VANCOUVER, BC, Dec. 7, 2023 /CNW/ – Uranium Royalty Corp. (NASDAQ: UROY) (TSX: URC) (“URC” or the “Company“) is pleased to report President and Chief Executive Officer, Scott Melbye, presented his views at the COP 28 Net-Zero Nuclear Pavilion in a panel discussion addressing the sustainability of the uranium sector. The panel was part of the United Nations Conference on Climate Change in Dubai, United Arab Emirates and hosted by the World Nuclear Association and Emirates Nuclear Energy Corporation. While at COP 28, URC demonstrated its support to the Net Zero Nuclear Industry Pledge, as one of 120 industry signatories.

The Net Zero Nuclear Industry Pledge, launched at COP 28 on December 5, 2023, commits to industry support for a tripling of global nuclear capacity by 2050. Twenty-two countries, including the United States, the United Kingdom, France, the United Arab Emirates, Japan, South Korea, and Canada, made the same declaration to tripling nuclear energy capacity by 2050 from a 2020 base in support of their net-zero commitments. The declaration recognizes the importance of extending lifetimes of existing reactors and supporting development and construction of nuclear reactors such as small modular and other advanced reactors for power generation.

Scott Melbye stated: “As a capital provider to miners and developers globally that can help fill this growing demand for uranium, we are excited about the government and industry commitment to support the tripling of nuclear energy by 2050. This growing demand for clean energy has reinforced nuclear power as an indispensable solution in global efforts to curb climate change.”

About Uranium Royalty Corp.

Uranium Royalty Corp. (URC) is the world’s only uranium-focused royalty and streaming company and the only pure-play uranium listed company on the NASDAQ. URC provides investors with uranium commodity price exposure through strategic acquisitions in uranium interests, including royalties, streams, debt and equity in uranium companies, as well as through trading of physical uranium.

Forward Looking Statements

Certain statements in this news release may constitute “forward looking information” and “forward looking statements”, as defined under applicable Canadian and U.S. securities laws (“forward looking statements”), including market expectations and the Company’s strategy and business plans, which ultimately remains the subject of the Company’s discretion. Forward looking statements include statements that address or discuss activities, events or developments that the Company expects or anticipates may occur in the future. When used in this news release, words such as “estimates”, “expects”, “plans”, “anticipates”, “will”, “believes”, “intends” “should”, “could”, “may” and other similar terminology are intended to identify such forward looking statements. Forward looking statements reflect the current expectations and beliefs of the Company’s management. These statements involve significant uncertainties, known and unknown risks, uncertainties and other factors and, therefore, actual results, performance or achievements of the Company and its industry may be materially different from those implied by such forward looking statements. They should not be read as a guarantee of future performance or results, and will not necessarily be an accurate indication of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from such forward looking statements, including, without limitation, risks inherent to royalty companies, any failures by counterparties to perform their respective obligations, market conditions, share price, uranium price volatility and risks related to the operators of the projects underlying the Company’s existing and proposed interests and those other risks described in filings with Canadian securities regulators and the U.S. Securities and Exchange Commission. These risks, as well as others, could cause actual results and events to vary significantly. Accordingly, readers should exercise caution in relying upon forward looking statements and the Company undertakes no obligation to publicly revise them to reflect subsequent events or circumstances, except as required by law.

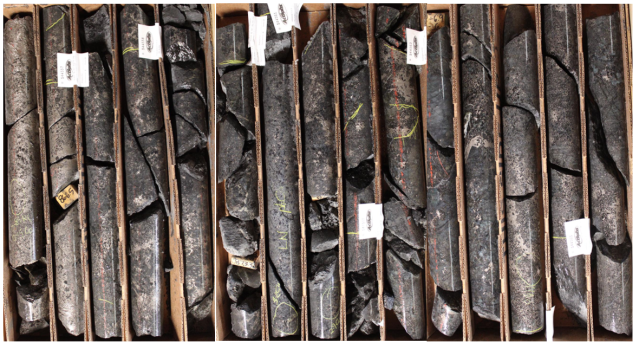

13.2 Metres of 3.8 g/t Au (including 5.6 m of 7.5 g/t Au)

Vancouver, British Columbia–(Newsfile Corp. – December 5, 2023) – Emperor Metals Inc. (CSE: AUOZ) (OTC Pink: EMAUF) (FSE: 9NH) (“Emperor“) is pleased to announce additional assay results from the summer 2023 drilling campaign at the Duquesne West Gold Project. A total of 14 diamond drillholes has been completed which represents 8,579metres.

Highlights

DQ23-09 intersects 13.2 metres (m) of 3.8 grams per tonne (g/t) gold (Au), including 5.6 m of 7.5 g/t Au in DQ23-09

Drilling confirms Phase 1 open-pit potential

DQ23-09; 5.6 m of 7.5 g/t Au exceeds the average grade of the deposit

DQ23-06 intersected 5.2 meters of 2.1 g/t Au (including 1.2 m of 6.1 g/t Au)

DQ23-06 expands mineralization down plunge over ½ kilometer from any known drillholes, implies additional inferred ounce potential

CEO John Florek commented:

“With the recent development of identifying the open pit potential on the property, holes DQ23-09 to 14 targeted the strategic vision to expand the Phase 1 open pit potential. DQ23-09 confirms that these high-grade lenses seen at depth are expressed at surface and could make very attractive stockpiles for delivery to nearby mills.

“Only an estimated 30% of the core from historical drilling was sampled at surface by previous operators who did not examine the additional lower-grade bulk tonnage material crucial to lowering the stripping ratio. As a result of recent work to locate and sample this material in the historical core library, more than 3,000 meters of additional sampling will be sent out for assays; sampling of historical core is ongoing.

“The intercept at DQ23-06 is very significant, since it expands the mineralization by an additional 0.55 km along strike and plunge, in an area of virtually no drilling. This area has potential to add significant ounces to this deposit.

“Our vision to develop a multimillion-ounce deposit with multiple mining scenarios on the property continues to progress. The proximity to multiple mills and infrastructure in a Tier 1 mining district makes this project highly valuable compared to any competitors.”

Summary of Drill Results:

DQ23-06 intersection (5.2 m of 2.1 g/t Au) was designed to extend mineralization +500 meters eastward along strike and down plunge of high-grade mineralization. It intersected mineralization predicted by the model, which will help to potentially increase the grade and add ounces laterally to the mineralized stopes model (Table 1, Image 1).

DQ23-09 intersection (13.2 Metres of 3.8 g/t Au (including 5.6 m of 7.5 g/t Au)) was designed to intersect near-surface mineralization to begin the strategic drilling of development of a potential area of development for a Phase 1 open pit (Image 2).

These partial results and the drill core visuals from our 2023 campaign suggest resource expansion within and outside the open pit concept.

The open pit concept in Image 1 shows an ultimate pit with a depth extent to 400 meters; the footprint is 1.8 km by 0.8 km. Initial exploration will strategically focus on the area of the phase 1 pit design. This will allow us to determine the potential economics as we progress through the phases having the necessary assay results for resource evaluation and eventually for economic evaluations. Currently, Emperor is sampling near-surface core from the historical core library that was not assayed by previous explorers. Up to 70% of this core has not been assayed. So far, over 3,000 meters have been sampled and will be sent to the laboratory for analysis (Image 3).

Partial assays for these reported drillhole results continue to increase confidence to consider an open pit potential to the Duquesne West deposit. Full laboratory results for drillholes DQ23-01, 03, 04, 05, and 09 have been received. DQ23-09 was rushed through the laboratory to advance our understanding related to near surface mineralization. Approximately 65% of the assays have been returned from the laboratory, Emperor is still awaiting additional assays results. A total of 14 diamond drillholes were completed this summer on this property.

Samples were sent to SGS Laboratories in Lakefield, ON.

Hole No.

From (m)

To (m)

Interval (m)

Au (g/t Au)

1DQ23-06

1032

1034

2

1.16

1034

1035

1

0.33

1035

1036

1

0.15

1036

1036.6

0.6

1.42

1036.6

1037.15

0.55

12.67

Wt. Avg.

5.15

2.06

Including:

1.15

6.80

1DQ23-09

26

27

1

5.51

27

28

1

6.24

28

29

1

1.37

29

29.8

0.8

19.52

29.8

30.6

0.8

0.04

30.6

31.6

1

13.46

31.6

32.6

1

0.01

32.6

33.6

1

0.005

33.6

34.6

1

0.2

34.6

35.6

1

5.45

35.6

36.1

0.5

0.01

36.1

37.1

1

0.05

37.1

38.25

1.15

0.05

38.25

39.2

0.95

1.51

Wt. Avg.

13.2

3.75

Including:

5.6

7.54

1Host Structures are interpreted to be steeply dipping and true widths are generally estimated to be 80 to 90%.

Image 1: Figure showing DQ23-06 intercept-expanding ounces +550 meters along strike and plunge of deposit. This intercept should continue building mineable stopes along this trend.

Image 2: Representation of mineralized and altered core from DQ23-09 (5.6 m of 7.5 g/t Au). Altered breccia zone in mafic volcanics; containing quartz veinlets, sericite, and ankerite.

The Quality Assurance and Quality Control (QAQC) was conducted by Technominex, a geological contractor hired by Emperor Metals, which adheres to CIM Best Practices Guidelines for exploration related activities conducted at its facility in Rouyn Noranda, Quebec. The QA/QC procedures are overseen by a Qualified Person on site.

Emperor Metals QA/QC protocols are maintained through the insertion of certified reference material (standards), blanks and lab duplicates within the sample stream totaling approximately one QA/QC sample per 7 samples. Drill core is cut in-half with a diamond saw, with one-half placed in sealed bags with appropriate tags and shipped to the SGS Lakefield laboratory and the other half retained on site in the original core box. A dispatch list consists of 88 or 176 samples along with their corresponding QA/QC samples for a single batch. This allows complete batches (88 samples) for fire assay. A file for sample tracking records tags used and weights of sample bags shipped to the SGS Lakefield. Shipment is done by Manitoulin Transport and coordination by Technominex staff in Rouyn-Noranda.

The third-party laboratory, SGS prep laboratory in Lakefield Ontario, processes the shipment of samples using standard sample preparation (code PRP91) and produces pulps from the specified samples. The pulps are then sent off to SGS Burnaby for analysis. Chain of custody is maintained from the drill to the submittal into the laboratory preparation facility all the way to analysis at the SGS Burnaby B.C. laboratory.

Analytical testing is performed by SGS laboratories in Burnaby, British Columbia. The entire sample is crushed to 75% passing 2mm, with a split of 500g pulverized to 85% passing 75 microns. Samples are then analyzed using Au – ore grade 50g Fire Assay, ICP-AES with reporting limits of 0.01 -100 part per million (ppm). High grade gold analysis based on the presence of visible gold or a Fire assay result exceeding 100 ppm, are analyzed by Au – metallic screening, 1kg screened to 106μm, 50g fire assay, gravimetric, AAS or ICP-AES of entire plus fraction and duplicate analysis of minus fraction. Reporting limit 0.01ppm.

About the Duquesne West Gold Project

The Duquesne West Gold Property is located 32 km northwest of the city of Rouyn-Noranda and 10 km east of the town of Duparquet. The property lies within the historic Duparquet gold mining camp in the southern portion of the Abitibi Greenstone Belt in the Superior Province.

Under an Option Agreement, Emperor agreed to acquire a one hundred percent (100%) interest in a mineral claim package comprising 38 claims covering approximately 1,389 ha, located in the Duparquet Township of Quebec (the “Duquesne West Property”) from Duparquet Assets Ltd., a 50% owned subsidiary of Globex Mining Enterprises Inc. For further information on the Duquesne West Property and Option Agreement, see Emperor’s press release dated October 12, 2022, available on SEDAR.

The Property hosts a historical inferred mineral resource estimate of 727,000 ounces of gold at a grade of 5.42 g/t Au.1,2 The mineral resource estimate predates modern CIM guidelines and a Qualified Person on behalf of Emperor has not reviewed or verified the mineral resource estimate, therefore it is considered historical in nature and is reported solely to provide an indication of the magnitude of mineralization that could be present on the property. The gold system remains open for resource identification and expansion.

Reinterpretation of the existing geological model was created using Artificial Intelligence (A.I) and Machine Learning. This model shows the opportunity for additional discovery of ounces by revealing gold trends unknown to previous workers and the potential to expand the resource along significant gold-endowed structural zones.

1 Watts, Griffis, and McOuat Consulting Geologists and Engineers, Oct 20, 2011, Technical Report and Mineral Resource Estimate Update for the Duquesne-Ottoman Property, Quebec, Canada for XMet Inc.

2 Power-Fardy and Breede, 2011. The Mineral Resource Estimate (MRE) constructed in 2011 is considered historical in nature as it was constructed prior to the most recent Canadian Institute of Mining and Metallurgy (CIM) standards (2014) and guidelines (2019) for mineral resources. In addition, the economic factors used to demonstrate reasonable prospects of eventual economic extraction for the MRE have changed since 2011. A qualified person has not done sufficient work to consider the MRE as a current MRE. Emperor is not treating the historical MRE as a current mineral resource. The reader is cautioned not to treat it, or any part of it, as a current mineral resource.

QP Disclosure

The technical content for the Duquesne West Project in this news release has been reviewed and approved by John Florek, M.Sc., P.Geol., a Qualified Person pursuant to CIM guidelines.

About Emperor Metals Inc.

Emperor Metals Inc. is an innovative Canadian mineral exploration company focused on developing high-quality gold properties situated in the Canadian Shield. For more information, please refer to SEDAR (www.sedarplus.ca), under the Company’s profile.

ON BEHALF OF THE BOARD OF DIRECTORS

s/ “John Florek”

John Florek, M.Sc., P.Geol President, CEO and Director Emperor Metals Inc.

CERTAIN STATEMENTS MADE AND INFORMATION CONTAINED HEREIN MAY CONSTITUTE “FORWARD-LOOKING INFORMATION” AND “FORWARD-LOOKING STATEMENTS” WITHIN THE MEANING OF APPLICABLE CANADIAN AND UNITED STATES SECURITIES LEGISLATION. THESE STATEMENTS AND INFORMATION ARE BASED ON FACTS CURRENTLY AVAILABLE TO THE COMPANY AND THERE IS NO ASSURANCE THAT ACTUAL RESULTS WILL MEET MANAGEMENT’S EXPECTATIONS. FORWARD-LOOKING STATEMENTS AND INFORMATION MAY BE IDENTIFIED BY SUCH TERMS AS “ANTICIPATES”, “BELIEVES”, “TARGETS”, “ESTIMATES”, “PLANS”, “EXPECTS”, “MAY”, “WILL”, “COULD” OR “WOULD”.

FORWARD-LOOKING STATEMENTS AND INFORMATION CONTAINED HEREIN ARE BASED ON CERTAIN FACTORS AND ASSUMPTIONS REGARDING, AMONG OTHER THINGS, THE ESTIMATION OF MINERAL RESOURCES AND RESERVES, THE REALIZATION OF RESOURCE AND RESERVE ESTIMATES, METAL PRICES, TAXATION, THE ESTIMATION, TIMING AND AMOUNT OF FUTURE EXPLORATION AND DEVELOPMENT, CAPITAL AND OPERATING COSTS, THE AVAILABILITY OF FINANCING, THE RECEIPT OF REGULATORY APPROVALS, ENVIRONMENTAL RISKS, TITLE DISPUTES AND OTHER MATTERS. WHILE THE COMPANY CONSIDERS ITS ASSUMPTIONS TO BE REASONABLE AS OF THE DATE HEREOF, FORWARD-LOOKING STATEMENTS AND INFORMATION ARE NOT GUARANTEES OF FUTURE PERFORMANCE AND READERS SHOULD NOT PLACE UNDUE IMPORTANCE ON SUCH STATEMENTS AS ACTUAL EVENTS AND RESULTS MAY DIFFER MATERIALLY FROM THOSE DESCRIBED HEREIN. THE COMPANY DOES NOT UNDERTAKE TO UPDATE ANY FORWARD-LOOKING STATEMENTS OR INFORMATION EXCEPT AS MAY BE REQUIRED BY APPLICABLE SECURITIES LAWS.

VANCOUVER, BC / ACCESSWIRE / December 5, 2023 /Stillwater Critical Minerals Corp. (TSXV:PGE)(OTCQB:PGEZF) (the “Company” or “Stillwater”) is pleased to provide an update on diamond drilling completed at the Company’s flagship Stillwater West Ni-PGE-Cu-Co + Au project in Montana in 2023, and other initiatives.

Figure 1 – Significant sulphide mineralization in hole CM2023-06 from approximately 865 to 888 feet (263.7 to 270.7 meters) depth as part of a broader mineralized interval from approximately 841 to 919 feet (256.4 to 280.1 meters) depth which tested a large and previously untested geophysical anomaly.More

Highlights – Stillwater West

The 2023 drill campaign focused on expansion of the NI 43-101-compliant resources, announced on January 25, 2023 (the “2023 Resource”), with particular focus on expanding recent high-grade discoveries at Chrome Mountain at the west end of the nine-kilometer-long resource area.

Six holes totaling 2,310 meters were completed within and outside of the current resource area, west and south of the current DR-Hybrid deposit, as part of a planned multi-phase program.

Multiple new mineralized zones were intercepted (see Figure 1 above and September 12, 2023, release).

Results include identification and expansion of the N series of sulphide-rich mineralized structures parallel to high-grade nickel sulphide mineralization first discovered by the Company in drill holes CM2021-05 and CM2020-04.

Drilling in 2023 intercepted the N2 and N3 mineralized zones in parallel to high-grade mineralization in CM2021-05, which is now known as N1. As reported May 3, 2022, N1 returned 13.2 meters grading 2.89% Recovered Nickel Equivalent1 (“NiEq”) (2.31% Ni, 1.51 g/t 4E, 0.35% Cu, and 0.115% Co), starting at 37.6 meters and is contained within 400.8 meters of continuous battery and precious metal mineralization.

N series structures and associated high-grade mineralization are now understood to be part of a series of north-south trending structures that crosscut the layered sequence and Platreef-style mineralization of the Stillwater Igneous Complex.

Drilling also confirmed nickel and copper sulphide mineralization in a large and previously untested geophysical anomaly which forms part of a string of untested anomalies extending over 12 kilometers along strike.

All core has now been submitted to the lab for assay with results expected over the coming weeks.

Mineralized zones were predicted by the updated exploration model, demonstrating the Company’s success in advancing the first ever detailed geologic model of the lower Stillwater Igneous Complex.

The 2023 drill campaign is the first campaign funded by the strategic investment made by Glencore PLC in June 2023, and the first to apply updated geological models which incorporate similar geology from South Africa’s Platreef district under the direction of Dr. Danie Grobler, who joined the team in May of 2022 as Vice-President of Exploration.

Drilling for 2024 is now being planned to continue expansion around known mineralization at the existing resource areas, at recent discoveries including the N series structures, and also more broadly across the 32-kilometer-long project.

Michael Rowley, Stillwater President and CEO, stated, “We continue to advance new sulphide-rich discoveries at our flagship Stillwater West project as we apply geologic models from South Africa’s giant polymetallic nickel sulphide mines to similar geology at our Stillwater West project. Recent work is identifying additional styles of mineralization, and we look forward to expanding further on these exciting developments as they advance. Overall, the Stillwater district remains underexplored – and therefore wide open for significant expansion of known mineralization – despite having produced critical and strategic minerals such as nickel, copper, palladium, platinum and chrome for over a century. We look forward to reporting assay results and providing updated analysis as we work with our partners at Glencore PLC and the US Geological Survey to advance primary domestic supply of nine of the commodities identified as critical by the US Government. Additional news is expected from our Kluane and Drayton-Black Lake projects, carbon sequestration studies, and other initiatives including continued work on government funding channels.”

Dr. Danie Grobler, Stillwater Vice-President of Exploration, said “Drilling in 2023 focused on intersecting several of the north-south trending high-grade and high-tenor nickel sulphide mineralized N-structures recognized during the 2022 field season. A 100% target intercept rate was achieved due to predictability and good correlation of the N-structure orientations within the 3D structural model developed by the team including results from a 2023 ground magnetic survey across Chrome Mountain. The first two holes intersected both of the sulphide-rich N1 and N2 structures at shallow depth. Drillhole CM2023-03 intersected an approximately 20-meter-thick zone of nickel sulphide mineralization at a depth of 223 meters from surface. All three of these holes also intersected a PGE+Ni+Cu mineralized pegmatoidal pyroxenite layer at its predicted position within the geological model. Drillhole CM2023-04 intersected disseminated, net-textured to semi-massive nickel sulphide mineralization from approximately 100 to 180 meters depth. In addition to the above, drillholes CM2023-05 and CM2023-06 both intersected zones of net-textured to semi-massive nickel and copper sulphide mineralization associated with a previously untested large shallow electromagnetic anomaly at Chrome Mountain. This anomaly forms part of a string of untested anomalies found near the footwall contact zone which runs more than 12 kilometers along strike from west of Chrome Mountain to Iron Mountain in the east. Visual inspection of the 2023 core shows many similarities to Stillwater’s CZ deposit, located approximately five kilometers to the east, which contains the highest nickel grades in the 2023 declared resource. This exciting discovery is expected to form a priority target for the upcoming 2024 campaign.”

Upcoming Events – Clean Energy and Precious Metals Virtual Investor Conference and AMEBC Core Shack

Stillwater Critical Minerals President & CEO, Michael Rowley, will present live on December 5th at 10am ET | 1pm PT with a Q&A to follow. Mr. Rowley is also available for one-on-one meetings following the event. For more information and to register click here.

The Company looks forward to displaying core from the 2023 drill season at the upcoming AMEBC Mineral Roundup event held in Vancouver, BC from January 22 to 25, 2024. For more information click here.

Government Funding

The Company continues to work with Cornell University under a Department of Energy grant, as announced February 14, 2023, and separately with the US Geological Survey on other programs at Stillwater West. In addition, the Company is actively pursuing other US government initiatives relating to developing domestic supply of critical minerals and will make further announcements as information becomes available.

Kluane PGE-Ni-Cu Project Update

Geological mapping, drone LiDAR and imagery acquisition, claim staking, and prospecting and rock sampling programs were completed in 2023 at the Company’s 100%-owned Kluane PGE-Ni-Cu project in Yukon, Canada, with field work funded in part by a Yukon Mineral Exploration Program grant. Follow-up work including completion of detailed geologic maps over priority areas and the advancement targets for later campaigns is on-going.

The Company has also begun to formally examine potential opportunities for carbon capture at the Kluane project with an initial focus on developing a procedure to identify and map rocks for their potential to sequester carbon based on existing data sources, remote sensing and imagery.

The Kluane project consists of a large 260 km2 land position containing the Spy, Ultra and Catalyst properties, all of which occur within the Kluane Mafic-Ultramafic Belt; a system of PGE-Ni-Cu deposits which are part of a sequence of mafic-ultramafic rocks that extends through the Yukon from northern British Columbia to central Alaska. Located near the Alaska Highway, the Kluane project properties are on trend with the Wellgreen Ni-Cu-PGE deposit.

Drayton – Black Lake

Heritage Mining (“Heritage”, CSE: HML) continues to meet the requirements of the earn-in agreement announced November 29, 2021, by the completion of exploration work on the Company’s district-scale Drayton-Black Lake gold project in Ontario, and the issuance of shares and cash to the Company. Results are pending from Heritage’s recent drill campaigns, and follow-up exploration programs are now being planned for 2024.

The Drayton-Black Lake Project site is located in northwestern Ontario in the Abrams‐Minnitaki Lake Archean greenstone belt approximately 25 kilometers east of the town of Sioux Lookout, Ontario. Access and infrastructure are excellent, featuring direct road access, and proximity to rail and power. Heritage Mining compiled the significant project database as part of advancing the substantial exploration potential of the project including demonstrated high-grade gold in drill results and bulk samples across more than 30 kilometers of underexplored strike in a geologic setting that is shared with Treasury Metals’ adjacent development-stage Goliath Gold Complex project. Work since the 1990s has proven more than 14 million ounces of gold in the broader district in this emerging and highly active gold belt lead by New Gold’s Rainy River mine and other deposits, and Heritage is effectively applying geological models and exploration methods that have been successful elsewhere in the district.

About Stillwater Critical Minerals Corp.

Stillwater Critical Minerals (TSX.V: PGE | OTCQB: PGEZF) is a mineral exploration company focused on its flagship Stillwater West Ni-PGE-Cu-Co + Au project in the iconic and famously productive Stillwater mining district in Montana, USA. With the addition of two renowned Bushveld and Platreef geologists to the team and a strategic investment by Glencore, the Company is well positioned to advance the next phase of large-scale critical mineral supply from this world-class American district, building on past production of nickel, copper, and chromium, and the on-going production of platinum group and other metals by neighboring Sibanye-Stillwater. An expanded NI 43-101 mineral resource estimate, released January 2023, delineates a compelling suite of critical minerals contained within five Platreef-style nickel and copper sulphide deposits at Stillwater West, which host a total of 1.6 billion pounds of nickel, copper and cobalt, and 3.8 million ounces of palladium, platinum, rhodium, and gold, and remains open for expansion along trend and at depth.

Stillwater also holds the high-grade Black Lake-Drayton Gold project adjacent to Treasury Metals’ development-stage Goliath Gold Complex in northwest Ontario, currently under an earn-in agreement with Heritage Mining, and the Kluane PGE-Ni-Cu-Co critical minerals project on trend with Nickel Creek Platinum‘s Wellgreen deposit in Canada‘s Yukon Territory.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Michael Rowley, President, CEO & Director – Stillwater Critical Minerals

1 – Recovered Nickel Equivalents (“NiEq”) are presented for comparative purposes using long-term metal prices (all USD): $8.00/lb nickel (Ni), $4.00/lb copper (Cu), $24.00/lb cobalt (Co), $1,000/oz platinum (Pt), $2,200/oz palladium (Pd), $1,800/oz gold (Au), and $10,000/oz rhodium (Rh). NiEq is determined as follows: NiEq% = [Ni% x recovery] + [Cu% x recovery x Cu price/ Ni price] + [Co% x recovery x Co price / Ni price] + [Pt g/t x recovery / 31.103 x Pt price / Ni price / 2,204 x 100] + [Pd g/t x recovery / 31.103 x Pd price / Ni price / 2,204 x 100] + [Au g/t x recovery / 31.103 x Au price / Ni price / 2,204 x 100]. In the above calculations: 31.103 = grams per troy ounce, 2,204 = lbs per metric tonne, and 100 and 0.01 convert assay results reported in % and g/t. The following recoveries have been assumed for purposes of the above equivalent calculations: 85% for Ni and 90% for all other listed metals, based on recoveries at similar nearby operations.

Quality Control and Quality Assurance

Mr. Mike Ostenson, P.Geo., is the qualified person for the purposes of National Instrument 43-101 for the Montana property, and he has reviewed and approved the technical disclosure contained in this news release.

Ms. Debbie James, P.Geo., is the qualified person for the purposes of National Instrument 43-101 for the Yukon and Ontario properties, and she has reviewed and approved the technical disclosure contained in this news release.

Forward-Looking Statements

This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this release, other than statements of historical facts including, without limitation, statements regarding potential mineralization, historic production, estimation of mineral resources, the realization of mineral resource estimates, interpretation of prior exploration and potential exploration results, the timing and success of exploration activities generally, the timing and results of future resource estimates, permitting time lines, metal prices and currency exchange rates, availability of capital, government regulation of exploration operations, environmental risks, reclamation, title, and future plans and objectives of the company are forward-looking statements that involve various risks and uncertainties. Although Stillwater Critical Minerals believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Forward-looking statements are based on a number of material factors and assumptions. Factors that could cause actual results to differ materially from those in forward-looking statements include failure to obtain necessary approvals, unsuccessful exploration results, changes in project parameters as plans continue to be refined, results of future resource estimates, future metal prices, availability of capital and financing on acceptable terms, general economic, market or business conditions, risks associated with regulatory changes, defects in title, availability of personnel, materials and equipment on a timely basis, accidents or equipment breakdowns, uninsured risks, delays in receiving government approvals, unanticipated environmental impacts on operations and costs to remedy same, and other exploration or other risks detailed herein and from time to time in the filings made by the companies with securities regulators. Readers are cautioned that mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral exploration and development of mines is an inherently risky business. Accordingly, the actual events may differ materially from those projected in the forward-looking statements. For more information on Stillwater Critical Minerals and the risks and challenges of their businesses, investors should review their annual filings that are available at www.sedar.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

NOT FOR DISTRIBUTION TO UNITED STATES NEWS WIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

Vancouver, British Columbia, Dec. 01, 2023 (GLOBE NEWSWIRE) — Terra Balcanica Resources Corp. (“Terra” or the “Company”) (CSE:TERA) announces the intent to complete a non-brokered, private placement (“Private Placement”) for gross proceeds of up to $150,000 through the issuance of up to 3,750,000 common shares (“Common Shares”) at a purchase price of $0.04 per share.

The Common Shares will be offered by way of prospectus exemptions in Canada and the Common Shares sold in the Private Placement will be subject to a hold period of four months plus one day. The Closing Date is expected to occur on or about December 11th, 2023, subject to regulatory approvals, including the approval by the CSE and certain other customary conditions including, but not limited to, execution of subscription agreements between the Company and the subscribers. The Private Placement will be utilized for opportunities in the critical battery metal exploration space in the Western Balkans.

About the Company Terra Balcanica is a polymetallic exploration company targeting large-scale mineral systems in the Balkans of southeastern Europe. The Company has 90% interest in the Viogor-Zanik Project in eastern Bosnia and Herzegovina, 100% of the Kaludra and Ceovishte mineral exploration licences in Serbia. The Company emphasizes responsible engagement with local communities and stakeholders. It is committed to proactively implementing Good International Industry Practice (GIIP) and sustainable health, safety and environmental management.

ON BEHALF OF THE BOARD OF DIRECTORS

Terra Balcanica Resources Corp. Aleksandar (Alex) Mišković President and CEO

This news release contains certain forward-looking information and forward-looking statements within the meaning of applicable securities legislation (collectively “forward-looking statements”). The use of any of the words “will”, “intends” and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. Such forward-looking statements should not be unduly relied upon. Actual results achieved may vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. The Company believes the expectations reflected in those forward-looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct. The Company does not undertake to update these forward-looking statements, except as required by law.

Vancouver, British Columbia–(Newsfile Corp. – December 1, 2023) – Emperor Metals Inc. (CSE: AUOZ) (OTCQB: EMAUF) (FSE: 9NH) (“Emperor“) is pleased to announce that its common shares are now listed for trading in the United States on the OTCQB Venture Market under the symbol “EMAUF”. The Company has additionally secured Depository Trust Company (“DTC”) eligibility for its common shares traded in the United States.

For this listing, the Company profile can be viewed at the OTC Market website at https://www.otcmarkets.com/stock/EMAUF/quote where North American and international investors can find Real-Time level 2 quotes (denominated in US dollars) along with current market information and Company news. Emperor’s common shares will continue to trade in Canada on the Canadian Stock Exchange (the “CSE”) under the symbol “AUOZ” and primary reporting for public disclosure will continue to be found under the company profile at www.sedarplus.ca.

Emperor CEO, John Florek commented: “This initiative will enable shareholders to benefit from the growing market interest in gold and the Duquesne West Gold Project from US-based retail and institutional investors as we continue our Advanced AI-Assisted exploration strategy to define a modern Mineral Resource Estimate (MRE). Our new OTCQB listing with DTC eligibility now provides exemptions from U.S state securities laws or “Blue Sky” exemptions which will enable US-based investment advisors to research and recommend investment in Emperor. It will also enable US-based investors to execute orders with greater ease on many popular trading platforms such as Fidelity, TD Ameritrade, Charles Schwab, TradeStation, FirstTrade, Interactive Brokers and E-Trade where access to Emperor’s common shares listed on the CSE may have been limited previously.”

About the OTCQB

The OTCQB® Venture Market is recognized by the Securities and Exchange Commission as an established public market providing public information for analysis. An OTCQB listing offers early-stage and developing U.S. and international companies the benefits of being publicly traded in the U.S. with lower cost and complexity than a U.S. exchange listing. Streamlined market standards enable Canadian companies to provide a strong baseline of transparency to inform and engage U.S. investors. To be eligible, Canadian companies must be current in their SEDAR reporting and undergo an annual verification and management certification process. As a verified market with efficient access for U.S. investors, OTCQB helps companies build shareholder value with the goal of enhancing liquidity and achieving a fair valuation.

OTC Markets Group Inc. (OTCQX: OTCM), located in New York, N.Y., operates the world’s largest electronic inter-dealer quotation system for broker dealers to trade US-based and global securities. It operates the OTCQX® Best Market, the OTCQB® Venture Market, and the Pink® Open Market for over 11,000 U.S. and global securities. Through OTC Link® ATS, it connects a diverse network of broker-dealers that provide liquidity and execution services, enabling investors to easily trade through the broker of their choice and empowering companies to improve the quality of information available for investors. To learn more about how OTC Markets creates better informed and more efficient markets, visit www.otcmarkets.com.

About the Depository Trust Company

The Depository Trust Company is a subsidiary of The Depository Trust & Clearing Corporation and manages the electronic clearing and settlement of publicly traded companies. Securities that are eligible to be electronically cleared and settled through the DTC are considered “DTC eligible”. This electronic method of clearing securities speeds up the receipt of stock and cash, and thus accelerates the settlement process for investors trading the Company’s shares on the OTCQB with reduced costs for U.S. investors and brokers, enabling the Company’s common shares to be traded through a much wider selection of firms through an electronic method of clearing securities.

About the Duquesne West Gold Project

Emperor’s flagship Duquesne West Gold Property is located 32 km northwest of the city of Rouyn-Noranda and 10 km east of the town of Duparquet. The property lies within the historic Duparquet gold mining camp in the southern portion of the Abitibi Greenstone Belt in the Superior Province.

Under an Option Agreement, Emperor agreed to acquire a one hundred percent (100%) interest in a mineral claim package comprising 38 claims covering approximately 1,389 ha, located in the Duparquet Township of Quebec (the “Duquesne West Property”) from Duparquet Assets Ltd., a 50% owned subsidiary of Globex Mining Enterprises Inc. (GMX-TSX). For further information on the Duquesne West Property and Option Agreement, see Emperor’s press release dated October 12, 2022, available on SEDAR.

The Property hosts a historical inferred mineral resource estimate of 727,000 ounces of gold at a grade of 5.42 g/t Au.1,2 The mineral resource estimate predates modern CIM guidelines and a Qualified Person has not reviewed or verified the mineral resource estimate on behalf of Emperor, therefore it is considered historical in nature and is reported solely to provide an indication of the magnitude of mineralization that could be present on the property. The gold system remains open for resource identification and expansion.

Reinterpretation of the existing geological model was completed using Artificial Intelligence (AI) and Machine Learning. This model shows the opportunity for additional discovery of ounces by revealing gold trends unknown to previous workers and the potential to expand the resource along significant gold-endowed structural zones.

1 Watts, Griffis, and McOuat Consulting Geologists and Engineers, Oct 20, 2011, Technical Report and Mineral Resource Estimate Update for the Duquesne-Ottoman Property, Quebec, Canada for XMet Inc.

2 Power-Fardy and Breede, 2011. The Mineral Resource Estimate (MRE) constructed in 2011 is considered historical in nature as it was constructed prior to the most recent Canadian Institute of Mining and Metallurgy (CIM) standards (2014) and guidelines (2019) for mineral resources. In addition, the economic factors used to demonstrate reasonable prospects of eventual economic extraction for the MRE have changed since 2011. A qualified person has not done sufficient work to consider the MRE as a current MRE. Emperor is not treating the historical MRE as a current mineral resource. The reader is cautioned not to treat it, or any part of it, as a current mineral resource.

QP Disclosure

The technical content for the Duquesne West Project in this news release has been reviewed and approved by John Florek, M.Sc., P.Geol., a Qualified Person pursuant to CIM guidelines.

About Emperor Metals Inc.

Emperor Metals Inc. is an innovative Canadian mineral exploration company focused on developing high-quality gold properties situated in the Canadian Shield. For more information, please refer to SEDAR (www.sedarplus.com), under the Company’s profile.

ON BEHALF OF THE BOARD OF DIRECTORS

s/ “John Florek”

John Florek, M.Sc., P.Geol President, CEO and Director Emperor Metals Inc.

CERTAIN STATEMENTS MADE AND INFORMATION CONTAINED HEREIN MAY CONSTITUTE “FORWARD-LOOKING INFORMATION” AND “FORWARD-LOOKING STATEMENTS” WITHIN THE MEANING OF APPLICABLE CANADIAN AND UNITED STATES SECURITIES LEGISLATION. THESE STATEMENTS AND INFORMATION ARE BASED ON FACTS CURRENTLY AVAILABLE TO THE COMPANY AND THERE IS NO ASSURANCE THAT ACTUAL RESULTS WILL MEET MANAGEMENT’S EXPECTATIONS. FORWARD-LOOKING STATEMENTS AND INFORMATION MAY BE IDENTIFIED BY SUCH TERMS AS “ANTICIPATES”, “BELIEVES”, “TARGETS”, “ESTIMATES”, “PLANS”, “EXPECTS”, “MAY”, “WILL”, “COULD” OR “WOULD”.

FORWARD-LOOKING STATEMENTS AND INFORMATION CONTAINED HEREIN ARE BASED ON CERTAIN FACTORS AND ASSUMPTIONS REGARDING, AMONG OTHER THINGS, THE ESTIMATION OF MINERAL RESOURCES AND RESERVES, THE REALIZATION OF RESOURCE AND RESERVE ESTIMATES, METAL PRICES, TAXATION, THE ESTIMATION, TIMING AND AMOUNT OF FUTURE EXPLORATION AND DEVELOPMENT, CAPITAL AND OPERATING COSTS, THE AVAILABILITY OF FINANCING, THE RECEIPT OF REGULATORY APPROVALS, ENVIRONMENTAL RISKS, TITLE DISPUTES AND OTHER MATTERS. WHILE THE COMPANY CONSIDERS ITS ASSUMPTIONS TO BE REASONABLE AS OF THE DATE HEREOF, FORWARD-LOOKING STATEMENTS AND INFORMATION ARE NOT GUARANTEES OF FUTURE PERFORMANCE AND READERS SHOULD NOT PLACE UNDUE IMPORTANCE ON SUCH STATEMENTS AS ACTUAL EVENTS AND RESULTS MAY DIFFER MATERIALLY FROM THOSE DESCRIBED HEREIN. THE COMPANY DOES NOT UNDERTAKE TO UPDATE ANY FORWARD-LOOKING STATEMENTS OR INFORMATION EXCEPT AS MAY BE REQUIRED BY APPLICABLE SECURITIES LAWS.

Gold’s (GC=F) upward trend above $2,000 per ounce is prompting calls for a rally to a new all-time high.

Futures were 0.5% higher on Monday, just north of $2,013 per ounce. Prices are at six-month highs and up two weeks in a row.

That has boosted hopes that the precious metal could top its all-time high of $2,074.88 reached in August 2020.

“Gold [is] showing additional proof that a rally back to new all-time Highs is underway,” Mark Newton, head of technical strategy at Fundstrat, wrote in a recent note to clients.

Most traders consider $2,050 as the breakout level for momentum to send prices to that level.

“My technical target for gold is $2500/oz, and it looks appealing to be long precious metals given falling real rates, rising cycles and ongoing geopolitical conflict,” said Newton.

Gold, seen as a safe-haven asset, has rallied in recent weeks. (Getty Images) (OsakaWayne Studios via Getty Images)

Michele Schneider, partner and director of trading education and research at MarketGauge.com, told Yahoo Finance last month that she thought gold could hit $3,000, noting that gold has held up “in the face of a stable dollar and higher rates.”

Gold is seen as a safe-haven asset during times of uncertainty. Its rise in price comes amid escalating geopolitical tensions in the Middle East following the surprise attack by Hamas on Israel last month.

Anticipation of an end to the Fed’s tightening cycle is also attracting buyers. The market’s speculation that the Federal Reserve is done raising interest rates has sent longer-term Treasury rates lower.

Central banks have been among the biggest gold buyers in the last couple of years, with a record-breaking first half of 2023.

Global official gold reserves are 120% higher quarter over quarter and the second highest third quarter total following the same period last year, according to industry group World Gold Council.

China is the largest buyer, followed by Poland and Singapore.

VANCOUVER, BC, Nov. 28, 2023 /CNW/ – Uranium Royalty Corp. (NASDAQ: UROY) (TSX: URC) (“URC” or the “Company“) is pleased to announce the publication of its inaugural 2023 Sustainability Report. This report presents the Company’s approach and performance on sustainability initiatives and outlines sustainability strategy and goals for the future.

FY23 Sustainability Report Highlights

Bolstered the Company’s strong due diligence process through strengthened focus on sustainability-related risks of operators, reviewing 100% of deals with the Company’s enhanced sustainability due diligence approach;

Strengthened the Company’s corporate risk management function;

Approved Sustainability Policy, Anti-Corruption Policy and Corporate Disclosure Policy to reinforce the Company’s commitment to sustainability and strong corporate governance;

Achieved executive-management diversity of 33% female and 33% ethnically-diverse representation; and

Donated approximately US$48,000 to local community programs.

Scott Melbye, the Company’s Chief Executive Officer, stated: “I am proud to present our inaugural 2023 Sustainability Report for Uranium Royalty Corp., the first and only pure play uranium royalty company. As a relatively young company, we are proud of our growing portfolio of 20 interests on 18 development, advanced, permitted and producing uranium projects in key uranium jurisdictions. As the first company to apply the successful royalty and streaming business model exclusively to the uranium sector, we leverage our first-mover advantage through providing needed capital to producing, developing, and next generation uranium mining companies. This supports our mission to fuel a cleaner tomorrow through carbon-free nuclear energy.”

He continued, “As a royalty company, we play an important role in promoting sustainability and innovation in mining. We carefully screen and seek to select operators who share our principles of responsible environmental stewardship and strong community support, and we strive to develop long-term relationships based on mutual commitment to those principles.”

About Uranium Royalty Corp.

Uranium Royalty Corp. (URC) is the world’s only uranium-focused royalty and streaming company and the only pure-play uranium listed company on the NASDAQ. URC provides investors with uranium commodity price exposure through strategic acquisitions in uranium interests, including royalties, streams, debt and equity in uranium companies, as well as through trading of physical uranium.

Forward Looking Statements

Certain statements in this news release may constitute “forward looking information” and “forward looking statements”, as defined under applicable Canadian and U.S. securities laws (“forward looking statements”), including market expectations and the Company’s strategy and business plans, which ultimately remains the subject of the Company’s discretion. Forward looking statements include statements that address or discuss activities, events or developments that the Company expects or anticipates may occur in the future. When used in this news release, words such as “estimates”, “expects”, “plans”, “anticipates”, “will”, “believes”, “intends” “should”, “could”, “may” and other similar terminology are intended to identify such forward looking statements. Forward looking statements reflect the current expectations and beliefs of the Company’s management. These statements involve significant uncertainties, known and unknown risks, uncertainties and other factors and, therefore, actual results, performance or achievements of the Company and its industry may be materially different from those implied by such forward looking statements. They should not be read as a guarantee of future performance or results, and will not necessarily be an accurate indication of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from such forward looking statements, including, without limitation, risks inherent to royalty companies, any failures by counterparties to perform their respective obligations, market conditions, share price, uranium price volatility and risks related to the operators of the projects underlying the Company’s existing and proposed interests and those other risks described in filings with Canadian securities regulators and the U.S. Securities and Exchange Commission. These risks, as well as others, could cause actual results and events to vary significantly. Accordingly, readers should exercise caution in relying upon forward looking statements and the Company undertakes no obligation to publicly revise them to reflect subsequent events or circumstances, except as required by law.

Burlington, Ontario–(Newsfile Corp. – November 27, 2023) – Silver Bullet Mines Corp. (TSXV: SBMI) (OTCQB: SBMCF) (‘SBMI’ or ‘the Company’) is pleased to announce high grade silver results as it moves to the next stage in the development of the new Zone1, as outlined in previous press releases.

In its press release of November 1, 2023, SBMI advised it was continuing to blast and muck in Zone1 towards what management believed to be a volume of higher grade silver mineralization. Since then, in the last three blasts the vein width significantly increased to over 19 feet wide, with current assays of up to 24.2 oz/ton silver from the new muck piles and directly from the vein (see chart below). This is significant as the Company believes it is very close to the 1969 historical drill holes, and expects the grade to increase in future blasts. It also provides strong support for management’s theory of the grade increasing as blasting penetrates further into Zone1.

Sample1

Oz/t silver

g/tonne silver

1A

17.6

603.4

1B

17.4

596.6

1C

18.0

617.1

Sample2

2A

11.0

377.1

2B

12.8

438.9

2C

12.8

438.9

Sample3

3A

20.2

692.6

3B

18.8

644.6

3C

20.2

692.6

Sample4

4A

24.2

829.7

4B

24.2

829.7

4C

24.2

829.7

“These results validate our interpretation of the historical and current data,” said A. John Carter, SBMI’s CEO. “The grades are increasing the further we blast into Zone1, as we expected. After battling through Covid, severe supply chain challenges, Mother Nature and unexpected price increases, it is rewarding to be hitting our targetted area, almost exactly where we expected it to be.”

As a result of these grades, management believes the recently blasted material to be economically viable and therefore is being prepared for transportation to the mill for processing. Upon receipt of the material the Company will restart the mill. SBMI is working with a transport company to arrange transportation to the mill.

The Company believes that due to the nugget effect nature of the host rock, milling could increase or decrease the overall grade.

SBMI believes Zone1 to be the zone outlined in the historical data, including the 1969 drill results, and could contain a significant quantity of silver and other metals. The Company intends to continue to drill and blast in Zone1.

As described in the November 1, 2023 press release, a third party has advised it intends to soon send 900 pounds of gold concentrate to SBMI’s mill for processing into a higher purity product. SBMI and the third party will agree upon commercial terms once SBMI has had an opportunity to inspect the gold concentrate. Only minor changes will be made to the mill to enable the processing of the concentrate.

QA/QC

Channel samples and grab samples are taken after each blast, to be processed at the Company’s production assay lab located at the mill. In accordance with best practices, multiple assays have been and should continue to be sent to third party ISO-accredited labs for multielement analysis including precious metals and PGMs. Readers are cautioned that these samples may not be representative of the Buckeye Mine as a whole.

Samples 1, 2 and 3 were processed on November 17, 2023. Sample 4 was processed on November 22, 2023. All samples were run in triplicate.

All samples above were analyzed by SBMI at its facility near Globe, Arizona. They were processed through the Lab Jaw Crusher, Lab Hammer Mill and Splitter Box into an aliquot. Most of the pulverized aliquot was mixed with a flux and flour combination and melted in a crucible at 1,850 degree Fahrenheit, with the remainder being logged and archived. Upon cooling, the poured melt was in the form of a metal button and slag, following which a bone ash cupel was utilized to eliminate the lead in the button to form a bead. The bead was then weighed, following which a solution of 6 to 1 distilled water to nitric acid was utilized to dissolve the silver in the bead at approximately 175 degrees Fahrenheit. A much more detailed description of the process and a picture of the assay lab can be found at https://www.silverbulletmines.com/qaqcassaylab.

Mr. Robert G. Komarechka, P.Geo., an independent consultant, has reviewed and verified SBMI’s work referred to herein, and is the Qualified Person for this release.

For further information, please contact:

John Carter Silver Bullet Mines Corp., CEO cartera@sympatico.ca +1 (905) 302-3843

Peter M. Clausi Silver Bullet Mines Corp., VP Capital Markets pclausi@brantcapital.ca +1 (416) 890-1232

Cautionary and Forward-Looking Statements

This news release contains certain statements that constitute forward-looking statements as they relate to SBMI and its subsidiaries. Forward-looking statements are not historical facts but represent management’s current expectation of future events, and can be identified by words such as “believe”, “expects”, “will”, “intends”, “plans”, “projects”, “anticipates”, “estimates”, “continues” and similar expressions. Although management believes that the expectations represented in such forward-looking statements are reasonable, there can be no assurance that they will prove to be correct.

By their nature, forward-looking statements include assumptions, and are subject to inherent risks and uncertainties that could cause actual future results, conditions, actions or events to differ materially from those in the forward-looking statements. If and when forward-looking statements are set out in this new release, SBMI will also set out the material risk factors or assumptions used to develop the forward-looking statements. Except as expressly required by applicable securities laws, SBMI assumes no obligation to update or revise any forward-looking statements. The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: the impact of SARS CoV-2 or any other global virus; reliance on key personnel; the thoroughness of its QA/QA procedures; the continuity of the global supply chain for materials for SBMI to use in the production and processing of ore; shareholder and regulatory approvals; activities and attitudes of communities local to the location of the SBMI’s properties; risks of future legal proceedings; income tax matters; fires, floods and other natural phenomena; the rate of inflation; availability and terms of financing; distribution of securities; commodities pricing; currency movements, especially as between the USD and CDN; effect of market interest rates on price of securities; and, potential dilution. SARS CoV-2 and other potential global pathogens create risks that at this time are immeasurable and impossible to define.

Vancouver, British Columbia–(Newsfile Corp. – November 24, 2023) – Emperor Metals Inc. (CSE: AUOZ) (OTC Pink: EMAUF) (FSE: 9NH) (“Emperor“) is pleased to announce that it has completed a non-brokered private placement financing previously announced on November 17, 2023.

The Company issued 15,419,400 units (“Units“) at a price of $0.10 per Unit for gross proceeds of up to $1,541,940. Each Unit consists of one common share and one share purchase warrant. Each whole warrant entitles the holder to purchase one additional common share of the Company at an exercise price of $0.20 until November 24, 2025.

In connection with the sale of the Units, the Company paid a total of $41,575.80 in cash, and issued 415,758 finder’s warrants (the “Finder’s Warrants“) to eligible finders for certain of the Units sold. Each Finders’ Warrant entitles the holder to purchase one common share of the Company at an exercise price of $0.20 per share until November 24, 2025.

All securities issued are subject to a hold period until March 25, 2024.

The gross proceeds from the sale of the Units will be utilized to fund exploration and development of the Company’s Duquesne West Gold Project, and for general working capital.

About Emperor Metals Inc.

Emperor Metals Inc. is an innovative Canadian mineral exploration company focused on developing high-quality gold properties situated in the Canadian Shield. For more information, please refer to SEDAR+ (www.sedarplus.ca), under the Company’s profile.

ON BEHALF OF THE BOARD OF DIRECTORS

s/ “Alexander Horsley” Alexander Horsley, Director

THIS NEWS RELEASE MAY CONTAIN CERTAIN “FORWARD LOOKING STATEMENTS”. FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES, ASSUMPTIONS AND OTHER FACTORS THAT MAY CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE COMPANY TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY THE FORWARD-LOOKING STATEMENTS. ANY FORWARD-LOOKING STATEMENT SPEAKS ONLY AS OF THE DATE OF THIS NEWS RELEASE AND, EXCEPT AS MAY BE REQUIRED BY APPLICABLE SECURITIES LAWS, THE COMPANY DISCLAIMS ANY INTENT OR OBLIGATION TO UPDATE ANY FORWARD-LOOKING STATEMENT, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR RESULTS OR OTHERWISE.