Proven and Probable

Where we deliver Mining Insights & Bullion Sales, in form of physical delivery, offshore depositories, and private blockchain distributed ledger technology you may reach us at contact@provenandprobable.com.

Maurice Jackson of Proven and Probable sits down with Michael Rowley the President and CEO of Group Ten Metals (TSX.V: PGE | NYSE: PGEZF) to discuss the latest Platinum, Palladium, Nickel, Copper and Cobalt Intercepts from the Camp Zone Target Area, Stillwater West Project, Montana, USA.

Category: Precious Metals

Maurice Jackson of Proven and Probable sits down with David Cole the President and CEO of EMX Royalty (TSX.V: EMX | NYSE: EMX) to discuss the virtues of the companies highly successful business model that incorporates Royalty Generation, Royalty Acquisition, and Strategic Investments. Mr. Cole will address how the company is strategically positioning itself on the continued global demand for Copper. And equally important, what actions the company will take from the proceeds of the $67 Million U.S. just received on the sale from the Malmyzh Project in Russia. Equally important, Mr. Cole will highlight the enormous value proposition at Cukaru Peki located in Serbia. EMX Royalty continues to demonstrate business and geological acumen, which has produced spectacular results on their balance sheet and their project portfolio.

Proven and Probable:

Where we deliver Mining Insights & Bullion Sales, in form of physical delivery, offshore depositories, and private blockchain distributed ledger technology you may reach us at contact@provenandprobable.com.

April 18, 2019

Vancouver, British Columbia, April 18, 2019 (TSX Venture: EMX; NYSE American: EMX) – EMX Royalty Corporation (the “Company” or “EMX”) is pleased to announce that it has received a US $2 million escrow distribution, which in addition to the initial US $65.15 million payment in 2018, brings the total cash paid to EMX to US $67.15 million from the sale of the Malmyzh project. A second distribution of up to US $2 million, subject to certain conditions, is due to EMX later in 2019 as remaining funds are released from escrow. Malmyzh was sold by IG Copper LLC (“IGC”) to Russian Copper Company for US $200 million in October 2018.1.

IGC’s Malmyzh project was an important EMX strategic investment that exemplifies the portfolio effect of the Company’s diversified business model. Proceeds from the sale of Malmyzh, combined with ongoing royalty and pre-production payments, have yielded a robust balance sheet. EMX is utilizing this strong position to take advantage of new royalty generation, royalty acquisition, and investment opportunities to grow the portfolio and build shareholder value.

About EMX. EMX is a precious and base metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to the risks inherent to operating companies. The Company’s common shares are listed on the TSX Venture Exchange and the NYSE American Exchange under the symbol EMX. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole

President and Chief Executive Officer

Phone: (303) 979-6666

Email: Dave@EMXroyalty.com

Scott Close

Director of Investor Relations

Phone: (303) 973-8585

Email: SClose@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the year ended December 31, 2018 (the “MD&A”), and the most recently filed Form 20-F for the year ended December 31, 2018, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the 20-F and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

While silver prices continue to languish around the $15 level, the less publicized signs that an eventual rise in price eventually must occur continue to emerge.

SRS Rocco reports how silver production is down again. Which is going to eventually have to impact the price.

To find out why, click to watch the video now!

Chris Marcus

Arcadia Economics

“Helping You Thrive While We Watch The Dollar Die”

www.ArcadiaEconomics.com

Is This Patriotism? Is This How We Make America Great Again?

David’s Commentary (In Blue)

Backwoods Jack is back. A year ago Backwoods sold his mansion in the suburbs and moved into a bespoke apartment in an upscale neighborhood in south Minneapolis. His unit occupies the desirable southeast facing corner, up high, one floor beneath the penthouse. Ol’ Backwoods is used to “the best”. He is constantly reminding me that Trump will make America great again and he proudly sports his red MAGA Trump baseball hat in public. Personally, I think a baseball hat on an 84-year old looks inappropriate with or without a MAGA logo on the front. Recently I wrote that he is convinced that Trump will have his likeness sculpted on Mt. Rushmore. When he moved into his condo he mounted a LARGE American flag on a flag pole that he had installed on his balcony. All day and all night long it flaps in the wind. I mean its BIG and it makes a lot of noise. Now, his neighbors are irate because the flapping flag is making so much noise it keeps them up at night. There is a lot of wind when your balcony is on an upper floor, so it really is a problem. When they confront him on the elevator, and politely ask him to take it down, his replies are – well, let’s just say….I can’t print them. That’s a nice way to influence people and make friends.

Our true patriot, who has tunnel vision and will not tolerate any views different from his own, recently decided that HE HATES ALL LIBERALS. He says he and his wife will not be in the same room with them. He tells me this, knowing that my daughter and her two girls are all liberals. He’s really not very smart. He mocks all people of color and gays. Really, I am not making this up. His most recent email to me reads as follows:

“Creepy Joe and Pocahontas are dead. Sorry not to see Trump eat them alive in 2020. He will feast on Bernie and Beto. Regarding Klobuchar (he misspelled her name), we are not ready for a fat, dumpy, ugly Jewish female POTUS from St. Louis Park MN. (He got the Jewish part wrong too, but when you’re Backwoods Jack, details don’t matter).

Of course he is all-in on Trump’s border wall. No more immigrants! I wonder if he ever stops to think about the open borders that allowed his Swedish ancestors to move to Minnesota?

Backwoods’ idea of what a Great America is – well, it’s very different than mine. A MAGA red hat and a large American flag do not make one a patriot. I’ve known Backwoods for 17 years, but it is only in the last few years that he showed his true colors. If you want to see real patriotism in action, watch Lynyrd Skynyrd sing Red White and Blue. I hope you take the time to watch this video. Now this is real southern patriotism.

There are a lot of Backwoods Jacks out there. In their eyes, if you are not a conservative Republican WASP then you don’t count. This mindset sort of parallels Germany in the 1930s, where you better be a blond, blue-eyed Protestant Arian. Hitler wanted to make Germany great again too.

But this is only one side of the problem, albeit an extreme one. On the other side, the liberal side, you have the views of Alexandria Ocasio-Cortez and Maxine Waters. (There are many more, but they are the equivalent of Backwoods.) They want America to be the land of opportunity – but only for the poor and people of color. If you are white, rich and successful you are their target. Backwoods, you better keep your guns locked and loaded. By the way, he sits at the back row of his church on Sundays and has his loaded gun tucked into his belt just waiting for trouble. Really, he does. Fortunately these extremists are in the minority. A majority of Americans are more open minded. But the trouble is, all it takes is a well-organized and vocal minority to wrest control. In post-WW1 Germany, a small minority, the NSDAP (NAZIS) took over the government.

I talk about Backwoods because he really is just like your rather normal next-door neighbor. You never know how normal someone is until you start talking politics.

Politically speaking, half the people in America are liberal and half are conservative. Fortunately, not all the Liberals or Conservatives are this extreme (thank God). But the Backwoods and the likes of Alexandria Ocassio-Cortez’s of the world are gaining in numbers. Doesn’t it disturb you that people like AOC and Maxine Waters can get elected into office? What does that say about the people who vote them in? It says that they are fed up with the establishment and they want a bigger piece of the pie – the piece that is on YOUR dinner table.

This is all about the haves and the have-nots. If you happen to be one of the unfortunates living on the street, or someone who is barely getting by on minimum wage, it’s only natural that you will be envious of those who have found a way to succeed. If you are in the upper-middle class with a little money in the bank and a decent job you probably should feel threatened by those who want to raise taxes and take what’s yours. Backwoods Jack doesn’t feel threatened. He just likes to feel superior. The best way to deal with people is to find a way to lift their standard of living, to provide them with decent jobs that put food on their table and give them a sense of self-respect.

I would like to believe that a majority of Americans are decent people who are not prejudice and do care. If you haven’t seen the movie Same Kind Of Different As Me, then by all means, make it a point to see it.

A recent interview with former CFTC Commissioner Bart Chilton nearly knocked me off my feet because it confirmed what I have alleged, starting more than 12 years ago. I’ll include the interview later, but first I will set the background of the subject and timeline in order put Chilton’s words into the proper perspective. The subject is JPMorgan’s manipulation of the silver market. The timeline is important because Chilton does misstate some facts that need to be corrected. I’m not a big fan of articles that include lots of links to past articles, but in this case it’s unavoidable.

Shortly after Bart Chilton took office as a commissioner in August 2007, he began to make public speeches in which he asserted that the CFTC was no regulatory pushover, like Barney Fife on the “Andy Griffith Show” but more like Elliot Ness or James Bond and that the agency was a tough cop on the beat. I assumed Chilton was genuine in his faith in the agency, but since he was brand new to commodity regulation I was sure that he was unaware of my allegations to the agency over the prior 20 years about a silver manipulation due to a concentrated short position on the COMEX. So I wrote to him about his claims of regulatory toughness at the agency and encouraged others to do so as well.

To his credit, Commissioner Chilton, responded to my and others’ e-mails quickly, pointing out that CFTC staff were aware of the allegations and having responded in the past, they would do so again in the future.

I would ask you to note that my first contacts with Commissioner Chilton took place shortly after he assumed office in 2007 and the subject matter revolved around the concentrated short position in COMEX silver futures, an issue that has remained at the heart of the allegations of price manipulation to this day.

This absolute must read commentary by Ted, which confirms everything that Ted has said about JPMorgan and the CFTC…plus more

Theodore Butler

Confirmation, Outrage and Disgust

A recent interview with former CFTC Commissioner Bart Chilton nearly knocked me off my feet because it confirmed what I have alleged, starting more than 12 years ago. I’ll include the interview later, but first I will set the background of the subject and timeline in order put Chilton’s words into the proper perspective. The subject is JPMorgan’s manipulation of the silver market. The timeline is important because Chilton does misstate some facts that need to be corrected. I’m not a big fan of articles that include lots of links to past articles, but in this case it’s unavoidable.

Shortly after Bart Chilton took office as a commissioner in August 2007, he began to make public speeches in which he asserted that the CFTC was no regulatory pushover, like Barney Fife on the “Andy Griffith Show” but more like Elliot Ness or James Bond and that the agency was a tough cop on the beat. I assumed Chilton was genuine in his faith in the agency, but since he was brand new to commodity regulation I was sure that he was unaware of my allegations to the agency over the prior 20 years about a silver manipulation due to a concentrated short position on the COMEX. So I wrote to him about his claims of regulatory toughness at the agency and encouraged others to do so as well.

To his credit, Commissioner Chilton, responded to my and others’ emails quickly, pointing out that CFTC staff were aware of the allegations and having responded in the past, they would do so again in the future.

I would ask you to note that my first contacts with Commissioner Chilton took place shortly after he assumed office in 2007 and the subject matter revolved around the concentrated short position in COMEX silver futures, an issue that has remained at the heart of the allegations of price manipulation to this day.

Much to his credit, Chilton always endeavored to answer each and every email sent to him from the public (provided those emails weren’t personally insulting). In fact, I continued to email him personally and encouraged others to do so as well, in addition to sending him and the other commissioners all articles I wrote. I think it’s fair to say that close to 99% of the thousands of public emails sent to Chilton concerned the silver and gold price manipulation and there can be little doubt that all of those emails came directly or indirectly at my urging. What else could possible account for the high volume of public correspondence with an official of the CFTC?

Early in 2008, Commissioner Chilton indicated to me privately that the agency would be coming out with a new finding concerning the continued numerous public allegations of a silver price manipulation. This new finding would supersede the 15 page public letter of 2004. Perhaps I misinterpreted his message, but I came to believe that the new finding would be much different than the original finding. Instead, on May 13, 2008, the CFTC published another 16-page denial that anything was wrong with the concentrated short position in COMEX silver futures.

Feeling betrayed (something I don’t believe I revealed previously), I told Chilton in not-so-polite terms how I felt and ceased personal email contact with him (although I did continue to send my articles to him and all the other commissioners, since they concerned regulatory matters).

In March 2008, nearly two months before the CFTC’s 2nd public silver letter was published, the largest concentrated COMEX silver (and gold) short, Bear Stearns, failed and its short positions were assumed by JPMorgan. I certainly knew that Bear Stearns collapsed and was taken over by JPMorgan, but I had no idea at the time that Bear was the biggest single short in COMEX silver and gold or that JPMorgan assumed those short positions. I would only learn of this months later, after the August 2008 Bank Participation Report was issued and revealed for the very first time an enormous silver and gold short position held, as it turned out, by a single US bank. (The reason Bear Stearns had never appeared in the Bank Participation Report was because it was an investment, not a commercial bank like JPMorgan).

Importantly, as a result of this article and others, which encouraged readers to again petition the CFTC, the agency confirmed it had initiated a formal investigation by its Enforcement Division – I believe primarily due to Chilton’s initiative (although for some reason, Chilton claims in his interview that the investigation started in 2010, at the prodding by Andrew Maguire). Fortunately the record of the timeline is clear, although the original confirmation was buried in an overall press release on Oct 2, 2008 –

The termination of the investigation was more fully announced five years later –

Within months of the August 2008 Bank Participation report, I had deduced that JPMorgan was the big COMEX silver and gold short and began publicly referring to the bank as the big silver and gold crook and price manipulator (albeit with more trepidation initially than as time passed). Please know that all my deductions and allegations came from studying public data and official correspondence from the CFTC to lawmakers, as many readers wrote to their elected officials about what had transpired. I never talked with anyone at the CFTC about any of this – to them, I was always persona non grata.

But in the fall of 2008 when I came to figure out that JPMorgan had been running the silver and gold manipulation since March of that year, it also dawned on me that there could be no way that the CFTC wasn’t fully aware that Bear Stearns was in deep trouble with its COMEX silver and gold short positions before the JPM takeover, since prices of each rose substantially from yearend 2007 to the day in March when JPM took over the short positions. Bear Stearns would have needed to have come up with more than a billion dollars in cash for margin calls, money it simply didn’t have.

Since the CFTC would have had to have known of Bear’s plight and of JPMorgan taking over its silver and gold short positions, it also became obvious to me that the CFTC had lied through its teeth when it failed to mention in its public letter of May 2008 that the biggest concentrated silver and gold short seller failed and needed to be taken over by JPMorgan. After all, the subject of the public letter was concentration on the short side of silver, so there was no way the Bear Stearns’ failure could have been innocently overlooked. I said so in a subsequent public article, even writing to the CFTC’s Inspector General about it –

OK, that’s the background and timeline, so why am I walking you down memory lane today? It seems that Bart Chilton, whose tenure as a commissioner at the CFTC ended in early 2014, has chosen to speak out on the silver manipulation and his and the agency’s role at the time. This is the very first time that an insider has confirmed virtually everything I’ve alleged about JPMorgan. In fact, Chilton goes beyond just confirming what I’ve alleged, he paints a picture of deep concern behind the scenes, as the CFTC struggled to get JPMorgan’s silver short position reduced – to no avail. Here is the interview with Chris Marcus of Arcadia Economics –

Since the interview is about 42 minutes long, please allow me to highlight what I believe are the key points.

At the 3:30 minute mark, Chilton acknowledges that he first learned of the allegations of a silver manipulation from me, but then goes on to say he asked for an Enforcement Division investigation only after Andrew Maguire contacted him in 2010, which as I indicated is contrary to the verified record which indicated the investigation began in September 2008.

At the 11:40 minute mark and continuing to the 18:30 mark, it gets interesting. This is where Chilton acknowledges publicly for the first time that JPMorgan took over Bear Stearns’ silver short position and goes on to explain how the CFTC had to approve the resultant excessively large combined short position and did so on a temporary basis of no more than a few months and how JPMorgan didn’t abide by the CFTC’s waiver. He also points out how the head silver trader for Bear Stearns also went over to JPM and continue to trade the position there. Chilton states that he was shocked about how large the JPMorgan silver short position grew to and implies it was eventually worked down. Perhaps JPM’s silver short position was worked down temporarily as it rigged prices lower, but as regular readers know, JPM has continued to add shorts and buy back on lower prices to this day, a decade later.

At the 20:20 mark, Chilton acknowledges the agency had plenty of evidence of manipulation, but not enough to bring charges and asked for outside help in determining whether the evidence was enough to bring charges. Chilton claims he extended the investigation for another year and believed there was enough evidence to bring charges. It should be noted, even though I caused the investigation to be initiated in the first place, I was never contacted.

At the 36:40 mark, Chilton acknowledges for the first time that the Justice Department was involved in the five year silver investigation but dropped interest after the CFTC closed its investigation. He suggests the DOJ is understaffed. Also mentioned is that Chilton had perhaps a hundred separate meetings on the silver investigation back then, in addition to the dozens of official agency meetings on silver that the agency held. It’s remarkable with all that attention, JPMorgan was able to continue to manipulate silver prices to this day without missing a beat. And I distinctly remember all through this time, which Chilton described as full of high drama behind the scenes, not one word was offered publicly to warn anyone that there were strong official suspicions of manipulation. All I ever recall is that the CFTC found all my allegations of silver manipulation to be completely unfounded. Chilton seems to be saying something quite different in this interview.

What Chilton said confirmed just about everything I’ve written and for that I am grateful. Again, all my analysis has been based strictly on public data. While I’m happy for the confirmation, I’m also outraged and disgusted that the CFTC and DOJ failed to end the manipulation and that JPMorgan has continued on its merry and illegal way. I’ve reached the conclusion that JPMorgan is so well-connected and backed by such legal firepower that even the US Government, certainly in the form of the CFTC, but now also including the Justice Department, is no match for it. As a result, my expectations for the DOJ cracking down on JPM have been reduced to a faint hope, although it saddens me to admit to that.

That said, I do believe more than ever that it will be JPMorgan’s actions over the past decade that will power silver (and gold) higher. No one would acquire the massive amount of physical silver and gold that JPMorgan has accumulated without the expectation of a monster payday. Separately, Chilton’s confirmation that the CFTC (and DOJ) were investigating and pressuring JPM would seem to dispel any notion that it was or is the US Government behind the silver (and gold) manipulation. The CFTC and DOJ are US Government institutions, after all.

They may be no match for JPMorgan, but that’s a far cry from either being involved in some conspiracy to manipulate prices. Finally, the degree of alarm and concern by the regulators, according to Chilton, would seem to mock all the manipulation deniers who maintain there is nothing to see. According to Chilton, the regulars saw plenty to be concerned about.

Ted Butler

April 4, 2019

www.butlerresearch.com

Vancouver, British Columbia, April 4th, 2019 (TSX Venture: EMX; NYSE American: EMX) – EMX Royalty Corporation (the “Company” or “EMX”) is pleased to announce the execution of an arm’s length purchase agreement (the “Agreement”) for the sale of thirteen exploration licenses (the “Properties”) comprising EMX’s Gold Line Project (the “Project”) in central Sweden to Gold Line Resources Ltd. (“GLR”), a private British Columbia company. The Agreement provides EMX with a 9.9% interest in GLR, advance royalty payments, and a 3% net smelter return (“NSR”) royalty interest in the Properties.

The Properties host mesothermal lode gold and/or intrusion related gold systems positioned along the well-known “Gold Line” in the Skellefteå mining region of central Sweden. The Properties contain a series of early stage gold exploration targets to more advanced projects with drill defined zones of gold mineralization. The region was the subject of intensive exploration by the Swedish government in the 1980s that led to the discovery of a series of gold deposits and occurrences along a roughly 200 kilometer long north-south trend west of Skellefteå. This belt became known as the “Gold Line”, where several mines have since been developed. As well, there are ongoing exploration programs at the nearby Barsele project (operated as a joint venture between Agnico Eagle Mines Ltd. and Barsele Minerals Corp.), and the Fäboliden development project (Dragon Mining Ltd.).

EMX assembled its land position in late 2016 and early 2017 prior to an increase in activity by competitor companies. Since that time, EMX has been compiling historic information on the Project and executing reconnaissance sampling and mapping programs in order to develop drill targets. EMX has now identified a number of prioritized exploration targets that will be further advanced by GLR.

PI Financial Corp. is acting as financial advisor to GLR in connection with the Agreement.

Commercial Terms Overview (all dollar amounts in CDN, unless otherwise noted).

- At closing, EMX will transfer to GLR its thirteen exploration licenses in the Skellefteå area.

- At closing, GLR will issue to EMX that number of common shares of GLR that represents a 9.9% equity ownership in GLR; GLR will have the continuing obligation to issue additional shares of GLR to EMX to maintain its 9.9% interest in GLR, at no additional cost to EMX, until GLR has raised $5,000,000 in equity; thereafter EMX will have the right to participate pro-rata in future financings at its own cost to maintain its 9.9% interest in GLR.

- At closing, GLR will reimburse EMX for its 2019-2020 license fees, which have been paid in advance and total US$101,390.

- GLR will also commit to raise $600,000 within 6 months of the signing date to fund exploration programs in 2019 on the Project. GLR will then commit to raising another $500,000 within two years of the closing date of the Agreement, and will be responsible for maintaining the Properties in good standing according to Swedish mining regulations.

- EMX will receive an uncapped 3% NSR royalty on the Properties. Within six years of the closing date, GLR has the right to buy down up to 1% of the royalty owed to EMX (leaving EMX with a 2% NSR) by paying EMX 2,500 ounces of gold, or its cash equivalent.

- EMX will receive annual advance royalty (“AAR”) payments of 30 ounces of gold on the Properties, commencing on the second anniversary of the closing, with each AAR payment increasing by 5 ounces of gold per year up to a maximum of 75 ounces of gold per year. These AAR payments may be made in gold bullion, their cash equivalents, or their value equivalent in shares of GLR, subject to certain conditions.

Overview of Properties. The Properties comprise 54,591 hectares of exploration licenses, which form a linear trend spanning 170 kilometers from north to south. These include EMX’s Storjuktan, Paubacken, Paubacken Norra, Blabarliden, Rotjarnen and Kankberg Norra license groups. Each of the license areas was acquired due to the presence of either reported gold mineralization or geological characteristics similar to other known gold occurrences and deposits in the area. Several of the EMX projects have outcropping or drill-defined zones of gold mineralization from historic programs that are in need of further assessment. This includes a historic intercept of 6 meters averaging 11.2 g/t gold in drill hole DH07-23 (true width unknown), drilled by Lappland Goldminers AB in 20071 within EMX’s Blabarliden license.

On the EMX licenses, gold mineralization is generally hosted by Svekofennian (Mid-Proterozoic) aged granitoid rocks and supracrustal sediments. The sediments are dominated by fine grained siliciclastics which include sulfide-rich black shales. Some carbonate units are also present. Gold tends to occur at, or near, the contacts between granitoid intrusive rocks and the supracrustal sedimentary rock units.

Styles of mineralization on the EMX licenses range from sheeted vein swarms developed along contacts between granitoids and metasedimentary rocks, to mineralized skarns rich in diopside and other calc-silicates. In one case, mineralization appears to be associated with a porphyritic felsic intrusion. Mineralization also tends to be developed along major structural features and appears concentrated in fold hinge environments and prominent shear zones.

EMX plans to work closely with GLR in the coming field season to continue to develop its exploration targets, and to prepare the portfolio for scout drill testing.

Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

About EMX. EMX leverages asset ownership and exploration insight into partnerships that advance our mineral properties, with EMX receiving pre-production payments and retaining royalty interests. EMX complements its royalty generation initiatives with royalty acquisitions and strategic investments.

For further information contact:

David M. Cole

President and Chief Executive Officer

Phone: (303) 979-6666

Email: Dave@EMXroyalty.com

Scott Close

Director of Investor Relations

Phone: (303) 973-8585

Email: SClose@EMXroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merits of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the year that ended on December 31, 2018 (the “MD&A”), and the most recently filed Form 20-F for the year that ended on December 31, 2018, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the 20-F and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

VANCOUVER, British Columbia, March 21, 2019 (GLOBE NEWSWIRE) — Riverside Resources Inc. (“Riverside” or the “Company”) (RRI.V) (RVSDF) (R99.F) is pleased to report initial results from the Company’s first-phase exploration program at the recently staked Sandy Project (the “Project”) located in northwestern Sonora, Mexico. Riverside continues to leverage its knowledge and experience in NW Mexico to cost-effectively acquire new prospective concessions with strong potential for new discoveries.

Riverside geologists have completed near surface sampling, mapping and geophysics to work up initial target areas at the Project. Riverside’s exploration team is targeting intrusion related and orogenic gold mineralization hosted by altered granite and linked with large structures adjacent to gneiss bedrock.

Riverside’s President and CEO, John-Mark Staude, stated: “The Sandy Project was a project the Company staked over a prospective area known to us from our past work in Sonora. We are pleased with the results from our first pass on the Sandy Project. Gold appears associated with large structures, intrusions and is an exciting potential step in the geologic deposit modeling for Sonora. We plan to follow up these positive results with some mapping and more sampling in 2019.”

The sampling done to date by Riverside has been concentrated on two areas in the center of the project with past historical mine workings (see Figure 1 below) associated with felsic intrusive stock and gneiss. A sample from one of these old workings returned 38.8 g/t Au. Chip channel samples of 1.5 meter in length returned gold results of 9.3 g/t, 4.7 g/t and 3.7 g/t Au. A total of 71 samples have been analyzed so far and further work at Sandy is anticipated to continue to define the structural nature and intrusion association to the gold.

Figure 1: Sandy Gold Target Areas and Geochemical Results.

Higher gold grades appear to be associated with intersecting structures within strongly foliated granitic intrusive bedrock. Primary structures strike NW-SE and dip between 40 and 70 degrees to the east in a general structural character with similar orientation and style to some of the shear zone gold mines in the region. Other smaller faults are noted striking roughly north-south and dipping steeply to the east which cut the main shear zone and could possibly hide extensive expansions of the gold system under shallow cover. The cross structures have been intruded by mafic dikes that show pervasive propylitic alteration indicating potential deeper intrusion related gold mineralization. The highest-grade gold material was found associated with a set of variously dipping felsic dikes which could be associated with the intrusive system. Silicification and minor quartz veining is noted associated with the structures and with through-going vein mineralization. The wall rock associated with these structures often shows sericitic and silica alteration.

Of note while visiting the property are the vast placer-gold workings immediately north of the project area. The source of the placer gold has not been determined and may be derived from intrusive bedrock within the Sandy project.

As can be seen in the district summary map (see Figure 1 above), the Riverside rock-chip samples confirm the existence of gold mineralization within the central part of the Company’s concession.

Click here to see the Sandy Project page on Riverside’s website.

Qualified Person & QA/QC:

The scientific and technical data contained in this news release pertaining to the Sandy Project was reviewed and approved by Freeman Smith, P.Geo, a non-independent qualified person to Riverside Resources, who is responsible for ensuring that the geologic information provided in this news release is accurate and who acts as a “qualified person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects.

The rock chip samples collected by Riverside’s field crew at the Sandy Project were taken from 4 main showings on the western slopes of the property, with most individual samples consisting of composites of bedrock fragments hammer-chipped from 0.5 and 1.5-metre-long intervals across rock faces showing evidence of alteration and silicification. The highest-grade sample which assayed 38.8 g/t Au was a select grab sample of loose rock found within a small underground working which are believed to date back to the 1960’s. The one grab sample is not representative of the mineralization that was chip-sampled from actual outcrops, however, they do support Riverside’s view that the Sandy property has excellent potential for the discovery of intrusion-related gold and silver mineralization. All of Riverside’s rock samples were analyzed at the Hermosillo and Vancouver laboratories of Bureau Veritas where gold content was determined by fire assaying with atomic adsorption finish and ICP-mass spectrometry was used to analyze for 45 other elements. For quality control purposes, three standard samples were included with the batch of 71 field samples.

About Riverside Resources Inc.:

Riverside is an exploration company driven by value generation and discovery. The company has fewer than 65M shares issued and a strong portfolio of gold-silver and copper assets in North America. Riverside has extensive experience and knowledge operating in Mexico and leverages its large database to generate a portfolio of prospective mineral properties. In addition to Riverside’s own exploration spending, the Company also strives to diversify risk by securing joint-venture and spin-out partnerships to advance multiple assets simultaneously and create more chances for discovery. Riverside has additional properties available for option, with more information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

| For additional information contact: | ||

| John-Mark Staude | Raffi Elmajian | |

| President, CEO | Corporate Communications | |

| Riverside Resources Inc. | Riverside Resources Inc. | |

| info@rivres.com | relmajian@rivres.com | |

| Phone: (778) 327-6671 | Phone: (778) 327-6671 | |

| Fax: (778) 327-6675 | TF: (877) RIV-RES1 | |

| Web: www.rivres.com | Web: www.rivres.com | |

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

New drill intercept in Idaho Vein assays 90.4 gpt gold / 4.27 m (2.6 oz per ton / 14.0 ft)New drill intercept includes 458 gpt gold over 0.81 m (13.4 oz per ton / 2.7 ft) Additional drilling targeting Idaho #1 Vein currently in progressMultiple 52 Vein intersections assayed up to 15.4 gpt gold over 1.63 m (0.45 opt / 5.3 ft)A shallow vein near surface assayed 8.5 gpt gold over 2.88 m (0.25 opt / 9.4 ft)

Vancouver, British Columbia–(Newsfile Corp. – March 19, 2019) – Rise Gold Corp. (CSE: RISE) (OTCQB: RYES) (the “Company“) is pleased to announce additional assay results from on-going diamond core drilling at the Idaho-Maryland (“I-M”) Gold Project.

The exploration drill program at the Idaho-Maryland continues to be successful. Recent drilling intersected the Idaho #1 Vein below historic mining areas and intersected the 52 Vein area prior to reaching the Idaho #1 Vein target. A shallow vein was also intersected at 259 m.

TABLE 1 – New Drill Hole Intercept Highlights

|

Hole

|

From (m)

|

To (m)

|

Gold

(gpt) |

Intercept

Length (m)* |

Vein

|

| Idaho #1 Vein | |||||

| I-18-11 |

1381.86

|

1384.33

|

3.6

|

2.47

|

Idaho #1

|

|

I-19-13

|

1007.97

|

1013.09

|

5.5

|

5.12

|

Idaho #1

|

|

I-19-13A

|

1005.31

|

1009.57

|

90.4

|

4.27

|

Idaho # 1

|

|

Including

|

1008.77

|

1009.57

|

458.0

|

0.81

|

|

|

Near Surface

|

|||||

|

I-18-11

|

259.16

|

262.04

|

8.5

|

2.88

|

?

|

|

Including

|

261.14

|

262.04

|

18.8

|

0.90

|

|

|

52 Vein Area

|

|||||

|

I-18-11

|

975.50

|

976.70

|

19.2

|

1.20

|

52

|

|

I-18-11

|

992.25

|

993.88

|

15.4

|

1.63

|

52

|

|

Including

|

992.70

|

993.22

|

35.6

|

0.52

|

|

|

I-18-11

|

1046.17

|

1052.58

|

3.9

|

6.42

|

52

|

|

I-18-11

|

1142.33

|

1144.08

|

5.4

|

1.75

|

52

|

|

I-18-12

|

950.50

|

960.49

|

2.6

|

9.98

|

52

|

*The Company is not able to estimate true widths for the intersected mineralization until further drilling is completed.

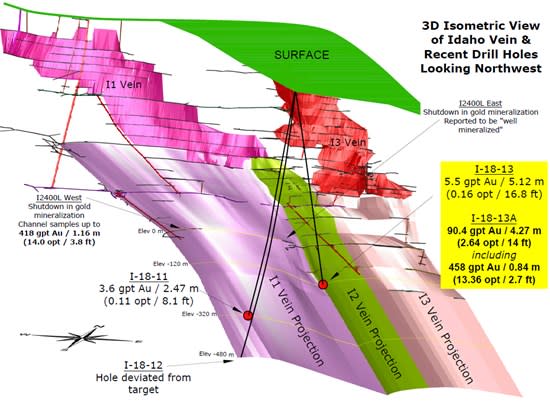

Very high-grade gold mineralization was encountered in drill hole I-19-13A which assayed 90.4 gpt gold over 4.27 m (2.6 oz per ton / 14 feet). Rise Gold has interpreted this intercept to represent a significant down-dip extension of the historic Idaho #1 Vein. The intercept in I-19-13A is near the elevation of the lowest haulage level of the mine accessed by the existing vertical mine shaft.

FIGURE 1 – Visible Gold in Drill Intercept I-19-13A (in retained half core)

Cannot view this image? Visit: https://media.zenfs.com/en-us/newsfile_64/eed21ca200e9ddb32b03302bbbe65f0d

To view an enhanced version of Figure 1, please visit:

https://orders.newsfilecorp.com/files/2255/43502_b873fb6414782965_002full.jpg

The Idaho #1 Vein was the most productive and highest-grade vein of the I-M Mine. Historic production from the Idaho #1 Vein is estimated at 935,000 oz of gold with an average head grade of 38.7 gpt (1.12 opt) gold. Total historic production from the Idaho Veins is estimated at 1,621,000 oz of gold with an average head grade of 28.4 gpt (0.74 opt) gold.

Idaho #1 Vein Drilling

The mineralized intercepts in drill holes I-19-13 and I-19-13A consist of a quartz shear vein and extensive zones of quartz-sericite-pyrite alteration in the walls of the vein.

- Drill hole I-19-13A was wedged from drill hole I-19-13 and the holes are offset approx. 1.5 meters apart at the vein intersection

- The vein in I-19-13 assayed 5.5 gpt gold over 5.12 m (0.16 opt / 16.8 ft)

- The vein in I-19-13A assayed 90.4 gpt gold over 4.27 m (2.64 opt / 14.0 ft)

- The weighted average of both holes is 44.1 gpt gold over 4.69m (1.29 opt / 15.4 ft)

- I-19-13A includes a sample which assayed 458 gpt gold over 0.84 m (13.36 opt / 2.7 ft)

- The vein in I-19-13A contains coarse visible gold in some samples of retained half core

- A 40 m wide zone of alteration surrounds the vein with an average grade of ~1.5 gpt gold and individual samples assaying up to 12 gpt gold

Drill hole I-18-11 intersected the Idaho #1 Vein approx. 525 m along strike to the north-west and 200 m below I-19-13A. The intercept consists of a quartz shear vein and extensive zones of quartz-sericite-pyrite alteration in the walls of the vein.

- The vein in I-18-11 assayed 3.6 gpt gold over 2.47 m (0.11 opt / 8.1 ft)

- A 100 m wide zone of alteration surrounds the vein with an average grade of ~1.1 gpt gold and individual samples assaying up to 8 gpt gold

- Additional drilling in the area of I-18-11 may reveal coarse gold similar to I-19-13A

Drill hole I-18-13A and I-18-11 are located 120 m and 320 m vertically below the I2400 level, the lowest level of exploration on the Idaho #1 Vein. Historic drifts were driven from each end of the vein and reported to be in gold mineralization at the time the mine was shut down.

- I2400L West: historic channel samples of the vein and wallrock averaged 19.9 gpt gold over 1.93 m (0.58 opt / 6.4 ft) for a distance of 165 m to the final shutdown face

- Channel samples include assays up to 481 gpt gold over 1.16 m (14.0 opt / 3.8 ft)

- I2400L East: drifting in the Idaho #1 Vein was reported to be “well mineralized” over a distance of 76 m to the final shutdown face

Drill hole I-18-12 was designed to test the down-dip extension of the mineralization encountered in I-18-11 but significantly deviated and did not reach the intended Idaho #1 Vein target.

Rise Gold is currently drilling the Idaho #1 Vein target between I-19-13A and I-18-11 and utilizing directional drilling to improve the accuracy of drilling and expedite the next intercepts.

A summary of drill hole assay results from recent exploration diamond drilling on the Idaho #1 Vein target are presented in Table 1 and illustrated in Figure 2. A photo of coarse visible gold in drill hole I-19-13A is displayed in Figure 1.

The Isometric drawing (Figure 2) showing the recent drill hole intercepts in the Idaho area can be downloaded from the following link.

https://riseg.sharefile.com/d-s8bc52c537474e41a

FIGURE 2 – Idaho Vein Intercepts – Isometric View

Cannot view this image? Visit: https://media.zenfs.com/en-us/newsfile_64/49d5152bcf6ca4b4db89aa4ff96fcefa

To view an enhanced version of Figure 2, please visit:

https://orders.newsfilecorp.com/files/2255/43502_b873fb6414782965_003full.jpg

52 Vein Area Drilling

Drill holes I-18-11 and I-18-12 drilled though the 52 Vein area en route to the Idaho #1 Vein target.

Important gold mineralization related to the 52 Vein was intersected in drill holes I-18-11 & I-18-12. The 52 Vein intercepts are located approximately 242 m and 125 m north-east of the previous drill intercept in drill hole I-18-10.

A similar style of mineralization to I-18-10 was encountered with a wide flat lying shear vein and high-grade extensional veins in the walls of vein.

Drill hole I-18-10 assayed 149.3 gpt gold over 6.8 m, including 2,190 gpt gold over 0.47 m and was previously reported by news release on Dec 13th 2018.

The current drill program is focussed on the Idaho #1 Vein target and therefore the 52 Vein intercepts are incidental to the Idaho #1 Vein drilling. The 52 Vein represents a large and compelling target for a focussed drilling program in the future.

A summary of drill hole assay results from recent exploration diamond drilling on the 52 Vein target are presented in Table 1 and illustrated in Figure 3.

FIGURE 3 – 52 Vein Intercepts – Plan View

Cannot view this image? Visit: https://media.zenfs.com/en-us/newsfile_64/401c4b4a686e20d6fca42f6abe4b4cc3

To view an enhanced version of Figure 3, please visit:

https://orders.newsfilecorp.com/files/2255/43502_b873fb6414782965_004full.jpg

Quality Control and Assay Methods

Richard Lippoth, M.Sc, CPG, the qualified person for the exploration drill results disclosure contained in this news release, has studied the drill core discussed in this news release and has reviewed the analytical and quality control results. Mr. Lippoth has reviewed and approved the scientific and technical contents of this news release.

Benjamin Mossman, P.Eng, CEO of Rise Gold, is the qualified person for the historic production disclosure contained in this news release. Historic production at the Idaho-Maryland Mine is disclosed in the Technical Report on the Idaho-Maryland Project dated June 1st, 2017 and available on www.sedar.com.

Rise has implemented a quality control program for its drill program to ensure best practice in the sampling and analysis of the drill core. This includes the insertion of blind blanks, duplicates and certified standards. HQ- and NQ-sized drill core is saw cut with half of the drill core sampled at intervals based on geological criteria including lithology, visual mineralization, and alteration. The remaining half of the core is stored on-site at the Company’s warehouse in Grass Valley, California. Drill core samples are transported in sealed bags to ALS Minerals analytical assay lab in Reno, Nevada.

All gold assays were obtained using a method of screen fire assaying. This procedure involves screening a large pulverized sample of up to 1 kg at 100 microns. Any +100 micron material remaining on the screen is retained and analyzed in its entirety by fire assay with gravimetric finish and reported as the Au (+) fraction result. The -100 micron fraction is homogenized and two sub-samples of 30-50 grams are analyzed by fire assay with AAS finish. If the grade of the material exceeds 10 gpt the sample is re-assayed using a gravimetric finish. The average of the two results is taken and reported as the Au (-) fraction result. All three values are used in calculating the combined gold content of the plus and minus fractions.

About Rise Gold Corp.

Rise Gold is an exploration-stage mining company. The Company’s principal asset is the historic past-producing Idaho-Maryland Gold Mine located in Nevada County, California, USA. The Idaho-Maryland Gold Mine is a past producing gold mine with total past production of 2,414,000 oz of gold at an average mill head grade of 17 gpt gold from 1866-1955. Historic production at the Idaho-Maryland Mine is disclosed in the Technical Report on the Idaho-Maryland Project dated June 1st, 2017 and available on www.sedar.com. Rise Gold is incorporated in Nevada, USA and maintains its head office in Vancouver, British Columbia, Canada.

On behalf of the Board of Directors:

Benjamin Mossman

President, CEO and Director

Rise Gold Corp.

For further information, please contact:

RISE GOLD CORP.

Suite 650, 669 Howe Street

Vancouver, BC V6C 0B4

T: 604.260.4577

info@risegoldcorp.com

www.risegoldcorp.com

The CSE has not reviewed, approved or disapproved the contents of this news release.

Forward-Looking Statements

This press release contains certain forward-looking statements within the meaning of applicable securities laws. Forward-looking statements are frequently characterized by words such as “plan”, “expect”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words or statements that certain events or conditions “may” or “will” occur.

Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, there can be no assurance that such expectations will prove to be correct. Such forward-looking statements are subject to risks, uncertainties and assumptions related to certain factors including, without limitation, obtaining all necessary approvals, meeting expenditure and financing requirements, compliance with environmental regulations, title matters, operating hazards, metal prices, political and economic factors, competitive factors, general economic conditions, relationships with vendors and strategic partners, governmental regulation and supervision, seasonality, technological change, industry practices, and one-time events that may cause actual results, performance or developments to differ materially from those contained in the forward-looking statements. Accordingly, readers should not place undue reliance on forward-looking statements and information contained in this release. Rise undertakes no obligation to update forward-looking statements or information except as required by law.

Corporate Logo

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/43502

THIS NEWS RELEASE IS NOT INTENDED FOR DISTRIBUTION TO UNITED STATES NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES AND DOES NOT CONSTITUTE AN OFFER OF THE SECURITIES DESCRIBED HEREIN

VANCOUVER, British Columbia, March 19, 2019 (GLOBE NEWSWIRE) — Riverside Resources Inc. (“Riverside” or the “Company”) (RRI.V) is pleased to announce it has closed its previously announced private placement. The placement was over-subscribed and the Company issued 17,488,875 units at a price of $0.16 per unit for gross proceeds of $2,798,220 instead of the 9,375,000 units ($1,500,000) originally contemplated.

Each unit consists of one common share and one whole common share purchase warrant (“Unit”). Each common share purchase warrant is exercisable into one common share for a period of two (2) years from closing at a price of $0.22 (“Warrant”). If, at any time after July 20, 2019, the closing price of the common shares on the TSX Venture Exchange (“TSX-V”) trades at a VWAP equal or greater than $0.45 for 10 consecutive trading days, the Company may accelerate the expiry date of the Warrants by disseminating a press release announcing the new expiry date whereupon the Warrants will expire on the 30th trading day after the date on which such press release is disseminated.

Management and insiders subscribed for 845,000 Units for $135,200 in total proceeds to the Company.

With respect to a portion of the funds raised in the private placement, the Company paid finders’ fees of $87,312 to Sprott Global Resource Investments Ltd., $20,076.80 and 12,000 Units to Haywood Securities Inc., 16,000 Units to Canaccord Genuity, and $1,280 to PI Financial Corp.

All securities issued pursuant to the private placement and as finders’ fees will be subject to a four-month hold period expiring on July 20, 2019.

The Company will use the proceeds of the financing to fund a focused drill program at the Cecilia Gold Project, additional project acquisitions and further target refinement on existing projects to advance towards new partnerships.

The securities being offered have not been and will not be registered under the U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States or to, or for the account or benefit of, U.S. persons without United States federal and state registration or an applicable exemption from registration requirements.

About Riverside Resources Inc.:

Riverside is an exploration company driven by value generation and discovery. The company has fewer than 65M shares issued and a strong portfolio of gold-silver and copper assets in North America. Riverside has extensive experience and knowledge operating in Mexico and leverages its large database to generate a portfolio of prospective mineral properties. In addition to Riverside’s own exploration spending, the Company also strives to diversify risk by securing joint-venture and spin-out partnerships to advance multiple assets simultaneously and create more chances for discovery. Riverside has additional properties available for option, with more information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

| John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com |

Raffi Elmajian Corporate Communications Riverside Resources Inc. relmajian@rivres.com Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com |

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Federal Reserve Fireworks This Wednesday According to Q?

After watching Federal Reserve chairman Jerome Powell change his tone in regards to Fed tightening over the last few months, the financial markets are largely expecting no action out of the central bank on Wednesday.

Although one potential wild-card has emerged, that could possibly make this week’s meetings one of the more memorable ones in recent times.

Certainly after watching the way the stock market started to really run into trouble last fall as interest rates were rising, it was hardly surprising to see the reversal by Powell and the Fed.

President Donald Trump even joined the action by criticizing the Fed for raising rates too quickly. Even though we’re a decade after the last crisis, and the Fed funds rate is still only at 2.5%.

Which is in direct contradiction to the notion that both Trump and the Fed have attempted to promote of the economy being strong and healthy. Because if that’s the case, why isn’t it time to normalize the rates and balance sheet yet?

However we live in a world where bankers and politicians don’t always do as they say, and don’t always say what they truly mean. During Trump’s election campaign he was talking about a gold standard, auditing the Fed, and how the stock market was a bubble. Now he’s done a 180 since then, and it’s a bit of a mystery what many of the key players might actually be thinking and planning.

Which is even more interesting now with the growing attention centered around the internet voice known as Q (or Qanon). Who many believe is a source of intelligence coming from within the White House.

To be clear, I am happy to admit that while I have been following the story, I am still discerning how much confidence I feel in the veracity of the posts. Yet with that said, I continue to hear from intelligent analysts who I trust and respect who have been completely won over and believe the messages are legitimate.

Which makes Q post 2575 rather intriguing. Especially ahead of this week’s Federal Reserve meeting.

(image courtesy of qanon.pub)

Whether this will manifest on Wednesday will be darn fascinating to watch. I have one reader who suggested to me that a 50-basis point hike may be coming this week. Which if that were to occur, especially given the context, would represent one of the more stunning events I can remember in financial history.

As not only would it serve as a confirmation of the messages Q has been sending, but also of the battle going on behind the scenes that many analysts and commentators have been talking about since before Trump took office.

Such a hike would also be significant in that it would be an indication towards the Fed really being prepared to let the bubbles pop. Which I was not sure they would ever really do, although if there is a 25-basis point hike, let alone a 50-basis point increase, the stock market conditions witnessed back in September and October could well end up looking like an appetizer compared to what would come next.

If nothing else, you can never argue that what’s going on is not more interesting than your average TV show. As Trump has essentially created the most fascinating reality show ever out of the Oval Office of the White House. And perhaps even regardless of what the Fed does this week, seeing how these bubbles are ultimately deflated will be some of the most stunning financial history the world has ever witnessed.

On Wednesday we get the next clue on how that path ultimately unfolds.

Chris Marcus

Arcadia Economics

“Helping You Thrive While We Watch The Dollar Die”

www.ArcadiaEconomics.com