Key Takeaways

- Uranium Market Steadies: While the spot price declined in November, the overall price environment for the year has strengthened. Additionally, uranium miners gained for the month while remaining flat year-to-date.

- Nuclear Energy Continues to Gain Momentum: Global support continues to grow as more countries pledged to triple global nuclear capacity by 2050 at COP29.

- Implications After U.S. Election: The Trump presidency is likely to continue with a pro-nuclear stance, focusing on nuclear energy’s contributions to energy independence, national security and economic competitiveness.

- Energy Strategy Remains Critical: With Trump’s plan likely to prioritize domestic energy production, the stance on international uranium imports, mainly from Russia and China, will be a critical area to watch.

- Russian Ban Disrupts Supply Chain: Uranium supply faces pressure as Russia accounts for approximately 44% of global uranium enrichment capacity and 35% of U.S. enrichment imports. In sharp contrast, Russia only accounts for 5% of the global U3O8 supply.

Performance as of November 30, 2024

| Asset | 1 MO* | 3 MO* | YTD* | 1 YR | 3 YR | 5 YR |

| U3O8 Uranium Spot Price 1 | -3.61% | -2.39% | -15.38% | -4.53% | 18.79% | 24.24% |

| Uranium Mining Equities (Northshore Global Uranium Mining Index) 2 | 1.18% | 15.38% | 0.13% | 2.89% | 9.15% | 34.74% |

| Uranium Junior Mining Equities (Nasdaq Sprott Junior Uranium Miners Index TR) 3 | 0.00% | 19.37% | 0.60% | -0.05% | 1.74% | 34.47% |

| Broad Commodities (BCOM Index) 4 | 0.05% | 2.14% | -0.51% | -3.60% | 0.81% | 4.94% |

| U.S. Equities (S&P 500 TR Index) 5 | 5.87% | 7.15% | 28.07% | 33.89% | 11.44% | 15.76% |

*Performance for periods under one year is not annualized.

Sources: Bloomberg and Sprott Asset Management LP. Data as of 11/30/2024. You cannot invest directly in an index. Included for illustrative purposes only. Past performance is no guarantee of future results.

Year-End Overhang on Uranium Spot Market

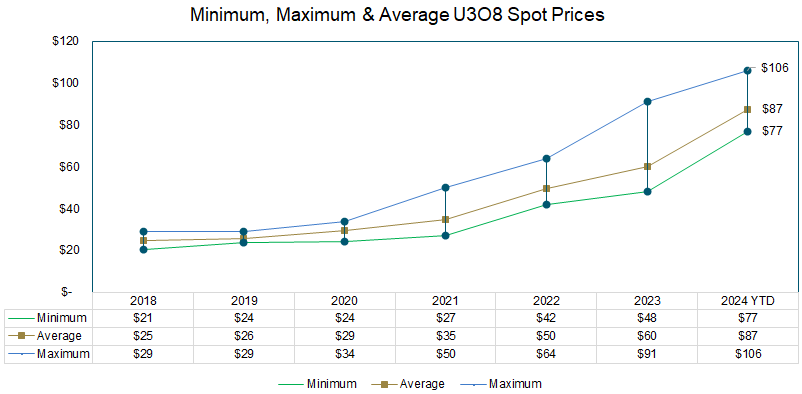

The uranium spot price retraced to support at $77.08 per pound at the end of November, which resulted in a 3.61% loss.1 The loss disguises a stronger price environment in the spot market for the year, with the minimum, average and maximum spot prices year-to-date at the highest levels compared to recent years (Figure 1). Given the growing sensitivity to geopolitical factors, we believe the uranium price will continue to behave in this staircase-like pattern over the intermediate term with short-term bouts of volatility. By contrast, uranium miners gained 1.18% in November and are flat year-to-date.

Uranium’s stairstep rally continues: spot prices soften, but term prices surge to 16-year highs.

Uranium miners have played catchup to the physical commodity and outperformed in 2024, a reversal of last year’s trend. Notably, uranium miners predominantly contract in the term market instead of the spot market and are therefore supported by term prices hitting 16-year highs. These term contracts also contain floors and ceilings, which continue to rise and are reported to be increasing with floor prices in the $70s and ceilings in the $130s (before escalation), indicating a midpoint of a triple-digit uranium price. Similarly, conversion and enrichment prices are at all-time highs, underscoring the strength of uranium’s current market dynamics.

The spot market is dealing with an overhang of supply as some traders look to clear their positions before the year’s end. Further pressuring the spot market are rampant rumors the Kazakh ANU physical uranium fund may be liquidating its 2+ million-pound inventory. While Russia’s retaliatory export ban on enriched uranium to the U.S. pushes utilities’ focus to the nuclear fuel cycle’s conversion and enrichment segments, we believe this attention will eventually cascade down to uranium oxide (U3O8). This year’s muted term contracting activity, at 100.7 million pounds of U3O8e, was heavily skewed by Chinese contracts with Kazatomprom and increases the likelihood of future contracting, as deferred purchases will eventually need to be addressed. Delaying these purchases risks depleting existing stockpiles, which is an unsustainable scenario from a risk management perspective.

Figure 1. Historical Physical Uranium Spot Prices

Source: UxC LLC. As of 11/30/2024.

Global Support for Nuclear Energy Continues to Grow

Meanwhile, global support for nuclear energy continues to gain momentum. At COP29, six additional countries pledged to triple global nuclear capacity by 2050, bringing the total to 31 nations committed to this ambitious goal.6 COP conferences and global forums for climate action highlight nuclear energy’s role in achieving net-zero emissions and meeting growing electricity demand.

On a regional level, positive news flows further bolster the case for nuclear power. Taiwan’s premier recently announced consideration of nuclear power to address energy needs tied to AI-driven electricity demand.7 Taiwan’s significance in this context is amplified by its position as a global leader in semiconductor manufacturing, in which advanced chips are critical for AI development, making a reliable and scalable electricity supply essential to maintain its competitive edge in this high-demand industry. Vietnam, too, is signaling a nuclear pivot, revising its national power development plan to incorporate nuclear options alongside renewables.8 The goal is to expand power generation capacity by 12-15% annually and support annual economic growth of 7%. As global electricity demand intensifies, we believe nuclear power and, by extension, uranium stand poised to be key enablers of this next growth phase, particularly in emerging markets.

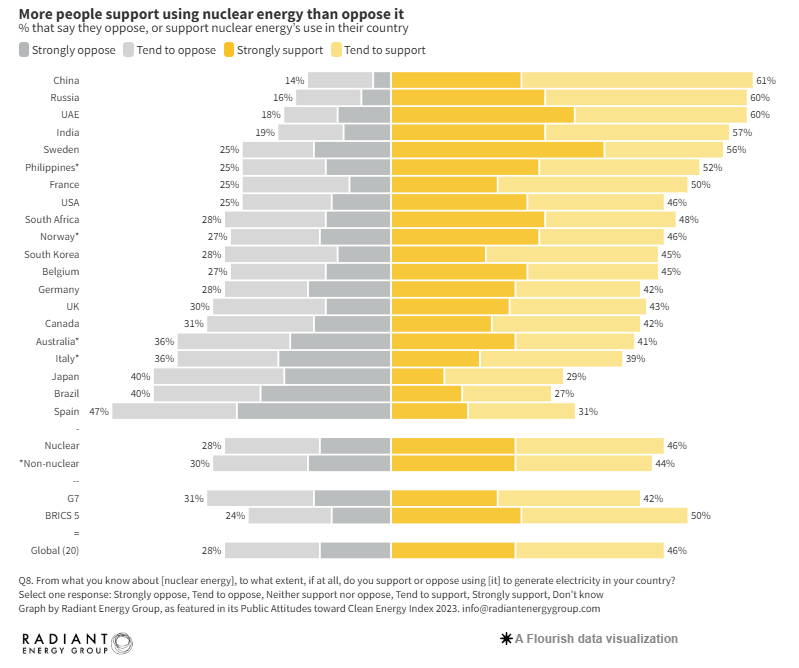

On an individual level, sentiment toward nuclear energy continues to improve, with a study finding that 1.5X more people support nuclear energy’s use than oppose it. Commissioned and analyzed by the Radiant Energy Group, the Public Attitudes Toward Clean Energy (PACE) index is the “world’s largest publicly released international study on what people think about nuclear energy.” Figure 2 shows that across the 20 countries surveyed, 28% of respondents oppose nuclear energy, while 46% support it, and 17 of the 20 countries had net support for nuclear energy. Further, the results found that nuclear energy was the second most preferred clean energy electricity source, after solar.

Figure 2. Public Attitudes Toward Nuclear Energy in 2023

Source: Radiant Energy Group https://www.radiantenergygroup.com/reports/public-attitudes-toward-clean-energy-2023-nuclear

U.S. Election and Potential Implications for the Nuclear Sector

The recent U.S. presidential election, which saw Donald Trump win the presidency along with Republican control of the Senate and the House of Representatives, will likely impact some elements of U.S. energy policy. It is important to note the Biden administration has been incredibly pro-nuclear for a Democratic government.

A second Trump administration is anticipated to maintain a pro-nuclear stance, though with motivations distinct from those of the Biden administration. While Democrats have emphasized nuclear energy as a cornerstone of their climate change strategy, Republicans are expected to champion it for its role in bolstering energy independence, enhancing national security, and driving economic competitiveness. Key industry initiatives that align with these priorities include expanding domestic uranium mining, simplifying nuclear permitting processes, and advancing innovative technologies like Small Modular Reactors (SMRs).

Bipartisan backing keeps U.S. nuclear strong, but policy shifts under Trump could reshape priorities.

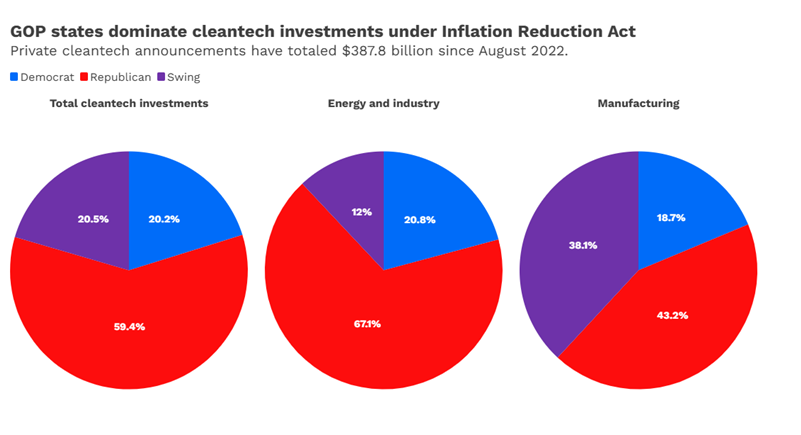

Significant legislation, such as the Bipartisan Infrastructure Law (BIL), the Inflation Reduction Act (IRA), and the Accelerating Deployment of Versatile, Advanced Nuclear for Clean Energy Act (ADVANCE Act), has provided substantial financial backing for nuclear projects, receiving broad bipartisan support. While some aspects of this legislation may undergo revision, we believe nuclear energy will continue to garner strong support. Notably, the fact that many IRA-driven projects are located in Republican-led states suggests that key components of these policies are likely to remain intact (Figure 3).

Trump’s energy strategy is expected to prioritize domestic energy production, including oil, gas and nuclear power, while potentially pulling back on climate-focused policies such as the Paris Agreement and offshore wind development. At the same time, the administration’s stance on international enriched uranium imports, mainly from Russia and China, will be a critical area to watch. Recent bipartisan legislation banning Russian enriched uranium imports, the Prohibiting Russian Uranium Imports Act (PRUIA), and calls for increased tariffs signal ongoing efforts to strengthen the U.S. domestic fuel cycle.

We believe the nuclear sector will continue to benefit from ongoing bipartisan support; however, potential shifts in policy priorities under a new Trump administration introduce uncertainty regarding the scale and direction of federal support. This uncertainty has contributed to the recent weakness in some clean energy sectors like renewables and electric vehicles.

Figure 3.

Source: https://www.ciphernews.com/articles/why-cleantech-is-booming-in-gop-led-states/. Clean Investment Monitor, Rhodium Group and MIT CEEPR. • Total announced investments range from Q3 2022 through Q2 2024. States are grouped as Republican, Democrat or Swing based on how they voted in the 2020 general election. Energy and Industry category includes the deployment of wind, solar, battery, geothermal, clean hydrogen, carbon management, sustainable aviation fuels and other electricity technologies. Manufacturing category refers to the production of these clean technologies.

Russia’s Retaliatory Restrictions on Enriched Uranium Exports

In November, Russia imposed restrictions on its enriched uranium exports to the U.S.9 The ban is seen as a “tit-for-tat” response to the U.S.’s Prohibiting Russian Uranium Imports Act, which came into effect in August. The PRUIA banned Russian-enriched uranium imports to the U.S. However, utilities may apply for waivers that authorize the importation of uranium to certain aggregate limits and up until the end of 2027 if the Secretary of Energy determines that there is no alternative viable source of uranium to sustain the continued operation of a U.S. nuclear reactor or if the importation of Russian-produced uranium is in the national interest.

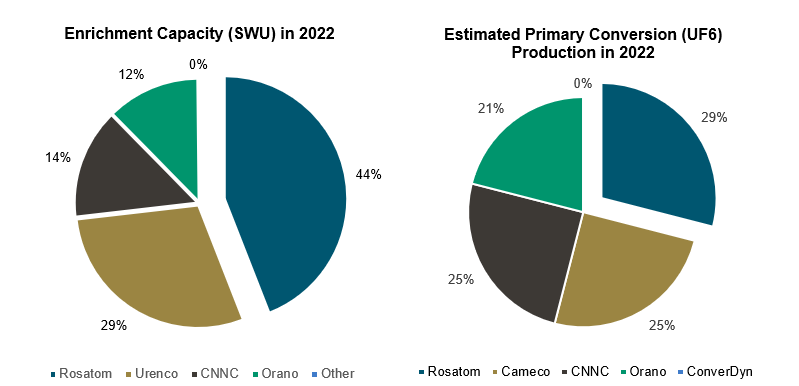

Russia’s retaliation has imposed a more immediate threat to the industry as uncertainty on the timing and scale of escalatory actions grows. At the same time, the West is working on expanding enrichment capacity. Russia’s restrictions have already created ripple effects, with uranium stocks climbing given concerns about supply disruptions. Russia accounts for approximately 44% of global uranium enrichment capacity and 35% of U.S. enrichment imports. In sharp contrast, Russia only accounts for 5% of the global U3O8 supply (Figure 4).

The timing of Russia’s restrictions poses a critical challenge. Western countries are still in the process of expanding their enrichment capacities, and these facilities will not be fully operational for several years. This leaves the nuclear fuel supply chain vulnerable to further disruptions, as Russia’s decision to withhold enriched uranium could potentially outpace Western efforts to establish an alternative supply.

This urgency has also accelerated shifts in enrichment practices. Western utilities are moving from underfeeding to overfeeding, requiring more raw uranium to compensate for reduced enrichment capacity. We believe this shift is expected to support uranium prices and increase demand in the coming years. Whether these measures can bridge the gap before Russia’s actions exert broader impacts remains a pivotal question for the nuclear energy sector.

Figure 4. Russia’s (Rosatom) Market Shares in Enrichment and Conversion

Source: WNA Nuclear Fuel Report 2023.

Kazakhstan and Niger Add to Supply Uncertainty

Kazatomprom, the world’s largest uranium supplier, has finalized a major agreement with China’s CNNC and China National Uranium Corporation for the sale of uranium concentrates. Combined with previous transactions involving these entities, the deal represents over 50% of Kazatomprom’s total book value, highlighting Kazakhstan’s deepening ties with Eastern markets. This agreement builds on a similar large-scale transaction with a Chinese utility in late 2023 and aligns with broader regional developments, including the construction of a massive trading hub and storage facility (with a capacity of approximately 60 million pounds) near the Kazakh-China border.

For Western utilities, this shift raises significant concerns. With an increasing portion of Kazatomprom’s supply being directed to China and Russia, Western buyers are under growing pressure to secure alternative uranium sources. These challenges are further exacerbated by Kazatomprom’s ongoing production difficulties, including weaker-than-expected output reported in Q3 2024. The combination of production constraints and shifting supply priorities underscores the urgent need for Western utilities to diversify their supply chains and mitigate potential risks to their energy security.

Niger, previously the seventh largest producer of uranium, has seen its production capabilities and stability unravel following a military coup in July 2023. The military junta has distanced itself from traditional Western allies like France and the U.S., forging closer ties with Russia and China. The political upheaval has severely impacted uranium operations in Niger. Most recently, on December 4, the French nuclear firm Orano confirmed the loss of operational control of SOMAÏR in Niger.10 This follows the previous announcement on October 23 that Niger’s growing financial difficulties forced it to suspend operations at the mine.11

As a result of the coup, Orano has been unable to export uranium, and a total of 1,150 tonnes of uranium concentrate from 2023 and 2024 stocks haven’t been exported, according to Orano.12 This is worth about $210 million. Additionally, Niger has revoked mining licenses for key projects, such as Orano’s Imouraren and Canada-based GoviEx’s Madaouela, signaling a shift in the country’s resource management strategy.

Despite these setbacks, some projects remain. Two uranium projects, the SOMINA Azelik project and Global Atomic’s Dasa project, are slated to commence production in the coming years. However, the nationalization of key assets and closer ties with Russia suggest that future uranium output may be increasingly directed away from Western markets.

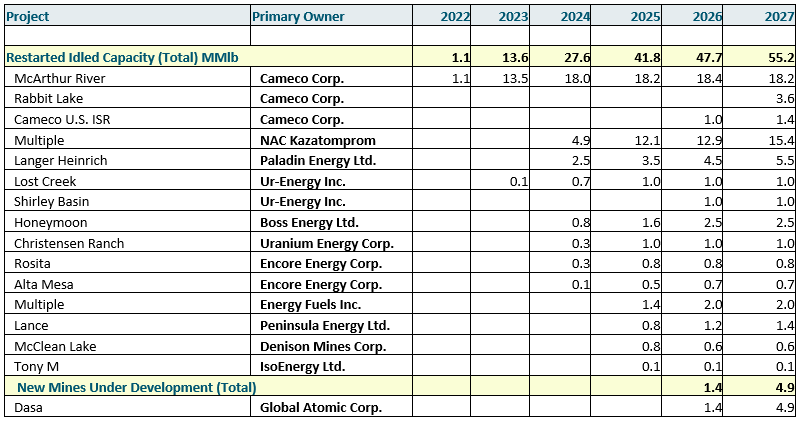

Junior Uranium Miners Helping to Address Supply Shortfalls

The shifting and uncertain dynamics of the global uranium supply underscore the urgent need to boost production through mine restarts and new developments. Junior uranium miners are playing a pivotal role in addressing this supply gap, with many resuming operations at previously idled mines to bring production back online (Figure 5). These projects are crucial for maintaining a stable uranium supply to Western utilities amid escalating geopolitical risks and dwindling access to traditional sources. By leveraging existing infrastructure, mine restarts can deliver uranium more quickly and cost-effectively than greenfield developments. Their success is essential to mitigating supply chain vulnerabilities and ensuring the long-term sustainability of the nuclear fuel cycle.

Junior uranium miners drive supply security, with quick restarts and new landmark projects like NexGen’s Rook I.

New uranium mines are poised to be vital in ensuring longer-term supply security. NexGen Energy Ltd. (NexGen) is a prominent junior uranium mining company developing the world’s largest single-source deposit of high-grade, low-cost uranium. Its renowned Rook 1 Project is situated in the Athabasca Basin in Saskatchewan, Canada. This location places it within one of the world’s top mining jurisdictions, known for its prolific uranium resources. The company boasts substantial uranium resources, totaling 337 million pounds. When NexGen had previously achieved provincial environmental approval, it marked the first uranium mine in Saskatchewan to reach this stage in over 20 years. The company projects a potential production output of up to 28.8 million pounds by 2030 and beyond.

NexGen’s recent progress with its flagship Rook I Project in Saskatchewan highlights the potential of junior uranium miners. The company recently reached a significant Rook I milestone, with the successful completion of the final federal technical review.13 This paves the way for the final steps of the approval process, including a Commission Hearing that could lead to a project approval decision.

NexGen has also taken significant strides toward commercializing its project by securing its first uranium sales contracts with leading U.S. utilities. These agreements cover the delivery of 5 million pounds of U3O8 over five years (2029–2033), with pricing mechanisms tied to market conditions. Notably, the contracts feature floor and ceiling prices of approximately $79 and $150 per pound, respectively, reflecting robust demand and favorable market conditions.14 It is important to highlight the contract ceiling price is notably higher than levels recently quoted by Cameco, which we believe reflects the strong market appetite for new sources of Western supply.

Figure 5. Uranium Supply Pipeline

Source: Mike Kozak, Uranium Analyst, Cantor Fitzgerald, September 2024. Company websites and UxC LLC. Assumes certain mines will be restarted that have yet to be announced. 2024-2027 is forecasted information from Cantor Fitzgerald’s report.

What to Make of Market Signals?

We believe the recent correction in the spot uranium price and the miners may represent an attractive entry point in the ongoing bull market. While the softness in the spot market over the past few months has been frustrating and confusing to watch, we believe it is sending a false signal given that the long-term fundamentals have only improved. Operational challenges appear to be getting worse, which will keep supply conditions tight, while the nuclear fuel supply chain remains highly susceptible to disruptions. Key producers remain steadfast in their supply discipline strategy and there appears to be a market standoff. Utilities are balking at the significant move in uranium prices over the past year, which will impact their future operating budgets, while producers are capitalizing on their long-awaited market leverage over utilities. As Cameco often repeats, utilities can “delay and defer,” but they will eventually be forced to buy.

Uranium supply deficits, tight market conditions and rising demand signal long-term strength.

A longstanding primary supply deficit and renewed interest in nuclear energy highlight the real challenges to bring the market back into balance. We believe this bull market has further room to run with no meaningful new supply on the horizon for three to five years. While last year’s multi-year record in long-term uranium contracting was celebrated, the overall numbers disguise a bifurcated market. Some utilities are well covered, while others have ignored the powerful market signals and failed to adapt their procurement strategies to the new market realities.

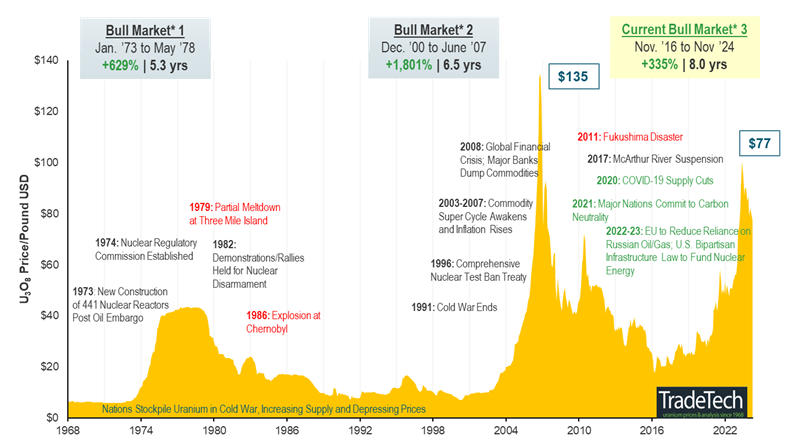

With global uranium mine production well short of the world’s uranium reactor requirements, the supply deficit building over the next decade, and near-term supply inhibited by long lead times and capital intensity, we believe that restarts and new mines in development are critical. The uranium price target as an incentive level for further restarts and greenfield development is a moving target, and we believe that we will need higher uranium prices to incentivize enough production to meet forecasted deficits. Over the long term, increased demand in the face of an uncertain uranium supply may continue supporting a sustained bull market (Figure 6).

Figure 6. Uranium Bull Market Continues (1968-2024)

Click here to enlarge this chart.

Note: A “bull market” refers to a condition of financial markets in which prices are generally rising. A “bear market” refers to a condition of financial markets in which prices are generally falling.

Source: TradeTech Data as of 11/30/2024. TradeTech is the leading independent provider of uranium prices and nuclear fuel market information. The uranium prices in this chart dating back to 1968 is sourced exclusively from TradeTech; visit https://www.uranium.info/.

Footnotes

| 1 | The U3O8 uranium spot price is measured by a proprietary composite of U3O8 spot prices from UxC, S&P Platts and Numerco. |

| 2 | The North Shore Global Uranium Mining Index (URNMX) was created by North Shore Indices, Inc. (the “Index Provider”). The Index Provider developed the methodology for determining the securities to be included in the Index and is responsible for the ongoing maintenance of the Index. The Index is calculated by Indxx, LLC, which is not affiliated with the North Shore Global Uranium Miners Fund (“Existing Fund”), ALPS Advisors, Inc. (the “Sub-Adviser”) or Sprott Asset Management LP (the “Adviser”). |

| 3 | The Nasdaq Sprott Junior Uranium Miners™ Index (NSURNJ™) was co-developed by Nasdaq® (the “Index Provider”) and Sprott Asset Management LP (the “Adviser”). The Index Provider and Adviser co-developed the methodology for determining the securities to be included in the Index and the Index Provider is responsible for the ongoing maintenance of the Index. |

| 4 | The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index that tracks prices of futures contracts on physical commodities, and is designed to minimize concentration in any one commodity or sector. It currently has 23 commodity futures in six sectors. |

| 5 | The S&P 500 or Standard & Poor’s 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. |

| 6 | Source: World Nuclear Association. Six More Countries Endorse the Declaration to Triple Nuclear Energy by 2050 at COP29. |

| 7 | Source: BNN Bloomberg. Taiwan Signals Openness to Nuclear Power Amid Surging AI Demand. |

| 8 | Source: Reuters. Vietnam to amend national power plan to include nuclear energy. |

| 9 | Source: World Nuclear News. Russia places ‘tit-for-tat’ ban on US uranium exports. |

| 10 | Source: Orano. Orano confirms the loss of operational control of SOMAÏR in Niger. |

| 11 | Source: Orano. Niger: growing financial difficulties will force SOMAÏR to suspend operations. |

| 12 | Source: BBC. Niger junta takes control of French uranium mine. |

| 13 | Source: Mining.com. NexGen Energy nears Rook I uranium project approval following final federal review. |

| 14 | Source: NexGen Energy Ltd. NexGen Announces First Uranium Sales Contracts for 5 Million Pounds with Major US Utilities. |