VANCOUVER, BC / ACCESSWIRE / February 21, 2023 / Metallic Minerals Corp. (TSXV:MMG)(OTCQB:MMNGF) (“Metallic Minerals” or the “Company”) is pleased to announce it will be participating in the inaugural Yukon Mining Alliance (“YMA”) Invest Yukon Core Shack to be held in the main Investors Exchange exhibit hall at the Prospectors and Developers Annual Convention (“PDAC”) in Toronto. The Invest Yukon Core Shack will be located at Booth #3314, adjacent to the main PDAC Core Shack and Metallic will be presenting core on March 5 and 6th from both of its key projects, the Keno Silver project in Yukon and the La Plata Copper-Silver project in Colorado. The Company will also have a presence in the main Investors Exchange from March 5-8 and investors are invited to visit booth # IE3024 to meet the team in person.

Metallic Minerals Corporate Presentation

In addition, President Scott Petsel will be providing a corporate presentation at a Forum for Investors on March 6th in the silver-focused session, Room 803, between 10:00 am and 12:00 pm at the Metro Toronto Convention Center. For more information, visit here.

Invest Canada North Reception

The Metallic Group of Companies is proud to be a sponsor of the 2023 Invest Canada North reception to be held March 6 in MTCC North Room 106 from 4pm – 7pm EST. Leaders from its members, Metallic Minerals, Granite Creek Copper and Stillwater Critical Minerals will be in attendance and the Group will have a display table where guests are invited to meet the team. For more information, visit here.

About Yukon Mining Alliance

Yukon Mining Alliance – the globally recognized Invest Yukon brand – is a strategic alliance of Yukon’s leaders in exploration and mining who, in partnership with the Government of Yukon, connect investors with Yukon’s competitive advantages through innovative capital attraction initiatives. For more information visit InvestYukon.ca.

Invest Canada North connects global investors with the competitive advantages and opportunities in Canada’s North, Yukon, Northwest Territories and Nunavut, at one of the world’s biggest annual mining conferences, the PDAC Convention. Our unique initiatives showcase each region, through keynote presentations, panels and special sessions, highlighting the leaders in exploration, development and production, as well as the mining ecosystem that is supported by significant geological potential, strong geopolitical stability and progressive Indigenous and community partnerships. Through our Invest Canada North mining portal catch up on the latest news in the north or dive into each region to discover your next great opportunity. To learn more visit https://investcanadanorth.ca.

About Metallic Minerals

Metallic Minerals Corp. is a leading exploration and development stage company, The Company is focused on silver and gold in the high-grade Keno Hill and Klondike districts of the Yukon, and copper, silver and other critical minerals in the La Plata mining district in Colorado. Our objective is to create shareholder value through a systematic, entrepreneurial approach to making exploration discoveries, growing resources and advancing projects toward development. Metallic Minerals has consolidated the second-largest land position in the historic Keno Hill silver district of Canada’s Yukon Territory, directly adjacent to Hecla Mining’s operations, with more than 300 million ounces of high-grade silver in past production and current M&I resources. Hecla Mining Company, the largest primary silver producer in the USA and third largest in the world, completed the acquisition of Alexco Resources and their Keno Hill operations in September 2022.

Metallic Minerals is also one of the largest holders of alluvial gold claims in the Yukon and is building a production royalty business by partnering with experienced mining operators, including Parker Schnabel of Little Flake Mining from the hit television show Gold Rush on the Discovery Channel. At the Company’s La Plata project in southwestern Colorado an inaugural NI 43-101 mineral resource estimate in April 2022 outlined a significant porphyry copper-silver resource with results from the 2022 expansion drill program pending.

All of the districts in which Metallic Minerals operates have seen significant mineral production and have existing infrastructure, including power and road access. Metallic Minerals is led by a team with a track record of discovery and exploration success on several major precious and base metal deposits in the region, as well as having large-scale development, permitting and project financing expertise. The Metallic Minerals team has been recognized for its environmental stewardship practices and is committed to responsible and sustainable resource development.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

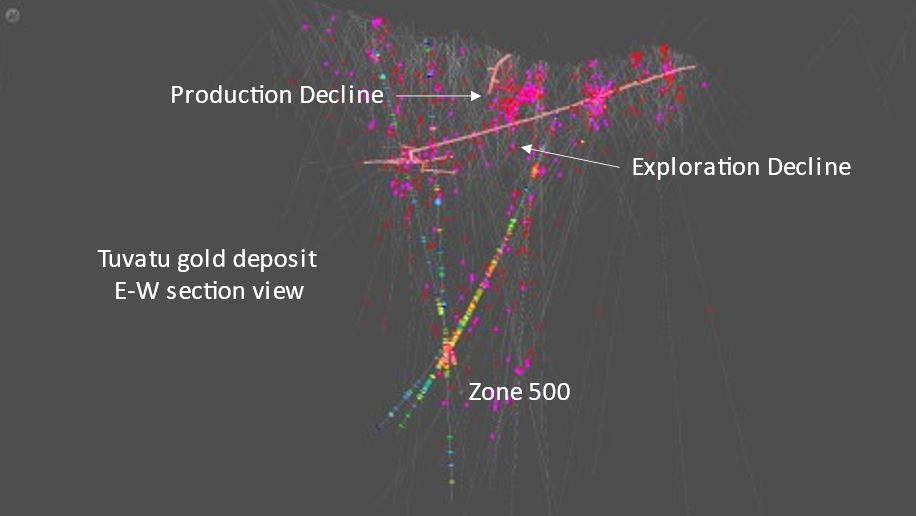

North Vancouver, British Columbia–(Newsfile Corp. – February 16, 2023) – Lion One Metals Limited (TSXV: LIO) (OTCQX: LOMLF) (ASX: LLO) (“Lion One” or the “Company”) announces the acceleration of mine development and plant construction following the completion of project financing, at the Company’s 100% owned Tuvatu Alkaline Gold Project in Fiji.

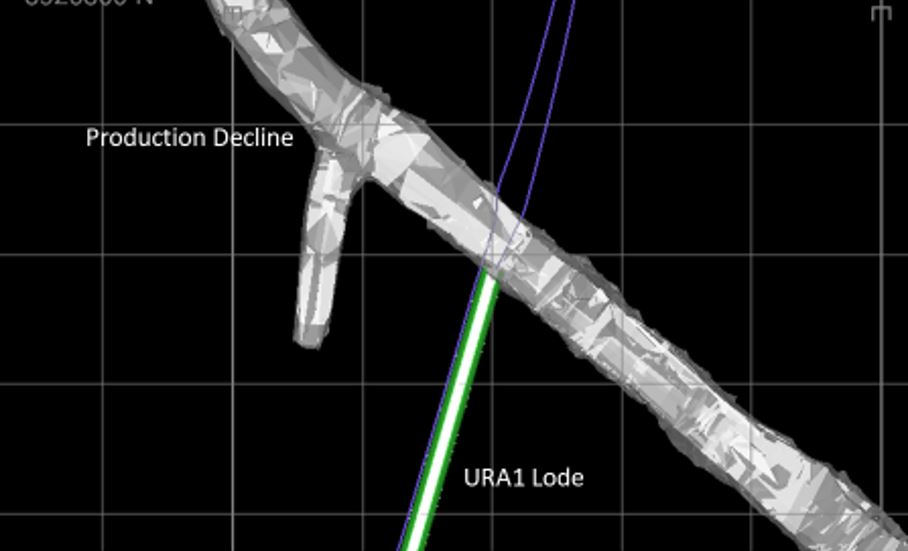

Lion One has advanced the number 2 development drive by over 250 meters and has completed the first cut of high-grade material from the URA1 lode. The samples taken from this first cut averaged 14 g/t gold and are designated for the high-grade ROM stockpile.

Lion One CEO Walter Berukoff commented, “In conjunction with ongoing mine development, we are preparing to mobilize personnel for the installation and commissioning of the Tuvatu gold processing plant. All of the processing plant components have already been delivered to Fiji, with shipments of the remaining bulk materials in progress and expected to be delivered by the end of March to coincide with the completion of infrastructure for the mill area, electrowinning facility, and gold room.”

The Lion One processing plant will treat material using a two-stage crushing process, with a primary jaw crusher and secondary cone crusher feeding a two-stage grinding circuit. The ground material will feed an integrated two stage gravity concentration circuit with some concentrates treated by an intensive cyanide leaching reactor and the remainder of the concentrates leached using conventional cyanide Carbon in Leach (CIL)) technology. Gold will be recovered from the gold laden carbon using conventional absorption desorption recovery (ADR) technology and smelted on site to produce gold doré bars. The leached tailings will be treated using the SO2/air process to remove any residual cyanide. Filtered tailings will be transported to Lion One’s tailings storage facility 3.5 km from the Tuvatu mine site.

Lion One plans to operate at an initial production capacity of 300 tonnes per day for the initial 18 months of operations before increasing the capacity to 500 tpd in mid-2025. The initial mining will focus on the near-surface resource while advancing underground development into high-grade mineralization in Zone 500.

The 2023 drilling program will be focused on three fronts: grade control drilling of the near-term production blocks; drill-testing regional targets with the aim of identifying additional separate mineralized systems within the greater Navilawa caldera; and completing the geophysical (CSAMT) surveys initiated in 2022 to delineate additional drill targets.

About Tuvatu The Tuvatu Alkaline Gold Project is located on the island of Viti Levu in Fiji. The January 2018 mineral resource for Tuvatu as disclosed in the technical report “Technical Report and Preliminary Economic Assessment for the Tuvatu Gold Project, Republic of Fiji”, dated September 25, 2020, and prepared by Mining Associates Pty Ltd of Brisbane Qld, comprises 1,007,000 tonnes indicated at 8.50 g/t Au (274,600 oz. Au) and 1,325,000 tonnes inferred at 9.0 g/t Au (384,000 oz. Au) at a cut-off grade of 3.0 g/t Au. The technical report is available on the Lion One website at U and on the SEDAR website at www.sedar.com.

Continued…

Photo 1: Aerial view of the Tuvatu plant site and surrounding Navilawa caldera

Qualified Person In accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43- 101”), Patrick Hickey, Chief Operating Officer, is the Qualified Person for the Company and has reviewed and is responsible for the technical and scientific content of this news release.

About Lion One Metals Limited Lion One’s flagship asset is 100% owned, fully permitted high grade Tuvatu Alkaline Gold Project, located on the island of Viti Levu in Fiji. Lion One envisions a low-cost high-grade underground gold mining operation at Tuvatu coupled with exciting exploration upside inside its tenements covering the entire Navilawa Caldera, an underexplored yet highly prospective 7km diameter alkaline gold system. Lion One’s CEO Walter Berukoff leads an experienced team of explorers and mine builders and has owned or operated over 20 mines in 7 countries. As the founder and former CEO of Miramar Mines, Northern Orion, and La Mancha Resources, Walter is credited with building over $3 billion of value for shareholders.

On behalf of the Board of Directors of Lion One Metals Limited “Walter Berukoff“, Chairman and CEO

Neither the TSX Venture Exchange nor its Regulation Service Provider accepts responsibility for the accuracy of this release

This press release may contain statements that may be deemed to be “forward-looking statements” within the meaning of applicable Canadian securities legislation. All statements, other than statements of historical fact, included herein are forward-looking information. Generally, forward-looking information may be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “proposed”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases, or by the use of words or phrases which state that certain actions, events or results may, could, would, or might occur or be achieved. This forward-looking information reflects Lion One Metals Limited’s current beliefs and is based on information currently available to Lion One Metals Limited and on assumptions Lion One Metals Limited believes are reasonable. These assumptions include, but are not limited to, the actual results of exploration projects being equivalent to or better than estimated results in technical reports, assessment reports, and other geological reports or prior exploration results. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance, or achievements of Lion One Metals Limited or its subsidiaries to be materially different from those expressed or implied by such forward-looking information. Such risks and other factors may include, but are not limited to: the stage development of Lion One Metals Limited, general business, economic, competitive, political and social uncertainties; the actual results of current research and development or operational activities; competition; uncertainty as to patent applications and intellectual property rights; product liability and lack of insurance; delay or failure to receive board or regulatory approvals; changes in legislation, including environmental legislation, affecting mining, timing and availability of external financing on acceptable terms; not realizing on the potential benefits of technology; conclusions of economic evaluations; and lack of qualified, skilled labor or loss of key individuals. Although Lion One Metals Limited has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. Accordingly, readers should not place undue reliance on forward-looking information. Lion One Metals Limited does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

KELOWNA, BC / ACCESSWIRE / February 16, 2023 / Diamcor Mining Inc. (TSXV:DMI)(OTCQB:DMIFF)(FRA:DC3A), (“Diamcor” or, the “Company”) today reported the results of its interim quarterly financial statements and related management discussion and analysis for the quarter ended December 31, 2022.

Fiscal Third Quarter 2022 Highlights

Tender and sale of 8,327.58 carats of rough diamonds during the period, a 120% increase quarter over quarter and a 53% increase relative to fiscal Q3 2021, generating revenue of (USD) $2,054,248.33 resulting in an average price of (USD) $246.68 per carat.

The Company recorded a net loss of $386,619 as compared to net income of $1,016,568 in the previous interim period ended September 30, 2022, and a net loss of $939,916 in fiscal Q3 2021.

Inconsistent power, the result of load shedding by national power supplier Eskom in South Africa, continued to have a direct impact on the Company’s processing plant operations. The Company is currently in the late stages of finalizing an agreement with a third party to install additional power back-up systems with an aim to reduce the long-term impact of the national power supply’s future load shedding. These back-up system additions will also include power conditioning equipment to improve power supply quality and variability, and thus have the potential of lowering maintenance costs.

In total, ongoing trial mining exercises at the Company’s Krone-Endora at Venetia project from inception thru December 31, 2022, have resulted in the incidental recovery, tender, and sale of 194,969.18 carats of rough diamonds generating revenue of (USD) $36,247,542.60, resulting in an average price of (USD) $185.91 per carat.

The management of operational salary and wages expenses, variable operational costs, and historical fixed costs continued to be a focus during the period.

“We are very pleased with the progress we have made at the Project in addressing the well documented issues surrounding the national power supply in South Africa,” stated Mr. Dean Taylor, Diamcor CEO. “We look forward to realizing the impact consistent power will have on our ability to operate our processing plant to its full capacity over the long-term”.

The Company’s recently filed financial statements for the quarter ended December 31, 2022, and accompanying Management Discussion and Analysis can be viewed by interested parties on SEDAR at www.sedar.com.

About Diamcor Mining Inc.

Diamcor Mining Inc. is a fully reporting publicly traded junior diamond mining company which is listed on the TSX Venture Exchange under the symbol V.DMI, and on the OTC QB International under the symbol DMIFF. The Company has a well-established operational and production history in South Africa and extensive prior experience supplying rough diamonds to the world market.

About the Tiffany & Co. Alliance

The Company has established a long-term strategic alliance and first right of refusal with Tiffany & Co. Canada, a subsidiary of world famous New York based Tiffany & Co., to purchase up to 100% of the future production of rough diamonds from the Krone-Endora at Venetia Project at then current prices to be determined by the parties on an ongoing basis. In conjunction with this first right of refusal, Tiffany & Co. Canada also provided the Company with financing to advance the Project. Tiffany & Co. is owned by Moet Hennessy Louis Vuitton SE (LVMH), a publicly traded company which is listed on the Paris Stock Exchange (Euronext) under the symbol LVMH and on the OTC under the symbol LVMHF. For additional information on Tiffany & Co., please visit their website at www.tiffany.com.

About Krone-Endora at Venetia

In February 2011, Diamcor acquired the Krone-Endora at Venetia Project from De Beers Consolidated Mines Limited, consisting of the prospecting rights over the farms Krone 104 and Endora 66, which represent a combined surface area of approximately 5,888 hectares directly adjacent to De Beers’ flagship Venetia Diamond Mine in South Africa. On September 11, 2014, the Company announced that the South African Department of Mineral Resources had granted a Mining Right for the Krone-Endora at Venetia Project encompassing 657.71 hectares of the Project’s total area of 5,888 hectares. The Company has also submitted an application for a mining right over the remaining areas of the Project. The deposits which occur on the properties of Krone and Endora have been identified as a higher-grade “Alluvial” basal deposit which is covered by a lower-grade upper “Eluvial” deposit. The deposits are proposed to be the result of the direct-shift (in respect to the “Eluvial” deposit) and erosion (in respect to the “Alluvial” deposit) of material from the higher grounds of the adjacent Venetia Kimberlite areas. The deposits on Krone-Endora occur in two layers with a maximum total depth of approximately 15.0 metres from surface to bedrock, allowing for a very low-cost mining operation to be employed with the potential for near-term diamond production from a known high-quality source. Krone-Endora also benefits from the significant development of infrastructure and services already in place due to its location directly adjacent to the Venetia Mine.

Qualified Person Statement:

Mr. James P. Hawkins (B.Sc., P.Geo.), is Manager of Exploration & Special Projects for Diamcor Mining Inc., and the Qualified Person in accordance with National Instrument 43-101 responsible for overseeing the execution of Diamcor’s exploration programmes and a Member of the Association of Professional Engineers and Geoscientists of Alberta (“APEGA”). Mr. Hawkins has reviewed this press release and approved of its contents.

This press release contains certain forward-looking statements. While these forward-looking statements represent our best current judgement, they are subject to a variety of risks and uncertainties that are beyond the Company’s ability to control or predict and which could cause actual events or results to differ materially from those anticipated in such forward-looking statements. Further, the Company expressly disclaims any obligation to update any forward looking statements. Accordingly, readers should not place undue reliance on forward-looking statements.

WE SEEK SAFE HARBOUR

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

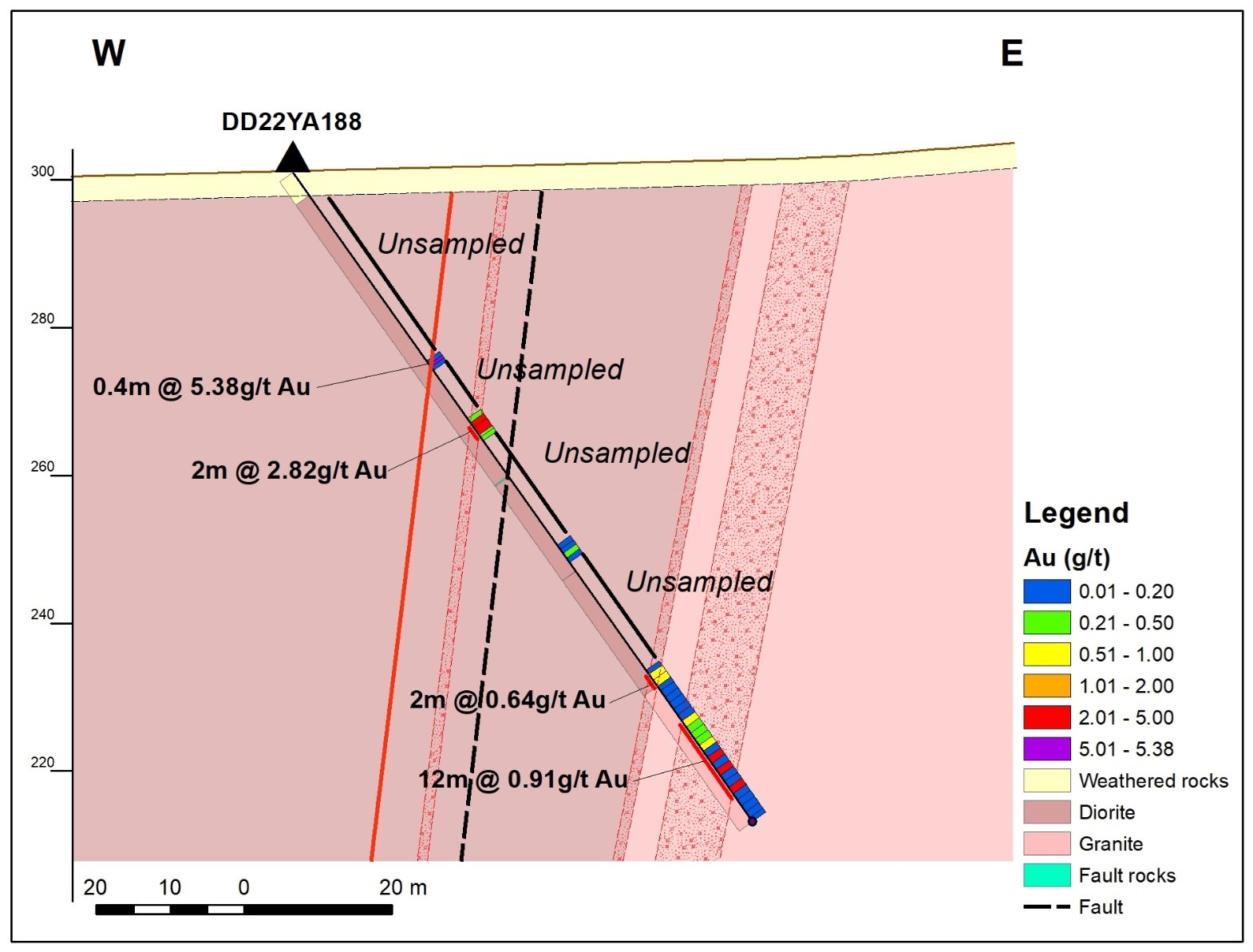

Vancouver, British Columbia–(Newsfile Corp. – February 16, 2023) – EMX Royalty Corporation (NYSE American: EMX) (TSXV: EMX) (FSE: 6E9) (the “Company” or “EMX”) is pleased to provide an update on the advancement of its 100% owned Yarrol Project in Queensland, Australia. The Yarrol Project contains zones of gold and copper mineralization in addition to areas with cobalt-enriched manganese oxide mineralization and heavy mineral sands deposits (see Figures 1 and 2). A recently executed reconnaissance drill program targeted all three styles of mineralization. Analytical results from a drill hole in the core of the historically defined zone of gold mineralization are highlighted by an intercept of 17.8 meters averaging 4.01 g/t gold from 61 meters in drill hole DD22-YA1871 (see Figure 3). A second hole (DD22-YA188) intersected multiple intervals of gold mineralization including 12 meters at 0.91 g/t gold from 92 meters (see Figure 4)1. These holes were intended to confirm the nature of the gold mineralization that have been historically mined and explored at Yarrol. It is notable that the selected sample intervals from both drill holes began and ended in gold mineralization2, and additional intervals will be sampled and analyzed from both holes.

Drill holes DD22-YA187 and DD22-YA188 were drilled as part of a 15 hole program, with two deeper core holes in the zones of gold mineralization and 13 shallow diamond and air core holes targeting the manganese-cobalt mineralization and mineral sands. EMX expects to receive additional analytical results for the manganese-cobalt mineralization and mineral sands deposits in the coming weeks. Results from those drill holes will be discussed in a separate disclosure.

The Yarrol Project is currently available for partnership, in accordance with the royalty generation aspect of EMX’s business model.

Yarrol Project. The 55,900 Ha Yarrol Project is located between EMX’s Queensland Gold project and Evolution Mining’s Mt Rawdon gold mine, and is positioned along the regional scale Yarrol Fault zone. Several other historical mines and active exploration projects also lie along the Yarrol Fault structural trend.

Yarrol was the site of historical gold mining activities in the 1800’s through the 1930’s, with historical gold production averaging ~10 g/t.3 Further exploration and assessments conducted in the 1980’s and 1990’s led to the definition of two historical gold resources (see notes regarding the historical mineral resources below). Gold mineralization at Yarrol is present as quartz sulfide veins and zones of silicification developed in and around Permian-aged dioritic intrusions as confirmed in holes DD22-YA187 and DD22-YA188.

In late 2021, while conducting exploration programs to expand the known zones of gold mineralization, EMX geologists encountered zones of cobalt-enriched manganese oxide mineralization on the northern side of the Project area. This led to an expansion of the land position, as well as new exploration programs targeting the manganese and cobalt mineralization. Surface sampling programs demonstrated that the zones of manganese oxide mineralization encountered in the field consistently averaged over 1% cobalt, accompanied by enrichments in both nickel and copper (see EMX news release dated January 4, 2022).

Dr. Eric P. Jensen, CPG, a Qualified Person as defined by National Instrument 43-101 and employee of the Company, has reviewed, verified and approved the disclosure of the technical information contained in this news release.

Comments on Sampling, Assaying, and QA/QC. EMX’s drill and surface samples were collected in accordance with accepted industry standards and best practices. The samples were submitted to ALS Laboratories in Brisbane for sample preparation and analysis. Gold was analyzed by Au_AA24 fire assay and AAS (50 g nominal sample weight) method, and multi-element analyses were performed by an ME-MS61 method combining a four-acid digestion with ICP-MS finish. As standard procedure, the Company conducts routine QA/QC analysis on all assay results, including the systematic utilization of certified reference materials, blanks, and field duplicates.

Comments on Historical Mineral Resources at Yarrol and Nearby Mines and Deposits. The historical mineral resources at Yarrol were reported in 2010 by MGT Mining Ltd, which was a publicly traded Australian company at the time of publication. EMX has not done sufficient work to verify the historical resources.

The nearby mines and deposits in the region provide geologic context for EMX’s Project, but this is not necessarily indicative that the Project hosts similar mineralization.

About EMX. EMX is a precious, base and battery metals royalty company. EMX’s investors are provided with discovery, development, and commodity price optionality, while limiting exposure to risks inherent to operating companies. The Company’s common shares are listed on the NYSE American Exchange and the TSX Venture Exchange under the symbol EMX, and also trade on the Frankfurt exchange under the symbol “6E9”. Please see www.EMXroyalty.com for more information.

For further information contact:

David M. Cole President and Chief Executive Officer Phone: (303) 973-8585 Dave@emxroyalty.com

Scott Close Director of Investor Relations Phone: (303) 973-8585 SClose@emxroyalty.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release may contain “forward-looking statements” that reflect the Company’s current expectations and projections about its future results. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserve and resource estimates, work programs, capital expenditures, timelines, strategic plans, market prices for precious and base metal, or other statements that are not statements of fact. When used in this news release, words such as “estimate,” “intend,” “expect,” “anticipate,” “will”, “believe”, “potential” and similar expressions are intended to identify forward-looking statements, which, by their very nature, are not guarantees of the Company’s future operational or financial performance, and are subject to risks and uncertainties and other factors that could cause the Company’s actual results, performance, prospects or opportunities to differ materially from those expressed in, or implied by, these forward-looking statements. These risks, uncertainties and factors may include, but are not limited to: unavailability of financing, failure to identify commercially viable mineral reserves, fluctuations in the market valuation for commodities, difficulties in obtaining required approvals for the development of a mineral project, increased regulatory compliance costs, expectations of project funding by joint venture partners and other factors.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this news release or as of the date otherwise specifically indicated herein. Due to risks and uncertainties, including the risks and uncertainties identified in this news release, and other risk factors and forward-looking statements listed in the Company’s MD&A for the quarter ended September 30, 2022 (the “MD&A”), and the most recently filed Revised Annual Information Form (the “AIF”) for the year ended December 31, 2021, actual events may differ materially from current expectations. More information about the Company, including the MD&A, the AIF and financial statements of the Company, is available on SEDAR at www.sedar.com and on the SEC’s EDGAR website at www.sec.gov.

1 True widths remain unknown, but are estimated to be in the 50-75% range of the reported drilled interval. The interval was calculated assuming a cutoff of 0.5 g/t gold. 2 Mineralization being defined as samples containing > 0.1 g/t gold. 3 Independent Geological Report for MGT Mining Ltd, 2010. https://www.nsx.com.au/ftp/news/021723444.PDF. EMX has not performed sufficient work to verify historical sample results and production figures, however, from EMX’s field reviews of the Yarrol property, these data are considered to be reliable and relevant.

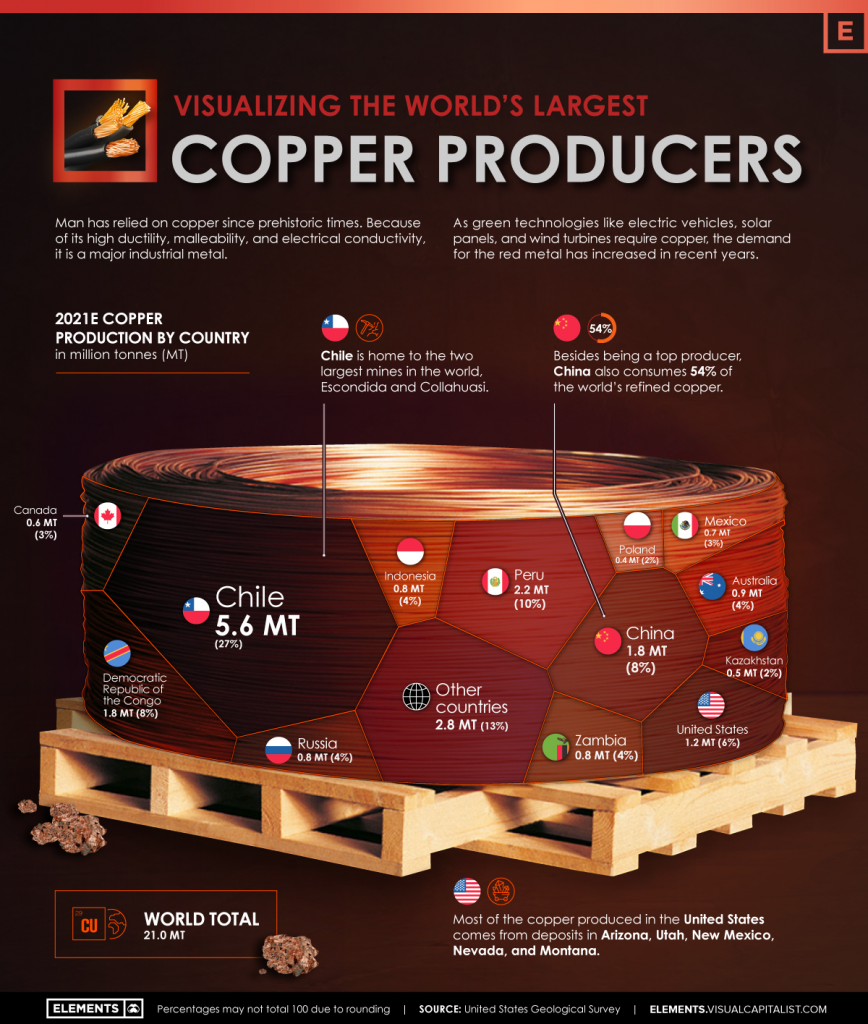

Man has relied on copper since prehistoric times. It is a major industrial metal with many applications due to its high ductility, malleability, and electrical conductivity.

Many new technologies critical to fighting climate change, like solar panels and wind turbines, rely on the red metal.

But where does the copper we use come from? Using the U.S. Geological Survey’s data, the above infographic lists the world’s largest copper producing countries in 2021.

The Countries Producing the World’s Copper

Many everyday products depend on minerals, including mobile phones, laptops, homes, and automobiles. Incredibly, every American requires 12 pounds of copper each year to maintain their standard of living.

North, South, and Central America dominate copper production, as these regions collectively host 15 of the 20 largest copper mines.

Chile is the top copper producer in the world, with 27% of global copper production. In addition, the country is home to the two largest mines in the world, Escondida and Collahuasi.

Chile is followed by another South American country, Peru, responsible for 10% of global production.

Rank

Country

2021E Copper Production (Million tonnes)

Share

#1

Chile

5.6

27%

#2

Peru

2.2

10%

#3

China

1.8

8%

#4

DRC

1.8

8%

#5

United States

1.2

6%

#6

Australia

0.9

4%

#7

Russia

0.8

4%

#8

Zambia

0.8

4%

#9

Indonesia

0.8

4%

#10

Mexico

0.7

3%

#11

Canada

0.6

3%

#12

Kazakhstan

0.5

2%

#13

Poland

0.4

2%

🌍 Other countries

2.8

13%

🌐 World total

21.0

100%

The Democratic Republic of Congo (DRC) and China share third place, with 8% of global production each. Along with being a top producer, China also consumes 54% of the world’s refined copper.

Copper’s Role in the Green Economy

Technologies critical to the energy transition, such as EVs, batteries, solar panels, and wind turbines require much more copper than conventional fossil fuel based counterparts.

For example, copper usage in EVs is up to four times more than in conventional cars. According to the Copper Alliance, renewable energy systems can require up to 12x more copper compared to traditional energy systems.

Technology

2020 Installed Capacity (megawatts)

Copper Content (2020, tonnes)

2050p Installed Capacity (megawatts)

Copper Content (2050p, tonnes)

Solar PV

126,735 MW

633,675

372,000 MW

1,860,000

Onshore Wind

105,015 MW

451,565

202,000 MW

868,600

Offshore Wind

6,013 MW

57,725

45,000 MW

432,000

With these technologies’ rapid and large-scale deployment, copper demand from the energy transition is expected to increase by nearly 600% by 2030.

As the transition to renewable energy and electrification speeds up, so will the pressure for more copper mines to come online.

Burlington, Ontario–(Newsfile Corp. – February 15, 2023) – Silver Bullet Mines Corp. (TSXV: SBMI) (OTCQB: SBMCF) (‘SBMI’ or ‘the Company’) announces strong initial assay results from the interception of the upper main vein at the Buckeye Mine near Globe, Arizona.

The vein was intercepted approximately 380 feet from the entrance to the adit. Immediately on contact with the vein, the first significant assays from the vein were 43, 178.6, and 270.6 ounces silver per ton. The samples yielding these results did not include material from the footwall. The samples were selected at random from the mineralized material removed from the vein and then were sent to SBMI’s assay lab for processing.

The Company is now mining along the exposed vein with assay results pending from the face. SBMI has extended the workings to 420 feet from the entrance to the adit, the vein is ten feet wide and eleven feet high, and the footwall is estimated by the field team to be four feet wide.

SBMI has stockpiled in excess of 450 tons of vein material at surface at the Buckeye Mine site, for shipment to the mill. The Company is mining 150 to 200 tons of mineralized material per day, although this rate will vary. The Company believes it has achieved the targetted grade necessary to support processing this material at the Company’s mill and to then pour dore bars or create concentrate. Both the dore bars and the concentrate will saleable product, and the Company does not expect to encounter any significant difficulties in finding buyers for those products.

SBMI is also pleased to announce it has begun to resolve the issues with pouring dore bars from this material. The picture below shows a malformed dore bar from September, 2022.

The Company thanks Dr. Andrew Macdonald, a mineralogist with Harquail School of Earth Sciences at Laurentian University, for his assistance. Initial results from his work indicate the presence of a highly magnetic iron alloy in the mineralized material. The iron alloy smelts at temperatures of over 3000 degrees F, which is above the silver smelting temperature of roughly 1800 degrees F, and therefore it interferes with the silver smelting process. SBMI has confirmed this thesis by using a high intensity magnet to pull the iron alloy from the concentrate prior to smelting. The dore bar below, poured in February, 2023, resulted from concentrate after the iron alloy was removed.

Dore bar poured after the iron alloy was removed; Feb 2023

As a result, the Company intends to permanently install a high intensity magnetic separator in the milling operation to improve the likelihood the Company can smelt silver dore bars. The Company intends to store the magnetic concentrates for future research. Continued research will be needed.

The Company is still awaiting the check assay results from American Assay Labs and Actlabs.

SBMI’s near term goal is to process the higher grade material at the Company’s mill to produce saleable product.

QAQC

All the samples above were collected by SBMI’s field team. Samples were collected and placed in sample bags with their appropriate tag and processed at the Company’s own assay lab. Like any responsible producer, the Company owns its own assay lab and regularly takes samples as part of its production process.

The samples analyzed by SBMI at its facility near Globe, Arizona were processed through the Lab Jaw Crusher, Lab Hammer Mill and Splitter Box into an aliquot. Most of the pulverized aliquot was mixed with a flux and flour combination and melted in a crucible at 1,850 degree Fahrenheit, with the remainder being logged and archived. Upon cooling, the poured melt was in the form of a metal button and slag, following which a bone ash cupel was utilized to eliminate the lead in the button to form a bead. The bead was then weighed, following which a solution of 6 to 1 distilled water to nitric acid was utilized to dissolve the silver in the bead at approximately 175 degrees Fahrenheit. A much more detailed description of the process and a picture of the assay lab can be found at https://www.silverbulletmines.com/qaqcassaylab.

Readers should be aware that the SBMI facilities have been designed for quick production grade control and are not ISO compliant; however, duplicate sampling with other ISO labs has been done on past samples with good correlation.

Mr. Robert G. Komarechka, P.Geo., an independent consultant, has reviewed and verified SBMI’s work referred to herein, and is the Qualified Person for this release.

For further information, please contact:

John Carter Silver Bullet Mines Corp., CEO cartera@sympatico.ca +1 (905) 302-3843

Peter M. Clausi Silver Bullet Mines Corp., VP Capital Markets pclausi@brantcapital.ca +1 (416) 890-1232

Cautionary and Forward-Looking Statements

This news release contains certain statements that constitute forward-looking statements as they relate to SBMI and its subsidiaries. Forward-looking statements are not historical facts but represent management’s current expectation of future events, and can be identified by words such as “believe”, “expects”, “will”, “intends”, “plans”, “projects”, “anticipates”, “estimates”, “continues” and similar expressions. Although management believes that the expectations represented in such forward-looking statements are reasonable, there can be no assurance that they will prove to be correct.

By their nature, forward-looking statements include assumptions, and are subject to inherent risks and uncertainties that could cause actual future results, conditions, actions or events to differ materially from those in the forward-looking statements. If and when forward-looking statements are set out in this new release, SBMI will also set out the material risk factors or assumptions used to develop the forward-looking statements. Except as expressly required by applicable securities laws, SBMI assumes no obligation to update or revise any forward-looking statements. The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: the impact of SARS CoV-2 or any other global virus; reliance on key personnel; the thoroughness of its QA/QA procedures; the continuity of the global supply chain for materials for SBMI to use in the production and processing of mineralized material; the presence of mineable economic mineralized material; shareholder and regulatory approvals; activities and attitudes of communities local to the location of the SBMI’s properties; risks of future legal proceedings; income tax matters; fires, floods and other natural phenomena; the rate of inflation; availability and terms of financing; distribution of securities; commodities pricing; currency movements, especially as between the USD and CDN; effect of market interest rates on price of securities; and, potential dilution. SARS CoV-2 and other potential global pathogens create risks that at this time are immeasurable and impossible to define.

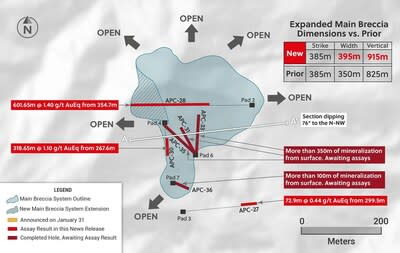

Step-out drill hole APC-28, which was drilled to the west from the eastern side of the Main Breccia system at Apollo cut the longest intercept to date as follows:

As a result of APC-28, the maximum width and vertical dimensions of the Main Breccia system have increased to 395 metres (previously 350 metres) and 915 metres (previously 825 metres), respectively.

Drill hole APC-28 bottomed while still in mineralization indicating that the Main Breccia system remains open for expansion to the west and at depth (as well as to the east and north based on previously announced assay results).

Hole APC-30 was drilled southwards on the western side of the deposit and intercepted the Main Breccia system over a broad interval as follows:

Four holes have now been completed into the Main Breccia system as part of the 2023 Phase II drill program at the Guayabales project. All four holes appear to have intercepted the Main Breccia system with mineralization beginning from surface. Assay results for these holes are expected in the near term.

Ari Sussman, Executive Chairman commented: “The Main Breccia system at Apollo continues to yield positive surprises. The Company drilled three long holes in 2022, APC-17, APC-22 and APC-28, with each hole expanding the size of the deposit and bottoming while still in mineralization. In addition, 2023 drilling is off to an excellent start with the initial four holes testing the Main Breccia system all intersecting mineralization beginning at surface. Our aim for 2023 is to define the newly discovered high-grade and near surface mineralization while continuing to be aggressive with expansion drilling. Without question, we have discovered a large copper-silver-gold deposit in a mining friendly jurisdiction of Colombia which will play a vital role in the country’s aggressive decarbonization goals.”

TORONTO, Feb. 15, 2023 /CNW/ – Collective Mining Ltd. (TSXV: CNL) (OTCQX: CNLMF) (“Collective” or the “Company”) is pleased to announce assay results from a further three holes drilled into the Main Breccia system at the Apollo target (“Apollo”), which is part of the Guayabales project located in Caldas, Colombia. The Main Breccia is a high-grade, bulk tonnage copper-silver-gold porphyry-related system, which owes its excellent metal endowment to multiple phases of mineralization which includes older copper-silver-gold porphyry mineralization and younger, overprinting, low and intermediate sulphidation, precious metal rich sheeted carbonate base metal vein systems.

Details (See Table 1 and Figures 1–5)

Assay results for all thirty-one diamond drill holes from the Phase I drilling program for 2022 have now been announced at Apollo. The Phase II drilling program for 2023 is advancing on schedule with assay results for the first holes expected in the near term. This press release summarizes assay results of the final three diamond drill holes from the Phase I program with results summarized below.

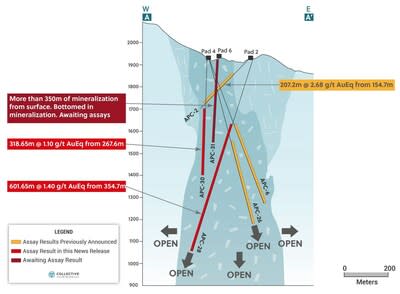

APC-28 was a step-out hole drilled steeply to the west from Pad 2 to a maximum depth of 956.35 metres (915 metres vertical) and was designed to test western and depth extensions to the Main Breccia system. The hole intersected the longest interval drilled to date within the system, commencing at 354.70 metres down hole (335 vertical) and averaging:

601.65 metres @ 1.4 g/t gold equivalent and including internal intervals of:

The mineralized angular breccia of this intercept represents the largest accumulation of metal returned to date within the Main Breccia system and contains a sulphide matrix which includes 0.5% up to 2.5% chalcopyrite and between 1% and 3% pyrite plus some pyrrhotite. The breccia has been overprinted by zones of carbonate and base metal (sphalerite and galena) veins, which yield the higher gold equivalent intervals. APC-28 stopped in mineralized breccia due to rig constraints. This hole has extended the main breccia westwards by 115 metres and is the deepest intercept drilled to date outlining continuity of mineralized breccia to a vertical depth of approximately 915 metres below surface. APC-28 also represents the westernmost hole drilled into the Main Breccia system and demonstrates that the mineralization is thickening with depth and has an inverted funnel morphology as outlined in Figure 2 below. This western area of the deposit remains open for expansion as the hole stopped in strong mineralization.

As a result of drill hole APC-28, the overall volume of rock in which the Main Breccia system is located has grown in width to 395 metres (from 350 metres) and a vertical dimension of 915 metres (from 825 metres). The strike of the system remains the same at 385 metres.

APC-30 was drilled southwards from Pad 4 to a total length of 589 metres downhole and intersected mineralized breccia from 267.60 metres downhole (240 metres vertical), averaging:

318.85 metres @ 1.10 g/t gold equivalent and including internal intervals of:

Gold, silver and copper mineralization relates to sulphides hosted within the angular breccia matrix with average concentrations of pyrite (2%) and chalcopyrite (0.5%). An upper zone of 60.8 metres bearing 2% to 3% chalcopyrite was intercepted at the beginning of the mineralized interval and a sheeted and overprinting sphalerite rich CBM vein zone of 81.4 metres was encountered from 472.3 metres downhole.

Reconnaissance hole APC-27 was drilled due east away from the Main Breccia system to test outcropping mineralization at surface. From 300.40 metres downhole (210 metres vertical depth) the Company intersected a new zone of continuous low-grade mineralization with assay results as follows:

Core logging of the breccia system at Apollo by the Company’s geologists has identified that the crackle breccia as seen in this newly discovered zone, is typically found both above and on the periphery of the more intensely mineralized angular breccia phase. As a result of this assessment, the Company may have drilled over top of an angular breccia zone with stronger mineralization than was intercepted in APC-27. Further exploratory drilling will be undertaken in this area.

The Company’s Phase II 2023 program is well underway with three rigs focused on drilling near surface, high grade mineralization below mineralized outcrops in the southern and central areas of the Main Breccia system from newly constructed pads 6 and 7. To date, four shallow holes have been completed and confirm continuous mineralized angular breccia from surface. Three of these holes were drilled from Pad 6 and were terminated while still in strong mineralization. The fourth hole from Pad 7 appears to have drilled out the east side of the system indicating a more vertical orientation to the system that was previously modelled. Assay results are expected in the near term.

The Apollo target area, as defined to date by surface mapping, rock sampling and copper and molybdenum soil geochemistry, covers a 1,000 metres X 1,200 metres area. The Apollo target area hosts the Company’s Main Breccia system and multiple additional untested breccia, porphyry and vein targets. The overall Apollo target area also remains open for further expansion.

Table 1: Apollo Target Assays Results for Holes APC-27, APC-28, and APC-30

Hole ID

From (m)

To (m)

Intercept (m)

Au (g/t)

Ag (g/t)

Cu %

Mo %

AuEq (g/t) *

APC-27

299.50

372.40

72.90

0.30

6

0.02

0.002

0.44

APC-28

286.60

305.55

18.95

1.11

12

0.04

0.001

1.30

And

354.70

956.35

601.65

0.89

24

0.10

0.001

1.40

Incl

354.70

614.65

259.95

1.21

43

0.20

0.001

2.15

713.10

772.80

59.70

2.04

15

0.14

0.04

2.23

863.15

868.80

5.65

2.00

13

0.04

0.001

2.17

APC-30

267.60

586.25

318.65

0.61

19

0.12

0.002

1.10

Incl

267.60

328.40

60.80

0.17

48

0.40

0.002

1.64

472.30

553.70

81.40

1.95

18

0.04

0.002

2.22

*AuEq (g/t) is calculated as follows: (Au (g/t) x 0.95) + (Ag g/t x 0.016 x 0.95) + (Cu (%) x 1.83 x 0.95)+ (Mo (%)*9.14 x 0.95) and CuEq (%) is calculated as follows: (Cu (%) x 0.95) + (Au (g/t) x 0.51 x 0.95) + (Ag (g/t) x 0.01 x 0.95)+ (Mo(%)x 3.75 x 0.95) utilizing metal prices of Cu – US$4.00/lb, Ag – $24/oz Mo US$20.00/lb and Au – US$1,500/oz and recovery rates of 95% for Au, Ag, Mo and Cu. Recovery rate assumptions are speculative as no metallurgical work has been completed to date.

** A 0.2 g/t AuEq cut-off grade was employed with no more than 15% internal dilution. True widths are unknown, and grades are uncut.

Figure 1: Plan View of the Main Breccia System at Apollo Highlighting Drill Holes APC-27, APC-28, APC-30 and Visual Results for APC-31, APC-33, APC-35 and APC-36 (CNW Group/Collective Mining Ltd.)

Figure 2: East-West Cross Section Highlighting APC-28, ACP-30, and Visual Results for APC-31 (CNW Group/Collective Mining Ltd.)

Figure 3: Plan View of the Guayabales Project Highlighting the Apollo Target (CNW Group/Collective Mining Ltd.)

To see our latest corporate presentation and related information, please visit www.collectivemining.com

Founded by the team that developed and sold Continental Gold Inc. to Zijin Mining for approximately $2 billion in enterprise value, Collective Mining is a copper, silver and gold exploration company based in Canada, with projects in Caldas, Colombia. The Company has options to acquire 100% interests in two projects located directly within an established mining camp with ten fully permitted and operating mines.

The Company’s flagship project, Guayabales, is anchored by the Apollo target, which hosts the large-scale, bulk-tonnage and high-grade copper, silver, and gold Main Breccia system. The Company’s near-term objective is to continue with expansion drilling of the Main Breccia system while increasing confidence in the highest-grade portions of the system.

Management, insiders and close family and friends own nearly 52% of the outstanding shares of the Company and as a result, are fully aligned with shareholders. The Company is listed on the TSXV under the trading symbol “CNL” and on the OTCQX under the trading symbol “CNLMF”.

Qualified Person (QP) and NI43-101 Disclosure

David J Reading is the designated Qualified Person for this news release within the meaning of National Instrument 43-101 (“NI 43-101”) and has reviewed and verified that the technical information contained herein is accurate and approves of the written disclosure of same. Mr. Reading has an MSc in Economic Geology and is a Fellow of the Institute of Materials, Minerals and Mining and of the Society of Economic Geology (SEG).

Technical Information

Rock and core samples have been prepared and analyzed at SGS laboratory facilities in Medellin, Colombia and Lima, Peru. Blanks, duplicates, and certified reference standards are inserted into the sample stream to monitor laboratory performance. Crush rejects and pulps are kept and stored in a secured storage facility for future assay verification. No capping has been applied to sample composites. The Company utilizes a rigorous, industry-standard QA/QC program.

Information Contact:

Follow Executive Chairman Ari Sussman (@Ariski) and Collective Mining (@CollectiveMini1) on Twitter

FORWARD-LOOKING STATEMENTS

This news release contains certain forward-looking statements, including, but not limited to, statements about the drill programs, including timing of results, and Collective’s future and intentions. Wherever possible, words such as “may”, “will”, “should”, “could”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict” or “potential” or the negative or other variations of these words, or similar words or phrases, have been used to identify these forward-looking statements. These statements reflect management’s current beliefs and are based on information currently available to management as at the date hereof.

Forward-looking statements involve significant risk, uncertainties, and assumptions. Many factors could cause actual results, performance, or achievements to differ materially from the results discussed or implied in the forward-looking statements. These factors should be considered carefully, and readers should not place undue reliance on the forward-looking statements. Although the forward-looking statements contained in this news release are based upon what management believes to be reasonable assumptions, Collective cannot assure readers that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as of the date of this news release, and Collective assumes no obligation to update or revise them to reflect new events or circumstances, except as required by law.

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this news release.

VANCOUVER, BC / ACCESSWIRE / February 14, 2023 / Stillwater Critical Minerals (TSX.V:PGE)(OTCQB:PGEZF)(FSE:5D32) (the “Company” or “SWCM”) is pleased to announce it has partnered with Cornell University under the MINER program, funded by the U.S. Department of Energy (“DOE”) via the Advanced Research Projects Agency program (“ARPA-E”). Test work, led by Dr. Greeshma Gadikota, will focus on novel hydrometallurgical techniques and carbon capture, with the objective of increasing the extraction of critical minerals using reduced energy for a carbon negative mining future.

Cornell University is the recipient of a federal grant from ARPA-E as part of a program entitled “Supercritical CO2-Based Mining for Carbon-Negative Critical Mineral Recovery”. Cornell University seeks to advance CO2-sourced hydrometallurgical pathways for recovering energy critical metals, including nickel, cobalt, platinum and palladium, coupled to the carbon mineralization of calcium and magnesium components to produce calcium and magnesium carbonates. Novel functional materials for the selective capture and recovery of these energy critical metals will be developed. Various sources for CO2 will be investigated including air for metal recovery coupled to carbon mineralization. These approaches will be specifically tuned to the mineralogy of the Company’s Stillwater West project in Montana.

Stillwater Critical Minerals, Tuesday, February 14, 2023, Press release picture

Dr. Greeshma Gadikota

Dr. Greeshma Gadikota stated, “The U.S. imports the great majority of its energy critical metals from mines all over the world, leaving the U.S. quite vulnerable. Our research is all about decarbonizing the mining industry and developing an independent, domestic supply chain of these critical metals. It’s important for U.S. manufacturing, green energy, national security, and competitiveness.”

Relating to the Cornell University partnership, Company President and CEO, Michael Rowley, will join Dr. Gadikota at the ARPA-E MINER kick-off event in Austin, Texas on February 14 and 15, 2023. Other presenters and attendees include Tesla Motors, major mining companies, top US government officials and financial institutions. More information on the MINER program is available here: https://arpa-e.energy.gov/technologies/programs/miner.

Michael Rowley, Stillwater Critical Minerals President & CEO, stated, “We are very pleased to be selected as the industry partner for Dr. Gadikota’s cutting-edge work and to work closely with her team toward our shared vision of securing the future domestic supply of the critical minerals the US so urgently needs. Our Stillwater West project is rapidly advancing as a potential large-scale, low-carbon source of nickel, copper, cobalt, palladium, platinum and rhodium. Located in an active and expanding US mining district with a long history of critical minerals production and demonstrated world-class scale and grade, Stillwater West is on a very short list of assets with the potential to play a significant role in realizing the goals set out in the bipartisan Inflation Reduction Act, and other ongoing initiatives. It is our belief that mining can do more than supply minerals by conventional means, and that partnerships such as this are the path toward more sustainable practices.”

About Dr. Greeshma Gadikota

Dr. Greeshma Gadikota is an Assistant Professor and Croll Sesquicentennial Fellow in the School of Civil and Environmental Engineering with a field appointment in the Smith School of Chemical and Biomolecular Engineering at Cornell University. Dr. Gadikota directs the Sustainable Energy and Resource Recovery Group. She held postdoctoral research associate appointments at Princeton University and Columbia University, and a research associate appointment at the National Institute of Standards and Technology (NIST). Her PhD in Chemical Engineering and MS degrees in Chemical Engineering and Operations Research are from Columbia University. Her BS in Chemical Engineering is from Michigan State University. She is a recipient of the DOE, NSF and ARO CAREER Awards, Sigma Xi Young Investigator Award, Cornell Engineering Research Excellence Award, Inaugural Cornell Rising Women Innovator Award, and AICHE Sabic Award for Young Professionals from the Particle Technology Forum. Dr. Gadikota received her PhD in Chemical Engineering and earned her MS degrees in Chemical Engineering and Operations Research, from Columbia University. Her BS in Chemical Engineering is from Michigan State University.

Research Interests

With more than 80% of our energy resources recovered from the subsurface environments which requires about 50 billion cubic meters of fresh water and contributes to more than 75% of global CO2 emissions, our grand societal challenge lies in meeting our growing demand for energy and resources while reducing environmental impact. Addressing these earth-scale challenges requires us to develop novel technologies to engineer targeted physico-chemical interactions in complex engineered and natural environments. Enabling emergent technologies for a sustainable earth requires us to advance the cross-scale science of fluid-solid interactions in complex and extreme environments. With this perspective, our research is directed towards applications that involve (i) engineering the natural environment for sustainable energy and resource recovery and (ii) designing novel chemical pathways for advancing low carbon and negative emissions technologies.

About ARPA-E

The Advanced Research Projects Agency-Energy (ARPA-E advances high-potential, high-impact energy technologies that are too early for private-sector investment. ARPA-E awardees are unique because they are developing entirely new ways to generate, store, and use energy. ARPA-E projects have the potential to radically improve U.S. economic prosperity, national security, and environmental well-being. We focus on transformational energy projects that can be meaningfully advanced with a small amount of funding over a defined period of time. Our streamlined awards process enables us to act quickly and catalyze cutting-edge areas of energy research.

ARPA-E empowers America’s energy researchers with funding, technical assistance, and market readiness. Our rigorous program design, competitive project selection process, and active program management ensure thoughtful expenditures. ARPA-E Program Directors serve for limited terms to ensure a constant infusion of fresh thinking and new perspectives. To learn more visit: https://arpa-e.energy.gov/.

About Stillwater Critical Minerals Corp.

Stillwater Critical Minerals (TSX.V: PGE | OTCQB: PGEZF) is a mineral exploration company focused on its flagship Stillwater West Ni-PGE-Cu-Co + Au project in the iconic and famously productive Stillwater mining district in Montana, USA. With the recent addition of two renowned Bushveld and Platreef geologists to the team, the Company is well positioned to advance the next phase of large-scale critical mineral supply from this world-class American district, building on past production of nickel, copper, and chromium, and the on-going production of platinum group and other metals by neighboring Sibanye-Stillwater. Per an expanded NI 43-101 mineral resource estimate released January 2023, the Platreef-style nickel and copper sulphide deposits at Stillwater West contain 1.6 billion pounds of nickel, copper and cobalt, and 3.8 million ounces of palladium, platinum, rhodium, and gold, in a compelling suite of critical minerals and are open for expansion along trend and at depth.

Stillwater Critical Minerals also holds the high-grade Black Lake-Drayton Gold project adjacent to Treasury Metals’ development-stage Goliath Gold Complex in northwest Ontario, currently under an earn-in agreement with Heritage Mining, and the Kluane PGE-Ni-Cu-Co critical minerals project on trend with Nickel Creek Platinum‘s Wellgreen deposit in Canada‘s Yukon Territory.

Note 1: References to adjoining properties are for illustrative purposes only and are not necessarily indicative of the exploration potential, extent or nature of mineralization or potential future results of the Company’s projects.

Note 2: Magmatic Ore Deposits in Layered Intrusions-Descriptive Model for Reef-Type PGE and Contact-Type Cu-Ni-PGE Deposits, Michael Zientek, USGS Open-File Report 2012-1010.

Forward Looking Statements: This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Stillwater Critical Minerals believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Stillwater Critical Minerals and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

VANCOUVER, BC, Feb. 14, 2023 /CNW/ – Bravo Mining Corp. (TSXV: BRVO) (OTCQX: BRVMF), (“Bravo” or the “Company“) announced that it has received assay results from eight diamond drill holes (“DDH”) in the Central and North Sectors highlighting the nickel sulphide potential of its 100% owned Luanga palladium + platinum + rhodium + gold + nickel project (“Luanga” or “Luanga PGM+Au+Ni Project“), located in the Carajás Mineral Province, state of Pará, Brazil. Two DDH in the Central Sector have identified a new zone and style of nickel sulphide mineralization. Follow up drilling to the previously announced massive sulphide intercept in the North Sector (August 16th, 2022 news release) has intersected higher-grade nickel sulphide 50m to the north and south, with evidence indicating potential extensions toward the south.

“Today’s results demonstrate the potential for higher-grade nickel ± copper sulphides at Luanga, underlie the existing ~8.1km strike of PGM+Au+Ni mineralization intersected in shallow historic drilling,” said Luis Azevedo, Chairman and CEO of Bravo. “We are at the early stages of understanding the distribution of, and controls on, this potential new style of nickel ± copper sulphide mineralization, which has now been intersected in both the North and Central Sectors,” he said. “We are very positive about the potential below Luanga and have deployed geophysical tools aimed at detecting this style of mineralization. Work is continuing and aims to drill test future geophysical targets in 2023.”

Highlights Include:

Follow up, step-out drilling to the massive nickel/copper sulphides intercepted in DDH22LU047 (August 16th, 2022 news release)intersected nickel/copper sulphides along strike, 50m to the north and to the south. Electromagnetics (EM) has identified conductors trending to the south where surface EM is ongoing.

Drilling in the Central Sector of Luanga has intersected a new zone and style ofnickel sulphide mineralization, potentially magmaticnickel sulphide mineralization. It occurs within a different rock-type than the PGM+Au+Ni mineralization at Luanga – further increasing the exploration prospectivity of Luanga. EM surveying is expected to begin shortly.

A noticeable change in PGM chemistry (significantly higher rhodium to palladium ratio) has been identified in most assay results from both nickel sulphide zones. This also points to a new style of mineralization and provides another possible vector into higher nickel sulphide zones.

HOLE-ID

From(m)

To(m)

Thickness (m)

Pd(g/t)

Pt(g/t)

Rh(g/t)

Au (g/t)

PGM + Au (g/t)

Ni (% Sulphide)

Cu (%)

Sector

DDH22LU039

128.2

155.9

27.7

0.40

0.10

0.11

0.01

0.62

0.42

Cent.

Including

128.2

132.8

4.6

0.74

0.12

0.25

0.01

1.12

1.12

Cent.

Including

130.2

131.2

1.0

1.08

0.25

0.51

0.01

1.85

2.08

Cent.

DDH22LU049

49.6

74.9

25.3

0.68

0.22

0.13

0.12

1.14

0.40

0.23

North

Including

66.9

70.3

3.4

1.18

0.52

0.29

0.12

2.12

0.84

0.34

North

DDH22LU052

151.0

158.1

7.1

0.69

0.04

0.30

0.11

1.13

0.82

0.45

North

Including

151.0

153.8

2.8

0.76

0.02

0.39

0.01

1.18

1.09

0.22

North

DDH22LU061

102.4

103.6

1.2

0.55

0.04

0.31

0.15

1.05

1.18

Cent.

DDH22LU073

136.9

155.8

18. 9

0.96

0.29

0.02

0.02

1.30

0.41

North

Including

150.8

153.8

3.0

2.57

0.50

0.04

0.02

3.14

1.15

North

DDH22LU077

169.4

175.5

6.1

0.57

0.04

0.33

0.02

0.96

0.63

North

Including

169.4

171.3

1.9

1.33

0.05

0.84*

0.04

2.27*

1.47

North

Including

170.6

171.3

0.7

1.54

0.04

>1.0*

0.01

2.59*

2.27

North

Notes: All ‘From’, ‘To’ depths, and ‘Thicknesses’ are downhole.

All intercepts were in fresh rock.

Given the orientation of the hole and the mineralization, the intercepts are estimated to be 85% to 100% of true thickness.

* Includes Rh >1.00g/t result. Overlimit analyses pending.

North = North Sector. Cent. = Central Sector. ** Bravo’s nickel grades are sulphide nickel, and do not include non-recoverable silicate nickel, unlike historic total nickel assays.

Central Sector Magmatic Nickel Sulphide Exploration Upside

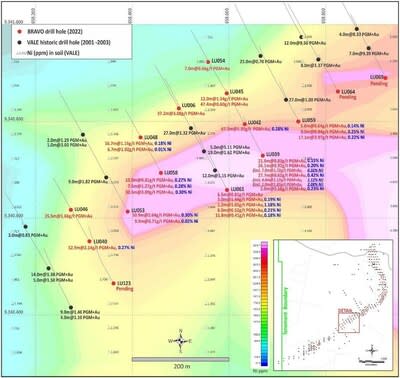

Drilling in the Central Sector (holes DDH22LU039 and DDH22LU061) identified a second zone of more concentrated magmatic sulphides, a style of mineralization not previously observed at Luanga in historic drilling. This style of mineralization features net-textures typical of magmatic nickel sulphide mineralization (Figure 1).

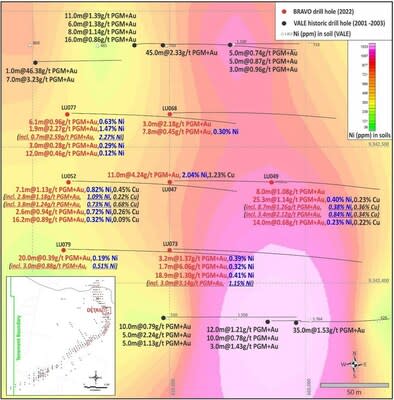

Figure 1: Core photos from Central Sector (039) and North Sector (049 and 052) with nickel ± copper sulphide mineralization. (CNW Group/Bravo Mining Corp.)

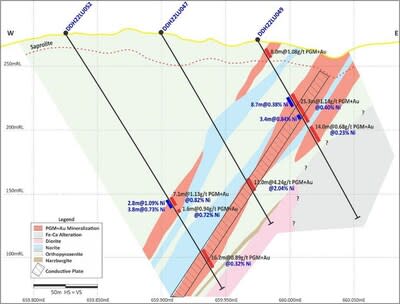

The Central Sector higher-grade magmatic nickel sulphide mineralization appears to be coincident with the main Luanga PGM mineralization but appears to have increasing concentrations of nickel sulphides to depth, while historic nickel-in-soil geochemistry (Figure 2) indicates that nickel sulphide mineralization may be gently diverging away from the strike of the PGM+Au mineralization. This style of mineralization has only been identified in this area of the Luanga deposit to date and is hosted in the basal sequence of harzburgites (ultramafic rocks) that underlie the dominant Luanga orthopyroxenite PGM+Au host rock.

Surface EM completed by Bravo in late 2022 is being extended to the southeast to look deeper into the basal harzburgite sequence (Figure 3) that underlies the main PGM+Au+Ni mineralization, beyond the extent of current drilling.

The Central Zone assay results (reported in this news release) from drill holes DDH22LU039 and DDH22LU061 demonstrate a noticeable change in PGM chemistry, where the Pd:Rh ratios range from 4:1 to <2:1. This is a significant divergence from the majority of existing drill holes across the 8.1km of the main Luanga PGM+Au mineralized zone, where the Pd:Rh ratio is typically ~10:1. There could also be a relationship between magmatic nickel and rhodium (high rhodium values highlighted in the table above). This, combined with the identification of a different host rock, is further supporting evidence of a new style or phase of mineralization that is more typically associated with magmatic nickel sulphide deposits. Mineralization remains open at depth (Figure 3) and along strike.

Figure 2: Nickel sulphide zone in the Central Sector, shown over historic Ni-in-soil geochemistry. (CNW Group/Bravo Mining Corp.)

DDH22LU039 is shown in the section below (Figure 3), where the concentration of magmatic nickel sulphides and nickel assay grades increase (from west to east) from DDH22LU054 where fresh rock mineralization has no significant nickel to report, to DDH22LU039 where magmatic nickel sulphides and assay grades reach their current peak.

Figure 3: Central Zone cross section showing the increase in nickel grade to the southeast (open at depth). (CNW Group/Bravo Mining Corp.)

Follow Up on North Sector Massive Magmatic Nickel ± Copper SulphideDiscovery

Follow up drilling to the north and south of the previously announced massive magmatic nickel ± copper sulphide mineralization in DDH22LU047 (August 16th, 2022 news release) in the North Sector has continued to intersect magmatic nickel sulphide mineralization.

New drill results indicate that the nickel ± copper mineralization is coincident with the main Luanga PGM+Au+Ni deposit, but that higher concentrations of nickel and copper are at depth. Alternatively, this mineralization style may be unrelated to the emplacement of the PGM portion of Luanga and related to a different, as yet unidentified, phase of mineralization at depth.

Higher-grade sulphide mineralization and EM anomalism is open to the south (Figure 4) but appears to taper off to the north. Like the Central Sector above, it may also be diverging away from the strike of the PGM+Au mineralization and occur below historic drilling to the south. This interpretation is supported to the southern limit of the current EM survey and is coincident with historic nickel-in-soil geochemistry (Figures 4 and 5).

Most assay results demonstrate the same noticeable change in PGM chemistry as the higher-grade magmatic sulphide mineralization intersected in the Central Zone, with Pd:Rh ratios ranging from to 5:1 to <2:1. As highlighted above this may indicate potential for a different phase or style of mineralization at depth.

Figure 4: Nickel ± copper sulphide zone in the North Sector, shown over historic Ni-in-soil geochemistry. (CNW Group/Bravo Mining Corp.)

Figure 5: North Sector Cross Section showing new drill holes DDH22LU052 and DDH22LU049 (open at depth). (CNW Group/Bravo Mining Corp.)

Luanga Drill Program Progress

A total of 144 drill holes (9 in 2023) have been completed by Bravo to date, for 23,950 metres (94% of the planned 25,500 metre Phase 1 Drilling Program), including all 8 planned twin holes (results for 2 twin holes outstanding) and all 8 metallurgical holes (not for routine assaying). Results have been reported for 60 Bravo drill holes to date.

Results for76 Bravo drill holes are currently outstanding.

The Phase 1 diamond drill program is close to completion, with 1,550m remaining before the commencement of the Phase 2 diamond drill program. The Phase 2 program will be focused on step out drilling (with the objective of extending known zones of PGM+Au+Ni mineralization to depth), follow-up on the newly identified higher-grade nickel ± copper magmatic sulphide mineralization styles, as well as exploration of new targets.

Aside from systematic step-out drilling, the Phase 2 program is designed to support a more intensive approach to exploration, with work to focus on exploring for magmatic nickel ± copper sulphides. This program will commence with an extensive program of geophysics consisting of ground EM, ground micro-gravity and ground magnetics. Targets generated would be drill tested during the Phase 2 program. Phase 2 will also include ongoing metallurgical test work designed to confirm and optimize metallurgical results reported by Vale SA., Luanga’s previous owner.

The key deliverable expected from the Phase 1 program is Luanga’s maiden NI 43-101 Mineral Resource Estimate (MRE). Approximately 3,600m of priority drilling remains to be completed to facilitate this work, including the balance of the Phase 1 program and a portion of the Phase 2 program. Completion of the maiden MRE remains on track for H2/2023.

Complete Table of Recent Intercepts

HOLE-ID

From(m)

To(m)

Thickness (m)

Pd(g/t)

Pt(g/t)

Rh(g/t)

Au (g/t)

PGM + Au (g/t)

Ni (% Sulphide)

Cu (%)

TYPE

DDH22LU039

41.2

61.2

21.0

0.54

0.19

0.00

0.11

0.83

0.15

FR

And

80.1

106.2

26.1

0.56

0.22

0.00

0.14

0.92

0.20

FR

Including

91.2

98.2

7.0

0.44

1.11

0.01

0.17

1.72

0.32

FR

And

128.2

155.9

27.7

0.40

0.10

0.11

0.01

0.62

0.42

FR

Including

128.2

132.8

4.6

0.74

0.12

0.25

0.01

1.12

1.12

FR

Including

130.2

131.2

1.0

1.08

0.25

0.51

0.01

1.85

2.08

FR

And

161.9

166.9

5.0

0.35

0.15

0.07

0.01

0.58

0.23

FR

DDH22LU049

8.7

16.7

8.0

0.71

0.26

0.02

0.10

1.08

NA

Ox

And

49.6

74.9

25.3

0.68

0.22

0.13

0.12

1.14

0.40

0.23

FR

Including

49.6

58.3

8.7

0.79

0.19

0.09

0.19

1.26

0.38

0.36

FR

Also Including

66.9

70.3

3.4

1.18

0.52

0.29

0.12

2.12

0.84

0.34

FR

And

78.4

92.4

14.0

0.42

0.14

0.04

0.08

0.68

0.23

0.22

FR

DDH22LU052

151.0

158.1

7.1

0.69

0.04

0.30

0.11

1.13

0.82

0.45

FR

Including

151.0

153.8

2.8

0.76

0.02

0.39

0.01

1.18

1.09

0.22

FR

Also Including

154.3

158.1

3.8

0.73

0.05

0.27

0.19

1.24

0.73

0.68

FR

And

161.9

164.5

2.6

0.58

0.06

0.28

0.01

0.94

0.72

0.26

FR

And

199.0

215.2

16.2

0.40

0.46

0.03

0.01

0.89

0.32

0.09

FR

DDH22LU061

59.3

65.8

6.5

0.49

0.19

0.00

0.13

0.81

0.09

FR

And

88.5

91.5

3.0

0.90

0.30

0.00

0.24

1.44

0.19

FR

And

102.4

103.6

1.2

0.55

0.04

0.31

0.15

1.05

1.18

FR

And

121.3

127.3

6.0

0.26

0.14

0.03

0.09

0.52

0.21

FR

And

139.0

150.8

11.8

0.27

0.10

0.02

0.02

0.41

0.18

FR

DDH22LU068

39.5

42.5

3.0

1.35

0.73

0.10

0.01

2.18

0.07

FR

And

54.4

62.2

7.8

0.33

0.10

0.02

0.01

0.45

0.30

FR

DDH22LU073

113.6

116.8

3.2

0.89

0.44

0.03

0.01

1.37

0.39

FR

And

127.8

129.5

1.7

0.89

5.11

0.05

0.01

6.06

0.32

FR

And

136.9

155.8

18. 9

0.96

0.29

0.02

0.02

1.30

0.41

FR

Including

150.8

153.8

3.0

2.57

0.50

0.04

0.02

3.14

1.15

FR

DDH22LU077

169.4

175.5

6.1

0.57

0.04

0.33

0.02

0.96

0.63

FR

And

169.4

171.3

1.9

1.33

0.05

0.84*

0.04

2.27*

1.47

FR

Including

170.6

171.3

0.7

1.54

0.04

>1.0*

0.01

2.59*

2.27

FR

And

204.1

207.1

3.0

0.27

0.01

0.00

0.01

0.28

0.29

FR

And

220.1

232.1

12.0

0.28

0.13

0.02

0.03

0.46

0.12

FR

DDH22LU079

179.3

199.3

20.0

0.23

0.11

0.04

0.01

0.39

0.19

FR

including

196.3

199.3

3.0

0.58

0.18

0.12

0.01

0.88

0.51

FR

Notes: All ‘From’, ‘To’ depths, and ‘Thicknesses’ are downhole.

Given the orientation of the hole and the mineralization, the intercepts are estimated to be 85% to 100% of true thickness.

Type: Ox = Oxide. LS = Low Sulphur. FR = Fresh Rock. Recovery methods and results will differ based on the type of mineralization.

* = Includes Rh >1.00g/t result. Overlimit analyses pending.

** = Bravo’s nickel grades are sulphide nickel, and do not include non-recoverable silicate nickel, unlike historic total nickel assays

Figure 6: Location of Bravo Drilling Reported in this News Release (CNW Group/Bravo Mining Corp.)

About Bravo Mining Corp.

Bravo is a Canada and Brazil-based mineral exploration and development company focused on advancing its Luanga PGM+Au+Ni Project in the world-class Carajás Mineral Province of Brazil.