officer of the Company to purchase up to an aggregate of 500,000 common shares of the Company. The stock options are exercisable at $1.00 per share and expire 5 years from the date of grant.

Qualified Person (NI43-101)

In accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43- 101”), Alex Nichol, MAIG, VP Geology and Exploration, is the Qualified Person for the Company, and has reviewed, validated, and approved the technical and scientific content of this news release.

About Lion One Metals Limited Lion One Metals is an emerging Canadian gold producer headquartered in North Vancouver BC, with new operations established in late 2023 at its 100% owned Tuvatu Alkaline Gold Project in Fiji. The Tuvatu project comprises the high-grade Tuvatu Alkaline Gold Deposit, the Underground Gold Mine, the Pilot Plant, and the Assay Lab. The Company also has an extensive exploration license covering the entire Navilawa Caldera, which is host to multiple mineralized zones and highly prospective exploration targets.

As disclosed in its “Technical Report and PEA Update for the Tuvatu Gold Project” dated April 29, 2022, the 2018 Tuvatu resource estimate comprises 1,007,000 tonnes indicated at 8.50 g/t Au (274,600 oz. Au) and 1,325,000 tonnes inferred at 9.0 g/t Au (384,000 oz. Au) at a cut-off grade of 3.0 g/t Au. The technical report is available on the Lion One website at www.liononemetals.com and under the Lion One profile on the SEDAR+ website at www.sedarplus.ca.

On behalf of the Board of Directors, Walter Berukoff, Chairman & CEO

Neither the TSX-V nor its Regulation Service Provider accepts responsibility or the adequacy or accuracy of this release

This press release may contain statements that may be deemed to be “forward-looking statements” within the meaning of applicable Canadian securities legislation. All statements, other than statements of historical fact, included herein are forward-looking information. Generally, forward-looking information may be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “proposed”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases, or by the use of words or phrases which state that certain actions, events or results may, could, would, or might occur or be achieved. This forward-looking information reflects Lion One Metals Limited’s current beliefs and is based on information currently available to Lion One Metals Limited and on assumptions Lion One Metals Limited believes are reasonable. These assumptions include, but are not limited to, the actual results of exploration projects being equivalent to or better than estimated results in technical reports, assessment reports, and other geological reports or prior exploration results. Forward-Looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance, or achievements of Lion One Metals Limited or its subsidiaries to be materially different from those expressed or implied by such forward-looking information. Such risks and other factors may include, but are not limited to: the stage development of Lion One Metals Limited, general business, economic, competitive, political and social uncertainties; the actual results of current research and development or operational activities; competition; uncertainty as to patent applications and intellectual property rights; product liability and lack of insurance; delay or failure to receive board or regulatory approvals; changes in legislation, including environmental legislation, affecting mining, timing and availability of external financing on acceptable terms; not realizing on the potential benefits of technology; conclusions of economic evaluations; and lack of qualified, skilled labor or loss of key individuals. Although Lion One Metals Limited has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated, or intended. Accordingly, readers should not place undue reliance on forward-looking information. Lion One Metals Limited does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

MONTREAL, Jan. 18, 2024 /CNW/ – Aya Gold & Silver Inc. (TSX: AYA) (OTCQX: AYASF) (“Aya” or the “Corporation”) is pleased to announce new high-grade drill exploration results from its 2023 completed program of 76,000 meters at Boumadine in the Kingdom of Morocco. The new results confirm the large, high-grade mineralized zones in the southern and northern portions of the Main Trend, which remains open in all directions.

Key Highlights1

Definition of new high-grade mineralization from the infill drilling program:

BOU-DD23-223 intersected 763 grams per tonne (“g/t”) silver equivalent (“AgEq”) over 38.3 meters (“m”) (1.53 g/t Au, 311 g/t Ag, 4.4% Zn, 1.8% Pb and 0.04% Cu), including 11.0m at 996 g/t AgEq

BOU-DD23-230 intersected 991 g/t AgEq over 17.6m (2.64 g/t Au, 247 g/t Ag, 7.7% Zn, 1.2% Pb and 0.3% Cu), including 3.7m at 1,662 g/t AgEq

BOU-DD23-248 intersected 1,136 g/t AgEq over 5.9m (5.94 g/t Au, 59 g/t Ag, 8.8% Zn, 1.0% Pb and 0.1% Cu)

BOU-DD23-220 intersected 575 g/t AgEq over 10.9m (1.77 g/t Au, 91 g/t Ag, 4.5% Zn, 1.7% Pb and 0.1% Cu), including 2.4m at 1,275 g/t AgEq

BOU-DD23-218 intersected 1,409 g/t AgEq over 4.2m (13.59 g/t Au, 115 g/t Ag, 0.1% Zn, 0.1% Pb and 0.1% Cu) and 978 g/t AgEq over 5.8m (9.21 g/t Au, 80 g/t Ag, 0.1% Zn, 0.1% Pb and 0.2% Cu)

BOU-DD23-251 intersected 531 g/t AgEq over 9.4m (2.66 g/t Au, 32 g/t Ag, 4.4% Zn, 0.2% Pb and 0.04% Cu), including 2.4m at 1,719 g/t AgEq

“Today’s high-grade drill results including BOU-DD23-223 in the south and BOU-DD23-218 in the north of the Main Trend confirm continuity and grade of the Main Trend at Boumadine,” said Benoit La Salle, President & CEO. “Infill drilling has decreased the spacings between drill holes to improve our confidence in grades and tonnages for the upcoming Q1-2024 mineral resource estimate, which will provide visibility on Boumadine’s potential for near-term value creation.”

______________________________

1All intersections are in core lengths; Ag equivalent is based on a 100% recovery with the following ratios: 1g/t Au: 93.4 g/t Ag; 1% Cu: 130.4 g/t Ag; 1% Pb: 31.8 g/t Ag; 1% Zn: 54.1 g/t Ag

Table 1 – Significant Intercepts from Boumadine Drill Exploration Program (Core Lengths)

DDH No.

Section

Zone

From (m)

To (m)

Au (g/t)

Ag (g/t)

Length* (m)

Cu (%)

Pb (%)

Zn (%)

Mo (g/t)

Ag Eq** (g/t)

BOU-DD23-208

6675N

Main

129.9

139.4

1.60

35

9.5

0.2

0.1

0.4

35

231

Including

134.9

139.4

2.51

59

4.5

0.3

0.1

0.5

55

367

BOU-DD23-211

9150N

Main

6.0

9.8

2.01

99

3.8

0.0

4.3

0.0

17

426

BOU-DD23-214

8850N

Main

214.0

223.0

4.77

61

9.0

0.1

0.1

0.2

5

535

Including

216.2

221.5

6.61

90

5.3

0.2

0.1

0.3

6

749

BOU-DD23-218

8850N

Para

244.3

247.5

14.72

19

3.2

0.0

0.2

0.1

4

1,411

BOU-DD23-218

8850N

Para

252.6

256.8

13.59

115

4.2

0.1

0.1

0.1

3

1,409

BOU-DD23-218

8850N

Para

261.2

275.1

1.22

30

13.9

0.0

0.0

0.1

5

153

Including

272.3

274.0

5.89

119

1.7

0.2

0.1

0.1

13

698

BOU-DD23-218

8850N

Main

280.3

286.1

9.21

80

5.8

0.2

0.1

0.1

8

978

Including

280.3

284.3

13.05

108

4.0

0.3

0.1

0.2

8

1,377

BOU-DD23-218

8850N

Para

290.0

302.0

1.98

58

12.0

0.1

0.1

0.2

8

265

Including

292.1

297.4

3.50

107

5.3

0.1

0.1

0.1

11

459

BOU-DD23-218

8850N

Para

333.1

334.3

0.03

1026

1.2

0.0

0.0

0.0

1

1,031

BOU-DD23-220

6575N

Main

105.0

115.9

1.77

91

10.9

0.1

1.7

4.5

133

575

Including

112.3

114.7

6.26

261

2.4

0.3

1.2

6.6

16

1,275

BOU-DD23-220

6575N

Para

133.4

136.8

0.89

76

3.4

0.3

2.5

7.0

7

649

BOU-DD23-221

6575N

Main

225.5

239.0

1.07

12

13.5

0.0

0.2

0.3

4

136

BOU-DD23-223

6525N

Main

131.6

169.9

1.53

311

38.3

0.0

1.8

4.4

101

763

Including

144.9

155.9

2.34

494

11.0

0.1

1.9

3.9

36

996

BOU-DD23-223

6525N

Para

239.5

247.0

0.46

94

7.5

0.0

0.2

0.7

35

192

BOU-DD23-225

9325N

Para

47.4

53.7

1.44

54

6.3

0.0

0.9

5.3

12

508

Including

50.8

53.7

2.88

86

2.9

0.0

1.0

9.9

21

927

BOU-DD23-225

9325N

Main

73.2

77.4

2.70

21

4.2

0.1

0.3

3.2

16

465

Including

75.2

77.4

4.72

31

2.2

0.1

0.3

4.5

16

738

BOU-DD23-226

9325N

Main

182.8

186.7

1.26

35

3.9

0.1

1.5

4.7

8

466

Including

184.5

185.7

3.33

53

1.2

0.1

1.8

9.5

14

951

BOU-DD23-226

9325N

Para

197.0

198.1

7.73

47

1.1

0.3

0.5

0.5

8

852

BOU-DD23-227

9325N

Main

259.7

268.3

3.34

18

8.6

0.1

0.1

0.5

6

369

Including

263.5

268.3

5.42

21

4.8

0.1

0.1

0.1

7

545

BOU-DD23-228

6300N

Main

267.2

276.1

1.99

81

8.9

0.0

1.0

3.4

59

488

Including

267.7

273.0

3.09

119

5.3

0.0

1.5

4.7

87

715

BOU-DD23-229

6525N

Para

111.9

116.0

1.60

175

4.1

0.1

1.9

7.3

259

810

BOU-DD23-230

6575N

Main

166.6

184.2

2.64

247

17.6

0.3

1.2

7.7

86

991

Including

177.6

181.3

2.91

651

3.7

0.1

3.2

11.5

106

1,662

BOU-DD23-230

6575N

Para

188.2

202.3

2.78

97

14.1

0.2

0.4

6.5

31

755

BOU-DD23-231

5375N

Main

582.0

585.7

0.96

110

3.7

0.0

0.6

2.4

339

371

BOU-DD23-232

7825N

Main

426.4

431.8

3.91

18

5.4

0.1

0.1

0.1

2

402

Including

426.4

427.7

10.72

49

1.3

0.2

0.1

0.2

2

1,092

BOU-DD23-234

6575N

Main

310.6

317.3

1.40

19

6.7

0.1

0.3

4.5

1

407

Including

315.0

316.3

4.78

41

1.3

0.2

0.4

18.4

2

1,518

BOU-DD23-238

7825N

Para

216.0

217.8

1.59

47

1.8

0.1

3.7

3.5

10

517

BOU-DD23-244

6450N

Para

64.0

70.4

1.06

49

6.4

0.0

0.7

2.0

131

287

BOU-DD23-244

6450N

Para

112.8

120.6

0.71

62

7.8

0.0

0.2

1.3

196

216

BOU-DD23-244

6450N

Para

134.6

145.4

0.41

41

10.8

0.0

0.8

1.2

361

190

BOU-DD23-244

6450N

Main

148.5

155.1

0.52

56

6.6

0.0

0.9

2.6

298

295

Including

150.5

152.1

1.19

187

1.6

0.0

2.5

9.0

946

925

BOU-DD23-245

6450N

Para

106.0

111.0

0.05

17

5.0

1.5

0.4

1.5

70

312

BOU-DD23-245

6450N

Main

198.4

206.5

0.73

122

8.1

0.0

2.3

4.7

68

524

Including

198.4

200.2

1.83

299

1.8

0.1

4.8

13.1

269

1,355

BOU-DD23-245

6450N

Para

217.5

226.5

0.86

6

9.0

0.0

0.3

0.3

2

112

BOU-DD23-248

6450N

Main

329.5

335.4

5.94

59

5.9

0.1

1.0

8.8

23

1,136

BOU-DD23-249

5800N

Main

598.7

601.8

4.19

48

3.1

0.1

0.1

2.5

12

587

BOU-DD23-249

5800N

Para

693.1

695.5

2.18

57

2.4

0.0

0.7

7.3

10

680

BOU-DD23-250

5800N

Para

236.7

239.7

3.34

1

3.0

0.0

0.0

0.0

5

316

BOU-DD23-250

5800N

Main

377.7

384.0

1.44

49

6.3…

0.1

0.1

0.5

12

225

BOU-DD23-250

5800N

Para

448.8

455.5

1.02

25

6.7

0.1

0.1

0.4

12

155

BOU-DD23-251

6450N

Main

345.9

355.3

2.66

32

9.4

0.0

0.2

4.4

14

531

Including

346.4

348.8

7.99

91

2.4

0.1

0.3

15.8

19

1,719

BOU-DD23-254

7650N

Main

241.4

243.4

5.63

61

2.0

0.3

0.2

1.4

6

703

* True width remains undetermined at this stage; all values are uncut.

** Ag equivalent is based on a 100% recovery with the following ratio: 1 g/t Au: 93.4 g/t Ag; 1% Cu:130.4 Ag; 1% Pb: 31.8 Ag;

1% Zn: 54.1 Ag.

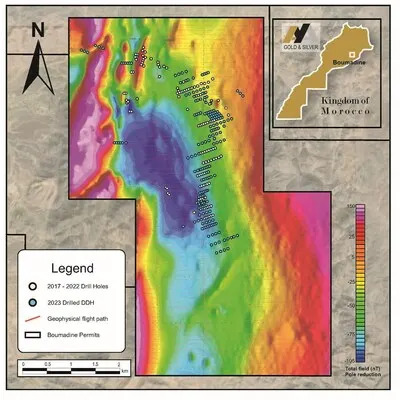

Figure 1 – Surface Plan of Boumadine Property with Magnetic Data (Residual Total Field) and 2023 Drill Holes (CNW Group/Aya Gold & Silver Inc)

2023 Exploration Results

For 2023, 197 diamond drill holes (“DDH”) for 74,295m were completed at Boumadine (Figure 1 and Appendix 2) with the remaining meterage of the 76,000m were completed in the first week of January 2024. Infill drilling was conducted on strike along the Main Trend (South, Central, and North Zones) while exploration drilling also targeted the North-West, Tizi and North-East Zones.

The majority of results have been received for drill holes up to BOU-DD23-255 (Table 1, Figure 3, Figure 4, and Appendix 1).

Results received since November 2023 confirm the high grade of the southern infill sections of the Main Trend, notably with holes BOU-DD23-223 and BOU-DD23-230 intersecting large, mineralized zones.

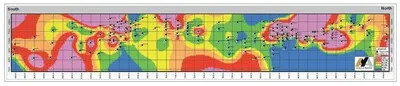

The main mineralization generally consists of 1m to 4m wide (locally reaching over a 10m width) N340- oriented massive sulphide lenses/veins sharply dipping eastward (> 70°). The massive sulphide veins (>80%) are mainly composed of pyrite, with variable proportions of sphalerite, galena, and chalcopyrite. Figure 3 presents the results of the Boumadine Main Zone on a longitudinal section along the deposit, defining ore shoots shallowly dipping toward south, in both the Central and South Zones.

Figure 2 – Longitudinal View of Boumadine Main Zone (CNW Group/Aya Gold & Silver Inc)

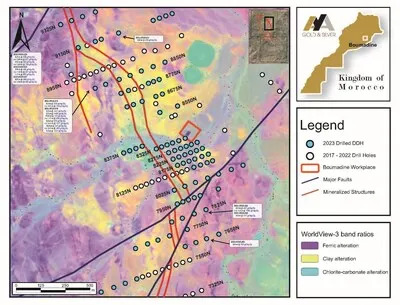

Figure 3 – Surface Plan of Central & North Zones with New 2023 DDH Results (CNW Group/Aya Gold & Silver Inc)

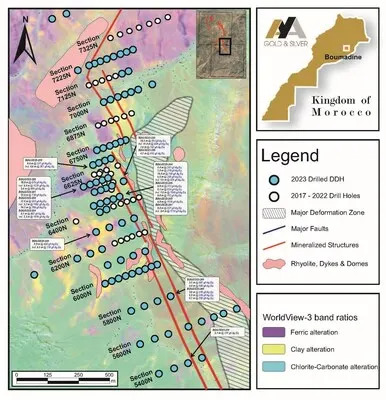

Figure 4 – Surface Plan of South Zones with New 2023 DDH Results (CNW Group/Aya Gold & Silver Inc)

Aya Gold & Silver Inc logo (CNW Group/Aya Gold & Silver Inc)

Next Steps

Following completion of the 2023 drilling program, the Corporation expects to publish an NI 43-101 compliant resource by the end of Q1-2024.

The 2024 drill program is already underway, a portion of which will continue extending the strike-length of the Boumadine Main Trend but with a primary focus on exploring targets outside of the Main Trend. Final numbers will be announced later in Q1.

Fieldwork commenced on the new permits in 2024 with a hyperspectral survey, mapping and prospecting. High resolution airborne geophysics (magnetics and MobileMT) is expected to begin later in Q1.

Technical Information

Aya has implemented a quality control program to comply with best practices in sampling and analysis of drill core. Drill core samples were transported in sealed bags for analysis at Afrilab laboratory in Marrakech. Standards of different grades and blanks were inserted every 20 samples in addition to the standards, blanks and pulp duplicate inserted by Afrilab.

Qualified Person

The scientific and technical information contained in this press release have been reviewed by David Lalonde, B. Sc, Head of Exploration, Qualified Person, for accuracy and compliance with National Instrument 43-101.

About Aya Gold & Silver Inc.

Aya Gold & Silver Inc. is a rapidly growing, Canada-based silver producer with operations in the Kingdom of Morocco.

The only TSX-listed pure silver mining company, Aya operates the high-grade Zgounder Silver Mine and is exploring its properties along the prospective South-Atlas Fault, several of which have hosted past-producing mines and historical resources. Aya’s Moroccan mining assets are complemented by its Tijirit Gold Project in Mauritania, which is being advanced to feasibility.

Aya’s management team maximizes shareholder value by anchoring sustainability at the heart of its production, resource, governance, and financial growth plans.

Forward-Looking Statements

This press release contains certain statements that constitute forward-looking information within the meaning of applicable securities laws (“forward-looking statements”), which reflects management’s expectations regarding Aya’s future growth and business prospects (including the timing and development of new deposits and the success of exploration activities) and other opportunities. Wherever possible, words such as “confirm”, “remains”, “confidence”, “potential”, “complete”, “expect” “extend”, “belief”, and similar expressions or statements that certain actions, events or results “may”, “could”, “would”, “might”, “will”, or are “likely” to be taken, occur or be achieved, have been used to identify such forward-looking information. Specific forward-looking statements in this press release include, but are not limited to, statements and information with respect to the exploration and development potential of Boumadine and the advancement of and success of the exploration program at Boumadine , and timing for the release of the Company’s disclosure in connection with the foregoing. Although the forward-looking information contained in this press release reflect management’s current beliefs based upon information currently available to management and based upon what management believes to be reasonable assumptions, Aya cannot be certain that actual results will be consistent with such forward-looking information. Such forward-looking statements are based upon assumptions, opinions and analysis made by management in light of its experience, current conditions, and its expectations of future developments that management believe to be reasonable and relevant but that may prove to be incorrect. These assumptions include, among other things, the ability to obtain any requisite governmental approvals, the accuracy of Mineral Reserve and Mineral Resource Estimates (including, but not limited to, ore tonnage and ore grade estimates), silver price, exchange rates, fuel and energy costs, future economic conditions, anticipated future estimates of free cash flow, and courses of action. Aya cautions you not to place undue reliance upon any such forward-looking statements.

The risks and uncertainties that may affect forward-looking statements include, among others: the inherent risks involved in exploration and development of mineral properties, including government approvals and permitting, changes in economic conditions, changes in the worldwide price of silver and other key inputs, changes in mine plans (including, but not limited to, throughput and recoveries being affected by metallurgical characteristics) and other factors, such as project execution delays, many of which are beyond the control of Aya, as well as other risks and uncertainties which are more fully described in Aya’s 2022 Annual Information Form dated March 31, 2023, and in other filings of Aya with securities and regulatory authorities which are available on SEDAR at www.sedarplus.ca. Furthermore, Aya’s corporate update of May 28, 2020 regarding the materiality of its assets as well as to studies regarding non-material assets remains applicable as at the date hereof. Aya does not undertake any obligation to update forward-looking statements should assumptions related to these plans, estimates, projections, beliefs, and opinions change. Nothing in this document should be construed as either an offer to sell or a solicitation to buy or sell Aya securities. All references to Aya include its subsidiaries unless the context requires otherwise.

Appendix 1 – Full Drill Results from Boumadine (core lengths)

DDH No.

Section

Zone

From (m)

To (m)

Au (g/t)

Ag (g/t)

Length* (m)

Cu (%)

Pb (%)

Zn (%)

Mo (g/t)

Ag Eq** (g/t)

BOU-DD23-170

8025N

Para

8.5

9.6

0.27

45

1.1

0.0

0.0

0.8

1

118

BOU-DD23-199

8275N

Para

28.6

29.1

0.22

35

0.5

0.0

0.2

0.4

7

84

BOU-DD23-199

8275N

Para

124.2

125.4

0.25

32

1.2

0.0

0.7

0.4

1

100

BOU-DD23-199

8275N

Para

154.9

155.5

0.81

51

0.6

0.0

0.5

6.2

5

481

BOU-DD23-199

8275N

Para

222.1

224.3

1.38

21

2.2

0.0

0.5

1.0

6

222

BOU-DD23-199

8275N

Main

255.0

255.8

0.19

12

0.8

0.0

0.5

1.0

235

112

BOU-DD23-199

8275N

Para

340.6

341.3

1.99

23

0.7

0.1

0.3

0.6

4

260

BOU-DD23-199

8275N

Para

365.6

366.1

0.33

40

0.5

0.0

0.6

1.2

5

154

BOU-DD23-199

8275N

Para

380.6

382.8

1.83

25

2.2

0.0

0.2

3.3

11

383

BOU-DD23-199

8275N

Para

436.8

437.4

0.76

16

0.6

0.0

0.1

1.6

8

180

BOU-DD23-199

8275N

Para

441.4

442.0

0.70

32

0.6

0.0

0.3

2.7

12

255

BOU-DD23-204

8375N

Para

7.8

9.0

0.59

32

1.2

0.0

0.3

0.5

7

127

BOU-DD23-204

8375N

Para

74.2

74.8

1.19

28

0.6

0.0

0.4

0.9

12

203

BOU-DD23-204

8375N

Para

367.2

368.5

0.54

16

1.3

0.1

0.2

0.3

1

97

BOU-DD23-204

8375N

Main

373.8

375.0

1.92

68

1.2

0.3

0.2

0.6

1

323

BOU-DD23-204

8375N

Para

428.3

429.9

2.38

79

1.6

0.3

0.9

1.6

3

460

BOU-DD23-205

8850N

Main

118.7

120.2

0.20

60

1.5

0.0

2.4

4.8

15

422

BOU-DD23-205

8850N

Para

415.0

415.9

0.56

24

0.9

0.0

0.1

0.1

10

85

BOU-DD23-206

6100N

NSR

0.0

207.0

0.00

0

207.0

0.0

0.0

0.0

0

0

BOU-DD23-207

6675N

Para

64.4

65.4

0.74

16

1.0

0.0

0.1

0.1

12

92

BOU-DD23-207

6675N

Para

68.4

69.6

0.73

8

1.2

0.0

0.1

0.2

8

89

BOU-DD23-207

6675N

Main

76.1

78.0

0.28

44

1.9

0.1

0.1

0.1

4

89

BOU-DD23-207

6675N

Para

92.4

93.1

0.44

19

0.7

0.1

0.1

0.1

7

80

BOU-DD23-207

6675N

Para

95.9

96.4

0.21

32

0.5

0.1

0.3

0.2

4

86

BOU-DD23-207

6675N

Para

146.5

148.7

1.36

27

2.2

0.0

0.6

1.3

27

249

BOU-DD23-207

6675N

Para

356.4

358.1

0.70

8

1.7

0.0

0.1

0.0

2

78

BOU-DD23-207

6675N

Para

360.8

362.7

0.83

1

1.9

0.0

0.0

0.0

6

82

BOU-DD23-207

6675N

Para

365.1

365.8

0.47

20

0.7

0.0

0.1

0.0

7

71

BOU-DD23-207

6675N

Para

367.9

369.0

0.66

48

1.1

0.0

1.4

0.7

5

192

BOU-DD23-207

6675N

Para

370.0

370.6

0.42

33

0.6

0.0

0.4

2.9

5

244

BOU-DD23-207

6675N

Para

417.8

418.4

0.18

60

0.6

0.0

0.7

1.2

198

173

BOU-DD23-207

6675N

Para

449.2

449.8

0.56

32

0.6

0.0

0.3

0.5

1

124

BOU-DD23-208

6675N

Para

119.4

120.4

1.42

29

1.0

0.1

0.2

0.1

5

190

BOU-DD23-208

6675N

Para

125.8

126.8

0.65

28

1.0

0.0

0.0

0.7

3

132

BOU-DD23-208

6675N

Main

129.9

139.4

1.60

35

9.5

0.2

0.1

0.4

35

231

Including

134.9

139.4

2.51

59

4.5

0.3

0.1

0.5

55

367

BOU-DD23-208

6675N

Para

239.0

243.5

0.51

9

4.5

0.0

0.0

0.1

7

66

BOU-DD23-208

6675N

Para

247.5

248.5

0.69

4

1.0

0.0

0.0

0.0

2

72

BOU-DD23-208

6675N

Para

250.5

252.1

0.65

9

1.6

0.0

0.0

0.1

5

76

BOU-DD23-209

6100N

Para

163.3

165.6

0.69

36

2.3

0.0

0.0

0.0

23

107

BOU-DD23-209

6100N

Main

170.5

171.3

1.77

65

0.8

0.1

0.1

0.3

35

258

BOU-DD23-209

6100N

Para

173.7

174.2

1.68

39

0.5

0.0

0.1

0.2

31

214

BOU-DD23-209

6100N

Para

213.5

217.5

0.34

72

4.0

0.0

0.9

0.8

57

180

BOU-DD23-209

6100N

Para

240.0

240.5

0.21

36

0.5

0.0

0.3

4.6

1

316

BOU-DD23-210

6100N

Para

221.8

222.8

0.63

8

1.0

0.0

0.0

0.0

64

73

BOU-DD23-210

6100N

Main

390.6

391.6

0.11

4

1.0

0.0

0.0

0.0

7

18

BOU-DD23-210

6100N

Para

575.6

576.2

0.33

16

0.6

0.0

0.1

0.1

2

56

BOU-DD23-210

6100N

Para

580.3

581.4

0.67

4

1.1

0.0

0.0

0.0

1

68

BOU-DD23-210

6100N

Para

585.6

586.6

0.55

8

1.0

0.0

0.0

0.0

1

62

BOU-DD23-211

9150N

Main

6.0

9.8

2.01

99

3.8

0.0

4.3

0.0

17

426

BOU-DD23-211

9150N

Para

18.0

18.8

0.96

44

0.8

0.0

0.3

0.0

13

147

BOU-DD23-211

9150N

Para

103.8

104.9

0.03

65

1.1

0.0

0.3

0.3

3

95

BOU-DD23-211

9150N

Para

140.6

143.0

1.20

26

2.4

0.0

0.2

1.0

6

200

BOU-DD23-212

6675N

Main

182.4

183.4

0.99

13

1.0

0.0

1.3

0.6

11

181

BOU-DD23-212

6675N

Para

189.4

190.3

0.03

61

0.9

0.1

0.1

0.6

21

109

BOU-DD23-213

6675N

Main

270.4

271.5

0.03

66

1.1

0.1

0.0

0.0

2

77

BOU-DD23-214

8850N

Para

146.6

147.6

0.97

12

1.0

0.0

0.3

0.5

23

143

BOU-DD23-214

8850N

Para

200.2

201.2

0.14

60

1.0

0.1

0.1

0.1

8

88

BOU-DD23-214

8850N

Main

214.0

223.0

4.77

61

9.0

0.1

0.1

0.2

5

535

Including

216.2

221.5

6.61

90

5.3

0.2

0.1

0.3

6

749

BOU-DD23-214

8850N

Para

224.0

226.0

0.52

10

2.0

0.0

0.0

0.3

5

76

BOU-DD23-214

8850N

Para

228.9

229.4

2.13

56

0.5

0.1

0.4

5.3

25

571

BOU-DD23-215

9150N

Para

39.6

40.8

0.48

20

1.2

0.0

0.2

1.0

12

125

BOU-DD23-215

9150N

Main

179.9

181.0

0.35

1

1.1

0.0

0.1

0.5

6

66

BOU-DD23-215

9150N

Para

276.8

277.6

0.46

24

0.8

0.0

0.3

0.2

3

88

BOU-DD23-215

9150N

Para

280.1

280.7

0.54

39

0.6

0.0

0.1

0.1

1

100

BOU-DD23-215

9150N

Para

294.8

297.6

1.38

22

2.8

0.0

0.5

0.9

5

217

BOU-DD23-215

9150N

Para

307.3

308.2

1.31

29

0.9

0.0

0.1

0.0

8

155

BOU-DD23-216

6100N

Para

296.0

297.2

0.59

4

1.2

0.0

0.0

0.0

1

62

BOU-DD23-216

6100N

Para

299.6

300.8

0.47

4

1.2

0.0

0.0

0.0

1

50

BOU-DD23-216

6100N

Main

483.1

485.5

1.25

32

2.4

0.2

0.3

0.1

22

194

BOU-DD23-216

6100N

Para

531.9

532.4

0.94

60

0.5

0.1

5.2

1.3

3

390

BOU-DD23-216

6100N

Para

559.0

559.8

0.51

16

0.8

0.2

0.3

0.3

10

110

BOU-DD23-217

9150N

Para

47.2

48.4

0.64

8

1.2

0.0

0.1

0.2

7

83

BOU-DD23-217

9150N

Para

220.4

220.9

1.03

39

0.5

0.1

0.6

7.8

19

593

BOU-DD23-217

9150N

Para

226.6

227.8

0.94

49

1.2

0.0

0.1

0.6

18

174

BOU-DD23-217

9150N

Main

232.9

233.5

6.92

58

0.6

0.1

1.0

2.8

7

895

BOU-DD23-217

9150N

Para

310.8

312.2

1.49

66

1.4

0.0

0.1

0.0

6

214

BOU-DD23-217

9150N

Para

313.2

314.3

0.25

24

1.1

0.0

0.1

0.0

1

55

BOU-DD23-217

9150N

Para

327.5

328.0

2.02

96

0.5

0.0

1.1

3.3

5

502

BOU-DD23-217

9150N

Para

337.3

337.8

1.28

84

0.5

0.0

0.1

0.0

9

211

BOU-DD23-218

8850N

Para

226.3

227.1

0.86

13

0.8

0.0

0.4

2.2

1

226

BOU-DD23-218

8850N

Para

238.6

239.7

0.57

12

1.1

0.0

0.1

0.4

5

91

BOU-DD23-218

8850N

Para

244.3

247.5

14.72

19

3.2

0.0

0.2

0.1

4

1,411

BOU-DD23-218

8850N

Para

250.6

251.6

0.53

8

1.0

0.0

0.0

0.3

1

76

BOU-DD23-218

8850N

Para

252.6

256.8

13.59

115

4.2

0.1

0.1

0.1

3

1,409

BOU-DD23-218

8850N

Para

257.8

258.7

0.43

28

0.9

0.0

0.1

0.1

8

78

BOU-DD23-218

8850N

Para

261.2

275.1

1.22

30

13.9

0.0

0.0

0.1

5

153

Including

272.3

274.0

5.89

119

1.7

0.2

0.1

0.1

13

698

BOU-DD23-218

8850N

Main

280.3

286.1

9.21

80

5.8

0.2

0.1

0.1

8

978

Including

280.3

284.3

13.05

108

4.0

0.3

0.1

0.2

8

1,377

BOU-DD23-218

8850N

Para

290.0

302.0

1.98

58

12.0

0.1

0.1

0.2

8

265

Including

292.1

297.4

3.50

107

5.3

0.1

0.1

0.1

11

459

BOU-DD23-218

8850N

Para

303.0

304.0

0.38

12

1.0

0.0

0.0

0.6

8

82

BOU-DD23-218

8850N

Para

333.1

334.3

0.03

1026

1.2

0.0

0.0

0.0

1

1,031

BOU-DD23-219

9150N

Para

278.6

279.1

0.42

44

0.5

0.0

0.4

0.1

9

103

BOU-DD23-219

9150N

Para

281.1

282.2

1.78

33

1.1

0.1

0.3

1.2

1

282

BOU-DD23-219

9150N

Para

286.3

288.4

1.72

69

2.1

0.1

0.1

0.0

4

242

BOU-DD23-219

9150N

Para

294.4

299.0

1.19

17

4.6

0.1

0.1

0.2

3

152

BOU-DD23-219

9150N

Para

309.1

310.2

0.54

4

1.1

0.0

0.0

0.0

1

59

BOU-DD23-219

9150N

Para

309.1

311.3

0.54

4

2.2

0.0

0.0

0.0

2

58

BOU-DD23-219

9150N

Para

312.4

313.6

0.49

1

1.2

0.0

0.0

0.0

1

49

BOU-DD23-219

9150N

Para

314.5

315.6

0.52

4

1.1

0.0

0.1

0.2

2

65

BOU-DD23-219

9150N

Para

325.0

325.5

1.27

12

0.5

0.0

0.1

0.0

1

136

BOU-DD23-219

9150N

Para

332.5

334.5

0.65

12

2.0

0.0

0.1

0.1

1

81

BOU-DD23-219

9150N

Para

337.1

337.9

2.09

27

0.8

0.1

1.0

5.1

1

544

BOU-DD23-219

9150N

Para

369.0

370.0

0.33

16

1.0

0.0

0.3

0.5

12

83

BOU-DD23-219

9150N

Main

371.9

377.2

0.95

17

5.3

0.0

0.1

0.5

6

137

BOU-DD23-220

6575N

Para

79.2

80.4

0.48

16

1.2

0.0

0.7

1.6

99

174

BOU-DD23-220

6575N

Para

97.2

98.4

0.83

28

1.2

0.0

0.1

1.1

69

172

BOU-DD23-220

6575N

Main

105.0

115.9

1.77

91

10.9

0.1

1.7

4.5

133

575

Including

112.3

114.7

6.26

261

2.4

0.3

1.2

6.6

16

1,275

BOU-DD23-220

6575N

Para

120.0

121.1

3.17

68

1.1

0.1

0.3

0.3

84

404

BOU-DD23-220

6575N

Para

129.0

130.1

0.41

8

1.1

0.0

0.5

0.8

4

105

BOU-DD23-220

6575N

Para

133.4

136.8

0.89

76

3.4

0.3

2.5

7.0

7

649

BOU-DD23-221

6575N

Para

62.7

63.7

4.48

11

1.0

0.0

0.0

0.0

1

434

BOU-DD23-221

6575N

Para

72.0

73.0

0.53

4

1.0

0.0

0.1

0.0

1

58

BOU-DD23-221

6575N

Para

80.2

81.4

0.08

126

1.2

0.1

0.1

0.0

4

147

BOU-DD23-221

6575N

Main

225.5

239.0

1.07

12

13.5

0.0

0.2

0.3

4

136

BOU-DD23-221

6575N

Para

345.0

345.5

0.59

20

0.5

0.0

0.3

0.4

12

107

BOU-DD23-222

9325N

NSR

0.1

171.1

0.00

0

171.0

0.0

0.0

0.0

0

0

BOU-DD23-223

6525N

Main

131.6

169.9

1.53

311

38.3

0.0

1.8

4.4

101

763

Including

144.9

155.9

2.34

494

11.0

0.1

1.9

3.9

36

996

BOU-DD23-223

6525N

Para

174.9

176.8

1.45

100

1.9

0.0

0.5

2.9

11

410

BOU-DD23-223

6525N

Para

188.4

189.2

0.28

20

0.8

0.0

0.1

0.8

7

90

BOU-DD23-223

6525N

Para

201.0

202.0

0.15

60

1.0

0.0

0.4

2.3

1

211

BOU-DD23-223

6525N

Para

216.0

216.6

0.23

43

0.6

0.0

1.1

3.6

8

292

BOU-DD23-223

6525N

Para

224.8

226.4

0.29

22

1.6

0.0

0.3

0.7

1

96

BOU-DD23-223

6525N

Para

227.5

228.0

0.43

94

0.5

0.0

1.8

0.7

8

231

BOU-DD23-223

6525N

Para

232.0

233.0

0.40

24

1.0

0.0

0.5

0.3

16

95

BOU-DD23-223

6525N

Para

239.5

247.0

0.46

94

7.5

0.0

0.2

0.7

35

192

BOU-DD23-223

6525N

Para

254.0

254.9

0.45

12

0.9

0.0

0.1

0.2

24

68

BOU-DD23-223

6525N

Para

262.7

263.2

0.54

8

0.5

0.0

0.1

0.0

2

64

BOU-DD23-224

6300N

Para

93.9

94.6

1.15

20

0.7

0.0

0.2

0.3

16

152

BOU-DD23-224

6300N

Para

106.9

108.8

0.90

44

1.9

0.0

0.2

0.1

151

152

BOU-DD23-224

6300N

Para

114.0

114.9

0.57

1

0.9

0.0

0.0

0.0

2

56

BOU-DD23-224

6300N

Para

159.0

160.0

0.32

23

1.0

0.0

0.2

0.5

307

102

BOU-DD23-224

6300N

Main

161.0

163.7

0.68

89

2.7

0.0

1.3

0.6

785

275

BOU-DD23-225

9325N

Para

41.9

43.4

0.37

54

1.5

0.0

1.5

4.7

49

400

BOU-DD23-225

9325N

Para

47.4

53.7

1.44

54

6.3

0.0

0.9

5.3

12

508

Including

50.8

53.7

2.88

86

2.9

0.0

1.0

9.9

21

927

BOU-DD23-225

9325N

Para

68.2

70.2

0.65

16

2.0

0.0

0.4

2.3

48

215

BOU-DD23-225

9325N

Main

73.2

77.4

2.70

21

4.2

0.1

0.3

3.2

16

465

Including

75.2

77.4

4.72

31

2.2

0.1

0.3

4.5

16

738

BOU-DD23-225

9325N

Para

79.3

80.7

0.34

14

1.4

0.0

0.2

0.9

5

104

BOU-DD23-225

9325N

Para

83.1

84.0

2.54

40

0.9

0.1

1.0

1.7

47

409

BOU-DD23-226

9325N

Para

175.9

176.4

0.25

52

0.5

0.0

3.9

4.5

2

447

BOU-DD23-226

9325N

Main

182.8

186.7

1.26

35

3.9

0.1

1.5

4.7

8

466

Including

184.5

185.7

3.33

53

1.2

0.1

1.8

9.5

14

951

BOU-DD23-226

9325N

Para

189.9

190.4

1.69

20

0.5

0.0

1.1

3.5

23

407

BOU-DD23-226

9325N

Para

197.0

198.1

7.73

47

1.1

0.3

0.5

0.5

8

852

BOU-DD23-227

9325N

Para

253.0

254.0

0.24

1

1.0

0.0

0.2

1.5

2

113

BOU-DD23-227

9325N

Main

259.7

268.3

3.34

18

8.6

0.1

0.1

0.5

6

369

Including

263.5

268.3

5.42

21

4.8

0.1

0.1

0.1

7

545

BOU-DD23-228

6300N

Para

43.0

44.0

0.03

83

1.0

0.4

0.0

0.0

4

138

BOU-DD23-228

6300N

Para

185.2

186.2

0.66

4

1.0

0.0

0.0

0.0

2

70

BOU-DD23-228

6300N

Para

258.2

260.8

0.55

18

2.6

0.0

0.8

1.2

10

159

BOU-DD23-228

6300N

Main

267.2

276.1

1.99

81

8.9

0.0

1.0

3.4

59

488

Including

267.7

273.0

3.09

119

5.3

0.0

1.5

4.7

87

715

BOU-DD23-228

6300N

Para

277.1

278.1

0.36

12

1.0

0.0

0.2

0.4

3

74

BOU-DD23-228

6300N

Para

301.1

302.1

0.38

12

1.0

0.0

0.0

0.3

53

72

BOU-DD23-228

6300N

Para

308.7

311.6

0.27

35

2.9

0.0

0.5

0.5

3

106

BOU-DD23-228

6300N

Para

312.6

313.6

0.27

20

1.0

0.0

0.3

0.8

1

99

BOU-DD23-228

6300N

Para

314.6

315.4

0.52

20

0.8

0.0

0.3

1.7

2

169

BOU-DD23-228

6300N

Para

319.3

325.0

0.36

23

5.7

0.0

0.1

0.3

8

80

BOU-DD23-228

6300N

Para

330.1

331.8

1.07

20

1.7

0.0

0.0

0.0

5

125

BOU-DD23-228

6300N

Para

333.5

334.5

0.58

27

1.0

0.0

0.0

0.0

14

86

BOU-DD23-228

6300N

Para

356.4

357.0

0.75

16

0.6

0.1

0.0

0.1

3

96

BOU-DD23-228

6300N

Para

364.0

365.5

3.31