Proven and Probable: Joining us today is Chris McFadden, the president, CEO, and director of

NxGold Ltd. (NXN:TSX.V), where the focus is on high-grade gold in world-class districts.

Mr. McFadden, in our previous interview, we conducted a thorough, comprehensive interview regarding the value proposition of NxGold. For current and prospective shareholders, please read our in-depth exclusive

interview published in September. Mr. McFadden, for someone new to the story, who is NxGold and what is the thesis you’re attempting to prove?

Chris McFadden:

Chris McFadden: NxGold is a Vancouver-based gold explorer. Our main objective is to discover high grade large volumes of gold in first-class jurisdictions. So currently we have projects in Canada, projects in Nunavut and also in Western Australia in the Pilbara region.

Proven and Probable: I want to begin our discussion at the 10,000-foot level and get your perspective on a topic that has a number of speculators’ attention and that is the discussion of peak gold and how this may serve as a catalyst for junior mining companies and, in particular, NxGold.

Chris McFadden: I think that’s a great question because I think what we’re seeing in the industry at the moment and it’s something that’s been coming over the horizon for a few years now is that the majors have really cut back their exploration. They’re not spending the volumes of money that they used to spend on exploration for new gold deposits. So, over the last 5-10 years, actually there’s been a dearth of high-class, large-scale gold deposits and the majors are huge drop off in their production, in my view. You look at some of the production profiles for the big companies and gold production is going to potentially drop significantly in the years ahead because there hasn’t been that money spent on exploration.

So for companies like us that are exploring, that are spending money in the ground pursuing the next great discovery, I think there’s great potential there because if majors want to grow and stay in existence they need to look to juniors like us who are actually doing the work and opening up new teraines.

Proven and Probable: In our last interview you shared the next unanswered question for NxGold will be the implementation of a systematic approach to exploration and the anticipation of drill results. Since then NxGold issued three important press releases. Beginning with the 10th of September (

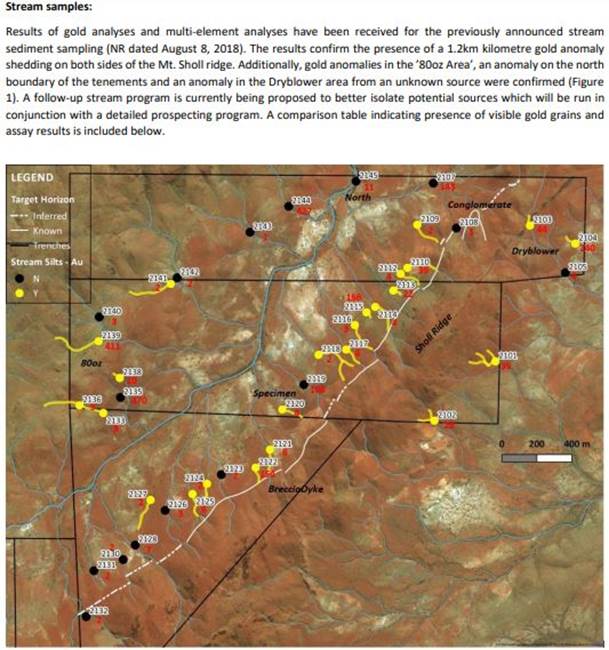

Press Release) the company received and compiled assay results, preliminary mapping, trenching and lab analysis from the stream sediment samples. Share the details with us.

Chris McFadden:

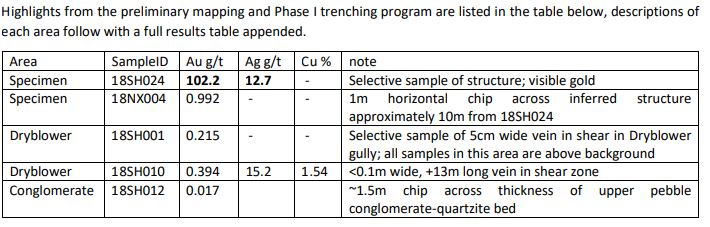

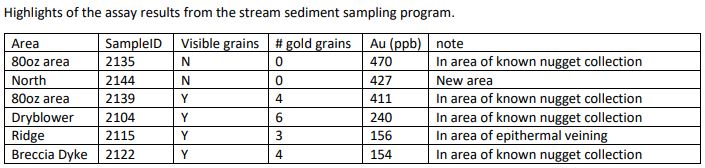

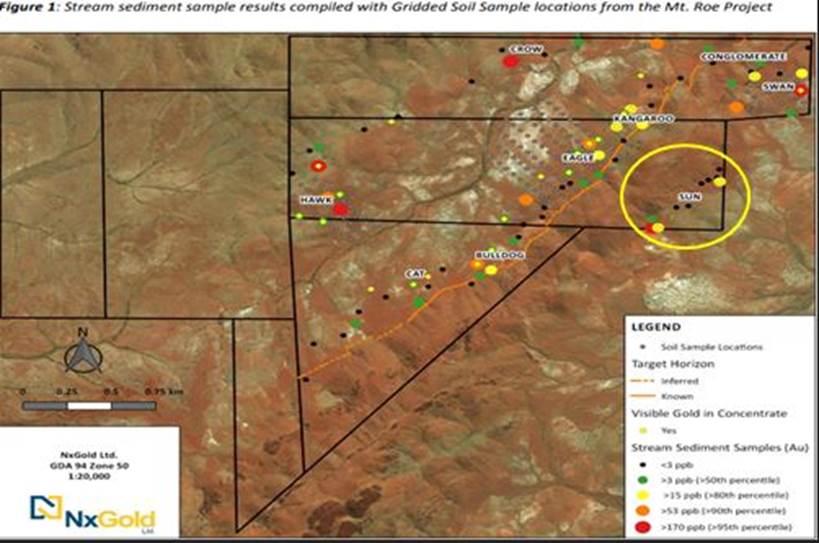

Chris McFadden: The company adopts a very systematic approach to its exploration. So we’re starting with very basic style exploration with stream sediment sampling, some trenching and grab samples. So that release from September was the output from the first phase of work at the Pilbara Project in Western Australia. One of the key highlights was in some of the trenches we opened up we had a visible gold in a specimen; after assay there’s 102 grams of gold in that specimen, also some silver, which was interesting as well.So that first pass work was a fairly random sediment sampling process. But those results were in that release. There were a number of other interesting results and in some of the sediment samples we took there was visible gold as well. So, obviously there’s some gold on the property and this highlights that for us.

Also it was very interesting because on the ridge we have on the southeastern side of the property there was consistent and numerous samples of an extended length of approximately 1.2 kilometers where there was visible gold in the stream sediment sampling. So that encouraged us. As I think I said in our original interview, each exploration dollar needs to be justified by success in the results that we obtain. So that encouraged us to proceed to continue our exploration work in the Pilbara Project.

Proven and Probable: On the 15th of October (

Press Release) NxGold discovered a new vein exposure on the east side of the property called the Sun Target Area. What can you share with us?

Chris McFadden:

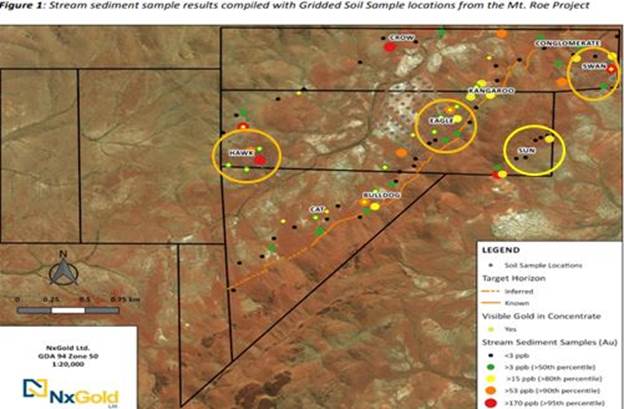

Chris McFadden: Well, the Sun area is right over on the eastern side and is on the other side of the ridge if you’d like. So, from that first release and subsequent release will say that a lot of the attention is on the western or northwestern side of the ridge of the property. Sun is over the other side in the area where we haven’t previously done much work. Where there also wasn’t much connectivity from prospectors. So it was a bit of a punt on our part to go to the other side of the ridge, but we’re looking to see what happened on the other side. We were very encouraged to find some bits of good results from that side. Also, to find that vein on that side because what we’ve seen on the northern, or nort western side of the ridge with our trenching, also with mapping, is that there are considerable numbers of veins. It’s really exciting that they’re continuing on the other side of the ridge.

Also on that side of the property we’re much closer to the Artemis Resources grab and we know that it has been finding some good veins and good nuggets on its property as well. So it seems that with that result that there is some extent potentially to the system in this area.

Proven and Probable: This week NxGold issued a third and equally important

press release regarding follow up work on stream soil and rock grab samples. What has the company excited here about the latest findings?

>p?

Chris McFadden:

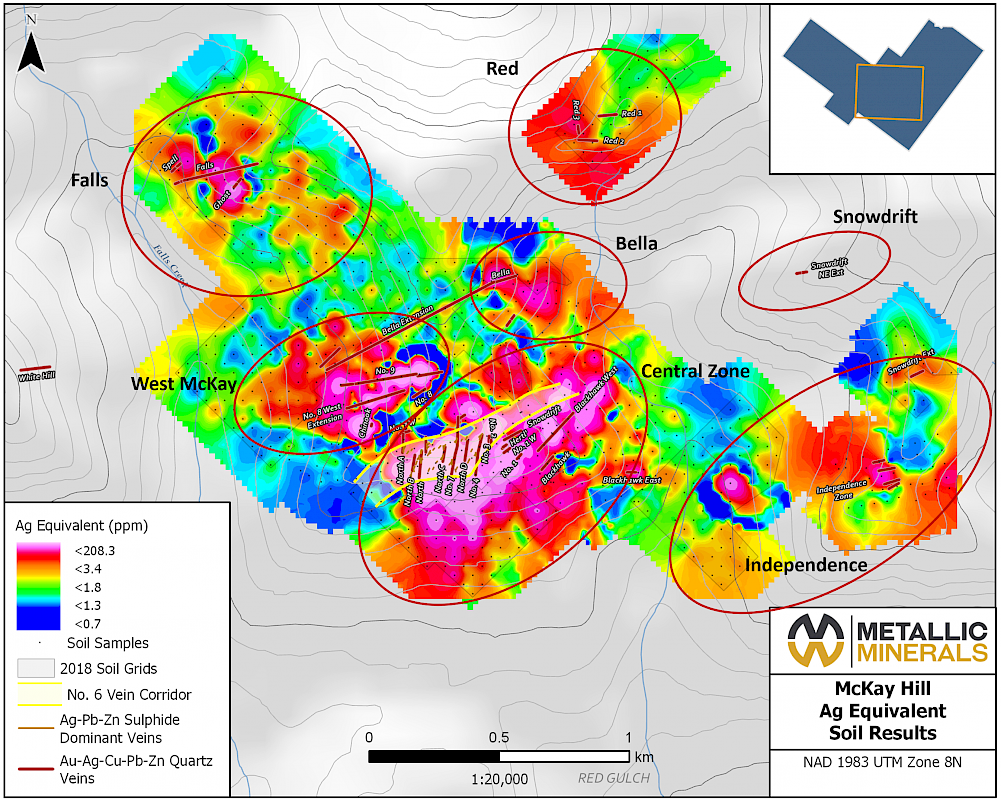

Chris McFadden: What’s interesting from this latest release is the consistency of the results we are obtaining and that’s it’s confirming our earlier work that there is a primary source of gold somewhere here on this property. So it’s highlighting the key prospects on the property that we’ve been working on in the Sun, in the areas we call Eagle in particular and Hawk. So the particular areas of the property, Eagle and Swan and Hawk, where prospectors have been finding nuggets for a considerable period of time. So the results tell us that there is a primary source of gold here and we’re narrowing our focus down onto those areas as a result of this work.

Proven and Probable: Switching gears, multilayered question, what is the next unanswered question for NxGold? When should we expect results? What determines success?

Chris McFadden: As we reported in our last press release, we have undertaken some very systematic grid soil sampling at the Pilbara Project in the Eagle, Swan, and Hawk areas. So it’ll be really interesting to see what comes out of that systematic soil sampling process. We have something like 140 samples in total on those areas that we’re expecting results from very soon, hopefully in the next week or two at the latest. That will give us a really strong indications of where the primary source of gold is we hope on this area of the property. So it’ll be really exciting for us and really interesting because we can then use that very systematic grid soil sampling and combine it with our stream sediment sampling and our trenching rock chip sampling and the magnetics that we’ve done over the area.

We’ll have multiple layers of geological information that we can then interrogate to ensure that we have a really strong picture of what’s going on under the ground here at the Pilbara Project in Western Australia. Another interesting or exciting element that’s coming over the horizon is we’re very hopeful that the remaining licenses in this area, which have been under application for the last 12 months since we acquired the property, we’re hoping that they will be granted to us again in a very short term. That will also allow us to extend our exploration efforts in the Pilbara Project area, particularly we’ve been working right up to the edge of the boundaries there at Hawk. We’ve done the systematic soil sampling pretty much right up to the edge of the granted area. This will allow us to move then into the application areas and effectively almost double the area that we can work at the Pilbara Project.

So in terms of what amounts to success from this project and the work that we’re doing and hopefully soon to announce, it’ll be the identification using the systematic multilayer approach to exploration that’ll allow us to narrow our focus on target it on areas for the next stages of work.

Proven and Probable: Last question here for you, what did I forget to ask?

Chris McFadden: Well, as usual Maurice, your questioning is very in depth, but one thing we haven’t spoken about is the Kuulu Project in Nunavut. That’s still a project of great interest to us, but we continue to be unable to obtain the surface license that we need. But we continue to work with the communities there and are working very hard to try and find a solution to that challenge that we have. But we’ve been very patient there because that has the potential to be a truly world-class exploration project.

Proven and Probable: Mr. McFadden, for someone listening that wants to get more information about NxGold please share the website address.

Chris McFadden: Certainly, it’s very simple. It’s

NxGold.ca.

Proven and Probable: As a reminder, NxGold trades on the TSX.V symbol NXN. For direct inquires please contact Travis McFearson at 604.816.2686. He may also be reached at

TMcFearson@NxGold.ca. NxGold is a sponsor of Proven and Probable and we’re proud shareholders for the virtues conveyed in today’s interview. Last but not least, please visit our website

www.provenandprobable.com where we interview the most respected names in the natural resource space. You may reach us at

contact@provenandprobable.com.

Chris McFadden of NxGold, thank you for joining us today on Proven and Probable.

Investor RelationsTravis McPherson

Tel: 604-816-2686

tmcpherson@nxgold.ca

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

1) Christopher McFadden: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: NxGold. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: NxGold.

2) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: NxGold. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: NxGold is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below.

3) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click herefor important disclosures about sponsor fees.

4) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

5) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.