Vancouver, British Columbia–(Newsfile Corp. – January 24, 2025) – EMPEROR METALS INC. (CSE: AUOZ) (OTCQB: EMAUF) (FSE: 9NH) (“Emperor” or the “Company“) is pleased to announce that it has paid Duparquet Assets Ltd., a private company owned 50% by Globex Mining Enterprises (“Globex“), the second year’s option payment to maintain Emperor’s option on the Duquesne West property in Duparquet township, Quebec, NTS-32D06. The option renewal for 2025 consisted of a $500,000 cash payment and the issuance of 3,671,569 common shares of Emperor equivalent to $300,000 based upon a 20-day volume weighted average price.

CEO John Florek commented: “We are excited to continue progressing with this option agreement. The compelling results from the 2024 drilling season have revealed the presence of visible gold within lower-grade zones, which could significantly impact both grade and total ounces in the open-pit environment. Infill drilling supports this scenario, and we look forward to the upcoming Q1 mineral resource estimate update.”

During 2024, Emperor undertook a 19-hole drill campaign totalling 8,166 meters and collected 7,994 meters of historical core as part of a program focused on outlining a near surface lower grade open pittable gold deposit rather than an underground higher grade mine. Pursuant to previous press releases, Emperor has announced both high grade and low grade intersections building upon the Company’s open pit model. Additional drill hole results are pending.

The Duquesne West property straddles the Porcupine-Destor Fault several kilometres east of the town of Duparquet, Quebec. A number of previous drill campaigns have outlined a historical inferred resource of 4.17 million tonnes grading 5.42 g/t Au (cut) or 6.36 g/t Au (uncut) as reported in the NI 43-101 report “Technical Report and Mineral Resource Estimate Update for the Duquesne-Ottoman Property, Quebec, Canada” by Watts, Griffis and McOuat, David Power-Fardy, M.Sc., Senior Geologist and Kurt Breede, P.Eng., Senior Resource Engineer dated October 20, 2011. This report is available on Globex’s website and is considered relevant and reliable. A “qualified person” as defined under NI 43-101 has not done sufficient work to classify the historical estimate as current mineral resources or mineral reserves. The Company is not treating the historical estimate as current mineral resources or mineral reserves.

The technical information in this press release was reviewed and approved by John Florek, P. Geo., President and CEO of Emperor in his capacity as the Company’s “qualified person”. For further information on the Duquesne West Property see Emperor’s press release dated October 12, 2022 available on SEDAR+.

About Emperor Metals Inc.

Emperor Metals Inc. is an innovative Canadian mineral exploration company focused on developing high-quality gold properties situated in the Canadian Shield. For more information, please refer to SEDAR+ (www.sedarplus.ca), under the Company’s profile.

CERTAIN STATEMENTS MADE AND INFORMATION CONTAINED HEREIN MAY CONSTITUTE “FORWARD-LOOKING INFORMATION” AND “FORWARD-LOOKING STATEMENTS” WITHIN THE MEANING OF APPLICABLE CANADIAN AND UNITED STATES SECURITIES LEGISLATION. THESE STATEMENTS AND INFORMATION ARE BASED ON FACTS CURRENTLY AVAILABLE TO THE COMPANY AND THERE IS NO ASSURANCE THAT ACTUAL RESULTS WILL MEET MANAGEMENT’S EXPECTATIONS. FORWARD-LOOKING STATEMENTS AND INFORMATION MAY BE IDENTIFIED BY SUCH TERMS AS “ANTICIPATES”, “BELIEVES”, “TARGETS”, “ESTIMATES”, “PLANS”, “EXPECTS”, “MAY”, “WILL”, “COULD” OR “WOULD”.

FORWARD-LOOKING STATEMENTS AND INFORMATION CONTAINED HEREIN ARE BASED ON CERTAIN FACTORS AND ASSUMPTIONS REGARDING, AMONG OTHER THINGS, THE ESTIMATION OF MINERAL RESOURCES AND RESERVES, THE REALIZATION OF RESOURCE AND RESERVE ESTIMATES, METAL PRICES, TAXATION, THE ESTIMATION, TIMING AND AMOUNT OF FUTURE EXPLORATION AND DEVELOPMENT, CAPITAL AND OPERATING COSTS, THE AVAILABILITY OF FINANCING, THE RECEIPT OF REGULATORY APPROVALS, ENVIRONMENTAL RISKS, TITLE DISPUTES AND OTHER MATTERS. WHILE THE COMPANY CONSIDERS ITS ASSUMPTIONS TO BE REASONABLE AS OF THE DATE HEREOF, FORWARD-LOOKING STATEMENTS AND INFORMATION ARE NOT GUARANTEES OF FUTURE PERFORMANCE AND READERS SHOULD NOT PLACE UNDUE IMPORTANCE ON SUCH STATEMENTS AS ACTUAL EVENTS AND RESULTS MAY DIFFER MATERIALLY FROM THOSE DESCRIBED HEREIN. THE COMPANY DOES NOT UNDERTAKE TO UPDATE ANY FORWARD-LOOKING STATEMENTS OR INFORMATION EXCEPT AS MAY BE REQUIRED BY APPLICABLE SECURITIES LAWS.

At Proven and Probable, we dive deep into the latest developments shaping the world of mining, royalties, and resource investments. 📈 Here’s what’s making headlines at EMX Royalty Corporation:

🔹 Strong Financial Results: EMX’s latest financial update showcases robust performance and strategic fiscal management. 🔹 Share Buyback Completion: The successful conclusion of their $5 million share buyback program underscores their commitment to enhancing shareholder value. 🔹 Strategic Divestment: EMX has executed an agreement to sell four projects in the western USA to Pacific Ridge Exploration, streamlining their portfolio. 🔹 Armenia Expansion: The acquisition of royalty interests in Hayasa’s Urasar Project further solidifies EMX’s position in the region. 🔹 Peruvian Opportunity: EMX’s purchase of a royalty on the Chapi Copper Mine highlights their continued focus on high-potential assets globally.

This is a pivotal moment for EMX Royalty, showcasing their strategic approach to growth, value creation, and global asset diversification.

A conversation with Maurice Jackson of ‘Proven and Probable’ and David Cole of EMX Royalty, the Royalty Generator – NYSE: EMX | TSX.V: EMX

Maurice: EMX Royalty is off to a strong start in 2025. For readers, could you briefly introduce EMX Royalty and its unique investment proposition?

David: Certainly. I’ll start by saying royalties are phenomenal financial instruments embedded with huge optionality, and you want to be exposed to a lot of royalties. My fundamental thesis is that the value of mineral rights is only going to go up over time, as it has throughout our lifetimes. The best way to be exposed to mineral rights is through royalty ownership.

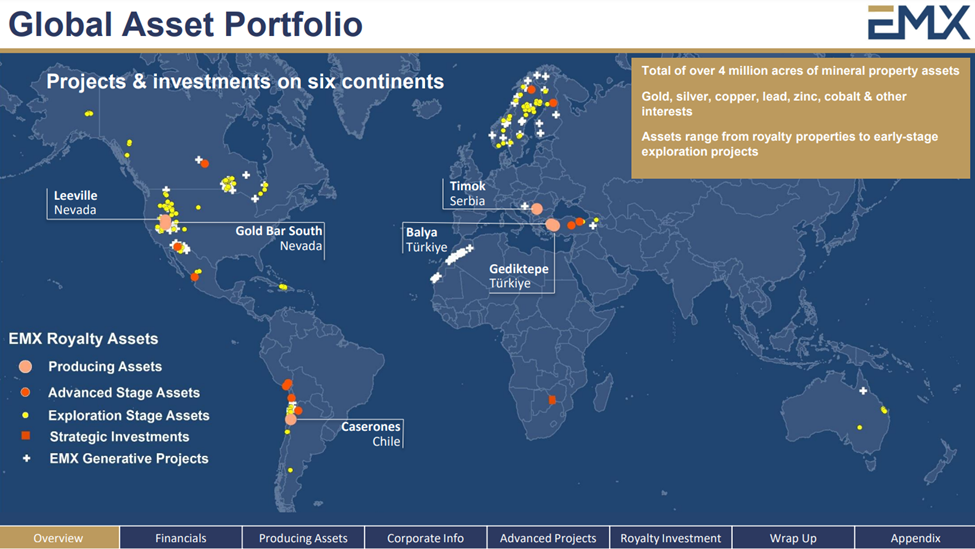

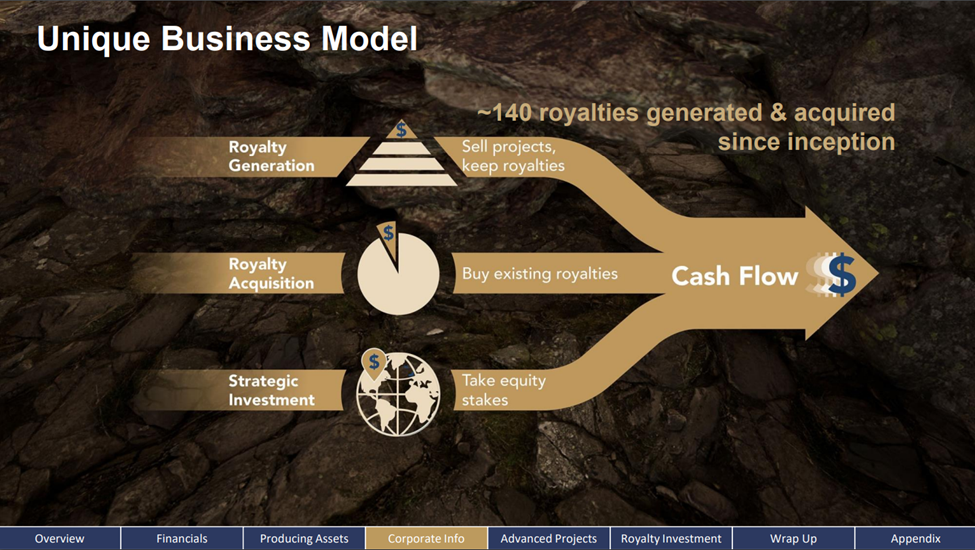

We accumulate royalties around the world, spanning 14 countries, and have built a portfolio of over 150 royalties. We do this through two primary mechanisms: acquiring royalties and generating royalties ourselves by acquiring mineral rights, adding value through geological data, selling assets, and retaining royalties.

Additionally, we make strategic investments along the way, which have been quite profitable. By integrating these three aspects into a synergistic business model, we have built a significant portfolio over the past two decades.

Maurice: You just referenced optionality. Could you expand on that term for someone who might be new to it?

David: That’s a fair question, Maurice, and I get asked about optionality often. It’s a common term within the industry. Essentially, optionality refers to the potential for outcomes—both good and bad—associated with an asset over time. There’s value that can be attributed to this potential.

The most significant aspect of optionality, in our view, is the potential for new discoveries. For example, if we generate or acquire a royalty on a project with a known resource—let’s say, a million ounces of gold in reserve with a 1% royalty—and during production, the geologists discover another half a million or even a million ounces, that additional discovery was not factored into our original acquisition price. That’s discovery optionality.

Other aspects of optionality include commodity prices, which can fluctuate. Over the course of my career, I’ve seen prices generally increase. Over time, as geological understanding improves, infrastructure is developed, and engineering and metallurgical techniques advance, the likelihood of additional discoveries and improved project economics increases.

A great example is the Goldstrike Royalty, which Pierre Lassonde of Franco Nevada acquired for $2 million Canadian dollars. Thanks to discovery optionality and other factors, that royalty has now generated over a billion dollars in cash flow and is still paying. It’s a tremendous example of how optionality can create extraordinary returns. Not every royalty turns out that way, of course, but the potential for these outcomes is what makes royalties so compelling.

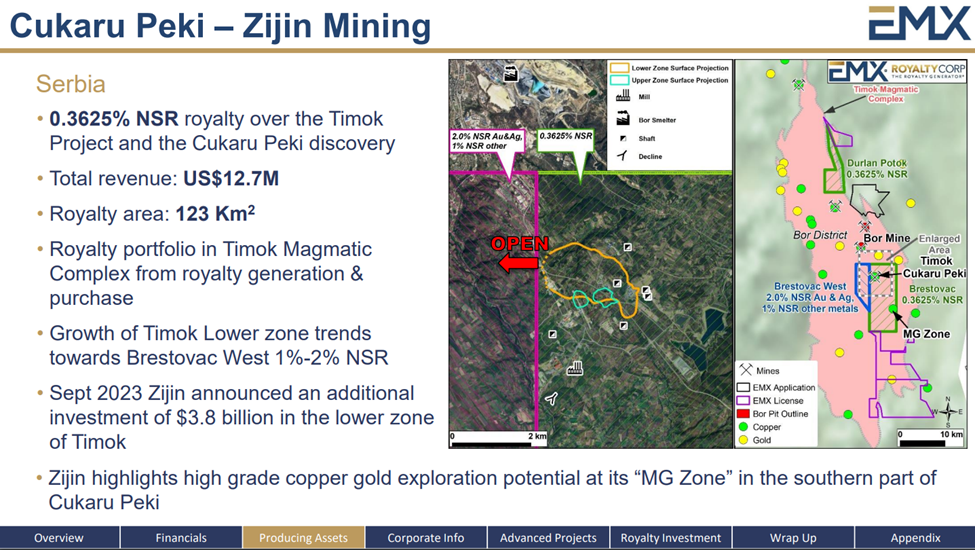

Maurice: Within your portfolio, you have the Timok investment—$200,000 initially, I believe. I don’t want to steal your thunder, so can you share the numbers with us?

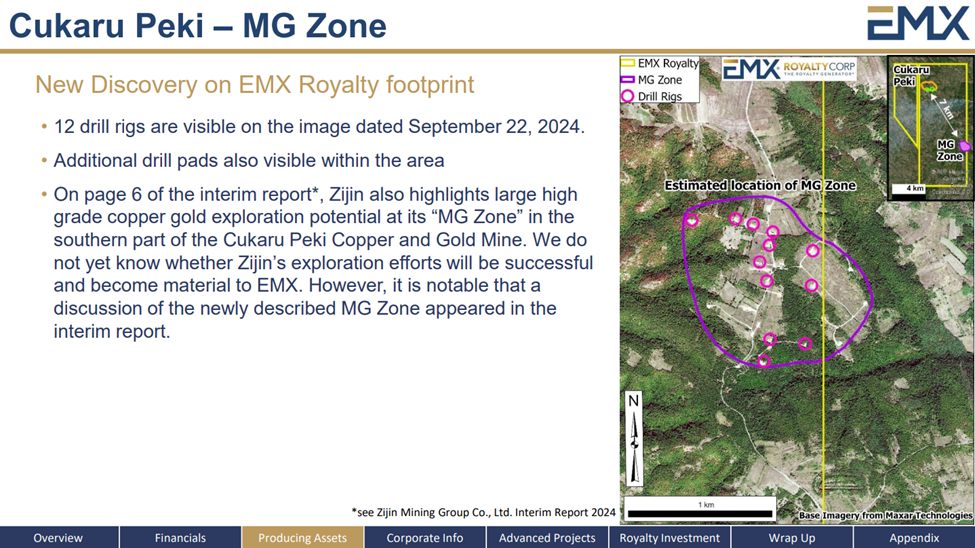

David: Certainly. So far, Timok has paid about $7 million to us. But that’s just the beginning—there’s potentially half a billion dollars or more coming to us over time based on the existing, known resource. And that’s before we fully account for the new MG Discovery. Zijin Mining recently announced in their last quarterly report that they’ve made a significant, high-grade copper-gold discovery within our royalty footprint. This new discovery is called the MG Zone.

We’ve been able to see its location through satellite imagery, but Zijin hasn’t disclosed the tonnage and grade yet. They’ve indicated they’ll provide more details in their next reporting period. We expect their annual report to be released toward the end of the first quarter or early second quarter.

Maurice: That’s a fantastic example. You mentioned commodity price optionality and the cost to shareholders. Could you explain how royalties mitigate those risks and costs?

David: Absolutely. The beauty of a royalty is that we get paid on the top-line revenue of a mine. Most of our royalties are net smelter return (NSR) royalties, which means we earn a percentage—commonly 1%-4%—of the revenue the mine receives from the smelter. As royalty holders, we don’t pay for the mine’s capital expenditures, exploration costs, or reclamation expenses. We simply receive our royalty payment based on production revenue. This structure exposes us to the upside potential of a project—like discoveries or commodity price increases—without the operational risks and costs borne by the mining company.

Maurice: That’s an profitable value proposition. Let’s transition to EMX’s recent developments. The company recently reported $27 million in cash and cash equivalents and $35 million in long-term debt maturing in 2029. How does this financial standing influence your strategic decisions for 2025 and beyond?

David: Capital allocation is one of the most critical decisions we make to benefit our shareholders. With our shares trading at a discount to price-to-net-asset value (PNAV), we’ve focused on buying back stock. Over the past year, we’ve purchased 5 million shares, fully utilizing the allotment permitted by the TSX exchange. We’ll likely apply for approval to buy back more in the coming year. We’re also incrementally paying down debt and acquiring royalties, all while generating cash flow from top assets like Timok, Caserones in Chile, and Carlin Trend in Nevada.

In addition to share buybacks, we plan to incrementally pay down debt, which, by the way, is held by Franco-Nevada—our capital partner and a significant shareholder. They’ve been a great partner in various royalty acquisitions.

Maurice: For shareholders who may not fully understand, how does the share buyback program impact EMX’s financial health?

David: By reducing the number of outstanding shares, we increase each shareholder’s proportional ownership in the company. When shares are trading below NAV, buybacks effectively create value for shareholders. It’s a tax-efficient alternative to dividends and reflects our confidence in the company’s intrinsic value. Of course, we’re also growing the portfolio organically and through strategic acquisitions, as you’ve seen with recent transactions.

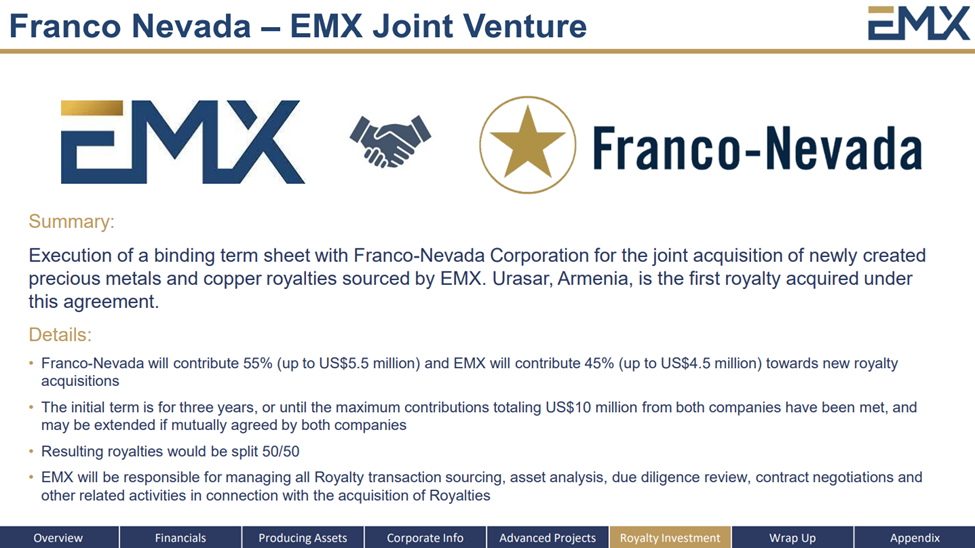

Maurice: Speaking of transactions, let’s start with Armenia, where EMX acquired a royalty interest in the Urasar gold-copper project. What motivated this acquisition, and what potential do you see in the project?

David: This acquisition was motivated by two factors: the geology of Armenia and our trust in the project’s steward, Dennis Moore. Dennis has a proven track record of world-class discoveries, and his involvement gives us confidence.

Geologically, Armenia offers excellent mineral potential, which aligns with our strategy of acquiring assets with strong long-term discovery potential. This royalty adds to the base of our portfolio, exposing us to future upside at minimal upfront cost.

Maurice: How does this transaction align with EMX’s broader strategy and portfolio?

David: This fits perfectly with our early-stage royalty acquisition strategy, where we aim to augment the foundation of our portfolio with assets that offer significant long-term potential.

This deal was part of our joint venture with Franco-Nevada, where they provide a premium for royalties we identify and acquire. This partnership not only validates our due diligence but also allows us to achieve a financial “lift” on the transaction.

Maurice: Let’s move to South America, where EMX recently acquired a royalty on the Chapi copper mine in Peru. Could you elaborate on the significance of this acquisition?

David: Certainly. The Chapi copper mine is located in a region with world-class copper endowment. This acquisition gives us exposure to a proven project with immediate cash-flow potential and substantial long-term discovery potential.

This project is being restarted by a team with a solid track record of copper production, and we anticipate cash flow within a couple of years. Beyond the restart, the exploration upside is what excites us most—it’s a classic example of how optionality can transform a royalty into a company-making asset.

Maurice: The optionality in the Chapi copper mine acquisition seems consistent with EMX’s strategy. Can you expand on the timing and significance of securing cash-flowing assets like this?

David: Acquiring cash-flowing or near-term cash-flowing assets is a deliberate part of our strategy. While we excel at generating royalties organically, the reality is that acquiring royalties on producing or development-stage assets can accelerate the financial returns to our shareholders.

The Chapi royalty exemplifies this. It strengthens our portfolio’s cash flow potential while maintaining long-term upside through exploration. By securing a mix of cash-flowing and earlier-stage royalties, we achieve a balanced portfolio that supports near-term financial health and long-term growth.

Maurice: Sticking in Peru, where EMX received an early property payment from Aftermath Silver. Aftermath Silver made an early $2.9 million property payment for the Berenguela project in Peru. How does this early payment impact EMX’s cash flow and plans for similar agreements?

David: EMX is fully supportive of what Aftermath Silver is doing on the ground there. They’re advancing a very interesting manganese and silver deposit, with some copper exploration on the property as well. We’re quite interested in that long-term copper optionality; there’s potential for the discovery of new copper deposits. But the manganese and silver deposit is particularly compelling.

The manganese, of course, is an important metal in the battery business, and this deposit has the potential to be a key source of manganese for batteries. That said, we’ll let them work on that. For us, a nice aspect is that we’re just sitting back here as a royalty holder. There are specific payments that have to be made to us over time. We’ve allowed them some flexibility—one payment was made a little late in exchange for an interest fee, and another was made a little early for a small reduction. We’re supportive of them advancing this asset. I believe it’s being managed by some very capable people.

Maurice: A good symbiotic relationship there. Now, let’s visit the U.S., where EMX announced the sale of four projects to Pacific Ridge Exploration. What benefits does this transaction bring to EMX, and how does it align with your growth strategy?

David: This is right down the alley of EMX’s bread-and-butter royalty generation business. We go out, acquire prospective mineral rights—commonly very inexpensively—consolidate data, collect additional field data, and illustrate prospectivity by building geological models. These models demonstrate the potential for significant gold or copper deposits. We then sell the projects on, often to junior companies, for a combination of commercial terms. These typically include share payments, incremental payments over time, and always a royalty at the end of the day.

This transaction with Pacific Ridge is just another example of what we do repeatedly—roughly 20 projects a year, and we might exceed that this year. These deals build long-term discovery optionality at the base of our portfolio pyramid. At the top, we have producing royalties; at the base, we have exploration assets being advanced using other people’s expertise and money, with EMX as the long-term beneficiary.

Maurice: Diversification seems to be a recurring theme in EMX’s strategy. How does the company ensure that its acquisitions align with its broader objectives?

David: Diversification is indeed one of our core principles. When evaluating acquisitions, we focus on several key criteria: the quality of the underlying asset, the jurisdiction, the operator’s track record, and the potential for long-term upside.

Our acquisitions span various geographies, commodities, and stages of development to reduce risk and enhance returns. For example, our portfolio includes royalties on gold, copper, and polymetallic projects in North and South America, Europe, Asia, and Australia. This global reach allows us to capitalize on opportunities in different markets while mitigating exposure to regional risks.

Maurice: It’s clear that EMX has been strategic in its acquisitions. As we wrap up, what’s next for the company in 2025 and beyond?

David: We’re fortunate to be in a strong position with positive cash flow for seven consecutive quarters. We anticipate this continuing for some time, driven by key assets like our Caserones royalty in Chile, operated by Lundin Mining Corporation. That’s performing nicely, with significant exploration work ongoing.

Zijin Mining is also producing at Timok in Serbia, generating handsome payments. Additionally, our royalty on the Carlin Trend in Nevada—advanced and produced by Barrick as part of their joint venture with Newmont—is generating over $4 million annually.

With these assets delivering robust returns, our focus is on astute capital allocation. This includes paying down debt, buying back shares while undervalued, and pursuing incremental acquisitions like the one at the Chapi Mine in Peru.

Maurice: Has EMX considered changing its logo to a cow surrounded by cash? EMX is quite literally becoming a cash cow.

David: I’ve said for years we’d become one, and we have! We’re thrilled to be in this position, allocating cash strategically to grow the portfolio, buy more royalties, and repurchase shares when the price is low. Managing long-term debt and driving shareholder value remains our priority.

Maurice: You’ve touched on this, but how do you plan to navigate potential challenges in the current market environment?

David: The money is coming in, and our royalties are performing exceptionally well. While metal prices are strong, the natural resource capital markets have been tough. It’s an intriguing bifurcation, but we’re capitalizing on our strengths.

By buying back stock at a discount to our net asset value, we maximize value. Once rectified, we’ll allocate more capital to expand the royalty portfolio. It’s about understanding and deploying our capital effectively in any market.

Our portfolio also boasts exciting developments. For instance, Zijin’s MG Zone in Serbia, with 12 drill rigs on-site, is remarkable. South 32’s Peak Discovery in Arizona could be a game-changer with promising copper-zinc-silver drill results. These discoveries reinforce why owning royalties is so valuable.

Maurice: Absolutely! In closing, what did I forget to ask?

David: Nothing comes to mind, Maurice. Insider buying, share buybacks, strong cash flow, and global discoveries—all make EMX a company worth following.

Maurice: If someone wants to learn more about EMX Royalty, where can they go?

What will the stock market look like in 2025, a year that has started grimly with catastrophic fires burning in California and dangerous snow and ice blanketing the east even before the presidential inauguration?

While interviewing 321gold’s Bob Moriarty this week on CEO & Market Expert Interviews on YouTube, Lucijan Valkovic said his own unofficial private polling found that 95% of people he asked said the market is heavily overvalued and is “about to crash or correct big.”

Moriarty said that while he was a “contrarian,” and it scares him “when 95% of people agree on anything,” the market is “clearly in a bubble.”

“The stock market is a giant bubble in search of a pin,” said Moriarty.

“There are some immense forces in play (and) no one can really predict what’s going to happen,” he said. “However, it’s very easy to predict whatever happens is going to be bad. So, my belief is the stock market’s an accident waiting to happen. And it’s like Bitcoin, you’ve got a lot of people playing musical chairs. And everybody thinks when the music stops, they’re going to be able to reach a chair. And there’s one slight problem with that theory, . . . and that is, what if there’s no chairs?”

Moriarty predicted the fall would be worse than 1929, “much worse.”

“We are going to go through pain, and it’s going to be extreme pain because this economy is so far out of whack,” he said.

Precious Metals as Insurance Policies

How to protect yourself? “You should put your money in something that is not part of the bubble,” Moriarty said.

“I happen to believe the highest value of precious metals is not their investment potential; it’s their potential as an insurance policy against chaos,” he said. “But the cheapest thing in the world right now is resource stocks. They’re literally being given away.”

The world’s central banks have “added significant amounts of gold to their reserves in recent years — and their buying continues even as gold’s price reaches new highs,” Sharon Wu reported for CBS News in December.

“While the precious metal offers unique protections during economic uncertainty, it also comes with challenges,” she wrote. “Storage costs and lack of income generation, for example, make it a complex investment choice.”

However, Valkovic noted that central bank gold purchases are expected to continue this year.

Gold and silver are insurance policies “against financial chaos,” Moriarty told him. “We all need reserves. You need it as an individual. You need it as a family. You need it as a town or city. You need it as a country. And you certainly need it as a bank.”

Moriarty said the banks are looking at the world and the state of the economy and deciding they need extra protection from negative events.

“There are some very dangerous black swans flying, and we need to protect ourselves,” he said. ” And that’s exactly the reason that individuals should be doing the same thing.”

Could Silver Outperform Gold?

Both gold and silver recently hit four-week highs, and gold is expected to have another solid year, but investors should brace for some volatility and temper their upside expectations, Kirill Kirilenko, Senior Analyst at CRU, told Kitco News’ Neils Christensen.

But he predicted gold prices would average around US$2,580 per ounce in 2025 as markets react to Trump’s proposed economic policies. The analyst had more optimism for silver, forecasting an average price of US$31.35 per ounce for the year.

“Silver could slightly outperform gold this year, driven by an increasingly tight fundamental outlook,” he said.

The British research firm expects silver, which as nature’s most conductive metal remains integral to the green energy transition, to remain well-supported.

Moriarty gave another reason for looking at the white metal. “Silver is absurdly cheap,” he said. “My belief is if you’re faced with three or four different alternatives for investing, you should buy what’s cheap, and you should save.”

“Silver has got a long way to run,” Moriarty said. “My opinion is silver will always be the most attractive investment in the resource sector.”

Nuclear: Very Cheap, Very Safe

Moriarty also said he saw uranium stocks performing well as artificial intelligence (AI) and a surging number of data centers recently helped push the price for element, the main fuel for nuclear reactors, to a record high, according to a Yolowire release posted on Barchart.

Prices for enriched uranium rose to US$190 per separative work unit, the commodity’s standard measure, which is up 239% from US$56 three years ago,” according to the report.

“A resurgence of interest in nuclear power has come as governments and companies source carbon-free power to service major industrial facilities and communities,” the release said.

“Nuclear power is a very cheap, very safe form of energy,” Moriarty said. “And we need more of it. … Green energy has been oversold. It is not a solution. It is a very expensive problem.”

But which uranium stocks to invest in? “I think you could walk into a dark room, and you could put the names of the stocks up on a wall. You could shut the light off and throw a dart, and hit something. Uranium is very cheap.”

Moriarty said he doesn’t know which bubble will burst first. But “we’ve got a lot of bubbles, and it is a time for safety, and in a time for safety, you go for what is the least bubbly,” he said.

“The least bubbly, I like that,” agreed Valkovic.

Want to be the first to know about interesting Gold, Silver, Special Situations and Uranium investment ideas? Sign up to receive the FREE Streetwise Reports’ newsletter.

Steve Sobek wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

North Vancouver, British Columbia–(Newsfile Corp. – January 23, 2025) – Lion One Metals Limited (TSXV: LIO) (OTCQX: LOMLF) (“Lion One” or the “Company“) is pleased to report significant new high-grade gold results from 3,866.8 metres of infill and grade control drilling at its 100% owned Tuvatu Alkaline Gold Project in Fiji. The drilling is focused on Zone 5 and includes the Zone’s best assay result to-date of 2,749.86 g/t of gold over 0.3 metres (88.42 oz/t of gold over 1.0 feet).

All drilling was completed from existing near surface underground workings. The Company intersected high-grade mineralized structures in 24 holes drilled up-dip, down-dip, and south along strike of the UR2 and URW3 lodes where current mining activities are in progress. 17 holes intersected multiple high-grade mineralized structures, all of which are near existing underground workings. Most of the drill holes did not exceed 130 metres in length from underground drill stations. Drill results include multiple bonanza grade assays such as 2,749.86 g/t, 269.5 g/t and 235.2 g/t over narrow widths of 0.3 metres. Due to proximity of drill results to existing workings there is a strong probability that some of these structures can be incorporated into the mine plan in the next six to twelve months.

Bonanza grades in Zone 5 at the Tuvatu Alkaline Gold Project are not unexpected. Previously the Company announced high-grade drill results from Zone 5 including 1,986.23 g/t gold over 0.6 metres (see press release dated December 13, 2023), 1,568.55 g/t over 0.3 metres (see press release dated June 5, 2024), and 1,517.79 g/t over 0.3 m (see press release dated December 17, 2024).

Lion One Chairman and CEO Walter Berukoff commented: “We’re extremely pleased with the new results from our Zone 5 infill and grade control drill program. These significant underground drill results continue to confirm the high-grade nature of the Tuvatu Alkaline gold system and provide strong support for our ongoing mining efforts in Zone 5. We’re excited to expand our near-term mine plan in Zone 5 and look forward to mining these areas in 2025. I was particularly interested to see that three of the highest-grade intersections were all identified in hole TGC-265 as separate and distinct structures.”

Highlights of New Drill Results:

2,749.86 g/t Au over 0.3 metres (TGC 265, from 96.2 m depth) Best assay to-date in Zone 5

162.97 g/t Au over 0.6 m (including 269.5 g/t Au over 0.3 m) (TGC-281, from 75.89 m depth)

53.11 g/t Au over 1.5 m (including 235.2 g/t over 0.3 m) (TGC-282, from 92.6 m depth)

96.5 g/t Au over 0.6 m (TGC-288, from 28.8 m depth)

46.94 g/t Au over 1.2 m (including 86.44 g/t Au over 0.3 m) (TGC-265, from 45.7 m depth)

47.22 g/t Au over 0.9 m (including 62.25 g/t over 0.3 m (TGC-265, from 81.1 m depth)

69.38 g/t Au over 0.6 m (including 126.5 g/t over 0.3 m (TGC-267, from 125 m depth)

*Drill intersects are downhole lengths, 3.0 g/t cutoff. See Table 1 in Appendix for additional data.

Figure 1. Location of the Zone 5 drilling reported in this news release. Left image: Plan view of Tuvatu showing Zone 5 drillholes in relation to the mineralized lodes at Tuvatu, shown in grey. Yellow dashed square represents the area shown in the right image. Right image: Oblique view of Zone 5 drilling looking approximately east-northeast. Zone 5 drilling is targeting the up-dip and down-dip extensions of the mineralized lodes above and below current underground developments, shown in red.

The Zone 5 area of Tuvatu is located along the main decline and includes the principal north-south oriented lodes (UR1 to UR3), the principal northeast-southwest oriented lodes (UR4 to UR8), and several of the western lodes (URW2, URW2A, URW3). These lodes are steeply dipping structures that converge at approximately 500 m depth to form Zone 500, which is the highest-grade part of the deposit and is interpreted to be a major feeder zone at Tuvatu. The system remains open at depth with the deepest high-grade intersections occurring below 1000 m depth.

The drilling reported in this news release targeted the near-surface portions of the UR2 and URW3 lodes. Drilling was focused on the up-dip and down-dip areas of the UR2 and URW3 lodes, directly above and below current underground developments. The drilling targeted a 200 m strike length of the UR2 and URW3 lodes. The current total strike length of the UR2 lode is approximately 620 m, while that of the URW3 lode is approximately 330 m. Both lodes remain open along strike and at depth.

The Zone 5 grade control drilling reported in this release was conducted from two underground locations: the 1135 drill station and the 1090 drill station. These drillholes are designed to intersect the mineralized lodes in a perpendicular to sub-perpendicular orientation such that the mineralized intervals approximate the true width of the lodes. Grade control drilling is being conducted on a 10 m grid to provide a detailed understanding of the geometry and mineralization of the Zone 5 lodes. The purpose of the current Zone 5 grade control drill program is to enhance the mine model and inform stope design in advance of mining in the target areas. The majority of the high-grade intervals reported in this release are located within 30 m of underground developments and are anticipated to be included in the mine plan in 2025. Highlights of the Zone 5 drilling reported here are shown in Figure 2.

Figure 2. Zone 5 infill and grade control drilling with high-grade intersects highlighted, 3.0 g/t gold cutoff. Plan view looking down with north to the left. The primary areas targeted by the Zone 5 drilling are the up-dip and down-dip areas of the UR2 and URW3 lodes above and below current underground developments. These areas are scheduled for near-term mining. Drill holes are oriented perpendicular to sub-perpendicular to the mineralized lodes.

The information in this report that relates to mineral exploration at the Tuvatu Gold Project is based on information compiled by the Lion One team and reviewed by Melvyn Levrel, who is the company’s Senior Geologist. Mr Levrel is a Member of the Australian Institute of Geoscientists and has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration, and to the activity being undertaken, to qualify as a Qualified Person as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43- 101”). Mr Levrel consents to the inclusion in this report of the matters based on the information in the form and context in which it appears.

Lion One Laboratories / QAQC

Lion One adheres to rigorous QAQC procedures above and beyond basic regulatory guidelines in conducting its drilling, sampling, testing, and analyses. The Company operates its own geochemical assay laboratory and its own fleet of diamond drill rigs using PQ, HQ and NQ sized drill rods.

Diamond drill core samples are logged by Lion One personnel on site. Exploration diamond drill core is split by Lion One personnel on site, with half core samples sent for analysis and the other half core remaining on site. Grade control diamond drill core is whole core assayed. Core samples are delivered to the Lion One Laboratory for preparation and analysis. All samples are pulverized at the Lion One lab to 85% passing through 75 microns and gold analysis is carried out using fire assay with an AA finish. Samples that return grades greater than 10.00 g/t Au are re-analyzed by gravimetric method, which is considered more accurate for very high-grade samples.

Duplicates of 5% of samples with grades above 0.5 g/t Au are delivered to ALS Global Laboratories in Australia for check assay determinations using the same methods (Au-AA26 and Au-GRA22 where applicable). ALS also analyses 33 pathfinder elements by HF-HNO3-HClO4 acid digestion, HCl leach and ICP-AES (method ME-ICP61). The Lion One lab can test a range of up to 71 elements through Inductively Coupled Plasma Optical Emission Spectrometry (ICP-OES), but currently focuses on a suite of 26 important pathfinder elements with an aqua regia digest and ICP-OES finish.

About Lion One Metals Limited

Lion One Metals is an emerging Canadian gold producer headquartered in North Vancouver BC, with new operations established in late 2023 at its 100% owned Tuvatu Alkaline Gold Project in Fiji. The Tuvatu project comprises the high-grade Tuvatu Alkaline Gold Deposit, the Underground Gold Mine, the Pilot Plant, and the Assay Lab. The Company also has an extensive exploration license covering the entire Navilawa Caldera, which is host to multiple mineralized zones and highly prospective exploration targets.

On behalf of the Board of Directors, Walter Berukoff, Chairman & CEO

Neither the TSX-V nor its Regulation Service Provider accepts responsibility or the adequacy or accuracy of this release

This press release may contain statements that may be deemed to be “forward-looking statements” within the meaning of applicable Canadian securities legislation. All statements, other than statements of historical fact, included herein are forward-looking information. Generally, forward-looking information may be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “proposed”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases, or by the use of words or phrases which state that certain actions, events or results may, could, would, or might occur or be achieved. This forward-looking information reflects Lion One Metals Limited’s current beliefs and is based on information currently available to Lion One Metals Limited and on assumptions Lion One Metals Limited believes are reasonable. These assumptions include, but are not limited to, the actual results of exploration projects being equivalent to or better than estimated results in technical reports, assessment reports, and other geological reports or prior exploration results. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance, or achievements of Lion One Metals Limited or its subsidiaries to be materially different from those expressed or implied by such forward-looking information. Such risks and other factors may include, but are not limited to: the stage development of Lion One Metals Limited, general business, economic, competitive, political and social uncertainties; the actual results of current research and development or operational activities; competition; uncertainty as to patent applications and intellectual property rights; product liability and lack of insurance; delay or failure to receive board or regulatory approvals; changes in legislation, including environmental legislation, affecting mining, timing and availability of external financing on acceptable terms; not realizing on the potential benefits of technology; conclusions of economic evaluations; and lack of qualified, skilled labor or loss of key individuals. Although Lion One Metals Limited has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated, or intended. Accordingly, readers should not place undue reliance on forward-looking information. Lion One Metals Limited does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

Appendix 1: Full Drill Results and Collar Information

Table 1. Collar coordinates for drillholes reported in this release. Coordinates are in Fiji map grid.

Hole ID

Easting

Northing

Elevation

Azimuth

Dip

Depth

TGC-0265

1876384

3920429

94

87.7

-11.1

116.0

TGC-0267

1876380

3920530

129

109.8

-10.5

131.0

TGC-0268

1876384

3920429

94

96.1

-14.0

10.7

TGC-0269

1876384

3920429

94

96.3

-10.3

110.2

TGC-0271

1876381

3920530

130

114.8

10.5

136.6

TGC-0273

1876384

3920429

94

103.2

-10.9

91.8

TGC-0275

1876384

3920428

94

111.2

-9.9

85.8

TGC-0277

1876384

3920428

94

119.3

-10.5

85.7

TGC-0278

1876381

3920530

131

116.9

20.3

135.0

TGC-0279

1876385

3920425

96

140.4

11.7

90.6

TGC-0281

1876384

3920425

96

154.2

11.6

102.5

TGC-0282

1876381

3920530

131

113.2

14.8

139.2

TGC-0284

1876381

3920530

131

108.5

19.8

135.7

TGC-0286

1876383

3920424

96

165.4

12.4

111.5

TGC-0287

1876381

3920532

131

88.2

14.4

118.0

TGC-0288

1876381

3920531

131

96.7

14.1

115.1

TGC-0289

1876383

3920424

96

175.0

10.5

126.3

TGC-0291

1876381

3920532

131

87.4

20.0

120.7

TGC-0292

1876382

3920425

94

174.2

-10.4

13.7

TGC-0294

1876382

3920425

94

174.8

-12.5

127.7

TGC-0295

1876381

3920531

131

95.2

23.0

180.7

TGC-0296

1876382

3920426

94

175.2

-24.6

152.1

TGC-0297

1876381

3920530

131

102.0

23.1

120.0

TGC-0299

1876382

3920426

94

174.8

-35.5

200.7

TGC-0300

1876381

3920530

130

104.1

13.5

122.1

TGC-0301

1876381

3920531

130

96.2

13.3

121.4

TGC-0302

1876383

3920425

94

160.5

-10.5

112.8

TGC-0303

1876380

3920530

129

120.6

-20.6

160.0

TGC-0304

1876383

3920426

94

155.6

-31.4

122.6

TGC-0306

1876380

3920529

129

126.1

-19.6

160.1

TGC-0307

1876383

3920426

93

154.5

-44.9

154.1

TGC-0309

1876384

3920427

93

130.5

-45.1

140.6

TGC-0310

1876380

3920532

128

78.4

-48.0

15.8

Table 2. Composite intervals from drillholes reported in this news release (composite grade >3.0 g/t Au, with <1 m internal dilution at <3.0 g/t Au).

We’re diving into the latest developments on the acquisition of the Motherlode Crown Grants—a significant addition to the Greenwood Precious Metals and Battery Metals Project in British Columbia. 🏔️

With historical production of copper, gold, and silver, coupled with promising exploration results, Grizzly Discoveries is well-positioned to play a critical role in meeting the demand for precious and battery metals. 🚀

📹 Watch the video to uncover: ✅ Key highlights of the Motherlode Crown Grants ✅ Exploration updates and high-grade sample results ✅ The strategic potential of this acquisition

💡 Don’t miss this chance to learn about the growth of Canadian resource exploration and its role in powering the future of clean energy!

Vancouver, British Columbia–(Newsfile Corp. – January 17, 2025) – Riverside Resources Inc.(TSXV: RRI) (OTCQB: RVSDF) (FSE: 5YY) (“Riverside” or the “Company”), is pleased to present its 2025 outlook while highlighting key milestones accomplished during 2024. With a 100% owned portfolio of high-potential exploration projects, a robust financial position, and well-established strategic partnerships, Riverside remains focused on delivering value through a disciplined and exploration-driven approach. The Company is committed to advancing its assets, fostering new opportunities, and positioning itself for sustained growth and success in the evolving resource sector.

The Company is in a strong cash position, with over C$4 million in cash reserves, no outstanding debt, and a tightly managed share structure with fewer than 75 million shares outstanding and no warrants. This robust financial foundation provides Riverside with the flexibility to advance its exploration initiatives and capitalize on emerging opportunities in North America as it continues to build its royalty portfolio of precious and base metals.

With a focus on maintaining fiscal discipline and strategically allocating resources, Riverside is well-positioned to pursue high-potential projects across its diverse portfolio. The Company’s financial stability and its ability to source high-potential projects enhance its ability to attract partnerships and drive shareholder value through exploration success and asset development. These factors, along with Riverside’s proven track record of delivering results, create a strong foundation for growth, the potential spinout of new businesses to shareholders, and continued exploration success in 2025 and beyond.

“Building on the strong foundation progressed in 2024, Riverside is poised to unlock key opportunities in 2025,” said Riverside’s President and CEO, John-Mark Staude. “With a solid financial position, a diverse portfolio of high-quality projects, and strategic partnerships, we are advancing our exploration efforts in Canada and Mexico while capitalizing on royalty opportunities and ongoing transactions to drive value creation.

The first half of 2025 is shaping up to be an active and pivotal period for Riverside. We are moving forward with plans to spin out our Ontario gold assets into a separate exploration company, a strategic initiative designed to unlock additional value for shareholders and provide secondary liquidity potential. Additionally, we are working closely with our partner, Fortuna Mining, on follow-on exploration the drilling success of 2024 with a program at the Cecilia Project in Mexico, on discovering now high-grade mineralization at the system the Company delineated during the 2024 program. Updates on both initiatives will be shared early in the year.

In British Columbia, we are prioritizing exploration for gold and rare earth elements across key properties, including the Deer Park, Revel and Taft projects, to take advantage of growing demand for critical minerals. These projects represent exciting opportunities to expand our resource base and further diversify our portfolio in a stable Canadian jurisdiction with drive up access and easy delivery to markets.

Looking ahead, we are actively evaluating potential acquisitions to grow our property portfolio in another North American jurisdiction. This expansion aligns with our strategy to capitalize on favorable markets and enhance Riverside’s position as a leader in exploration-driven value creation. With these initiatives and a strengthening commodities market, we are confident in our ability to deliver meaningful results and shareholder value in 2025.”

2025 Strategic Goals and Potential Milestones

Advancing Canadian Assets:

In the first half of 2025, Riverside Resources plans to present a proposal to its shareholders for the potential spinout of its Ontario gold properties-Pichette, Oakes, and Duc-into a dedicated exploration company named Blue Jay Gold (Resources). This strategic initiative aims to create a standalone entity that will focus exclusively on advancing these high-potential gold assets, strategically located within the prolific Geraldton-Beardmore Greenstone Belt in Northwestern Ontario. Shareholders previously benefited from the successful spinout of Capitan Mining (TSXV: CAPT) in 2021, as highlighted in Riverside’s press release at the time. Now, shareholders have another opportunity to unlock value through the proposed spinout of Riverside’s Ontario gold assets into a new company. This initiative aims to create a focused exploration entity, providing shareholders with direct exposure to its potential success and unlocking the embedded value within Riverside’s portfolio.

Riverside intends to execute follow-up exploration on its gold and rare earth element properties in British Columbia with a focus on advancing these projects to drill-ready status. Planned work includes detailed mapping, geochemical sampling, and geophysical surveys to refine targets and evaluate resource potential. Riverside aims to capitalize on the growing demand for gold and critical minerals, leveraging its technical expertise to advance these high-potential assets while seeking partnerships to accelerate exploration efforts.

Mexico Exploration and Partnerships:

The Company is collaborating closely with our partner, Fortuna Mining, to design and launch a follow-on exploration program at the Cecilia Project in Mexico. This next phase of exploration will continue to delineate and define the full extent of the mineralized system, building on the results from the successful 2024 drill program. By focusing on key structural zones and high-priority areas identified through geophysical surveys and earlier drilling, we aim to target higher-grade gold zones and large-scale deposits.

This planned program will include additional detailed mapping and geochemical analysis to refine targets and identify areas of significant gold and silver potential. Geophysics is also planned to refine targets ahead of the next 2025 drill program at Cecilia based upon this spring 2025 exploration results. The project exhibits many technical similarities to nearby operations, such as the Santa Elena District, where Coeur Mining recently acquired Silvercrest Metals for over $1 billion USD, and First Majestic’s most productive operation in Mexico. Updates on this initiative, along with the drill results from the 2024 program, are expected to be shared in Q1 2025 as laboratory results are finalized.

Pursue additional joint ventures or sale agreements for key projects such as Union and Ariel to further de-risk and monetize Riverside’s asset base. This strategic approach aligns with the Company’s goal of diversifying beyond Mexico while capturing value from the high-quality assets developed over the past five years.

Royalty and Strategic Opportunities:

Actively advance and expand Riverside’s royalty portfolio to enhance its value as key royalties are developed and progressed through the pipeline by major partners, such as Fresnillo PLC. The portfolio includes significant assets, such as the Net Smelter Return (NSR) royalty on the Tajitos Gold Project in Mexico with Fresnillo, which holds promising potential for future production. Fresnillo is actively advancing development and permitting at Tajitos with the project well-positioned for continued progress toward production, enhancing the royalty’s value. Further, the recent election of Mexico’s new President, who has maintained a pro-business stance bolsters the attractiveness of the Tajitos NSR.

Continue advancing discussions with U.S.-based exploration groups and other partners across the Americas to explore potential generative exploration alliances. These partnerships and portfolios have the potential to strategically enhance value for Riverside shareholders over the coming year.

Corporate Development:

Maintain a strong focus on financial discipline while strategically expanding and upgrading the Company’s portfolio of quality mineral assets. Riverside remains committed to managing its capital prudently, ensuring resources are allocated efficiently to projects with the highest potential for discovery and value creation. This disciplined approach enables the Company to advance its exploration initiatives while safeguarding its robust balance sheet.

As part of this strategy, Riverside will prioritize opportunities to acquire high-quality assets in mining-friendly jurisdictions, leveraging its proprietary databases and technical expertise to identify projects with significant upside potential. In addition to its current focus in Canada and Mexico, the Company is exploring the potential for acquisitions in another mining-friendly North American jurisdiction, further diversifying its asset base and creating new growth opportunities.

Actively engage with the investment community through attending conferences and events, including Vancouver Round Up, PDAC 2025, Swiss Mining Institute, the Rule Symposium 2025

2024 Recap and Highlights

Canada

Ontario Projects:

Riverside transferred its three key projects into a new subsidiary company, strategically positioning them for a potential unlocking of value in 2025.

Pichette Gold Project: through integrating structural geology LiDAR and geochemical data Blue Jay Gold has identified several new zones with mineralization. Recent fieldwork led to the discovery of mineralized banded iron formations, with samples returning assays up to 21 g/t gold. (Press Release, February 29, 2024)

Duc Project: The company completed a Light Detection and Ranging (LiDAR) survey, enhancing the understanding of surface projections and structural features. This data coupled with last year’s magnetics survey has improved the targeting for future exploration, particularly in identifying major shears indicative of Abitibi greenstone-style gold deposits.

Blue Jay Gold (Resources) Spinout: Riverside announced plans to transfer its Ontario gold assets, including Pichette, Oakes, and Duc, into a wholly owned subsidiary, Blue Jay Gold. (Press Release, November 14, 2024) This strategic move aims to unlock shareholder value by creating a focused exploration company dedicated to advancing these high-potential gold projects in the Geraldton-Beardmore Greenstone Belt.

British Columbia Projects:

Deer Park and Sunrise Gold Projects: Riverside has an option to acquire these projects north of Castlegar and the Rossland Gold Camp. Initial exploration identified two main targets: Viking Horde and Cougar Ridge with rock samples returning assays up to 7.07 g/t gold. These acquisitions align with Riverside’s strategy to expand its presence in British Columbia’s prolific mining regions.

Taft Project: The company secured an option to acquire a 100% interest in the Taft Project, covering 3,000 hectares in the Perry River Carbonatite Belt west of Revelstoke. This project is prospective for rare earth elements and gold, aligning with Riverside’s focus on critical minerals essential for renewable energy and advanced technologies.

Mexico

Cecilia Project: Riverside, in collaboration with Fortuna Mining, launched a fully funded 2,250-meter drill program targeting geologic exploration zones: the Agua Prieta Breccia, East Target, and Mayra vein system. This program expanded on previous exploration efforts to delineate and define the strength and continuity of hydrothermal alteration which was supported by geophysical and field data. This partnership highlights Cecilia’s potential as a cornerstone asset in Sonora and demonstrates Riverside’s expertise in leveraging its extensive Mexican database to identify high-quality opportunities that secure partnerships.

Union Project: Riverside has continued to consolidate the Union Project district by securing property agreements and integrating the data from multiple properties. This effort is aimed at developing a comprehensive, district-wide understanding of the geological framework and identifying high-priority exploration targets. The Company signed a Letter of Intent (LOI) with Questcorp Mining Inc. for an option agreement to acquire a 100% interest in the Union Project for which the Company was paid a fee of $12,500. (Press Release, September 6, 2024). The agreement includes $5.5 million in exploration expenditures, cash payments, and share issuances over four years, with Riverside retaining a 2.5% NSR royalty. Exploration efforts in 2024 focused on mapping, sampling, and geochemical surveys, identifying high-grade gold and zinc zones. These findings have positioned the project for further development in partnership with Questcorp.

Ariel Copper-Gold Project: The company has continued to advance the Ariel Project by consolidating landholdings and conducting early-stage exploration. Riverside has identified porphyry copper-gold-molybdenum potential across a 16 km² area. Recent efforts have focused on securing joint venture opportunities to unlock the project’s value.

Qualified Person & QA/QC:

The scientific and technical data contained in this news release was reviewed and approved by Freeman Smith, P.Geo, a non-independent qualified person to Riverside Resources who is responsible for ensuring that the information provided in this news release is accurate and who acts as a “qualified person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects.

About Riverside Resources Inc.:

Riverside is a well-funded exploration company driven by value generation and discovery. The Company has over $4M in cash, no debt and less than 75M shares outstanding with a strong portfolio of gold-silver and copper assets and royalties in North America. Riverside has extensive experience and knowledge operating in Mexico and Canada and leverages its large database to generate a portfolio of prospective mineral properties. In addition to Riverside’s own exploration spending, the Company also strives to diversify risk by securing joint-venture and spin-out partnerships to advance multiple assets simultaneously and create more chances for discovery. Riverside has properties available for option, with information available on the Company’s website at www.rivres.com.

ON BEHALF OF RIVERSIDE RESOURCES INC.

“John-Mark Staude”

Dr. John-Mark Staude, President & CEO

For additional information contact:

John-Mark Staude President, CEO Riverside Resources Inc. info@rivres.com Phone: (778) 327-6671 Fax: (778) 327-6675 Web: www.rivres.com

Eric Negraeff Investor Relations Riverside Resources Inc. Phone: (778) 327-6671 TF: (877) RIV-RES1 Web: www.rivres.com

Certain statements in this press release may be considered forward-looking information. These statements can be identified by the use of forward-looking terminology (e.g., “expect”,” estimates”, “intends”, “anticipates”, “believes”, “plans”). Such information involves known and unknown risks — including the availability of funds, the results of financing and exploration activities, the interpretation of exploration results and other geological data, or unanticipated costs and expenses and other risks identified by Riverside in its public securities filings that may cause actual events to differ materially from current expectations. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Vancouver, British Columbia–(Newsfile Corp. – January 17, 2025) – Goldshore Resources Inc. (TSXV: GSHR) (OTCQB: GSHRF) (FSE: 8X00) (“Goldshore” or the “Company“), is pleased to announce the first assay results from its 15,000 meter drill program at the Moss Gold Project in Northwest Ontario, Canada (the “Moss Gold Project“). The primary goal of the winter drill program is to add ounces to the current resource model by extending mineralization in the top 100 – 200 meters from surface within the conceptual open pit, effectively converting waste rock to prospective mineable material and potentially reducing the strip ratio of the deposit.

Michael Henrichsen, CEO of Goldshore commented, “We believe that the results from the first three holes prove our thesis that mineralization can be expanded within the top 100 – 200 meters from surface. We believe that these results have the potential to add to the ounce production profile in the first several years of mine life enhancing the economic performance of the project moving forward. Importantly, the PEA currently being completed by G Mining Services represents a conservative case scenario as it will not include the results from the winter drill program.”

Highlights

Results from the first hole (MMD-24-133), drilled to infill a gap in the resource model at the eastern end of the Southwest Zone under Snodgrass Lake, has expanded the width and increased the grade in a number of mineralized shears in the Southwest Zone with a combined intercept of 79.0m of 1.28 g/t Au from 27.0m, including several discrete higher-grade shear zones:

2.0m of 8.61 g/t Au from 27.0m and

32.3m of 1.73 g/t Au from 42.7m, including

16.25m of 2.95 g/t Au from 47.3m

22.0m of 1.19 g/t Au from 84.0m, including

10.0m of 2.13 g/t from 87.0m

Hole MMD-24-134 was also drilled to infill a gap in the resource model at the eastern end of the Southwest Zone under Snodgrass Lake. Mineralization was extended above the known resource with intercepts of:

21.85m of 0.66 g/t Au from 4.5m, including

7.75m of 1.36 g/t Au from 5.0m

12.0m of 0.90 g/t Au from 137.0m

These results will allow for the modelling of mineralized shear zones to surface and into volumes that are currently modelled as waste. The deeper intercepts also add approximately 75 meters to the overall width of the Southwest Zone mineralized shear corridor.

Technical Overview

Figure 1 shows the location of the drill holes being reported with respect to the planned winter drill program, while Figure 2 illustrates a cross section through drill hole MMD-24-133 that demonstrates significant mineralization outside of the current mineral resource. Tables 1 & 2 summarize significant intercepts and drill hole locations, respectively.

Figure 1: Illustrates the 2025 ongoing winter drill program targeting resource expansion within the conceptual open pit outlined in grey. Drill holes being reported are highlighted in red.

Figure 2: Illustrates a cross -section through MMD-24-133 that demonstrates the presence of a wider series of shears within the top 100 meters from surface. Collectively the shear zones intersected demonstrate greater width to mineralized shear zones than represented in the current resource model as well as the extension of mineralized shears from depth toward the surface. The cross-section also highlights the growth potential beneath the open pit that may enable the open-pit resource to be as deep as the Main-QES pit.

Drilling at the Southwest Zone aims to add to the mineral resource by infilling gaps within the current model created by sparse drilling. Drilling at shallow depths of 100 – 200 meters will allow for mineralized shear zones to be extended to the surface. Drilling at depths of 200 to 400 meters will allow the expansion of the open pit resource to a similar depth as the Main-QES pit that are approximately 500 meters deep.

Two holes (MMD-24-133 and MMD-24-134) were drilled along the western edge of Snodgrass Lake to further delineate the trend of the high-grade core shears and to test the up-dip potential of lower grade marginal shear zones.

Hole MMD-24-133 intersected several closely spaced, high-grade shears hosting quartz-carbonate veinlets with up to 2-3% pyritechalcopyrite within a strongly hematite-albite and silica-sericite-pyrite altered granodiorite intrusion along the contact of a more competent porphyritic diorite (Figure 3). Results were wider and higher grade than suggested in the resource model with 79.0m of 1.28 g/t Au from 27.0m, including 32.3m of 1.73 g/t Au and 22.0m of 1.19 g/t Au. These results are top cut with a cap at 30 g/t Au, which only impacted a 1.2m veined shear assaying 34.8 g/t Au. The hole then transitions into weaker shearing and mineralization within silica-sericite and epidote-chlorite altered diorite intrusions with lower grade intercepts, such as 12.0m of 0.57 g/t Au from 158.0m depth.

Figure 3: Illustrates drill core from hole MMD-24-133 that is characterized by a stacked sequence of high-grade shears within an altered granodiorite returning 16.25m of 2.95 g/t Au from 47.3-66.55m.

Hole MMD-24-134 collared into the same mineralized and sheared altered granodiorite intrusion yielding grade intercepts such as 21.85m of 0.66 g/t Au from 4.5m depth, including 7.75m of 1.36 g/t Au. The hole quickly transitions into the wide multi-stage silica-sericite and epidote-chlorite altered diorite intrusion package, as seen in MMD-24-133, yielding broad lower grade intercepts such as 32.15m of 0.36 g/t Au from 84.85m and 12.0m of 0.90 g/t Au from 137.0m.

Both deeper intercepts in MMD-24-133 and -134 represent new mineralized shears not previously included in the current resource model that will potentially add to the overall width of the shear corridor by approximately 75 meters.

Hole MMD-24-136 was drilled underneath Snodgrass Lake from a peninsula along the southeastern shore to properly identify the southeastern limit of the Southwest Zone. The hole encountered varying andesitic and dacitic volcanics before intersecting the diorite package at the end of the hole. The diorite is weakly sheared with pervasive sericite-silica alteration similar to that encountered towards the end of the previous two holes and is weakly mineralized yielding an intercept of 8.8m of 0.39 g/t Au from 218.0m depth. The hole was terminated as the remaining zone had been previously drilled from the southwestern side of the lake.

The ongoing drill program continues to infill wide-spaced drilling gaps within the Southwest Zone, improving the understanding of the controls on mineralization with the aim of growing it into a larger, more continuous mineralized domain, like that of the Main and QES zones. This includes drilling at 200 to 400 meters depth to test mineralization that may extend the mineral resource and enable the pit to extend to a similar depth as the Main-QES pit (~500 meters).

Winter temperatures have been sufficient to allow access to the muskeg-covered, northern portion of the QES zone and the Company is also commencing ice making activities on Snodgrass Lake. Both are high priorities for the current drill campaign, as they have not been drill-tested by Goldshore and have limited historical exploration drilling completed. As a result, there are significant volumes within the current conceptual open pit that are modelled as waste but have the potential to contain shear-hosted gold mineralization, which in turn, has the potential to add ounces to the current mineral resource estimate.

Table 1: Significant intercepts

HOLE ID

FROM

TO

LENGTH (m)

TRUE WIDTH (m)

CUT GRADE (g/t Au)

UNCUT GRADE (g/t Au)

MMD-24-133

27.00

29.00

2.00

1.2

8.61

8.61

42.70

75.00

32.30

18.6

1.73

1.91

incl

47.30

63.55

16.25

9.3

2.95

3.30

incl

47.30

48.50

1.20

0.7

30.0

34.8

84.00

106.00

22.00

12.7

1.19

1.19

incl

87.00

97.00

10.00

5.8

2.13

2.13

123.00

128.00

5.00

2.9

0.33

0.33

158.00

170.00

12.00

6.9

0.57

0.57

incl

159.00

161.75

2.75

1.6

1.06

1.06

MMD-24-134

4.50

26.35

21.85

15.5

0.66

0.66

incl

5.00

12.75

7.75

5.5

1.36

1.36

35.00

46.00

11.00

7.9

0.79

0.79

incl

39.00

42.00

3.00

2.2

2.03

2.03

63.00

66.95

3.95

2.9

0.75

0.75

84.85

127.00

42.15

31.3

0.36

0.36

137.00

149.00

12.00

9.1

0.90

0.90

159.00

165.80

6.80

5.2

0.30

0.30

MMD-24-136

218.00

226.80

8.80

7.0

0.39

0.39

Intersections calculated above a 0.3 g/t Au cut off with a top cut of 30 g/t Au and a maximum internal waste interval of 5 metres and minimum mineralized width of 2m. Bordered intervals are intersections calculated above a 1.0 g/t Au cut off. Intervals in bold are those with a grade thickness factor exceeding 20 gram x metres / tonne gold. True widths are approximate and assume a subvertical body.

Table 2: Drill Collars

HOLE

EAST

NORTH

RL

AZIMUTH

DIP

EOH

MMD-24-133

668,515

5,378,324

428

90

-45

225

MMD-24-134

668,522

5,378,305

428

105

-45

225

MMD-24-136

668,645

5,378,012

430

350

-45

228

Analytical and QA/QC Procedures

All samples were sent to ALS Geochemistry in Thunder Bay for preparation and analysis was performed in the ALS Vancouver analytical facility. ALS is accredited by the Standards Council of Canada (SCC) for the Accreditation of Mineral Analysis Testing Laboratories and CAN-P-4E ISO/IEC 17025. Samples were analysed for gold via fire assay with an AA finish (“Au-AA23”) and 48 pathfinder elements via ICP-MS after four-acid digestion (“ME-MS61”). Samples that assayed over 10 ppm Au were re-run via fire assay with a gravimetric finish (“Au-GRA21”).

In addition to ALS quality assurance / quality control (“QA/QC”) protocols, Goldshore has implemented a quality control program for all samples collected through the drilling program. The quality control program was designed by a qualified and independent third party, with a focus on the quality of analytical results for gold. Analytical results are received, imported to our secure on-line database and evaluated to meet our established guidelines to ensure that all sample batches pass industry best practice for analytical quality control. Certified reference materials are considered acceptable if values returned are within three standard deviations of the certified value reported by the manufacture of the material. In addition to the certified reference material, certified blank material is included in the sample stream to monitor contamination during sample preparation. Blank material results are assessed based on the returned gold result being less than ten times the quoted lower detection limit of the analytical method. The results of the on-going analytical quality control program are evaluated and reported to Goldshore by Orix Geoscience Inc.

Qualified Person

Peter Flindell, PGeo, MAusIMM, MAIG, Vice-President, Exploration, of the Company, and a qualified person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects, has approved the scientific and technical information contained in this news release.

Mr. Flindell has verified the data disclosed. To verify the information related to the winter drill program at the Moss Gold Project, Mr. Flindell has visited the property several times; discussed and reviewed logging, sampling, bulk density, core cutting and sample shipping processes with responsible site staff; discussed and reviewed assay and QA/QC results with responsible personnel; and reviewed supporting documentation, including drill hole location and orientation and significant assay interval calculations. He has also overseen the Company’s health and safety policies in the field to ensure full compliance, and consulted with the Project’s host indigenous communities on the planning and implementation of the drill program, particularly with respect to its impact on the environment and the Company’s remediation protocols.

Marketing Communications Engagements

The Company also announces that it has engaged the following service providers (the “Contractors”) to advise and coordinate market communications and investor relations on behalf of the Company. The Company is at arms-length from each of the Contractors and does not propose to issue any securities to any of the Contractors in consideration of services to be provided to the Company. Each Contractor has agreed to comply with all applicable securities laws and the policies of the TSX Venture Exchange.

The Company has engaged Cambridge House International. (“Cambridge House“) to provide a 3 interview studio series for a term ending March 31, 2025. Cambridge House will receive a total fee of US$34,500 in consideration, of which US$19,500 was paid on entry of the engagement and US$5,000 will be paid with the completion of each video interview. Cambridge House is based in Squamish, British Columbia and is wholly owned by Jay Martin. To the Company’s knowledge, neither Cambridge House nor Jay Martin have any interest, directly or indirectly, in the securities of the Company.

The Company has entered into an agreement (the “SRC Agreement“) with SRC Swiss Resource Capital AG (“SRC“) for investor relations and communications services in Europe. The SRC Agreement is effective as of January 15, 2025, for a period of one year, after which time the SRC Agreement is renewable on a quarterly basis. The services to be provided by SRC to the Company include communications services, generally viewed as investor relations, including dissemination of information to existing and potential shareholders, creating media through interview and videos as well as supporting or representing the Company at trade and investment shows. Pursuant to the terms of the SRC Agreement, SRC is to be paid 5,000 CHF per month with additional fees for special services such as trade and investment shows.

SRC is a private company with a business address at Poststr. 1, CH-9100, Herisau, Switzerland. SRC is led by Jochen Staiger, Chief Executive Officer. To the best of the Company’s knowledge, neither SRC nor Jochen Staiger have any interest, directly or indirectly, in the securities of the Company.

About Goldshore

Goldshore is a growth-oriented gold company focused on delivering long-term shareholder and stakeholder value through the acquisition and advancement of primary gold assets in tier-one jurisdictions. It is led by the ex-global head of structural geology for the world’s largest gold company and backed by one of Canada’s pre-eminent private equity firms. The Company’s current focus is the advanced stage 100% owned Moss Gold Project which is positioned in Ontario, Canada, with direct access from the Trans-Canada Highway, hydroelectric power near site, supportive local communities and skilled workforce. The Company has invested over $60 million of new capital and completed approximately 80,000 meters of drilling on the Moss Gold Project, which, in aggregate, has had over 235,000 meters of drilling. The 2024 updated NI 43-101 mineral resource estimate (“MRE”) has expanded to 1.54 million ounces of Indicated gold resources at 1.23 g/t Au and 5.20 million ounces of Inferred gold resources at 1.11 g/t Au. The MRE only encompasses 3.6 kilometers of the 35+ kilometer mineralized trend, remains open at depth and along strike and is one of the few remaining major Canadian gold deposits positioned for development in this cycle. Please see NI 43-101 technical report titled: “Technical Report and Updated Mineral Resource Estimate for the Moss Gold Project, Ontario, Canada,” dated March 20, 2024 with an effective date of January 31, 2024 available under the Company’s SEDAR+ profile at www.sedarplus.ca. For more information, please visit SEDAR+ (www.sedarplus.ca) and the Company’s website (www.goldshoreresources.com).

For More Information – Please Contact:

Michael Henrichsen President, Chief Executive Officer and Director Goldshore Resources Inc.

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

This news release contains statements that constitute “forward-looking statements.” Such forward looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results, performance or achievements, or developments to differ materially from the anticipated results, performance or achievements expressed or implied by such forward-looking statements. Forward looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. Forward-looking statements in this news release include, among others, statements relating to expectations regarding the exploration and development of the Moss Gold Project; the potential mineralization at the Moss Gold Project based on the winter drill program, including the potential for additional mineral resources; the enhancement of the Moss Gold Project and potential mining methods; the timing of technical reports and economic studies; statements regarding the Company’s future drill programs, including the expected benefits and results thereof; and other statements that are not historical facts.

By their nature, forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements, or other future events, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors and risks include, among others: uncertainty and variation in the estimation of mineral resources; risks related to exploration, development, and operation activities; exploration and development of the Moss Gold Project will not be undertaken as anticipated; the Company may require additional financing from time to time in order to continue its operations which may not be available when needed or on acceptable terms and conditions acceptable; the fluctuating price of gold; unknown labilities in connection with acquisitions; compliance with extensive government regulation; delays in obtaining or failure to obtain governmental permits, or non-compliance with permits; environmental and other regulatory requirements; domestic and foreign laws and regulations could adversely affect the Company’s business and results of operations; risks related to natural disasters, terrorist acts, health crises, and other disruptions and dislocations; global financial conditions; uninsured risks; climate change risks; competition from other companies and individuals; conflicts of interest; risks related to compliance with anti-corruption laws; the Company’s limited operating history; intervention by non-governmental organizations; outside contractor risks; the stock markets have experienced volatility that often has been unrelated to the performance of companies and these fluctuations may adversely affect the price of the Company’s securities, regardless of its operating performance; and other risks associated with executing the Company’s objectives and strategies as well as those risk factors discussed in the Company’s continuous disclosure documents filed under the Company’s SEDAR+ profile at www.sedarplus.ca.