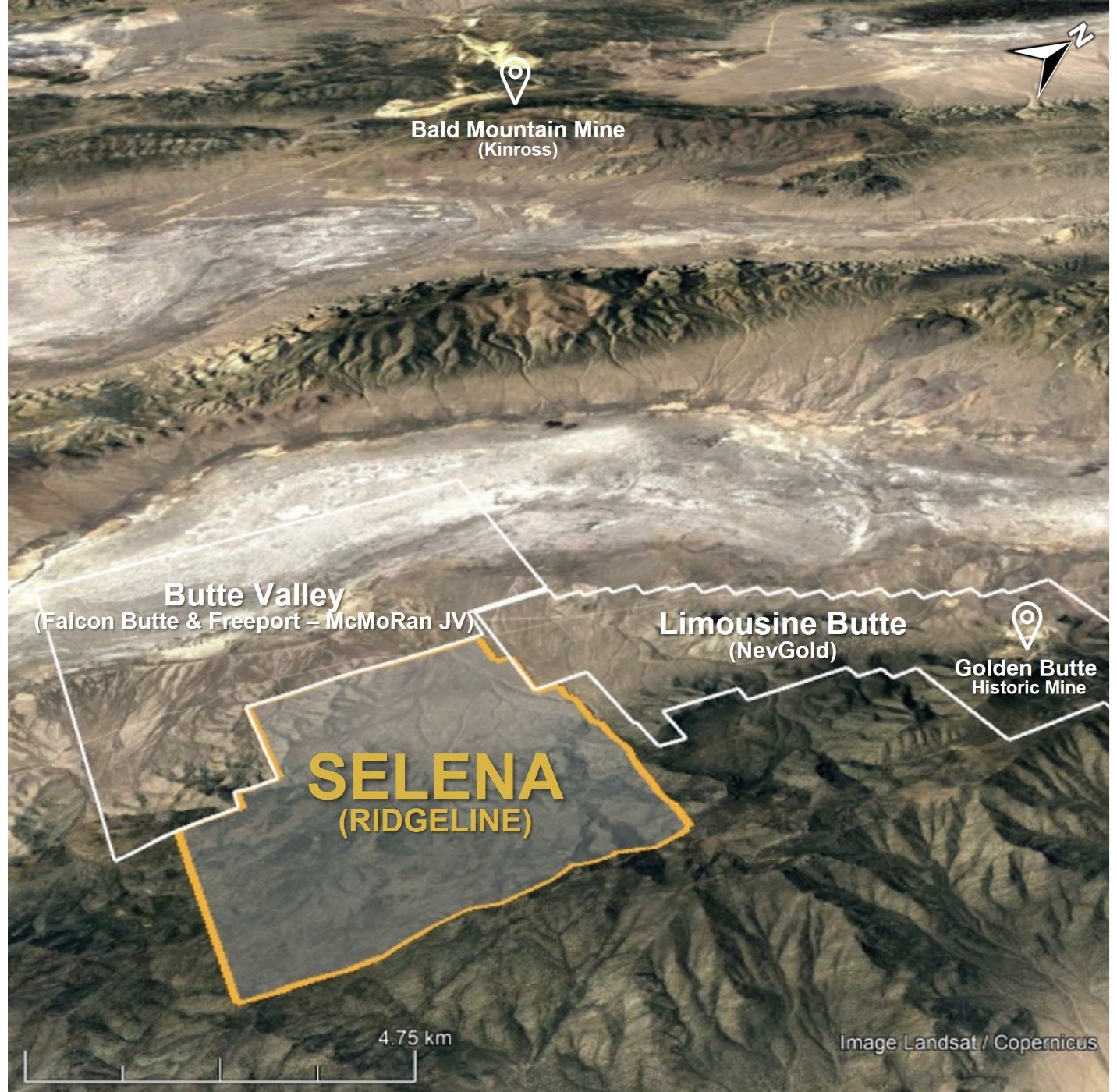

Vancouver, British Columbia–(Newsfile Corp. – July 24, 2023) – Ridgeline Minerals Corp. (TSXV: RDG) (OTCQB: RDGMF) (FSE: 0GC0) (“Ridgeline” or the “Company”) is pleased to announce the commencement of the Company’s diamond core drill program at the Selena project (“Selena”). Selena is host to a silver (“Ag”) – gold (“Au”) – lead (“Pb”) – zinc (“Zn”) carbonate replacement (“CRD”) style discovery located in White Pine County, Nevada (Figure 1).

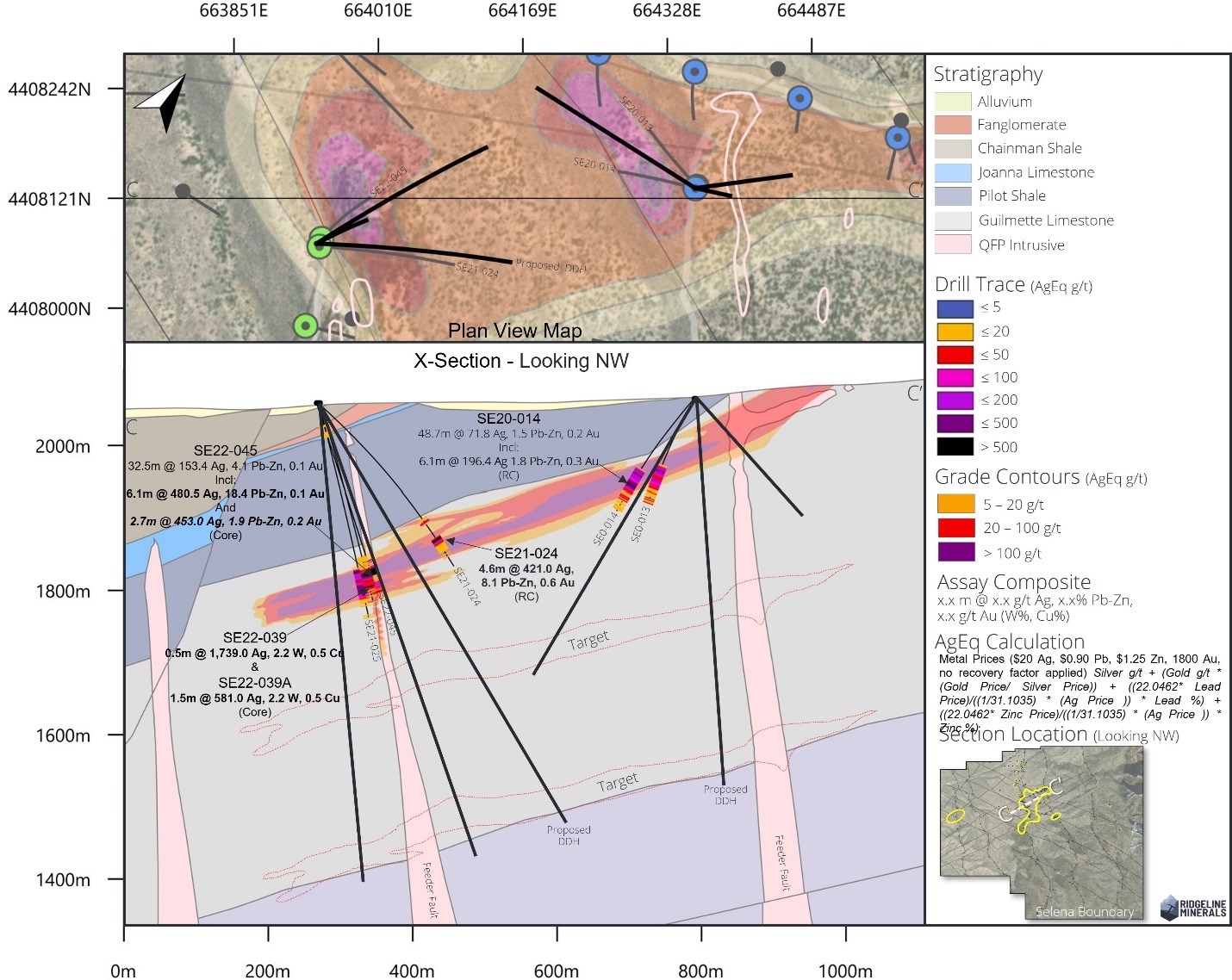

The drill program has been designed to follow-up on bonanza grade CRD intercepts drilled at the Chinchilla zone in 2022, with highlights including 6.1 meters (“m”) grading 480 grams per tonne (“g/t”) Ag, 12.0% Pb, 6.4% Zn, and 0.1 g/t Au in SE22-045 and 0.5 m grading 1,793 g/t Ag, 2.2% tungsten (“W”) and 0.5% copper (“Cu”) in SE22-039 (see January 24, 2023 press release HERE). The program will complete up to six (6) core holes for a total of 3,000 m with results to be released as they are received (Figure 2).

Mike Harp, Vice President, Exploration commented, “Last year’s program delivered the best intercepts in the project’s history. It also confirmed our theory that core drilling would significantly upgrade historical reverse circulation assay results, indicating substantial upside as we convert historically drilled RC intercepts to core. Our 2023 program will build off that success and focus on expanding the high-grade mineralization at two known “chimney” or feeder structures that make up the core of the Chinchilla Zone. We will also drill the lower half of the Guilmette Limestone host rocks, which we believe have potential to host multiple stacked CRD horizons adjacent to known chimney structures.”

Selena Project Selena is located in White Pine County, Nevada, approximately 64 kilometers (“km”) north of the town of Ely, NV. The project shares a property boundary with the Butte Valley project, a US $33M earn-in agreement between Freeport-McMoRan and Falcon Butte Minerals. The 100% owned project is comprised of 39 square kms of highly prospective exploration ground including Ridgeline’s shallow-oxide Ag-Au-Pb-Zn Chinchilla discovery. Subsequent drilling has continued to highlight the potential for high-grade CRD type mineralization (Ag-Au-Pb-Zn ±Cu) between Chinchilla and the Butte Valley Cu-Au-Ag porphyry located directly west of the property. (View the Selena VRIFY Deck Here)

Figure 1: Plan view map showing location of the Selena project which sits directly adjacent to the Butte Valley Porphyry, a US $33M earn-in exploration agreement between Freeport-McMoRan and Falcon Butte Minerals

Figure 2: X-Section C-C’ with scaled plan view map showing past Chinchilla zone intercepts and proposed chimney and manto targets to be tested beneath known high-grade CRD intercepts

QAQC Procedures Samples are submitted to American Assay Laboratories (AAL) of Sparks, Nevada, which is a certified and accredited laboratory, independent of the Company. Samples are prepared using industry-standard prep methods and analysed using FA-PB30-ICP (Au; 30 g fire assay) and ICP-5AM48 (48 element Suite; 0.5 g 5-acid digestion/ICP-MS) methods. AAL also undertakes its own internal coarse and pulp duplicate analysis to ensure proper sample preparation and equipment calibration. Ridgeline’s QA/QC program includes regular insertion of CRM standards, duplicates, and blanks into the sample stream with a stringent review of all results completed by the Company’s Qualified Person, Michael T. Harp, Vice President, Exploration.

Technical information contained in this news release has been reviewed and approved by Michael T. Harp, CPG. the Company’s Vice President, Exploration, who is Ridgeline’s Qualified Person under National Instrument 43-101 and responsible for technical matters of this release.

About Ridgeline Minerals Corp. Ridgeline is a discovery focused gold-silver explorer with a proven management team and a 192 km² exploration portfolio across six projects in Nevada and Idaho, USA. More information about Ridgeline can be found at www.RidgelineMinerals.com.

On behalf of the Board “Chad Peters” President & CEO

Further Information: Chad Peters, P.Geo. President & CEO Ridgeline Minerals Corp. (775) 304-9773 | info@ridgelineminerals.com

Neither the TSX Venture Exchange nor its Regulation Service Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this press release.

Cautionary Note regarding Forward-Looking Statements Statements contained in this press release that are not historical facts are “forward-looking information” or “forward-looking statements” (collectively, “Forward-Looking Information”) within the meaning of applicable Canadian securities legislation and the United States Private Securities Litigation Reform Act of 1995. Forward-Looking Information includes, but is not limited to, the anticipated benefits of the Earn-In Agreement and the transaction contemplated thereby. The words “potential”, “anticipate”, “meaningful”, “discovery”, “forecast”, “believe”, “estimate”, “expect”, “may”, “will”, “project”, “plan”, “historical”, “historic” and similar expressions are intended to be among the statements that identify Forward-Looking Information. Forward-Looking Information involves known and unknown risks, uncertainties and other factors which may cause the actual results to be materially different from any future results expressed or implied by the Forward-Looking Information. In preparing the Forward-Looking Information in this news release, Ridgeline has applied several material assumptions, including, but not limited to, assumptions that TSX Venture Exchange approval will be granted in a timely manner subject only to standard conditions; the current objectives concerning the Project can be achieved and that its other corporate activities will proceed as expected; that general business and economic conditions will not change in a materially adverse manner; and that all requisite information will be available in a timely manner. Forward-Looking Information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance, or achievements of Ridgeline to be materially different from any future results, performance or achievements expressed or implied by the Forward-Looking Information. Such risks and other factors include, among others, risks related to dependence on key personnel; risks related to unforeseen delays; risks related to historical data that has not been verified by the Company; as well as those factors discussed in Ridgeline’s public disclosure record. Although Ridgeline has attempted to identify important factors that could affect Ridgeline and may cause actual actions, events, or results to differ materially from those described in Forward-Looking Information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that Forward-Looking Information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on Forward-Looking Information. Except as required by law, Ridgeline does not assume any obligation to release publicly any revisions to Forward-Looking Information contained in this news release to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

VANCOUVER, BC / ACCESSWIRE / July 28, 2023 / Blackwolf Copper and Gold Ltd. (“Blackwolf”, or the “Company”) (TSXV:BWCG)(OTC PINK:BWCGF) is pleased to announce the launch of the maiden drill program at the Cantoo Mountain Project (“Cantoo”) in Southwest Alaska. The Cantoo Property is located adjacent to the Canadian border and the historic Premier Gold Mine that is currently in redevelopment. Initial drill holes could be in excess of 700 meters to test the multiple structures. This marks the first modern exploration effort at Cantoo since the 1920s and the first ever diamond drill program testing Multiple stacked shallow-dipping vein structures and breccia, including a 30m (100ft) wide vein. During preliminary sampling, Blackwolf uncovered a significant 30-meter (100ft) vein exhibiting high-grade results of up to 30.4g/t Gold, 2860 g/t Silver, and 5.8% Copper outcropping at surface. The initial drill program is planned to cover up to 2000 meters in 4 drill holes over a 1.5 month period with Initial results expected early September.

Morgan Lekstrom, CEO and Director of Blackwolf, commented, “We are proud to commence this drill program, a testament to our commitment to unlocking the potential of this promising location. Cantoo stands out as one of the most compelling untested drill targets in the Golden Triangle. Notably, it lies just approximately 600 meters away from the Premier Mine on the Canadian side of the border. As we know, geology transcends boundaries and borders, and in this prolific region, which is also home to the renowned Brucejack Mine (acquired in 2021 for $2.8 Billion) and numerous other significant mining endeavors, we are poised to unveil the hidden treasures that lie beneath its surface.”

Blackwolf Copper and Gold Ltd, Friday, July 28, 2023, Press release picture

Figure 1: Sampling Results and Drill Plan

Blackwolf Copper and Gold Ltd, Friday, July 28, 2023, Press release picture

Photo 1: Drill pad under construction

Market Making Agreement

Blackwolf is also pleased to announce that it has retained PI Financial Corp. (“PI”) to trade the securities of Blackwolf on the TSX‐V for the purposes of maintaining an orderly market. In consideration of the services provided by PI, the Company will pay PI a monthly cash fee of $5,000 for a minimum term of six months and renewable thereafter. Blackwolf and PI are unrelated and unaffiliated entities. PI will not receive shares or options as compensation. The capital used for market making will be provided by PI.

QA/QC AND QUALIFIED PERSON

The analytical work on the Hyder project will be performed by MSALABS a certified, analytical services provider, at its laboratory in Langley, British Columbia. All samples will be prepared using procedure PRP-910 (dry, crush to 70% passing 2mm, riffle split off 250g, pulverize split to better than 85% passing 75 microns) and analyzed by method FAS-111 (30g fire assay with AAS finish) and IMS-130 (0.5g, aqua regia digestion and ICP-AES/MS analysis). Any samples containing >10g/t Au were reanalyzed using method FAS-415 (30g Fire Assay with gravimetric finish). Samples containing >100 ppm Ag and/or >1% Cu, Pb, & Zn are reanalyzed using method ICF-6 (0.2g, 4-acid digest and ore grade ICP-AES analysis). Samples containing >1000 g/t Ag were reanalyzed using method FAS-418 (30g fire assay with AAS finish) and samples containing >20% Pb were reanalyzed using method STI-8Pb (volumetric titration).

The reported work was completed using industry standard procedures, including a quality assurance/quality control (“QA/QC”) program consisting of the insertion of certified standard, blanks and duplicates into the sample stream. The Qualified Person has reviewed the data and detected no significant QA/QC issues.

Andrew Hamilton, P.Geo., Consultant to the Company, is a Qualified People under NI 43-101, will oversee the 2023 Program and has reviewed and approved the scientific and technical content of this release.

About Blackwolf Copper & Gold Ltd.

The Company holds a 100% interest in the high-grade Niblack copper-gold-zinc-silver VMS project, located adjacent to tidewater in southeast Alaska as well as five Hyder Area gold-silver and VMS properties in southeast Alaska and northwest British Columbia in the Golden Triangle, including the high-priority wide gold-silver veins at the Cantoo Property. Blackwolf’s founding vision is to be an industry leader in transparency, inclusion and innovation. Guided by our Vision and through collaboration with local and Indigenous communities and stakeholders, Blackwolf builds shareholder value through our technical expertise in mineral exploration, engineering and permitting. For more information on Blackwolf, please visit the Company’s website at www.blackwolfcopperandgold.com.

On behalf of the Board of Directors of Blackwolf Copper & Gold Ltd.

“Morgan Lekstrom” CEO and Director

For more information, contact:

Morgan Lekstrom 250-574-7350 (Mobile) 604-343-2997 (Office) rm@bwcg.ca

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Statement Regarding Forward-Looking Information

All statements, trend analysis and other information contained in this press release about anticipated future events or results constitute forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as “seek”, “anticipate”, “believe”, “plan”, “estimate”, “expect” and “intend” and statements that an event or result “may”, “will”, “should”, “could” or “might” occur or be achieved and other similar expressions. All statements, other than statements of historical fact, included herein, including, without limitation, statements regarding anticipated benefits of the Transaction, the closing of the Transaction, the Company’s position in the Golden Triangle and the Company bringing greater awareness to the Company and engaging with current and future shareholders are forward-looking statements. Although Blackwolf believes that the expectations reflected in such forward-looking statements and/or information are reasonable, undue reliance should not be placed on forward-looking statements since Blackwolf can give no assurance that such expectations will prove to be correct. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements, including the risks, uncertainties and other factors identified in Blackwolf’s periodic filings with Canadian securities regulators, and assumptions made with regard to: the ability of Blackwolf and Optimum (the “Companies”) to complete the Transaction; the Companies’ ability to secure the necessary shareholder, securityholder, legal and regulatory approvals required to complete the Transaction; and the Companies’ ability to achieve the synergies expected as a result of the Transaction. Forward-looking statements are subject to business and economic risks and uncertainties and other factors that could cause actual results of operations to differ materially from those contained in the forward-looking statements. Important factors that could cause actual results to differ materially from Blackwolf’s expectations include risks associated with the business of the Companies; risks related to the satisfaction or waiver of certain conditions to the closing of the Transaction; non-completion of the Transaction; risks related to reliance on technical information provided by the Companies; risks related to exploration and potential development of the Companies’ projects; business and economic conditions in the mining industry generally; fluctuations in commodity prices and currency exchange rates; uncertainties relating to interpretation of drill results and the geology, continuity and grade of mineral deposits; the need for cooperation of government agencies and native groups in the exploration and development of properties and the issuance of required permits; the need to obtain additional financing to develop properties and uncertainty as to the availability and terms of future financing; the possibility of delay in exploration or development programs and uncertainty of meeting anticipated program milestones; uncertainty as to timely availability of permits and other governmental approvals; and other risk factors as detailed from time to time and additional risks identified in the Companies’ filings with Canadian securities regulators on SEDAR in Canada (available at www.sedar.com). Forward-looking statements are based on estimates and opinions of management at the date the statements are made. The Company does not undertake any obligation to update forward-looking statements except as required by applicable securities laws. Investors should not place undue reliance on forward-looking statements.

VANCOUVER, British Columbia, July 27, 2023 (GLOBE NEWSWIRE) — West Red Lake Gold Mines Ltd.(“West Red Lake Gold” or “WRLG” or the “Company”) (TSXV: WRLG)(OTCQB: WRLGF) is pleased to announce the appointment of independent director, Hugh Agro, to the Company’s board of Directors.

Mr. Agro, B.Sc., MBA, P.Eng.(non-practising) has over 35 years of leadership and business experience in the mining industry. Since 2017, Mr. Agro has served as President & CEO and Director of Revival Gold Inc., a U.S. focused gold exploration and development company. Prior to Revival Gold Inc., Mr. Agro co-founded Carbon Arc Capital Investments Inc., a private-equity backed investor in mining and metals and served as Executive Vice President, Strategic Development with Kinross Gold Corporation. At Kinross, Mr. Agro was a member of the Executive Leadership Team and responsible for strategic and operational leadership of Kinross’ growth initiatives including corporate development, global exploration and commercial activities in Russia. Previously, Mr. Agro held senior executive positions with Placer Dome and in investment banking with Deutsche Bank’s Global Metals and Mining Group. Mr. Agro has served on the Board and Audit Committees of Victoria Gold Corp., Chantrell Ventures and Americas Silver Corp. and currently serves as a Director of Fort Berens Estate Winery Ltd., an award-winning winery located in British Columbia, Canada. Mr. Agro holds a Bachelor of Science in Mining Engineering from Queen’s University (1989) and MBA Finance from UBC & London Business School (1997).

The appointment of Mr. Agro follows the resignation of Mr. Rob van Egmond from its Board of Directors effective 26, 2023. The Company would like to thank Mr. van Egmond for his contributions to the Company’s success to date.

Shane Williams, President and CEO comments, “We are delighted to welcome Hugh Agro to the West Red Lake Gold team. His qualifications and skillset expand the Board’s expertise as he brings a wealth of experience in executive leadership, strategy, technical expertise and finance. He will be a significant contributor to the expansion and development of West Red Lake Gold’s future.”

The Company has granted 400,000 stock options to Mr. Agro, which vest over a three year period with 25% vesting in 3 months from the grant date and 25% vesting on the first, second and third anniversary of the grant date at an exercise price of $0.69 and will be exercisable for a 5 year period expiring July 26, 2028.

In addition, 100,000 DSUs have been granted to Mr. Agro which will vest on the first anniversary of the grant date of July 26, 2023.

Further to its news release of July 6, 2023, the Company is pleased to announce that due to excess demand, it has increased its non-brokered flow-through private placement financing to $7,000,000 by the issuance of up to 10,000,000 flow-through shares at $0.70 per flow-through share (the “Offering”). The Offering is subject to TSXV approval. The Company intends to use the proceeds from the Offering for the exploration and advancement of its properties in Red Lake, Ontario.

ABOUT WEST RED LAKE GOLD MINES

West Red Lake Gold Mines Ltd. is a mineral exploration company that is publicly traded and focused on advancing and developing its flagship Madsen Gold Mine and the associated 47 Km2 highly prospective land package in the Red Lake district of Ontario. The highly productive Red Lake Gold District of Northwest Ontario, Canada has yielded over 30 million ounces of gold from high-grade zones and hosts some of the world’s richest gold deposits. WRLG also holds the wholly owned Rowan Property in Red Lake, with an expansive property position covering 31 Km2 including three past producing gold mines – Rowan, Mount Jamie and Red Summit.

ON BEHALF OF WEST RED LAKE GOLD MINES LTD.

“Shane Williams”

Shane Williams President & Chief Executive Officer

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Certain statements contained in this news release constitute “forward-looking statements”. When used in this document, the words “anticipated”, “expect”, “estimated”, “forecast”, “planned”, and similar expressions are intended to identify forward-looking statements or information. These statements are based on current expectations of management, however, they are subject to known and unknown risks, uncertainties and other factors that may cause actual results to differ materially from the forward-looking statements in this news release. Readers are cautioned not to place undue reliance on these statements. West Red Lake Gold Mines Ltd. does not undertake any obligation to revise or update any forward- looking statements as a result of new information, future events or otherwise after the date hereof, except as required by securities laws.

Costa Fuego Copper-Gold Project Preliminary Economic Assessment (PEA)1 Outlines One of World’s Lowest Capital Intensity, Major Copper Developments

Strong Economics: Costa Fuego PEA delivers using an 8% discount rate and long-term metal price assumptions of US$3.85/lb copper (Cu) and US$1,750/oz gold (Au)

Base-case post-tax Net Present Value (NPV8%) of US$1.10 Billion (approximately, within a range of US$733 Million to US$1.46 Billion) and Internal Rate of Return (IRR) of 21% (approximately, within a range of 17% to 25%)

Low Start-up Capital: US$1.05 Billion estimated, resulting in fast 3.5-year payback. Initial phases of open pit mining fully fund development of a bulk underground operation

Low Capital Intensity: One of the lowest capital intensities of global copper development projects

Approximately 112 ktpa Average CuEq2 Production Rate: Including 95 kt Cu and 49 koz Au during primary production (first 14 years) at C1 Cash Cost[3] of US$1.33/lb (estimated, net of by-product credits)

Initial Mine Life: 16-years with 1.41 Mt Cu and 718 koz Au produced for total revenue of approximately US$13.52 Billion and total free cash flow of approximately US$3.28 Billion (post-tax, after operating costs, capital costs, and royalties)

US$15 Million Investment Agreement with Osisko Gold Royalties

Strong endorsement from a leading North American royalty-streaming group with funds to be used to advance the Costa Fuego Pre-feasibility Studies (PFS), resource growth drilling programmes and general project advancement.

30,000 m drilling program across multiple targets to commence shortly

Single, Large Pit Scenario for Cortadera being studied in H2 2023

Strong Cash balance of $26 million

__________________________

1 The PEA is preliminary in nature and includes 3% of production feed from Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorised as Mineral Reserves (NI 43-101) or Ore Reserves (JORC 2012), and there is no certainty that the PEA will be realised. Mineral Resources that are not Mineral Reserves or Ore Reserves do not have demonstrated economic viability. References to “Mineral Reserves” in this announcement include Ore Reserves (JORC 2012). See page 39 for additional cautionary language. 2 The copper-equivalent (CuEq) annual production rate was based on the combined processing feed (across all sources) and used long-term commodity prices of: Copper US$3.85/lb, Gold US$1,750/oz, Molybdenum US$17/lb, and Silver US$21/oz; and estimated metallurgical recoveries for the production feed to the following processes: Concentrator (87% Cu, 56% Au, 37% Ag, 58% Mo), Oxide Leach (55% Cu only), & Low-grade Sulphide Leach (40% Cu only). 3 See page 16 for full non-IFRS measures disclaimer.

Hot Chili’s Managing Director and Chief Executive Officer Mr Christian Easterday is responsible for this announcement and has provided sign-off for release to the ASX and TSXV.

The Preliminary Economic Assessment referred to in this report is equivalent to a Scoping Study under JORC Code (2012) reporting guidelines. It has been undertaken for the purpose of initial evaluation of a potential development of the Costa Fuego Copper Project in Chile. It is a preliminary technical and economic study of the potential viability of the Costa Fuego Copper Project. The PEA outcomes, production target and forecast financial information referred to in the report are based on low level technical and economic assessments that are insufficient to support estimation of Ore Reserves. The PEA is presented in US dollars to an accuracy level of +/- 35%. While each of the modifying factors was considered and applied, there is no certainty of eventual conversion to Ore Reserves or that the production target itself will be realised. Further exploration and evaluation and appropriate studies are required before Hot Chili will be in a position to estimate any Ore Reserves or to provide any assurance of any economic development case. Given the uncertainties involved, investors should not make any investment decisions based solely on the results of the PEA.

Of the Mineral Resources scheduled for extraction in the PEA production plan, approximately 97% are classified as Indicated and 3% as Inferred during the 18-year evaluation period. The Company has concluded that it has reasonable grounds for disclosing a production target which includes a small amount of Inferred Mineral Resources. There is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the determination of Indicated Mineral Resources or that the production target itself will be realised. Inferred Mineral Resources comprise 2.5% of the production schedule in the first four years of operation. The viability of the development scenario envisaged in the PEA does not depend on the inclusion of Inferred Mineral Resources.

The Mineral Resources underpinning the production target in the PEA have been prepared by a competent person in accordance with the requirements of the JORC 2012. For full details on the Mineral Resource estimate, please refer to the ASX announcement of 31 March 2022. Hot Chili confirms that it is not aware of any new information or data that materially affects the information included in that release and that all material assumptions and technical parameters underpinning the estimate continue to apply and have not been changed.

To achieve the outcomes indicated in the PEA, including reaching Definitive Feasibility Study (“DFS”) stage, funding in the order of US$1.10 Billion will be required, including pre-production and working capital and assumed financing charges. Investors should note that that there is no certainty that Hot Chili will be able to raise that amount of funding when needed. One of the key assumptions is that the funding for the Project will be available when required. It is also possible that such funding may only be available on terms that may be dilutive to or otherwise affect the value of Hot Chili’s existing shares. It is also possible that Hot Chili could pursue other value realisation strategies such as debt financing, a sale or partial sale of its interest in the Costa Fuego Copper Project, sale of further royalties and/or streaming rights, sale of non-committed offtake rights, and sale of non-core assets.

This report contains forward-looking statements. Hot Chili has concluded that it has a reasonable basis for providing these forward-looking statements and believes it has a reasonable basis to expect it will be able to fund development of the Costa Fuego Copper Project. However, a number of factors could cause actual results or expectations to differ materially from the results expressed or implied in the forward-looking statements. Given the uncertainties involved, investors should not make any investment decisions based solely of the results of the PEA.

SUMMARY OF OPERATIONAL ACTIVITIES

Costa Fuego Copper-Gold Project Preliminary Economic Assessment (PEA)1 Outlines One of World’s Lowest Capital Intensity, Major Copper Developments

The Costa Fuego PEA has been prepared by Wood Australia Pty. Ltd. as an update to the historical Productora 2016 Pre-Feasibility Study (the “2016 PFS”). It follows significant regional consolidation and a near quadrupling of the Company’s resource inventory with the addition of the Cortadera porphyry resource, and the San Antonio high-grade satellite resource. The expanded resource base provided the opportunity to lift the scale of development for a combined development hub (Costa Fuego) and optimise infrastructure required to transport these resources to a proposed centralised processing plant at Productora. The PEA therefore presents a materially different project to that contemplated in the 2016 PFS.

The Costa Fuego PEA presents the largest copper development project listed on the Australian Securities Exchange (ASX). Already the ASX’s largest copper development resource, the PEA confirms Costa Fuego as having the largest potential copper production in the exchange’s development pipeline, (refer to ASX Announcement “Costa Fuego PEA Presentation”, released 28th June 2023, slide 51 “New Material Copper Supply”) at a time when the ASX is losing its significant copper-players, with Oz Minerals taken over by diversified-miner BHP and Newcrest under takeover by US-based Newmont.

The strong economics of Costa Fuego are described below in Table 1, using financial assumptions of an 8% discount rate and long-term metal price assumptions for the base case of US$3.85/lb copper (Cu) and US$1,750/oz gold (Au).

__________________________

1 The PEA is preliminary in nature and includes 3% of production feed from Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorised as Mineral Reserves (NI 43-101) or Ore Reserves (JORC 2012), and there is no certainty that the PEA will be realised. Mineral Resources that are not Mineral Reserves or Ore Reserves do not have demonstrated economic viability. References to “Mineral Reserves” in this announcement include Ore Reserves (JORC 2012). See page 19 for additional cautionary language.

Table 1. Copper Price Ranges: Lower-, Base-, and Upper-Case Scenarios1,2

Project Metric

Units

Copper Price

Lower(US$3.50/lb)

Base(US$3.85/lb)

Upper(US$4.20/lb)

Pre-Tax

NPV8%

US$M

1,046

1,540

2,029

IRR

%

19 %

24 %

29 %

Post-Tax

NPV8%

US$M

733

1,100

1,463

IRR

%

17 %

21 %

25 %

Annual Average Revenue

US$M

779

845

911

Annual Average EBITDA

US$M

384

445

506

Annual Average Free Cash Flow

US$M

226

271

315

Payback period (From First Production)

years

4.25

3.50

3.25

Post-Tax NPV8% /Start-up Capital

0.7

1.1

1.4

Within the base-case scenario of the PEA, the positive economics shown in Table 2 outline a project that leverages its low-elevation advantage to achieve low start-up capital costs and consequently one of the lowest capital intensities of global copper development projects at this scale. Annual average revenue of around US$845 Million allow the project to achieve a fast 3.5-year payback on the back of initial open pit mining that fully funds the project expansion and development of underground bulk mining.

______________________________

1 Certain terms of measurement used in this news release are not performance measures reported in accordance with International Financial Reporting Standards (“IFRS”). Non-IFRS terms measures used such as “Cash Cost”, “All-in Sustaining Costs”, “C1”, “Expansion Costs”, “Free Cashflow” and “All-in costs” are included because these statistics are measures that management uses internally to evaluate performance, to assess how the Project ranks against its peer projects and to assess the overall effectiveness and efficiency of the contemplated mining operations. These performance measures do not have a meaning within IFRS and, therefore, amounts presented may not be comparable to similar data presented by other mining companies. These performance measures should not be considered in isolation as a substitute for measures of performance in accordance with IFRS.

2 The PEA is preliminary in nature and includes 3% of production feed from Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorised as Mineral Reserves, and there is no certainty that the PEA will be realised. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. See page 19 for additional cautionary language.

Table 2: Costa Fuego PEA1Economic Highlights2– Base Case

Project Metric

Units

Estimated Value

Financial Measures

Pre-tax

Cu US$3.85/lb

NPV8%

US$M

1,540

IRR

%

24

Post-tax

Cu US$3.85/lb

NPV8%

US$M

1,100

IRR

%

21

Payback period (from start of operations)

years

3.5

Open Pit Strip Ratio

W/P

1.8

Post-tax NPV/Start-up Capex

Ratio

1.1

Capital Costs Costs2

Total Pre-production Capital Expenditure

US$M

1,046

Expansion

US$M

708

Sustaining

US$M

1,014

Total

US$M

2,768

Operating Costs2

C1

$/lb Cu

1.33

Total Cash Cost (net by-products and including royalties)

$/lb Cu

1.43

All-in-Sustaining Cost

$/lb Cu

1.74

All-In Cost LOM

$/lb Cu

2.31

Mine Life & Metal Production

Primary Mine Production Including Ramp-up

years

14

Mine Life (Life of Mine Processing)

years

16

Primary Mine Production – Average Annual Copper Equivalent Metal[9]

kt

112

Primary Mine Production – Average Annual Copper Metal

kt

95

Primary Mine Production – Average Annual Gold Metal

koz

49

Following the pre-production Capital Cost of around US$1.05 Billion, operations are expanded to access the remaining deposits at an estimated Capital Cost of US$708 Million, with Sustaining Capital Costs bringing the total project Capital Cost to around US$2.77 Billion. Capital Cost incorporated a 20% contingency, with further contingency applied to the mining pit shells, which were developed using a copper price of US$3.30/lb to hedge against downside price risk impacting the production feed inventory.

Operating costs for Costa Fuego average (estimated net of by-products) a C1 Cash Cost of US$1.33/lb of copper, with an approximate average production rate of 112 ktpa CuEq4: Including 95 kt Cu and 49 koz Au during primary production (first 14 years).

__________________________

1 The PEA is preliminary in nature and includes 3% of production feed from Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorised as Mineral Reserves, and there is no certainty that the PEA will be realised. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. See page 39 for additional cautionary language.

2 Certain terms of measurement used in this news release are not performance measures reported in accordance with International Financial Reporting Standards (“IFRS”). See page 40 for full non-IFRS measures disclaimer.

3 Includes Payability

4 The copper-equivalent (CuEq) annual production rate was based on the combined processing feed (across all sources) and used long-term commodity prices of: Copper US$3.85/lb, Gold US$1,750/oz, Molybdenum US$17/lb, and Silver US$21/oz; and estimated metallurgical recoveries for the production feed to the following processes: Concentrator (87% Cu, 56% Au, 37% Ag, 58% Mo), Oxide Leach (55% Cu only), & Low-grade Sulphide Leach (40% Cu only).

The Costa Fuego life-of-mine processing runs for 16-years, producing an estimated 1.41 Mt of copper and 718 koz of gold (plus 22 kt of molybdenum and 1.7 Moz of silver) for total revenue of approximately US$13.52 Billion and total free cash flow of approximately US$3.28 Billion (post-tax, after operating costs, capital costs, and royalties)

Revenues from the PEA metal payload are described in Table 3 below, with 85% of revenue deriving from copper. Costa Fuego is highly leveraged to the copper price, with analysis identifying that for every US$0.10/lb increase above US$ 3.85/lb Cu price, US$100 Million (approximately) is added in post-tax NPV8%

Table 3: Costa Fuego Revenue Breakdown1

LOM Revenue Contribution

Revenue (US$M)

% of Total

Copper in Concentrate

10,342

76 %

Copper Cathode

1,218

9 %

Gold

1,132

8 %

Molybdenum

799

6 %

Silver

32

0.2 %

Total

13,523

100 %

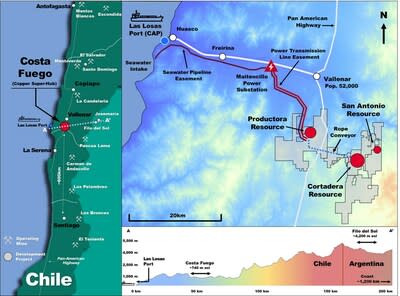

Hot Chili has been systematic in its approach to de-risking the project with over a decade of work in consolidating the deposits and securing infrastructure easements and surface rights. Costa Fuego is one of the very few projects globally that holds a granted water permit, approval for power connection to the national grid and the necessary easement corridors for water and power infrastructure that would support the advancement of the project to construction.

30,000 m drilling program across multiple targets to commence shortly

The Company plans to rapidly begin drilling high priority growth targets proximal to the current resource. Drilling will also test promising greenfield targets as shown in Figure 1. Further strategic regional consolidation options are concurrently being pursued, with mineral resource estimate upgrades expected in Q4 2023 and H1 2025.

_________________________________

1 Includes Payability

Figure 1. Exploration Growth Targets Across the Costa Fuego Project

Figure 1. Exploration Growth Targets Across the Costa Fuego Project (CNW Group/Hot Chili Limited)

Figure 2. Cortadera Porphyry Expansion Targets1

Figure 2. Cortadera Porphyry Expansion Targets (CNW Group/Hot Chili Limited)

Figure 2. Cortadera Porphyry Expansion Targets (CNW Group/Hot Chili Limited)

______________________________________

1 Refer to announcement dated 28th August 2019 for further information regarding Induced Polarisation (IP/MT– MIMDAS) Survey. * Resource Copper Equivalent (CuEq) considers assumed commodity prices and average metallurgical recoveries for the Mineral Resource from testwork. See Page 43 for complete Mineral Resource disclosure of Costa Fuego.

Single, Large Pit Scenario for Cortadera being studied in H2 2023

The Company is investigating a large single open pit scenario for Cortadera (no underground block cave) with the potential to materially increase processing feed inventory and mine-life.

This scenario would necessitate a second PEA, studied while refining of the model inputs for metallurgy, geotechnical engineering and hydrogeology, to be incorporated into the Pre-feasibility. Once both PEA scenarios are assessed, the Company would select a single scenario to complete the final stages of its PFS for Costa Fuego, which is expected to be completed by H2 2024.

SUMMARY OF CORPORATE ACTIVITIES

US$15 Million Investment Agreement with Osisko Gold Royalties

The significant investment by Osisko provides strong endorsement from one of North America’s leading royalty-streaming groups. The key elements of the royalty agreement, which closed in late July, are:

US$15 million in funds for growth and development with the investment (Royalty Consideration) to be used to advance the Costa Fuego Pre-Feasibility Studies (PFS), resource growth drilling programmes and for the general advancement of the Project

Clear “look-through” value given the Osisko NSR is equivalent to a 1.12% CuEq1 NSR royalty across payable metals for US$15 million and Hot Chili’s market capitalisation at the time of announcing the royalty was US$80 million

Buyback rights if a change of control event occurs prior to the fourth anniversary of Closing. The Osisko NSR can be reduced to 0.5% NSR royalty on copper and 2.5% NSR royalty on gold

Osisko to have a Right of First Offer (ROFO) with respect to the sale of any future royalty, stream, or similar interests by Hot Chili

Development and Growth Funding

The Investment by Osisko has strengthened the Company’s cash position to approximately A$26 million and the project is now fully funded for the next 12 to 18 months to deliver the next steps in its growth and development plan, (refer Figure 3) including:

Commencement of 30,000 m drill program – preparations well-advanced, drilling operations set to commence in the coming week.

Completion of Costa Fuego resource upgrade by late 2023.

Delivery of Costa Fuego PFS by H2 2024 – The Company has already considerably advanced its PFS (approximately 80% complete) with minimal expenditure required for completion.

____________________________

1 CuEq considers assumed commodity prices and average metallurgical recoveries from test work. See qualifying statements on page 19.

Figure 3. Costa Fuego Project Roadmap1

Figure 3. Costa Fuego Project Roadmap (CNW Group/Hot Chili Limited)

Figure 4. Location of the Costa Fuego Project Regionally in Relation to Key Infrastructure

Figure 4. Location of the Costa Fuego Project Regionally in Relation to Key Infrastructure (CNW Group/Hot Chili Limited)

______________________________

1 The Mining Project delivery schedule mentioned herein is subject to various risks inherent to the mining industry, and external factors beyond the control of the project stakeholders, including but not limited to, geological and processing challenges, government policies, permits, or regulations, fluctuations in commodity prices, or market conditions. These external factors can impact the Project timeline and potentially result in delays. The delivery schedule provided is based on the best estimates and assumptions available at the time of its creation, and the Project team is committed to minimising disruptions and implementing mitigation measures to the best of their abilities. However, the effectiveness of these measures in avoiding delays cannot be guaranteed.

Drill Results Reported for Costa Fuego in Quarter 2 2023

No further drilling has been completed in Q2, subsequently there are no details to report.

Additional ASX Disclosure Information

ASX Listing Rule 5.3.2: There was no substantive mining production and development activities during the quarter.

ASX Listing Rule 5.3.3 – Schedule of Mineral Tenements as at 30 June 2023

The schedule of Mineral Tenements and changes in interests is appended at the end of this activities report.

ASX Listing Rule 5.3.4: Reporting under a use of funds statement in a Prospectus does not apply to the Company currently.

ASX Listing Rule 5.3.5: Payments to related parties of the Company and their associates during the quarter per Section 6.1 of the Appendix 5B totaled $151,667. This is comprised of directors’ salaries and superannuation of $151,667.

Health, Safety, Environment and Quality

Field operations during the period included geological reconnaissance activities, core-testing and logging, field mapping, and sampling exercises across the Cortadera, El Fuego and Productora landholdings. El Fuego field activities are run from the Cortadera operations centre and safety statistics are combined for reporting.

No safety incidents were recorded during the quarter. The Company’s HSEQ quarterly performance is summarised in Table 3 below.

Hot Chili’s sustainability framework ensures an emphasis on business processes that target long-term economic, environmental and social value. The Company is dedicated to continual monitoring and improvement of health, safety and the environmental systems. There is no greater importance than ensuring the safety of our people and their families.

Table 3 HSEQ Quarter 1 2023 Performance and Statistics

Deposit

Productora

Cortadera

Las Cañas

Timeframe

Q2 2023

Cum.

Q2 2023

Cum.

Q2 2023

Cum.

LTI events

0

0

0

6

0

1

NLTI events

0

2

0

5

0

1

Days lost

0

0

0

152

0

23

LTIFR index

0

0

0

24

0

170

ISR index

0

0

0

596

0

3,898

IFR Index

0

39

0

43

0

339

Thousands of manhours¹

2.1

51.2

7.9

257

0

5.9

Incidents on materials and assets

0

0

0

0

0

0

Environmental incidents

0

0

0

0

0

0

Headcount²

4

11

15

37

0

21

Notes: HSEQ is the acronym for Health, Safety, Environment and Quality. LTIFR per million-manhours. Safety performance is reported on a monthly basis to the National Mine Safety Authority on a standard E-100 form; (1) manhours; (2) Average monthly headcount (3) Cumulative statistics since April 2019.

Tenement Changes During the Quarter

During the Quarter, the Company has renewed the mining exploration concessions Porfiada I (replaces Porfiada I, which expired on June, 14th, 2023), Porfiada II (replaces Porfiada II, which expired on July, 5th, 2023), Porfiada III (replaces Porfiada III, which expired on June, 15th, 2023) and Porfiada IV (replaces Porfiada IV, which expired on July, 5th, 2023).

The Company’s existing tenements are detailed in the table below.

Table 4. Current Tenement (Patente) Holdings in Chile as at 30 June 2023

Cortadera Project

License ID

HCH % Held

HCH % Earning

Area (ha)

Agreement Details

MAGDALENITA 1/20

100% Frontera SpA

100

ATACAMITA 1/82

100% Frontera SpA

82

AMALIA 942 A 1/6

100% Frontera SpA

53

PAULINA 10 B 1/16

100% Frontera SpA

136

PAULINA 11 B 1/30

100% Frontera SpA

249

PAULINA 12 B 1/30

100% Frontera SpA

294

PAULINA 13 B 1/30

100% Frontera SpA

264

PAULINA 14 B 1/30

100% Frontera SpA

265

PAULINA 15 B 1/30

100% Frontera SpA

200

PAULINA 22 A 1/30

100% Frontera SpA

300

PAULINA 24 1/24

100% Frontera SpA

183

PAULINA 25 A 1/19

100% Frontera SpA

156

PAULINA 26 A 1/30

100% Frontera SpA

294

PAULINA 27A 1/30

100% Frontera SpA

300

CORTADERA 1 1/200

100% Frontera SpA

200

CORTADERA 2 1/200

100% Frontera SpA

200

CORTADERA 41

100% Frontera SpA

1

CORTADERA 42

100% Frontera SpA

1

LAS CANAS 16

100% Frontera SpA

1

LAS CANAS 1/15

100% Frontera SpA

146

CORTADERA 1/40

100% Frontera SpA

374

LAS CANAS ESTE 2003 1/30

100% Frontera SpA

300

CORROTEO 1 1/260

100% Frontera SpA

260

CORROTEO 5 1/261

100% Frontera SpA

261

ROMERO 1 AL 31

100% Frontera SpA

31

PURISIMA

100% Frontera SpA

20

NSR 1.5%

Note. Frontera SpA is a 100% owned subsidiary company of Hot Chili Limited

Productora Project

License ID

HCH % Held

HCH % Earning

Area (ha)

Agreement Details

FRAN 1, 1-60

80% SMEA SpA

220

FRAN 2, 1-20

80% SMEA SpA

100

FRAN 3, 1-20

80% SMEA SpA

100

FRAN 4, 1-20

80% SMEA SpA

100

FRAN 5, 1-20

80% SMEA SpA

100

FRAN 6, 1-26

80% SMEA SpA

130

FRAN 7, 1-37

80% SMEA SpA

176

FRAN 8, 1-30

80% SMEA SpA

120

FRAN 12, 1-40

80% SMEA SpA

200

FRAN 13, 1-40

80% SMEA SpA

200

FRAN 14, 1-40

80% SMEA SpA

200

FRAN 15, 1-60

80% SMEA SpA

300

FRAN 18, 1-60

80% SMEA SpA

273

FRAN 21, 1-46

80% SMEA SpA

226

ALGA 7A, 1-32

80% SMEA SpA

89

ALGA VI, 5-24

80% SMEA SpA

66

MONTOSA 1-4

80% SMEA SpA

35

NSR 3%

CHICA

80% SMEA SpA

1

ESPERANZA 1-5

80% SMEA SpA

11

LEONA 2A 1-4

80% SMEA SpA

10

CARMEN I, 1-50

80% SMEA SpA

222

CARMEN II, 1-60

80% SMEA SpA

274

ZAPA 1, 1-10

80% SMEA SpA

100

ZAPA 3, 1-23

80% SMEA SpA

92

ZAPA 5A, 1-16

80% SMEA SpA

80

ZAPA 7, 1-24

80% SMEA SpA

120

CABRITO, CABRITO 1-9

80% SMEA SpA

50

CUENCA A, 1-51

80% SMEA SpA

255

CUENCA B, 1-28

80% SMEA SpA

139

CUENCA C, 1-51

80% SMEA SpA

255

CUENCA D

80% SMEA SpA

3

CUENCA E

80% SMEA SpA

1

CHOAPA 1-10

80% SMEA SpA

50

ELQUI 1-14

80% SMEA SpA

61

LIMARÍ 1-15

80% SMEA SpA

66

LOA 1-6

80% SMEA SpA

30

MAIPO 1-10

80% SMEA SpA

50

TOLTÉN 1-14

80% SMEA SpA

70

CACHIYUYITO 1, 1-20

80% SMEA SpA

100

CACHIYUYITO 2, 1-60

80% SMEA SpA

300

CACHIYUYITO 3, 1-60

80% SMEA SpA

300

LA PRODUCTORA 1-16

80% SMEA SpA

75

ORO INDIO 1A, 1-20

80% SMEA SpA

82

AURO HUASCO I, 1-8

80% SMEA SpA

35

URANIO, 1-70

0 %

0 %

350

25-year Lease AgreementUS$250,000 per year (average for the 25 year term); plus 2% NSR all but gold; 4% NSR gold; 5% NSR non-metallic

JULI 9, 1-60

80% SMEA SpA

300

JULI 10, 1-60

80% SMEA SpA

300

JULI 11 1/60

80% SMEA SpA

300

JULI 12 1/42

80% SMEA SpA

210

JULI 13 1/20

80% SMEA SpA

100

JULI 14 1/50

80% SMEA SpA

250

JULI 15 1/55

80% SMEA SpA

275

JULI 16, 1-60

80% SMEA SpA

300

JULI 17, 1-20

80% SMEA SpA

100

JULI 19

80% SMEA SpA

300

JULI 20

80% SMEA SpA

300

JULI 21 1/60

80% SMEA SpA

300

JULI 22

80% SMEA SpA

300

JULI 23 1/60

80% SMEA SpA

300

JULI 24, 1-60

80% SMEA SpA

300

JULI 25

80% SMEA SpA

300

JULI 27 1/30

80% SMEA SpA

150

JULI 27 B 1/10

80% SMEA SpA

50

JULI 28 1/60

80% SMEA SpA

300

JULIETA 5

80% SMEA SpA

200

JULIETA 6

80% SMEA SpA

200

JULIETA 7

80% SMEA SpA

100

JULIETA 8

80% SMEA SpA

100

JULIETA 9

80% SMEA SpA

100

JULIETA 10 1/60

80% SMEA SpA

300

JULIETA 11

80% SMEA SpA

300

JULIETA 12

80% SMEA SpA

300

JULIETA 13, 1-60

80% SMEA SpA

298

JULIETA 14, 1-60

80% SMEA SpA

269

JULIETA 15, 1-40

80% SMEA SpA

200

JULIETA 16

80% SMEA SpA

200

JULIETA 17

80% SMEA SpA

200

JULIETA 18, 1-40

80% SMEA SpA

200

ARENA 1 1-6

80% SMEA SpA

40

ARENA 2 1-17

80% SMEA SpA

113

ZAPA 1 – 6

80% SMEA SpA

6

GSR 1%

JULIETA 1-4

80% SMEA SpA

4

Note. SMEA SpA is subsidiary company – 80% owned by Hot Chili Limited, 20% owned by CMP (Compañía Minera del Pacífico)

El Fuego Project

Licence ID

HCH % Held

HCH % Earning

Area (ha)

Exploration and Expenditure Commitment- Payments

Santiago 21 al 36

90% Frontera SpA

76

90% (HCH)-10% (Arnaldo del Campo) JV.6-year term.USD 300,000 already paid.USD 300,000 to be paid by September 7, 2023USD 6,600,000 final exercise payment to be paid by September 7, 2024.

Santiago 37 al 43

90% Frontera SpA

26

Santiago A, 1 al 26

90% Frontera SpA

236

Santiago B, 1 al 20

90% Frontera SpA

200

Santiago C, 1 al 30

90% Frontera SpA

300

Santiago D, 1 al 30

90% Frontera SpA

300

Santiago E, 1 al 30

90% Frontera SpA

300

Prima Uno

90% Frontera SpA

1

Prima Dos

90% Frontera SpA

2

Santiago 15 al 19

90% Frontera SpA

25

San Antonio 1 al 5

90% Frontera SpA

25

Santiago 1 AL 14 Y 20

90% Frontera SpA

75

Mercedes 1 al 3

90% Frontera SpA

50

Kreta 1 al 4

90% Frontera SpA

16

Mari 1 al 12

90% Frontera SpA

64

PORFIADA VII

90% Frontera SpA

300

PORFIADA VIII

90% Frontera SpA

300

PORFIADA IX

90% Frontera SpA

300

PORFIADA X

90% Frontera SpA

200

PORFIADA A

90% Frontera SpA

200

PORFIADA B

90% Frontera SpA

300

PORFIADA C

90% Frontera SpA

300

PORFIADA D

90% Frontera SpA

300

PORFIADA E

90% Frontera SpA

300

PORFIADA F

90% Frontera SpA

300

PORFIADA G

90% Frontera SpA

200

CORTADERA 1

100% Frontera SpA

200

CORTADERA 2

100% Frontera SpA

200

CORTADERA 3

100% Frontera SpA

200

CORTADERA 4

100% Frontera SpA

200

CORTADERA 5

100% Frontera SpA

200

CORTADERA 6

100% Frontera SpA

300

CORTADERA 7, 1-20

100% Frontera SpA

93

SAN ANTONIO 1

100% Frontera SpA

200

SAN ANTONIO 2

100% Frontera SpA

200

SAN ANTONIO 3

100% Frontera SpA

300

SAN ANTONIO 4

100% Frontera SpA

300

SAN ANTONIO 5

100% Frontera SpA

300

DORO 1

100% Frontera SpA

200

DORO 2

100% Frontera SpA

200

DORO 3

100% Frontera SpA

300

SANTIAGO Z 1/30

100% Frontera SpA

300

100% HCH Purchase Option AgreementUSD 200,000 already paid.USD 400,000 to be paid by January 22, 2024.NSR 1.5%

PORFIADA I

100% Frontera SpA

300

PORFIADA II

100% Frontera SpA

300

PORFIADA III

100% Frontera SpA

300

PORFIADA IV

100% Frontera SpA

300

PORFIADA V

100% Frontera SpA

200

PORFIADA VI

100% Frontera SpA

100

SAN JUAN SUR 1/5

90% Frontera SpA

10

90% (HCH) Option AgreementUSD 150,000 already paidUSD 4,000,000 by June 1, 2024.

SAN JUAN SUR 6/23

90% Frontera SpA

90

CHILIS 1

100% Frontera SpA

200

CHILIS 2

100% Frontera SpA

200

CHILIS 3

100% Frontera SpA

100

CHILIS 4

100% Frontera SpA

200

CHILIS 5

100% Frontera SpA

200

CHILIS 6

100% Frontera SpA

200

CHILIS 7

100% Frontera SpA

200

CHILIS 8

100% Frontera SpA

200

CHILIS 9

100% Frontera SpA

300

CHILIS 10

100% Frontera SpA

200

CHILIS 11

100% Frontera SpA

200

CHILIS 12

100% Frontera SpA

300

CHILIS 13

100% Frontera SpA

300

CHILIS 14

100% Frontera SpA

300

CHILIS 15

100% Frontera SpA

300

CHILIS 16

100% Frontera SpA

300

CHILIS 17

100% Frontera SpA

300

CHILIS 18

100% Frontera SpA

300

SOLAR 1

100% Frontera SpA

300

SOLAR 2

100% Frontera SpA

300

SOLAR 3

100% Frontera SpA

300

SOLAR 4

100% Frontera SpA

300

SOLAR 5

100% Frontera SpA

300

SOLAR 6

100% Frontera SpA

300

SOLAR 7

100% Frontera SpA

300

SOLAR 8

100% Frontera SpA

300

SOLAR 9

100% Frontera SpA

300

SOLAR 10

100% Frontera SpA

300

SOLEDAD 1

100% Frontera SpA

300

SOLEDAD 2

100% Frontera SpA

300

SOLEDAD 3

100% Frontera SpA

300

SOLEDAD 4

100% Frontera SpA

300

CF 1

100% Frontera SpA

300

CF 2

100% Frontera SpA

300

CF 3

100% Frontera SpA

300

CF 4

100% Frontera SpA

300

CF 5

100% Frontera SpA

300

CHAPULIN COLORADO 1/3

100% Frontera SpA

3

PEGGY SUE 1/10

100% Frontera SpA

100

DONA FELIPA

100% Frontera SpA

50

ELEANOR RIGBY 1/10

100% Frontera SpA

100

CF 6

100% Frontera SpA

200

CF 7

100% Frontera SpA

100

CF 8

100% Frontera SpA

200

CF 9

100% Frontera SpA

100

MARI 1

100% Frontera SpA

300

MARI 6

100% Frontera SpA

300

MARI 8

100% Frontera SpA

300

FALLA MAIPO 2 1/10

100% Frontera SpA

99

FALLA MAIPO 3 1/8

100% Frontera SpA

72

FALLA MAIPO 4 1/26

100% Frontera SpA

26

ARBOLEDA 7 1/2

Option AMSA

234

100% HCH Purchase Option AgreementUSD 1,500,000 to be paid by November 15, 2024

NAVARRO 1 41/60

Option AMSA

81

NAVARRO 2 21/37

Option AMSA

78

MONICA 21/40

Option AMSA

85

MONICA 41/52

Option AMSA

39

Note. Frontera SpA is a 100% owned subsidiary company of Hot Chili Limited

Qualifying Statements

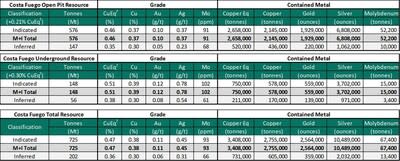

Costa Fuego Combined Mineral Resource (Effective Date 31st March 2022)

Costa Fuego Combined Mineral Resource (Effective Date 31st March 2022) (CNW Group/Hot Chili Limited)

1 Mineral Resources are reported on a 100% Basis – combining Mineral Resource estimates for the Cortadera, Productora and San Antonio deposits. All figures are rounded, reported to appropriate significant figures, and reported in accordance with the Joint Ore Reserves Committee Code (2012) and the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definition, as required by National Instrument 43-101.

2 The Productora deposit is 100% owned by Chilean incorporated company Sociedad Minera El Aguila SpA (SMEA). SMEA is a joint venture (JV) company – 80% owned by Sociedad Minera El Corazón Limitada (a 100% subsidiary of Hot Chili Limited), and 20% owned by CMP Productora (a 100% subsidiary of Compañía Minera del Pacífico S.A (CMP)).

3 The Cortadera deposit is controlled by a Chilean incorporated company Sociedad Minera La Frontera SpA (Frontera). Frontera is a subsidiary company – 100% owned by Sociedad Minera El Corazón Limitada, which is a 100% subsidiary of Hot Chili Limited.

4 The San Antonio deposit is controlled through Frontera (100% owned by Sociedad Minera El Corazón Limitada, which is a 100% subsidiary of Hot Chili Limited) and has an Option Agreement with a private party to earn a 90% interest.

5 The Mineral Resource estimates in the tables above form coherent bodies of mineralisation that are considered amenable to a combination of open pit and underground extraction methods based on the following parameters: Base Case Metal Prices: Copper US$ 3.00/lb, Gold US$ 1,700/oz, Molybdenum US$ 14/lb, and Silver US$20/oz.

6 Metallurgical recovery averages for each deposit consider Indicated + Inferred material and are weighted to combine sulphide flotation and oxide leaching performance. Process recoveries: Cortadera and San Antonio – Weighted recoveries of 82% Cu, 55% Au, 82% Mo and 37% Ag. CuEq(%) = Cu(%) + 0.56 x Au(g/t) + 0.00046 x Mo(ppm) + 0.0043 x Ag(g/t). Productora – Weighted recoveries of 84% Cu, 47% Au, 47% Mo and 0% Ag (not reported). CuEq(%) = Cu(%) + 0.46 x Au(g/t) + 0.00026 x Mo(ppm). Costa Fuego – Recoveries of 83% Cu, 53% Au, 69% Mo and 23% Ag. CuEq(%) = Cu(%) + 0.52 x Au(g/t) + 0.00039 x Mo(ppm) + 0.0027 x Ag(g/t).

7 Resource Copper Equivalent (CuEq) grades are calculated based on the formula: CuEq% = ((Cu% × Cu price 1% per tonne × Cu_recovery) + (Mo ppm × Mo price per g/t × Mo_recovery)+(Au ppm × Au price per g/t × Au_recovery)+ (Ag ppm × Ag price per g/t × Ag_recovery)) / (Cu price 1% per tonne × Cu recovery). The base case cut-off grade for mineral resources considered amenable to open pit extraction methods at the Cortadera, Productora and San Antonio deposits is 0.21% CuEq while the cut-off grade for mineral resources considered amenable to underground extraction methods at the Cortadera deposit is 0.3% CuEq.

8 Mineral resources are not mineral reserves and do not have demonstrated economic viability. These Mineral Resource estimates include Inferred Mineral Resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorised as Mineral Reserves. It is reasonably expected that the majority of Inferred mineral resources could be upgraded to Measured or Indicated Mineral Resources with continued exploration.

9 The effective date of the estimate of Mineral Resources is March 31st, 2022. Refer to ASX Announcement “Hot Chili Delivers Next Level of Growth” (“Resource Announcement”) for JORC Code Table 1 information related to the Costa Fuego Resource Estimate (MRE) by Competent Person Elizabeth Haren, constituting the MREs of Cortadera, Productora and San Antonio (which combine to form Costa Fuego). Hot Chili confirms it is not aware of any new information or data that materially affects the information included in the Resource Announcement and all material assumptions and technical parameters stated for the Mineral Resource Estimates in the Resource Announcement continue to apply and have not materially changed.

10 Hot Chili Limited is not aware of political, environmental or other risks that could materially affect the potential development of the Mineral Resources

Competent Person’s Statement- Exploration Results

Exploration information in this Report is based upon work compiled by Mr Christian Easterday, the Managing Director and a full-time employee of Hot Chili Limited whom is a Member of the Australasian Institute of Geoscientists (AIG). Mr Easterday has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a ‘Competent Person’ as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’ (JORC Code). Mr Easterday consents to the inclusion in the report of the matters based on their information in the form and context in which it appears.

Disclaimer

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this report.

This report is to be used by the recipient for informational purposes only and does not purport to be complete or contain all the information that may be material to the current or future business, operations, financial condition, or prospects of Hot Chili Limited (“Hot Chili” or the “Company”). Each recipient should perform its own independent investigation and analysis of Hot Chili, and the information contained in this report is not a substitute therefore. Hot Chili makes no representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this report or in any other written or oral communication transmitted to any recipient by any party. Except for liability that cannot be disclaimed by law, by accepting this Document, the recipient agrees that neither Hot Chili nor any of its officers, directors, employees, or representatives has any liability for any representations or warranties, express or implied, contained in, or for any omissions from, this report or any such other written or oral communication from any person.

Certain information contained herein is based on, or derived from, information provided by independent third-party sources. Hot Chili believes that such information is accurate and that the sources from which it has been obtained are reliable; however, Hot Chili has not independently verified such information and does not assume any responsibility for the accuracy or completeness of such information.

This report should not be considered as a recommendation from any person to purchase any securities. Each person for whom this report is made available should consult its own professional advisors in making its own independent investigations and assessment and, after making such independent investigations and assessments, as it deems necessary, in determining whether to proceed with any investment in the Company.

Technical Report

For readers to fully understand the information in this report, they should read the PEA Technical Report prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) (to be available on www.sedar.com or at www.hotchili.net.au within 45 days of June 30, 2023) in its entirety, including all qualifications, assumptions, limitations and exclusions that relate to the information set out in this report that qualifies the technical information contained in the PEA. The PEA is intended to be read as a whole, and sections should not be read or relied upon out of context. The technical information in this report is subject to the assumptions and qualifications contained in the PEA.

Qualified Persons – NI 43-101

The PEA was compiled by Wood Australia Pty Ltd with contributions from a team of independent Qualified Persons within the meaning of Canadian Securities Administrators’ National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43 -101”). The scientific and technical information contained in this report pertaining to Coast Fuego has been reviewed and verified by the following independent qualified persons within the meaning of NI 43-101:

Ms Elizabeth Haren (MAUSIMM (CP) & MAIG) of Haren Consulting – Mineral Resource Estimate

Mr Dean David (FAUSIMM (CP)) of Wood Pty Ltd – Metallurgy

Mr Piers Wendlandt (PE) of Wood Pty Ltd – Market Studies and Contracts, Economic Analysis

Farzard Kossari (PE) of Wood Pty Ltd – Cost Estimation

Mr Anton von Wielligh (FAUSIMM) of ABGM Consulting Pty Ltd – Mine Planning and Scheduling

The independent qualified persons have verified the information disclosed herein, including the sampling, preparation, security, and analytical procedures underlying such information.

Disclosure regarding mine planning and infrastructure has been reviewed and approved by Mr Grant King, FAUSIMM, Hot Chili’s Chief Operations Officer, and a Qualified Person within the meaning of NI43-101.

Competent Persons – JORC

The information in this report that relates to Mineral Resources for the Costa Fuego Project is based on information compiled by:

Ms Elizabeth Haren (MAUSIMM (CP) & MAIG) of Haren Consulting – Mineral Resource Estimate

Mr Dean David (FAUSIMM (CP)) of Wood Pty Ltd – Metallurgy

Mr Piers Wendlandt (PE) of Wood Pty Ltd – Market Studies and Contracts, and Economic Analysis

Mr Anton von Wielligh (FAUSIMM) of ABGM Consulting Pty Ltd – Mine Planning and Scheduling

Ms Haren, Mr David, Mr Wendlandt, Mr Kossari and Mr von Wielligh have sufficient experience, which is relevant to the style of mineralisation and types of deposits under consideration and to the activities undertaken, to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code of Reporting of Exploration Results, Mineral Resources and Ore Reserves’ and as Qualified Persons under NI43-101.

For further information on the Costa Fuego Project, refer to the technical report titled “NI 43-101 Resource Report for the Costa Fuego Copper Project Located in Atacama, Chile”, dated May 13, 2022 with an effective date of March 31, 2022, which is available for review on SEDAR (www.sedar.com) under Hot Chili’s issuer profile.

Cautionary Note for U.S. Investors Concerning Mineral Resources

National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) is a rule of the Canadian Securities Administrators which establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Technical disclosure contained in this report has been prepared in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum Classification System. These standards differ from the requirements of the U.S. Securities and Exchange Commission (“SEC”) and resource information contained in this press release may not be comparable to similar information disclosed by domestic United States companies subject to the SEC’s reporting and disclosure requirements.

All amounts in this report are in U.S. dollars unless otherwise noted.

Non IFRS Financial Performance Measures

“Total Cash Cost”, “All-in Sustaining Cost”, “All-in cost LOM”, “C1”, and “Free Cashflow” are not performance measures reported in accordance with International Financial Reporting Standards (“IFRS”). These performance measures are included because these statistics are key performance measures that management uses to monitor performance. Management uses these statistics to assess how the Costa Fuego Project compares against its peer projects and to assess the overall effectiveness and efficiency of the contemplated mining operations. These performance measures do not have a meaning within IFRS and, therefore, amounts presented may not be comparable to similar data presented by other mining companies. These performance measures should not be considered in isolation as a substitute for measures of performance in accordance with IFRS.

Scientific and Technical Information

The scientific and technical information contained in this document was reviewed and approved by Ms Kirsty Sheerin, a Member of the Australian Institute of Geoscientists, Hot Chili’s Resource Development Manager and a qualified person for the purposes of National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

Ms Sheerin has undertaken extensive data verification and is satisfied with the exploration, sampling, security, and QA/QC procedures employed by Hot Chili for Costa Fuego and that their results are sufficient to produce data suitable for the purposes described in the technical report titled “NI 43-101 Resource Report for the Costa Fuego Copper Project Located in Atacama, Chile”, dated May 13, 2022 with an effective date of March 31, 2022, as well as for public reporting purposes subsequent to the technical report.

Sampling, Analysis and Data Verification

A fixed cone splitter was used to create two nominal 12.5% samples (Sample “A” and “B”), along with the large bulk reject sample. The “A” sample is always taken from the same sampling chute, and comprises the primary sample submitted to the laboratory. The “B” samples were retained for use as the field duplicate sample. The coarse residues were collected into large plastic bags and were retained on the ground near the drillhole collar, generally in rows of 50 bags.

All RC drillhole sampling was executed at two metre intervals for Costa Fuego. Within logged mineralisation zones, the 2-metre sample (“A” sample) was submitted. Outside the main mineralised zones (as determined by the logging geologist), 4-metre composites were created from scoops of 2-metre sample residues over this interval. The composited 4-metre samples were analysed first and, if required, the individual and original 2-metre “A” samples comprising this 4-metre interval were sent for analysis. This ensured that no mineralisation was missed while minimising analytical costs. The same procedure was applied to RC drilling undertaken across Productora, however, drillhole sampling was executed at 1-metre intervals.

At Costa Fuego, the majority of diamond core has had systematic half-core sampled at 2-metre intervals. Half-core was chosen as the preferred sampling method to ensure a representative sample was submitted for analysis, while also retaining half-core for review of lithology and mineralisation, and for further test work as required.

Prior to the cutting and sample process, two additional samples are also taken for Costa Fuego being Density and Geotechnical samples.

Density samples are selected every 30 metres if the geological conditions allow it and are provided to the laboratory for testwork.

Geotechnical samples are taken for tests including triaxial (one sample per 250 m) and uniaxial tests (one sample per 50 m).

Once assigned a sample number, individual samples to be sent to ALS laboratories were sealed using a staple gun and accompanied by three identical sample tickets (one stapled to plastic bag to identify any tampering/breakage of seal prior to opening at the laboratory in preparation and another placed in the bag). Any broken staple seals on samples were to be notified by ALS to Hot Chili. No sealed bags were reported as being opened or broken by ALS.

For both RC and diamond samples, sample bags were placed inside larger plastic bags and delivered by a dedicated truck to the ALS analytical laboratory in Coquimbo (Chile) for sample preparation and routine analysis.

Following analysis at ALS, the RC and diamond drilling coarse rejects were returned to site and stored in sequence in plastic bags under shade cloth at Hot Chili’s nearby Productora core farm. The laboratory pulps were returned and stored at the Productora core farm where they are stored in organised, dry and safe storage containers.

Hot Chili has strict chain of custody security procedures for all samples sent to and from the analytical laboratories.

The ALS analytical laboratory in Coquimbo (Chile) completed all sample preparation and specific gravity test work, while ALS Santiago (Chile) completed all gold analysis, and ALS Lima (Peru) completed all other multielement analysis for the Cortadera assays used in the resource estimate. Hot Chili has implemented rigorous sample preparation and analytical procedures for both RC and diamond core samples, following consultation with ALS in Chile, to ensure that mineralised assays were reported with a high degree of confidence and a wide range of appropriate commodities were assessed.

Samples have been analysed by certified laboratories in Chile and Lima, Peru by standard analytical techniques including:

Copper, silver and molybdenum were analysed by 4-acid digestion (Hydrochloric-Nitric- Perchloric-Hydrofluoric) followed by evaluation using Inductively Coupled Plasma – Optical Emission Spectrometry (“ICP-OES”) or Atomic Absorption Spectrometry (“AAS”);

Copper results > 10,000 ppm were analysed by “ore grade” method Cu-AA62 (upper limit 40% Cu);

Samples within the oxide and transitional weathering domains (as determined by geologists’ logging) were analysed for “soluble copper” (upper limit 10% Cu) to detect the leachability of copper oxide minerals within these domains; and

Gold was analysed by 30 or 50 g lead-collection Fire Assay, followed by ICP-OES or AAS.

The verification of input data included the use of company QA/QC blanks and reference material, field and laboratory duplicates, umpire laboratory checks and independent sample and assay verification.

The Qualified Person has assessed the drillhole database validation work and QAQC undertaken by Hot Chili and was satisfied the input data could be relied upon for the estimation of Indicated and Inferred Classified Mineral Resources.

All laboratories used are independent of Hot Chili and the work is performed under a commercial arrangement.

Forward Looking Statements

This report contains certain statements that are “forward-looking information” within the meaning of Canadian securities legislation and Australian securities legislation (each, a “forward-looking statement”). Forward-looking statements reflect the Company’s current expectations, forecasts, and projections with respect to future events, many of which are beyond the Company’s control, and are based on certain assumptions. No assurance can be given that these expectations, forecasts, or projections will prove to be correct, and such forward-looking statements included in this report should not be unduly relied upon. Forward-looking information is by its nature prospective and requires the Company to make certain assumptions and is subject to inherent risks and uncertainties. All statements other than statements of historical fact are forward-looking statements. The use of any of the words “anticipate”, “believe”, “could”, “estimate”, “expect”, “may”, “plan”, “potential”, “project”, “should”, “will”, “would” and similar expressions are intended to identify forward-looking statements.

The forward-looking statements within this report are based on information currently available and what management believes are reasonable assumptions. Forward-looking statements speak only as of the date of this report. In addition, this report may contain forward-looking statements attributed to third-party industry sources, the accuracy of which has not been verified by the Company.